Debt Liens Explained: What They Are and How They Affect Property Sales

Imagine discovering that your property—your most valuable asset—cannot be sold because of a legal claim you didn’t even know existed. This nightmare scenario happens to thousands of property owners every year when

debt liens attach to their real estate. Understanding debt liens explained: what they are and how they affect property sales can mean the difference between a smooth transaction and a financial crisis that derails your plans for months or even years.

A

debt lien is a legal claim placed on property by creditors or government agencies to secure payment of unpaid debts. When property owners fall behind on taxes, contractor payments, homeowner association fees, or court judgments, these obligations don’t simply disappear—they attach directly to the property itself. This creates a powerful legal mechanism that ensures creditors get paid, but it also creates significant complications for property owners trying to sell, refinance, or transfer their real estate.

The impact of debt liens on property sales cannot be overstated. Properties with liens face reduced marketability, delayed transactions, lower sale prices, and in some cases, complete inability to transfer ownership until the debt is resolved. For property owners already facing financial challenges, this can feel overwhelming.

The good news? With helpful guidance from industry experts who understand these complex situations, property owners can navigate lien issues and find practical solutions. This comprehensive guide will walk through everything needed to understand debt liens explained: what they are and how they affect property sales.

Key Takeaways

- Debt liens are legal claims placed on property by creditors or government agencies to secure payment of unpaid debts, preventing sale or refinancing until resolved

- Multiple types of liens exist, including tax liens, judgment liens, mechanic’s liens, and mortgage liens, each with different priority levels and resolution processes

- Property sales are significantly impacted by liens, requiring full payment or negotiated settlement before title can transfer to a new owner

- Credit scores suffer when liens are placed on property, affecting future borrowing ability and financial opportunities

- Removal is possible through payment, negotiation, or legal challenge, with expert service available to guide property owners through the resolution process

What Is a Debt Lien?

A

debt lien represents one of the most powerful tools creditors have to collect unpaid obligations. At its core, a lien is a legal right or claim against property that serves as security for a debt. When someone owes money and fails to pay, the creditor can place a lien on their property, creating a public record that must be satisfied before the property can be sold or refinanced.[1]

The Legal Foundation of Liens

Liens operate under a simple principle: the property itself becomes collateral for the debt. This legal mechanism ensures that creditors have recourse when debtors fail to meet their financial obligations. Unlike unsecured debts that rely solely on the borrower’s promise to pay, liens create a direct connection between the debt and a tangible asset.

The process typically works like this:

- A debt goes unpaid despite notice and opportunity to pay

- The creditor obtains legal authority to place a lien (through court judgment, statutory right, or contractual agreement)

- The lien is recorded with the county recorder’s office in the jurisdiction where the property is located

- The lien becomes part of the public record, attached to the property’s title

- The lien must be satisfied before clear title can transfer to a new owner

Real Property Lien: Understanding the Legal Definition

A

real property lien specifically refers to claims against real estate—land and any structures permanently attached to it. This distinguishes it from personal property liens, which attach to movable assets like vehicles or equipment.

Real property liens carry significant legal weight because real estate typically represents substantial value and cannot be easily hidden or moved. The lien “runs with the land,” meaning it stays attached to the property regardless of who owns it. If a property owner sells real estate with an existing lien, the lien doesn’t disappear—it either must be paid from sale proceeds or transfers with the property to the new owner (though most buyers refuse to accept property with liens).

Key characteristics of real property liens include:

- Public record status: Recorded with county or municipal authorities

- Priority order: Liens are paid in specific order based on recording date and type

- Enforceability: Can lead to forced sale (foreclosure) if unpaid

- Transferability: Remain attached even when property ownership changes

- Duration: Continue until paid, released, or expired under statute of limitations

How Liens Differ from Other Debts

Understanding what makes liens unique helps property owners recognize their seriousness:

Secured vs. Unsecured Debt: Most credit card debt, medical bills, and personal loans are unsecured—creditors can sue and obtain judgments, but they don’t automatically have claims on specific property. Liens, by contrast, create secured interests in real estate from the outset.

Voluntary vs. Involuntary: Some liens are voluntary (like mortgages, where property owners agree to the lien when borrowing). Others are involuntary (like tax liens or judgment liens), placed without the owner’s consent when debts go unpaid.

Impact on Property Rights: While property owners retain ownership and can continue living in or using their property, liens significantly restrict what they can do with it. Selling, refinancing, or transferring property becomes extremely difficult or impossible until liens are resolved.

