Imagine discovering that someone else has a legal claim on your property—even though you still own it. That’s exactly what happens when a judgment lien attaches to your real estate. This powerful legal tool can prevent you from selling, refinancing, or even passing your property to heirs without first satisfying someone else’s debt claim.

Understanding a judgment lien on property: what it is & how to remove it is essential for anyone facing unpaid debts, inherited property complications, or unexpected legal claims. Whether you’re dealing with an existing lien or want to protect your property from future claims, this comprehensive guide provides helpful solutions and expert guidance to navigate these complex situations.

Key Takeaways

- 📋 A judgment lien is a court-ordered legal claim against your property that secures a creditor’s right to payment from an unpaid debt judgment

- ⏰ Judgment liens typically last 10-20 years depending on your state, and can often be renewed if the debt remains unpaid

- 🏠 The lien doesn’t transfer ownership but prevents you from selling or refinancing without paying the debt first

- 💰 Multiple removal methods exist including payment in full, negotiated settlement, bankruptcy, legal challenges, or waiting for expiration

- 🤝 Professional guidance helps navigate removal especially when dealing with multiple liens, inherited property, or complex title issues

What Is a Judgment Lien on Property?

A judgment lien is a legal claim placed on a debtor’s property after a court issues a judgment against them for unpaid debt. This gives the creditor a secured interest in the debtor’s real or personal property.[1]

Think of it like a legal “hold” on your property. The creditor doesn’t own your house or land, but they have a right to be paid from it before you can freely transfer or leverage that asset.

How Judgment Liens Differ from Other Liens

Not all liens are created equal. Understanding the differences helps property owners recognize what they’re facing:

| Type of Lien | How It’s Created | Priority Level | Common Examples |

|---|---|---|---|

| Judgment Lien | Court judgment + recording | Lower priority | Lawsuit judgments, unpaid debts |

| Tax Lien | Government assessment | Highest priority | IRS liens, property taxes |

| Mortgage Lien | Voluntary agreement | High priority (first position) | Home loans, refinancing |

| Mechanic’s Lien | Unpaid contractor work | Varies by state | Construction, repairs |

Property tax liens and mortgage liens typically take priority over judgment liens. This means if your property sells, those debts get paid first.[2]

Real Property vs. Personal Property Liens

Judgment liens can attach to different types of assets:

Real Property includes:

- Houses and residential buildings

- Vacant land and lots

- Commercial buildings

- Rental properties

- Any interest in real estate

Personal Property may include:

- Vehicles and boats

- Business equipment

- Bank accounts (through levy)

- Investment accounts

The specific application varies by state law. Some states allow judgment liens to automatically attach to all real property in the county where the judgment is recorded.

