Can I Sell My House in Pre-Foreclosure? Your Complete Options

Facing pre-foreclosure can feel like standing at the edge of a financial cliff. The notices pile up, the phone calls intensify, and the uncertainty about your home’s future keeps you awake at night. But here’s the truth that many homeowners don’t realize: you absolutely can sell your house in pre-foreclosure, and doing so might be your smartest financial move. Understanding your complete options during this critical window can mean the difference between protecting your credit and facing devastating long-term consequences.

The question “Can I Sell My House in Pre-Foreclosure? Your Complete Options” comes up thousands of times each month from homeowners searching for helpful solutions during one of life’s most stressful situations. The answer is emphatically yes—and you have more control than you might think. The pre-foreclosure period actually represents a valuable opportunity window where you maintain ownership rights and can make strategic decisions about your property’s future.

Key Takeaways

- ✅ You can absolutely sell your house during pre-foreclosure—you retain full ownership rights until the foreclosure auction occurs

- ⏰ Time is critical—the pre-foreclosure window typically lasts 3-10 months depending on your state, giving you a limited but actionable timeframe

- 💰 Multiple selling options exist—from traditional listings to cash buyers to short sales, each with different timelines and outcomes

- 🤝 Lender communication is essential—proactive contact with your mortgage company can unlock alternatives and buy you additional time

- 🛡️ Selling protects your financial future—avoiding foreclosure preserves your credit score and prevents deficiency judgments that could follow you for years

Understanding Pre-Foreclosure: What It Means for Homeowners

Pre-foreclosure represents the period between when you fall behind on mortgage payments and when the lender completes the foreclosure process through auction or repossession. This isn’t just a technical legal term—it’s a crucial window of opportunity.

During this phase, you still own your home. The deed remains in your name. You have rights, options, and most importantly, the ability to take action that can dramatically improve your financial outcome.