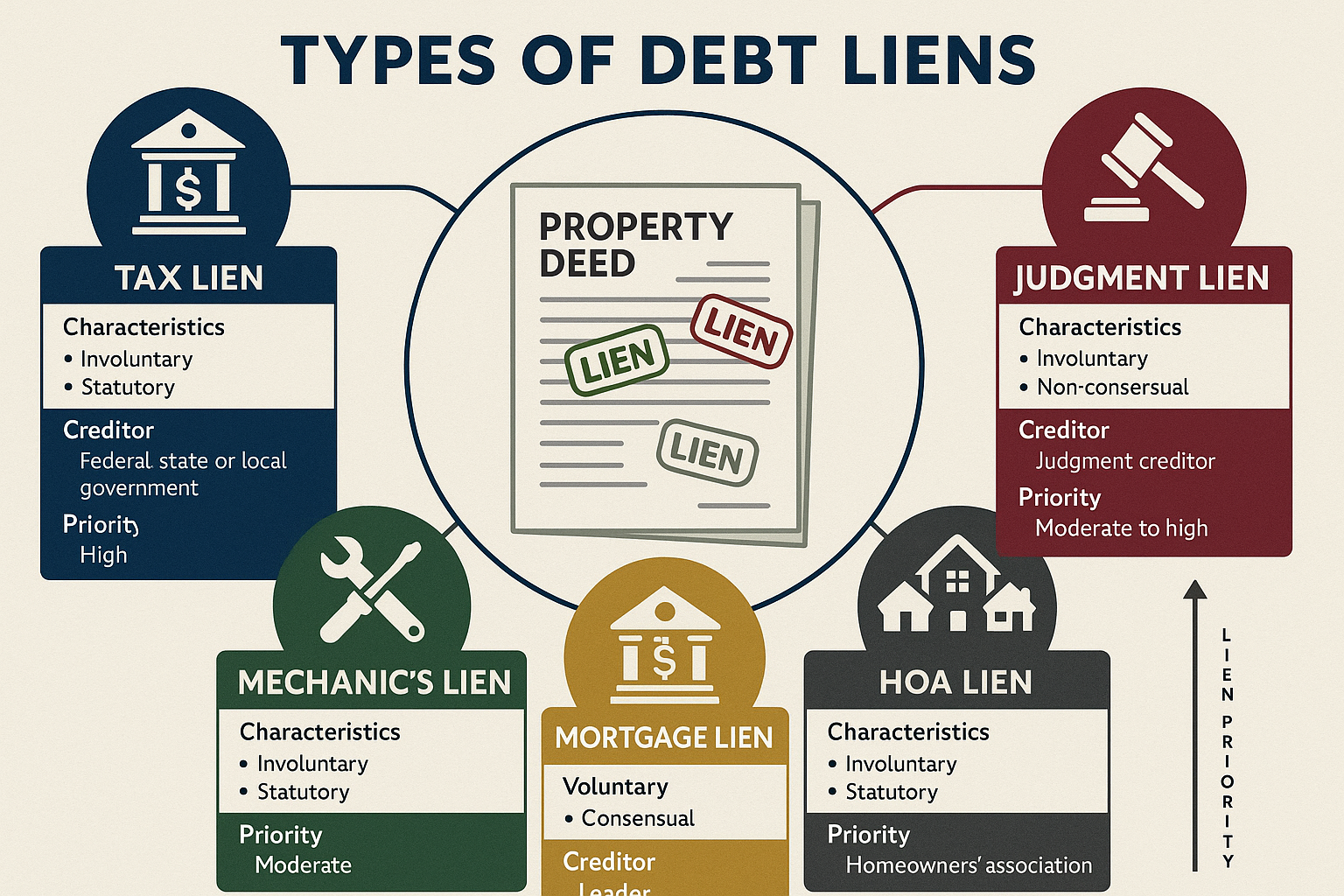

Types of Debt Liens

Not all liens are created equal. Different types of debt liens carry different priorities, legal requirements, and resolution processes. Understanding these distinctions helps property owners develop appropriate strategies for addressing lien issues.

Tax Liens: The Government’s Priority Claim

Tax liens rank among the most serious types of liens because government entities have extraordinary collection powers. When property owners fail to pay property taxes, income taxes, or other tax obligations, tax authorities can place liens that take priority over nearly all other claims.[2]

Property Tax Liens

Local governments depend on property tax revenue to fund schools, emergency services, and infrastructure. When property owners fall behind on these taxes, counties and municipalities act quickly to protect this critical revenue stream.

The property tax lien process typically follows this timeline:

- Property taxes become delinquent (usually after 30-90 days past due date)

- County sends notices and adds penalties and interest

- Tax lien is recorded against the property

- If unpaid, the county may sell the tax lien to investors or eventually foreclose

In many jurisdictions, tax liens are sold through public auctions where investors bid on the interest rate they’re willing to accept, with the lowest bid winning. The investor pays the delinquent taxes to the government and gains the right to collect from the property owner with interest.[3]

For example, in New York City, the 2025 lien sale was held on June 3, 2025, transferring unpaid property taxes, water and sewer charges, and other related fees to an authorized buyer. Once transferred, the new lienholder can charge additional interest and fees, and foreclosure can begin within one year if the debt isn’t paid or a payment agreement isn’t reached.[4]

Federal and State Tax Liens

The IRS and state tax agencies can place liens for unpaid income taxes, creating federal or state tax liens that attach to all property the taxpayer owns. These liens are particularly troublesome because:

- They take priority over most other liens (except some property tax liens)

- They appear on credit reports and severely damage credit scores

- They can attach to property acquired even after the lien is filed

- They require full payment or formal negotiation to release

Judgment Liens: Court-Ordered Claims

When creditors sue debtors and win, courts issue money judgments. In most states, these judgments can be converted into

judgment liens by recording the judgment with the county recorder’s office where the debtor owns property.

Judgment liens arise from various situations:

- Unpaid credit card debt lawsuits

- Breach of contract claims

- Personal injury awards

- Unpaid medical bills

- Business disputes

Once recorded, a judgment lien prevents property sale or refinancing until the judgment is satisfied. The judgment creditor may also be able to force sale of the property through judicial foreclosure to collect what they’re owed.

Mechanic’s Liens: Contractor and Supplier Protection

Mechanic’s liens (also called construction liens or materialman’s liens) protect contractors, subcontractors, and material suppliers who improve property but don’t receive payment for their work.[5]

These liens serve an important policy purpose: ensuring that people who add value to property get paid for their labor and materials. Without mechanic’s lien rights, contractors would face significant risk when working on projects.

