Facing foreclosure can feel overwhelming. The stress of mounting mortgage payments, threatening letters from lenders, and the fear of losing your home creates an emotional and financial burden that keeps many homeowners awake at night. But what if there was a way to avoid the public embarrassment and legal complications of foreclosure while still resolving your mortgage debt?

A deed in lieu of foreclosure offers exactly that solution. This comprehensive guide on the Deed in Lieu of Foreclosure: Complete Guide, Process & Requirements will walk you through everything you need to know about this foreclosure alternative, from understanding the basic concept to navigating the qualification requirements and completing the process successfully.

Key Takeaways

- ✅ A deed in lieu of foreclosure allows homeowners to voluntarily transfer property ownership to their lender to satisfy mortgage debt and avoid formal foreclosure proceedings

- ✅ The process requires demonstrating financial hardship, attempting other alternatives first, and ensuring the property is free of additional liens before lender approval

- ✅ While credit impact is significant (85-160 point drop), it’s typically less severe than foreclosure and allows homeowners to avoid public foreclosure records

- ✅ The timeline ranges from 90-120 days, including lien release negotiations and financial documentation review

- ✅ Lenders may offer cash-for-keys assistance and relocation time, making the transition more manageable for struggling homeowners

What Is a Deed in Lieu of Foreclosure?

A deed in lieu of foreclosure is a legal agreement where a borrower voluntarily transfers property ownership to their mortgage lender to satisfy outstanding debt and avoid formal foreclosure proceedings.[1]

Think of it as a mutual exit strategy. Instead of going through the lengthy, expensive, and public foreclosure process, both parties agree to a simpler solution. The homeowner hands over the property deed, and in return, the lender cancels the remaining mortgage debt.

How It Works in Practice

When homeowners can no longer afford their mortgage payments, they typically have several options. A deed in lieu represents a middle ground between continuing to struggle with payments and facing a forced foreclosure sale.

Here’s the basic framework:

The homeowner contacts their lender and requests consideration for a deed in lieu arrangement. This signals their willingness to cooperate rather than fight the inevitable.

The lender evaluates the request based on specific criteria, including the property’s condition, market value, and whether any additional liens exist.

Both parties negotiate terms, which may include relocation assistance, timeline for vacating the property, and release from deficiency judgments.

The property title transfers to the lender once all conditions are met and documentation is complete.

Why Lenders Consider This Option

Lenders don’t automatically approve deed in lieu requests. However, they often prefer this option because it:

- Reduces legal costs associated with foreclosure proceedings

- Speeds up the timeline to take possession of the property

- Minimizes property deterioration that often occurs during lengthy foreclosures

- Avoids negative publicity and community relations issues

For homeowners, this option provides helpful solutions to an otherwise devastating situation, allowing them to exit with dignity while minimizing long-term financial damage.

The Legal Framework

A deed in lieu is a binding legal contract governed by state real estate laws. The agreement must be executed properly with:

- Written documentation signed by both parties

- Proper notarization and recording with county offices

- Clear title transfer without encumbrances

- Release of mortgage lien upon completion

This legal protection ensures both parties fulfill their obligations and provides a clear path forward for everyone involved.

Deed in Lieu Process & Timeline: Complete Guide, Process & Requirements

Understanding the deed in lieu process helps homeowners prepare properly and set realistic expectations. The timeline typically spans 90-120 days from initial contact to final property transfer.[2]

Step 1: Initial Contact and Request (Week 1-2)

The process begins when the homeowner contacts their mortgage servicer’s loss mitigation department. This conversation should happen before missing multiple payments, ideally when financial hardship first becomes apparent.

During this initial contact:

📞 Request information about foreclosure alternatives

📞 Ask specifically about deed in lieu eligibility

📞 Document the name and contact information of your assigned representative

📞 Request a list of required documentation

Pro tip: Keep detailed records of every conversation, including dates, times, names, and discussion points. This documentation proves invaluable if disputes arise later.

Step 2: Financial Documentation Submission (Week 2-4)

Lenders require comprehensive financial documentation to verify hardship and evaluate the request. Homeowners must gather and submit:

Income verification:

- Recent pay stubs (typically last 2-3 months)

- Tax returns (previous 2 years)

- Profit and loss statements for self-employed borrowers

- Social Security or disability income documentation

Asset documentation:

- Bank statements (last 2-3 months for all accounts)

- Investment account statements

- Retirement account balances

- Vehicle titles and valuations

Expense verification:

- Utility bills

- Medical expenses

- Insurance payments

- Child care costs

- Other monthly obligations

Hardship letter:

A detailed explanation of circumstances causing the inability to maintain mortgage payments. Common qualifying hardships include job loss, medical emergencies, divorce, or business failure.

