Can You Sell a House with a Lien? Everything You Need to Know

Discovering a lien on your property when you’re ready to sell can feel like hitting a brick wall. Many homeowners facing this situation wonder if their plans to sell are completely derailed. The good news? Can you sell a house with a lien? Everything you need to know starts with understanding that yes, selling is absolutely possible—but it requires navigating specific steps to ensure a successful transaction. Whether you’re dealing with tax liens, judgment liens, or other encumbrances, helpful solutions exist to move forward with your sale.

Property liens represent legal claims against your home, typically filed by creditors, government agencies, or contractors who are owed money. While these claims can complicate the selling process, they don’t make it impossible. Understanding how liens work, what types affect home sales, and the practical steps to resolve them empowers property owners to make informed decisions during what can be a stressful time.

Key Takeaways

- Yes, you can sell a house with a lien, but the lien must be resolved before closing to transfer clear title to the buyer

- Sale proceeds typically pay off liens in approximately 90% of cases, eliminating the need for out-of-pocket payments

- Title searches identify all recorded liens, and title companies ensure these are satisfied at closing

- Multiple resolution options exist, including negotiating debt, disputing errors, or incorporating payoff into sale proceeds

- Professional guidance from industry experts can simplify complex lien situations and accelerate the selling process

Understanding Property Liens and Their Impact

A property lien is a legal claim or “hold” on real estate that serves as security for a debt or obligation. When someone files a lien against your property, they’re essentially saying, “This person owes me money, and I have a legal right to be paid from the proceeds if this property sells.”

What Makes a Lien Legally Binding?

Creditors record liens in the county clerk’s office to protect their interest and provide public notice of their claim. This recording creates what’s called “constructive notice”—meaning anyone who searches public records will discover the lien exists[3].

Here’s what makes this important:

- Even if a buyer doesn’t know about a lien, they can still inherit the liability if it was properly recorded before the sale

- The lien “follows” the property, not just the person who incurred the debt

- Buyers receive title subject to any existing liens, which is why title searches are essential

Common misconception: Many people believe a lien legally prevents selling property altogether. In reality, you can validly sell property with a lien attached—but doing so without resolving it encumbers the buyer with that liability[3]. No reasonable buyer would accept this situation, which is why liens must be addressed before closing.

How Liens Affect the Selling Process

When you attempt to sell a property with liens, several things happen:

- Title search reveals all recorded liens during the preliminary stages

- Title insurance companies refuse to insure until liens are cleared

- Buyers’ lenders won’t approve financing for properties with unresolved liens

- Closing cannot proceed until clear title can be transferred

This creates a practical barrier to selling, even though it’s not technically a legal prohibition. The trustworthy service of title companies protects both buyers and sellers by ensuring all claims are satisfied before ownership transfers.

Can You Sell a House with a Lien? The Definitive Answer

Yes, you absolutely can sell a house with a lien—but with important conditions. The lien must be resolved before the sale can complete and the buyer can take possession of the property[1][3]. This doesn’t mean you need thousands of dollars sitting in your bank account before listing your home. In fact, most sellers use the sale proceeds themselves to pay off liens at closing.

The Reality of Selling with Liens

Think of a lien like a toll booth on the highway to selling your home. You can travel the road, but you must pay the toll before reaching your destination. The helpful guidance from real estate professionals ensures you know exactly how much that “toll” costs and the best route to pay it.

In approximately 90% of cases, sale proceeds are sufficient to pay off liens without requiring the seller to contribute additional out-of-pocket funds[1]. This happens seamlessly at the closing table, where the title company coordinates payments to all lien holders from the buyer’s purchase funds.

When Liens Exceed Property Value

The more challenging situation occurs when liens total more than the property’s market value. This is called being “underwater” or “upside down” on the property. In these cases:

- Traditional buyers cannot purchase the property

- Lenders won’t approve mortgages

- Alternative solutions become necessary

- Cash buyers or investors may still be interested

- Short sales might be an option (with lender approval)

This is where expert service from companies like Sure Path Property Solutions becomes invaluable. Industry experts who specialize in complicated real estate issues can coordinate with counties, title professionals, and lien holders to find practical solutions even in difficult situations.