Mechanic’s lien requirements vary by state but generally include:

- Preliminary notice sent to property owner before or shortly after work begins

- Strict deadlines for filing the lien (often 60-120 days after work completion)

- Detailed documentation of work performed and amounts owed

- Foreclosure lawsuit filed within specified timeframe (typically 1-2 years)

Property owners sometimes face mechanic’s liens even when they’ve paid the general contractor, if that contractor failed to pay subcontractors or suppliers. This creates frustrating situations requiring legal resolution.

Mortgage Liens: Voluntary Security Interests

Mortgage liens differ from other debt liens because property owners voluntarily agree to them when purchasing or refinancing real estate. The mortgage or deed of trust creates a lien that secures repayment of the loan.

While consensual, mortgage liens share key characteristics with other liens:

- They’re recorded in public records

- They must be satisfied before clear title can transfer

- They can lead to foreclosure if the borrower defaults

- They take priority based on recording date (first mortgage, second mortgage, etc.)

Most property sales involve paying off existing mortgage liens from sale proceeds, making this a routine part of real estate transactions.

HOA and Condo Association Liens

Homeowners associations and condominium associations can place liens for unpaid dues, assessments, and fees. These

residential liens have grown more common as association-governed communities have proliferated.

Association liens can be surprisingly powerful:

- Some states give them “super-priority” status, allowing them to take priority even over first mortgages for certain amounts

- Associations can foreclose on properties for relatively small amounts of unpaid dues

- Special assessments for major repairs can create substantial lien amounts quickly

Lien on Land: Special Considerations for Vacant Property

When discussing

lien on land specifically, vacant or undeveloped property faces unique challenges. Land without structures may seem like a simpler asset, but liens affect it just as seriously as improved property.

Special considerations for liens on land include:

- Lower value: Vacant land typically has less value than improved property, making liens a larger percentage of total worth

- Limited income: Land doesn’t generate rental income to help pay off liens

- Tax delinquency: Owners sometimes neglect tax payments on vacant land they’re not actively using

- Development obstacles: Liens must be cleared before land can be developed or sold to builders

- Reduced buyer pool: Fewer buyers seek vacant land, making lien-encumbered land even harder to sell

Property owners who inherited land or purchased it as an investment sometimes discover tax liens or other claims that have accumulated over years of neglect. Resolving these issues requires helpful solutions from professionals who understand both real estate and lien law.

Comparison of Common Lien Types

| Lien Type |

Common Causes |

Typical Priority |

Foreclosure Timeline |

Resolution Options |

| Property Tax Lien |

Unpaid property taxes |

Highest (usually first position) |

1-3 years depending on state |

Payment, payment plan, lien sale redemption |

| Federal Tax Lien |

Unpaid income taxes |

Very high (after property tax) |

Varies (IRS has extensive collection period) |

Payment, offer in compromise, installment agreement |

| Judgment Lien |

Court judgments from lawsuits |

Based on recording date |

1-2 years after recording |

Payment, settlement negotiation, appeal |

| Mechanic’s Lien |

Unpaid contractor/supplier bills |

Can relate back to project start |

1-2 years from filing |

Payment, bond, legal challenge |

| Mortgage Lien |

Home loan |

Based on recording date |

3-18 months from default |

Payment, loan modification, short sale |

| HOA Lien |

Unpaid association dues |

Varies by state (some super-priority) |

6 months – 2 years |

Payment, payment plan, negotiation |

How Debt Liens Affect Property Sales

Understanding debt liens explained: what they are and how they affect property sales requires examining the practical impact on real estate transactions. Liens create substantial obstacles that can delay, complicate, or completely prevent property sales.

The Title Search Revelation

Every legitimate property sale involves a

title search—a comprehensive examination of public records to identify any liens, encumbrances, or defects in the property’s ownership history. This is when many sellers first discover liens they didn’t know existed.

The title company or attorney conducting the search will uncover:

- All recorded liens against the property

- Judgments against the property owner

- Tax delinquencies

- Unpaid assessments

- Other clouds on title

When liens appear in the title search, the transaction cannot proceed to closing until they’re addressed. Title companies won’t issue title insurance (which protects buyers and lenders) on property with unresolved liens, and buyers won’t accept property with claims against it.

Impact on Marketability and Sale Price

Properties with liens suffer from significantly reduced marketability. Even before listing a property, sellers with lien issues face challenges:

Limited buyer pool: Most traditional buyers and their lenders won’t consider properties with title issues. Conventional mortgages require clear title, eliminating the largest segment of potential buyers.

Reduced sale price: Buyers willing to consider lien-encumbered properties (often investors or cash buyers) typically demand substantial discounts to compensate for the additional risk and complexity.

Extended marketing time: Properties with liens sit on the market longer as sellers work to resolve issues or search for specialized buyers.

Negotiation leverage: Buyers gain significant leverage when sellers are motivated to close despite lien complications, often resulting in lower offers.

The Lien Payoff Requirement

In most property sales, liens must be paid in full from sale proceeds before the transaction can close. This process works as follows:

- Payoff demand: The seller or closing agent requests payoff amounts from all lienholders

- Closing statement: Sale proceeds are allocated to pay liens in priority order

- Lien release: Lienholders provide satisfaction or release documents

- Recording: Releases are recorded to clear the title

- Remaining proceeds: After liens and closing costs, any remaining funds go to the seller

This seems straightforward, but complications arise when:

- Insufficient equity: The property’s value doesn’t cover all liens and sale costs

- Disputed amounts: Seller contests the lien amount or validity

- Multiple lienholders: Coordinating releases from numerous creditors delays closing

- Priority disputes: Competing claims about which lien gets paid first

Short Sales and Lien Negotiations

When property value falls below total debt (including liens), sellers face a

short sale scenario. This requires negotiating with lienholders to accept less than the full amount owed.