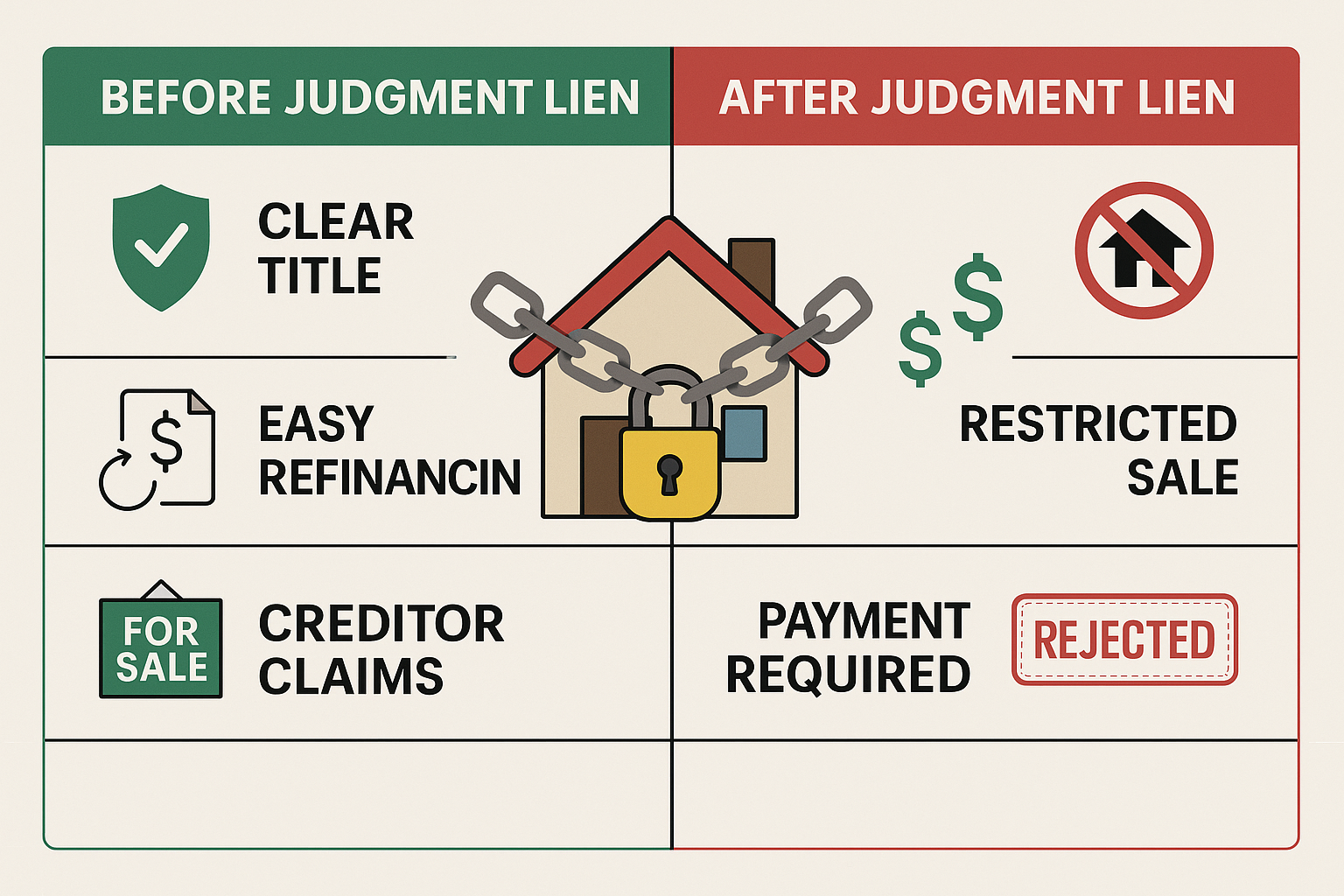

The Public Record Impact

Once recorded, a judgment lien creates a public record that alerts everyone—including potential buyers, lenders, and other creditors—that you have outstanding debts.[3]

This public notice affects your ability to:

- ✖️ Sell your property without paying the debt

- ✖️ Refinance your mortgage

- ✖️ Obtain new credit using the property as collateral

- ✖️ Transfer clear title to heirs

Title companies and lenders routinely check for judgment liens during property transfers. They’ll require the lien to be satisfied before clearing title for a new owner.

How Judgment Liens Are Placed on Property

Understanding the process helps property owners recognize when they’re at risk and take action before a lien attaches.

The Court Judgment Process

The journey to a judgment lien starts in court:

- Lawsuit Filed: A creditor sues you for unpaid debt

- Court Proceedings: You receive notice and opportunity to respond

- Judgment Entered: The court rules in the creditor’s favor

- Monetary Judgment: The court orders you to pay a specific amount

At this point, the creditor has a judgment but not yet a lien. The judgment is simply a court order saying you owe money.

Recording the Judgment

To convert the judgment into a lien on your property, the creditor must take additional steps:

Recording Requirements:

- File the judgment with the county recorder’s office

- Pay recording fees (typically $25-$100)