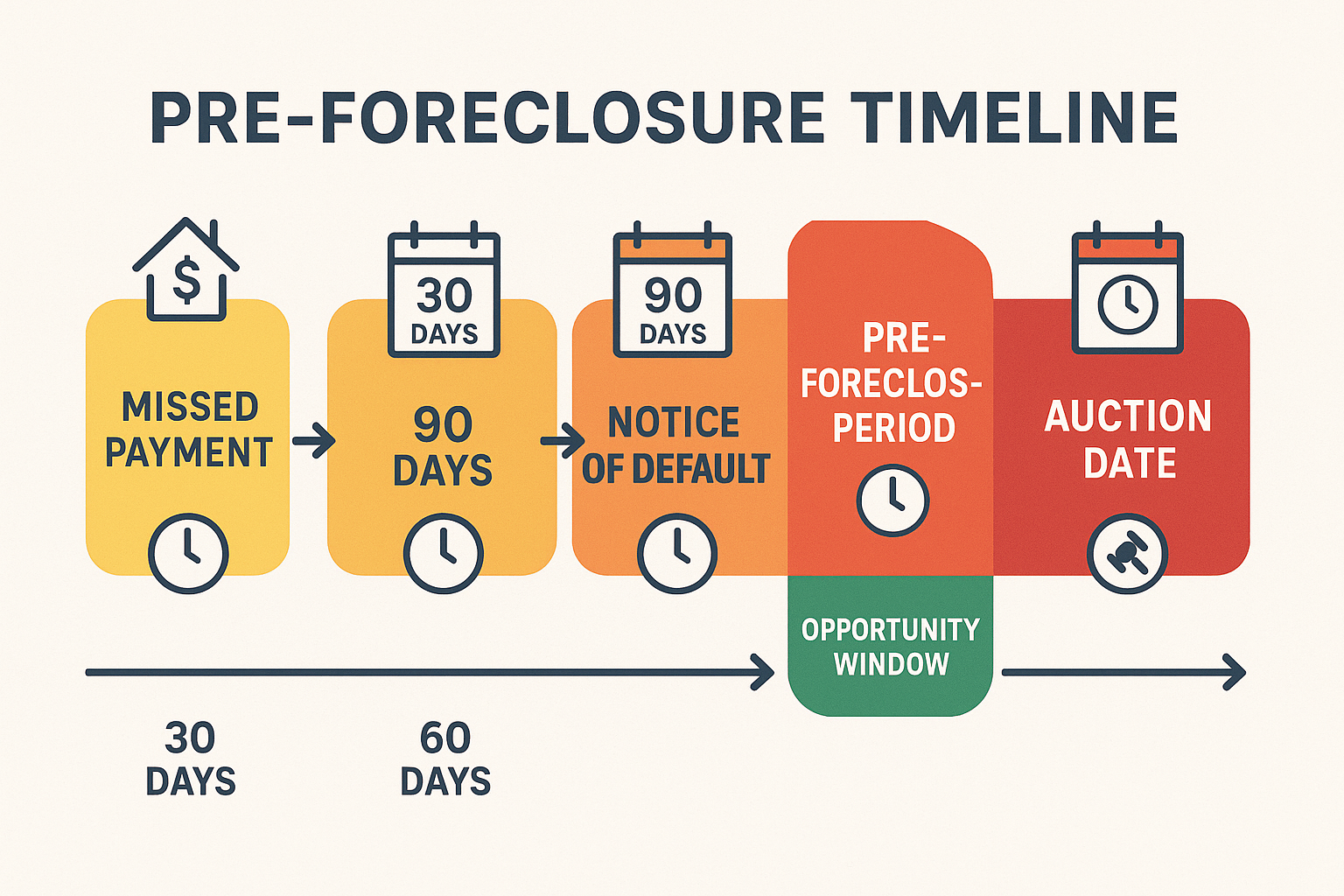

The Pre-Foreclosure Timeline Explained

The pre-foreclosure timeline varies significantly by state, but understanding the general progression helps you recognize where you stand and how much time remains for action.

Month 1: The First Missed Payment

After missing your first mortgage payment, you’ll typically receive phone calls and letters from your lender. This isn’t pre-foreclosure yet—it’s the delinquency phase. Your lender wants to work with you at this stage because foreclosure is expensive for them too.

Months 2-3: Escalating Communications

Missing a second and third payment triggers more serious communications. Late fees accumulate, and your account moves to the lender’s loss mitigation department. Some lenders may still offer payment plans or forbearance options at this stage[1].

Month 4: Notice of Default (NOD)

After 90-120 days of non-payment, most lenders issue a Notice of Default or similar legal notification. This marks the official start of pre-foreclosure. The notice gets recorded with the county, becoming public record. This is when your property appears on pre-foreclosure lists that investors and cash buyers monitor.

Months 4-10: The Pre-Foreclosure Window

Depending on your state’s foreclosure laws (judicial vs. non-judicial), you have anywhere from 30 days to several months before the foreclosure auction. Judicial foreclosure states like Florida, New York, and Illinois can take 6-12 months or longer. Non-judicial states like California, Texas, and Arizona move faster—sometimes completing foreclosure in 3-4 months[2].

This is your action window. Every day counts.

Foreclosure Auction Day

Once the auction occurs and a buyer purchases the property, your ownership ends. In some states, you may have a redemption period allowing you to reclaim the property by paying all amounts due, but this option is rarely practical for homeowners already in financial distress.

“The pre-foreclosure period is when homeowners have the most leverage and the most options. Once that auction gavel falls, those options disappear completely.” — Real Estate Attorney

Can You Sell During Pre-Foreclosure? The Definitive Answer

Yes, you absolutely can sell your house during pre-foreclosure. In fact, selling during this period is often the best strategy for protecting your financial future and maximizing your outcome.

Here’s why this works: Until the foreclosure auction actually occurs, you remain the legal owner of the property. You hold the deed. You have the right to sell, just as you would in any other circumstance. The pre-foreclosure status doesn’t strip away your ownership rights—it simply means your lender has initiated legal proceedings that will eventually result in forced sale if you don’t take action.

Why Selling Makes Financial Sense

Selling your house in pre-foreclosure offers several compelling advantages over letting the foreclosure process complete:

Credit Score Protection

A completed foreclosure can drop your credit score by 200-400 points and remain on your credit report for seven years[3]. Selling before foreclosure completion, especially if you can pay off the mortgage in full, prevents this devastating impact. Even a short sale (discussed later) causes less credit damage than foreclosure.

Deficiency Judgment Avoidance

When your home sells at foreclosure auction for less than you owe, the lender may pursue a deficiency judgment for the difference. If you owed $300,000 but the property sold for $250,000, you could face a $50,000 judgment plus legal fees. Selling the property yourself—and negotiating with the lender if needed—can eliminate or reduce this risk.

Equity Preservation

If your property has equity (worth more than you owe), selling lets you capture that value. Foreclosure auctions typically sell properties below market value, meaning you’d lose equity that rightfully belongs to you.

Control Over the Process

Selling gives you control over timing, terms, and how the transaction unfolds. Foreclosure strips away that control, forcing you to vacate on the lender’s timeline and potentially facing eviction proceedings.

Legal Considerations When Selling in Pre-Foreclosure

While you can sell during pre-foreclosure, certain legal realities affect the process:

Payoff Requirements

You must pay off the entire mortgage balance (plus fees, interest, and penalties) to transfer clear title to a buyer. This means you need to sell for enough to cover what you owe, or negotiate a short sale if the property is underwater.

Lender Communication

Inform your lender that you’re actively selling. This may pause or slow foreclosure proceedings, giving you additional time. Lenders generally prefer you sell the property rather than forcing them through costly foreclosure.