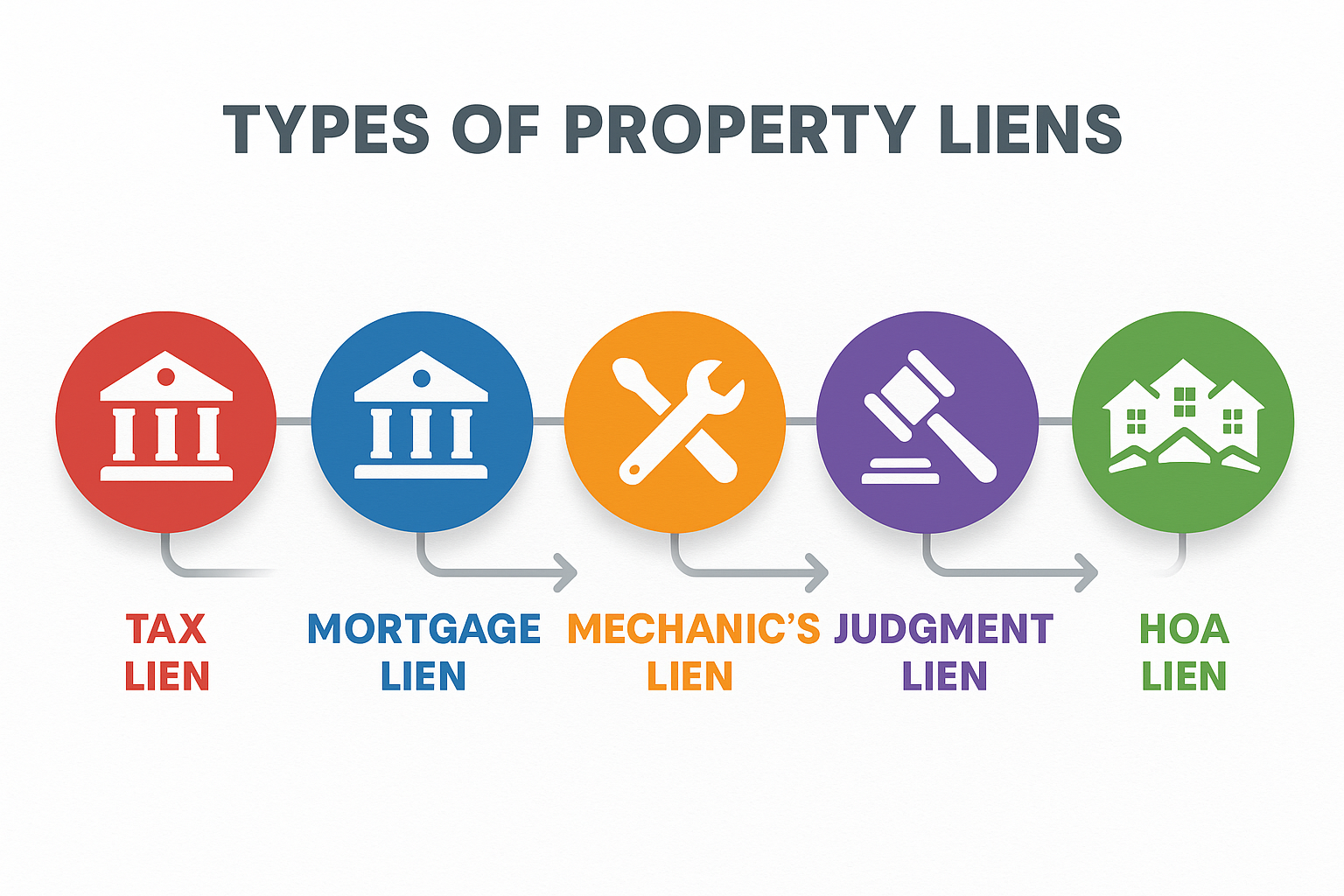

Types of Liens That Affect Home Sales

Not all liens are created equal. Understanding the different types helps property owners prioritize which debts to address first and anticipate potential complications. Some liens take legal priority over others, affecting the order in which they must be paid from sale proceeds.

Tax Liens: The Priority Claim

Tax liens are recorded by government agencies when property owners owe back taxes—whether property taxes, income taxes, or other government debts[1]. These liens carry special significance because they typically take priority over all other liens, including even primary mortgage liens.

Why tax liens take priority:

- Government claims are legally prioritized in most jurisdictions

- Property taxes fund essential local services

- Federal tax liens can supersede nearly all other claims

- Mortgage lenders recognize this priority, which is why they often include property taxes in monthly payment schedules[1]

Real-world example: Imagine Sarah owns a home worth $300,000 with a $200,000 mortgage and $15,000 in unpaid property taxes. When she sells, the tax lien gets paid first from the proceeds, then the mortgage, then any remaining funds go to Sarah. This priority system protects government revenue while ensuring fair distribution of sale proceeds.

Mortgage Liens: The Expected Encumbrance

When you finance a home purchase, the lender places a mortgage lien on the property. This is the most common type of lien and is expected in most real estate transactions. Mortgage liens are voluntary liens—you agreed to them when you borrowed money to buy the property.

Key characteristics:

- Usually the largest debt against the property

- Must be paid in full at closing (unless buyer assumes the mortgage)

- Lender provides a “payoff statement” showing exact amount owed

- Relatively straightforward to resolve through sale proceeds

Mechanic’s Liens: When Contractors Aren’t Paid

Contractors, subcontractors, and material suppliers can file mechanic’s liens (also called construction liens) when they perform work or provide materials for your property but don’t receive payment. These liens protect workers and suppliers in the construction industry.