- Provide proper documentation and legal descriptions

- Record in each county where you own property

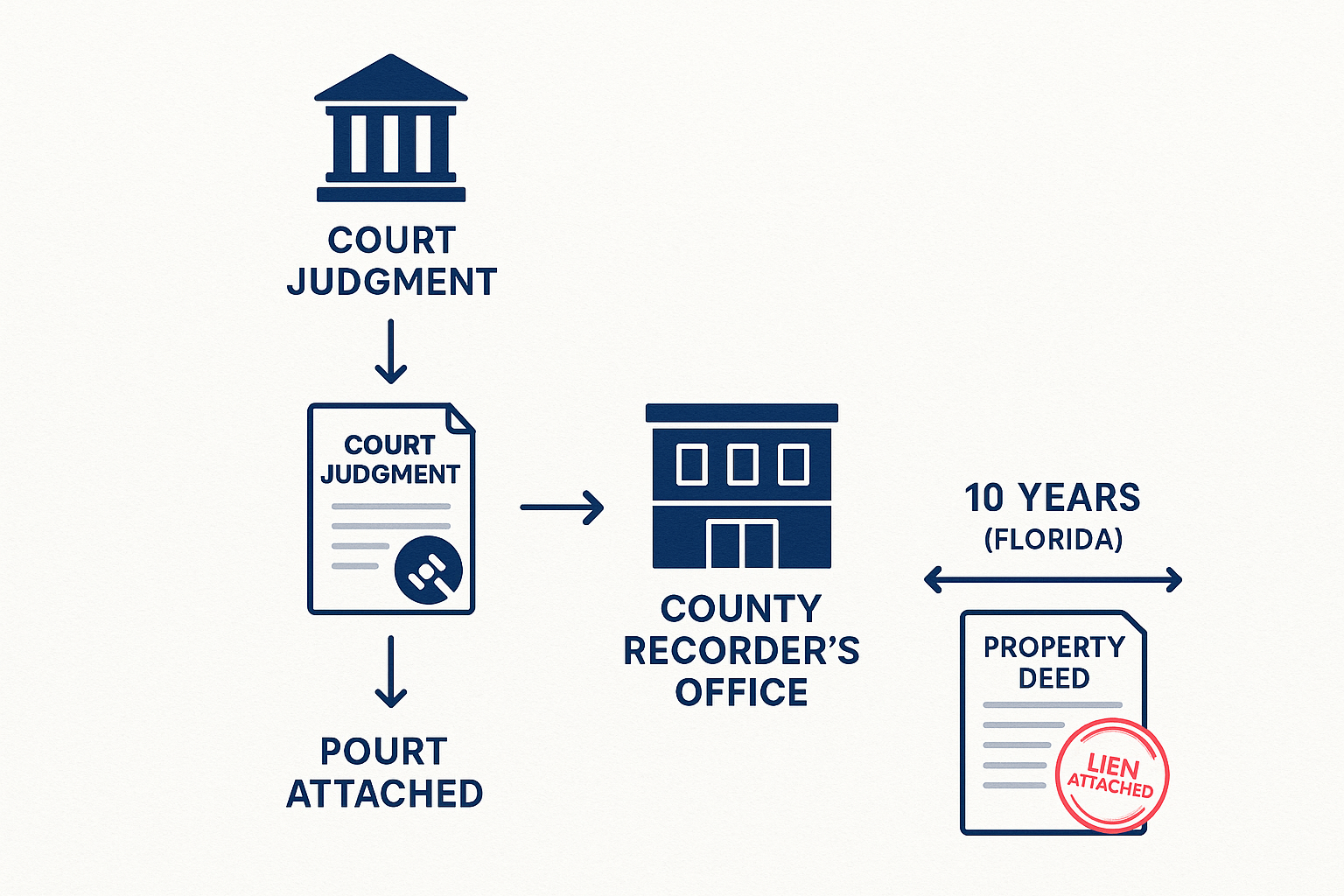

Once recorded, the judgment becomes a judgment lien that attaches to your real property in that county.[4]

Automatic Attachment in Some States

State laws vary significantly:

States with Automatic Attachment:

In some jurisdictions, a judgment automatically becomes a lien on all real property you own in the county without additional recording.

States Requiring Specific Recording:

Other states require the creditor to record an “abstract of judgment” or similar document to create the lien.

Florida Example:

In Florida, judgment liens are governed by Chapter 55 of the Florida Statutes. The lien attaches when the judgment is recorded with the clerk of court and remains valid for 10 years from the date of recording. Creditors can renew for an additional 10 years if the debt isn’t satisfied.[5]

Notice to Property Owners

Many property owners discover judgment liens only when:

- Attempting to sell their property

- Refinancing their mortgage

- Receiving a title report

- Applying for a home equity loan

Pro Tip: Regularly check public records in your county to monitor for any liens or judgments against your property. This proactive approach provides helpful guidance for addressing issues before they complicate property transactions.

Lis Pendens: The Warning Before the Lien

A lis pendens (Latin for “suit pending”) is different from a judgment lien but equally important to understand.

What Is a Lis Pendens on Property?

A lis pendens is a recorded notice that a lawsuit has been filed involving the property itself. It warns potential buyers and lenders that the property’s ownership is being disputed in court.[6]

Key Differences:

| Lis Pendens | Judgment Lien |

|---|---|

| Filed during pending litigation | Filed after judgment is entered |

| Warns of potential claim | Secures actual debt |

| Relates to property ownership disputes | Relates to money judgments |

| Clouds title temporarily | Creates enforceable lien |

A lis pendens doesn’t necessarily mean you’ll lose your property, but it makes selling nearly impossible until the lawsuit resolves. Lenders won’t provide financing on property with a lis pendens attached.

Impact of a Judgment Lien on Property Owners

A judgment lien creates immediate and long-term consequences that affect your financial flexibility and property rights.

Restrictions on Selling Property

When you try to sell property with a judgment lien attached, the lien must be satisfied from the sale proceeds before you receive any funds.[7]

Example Scenario:

- Your property sells for $250,000

- First mortgage balance: $180,000

- Judgment lien: $25,000

- Closing costs: $15,000

- Your net proceeds: $30,000

The title company will require the judgment lien to be paid at closing. There’s no way around it—the lien follows the property.