Title Considerations

The Notice of Default appears on the title report, which buyers and their lenders will see. This doesn’t prevent sale, but it requires addressing during the transaction. Working with experienced title professionals and real estate experts who understand these situations proves invaluable.

Your Complete Selling Options During Pre-Foreclosure

When facing pre-foreclosure, you have several distinct pathways for selling your property. Each option offers different advantages, timelines, and outcomes. Understanding these choices empowers you to select the strategy that best fits your situation.

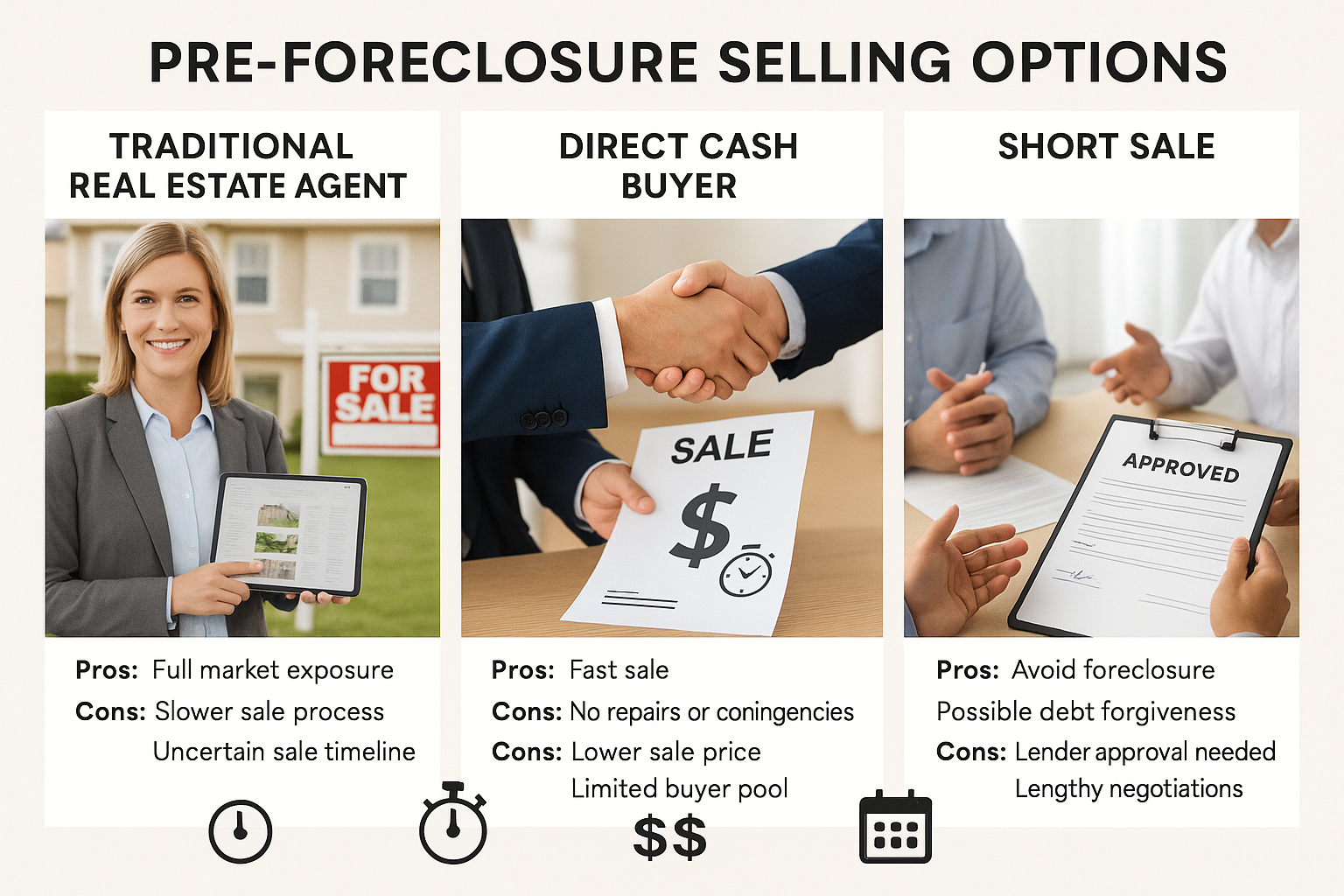

Option 1: Traditional Sale with a Real Estate Agent

A traditional sale through a licensed real estate agent works exactly like selling under normal circumstances—with one critical difference: you’re racing against the foreclosure timeline.

How It Works:

You list your property on the Multiple Listing Service (MLS) at market value, show the home to potential buyers, negotiate offers, and close through normal channels. The sale proceeds pay off your mortgage balance, and any remaining equity comes to you.