Step 3: Property Evaluation (Week 4-6)

The lender orders a Broker Price Opinion (BPO) or full appraisal to determine the property’s current market value. This evaluation is critical because lenders only approve deed in lieu requests when the property value approximates or exceeds the outstanding loan balance.

During this phase, the lender also:

- Conducts a title search to identify any additional liens

- Inspects the property condition

- Assesses environmental concerns

- Reviews local market conditions

Homeowners should maintain the property in reasonable condition during this evaluation period. Significant damage or neglect can result in request denial.

Step 4: Lien Resolution (Week 6-16)

This step often represents the most time-consuming part of the process. If second mortgages, home equity lines of credit (HELOCs), tax liens, or judgment liens exist, those lien holders must provide written approval through a Second-Lien Release.[3]

The subordinate lien holder process typically requires:

⏱️ 30-90 days for negotiation and approval

⏱️ Written agreements from all parties

⏱️ Potential settlement payments to junior lien holders

⏱️ Legal documentation releasing their claims

Without these releases, the deed in lieu cannot proceed. The property title must transfer to the lender completely free of encumbrances.

Step 5: Agreement Execution (Week 16-18)

Once the lender approves the request and all liens are resolved, both parties execute the formal deed in lieu agreement. This legal document specifies:

- Property transfer date

- Relocation timeline (typically 30 days)

- Cash-for-keys stipend amount (if applicable)

- Deficiency waiver or remaining liability

- Property condition requirements

- Keys and access surrender procedures

Industry experts recommend having a real estate attorney review this agreement before signing to ensure all terms are clearly understood and protect the homeowner’s interests.

Step 6: Property Vacating and Transfer (Week 18-20)

Homeowners typically have up to 30 calendar days to relocate from the property, depending on local laws and loan type.[4] During this period:

✅ Remove all personal belongings

✅ Complete any agreed-upon repairs or cleaning

✅ Arrange for utility disconnection

✅ Forward mail to new address

✅ Conduct final walk-through with lender representative

Step 7: Final Recording and Release (Week 20-22)

The lender records the deed transfer with the county recorder’s office, officially transferring ownership. The mortgage lien is released, and the borrower receives documentation confirming:

- Mortgage satisfaction

- Release from further payment obligations (if deficiency is waived)

- Property transfer completion

- Final account status

This marks the official conclusion of the deed in lieu process.

Timeline Comparison Table

| Process Stage | Timeframe | Key Activities |

|---|---|---|

| Initial Contact | Week 1-2 | Request submission, representative assignment |

| Documentation | Week 2-4 | Financial documents, hardship letter |

| Property Evaluation | Week 4-6 | BPO/appraisal, title search, inspection |

| Lien Resolution | Week 6-16 | Second-lien releases, subordinate negotiations |

| Agreement Execution | Week 16-18 | Contract signing, terms finalization |

| Relocation | Week 18-20 | Moving, property preparation |

| Final Transfer | Week 20-22 | Recording, lien release, completion |

Qualification Requirements for Deed in Lieu of Foreclosure

Not every homeowner qualifies for a deed in lieu arrangement. Lenders maintain specific eligibility criteria that must be met before they’ll consider this option. Understanding these requirements helps homeowners determine if this path makes sense for their situation.

Primary Qualification Criteria

1. Demonstrated Financial Hardship

Borrowers must prove they cannot afford current mortgage payments due to legitimate financial hardship. Acceptable hardships include:

💼 Job loss or income reduction – Layoffs, business closures, reduced hours

🏥 Medical emergencies – Serious illness, disability, catastrophic medical bills

💔 Divorce or separation – Loss of dual income, legal expenses

📉 Business failure – Self-employment income loss, bankruptcy

🏠 Property issues – Uninsurable damage, environmental hazards

Simply wanting to walk away from an underwater mortgage doesn’t constitute qualifying hardship. Lenders require evidence that circumstances beyond the borrower’s control created the financial crisis.

2. Ineligibility for Loan Modification

Before approving a deed in lieu, lenders require proof that the borrower doesn’t qualify for loan modification programs. This demonstrates that keeping the home isn’t financially viable even with adjusted terms.

Homeowners must typically apply for and be denied:

- Interest rate reductions

- Term extensions

- Principal forbearance

- Payment deferrals

This requirement ensures deed in lieu serves as a last resort rather than a first choice.

3. Unsuccessful Short Sale Attempts

Most lenders require homeowners to attempt selling the property through a short sale before considering deed in lieu.[5] This typically means:

- Listing the property with a licensed real estate agent

- Marketing for 60-90 days minimum

- Demonstrating no qualified offers were received

- Providing documentation of marketing efforts

The logic is simple: if the property can sell and satisfy most or all of the debt, that outcome benefits both parties more than deed in lieu.