Refinancing Complications

Mortgage lenders won’t refinance property with outstanding judgment liens. The lien represents additional risk and creates title defects that prevent clear ownership transfer.

To refinance, you must either:

- Pay the judgment in full

- Negotiate a settlement and release

- Have the creditor subordinate their lien (rare)

Priority Order and Subordination

Understanding lien priority is crucial when multiple claims exist on your property:

Typical Priority Order:

- 🥇 Property tax liens (highest priority)

- 🥈 First mortgage lien

- 🥉 Mechanic’s liens (varies by state)

- 4️⃣ Judgment liens (order of recording)

- 5️⃣ Second mortgages and HELOCs

If your property sells for less than the total debt, subordinate liens may receive nothing. This affects creditors’ willingness to negotiate settlements.

Impact on Inherited Property

Judgment liens create special challenges for inherited property with multiple heirs:

Common Complications:

- One heir’s judgment lien may attach to the entire property

- Other heirs can’t sell without addressing the lien

- Family disputes arise over who should pay the debt

- Property remains in limbo while heirs negotiate

Sure Path Property Solutions specializes in helping families navigate these complex situations. Our industry experts provide helpful solutions for properties with multiple owners, liens, and unclear title issues.

Effect on Credit and Future Borrowing

Beyond the property itself, judgment liens damage your financial standing:

- ❌ Appear on credit reports for 7+ years

- ❌ Lower credit scores significantly

- ❌ Signal financial distress to lenders

- ❌ Limit access to new credit

- ❌ Increase insurance premiums in some cases

Forced Sale Through Execution

If the judgment remains unpaid, creditors may pursue more aggressive collection methods.

What Is a Writ of Execution on Property?

A writ of execution is a court order that authorizes a sheriff or marshal to seize and sell your property to satisfy the judgment debt.[8]

The Execution Process:

- Creditor requests writ of execution from court

- Court issues the writ to law enforcement

- Sheriff levies (seizes) the property

- Property is sold at public auction

- Proceeds pay the judgment debt

- Any excess returns to the debtor

Important Limitations:

Most states provide homestead exemptions that protect a certain amount of equity in your primary residence from execution sales. These exemptions vary widely:

- Florida: Unlimited homestead protection (with acreage limits)

- Texas: Strong homestead protections

- California: $300,000-$600,000 depending on circumstances

- Other states: $5,000-$500,000 range

Even with homestead protection, the judgment lien remains attached to the property and must be paid when you sell or refinance.

Emotional and Practical Stress

Beyond the legal and financial impacts, judgment liens create significant stress:

- 😰 Anxiety about losing your home

- 😔 Embarrassment from public records

- 😤 Frustration with complex legal processes

- 😕 Confusion about options and rights

- 😞 Family tension when inherited property is involved

Seeking friendly and caring professional guidance early can reduce this stress and provide clear paths forward.