Important facts about mechanic’s liens:

- Must be filed within specific timeframes (varies by state, typically 30-120 days after work completion)

- Can be filed even if you paid the general contractor (if they didn’t pay their subcontractors)

- Often require legal assistance to resolve

- May be negotiable, especially if the work was defective or incomplete

Helpful tip: Always obtain lien waivers from contractors and subcontractors when paying for property improvements. This prevents future lien claims.

Judgment Liens: Court-Ordered Claims

When someone sues you and wins a monetary judgment, they can record a judgment lien against your property. These liens arise from unpaid debts that went through the court system—credit card debt, medical bills, personal loans, or other obligations[1][2].

Judgment liens present unique challenges:

- Require court approval to sell the property in many jurisdictions[1][2]

- May involve additional court costs and attorney’s fees[1][2]

- Can remain attached to property for years (typically 5-20 years depending on state law)

- Creditor may be willing to negotiate for less than full amount

- Real estate attorneys provide invaluable guidance for these complex situations[1][2]

Child Support and Alimony Liens

Government agencies can place liens on property for unpaid child support or alimony obligations[1]. These liens protect the interests of children and former spouses who depend on court-ordered support payments.

Special considerations:

- Obtaining court approval for sale can take considerable time[1]

- These liens often cannot be negotiated or reduced

- Courts prioritize these claims due to their nature

- May require family law attorney involvement

HOA Liens: Community Association Claims

Homeowners associations can file liens for unpaid dues, assessments, or fines. While typically smaller than other lien types, HOA liens can still prevent property sales and may accumulate significant late fees and legal costs over time.

HOA lien characteristics:

- Vary significantly based on association bylaws

- May include collection costs and attorney fees

- Some states give HOA liens “super priority” status over even mortgage liens

- Usually easier to resolve than government liens

Lien Priority: Understanding the Pecking Order

When multiple liens exist on a property, they’re typically paid in this order from sale proceeds:

- Property tax liens (highest priority)

- Federal tax liens

- First mortgage lien

- Second mortgage or home equity liens

- Judgment liens (paid in order of recording)

- Mechanic’s liens

- HOA liens (varies by state)

This hierarchy matters when sale proceeds aren’t sufficient to pay all debts. Lower-priority lien holders may receive partial payment or nothing at all.

The Process of Selling a House with a Lien

Understanding the step-by-step process of selling property with liens removes much of the anxiety and uncertainty. While each situation has unique elements, the general framework remains consistent across most transactions.