Short sale negotiations with lienholders involve:

Hardship documentation: Demonstrating financial inability to pay liens in full

Comparative market analysis: Proving property value doesn’t support full payoff

Settlement offers: Proposing reduced payoff amounts

Lien priority considerations: Senior lienholders (like first mortgages) typically receive more favorable treatment than junior liens

Not all lienholders agree to short sale terms. Tax authorities, in particular, may refuse to compromise, requiring creative solutions or alternative sale structures.

Properties That Cannot Be Sold

Some lien situations make property sales impossible through traditional means:

- Excessive liens: Total liens exceed property value by substantial margins

- Uncooperative lienholders: Creditors refuse to release liens or negotiate

- Disputed liens: Legal challenges pending that cloud title

- Redemption periods: Properties in tax lien redemption periods face restrictions

Property owners in these situations need expert service from professionals who specialize in complex title issues. Companies like

Sure Path Property Solutions help owners navigate complicated real estate issues—back taxes, multiple heirs, liens, judgments, or unclear title—by coordinating with counties and title professionals to find practical solutions.

Impact on Inherited Property Sales

Heirs who inherit property often discover liens that accumulated during the previous owner’s lifetime. This creates unique challenges:

- Surprise debts: Heirs may be unaware of the deceased’s financial obligations

- Multiple owners: When several heirs inherit together, coordinating lien resolution becomes complex

- Estate complications: Some liens must be addressed through probate proceedings

- Emotional stress: Dealing with liens while grieving adds to family burden

Inherited property with liens requires patient, friendly and caring guidance to help multiple owners understand their options and work together toward resolution.

The Redemption Period: A Critical Window

Many states provide a

redemption period after tax lien sales or foreclosure proceedings during which property owners can reclaim their property by paying the debt plus interest and fees. This period varies significantly by state—from as short as six months to as long as three years.[6]

During the redemption period:

- Property owners retain ownership but face restrictions

- The debt amount increases as interest and fees accumulate

- Sale or refinancing becomes extremely difficult

- Pressure mounts as the redemption deadline approaches

Property owners in redemption periods need to act quickly to explore all options: paying the lien, negotiating payment plans, or finding alternative solutions before the redemption period expires and they lose the property entirely.

Real-World Example: The Compounding Problem

Consider a property owner who fell behind on property taxes by $5,000. The county sold the tax lien to an investor who now charges 18% annual interest. After one year, the debt has grown to $5,900. The property owner also has a $3,000 mechanic’s lien from unpaid roof repairs and a $7,500 judgment lien from a credit card lawsuit.

Total liens: $16,400

If the property is worth $150,000 with a $100,000 mortgage, there’s theoretically enough equity to pay everything. But the owner cannot refinance to access that equity because lenders won’t refinance properties with liens. They cannot sell without paying off all liens first, and they don’t have $16,400 in cash.

This is where trustworthy service from industry experts becomes essential. Professionals can coordinate with lienholders, structure payment plans, or arrange sales that satisfy all parties and help the property owner move forward.

Does a Property Lien Affect Your Credit? Understanding the Credit Impact

One of the most frequently asked questions about liens concerns credit:

does a property lien affect your credit? The answer is nuanced and depends on the type of lien and how credit reporting has evolved.

How Liens Impact Credit Scores

Historically, all liens appeared on credit reports and significantly damaged credit scores. Recent changes have altered this landscape, but liens still affect creditworthiness in important ways.

Tax liens were removed from credit reports by the major credit bureaus (Equifax, Experian, and TransUnion) in 2018 as part of the National Consumer Assistance Plan. This means federal and state tax liens no longer directly appear on credit reports or factor into credit score calculations.[7]

However, this doesn’t mean tax liens have no credit impact:

- Indirect effects: The financial distress that leads to tax liens often coincides with other credit problems

- Public records: Liens remain in public records even if not on credit reports

- Lender checks: Mortgage lenders and some other creditors check public records independently

- Application questions: Loan applications often ask about liens, requiring disclosure

Judgment liens also were removed from credit reports in 2018, eliminating their direct credit score impact. But like tax liens, they remain public records that lenders can discover through title searches and public record checks.

Mechanic’s liens and other specialized liens typically don’t appear on consumer credit reports unless they lead to judgments or collections.

The Broader Credit Implications

Even though liens may not appear on credit reports, they affect creditworthiness in several ways:

Mortgage applications: Lenders conducting title searches for mortgage applications will discover all recorded liens. Properties with liens cannot be used as collateral for new loans until liens are cleared.

Debt-to-income ratio: The underlying debts that led to liens (unpaid taxes, judgments, etc.) represent financial obligations that affect debt-to-income calculations, even if not on credit reports.

Financial instability signals: Liens indicate serious financial problems—inability to pay debts, legal judgments, or tax delinquency. Lenders view these as red flags regardless of credit score impact.

Future borrowing: While a lien may not lower a credit score directly, it prevents using the property as collateral and signals risk to lenders evaluating creditworthiness.