Advantages:

- Potentially achieves the highest sale price through market exposure

- Professional marketing and negotiation expertise

- Familiar process for buyers and their lenders

- Preserves your credit if you sell for enough to pay off the loan

Disadvantages:

- Takes 60-90 days on average, which may exceed your foreclosure timeline

- Requires the property to be in showing condition

- No guarantee of sale before auction date

- Agent commissions (typically 5-6%) reduce your net proceeds

Best For: Homeowners with at least 4-6 months before foreclosure auction, properties in good condition, and situations where the home has equity or breaks even.

Option 2: Sell to a Cash Buyer or Real Estate Investor

Cash buyers and investment companies specialize in purchasing properties quickly, often in as-is condition. This option has gained popularity among homeowners facing time-sensitive situations like pre-foreclosure.

How It Works:

Companies like Sure Path Property Solutions evaluate your property and situation, then make a direct cash offer. If you accept, closing can happen in as little as 7-14 days. No repairs, no showings, no traditional financing contingencies.

Advantages:

- ⚡ Speed: Close in days or weeks, not months

- 🏚️ As-is sales: No repairs or cleaning required

- 💯 Certainty: Cash offers rarely fall through

- 🤝 Simplified process: No showings or ongoing marketing

- 📋 Expert guidance: Experienced with complex situations like liens, judgments, and title issues

Disadvantages:

- Offers typically come in at 70-85% of market value to account for repairs and investor profit

- Less competitive bidding than open market listings

Best For: Homeowners with limited time (less than 90 days), properties needing repairs, situations with complications like liens or judgments, or anyone prioritizing speed and certainty over maximum price.

“We’ve helped hundreds of homeowners navigate pre-foreclosure situations. The relief they feel when they realize they have options—and that someone understands their situation without judgment—is why we do this work.” — Sure Path Property Solutions

Option 3: Short Sale

A short sale occurs when your lender agrees to accept less than the full mortgage balance as payment in full, allowing you to sell the property even when underwater (owing more than it’s worth).

How It Works:

You (or your agent) submit a short sale package to your lender, including financial hardship documentation, property valuation, and buyer offer. The lender reviews and either approves, counters, or denies. If approved, the sale proceeds, with the lender accepting the shortage as a loss.

Advantages:

- Enables sale when property value is less than mortgage balance

- Less credit damage than foreclosure (typically 50-150 point drop vs. 200-400)

- May eliminate deficiency judgment (depending on state and agreement terms)

- Provides a solution when you have no equity

Disadvantages:

- ⏱️ Time-consuming: Lender approval takes 60-120 days or longer

- 📄 Complex paperwork: Requires extensive financial documentation

- ❌ No guarantee: Lenders can deny short sale requests

- 💰 No proceeds: You receive nothing from the sale

- 💳 Tax implications: Forgiven debt may be taxable income (consult a tax professional)

Best For: Homeowners who are underwater on their mortgage, have documented financial hardship, and have sufficient time before foreclosure auction to complete the lengthy approval process.

Option 4: Sell to a Family Member or Friend

Selling to someone you know can provide a creative solution, though it requires careful handling to ensure legitimacy and fairness.

How It Works:

A trusted family member or friend purchases your property at fair market value, pays off your mortgage, and you transfer the deed. They might allow you to stay as a renter or work out other arrangements.

Advantages:

- Flexible terms and timing

- Keeps the property “in the family”

- May allow you to continue living there

- Potentially faster than traditional sale

Disadvantages:

- Requires someone with cash or financing ability

- Must be conducted at fair market value to avoid lender challenges

- Can strain personal relationships if complications arise

- Still requires proper legal documentation and title transfer

Best For: Homeowners with financially capable family or friends willing to help, situations where staying in the home is important, and when all parties understand the legal and financial implications.

The Pre-Foreclosure Sale Process: Step-by-Step Guide

Successfully selling your house during pre-foreclosure requires strategic action and careful timing. This step-by-step guide provides a roadmap for navigating the process effectively.

Step 1: Assess Your Timeline (Days 1-3)

Immediately determine how much time you have before the foreclosure auction. This single factor influences every subsequent decision.

Action Items:

- 📅 Review your Notice of Default for the auction date

- 📞 Contact your lender to confirm the foreclosure timeline

- 🔍 Research your state’s foreclosure laws (judicial vs. non-judicial)

- ✍️ Calculate your realistic action window

Most states require the lender to provide specific notice periods. In California, for example, you receive at least 90 days from the Notice of Default to the auction. In Florida, the judicial process typically takes 6-12 months[2].

Step 2: Determine Your Property’s Value and Equity Position (Days 3-7)

Understanding what your property is worth and how much you owe determines which selling options are viable.