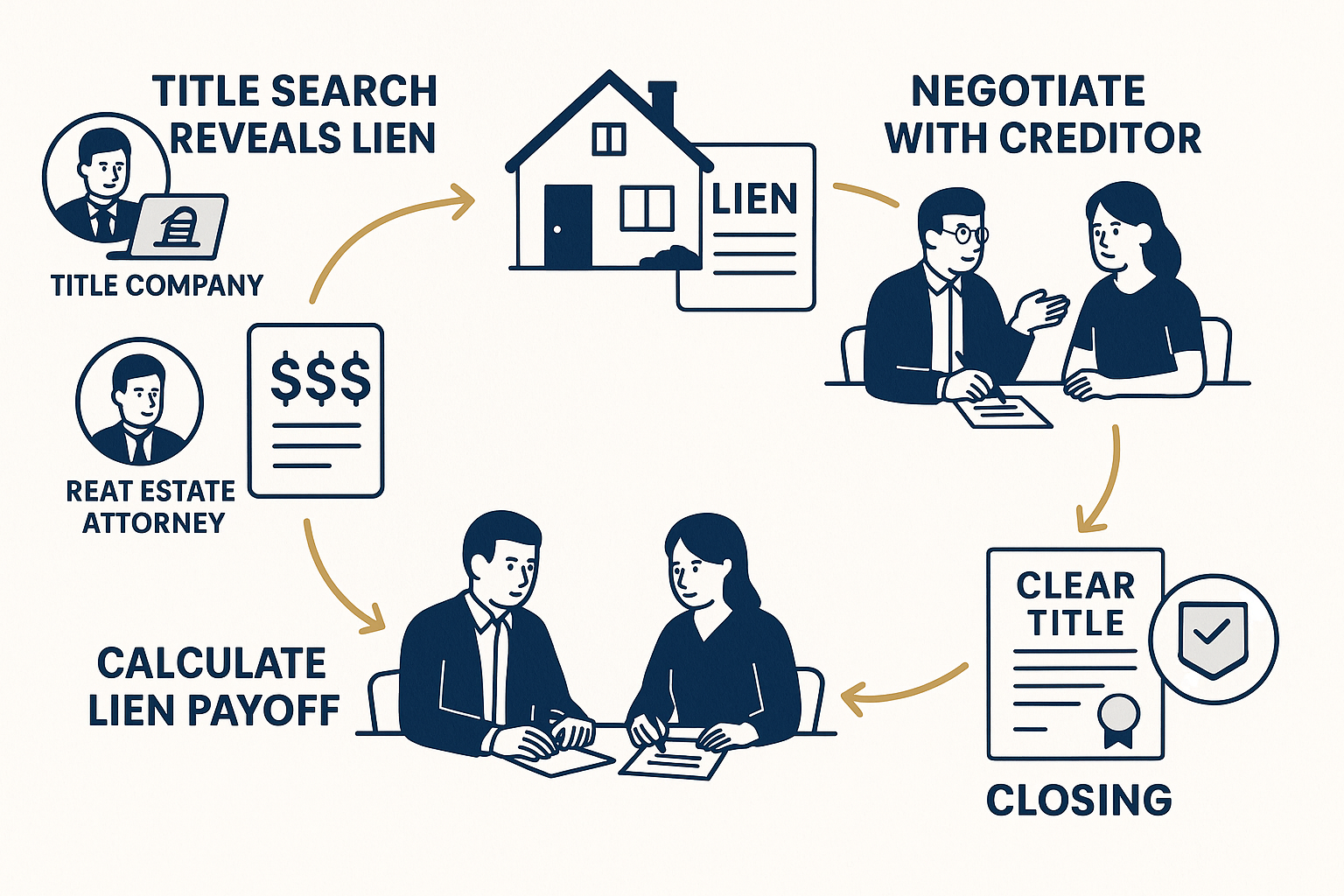

Step 1: Discover Liens Through Title Search

The journey begins with a comprehensive title search conducted by a title company or real estate attorney. This search examines public records to identify all liens, encumbrances, claims, and ownership issues affecting the property.

What the title search reveals:

- All recorded liens with amounts owed

- The lien holders’ contact information

- Recording dates (establishing priority)

- Any errors or discrepancies in public records

- Other title issues like easements or boundary disputes

Professional insight: Don’t skip this step or rely on your own research. Title professionals have access to specialized databases and understand the nuances of property records that laypeople often miss.

Step 2: Obtain Payoff Statements

Once liens are identified, contact each lien holder to request a payoff statement or payoff quote. This document specifies:

- The exact amount needed to satisfy the lien

- The date through which the payoff amount is valid

- Daily interest accrual (if applicable)

- Any additional fees or costs

- Instructions for submitting payment

Payoff amounts often differ from the original debt due to accumulated interest, penalties, and fees. Getting accurate, current payoff figures prevents surprises at closing.

Step 3: Calculate Your Net Proceeds

With payoff statements in hand, calculate whether sale proceeds will cover all liens and selling costs:

Estimated Sale Price

− Real estate commissions (typically 5-6%)

− Closing costs (1-3% of sale price)

− All lien payoffs

− Any other debts or obligations

= Your Net Proceeds

This calculation reveals whether you’ll walk away from closing with money in hand or need to bring funds to the table. If the numbers don’t work with traditional buyers, alternative solutions become necessary.

Step 4: Choose Your Resolution Strategy

Based on your financial situation and the lien amounts, select the most appropriate strategy:

Option A: Pay Liens at Closing (Most Common)

In this scenario, the title company acts as an intermediary:

- Buyer’s funds arrive at closing

- Title company pays off all liens directly

- Remaining proceeds go to the seller

- Lien holders issue lien releases

- Clear title transfers to buyer

This is the cleanest, most straightforward approach and works in approximately 90% of cases[1].

Option B: Pay Liens Before Listing

Some sellers prefer to clear liens before marketing the property:

✅ Advantages:

- Simpler marketing (no lien disclosure needed)

- Faster closing process

- More attractive to traditional buyers

- Eliminates last-minute complications

❌ Disadvantages:

- Requires upfront cash

- May delay listing while gathering funds

- Unnecessary if proceeds would cover liens anyway

Option C: Negotiate Lien Amounts

Many lien holders, especially judgment creditors, will accept less than the full amount owed. This process, called “settling” or “negotiating” the debt, can significantly reduce what you owe[1].

Negotiation tips:

- Offer a lump sum payment (creditors prefer certainty)

- Explain your financial hardship honestly

- Get all settlement agreements in writing

- Ensure the agreement includes lien release upon payment

- Consider hiring a real estate attorney for complex negotiations[1][2]

Real-world example: Marcus owed $12,000 on a judgment lien from an old credit card debt. The creditor agreed to accept $7,000 as payment in full because they’d been trying to collect for years and valued the guaranteed payment. Marcus saved $5,000 through friendly and caring negotiation.

Option D: Dispute Erroneous Liens

Sometimes liens are filed incorrectly—wrong property, wrong person, debt already paid, or procedural errors in filing. Disputing debt errors requires legal assistance[1] but can completely eliminate invalid liens.

Grounds for disputing liens:

- Lien filed against wrong property (mistaken identity)

- Debt was already satisfied but lien not released

- Statute of limitations has expired

- Procedural defects in lien filing

- Fraudulent lien (rare but serious)

An experienced real estate attorney can file the necessary motions and represent your interests in court if needed.