Credit Report vs. Public Records

Understanding the distinction between credit reports and public records is crucial:

| Aspect |

Credit Reports |

Public Records |

| Accessibility |

Available to consumer and creditors with permissible purpose |

Open to public, searchable by anyone |

| Current lien reporting |

Tax and judgment liens no longer included |

All recorded liens appear |

| Credit score impact |

No direct impact from liens (as of 2018) |

No direct impact, but affects lending decisions |

| Duration |

N/A for liens (not reported) |

Liens remain until satisfied and released |

| Lender use |

Primary tool for credit decisions |

Checked for mortgage and major loans |

| Removal |

N/A for liens |

Requires formal lien release and recording |

Repairing Credit After Lien Resolution

Once liens are paid and released, property owners can take steps to rebuild credit:

Obtain lien release documentation: Ensure all releases are properly recorded with the county recorder’s office.

Verify public records: Check that releases appear in public records and title searches.

Address underlying debts: Pay or settle the debts that led to liens in the first place.

Establish positive payment history: Make timely payments on current obligations to rebuild credit.

Monitor credit reports: Ensure no errors appear related to the resolved liens.

Consider credit counseling: Professional guidance can help develop strategies for credit recovery.

The journey from lien problems to restored creditworthiness takes time, but with helpful guidance and consistent effort, property owners can recover their financial standing.

What to Do If a Lien Is Placed on Your Property: Action Steps

Discovering a lien on property can feel overwhelming, but taking prompt, informed action makes a significant difference. Here’s a comprehensive guide on

what to do if a lien is placed on your property.

Step 1: Verify the Lien and Gather Information

Don’t panic—start by confirming the lien’s details:

Obtain official documentation: Request copies of the lien from the county recorder’s office or the entity that filed it.

Verify accuracy: Check that the lien amount, property description, and debtor information are correct. Errors do occur, and incorrect liens can be challenged.

Identify the lienholder: Determine exactly who holds the lien and their contact information.

Review the underlying debt: Examine the original debt that led to the lien—was it a legitimate obligation?

Check recording date: The date the lien was recorded affects its priority and may impact statute of limitations.

Understand deadlines: Determine if there are critical deadlines (like redemption periods or foreclosure timelines) requiring immediate action.

Step 2: Assess Your Financial Situation

Honest evaluation of finances helps determine the best approach:

Calculate total debt: Add up all lien amounts plus any interest, penalties, and fees.

Evaluate property equity: Determine property value minus all liens and mortgages.

Review available resources: Identify cash, savings, or other assets that could pay liens.

Consider income: Can regular income support a payment plan?

Explore borrowing options: Could family loans or other sources provide payoff funds?

Analyze sale scenarios: Would selling the property generate enough to pay all liens and costs?

Step 3: Contact the Lienholder Directly

Communication often opens doors to resolution:

Request payoff amount: Get the exact current payoff figure in writing, including all interest and fees through a specific date.

Explain your situation: Many lienholders will work with property owners who communicate proactively and honestly.

Explore payment plans: Ask about installment agreements or structured payment options.

Negotiate settlements: Some lienholders accept reduced amounts, especially for older debts or when property value is limited.

Get agreements in writing: Any payment plan or settlement must be documented in a formal written agreement.

Request lien release terms: Clarify exactly what must happen for the lien to be released.

Step 4: Consider Dispute or Challenge Options

If a lien is incorrect or invalid, legal remedies exist:

Grounds for challenging liens include:

- Debt was already paid

- Lien amount is incorrect

- Proper procedures weren’t followed when filing the lien

- Statute of limitations has expired

- Lien was filed against wrong property or owner

- Underlying debt is disputed or invalid

Legal challenge process:

- Consult with an attorney specializing in lien law

- File a motion to release or expunge the lien

- Present evidence supporting your challenge

- Attend hearing if required

- Obtain court order releasing the lien if successful

Challenging liens requires legal expertise, but it’s essential when liens are truly invalid.

Step 5: Explore Payment and Resolution Options

Several pathways can lead to lien resolution:

Option A: Pay in Full

The simplest solution—if financially feasible—is paying the lien in full:

- Request payoff statement

- Pay by certified check or wire transfer

- Obtain satisfaction or release document

- Record the release with county recorder

- Verify the release appears in public records

Option B: Negotiate a Payment Plan

Many lienholders offer installment agreements:

- Propose a realistic monthly payment based on your budget

- Get the agreement in writing with clear terms

- Make payments consistently and on time

- Obtain lien release upon completion

- Keep detailed payment records

Option C: Settle for Less

Some lienholders accept reduced payoff amounts:

- Present evidence of financial hardship

- Offer a lump sum that’s less than the full amount

- Negotiate the settlement terms

- Get written agreement before paying

- Ensure agreement includes full lien release

- Pay the agreed amount promptly

- Obtain and record the release

Option D: Sell the Property

If keeping the property isn’t essential or feasible:

- Determine if sale proceeds will cover all liens

- Work with real estate professionals experienced in lien sales

- Coordinate with all lienholders for payoff statements

- Structure closing to pay liens in proper priority order

- Obtain releases at closing

- Accept remaining proceeds (if any) after all debts are paid

Step 6: Seek Professional Help

Complex lien situations benefit from expert service:

Real estate attorneys: Provide legal advice on lien rights, challenges, and resolution strategies.

Tax professionals: Help negotiate with tax authorities and structure payment plans for tax liens.

Real estate specialists: Companies like

Sure Path Property Solutions offer helpful solutions for property owners facing liens, judgments, and title issues. These industry experts coordinate with counties and title professionals to guide owners through complicated situations.

Credit counselors: Assist with overall debt management and financial planning.

Title companies: Help navigate the technical aspects of lien releases and title clearing.