Action Items:

- 🏡 Get a professional property valuation or comparative market analysis

- 📊 Request a payoff statement from your lender (includes principal, interest, fees, and penalties)

- 🧮 Calculate your equity position: Property Value – Mortgage Payoff = Equity

- 💰 Factor in selling costs (agent commissions, closing costs, repairs if needed)

Three Possible Scenarios:

- Positive Equity: Property worth more than you owe—you can sell traditionally and walk away with money

- Break-Even: Property worth approximately what you owe—you can sell but receive minimal proceeds

- Underwater: You owe more than the property is worth—short sale or cash buyer may be your best options

Step 3: Choose Your Selling Strategy (Days 7-10)

Based on your timeline and equity position, select the selling approach that best fits your situation.

Decision Framework:

| Your Situation | Recommended Option | Typical Timeline |

|---|---|---|

| 6+ months, positive equity, good condition | Traditional agent listing | 60-90 days |

| 3-6 months, any equity, any condition | Cash buyer or investor | 7-30 days |

| Underwater, 4+ months available | Short sale | 90-180 days |

| Under 90 days, any situation | Cash buyer (urgent) | 7-14 days |

Step 4: Contact Your Lender Immediately (Days 10-12)

Proactive communication with your mortgage company is essential. This conversation can unlock additional time and options.

What to Say:

“I’m currently in pre-foreclosure on my property at [address]. I’m actively working to sell the property before the foreclosure auction scheduled for [date]. I want to keep you informed of my progress and discuss any options that might provide additional time to complete the sale.”

What to Ask:

- Can the foreclosure proceedings be paused while I actively market the property?

- What documentation do you need to see that I’m making good-faith efforts to sell?

- Are there any loss mitigation options available while I pursue the sale?

- What is the exact payoff amount, and how quickly does it increase with fees and interest?

Many lenders will slow the foreclosure process when you demonstrate active, good-faith efforts to sell. They prefer this outcome to the expense and uncertainty of auction.

Step 5: Execute Your Chosen Selling Strategy (Days 12+)

Take immediate action on your selected approach. Speed and focus are critical.

For Traditional Listing:

- Interview and hire an experienced agent immediately

- Prepare the property for showing (clean, declutter, minor repairs)

- Price aggressively to attract quick offers

- Review offers within 24 hours

- Negotiate shortest possible closing timeline

For Cash Buyer Sale:

- Contact reputable companies like Sure Path Property Solutions

- Provide accurate property information

- Review cash offers quickly

- Ask questions about the process and timeline

- Choose a buyer with proven track record and trustworthy service

For Short Sale:

- Hire an agent experienced in short sales

- Gather all required financial documentation

- Submit complete short sale package to lender

- Find a patient buyer willing to wait for approval

- Follow up with lender weekly on approval status

Step 6: Navigate the Closing Process (Final 30-45 Days)

Once you have a buyer and contract, focus on moving efficiently toward closing.

Critical Actions:

- ✅ Respond to all requests from the title company within 24 hours

- ✅ Maintain communication with your lender about the pending sale

- ✅ Address any title issues immediately (liens, judgments, etc.)

- ✅ Coordinate with the buyer to prevent delays

- ✅ Prepare for move-out to meet the closing timeline

Working with Title Professionals:

Complex situations involving pre-foreclosure often include additional complications like tax liens, mechanic’s liens, or judgments. Companies with expert service in these areas, like Sure Path Property Solutions, coordinate with counties and title professionals to resolve these issues efficiently.

Step 7: Close and Move Forward (Closing Day)

At closing, the sale proceeds pay off your mortgage (and any other liens), the deed transfers to the buyer, and you move forward with your financial fresh start.

What Happens at Closing:

- All parties sign the necessary documents

- The buyer’s funds are transferred

- Your mortgage is paid in full

- Any liens or judgments are satisfied

- Remaining proceeds (if any) are distributed to you

- The foreclosure case is dismissed

After Closing:

- Request written confirmation from your lender that the loan is paid in full

- Obtain documentation showing the foreclosure case was dismissed

- Monitor your credit report to ensure accurate reporting

- Begin rebuilding your financial foundation

Working with Your Lender: Communication Strategies That Work

Your mortgage lender isn’t your enemy during pre-foreclosure—they’re a stakeholder who also wants to avoid the costly foreclosure process. Strategic communication can unlock options and buy valuable time.

The Psychology of Lender Communication

Understand that lenders are large institutions with specific procedures and metrics. The loss mitigation department representatives you speak with are evaluated on their ability to recover money while minimizing losses. They have authority to offer various solutions, but you must ask for them and provide necessary documentation.

Key Principles:

- Be proactive, not reactive: Contact them before they escalate contact with you

- Document everything: Keep records of every call, email, and letter

- Be honest about your situation: Trying to hide information backfires

- Demonstrate good faith: Show you’re taking concrete action

- Ask for specific solutions: Know what you’re requesting

Hardship Letter Template

When requesting lender cooperation or short sale approval, a well-written hardship letter explains your situation clearly and professionally.