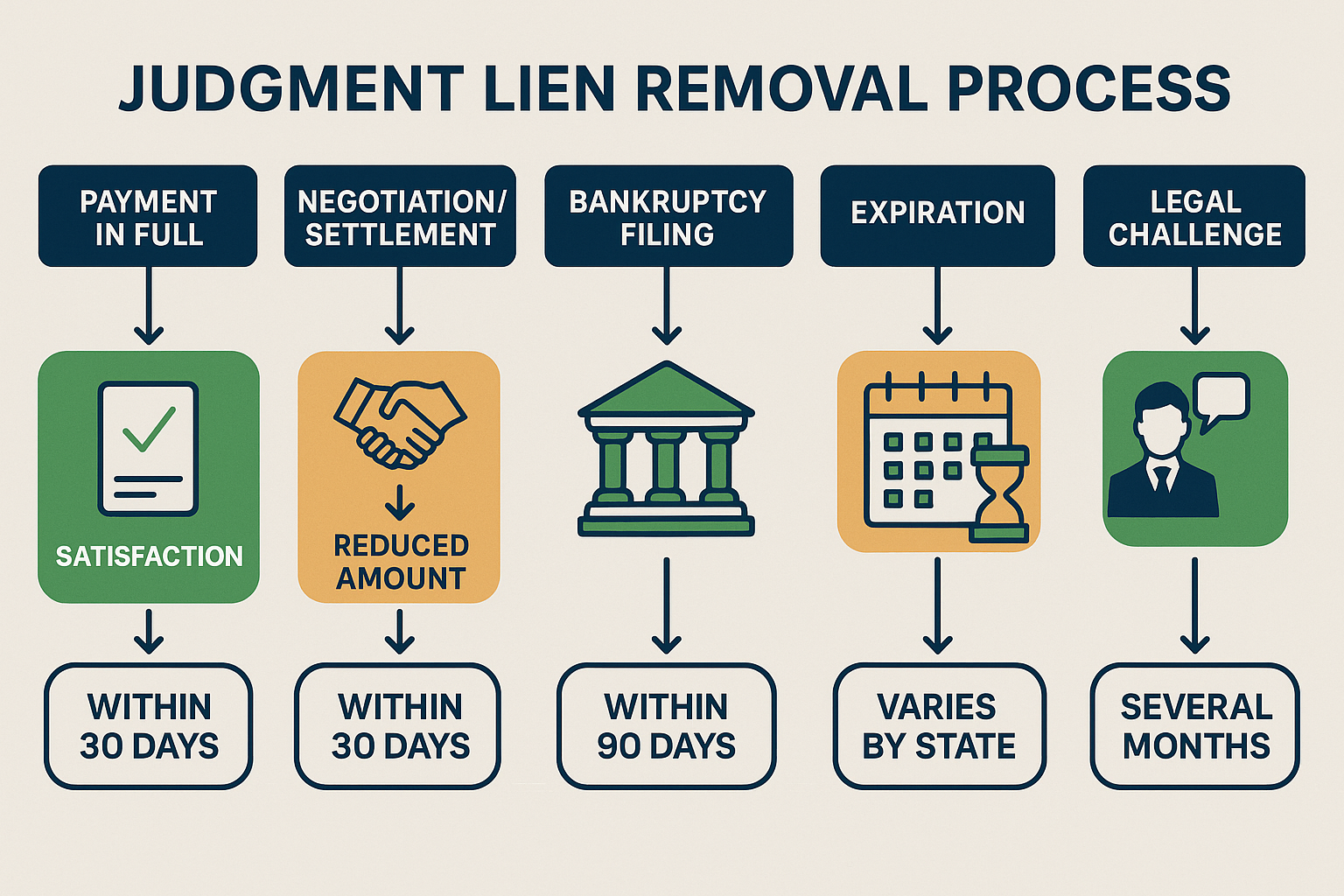

How to Remove a Judgment Lien on Property

Understanding judgment lien on property: what it is & how to remove it empowers you to take action. Multiple removal strategies exist, each suited to different circumstances.

Method 1: Pay the Judgment in Full

The most straightforward approach is paying the entire debt.

Steps to Remove Through Payment:

- Contact the creditor or their attorney

- Verify the exact amount owed (principal + interest + costs)

- Request a payoff statement in writing

- Make payment via certified check or wire transfer

- Obtain a Satisfaction of Judgment document

- Record the satisfaction with the county recorder

- Verify removal from property records

Important: Always get a written satisfaction of judgment. This legal document confirms the debt is paid and releases the lien. Without it, the lien remains on your property even after payment.[9]

The creditor must file this satisfaction with the same office where the original judgment was recorded. Some states require this within 30-60 days of payment.

Method 2: Negotiate a Settlement

Creditors often accept less than the full amount, especially for older judgments or when collection seems unlikely.

Effective Negotiation Strategies:

💡 Start Low: Offer 30-50% of the total debt initially

💡 Emphasize Hardship: Explain financial difficulties honestly

💡 Highlight Collection Challenges: Point out homestead exemptions or lack of equity

💡 Request Lump Sum Discount: Creditors prefer immediate payment over payment plans

💡 Get Everything in Writing: Never pay without a written settlement agreement

Sample Settlement Approach:

“I understand I owe $25,000 on this judgment. I’m experiencing financial hardship and cannot pay the full amount. However, I can offer $10,000 as a lump sum settlement if you’ll provide a full satisfaction of judgment. This gives you immediate payment rather than uncertain collection efforts.”

Critical Settlement Requirements:

The settlement agreement must specify:

- ✅ Exact settlement amount

- ✅ Payment deadline

- ✅ Full release and satisfaction of judgment

- ✅ Lien removal from property

- ✅ No further collection efforts

- ✅ No negative credit reporting after settlement

Method 3: File for Bankruptcy

Bankruptcy can eliminate or discharge judgment liens in certain circumstances.

Chapter 7 Bankruptcy:

- Discharges the underlying debt

- May allow lien avoidance if it impairs homestead exemption

- Doesn’t automatically remove recorded liens

- Requires additional motion to avoid lien

Chapter 13 Bankruptcy:

- Creates repayment plan for debts

- May strip wholly unsecured judgment liens

- Provides time to catch up on payments

- Stops collection efforts during bankruptcy

Lien Avoidance:

Federal bankruptcy law allows debtors to “avoid” (remove) judgment liens that impair homestead exemptions. This complex process requires:

- Filing bankruptcy

- Filing a separate motion to avoid lien

- Proving the lien impairs your exemption

- Obtaining court order removing the lien

- Recording the order with the county

Example:

- Home value: $200,000

- First mortgage: $150,000

- Homestead exemption: $50,000

- Judgment lien: $25,000

The judgment lien “impairs” your homestead exemption because your equity ($50,000) is fully covered by the exemption. The court may allow you to avoid the entire judgment lien.