Step 7: Prevent Future Liens

Once liens are resolved, take steps to prevent recurrence:

✅

Pay property taxes on time: Set up automatic payments or escrow accounts

✅

Monitor property tax bills: Verify you receive bills and that amounts are correct

✅

Pay contractors promptly: Don’t give contractors reason to file mechanic’s liens

✅

Address lawsuits quickly: Respond to legal actions to prevent default judgments

✅

Keep financial records: Maintain proof of payments for all property-related obligations

✅

Review title periodically: Check public records annually to catch any issues early

✅

Communicate with creditors: If facing financial difficulty, contact creditors before debts become liens

Special Considerations for Inherited Property

When dealing with liens on inherited property, additional steps apply:

Determine estate responsibility: Some liens may be payable from estate assets through probate.

Coordinate with co-heirs: If multiple people inherited the property, all must agree on resolution approach.

Consider estate claims period: Some liens against the deceased may be subject to estate claims procedures.

Evaluate keeping vs. selling: Heirs should decide together whether to keep the property and pay liens or sell it.

Seek legal guidance: Estate and real estate attorneys can clarify heir responsibilities and options.

Communicate clearly: Multiple owners need friendly and caring guidance to work together effectively.

The Emotional Aspect: Staying Positive

Dealing with liens creates stress, but maintaining an optimistic outlook helps:

💪

Remember liens are solvable: Nearly every lien situation has a resolution path

🤝

You’re not alone: Thousands of property owners face similar challenges and successfully resolve them

📞

Help is available: Professionals with expertise in these exact situations can provide helpful guidance

⏰

Time is on your side: Acting promptly gives you more options and better outcomes

🎯

Focus on solutions: Rather than dwelling on how the lien happened, concentrate on moving forward

The journey from discovering a lien to resolving it may take weeks or months, but with the right approach and expert support, property owners can navigate these challenges and emerge with clear title and renewed financial stability.

Removing a Debt Lien: The Path to Clear Title

The ultimate goal for any property owner facing lien issues is complete removal—achieving clear title that allows unrestricted use, sale, or refinancing of the property. Understanding the lien removal process helps property owners work systematically toward this objective.

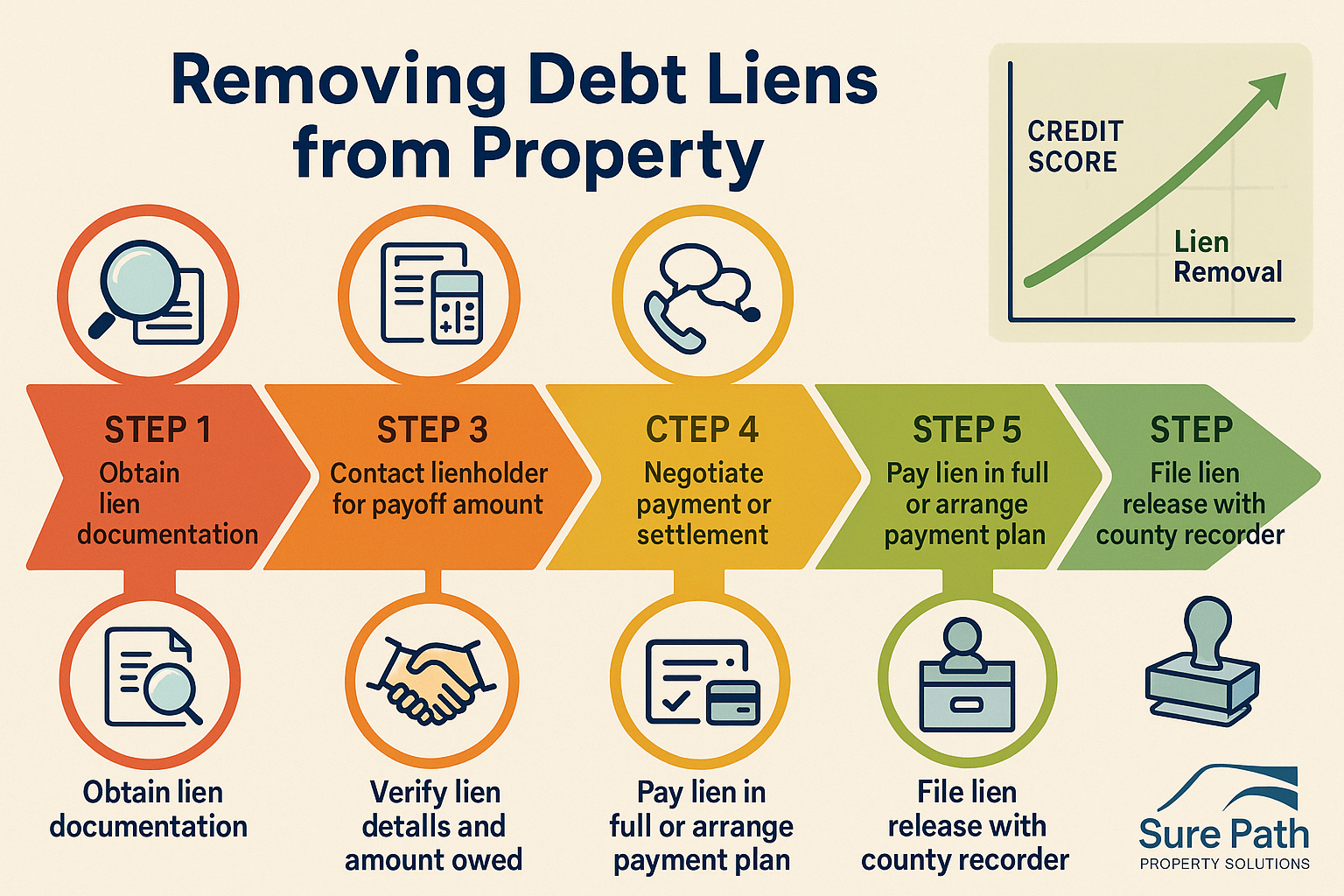

The Lien Release Process

Lien release (also called satisfaction of lien or discharge of lien) is the formal process by which a lienholder acknowledges the debt has been paid and removes their claim on the property.