Sample Hardship Letter Structure:

[Your Name]

[Property Address]

[Loan Number]

[Date]

[Lender Name]

Loss Mitigation Department

[Lender Address]

Re: Request for [Short Sale Approval/Foreclosure Delay/Loan Modification]

Loan Number: [Your Loan Number]

Property Address: [Your Property Address]

Dear Loss Mitigation Team:

I am writing to request [specific request] for the above-referenced property. I have fallen behind on my mortgage payments due to [specific hardship: job loss, medical emergency, divorce, etc.].

[2-3 paragraphs explaining your specific situation, when the hardship began, what you've done to try to resolve it, and why you cannot continue making payments]

I am currently working with [real estate agent/cash buyer/etc.] to sell the property. [Include specific details about your selling efforts, timeline, and any offers received]

I am requesting your cooperation in [pausing foreclosure proceedings/approving the short sale/etc.] to allow this sale to complete. This outcome will benefit both parties by avoiding the costs and uncertainty of foreclosure.

I have attached [list all supporting documents: financial statements, pay stubs, medical bills, property valuation, purchase offer, etc.].

Thank you for your consideration. I am committed to resolving this situation responsibly and appreciate your helpful guidance.

Sincerely,

[Your Signature]

[Your Printed Name]

[Contact Phone]

[Contact Email]

Loss Mitigation Options to Request

While your primary goal is selling the property, understanding alternative options provides negotiating leverage and backup plans.

Forbearance Agreement

Temporary pause or reduction of payments while you resolve your situation. Useful for buying time to complete a sale.

Repayment Plan

Spreading missed payments over future months while resuming regular payments. Only viable if your financial situation has improved.

Loan Modification

Permanent change to loan terms (interest rate, length, etc.) to make payments affordable. Requires demonstrated ability to make modified payments.

Deed in Lieu of Foreclosure

Voluntarily transferring the deed to the lender in exchange for release from the mortgage. Less credit damage than foreclosure, but you receive no proceeds and must vacate.

Alternatives to Selling: Other Options to Consider

While selling during pre-foreclosure is often the best solution, understanding alternatives helps you make informed decisions.

Loan Modification

If your financial hardship was temporary and you can now afford modified payments, loan modification might allow you to keep your home.

Pros:

- Remain in your home

- Avoid credit damage from foreclosure or sale

- Potentially lower monthly payments

Cons:

- Requires proof of current income and ability to pay

- Not available if you have no income

- May extend loan term or increase total interest paid

- Doesn’t address underlying affordability issues

Bankruptcy

Filing Chapter 7 or Chapter 13 bankruptcy triggers an automatic stay that temporarily halts foreclosure proceedings.

Chapter 13 Bankruptcy:

Creates a 3-5 year repayment plan that can include catching up on missed mortgage payments while keeping your home.

Chapter 7 Bankruptcy:

Discharges unsecured debts but doesn’t stop foreclosure long-term unless you can resume payments.

Important Considerations:

- Bankruptcy has severe credit consequences (7-10 years on credit report)

- Requires legal representation and court fees

- Doesn’t eliminate the mortgage debt—only delays foreclosure

- Should be considered carefully with bankruptcy attorney guidance

Refinancing

Refinancing to a new loan with better terms can work if you have equity, decent credit, and documented income.

Reality Check:

Most homeowners in pre-foreclosure cannot qualify for refinancing due to:

- Damaged credit from missed payments

- Insufficient equity

- Difficulty documenting income

- Lender reluctance to refinance distressed loans

If you can qualify, refinancing might help, but it’s rarely viable once pre-foreclosure begins.

Renting Out the Property

Some homeowners consider renting the property to generate income for mortgage payments.

Challenges:

- Requires upfront capital for repairs and marketing

- Doesn’t address existing payment arrears

- Rental income may not cover full mortgage payment

- Becoming a landlord adds complexity and responsibility

- Doesn’t solve the problem if you’re already in pre-foreclosure

Time-Sensitive Action Checklist for Pre-Foreclosure

Use this checklist to ensure you’re taking all necessary steps to successfully sell your house during pre-foreclosure.

Immediate Actions (Within 7 Days)

- Locate and review your Notice of Default or foreclosure notice

- Determine exact foreclosure auction date

- Request mortgage payoff statement from lender

- Get property valuation (CMA from agent or professional appraisal)

- Calculate equity position (value minus payoff)

- Research your state’s foreclosure timeline and laws

- Gather all property documents (deed, title, mortgage, tax records)

- Contact lender’s loss mitigation department

- Document all communications with lender

- Identify and address any liens or judgments on the property

Within 14 Days

- Choose your selling strategy based on timeline and equity

- Interview and select real estate professional or cash buyer

- Write and send hardship letter to lender

- Request foreclosure proceedings pause while actively selling

- Begin property preparation (cleaning, minor repairs if listing traditionally)

- Gather documentation for short sale if underwater

- Contact Sure Path Property Solutions or similar expert service if situation is complex

- Create realistic timeline with milestones

- Identify temporary housing options if needed

- Consult with real estate attorney if situation is complicated

Within 30 Days

- Have property listed or cash offer in hand

- Review and respond to all offers within 24 hours

- Maintain weekly communication with lender

- Address any title issues with title professionals

- Coordinate with buyer on inspection and appraisal

- Prepare for move-out logistics

- Update lender on sale progress

- Resolve any outstanding liens or judgments

- Finalize closing date that meets foreclosure timeline

- Arrange for utilities, mail forwarding, etc.