Important: Bankruptcy is a serious decision with long-term consequences. Consult with a qualified bankruptcy attorney before proceeding.

Method 4: Challenge the Lien’s Validity

Sometimes judgment liens can be removed by proving legal defects.

Grounds for Challenging a Judgment Lien:

🔍 Improper Service: You never received proper notice of the lawsuit

🔍 Expired Judgment: The lien exceeded the statutory time limit

🔍 Incorrect Recording: The lien was filed improperly or in the wrong county

🔍 Identity Error: The judgment is against someone else with a similar name

🔍 Satisfied Debt: The debt was already paid but not released

🔍 Procedural Errors: The creditor failed to follow required legal procedures

Legal Process:

- Consult with an attorney

- File a motion to vacate or release the lien

- Present evidence of the defect

- Attend court hearing

- Obtain court order removing the lien

- Record the order

This method requires legal expertise and is most effective when clear errors exist.

Method 5: Wait for Expiration

Judgment liens don’t last forever. Each state sets specific time limits.

Judgment Lien Expiration by State:

| State | Initial Duration | Renewal Option | Maximum Duration |

|---|---|---|---|

| Alabama | 10 years | Yes, 10 years | 20 years |

| California | 10 years | Yes, 10 years | 20 years |

| Florida | 10 years | Yes, 10 years | 20 years |

| Georgia | 7 years | Yes, multiple | Indefinite with renewals |

| Illinois | 7 years | Yes, 7 years | 27 years (max 3 renewals) |

| New York | 10 years | Yes, 10 years | 20 years |

| North Carolina | 10 years | Yes, 10 years | 20 years |

| Ohio | 5 years | Yes, 5 years | Indefinite with renewals |

| Pennsylvania | 5 years | Yes, 5 years | 20 years (max 3 renewals) |

| Texas | 10 years | Yes, 10 years | 20 years |

Important Considerations:

- ⏰ Creditors can renew liens before expiration in most states

- ⏰ Interest continues accruing during the lien period

- ⏰ The creditor may pursue other collection methods before expiration

- ⏰ Waiting doesn’t prevent wage garnishment or bank levies in many states

When Waiting Makes Sense:

Waiting for expiration works best when:

- You have strong homestead protection

- The judgment amount is small relative to property value

- You don’t plan to sell or refinance soon

- The creditor is unlikely to renew

- Other debts take priority

Method 6: Property Sale with Lien Payoff

Sometimes selling the property and paying the lien from proceeds is the most practical solution.

This Approach Works When:

✅ You have sufficient equity to cover the lien

✅ You’re ready to sell anyway

✅ The property is inherited and heirs want to divide proceeds

✅ Maintaining the property is burdensome

✅ You can relocate to less expensive housing

Process:

- Obtain current property valuation

- Calculate total liens and mortgages

- Estimate net proceeds after liens and costs

- List property for sale (or consider cash buyers)

- Negotiate sale price

- Pay liens at closing from proceeds

- Receive remaining equity

For properties with complex title issues, multiple liens, or difficult circumstances, working with companies like Sure Path Property Solutions provides helpful guidance. Our expert service includes coordinating with counties, title professionals, and creditors to clear liens and complete sales smoothly.

Removal Methods Flowchart

Choosing the Right Removal Strategy:

START: Judgment Lien on Property

↓

Can you afford full payment?

↓ YES → Pay in full → Obtain satisfaction → LIEN REMOVED

↓ NO

↓

Is there equity above exemptions?

↓ YES → Negotiate settlement (30-70% discount)

↓ NO → Consider bankruptcy lien avoidance

↓

Are there legal defects?

↓ YES → Challenge lien validity in court

↓ NO

↓

Need to sell property soon?

↓ YES → Sell property, pay lien from proceeds

↓ NO → Wait for expiration (monitor renewal)

↓

CONSULT ATTORNEY for complex situations

Preventing Future Judgment Liens

While this guide focuses on judgment lien on property: what it is & how to remove it, prevention is equally important.

Respond to Lawsuits Promptly

Never ignore a lawsuit. Even if you owe the debt, responding gives you options:

- 📝 Negotiate settlement before judgment

- 📝 Request payment plans

- 📝 Challenge incorrect amounts

- 📝 Assert legal defenses

- 📝 Avoid default judgment

Default judgments (when you don’t respond) are harder to overturn and give you less negotiating power.