The standard release process follows these steps:

1. Debt satisfaction: Pay the lien in full, settle for an agreed amount, or fulfill payment plan terms completely.

2. Release document: The lienholder prepares a satisfaction, release, or discharge document. This official form varies by state and lien type but generally includes:

- Property legal description

- Lien recording information (book and page or document number)

- Statement that the debt is satisfied

- Lienholder signature and notarization

- Date of release

3. Recording: The release must be recorded with the same county recorder’s office where the original lien was filed. This creates a public record that the lien has been removed.

4. Verification: After recording, verify that the release appears in property records and title searches show the lien as satisfied.

5. Documentation: Keep copies of the release, recording receipt, and proof of payment permanently with property records.

Timeline for Lien Removal

The time required to remove liens varies significantly:

| Lien Type |

Typical Removal Timeline |

Factors Affecting Timeline |

| Property Tax Lien |

2-8 weeks after payment |

County processing speed, redemption period status |

| Federal Tax Lien |

30-90 days after payment |

IRS processing, certificate of release issuance |

| Judgment Lien |

2-6 weeks after satisfaction |

Court processing, creditor cooperation |

| Mechanic’s Lien |

1-4 weeks after payment |

Contractor responsiveness, recording backlog |

| Mortgage Lien |

At closing (immediate) |

Title company handling, lender release process |

| HOA Lien |

1-3 weeks after payment |

Association processing, management company efficiency |

When Lienholders Don’t Cooperate

Sometimes lienholders fail to provide releases after debts are paid:

Common reasons for delayed releases:

- Administrative oversight or backlog

- Lienholder went out of business

- Lienholder cannot be located

- Dispute over whether debt is fully satisfied

- Simple neglect or poor record-keeping

Solutions for obtaining releases:

Send formal demand: Written request with proof of payment, sent certified mail, demanding release within specific timeframe (typically 30 days).

State statutory remedies: Many states have laws requiring lienholders to release liens within specific periods after payment, with penalties for non-compliance.

Court action: File a motion to release lien, presenting evidence of payment and the lienholder’s failure to release.

Bond substitution: In some cases, posting a bond can remove the lien from the property while disputes are resolved.

Title insurance solutions: Title companies sometimes insure over old liens that can’t be released due to lienholder unavailability, if sufficient evidence of payment exists.

Partial Releases and Subordination

Sometimes full lien removal isn’t immediately possible, but partial solutions help:

Partial release: When property has sufficient value, lienholders may release their claim on a portion of the property while retaining the lien on the remainder. This is common with large parcels being subdivided.

Subordination agreement: The lienholder agrees to move to a lower priority position, allowing refinancing or new loans to take senior position. This doesn’t remove the lien but makes it less obstructive.

Payment from sale proceeds: Lienholders may agree to release their lien upon receiving payment from an upcoming property sale, allowing the transaction to proceed.

Tax Lien Certificates and Redemption

Properties with tax liens sold to investors face a unique removal process:

During redemption period: Property owners can redeem by paying the investor the amount they paid for the lien plus accrued interest and fees. The investor must then release the lien.

Redemption calculation example:

- Investor paid $10,000 for tax lien

- Interest rate: 12% annually

- Time elapsed: 18 months

- Interest: $10,000 × 12% × 1.5 years = $1,800

- Additional fees: $300

- Total redemption amount: $12,100

After redemption period: If the owner doesn’t redeem, the investor may foreclose and take ownership of the property. At this point, redemption is no longer possible.

Expungement and Legal Challenges

When liens are invalid, property owners can seek

expungement—court-ordered removal of the lien:

Grounds for expungement:

- Lien was fraudulently filed

- Debt was never owed

- Lien procedures weren’t properly followed

- Statute of limitations expired before lien was filed

- Debt was discharged in bankruptcy

- Property description is incorrect

Expungement process:

- File petition or motion with appropriate court

- Serve notice on lienholder

- Present evidence supporting expungement

- Attend hearing

- Obtain court order expunging the lien

- Record the court order

- Verify removal from title records

Legal challenges require attorney representation but are essential when liens are truly improper.

The Role of Title Insurance

Title insurance protects property buyers and lenders from undiscovered liens and title defects. When selling property, title insurance plays a crucial role:

Before closing: The title company searches public records to identify all liens, then requires them to be paid or released before issuing a policy.

Title exceptions: If liens can’t be removed, they’re listed as exceptions to coverage—meaning the title insurance won’t cover losses related to those specific liens.

Curative work: Title companies often help coordinate lien releases, contact lienholders, and resolve title issues to “cure” defects and make property insurable.

Owner’s policy: Protects buyers if liens that should have been discovered in the title search later appear.

Lender’s policy: Protects the mortgage lender’s interest, required for virtually all financed purchases.

State-Specific Lien Laws

Lien laws vary significantly by state, affecting removal processes:

California: Tax sale deeds convey title free of all encumbrances existing before the sale, with limited exceptions for specific liens and assessments.[8] This means tax foreclosure effectively wipes out junior liens.