Before Closing

- Respond immediately to all title company requests

- Complete any required repairs or agreements

- Do final walk-through with buyer

- Confirm all closing documents are prepared

- Verify payoff amount is current

- Arrange moving logistics

- Prepare for final utility readings

- Collect all property keys, garage openers, etc.

- Review closing settlement statement carefully

Why Expert Help Matters in Complex Pre-Foreclosure Situations

Pre-foreclosure often comes with additional complications that make selling more challenging: back taxes, multiple liens, judgments, unclear title, or properties with multiple heirs. These situations require specialized expertise.

Common Complications and Solutions

Back Property Taxes

Unpaid property taxes create liens that must be satisfied at closing. Companies like Sure Path Property Solutions specialize in coordinating with county tax offices to resolve these issues, often negotiating payment plans or settlements that allow the sale to proceed.

Multiple Liens and Judgments

Mechanic’s liens, HOA liens, IRS liens, and court judgments all attach to your property and must be addressed before clear title can transfer. Industry experts navigate these complexities, negotiating with lien holders and ensuring proper payoff at closing.

Inherited Property with Multiple Owners

When multiple heirs own a property in pre-foreclosure, coordinating agreement among all parties becomes essential. Helpful guidance from professionals experienced in heir property situations can facilitate consensus and smooth transactions.

Unclear or Clouded Title

Title issues like missing heirs, unreleased mortgages, or boundary disputes require resolution before sale. Expert service providers work with title companies and attorneys to clear these obstacles efficiently.

The Sure Path Property Solutions Advantage

When facing pre-foreclosure with complications, working with a company that offers helpful solutions and trustworthy service makes the difference between success and failure.

What Sets Expert Buyers Apart:

- 🤝 Friendly and caring approach: Understanding that you’re facing a difficult situation, not just a transaction

- ⚡ Speed when you need it: Closing in days or weeks, not months

- 🔧 Problem-solving expertise: Handling liens, taxes, title issues, and multiple owners

- 💼 Professional coordination: Working with counties, title companies, and attorneys on your behalf

- 🎯 Clear communication: Explaining options without pressure or confusion

- ✅ Proven track record: Years of experience helping homeowners in distressed situations

“We don’t just buy houses—we help people navigate complicated situations and find their path forward. Every homeowner deserves dignity and respect, regardless of their circumstances.” — Sure Path Property Solutions

Protecting Your Credit and Financial Future

The decisions you make during pre-foreclosure have long-lasting impacts on your financial health. Understanding these consequences helps you choose wisely.

Credit Score Impact Comparison

Different outcomes affect your credit differently:

| Outcome | Credit Score Impact | Duration on Report | Long-term Effect |

|---|---|---|---|

| Completed Foreclosure | -200 to -400 points | 7 years | Severe difficulty obtaining credit |

| Short Sale | -50 to -150 points | 7 years | Moderate difficulty, improves faster |

| Deed in Lieu | -50 to -125 points | 7 years | Similar to short sale |

| Sale Before Foreclosure | Minimal to none | Late payments only (2 years) | Preserves creditworthiness |

| Bankruptcy + Foreclosure | -300 to -500 points | 7-10 years | Most severe impact |

The Clear Winner: Selling your property before foreclosure completion, especially if you can pay off the loan in full, causes the least credit damage and positions you best for financial recovery.

Deficiency Judgments: A Hidden Danger

In many states, if your home sells at foreclosure auction for less than you owe, the lender can pursue a deficiency judgment against you personally for the difference[3].

Example:

- Mortgage balance owed: $300,000

- Foreclosure auction sale price: $240,000

- Deficiency: $60,000

- Plus legal fees, interest, and costs: $70,000+

This judgment can lead to wage garnishment, bank account levies, and additional credit damage. Selling the property yourself—even through short sale with negotiated deficiency waiver—avoids this risk.

Tax Implications of Forgiven Debt

When a lender forgives debt through short sale or foreclosure, the IRS may consider the forgiven amount as taxable income. The Mortgage Forgiveness Debt Relief Act provided exemptions for primary residences, but tax laws change frequently[4].

Action Step: Consult with a tax professional about potential tax liability from any debt forgiveness in your situation.