Step 5: Coordinate with Title Company

The title company serves as the central coordinator for lien resolution. Their responsibilities include:

- Verifying all payoff amounts

- Ensuring sufficient funds at closing

- Disbursing payments to lien holders

- Obtaining lien releases

- Recording releases with the county

- Issuing title insurance to the buyer

This expert service protects all parties and ensures the transaction complies with legal requirements. Title companies will not allow closing to proceed unless all liens are satisfied[1], providing an essential safeguard in the process.

Step 6: Close the Sale and Transfer Clear Title

At the closing table, everything comes together:

- Buyer’s funds are deposited with title company

- Seller signs deed transferring ownership

- Title company pays all liens from buyer’s funds

- Remaining proceeds distributed to seller

- Lien releases recorded

- Clear title transfers to buyer

- Title insurance policy issued

The buyer receives the property free and clear of all liens, and the seller moves forward without those debts following them (since they were satisfied through the property sale).

Your Options When Selling a House with a Lien

Property owners facing lien situations have multiple pathways forward. The best choice depends on individual circumstances, including equity position, urgency to sell, and the types of liens involved.

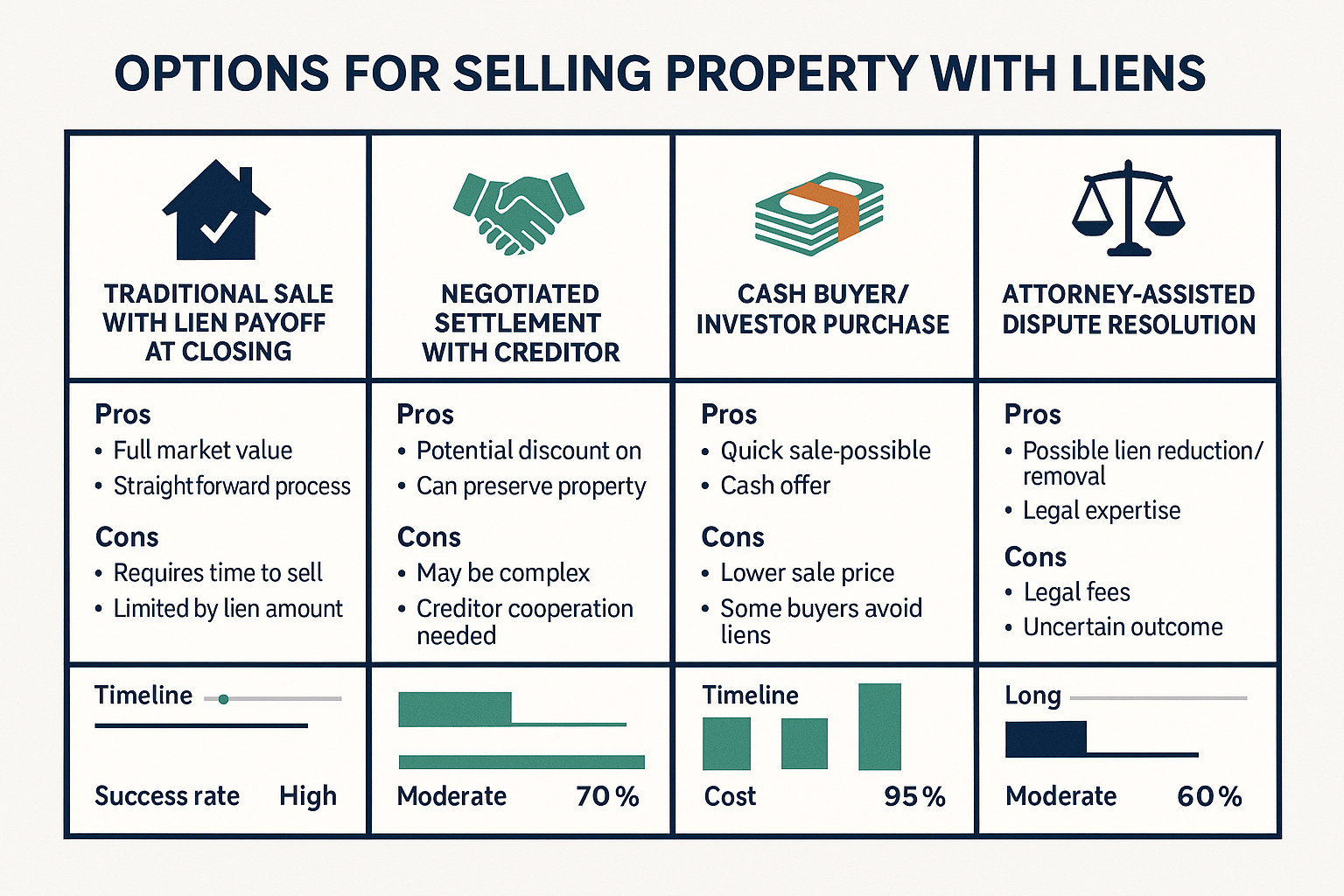

Traditional Sale Through Real Estate Agent

Best for: Properties where sale proceeds will cover all liens with equity remaining