Address Debts Before Lawsuits

Proactive debt management prevents judgments:

- Contact creditors when you fall behind

- Negotiate payment arrangements

- Request hardship programs

- Consider credit counseling

- Explore debt consolidation

Creditors prefer payment arrangements over costly litigation.

Use Homestead Exemptions Wisely

If your state offers homestead protection, ensure you:

- File homestead declarations if required

- Understand exemption limits

- Know which properties qualify

- Maintain primary residence status

These exemptions protect equity from judgment liens and execution sales.

Monitor Public Records

Regularly check:

- County recorder’s office for new liens

- Court records for pending lawsuits

- Credit reports for judgments

- Property tax records for assessments

Early detection allows faster response and resolution.

Maintain Clear Title

For inherited property or properties with multiple owners:

- Resolve title issues promptly

- Record all ownership changes properly

- Address estate debts before distributing property

- Work with title professionals to clear defects

Sure Path Property Solutions offers trustworthy service for property owners navigating these complex situations, providing helpful solutions for unclear titles and multiple ownership issues.

Working with Professionals for Lien Removal

Complex judgment lien situations benefit from professional expertise.

When to Hire an Attorney

Consider legal representation when:

- 🏛️ The judgment amount exceeds $10,000

- 🏛️ Multiple liens exist on the property

- 🏛️ You’re considering bankruptcy

- 🏛️ The lien validity is questionable

- 🏛️ Negotiations have failed

- 🏛️ Foreclosure or execution is threatened

Attorneys specializing in debt collection defense, real estate law, or bankruptcy provide expert service for challenging situations.

Title Companies and Lien Resolution

Title companies play a crucial role in:

- Identifying all liens during property sales

- Calculating exact payoff amounts

- Coordinating lien releases at closing

- Ensuring clear title transfer

- Recording satisfaction documents

They serve as neutral third parties ensuring all parties meet their obligations.

Real Estate Solutions Companies

Companies like Sure Path Property Solutions specialize in properties with complicated issues:

Our Helpful Solutions Include:

✨ Coordinating with creditors to negotiate lien payoffs

✨ Working with counties and title professionals to clear title defects

✨ Providing options for properties with back taxes and multiple liens

✨ Guiding families through inherited property complications

✨ Offering alternatives to traditional sales when liens complicate transactions

✨ Simplifying complex situations with friendly and caring support

Our industry experts understand that properties with judgment liens, tax issues, or unclear title require specialized knowledge. We provide helpful guidance through every step of the process.

Credit Counselors and Financial Advisors

These professionals help with:

- Overall debt management strategies

- Budget planning to address judgments

- Negotiation support with creditors

- Long-term financial recovery planning

Non-profit credit counseling agencies offer low-cost or free services.

Special Situations and Considerations

Certain circumstances create unique challenges for judgment lien removal.

Inherited Property with Judgment Liens

When inheriting property with liens:

Determine Lien Origin:

- Was it the deceased owner’s debt?

- Did an heir’s judgment attach after inheritance?

- Are there estate debts creating new liens?

Heir Responsibilities:

Generally, heirs aren’t personally liable for the deceased’s debts beyond the estate’s value. However:

- Liens attached before death remain on the property

- The property cannot be sold without addressing liens

- Estate assets may need to satisfy judgments before distribution

Resolution Options:

- Pay liens from estate assets

- Sell property and pay liens from proceeds

- One heir buys out others and assumes lien responsibility

- Negotiate settlements with creditors

- Disclaim inheritance if debts exceed value

Multiple heirs complicate decisions. Professional mediation or legal guidance helps families reach agreements.

Properties with Multiple Liens

When several liens exist, prioritize strategically:

Priority Considerations:

- Property taxes: Must be paid to avoid tax sale

- First mortgage: Prevents foreclosure

- Judgment liens: Address based on amount and enforcement likelihood

- Second mortgages/HELOCs: May be negotiable

Strategic Approaches:

- Negotiate with junior lien holders (lower priority)

- They receive less if property sells at auction

- May accept significant discounts to avoid receiving nothing

- Focus resources on liens that pose immediate threats

Out-of-State Judgment Liens

Judgments from other states can follow you:

Domestication Process:

Creditors can “domesticate” out-of-state judgments by:

- Filing the foreign judgment in your current state

- Following that state’s recognition procedures

- Creating a new judgment lien in your state

Defenses:

You may challenge domestication based on:

- Improper service in the original case

- Lack of jurisdiction in the original state

- Expired judgment in the original state

Business vs. Personal Judgment Liens

Business Judgments:

Judgments against your business may or may not attach to personal property, depending on:

- Business structure (LLC, corporation, sole proprietorship)

- Whether you personally guaranteed the debt

- Piercing the corporate veil circumstances

Personal Judgments:

Personal judgments generally cannot attach to business property unless you’re a sole proprietor or the business is your alter ego.