Frequently Asked Questions About Selling in Pre-Foreclosure

How long does pre-foreclosure last?

Pre-foreclosure typically lasts 3-10 months depending on your state’s laws. Judicial foreclosure states (requiring court proceedings) take longer—often 6-12 months or more. Non-judicial states can complete foreclosure in as little as 90-120 days.

Can I sell my house the day before foreclosure auction?

Technically yes, if you can close the transaction before the auction occurs. However, this creates extreme risk. Title companies need time to process documents, funds must transfer, and any complications could cause failure. Aim to close at least 7-10 days before the auction date.

Will selling in pre-foreclosure hurt my credit?

Selling before foreclosure completion actually protects your credit. The missed payments already reported will affect your score, but avoiding the foreclosure itself prevents the most severe damage (200-400 point drop).

Do I need my lender’s permission to sell?

No, you don’t need permission to sell—you own the property. However, you must pay off the full mortgage balance (or get short sale approval) to transfer clear title. Communicating with your lender about your sale efforts is wise and may buy you additional time.

What if I owe more than my house is worth?

If you’re underwater, you have two primary options: short sale (where the lender agrees to accept less than owed) or sell to a cash buyer who can close quickly and help negotiate the shortage with your lender.

Can I sell to a family member during pre-foreclosure?

Yes, but the transaction must be legitimate and at fair market value. The lender will scrutinize related-party transactions to ensure they’re not fraudulent attempts to avoid foreclosure.

Taking Action: Your Next Steps

Pre-foreclosure feels overwhelming, but you’ve now armed yourself with knowledge about your complete options. The question “Can I Sell My House in Pre-Foreclosure? Your Complete Options” has a clear answer: yes, you can sell, and you have multiple pathways to do so successfully.

Your immediate action plan:

- Assess your timeline today: How many days until foreclosure auction?

- Determine your equity position: Get a property valuation and payoff statement this week

- Choose your strategy: Based on time available and equity, select traditional listing, cash buyer, or short sale

- Contact your lender: Inform them of your selling efforts and request cooperation

- Take action immediately: Every day matters—contact professionals who can help

- Get expert help if needed: Complex situations with liens, taxes, or title issues require specialized expertise

How Sure Path Property Solutions Can Help

If you’re facing pre-foreclosure with complications—back taxes, liens, judgments, multiple owners, or simply need to sell quickly—Sure Path Property Solutions offers the helpful solutions and expert service you need.

We specialize in:

- ✅ Fast cash purchases (close in 7-14 days)

- ✅ Buying properties as-is (no repairs needed)

- ✅ Resolving complex title issues

- ✅ Coordinating with counties on tax matters

- ✅ Working with multiple heirs and owners

- ✅ Handling properties with liens and judgments

- ✅ Providing clear, honest guidance without pressure

Our process is simple:

- Contact us with your property information

- Receive a fair cash offer within 24-48 hours

- Choose your closing date (as fast as 7 days)

- Close and move forward with cash in hand

You don’t have to navigate pre-foreclosure alone. Friendly and caring professionals who understand your situation can make this challenging time manageable and help you emerge with your financial dignity intact.

Conclusion: You Have Options and You Have Time—Use Both Wisely

The pre-foreclosure period represents a critical window of opportunity. While it arrives during a stressful and difficult time, it also provides you with options, rights, and the ability to control your outcome. The worst decision is inaction—hoping the problem resolves itself or that the lender will simply go away.

You can absolutely sell your house in pre-foreclosure. Whether through traditional listing, cash sale, or short sale, you have pathways to avoid foreclosure’s devastating consequences and protect your financial future.

The key factors for success are:

- Speed: Act immediately—every day counts

- Information: Understand your timeline, equity position, and options

- Communication: Keep your lender informed and request cooperation

- Professional help: Work with industry experts who specialize in these situations

- Decisiveness: Choose a strategy and execute it fully

Remember that companies like Sure Path Property Solutions exist specifically to help homeowners in complicated situations. We’ve seen it all—back taxes, liens, judgments, multiple heirs, unclear titles—and we’ve helped hundreds of property owners find their path forward with helpful guidance and trustworthy service.

Your pre-foreclosure situation doesn’t define you. It’s a financial challenge, and like all challenges, it can be overcome with the right information, the right help, and decisive action. Take the first step today. Your future self will thank you.

References

[1] Consumer Financial Protection Bureau. (2025). “What happens if I miss mortgage payments?” CFPB Mortgage Resources.

[2] National Association of Realtors. (2025). “State Foreclosure Laws and Timelines.” NAR Legal Research.

[3] Experian. (2025). “How Foreclosure Affects Your Credit Score.” Credit Education Resources.

[4] Internal Revenue Service. (2025). “Cancellation of Debt and Mortgage Forgiveness.” IRS Publication 4681.