This conventional approach works when the numbers make sense:

✅ Advantages:

- Maximum market exposure

- Competitive offers

- Professional marketing

- Familiar process for buyers

❌ Challenges:

- Takes longer (typically 60-120 days)

- Requires property preparation and showings

- Buyers may be concerned about lien complications

- Agent commissions reduce net proceeds

Action steps:

- Complete title search to identify all liens

- Obtain payoff statements

- Calculate estimated net proceeds

- Hire experienced real estate agent

- Price property appropriately

- Disclose liens to potential buyers

- Work with title company to coordinate payoff at closing

Selling to Cash Buyers or Real Estate Investors

Best for: Properties with significant lien amounts, urgent timelines, or complicated title issues

Companies like Sure Path Property Solutions specialize in purchasing properties with liens, back taxes, and other complications. This option provides helpful solutions when traditional sales aren’t feasible.

✅ Advantages:

- Fast closing (often 7-30 days)

- No repairs or preparation needed

- Expert service handling all lien negotiations

- Certainty of closing

- No agent commissions

- Industry experts coordinate with counties and title professionals

❌ Considerations:

- Offer price typically below market value

- Less competitive than open market

- Reduced net proceeds compared to traditional sale (in some cases)

When this option makes sense:

- Liens exceed 70% of property value

- Multiple complicated liens (judgments, tax liens, mechanic’s liens)

- Urgent need to sell quickly

- Property needs significant repairs

- Inherited property with unclear title or multiple heirs

- Difficulty selling via traditional means

Real-world example: Jennifer inherited her father’s house with $45,000 in back taxes, a $30,000 judgment lien, and needed $20,000 in repairs. Traditional buyers wouldn’t touch it. Sure Path Property Solutions purchased the property, coordinated with the county and creditors, handled all lien payoffs, and closed in 21 days. Jennifer received cash and avoided months of stress dealing with multiple creditors and government agencies.

Short Sale (For Underwater Properties)

Best for: Properties where total liens exceed market value and the primary mortgage holder agrees to accept less than owed

A short sale requires the primary lien holder (usually the mortgage lender) to agree to accept less than the full payoff amount. This is challenging but sometimes possible:

Requirements:

- Demonstrated financial hardship

- Property value less than total debt

- Lender approval (not guaranteed)

- Extensive documentation

- Patience (process takes 3-6 months typically)

✅ Advantages:

- Avoids foreclosure

- May eliminate deficiency judgment

- Resolves multiple liens simultaneously

❌ Challenges:

- Lender must approve (many don’t)

- Damages credit (though less than foreclosure)

- Tax implications (forgiven debt may be taxable income)

- Very time-consuming process

- No guarantee of approval

Attorney-Assisted Lien Resolution

Best for: Complex situations involving judgment liens, disputes, or legal challenges

Real estate attorneys provide invaluable guidance for complicated lien situations[1][2]. They can:

- Negotiate with creditors on your behalf

- Dispute invalid or erroneous liens

- Navigate court approval processes for judgment liens[1][2]

- Identify legal defenses or procedural defects

- Represent you in lien-related litigation

- Coordinate with title companies and other professionals

When to hire an attorney:

- Judgment liens requiring court approval[1][2]

- Disputed or questionable liens

- Multiple liens from different sources

- Liens involving court costs and attorney’s fees[1][2]

- Mechanic’s liens for defective work

- Complex title issues beyond standard liens

The cost of attorney services (typically $1,500-$5,000 for lien matters) often pays for itself through successful negotiations or dispute resolutions.

Practical Steps to Take Today

If you’re facing the challenge of selling a house with a lien, taking action now moves you closer to resolution. Here’s your practical roadmap:

Immediate Actions (This Week)

1. Order a comprehensive title search

Contact a title company or real estate attorney to examine public records and identify all liens against your property. This creates a complete picture of what you’re dealing with.

2. Request payoff statements

Contact each lien holder identified in the title search and request current payoff amounts. Get these in writing with specific validity dates.

3. Calculate your equity position

Determine your property’s current market value (request a comparative market analysis from a real estate agent or order an appraisal). Subtract all lien payoffs and estimated selling costs to see if you’ll have positive equity.

Short-Term Actions (This Month)

4. Explore resolution options

Based on your equity position and circumstances, evaluate which selling approach makes most sense:

- Traditional sale if you have significant equity

- Cash buyer if liens are substantial or timeline is urgent

- Attorney assistance if liens are disputed or complex

5. Gather documentation

Compile all relevant documents:

- Property deed

- Mortgage statements

- Tax bills

- Lien notices and correspondence

- Proof of payments made

- Any dispute-related documentation

6. Consult with professionals

Speak with:

- Real estate agents experienced with lien sales

- Real estate attorneys for legal guidance

- Cash buyers like Sure Path Property Solutions for alternative options

- Tax professionals about potential tax implications

Medium-Term Actions (Next 1-3 Months)

7. Implement your chosen strategy

Whether listing traditionally, negotiating with lien holders, or selling to a cash buyer, move forward with your selected approach.