Proper business structuring provides asset protection, but requires maintaining corporate formalities.

Judgment Lien Legal Disclaimer and Professional Consultation

⚖️ Legal Disclaimer:

This article provides general information about judgment liens and removal strategies. It does not constitute legal advice, and should not be relied upon as a substitute for consultation with a qualified attorney licensed in your jurisdiction.

Judgment lien laws vary significantly by state, and individual circumstances affect available options and strategies. What works in one situation may not apply to another.

When to Seek Legal Counsel:

Consult with an attorney before:

- Responding to a lawsuit that could result in a judgment

- Attempting to negotiate lien settlements

- Filing bankruptcy to address judgment liens

- Challenging a lien’s validity in court

- Facing property execution or foreclosure

- Dealing with multiple complex liens

Finding Qualified Attorneys:

Look for attorneys specializing in:

- Debt collection defense

- Real estate law

- Bankruptcy law

- Consumer protection

State bar associations offer referral services to help find qualified professionals in your area.

Conclusion: Taking Action on Judgment Liens

Understanding judgment lien on property: what it is & how to remove it empowers property owners to protect their assets and financial future. While judgment liens create serious complications, multiple removal strategies exist for nearly every situation.

Key Action Steps:

- Verify the lien details: Obtain copies of the judgment and recorded lien from county records

- Calculate your equity: Determine property value minus all mortgages and liens

- Understand your state’s laws: Research judgment lien duration, renewal rules, and homestead exemptions

- Evaluate removal options: Consider payment, settlement, bankruptcy, legal challenge, or waiting for expiration

- Seek professional guidance: Consult attorneys, title professionals, or property solutions experts

- Take action promptly: Liens don’t disappear on their own and may worsen over time

For Property Owners Facing Complex Situations:

If your property has judgment liens combined with other challenges—back taxes, multiple heirs, unclear title, or difficulty selling through traditional means—specialized help makes the difference.

Sure Path Property Solutions provides:

✅ Expert service from industry experts who understand complex property issues

✅ Helpful solutions tailored to your specific circumstances

✅ Trustworthy service coordinating with counties, creditors, and title professionals

✅ Friendly and caring support throughout the entire process

✅ Helpful guidance toward clear, practical solutions

We simplify complicated situations and help property owners move forward with confidence.

Don’t let judgment liens hold your property hostage. Whether you choose to pay, negotiate, challenge, or sell, taking informed action protects your interests and creates a path forward.

The journey from discovering a judgment lien to removing it may seem overwhelming, but with the right information and support, property owners successfully resolve these issues every day. Your property represents significant value—both financial and personal. Protecting it starts with understanding your options and taking decisive action.

Remember: judgment liens are legal tools, but they’re not permanent obstacles. With helpful guidance, expert service, and the right strategy, you can remove judgment liens and regain full control of your property.

References

[1] Cornell Legal Information Institute. “Judgment Lien.” LII / Legal Information Institute. https://www.law.cornell.edu/wex/judgment_lien

[2] National Association of Realtors. “Understanding Property Liens and Priority.” NAR Real Estate Resources, 2024.

[3] American Bar Association. “How Liens Affect Property Ownership.” ABA Consumer Guide to Legal Help, 2025.

[4] Florida Legislature. “Chapter 55 – Enforcement of Judgments.” The 2025 Florida Statutes. http://www.leg.state.fl.us/statutes/index.cfm?App_mode=Display_Statute&Title=-%3E2025-%3EChapter%2055

[5] Florida Courts. “Judgment Liens in Florida: Duration and Renewal.” Florida State Courts Self-Help Resources, 2025.

[6] Nolo. “Lis Pendens: What It Means When a Lawsuit Affects Your Property.” Nolo Legal Encyclopedia, 2025.

[7] Consumer Financial Protection Bureau. “What happens to liens when I sell my home?” CFPB Consumer Resources, 2025.

[8] Legal Information Institute. “Writ of Execution.” Cornell Law School. https://www.law.cornell.edu/wex/writ_of_execution

[9] National Consumer Law Center. “Satisfaction of Judgments and Lien Release Requirements.” NCLC Consumer Credit and Sales Legal Practice Series, 2024.

Sure Path is a family-owned, curative-title cash buyer. We handle the paperwork and pay what’s owed at closing — no fees, no repairs, no pressure.