New York: Provides extensive redemption rights, with foreclosure proceedings taking 1-3 years, giving property owners substantial time to resolve liens.[9]

Texas: Offers relatively short redemption periods (typically 6 months to 2 years) but provides homestead protections that limit some types of liens.

Florida: Has specific procedures for homestead property that restrict certain liens and provide additional protections.

Property owners should consult local real estate attorneys familiar with their state’s lien laws to understand specific rights and procedures.

Working with Property Solutions Experts

Complex lien situations benefit enormously from professional assistance.

Sure Path Property Solutions specializes in helping property owners navigate complicated scenarios involving:

- Multiple liens from different creditors

- Back taxes and tax lien sales

- Properties with unclear title

- Inherited property with lien issues

- Situations involving multiple heirs or owners

- Judgments and legal claims

These industry experts provide:

✨

Comprehensive lien research: Identifying all claims against property

✨

Coordination services: Working with counties, title companies, and creditors

✨

Negotiation assistance: Helping structure payment plans or settlements

✨

Transaction facilitation: Guiding sales that satisfy all lienholders

✨

Clear communication: Explaining complex situations in understandable terms

✨

Practical solutions: Finding workable paths forward even in difficult circumstances

The combination of expert knowledge and friendly, caring service helps property owners move from overwhelming lien problems to clear title and fresh starts.

After Lien Removal: Protecting Your Property

Once liens are successfully removed, take steps to protect your property going forward:

🛡️

Maintain good records: Keep all lien release documents, proof of payment, and title reports permanently

🛡️

Monitor property records: Periodically check public records to ensure no new liens appear

🛡️

Stay current on obligations: Pay property taxes, HOA dues, and other property-related debts on time

🛡️

Review title before major transactions: Before selling or refinancing, run a preliminary title search to identify any issues early

🛡️

Consider title insurance: When purchasing property, always obtain owner’s title insurance for protection

🛡️

Address problems promptly: If financial difficulties arise, communicate with creditors before debts become liens

🛡️

Seek help early: If problems develop, contact professionals before situations become critical

Clear title represents financial freedom and peace of mind. The effort invested in removing liens pays dividends in restored property rights and renewed opportunities.

Conclusion: Moving Forward with Confidence

Understanding

debt liens explained: what they are and how they affect property sales empowers property owners to face these challenges with knowledge and confidence rather than fear and confusion. While liens create serious complications, they’re not insurmountable obstacles.

The key takeaways for property owners facing lien issues:

Knowledge is power: Understanding lien types, priorities, and resolution processes enables informed decision-making.

Action beats inaction: Ignoring liens makes situations worse as interest, fees, and penalties accumulate. Prompt action preserves options and opportunities.

Communication opens doors: Many lienholders will work with property owners who reach out proactively and honestly.

Professional help matters: Complex lien situations benefit from expert guidance from attorneys, tax professionals, and real estate specialists.

Solutions exist: Nearly every lien situation has a resolution path, whether through payment, negotiation, legal challenge, or structured sale.

Time and patience pay off: Resolving liens may take weeks or months, but persistence leads to clear title and renewed financial freedom.

For property owners struggling with liens, judgments, back taxes, or unclear title, remember that helpful solutions are available. Companies like

Sure Path Property Solutions provide the trustworthy service and expert guidance needed to navigate these complicated situations. By coordinating with counties, title professionals, and creditors, these industry experts help property owners find practical paths forward.

Your Next Steps

If liens are affecting your property, take these actions today:

- Gather information: Obtain copies of all liens from the county recorder’s office

- Verify details: Check that lien amounts and information are accurate

- Assess your situation: Evaluate property value, equity, and financial resources

- Contact lienholders: Request payoff amounts and explore payment options

- Seek professional guidance: Consult with real estate attorneys or property solution specialists

- Develop a plan: Create a realistic strategy for resolving liens based on your specific circumstances

- Take action: Begin implementing your plan, whether through payment, negotiation, or sale

- Stay persistent: Follow through until liens are fully released and title is clear

The journey from lien problems to clear title requires patience, but the destination—property free from legal claims and restrictions—is worth the effort. With the right approach, helpful guidance from caring professionals, and commitment to resolution, property owners can overcome lien challenges and move forward with optimism toward their real estate goals.

Whether planning to sell, refinance, pass property to heirs, or simply secure peace of mind, resolving liens clears the path to achieving those objectives. The time to start is now—every day of delay adds interest and fees while limiting options. But every step toward resolution brings you closer to the financial freedom and security that clear property title provides.

References

[1] Cornell Law School, Legal Information Institute. “Lien.” Available at:

https://www.law.cornell.edu/wex/lien

[2] Internal Revenue Service. “Understanding a Federal Tax Lien.” IRS Publication 1468. Available at:

https://www.irs.gov/businesses/small-businesses-self-employed/understanding-a-federal-tax-lien

[3] National Tax Lien Association. “Tax Lien Investing Basics.” Available at:

https://www.ntla.org/

[4] New York City Department of Finance. “Lien Sale Information.” 2025. Available at:

https://www.nyc.gov/site/finance/taxes/lien-sale.page

[5] American Bar Association. “Mechanic’s Liens: What Property Owners Need to Know.” Real Property, Trust and Estate Law Section.

[6] National Association of Counties. “Property Tax Collection and Tax Lien Sales.” Research report, 2024.

[7] Consumer Financial Protection Bureau. “Changes to Public Records on Credit Reports.” Available at:

https://www.consumerfinance.gov/

[8] California Revenue and Taxation Code Section 3712. “Effect of Tax Deed.”

[9] New York Real Property Tax Law Article 11. “Enforcement of Collection of Delinquent Taxes.”