8. Maintain communication

Stay in regular contact with all parties:

- Lien holders (especially during negotiations)

- Real estate professionals assisting you

- Title company coordinating the transaction

- Potential buyers or their representatives

9. Prepare for closing

Work with your title company to ensure:

- All payoff amounts are current and accurate

- Lien releases will be provided upon payment

- Closing date allows sufficient time for lien processing

- All parties understand their responsibilities

Common Mistakes to Avoid

Learning from others’ errors saves time, money, and frustration. Avoid these common pitfalls when selling property with liens:

❌ Ignoring Liens and Hoping They’ll Disappear

Liens don’t vanish on their own. They remain attached to the property until satisfied, and ignoring them only allows interest and penalties to accumulate. Take action early rather than hoping the problem resolves itself.

❌ Attempting to Hide Liens from Buyers

Some sellers think they can conceal liens and complete a sale before anyone discovers them. This approach:

- Violates disclosure laws in most states

- Creates legal liability for fraud

- Will be discovered during title search anyway

- Destroys trust and kills deals

- May result in lawsuits

Transparency is always the better path. Honest disclosure with a clear resolution plan actually builds buyer confidence.

❌ Accepting the First Payoff Amount Without Verification

Lien holders sometimes provide inflated payoff amounts or include questionable fees. Always:

- Request itemized payoff statements

- Verify interest calculations

- Question unusual fees

- Compare amounts to original debt

- Consider negotiating even “non-negotiable” amounts

❌ Proceeding Without Professional Guidance

While it’s possible to handle simple lien situations independently, most benefit from expert service. The cost of professional assistance (title company, attorney, or experienced cash buyer) typically pays for itself through:

- Avoided mistakes

- Successful negotiations

- Faster resolution

- Reduced stress

- Legal protection

❌ Failing to Get Settlement Agreements in Writing

Verbal agreements with creditors are worthless. Always get negotiated settlements in writing before making any payments. The agreement should specify:

- Exact payment amount

- Payment deadline

- That payment satisfies the debt in full

- Lien release will be provided

- No further claims will be made

❌ Not Following Up on Lien Releases

After paying off liens, ensure releases are actually recorded with the county. Some creditors are slow to file releases, leaving the lien appearing active in public records. Follow up within 30 days of payment to confirm:

- Release document was prepared

- Release was recorded with county clerk

- Your title is clear in public records

Frequently Asked Questions

Can I sell my house with a lien on it?

Yes, you can sell your house with a lien on it. The lien must be resolved before closing, but in approximately 90% of cases, the sale proceeds themselves pay off the lien without requiring out-of-pocket payment from the seller[1]. The title company coordinates lien payoff at closing, ensuring clear title transfers to the buyer.

Can you sell a house with liens on it to a traditional buyer?

Yes, you can sell to traditional buyers if the sale price exceeds the total of all liens and selling costs. The buyer’s lender will require all liens to be satisfied at closing as a condition of financing. Your real estate agent and title company will coordinate the process to ensure all liens are paid from the sale proceeds before ownership transfers.

What happens if I can’t pay off the liens when selling?

If liens exceed your property’s value or you can’t cover the gap between sale price and lien amounts, you have several options:

- Negotiate with lien holders to accept reduced payments

- Sell to a cash buyer who specializes in complicated situations

- Pursue a short sale (requires lender approval)

- Bring cash to closing to cover the shortfall

- Explore lien dispute if you believe liens are invalid

Companies like Sure Path Property Solutions provide helpful guidance for these challenging scenarios, working with counties and creditors to find practical solutions.

How long does it take to sell a house with a lien?

The timeline varies based on your approach:

- Traditional sale: 60-120 days (plus time to resolve liens before listing)

- Cash buyer sale: 7-30 days (buyer handles lien coordination)

- Short sale: 3-6 months (requires lender approval)

- Attorney-assisted resolution: Varies widely based on complexity

Starting the process early and working with industry experts accelerates the timeline significantly.

Do all liens have to be paid when selling a house?

Yes, all liens must be satisfied before clear title can transfer to a buyer. Title companies will not issue title insurance—and buyers’ lenders will not fund the purchase—until all liens are resolved. This protects the buyer from inheriting your debts with the property.

Can I sell my house if I have a tax lien?

Absolutely. Tax liens are actually among the most straightforward to resolve because the payoff amount is clear and non-negotiable. The sale proceeds pay the tax lien at closing (tax liens receive priority payment), and the government agency releases the lien. Many property owners successfully sell homes with tax liens every year.

Will a lien affect my credit score?

The lien itself may already be affecting your credit (especially judgment liens and tax liens). However, satisfying the lien through your property sale typically improves your credit because the debt is resolved. The lien notation on your credit report will update to show “satisfied” or “paid,” which is much better than an outstanding lien.

Can I negotiate liens for less than the full amount?

Yes, many liens are negotiable, particularly:

- Judgment liens: Creditors often accept 40-70% of the amount owed

- Mechanic’s liens: Especially if work quality is disputed

- Some medical liens: Healthcare providers may reduce amounts

- Old debts: The longer unpaid, the more negotiable

Tax liens and mortgage liens are typically non-negotiable, though payment plans may be available. An experienced real estate attorney can provide invaluable guidance for negotiations[1][2].

Why Sure Path Property Solutions Offers the Best Path Forward

When facing complicated property situations involving liens, back taxes, judgments, or unclear title, working with specialists makes all the difference. Sure Path Property Solutions provides expert service for property owners navigating these challenging circumstances.

What Makes Sure Path Different

Specialized expertise: Unlike traditional real estate agents who occasionally encounter lien situations, Sure Path Property Solutions specializes exclusively in complicated real estate issues. This focused expertise means:

- Deep understanding of lien resolution processes

- Established relationships with counties and title professionals

- Experience coordinating with multiple creditors simultaneously

- Knowledge of creative solutions for difficult situations

Comprehensive coordination: Rather than property owners juggling communication with tax authorities, creditors, courts, and title companies, Sure Path handles all coordination. This trustworthy service removes the burden from overwhelmed property owners.

Solutions for “unsellable” properties: When traditional buyers walk away due to:

- Back taxes on property (land or houses)

- Multiple liens and judgments

- Inherited property with multiple heirs

- Unclear or clouded title

- Properties requiring significant repairs

Sure Path provides helpful solutions where others see only problems.

The Sure Path Process

- Free consultation: Discuss your situation without obligation

- Comprehensive evaluation: Review all liens, title issues, and property condition

- Fair cash offer: Receive a straightforward offer based on property value and resolution costs

- Complete coordination: Sure Path handles all lien negotiations and payoffs

- Fast closing: Close in as little as 7 days or on your timeline

- Clear resolution: Walk away with cash and all liens satisfied

This friendly and caring approach transforms what seems like an impossible situation into a clear path forward.

When to Contact Sure Path Property Solutions

Consider reaching out if you’re experiencing:

- Multiple complicated liens making traditional sales difficult

- Time pressure requiring fast resolution

- Inherited property with unclear ownership or multiple heirs

- Back taxes creating financial stress

- Judgment liens requiring court coordination

- Difficulty selling through traditional real estate channels

- Property condition issues combined with lien problems

The industry experts at Sure Path Property Solutions provide helpful guidance regardless of how complicated your situation appears. Sometimes a simple conversation reveals solutions you hadn’t considered.

Conclusion: Your Path to Selling Success

Can you sell a house with a lien? Everything you need to know comes down to this: yes, selling is absolutely possible, and you have more options than you might think. While liens create complications, they don’t create impossibilities. Whether your property has tax liens, judgment liens, mechanic’s liens, or multiple encumbrances, practical solutions exist to move forward successfully.

The key is taking informed action rather than avoiding the situation. Start with a comprehensive title search to understand exactly what you’re facing. Obtain accurate payoff statements from all lien holders. Calculate your equity position realistically. Then choose the approach that best fits your circumstances—whether that’s a traditional sale, negotiating with creditors, or working with specialized cash buyers who handle complicated situations.

Remember these essential points:

🏠 Liens must be resolved before closing, but sale proceeds typically cover them without out-of-pocket costs

📋 Title companies ensure all liens are satisfied, protecting both buyers and sellers

💡 Multiple resolution strategies exist, from negotiation to dispute to alternative buyers

⚖️ Professional guidance accelerates the process and often saves money through expert negotiations

🤝 Specialized companies like Sure Path Property Solutions provide helpful solutions for complicated situations involving liens, back taxes, multiple heirs, and unclear title

Your Next Steps

Don’t let liens keep you trapped in property ownership when you’re ready to move forward. Take these actions today:

- Order a title search to identify all liens against your property

- Request payoff statements from all lien holders

- Evaluate your options based on your equity position and timeline

- Consult with professionals who specialize in lien situations

- Take action rather than hoping the problem resolves itself

If your situation involves complicated liens, back taxes, multiple heirs, or other challenges that make traditional sales difficult, contact Sure Path Property Solutions for a free consultation. The friendly and caring team provides expert service to property owners navigating exactly these situations, offering helpful guidance and practical solutions when you need them most.

Your property doesn’t have to remain a burden. With the right approach and trustworthy service from industry experts, you can resolve liens, satisfy debts, and move forward to your next chapter. The path to selling success starts with a single step—take it today.

References

[1] Title company industry standards and practices for lien resolution in real estate transactions, based on standard title insurance requirements and closing procedures.

[2] Real estate attorney services and legal procedures for judgment lien resolution, court approval processes, and creditor negotiations in property sales.

[3] Property law principles regarding constructive notice, lien attachment to real property, and the legal ability to transfer property subject to encumbrances.