4. Property Free of Additional Liens

The property must be free of any liens beyond the primary mortgage before title can transfer to the lender. This includes:

🚫 Second mortgages

🚫 Home equity loans or lines of credit

🚫 Tax liens (federal, state, or local)

🚫 Mechanic’s liens

🚫 Judgment liens

🚫 HOA liens

If subordinate liens exist, those lien holders must provide written approval through a Second-Lien Release. This process typically takes approximately 90 calendar days and requires negotiation with each lien holder.[6]

5. Property Condition Standards

Lenders expect the property to be in reasonable, marketable condition. They typically won’t accept deed in lieu if:

- Significant structural damage exists

- Environmental hazards are present (mold, asbestos, contamination)

- The property has been vandalized or stripped

- Major code violations exist

- The property is uninhabitable

Think of it this way: the lender is accepting property instead of cash payment. They won’t accept a property they can’t reasonably resell.

Additional Considerations

Occupancy Status

Most lenders prefer (and some require) that the property be owner-occupied rather than investment property. This ensures the program helps homeowners facing genuine hardship rather than investors seeking to offload bad investments.

Loan Status

While some lenders consider deed in lieu requests before default, most require the borrower to be:

- Currently delinquent on payments, OR

- Facing imminent default within 30-60 days

Being current on payments often disqualifies borrowers because it suggests they can afford the mortgage.

Lender-Specific Requirements

Each lender maintains unique eligibility criteria beyond these standard requirements. Government-backed loans (FHA, VA, USDA) have additional federal guidelines that must be followed.

Trustworthy service from experienced professionals can help navigate these lender-specific requirements and improve approval chances.

Why Lenders Deny Requests

Understanding common denial reasons helps homeowners prepare stronger applications:

❌ Property value significantly below loan balance – Creates excessive deficiency

❌ Unresolved subordinate liens – Title can’t transfer cleanly

❌ Insufficient hardship documentation – Can’t verify financial need

❌ Property condition issues – Not marketable in current state

❌ Borrower has significant liquid assets – Could continue making payments

❌ Fraud or misrepresentation – Dishonesty in application process

Short Sale vs Foreclosure vs Deed in Lieu: Comprehensive Comparison

Understanding the differences between foreclosure alternatives helps homeowners choose the best option for their specific circumstances. Each path has distinct advantages, disadvantages, and consequences.

Detailed Comparison Table

| Factor | Deed in Lieu | Short Sale | Foreclosure | Loan Modification |

|---|---|---|---|---|

| Timeline | 90-120 days | 120-180 days | 180-360+ days | 30-90 days |

| Credit Impact | 85-160 point drop | 85-160 point drop | 200-250+ point drop | Minimal if approved |

| Public Record | No | No | Yes | No |

| Deficiency Judgment | Often waived | Varies by state | Likely | N/A |

| Relocation Assistance | Often $2,000-$5,000 | Sometimes $3,000-$10,000 | Rarely | N/A (keep home) |

| Control Over Process | Moderate | High | None | High |

| Tax Consequences | Possible forgiven debt | Possible forgiven debt | Likely forgiven debt | None |

| Future Mortgage Eligibility | 2-4 years | 2-4 years | 5-7 years | Immediate |

| Lender Cooperation Required | Yes | Yes | No | Yes |

| Property Must Sell | No | Yes | Yes (at auction) | No |

Short Sale vs Deed in Lieu: Direct Comparison

These two options are often confused because both avoid formal foreclosure. However, they differ significantly in execution and outcomes.

Short Sale Characteristics:

✅ Property actively marketed and sold to third-party buyer

✅ Homeowner retains some control over buyer selection

✅ Potentially higher relocation assistance

✅ Longer timeline due to marketing period

✅ Requires active real estate market participation

✅ May yield better outcome if property sells near market value

Deed in Lieu Characteristics:

✅ Direct transfer to lender without marketing

✅ Faster resolution timeline

✅ Less uncertainty about outcome

✅ No showings, open houses, or buyer negotiations

✅ Simpler process with fewer parties involved

✅ Better option when property won’t sell quickly

When to Choose Each Option

Choose Short Sale if:

- The property has marketable value and equity

- Local real estate market is active

- Time isn’t critically urgent

- Maximizing relocation assistance is priority

- Comfortable with showings and marketing process

Choose Deed in Lieu if:

- Property has been unsuccessfully listed

- Need faster resolution

- Property condition makes sale difficult

- Prefer simplified process with fewer parties

- Lender offers favorable deficiency waiver

Choose Loan Modification if:

- Want to keep the home

- Hardship is temporary

- Income can support modified payment

- Qualify under lender programs

Accept Foreclosure only if:

- All other options have been exhausted or denied

- Strategic default is intentional

- Bankruptcy is concurrent strategy

- No other viable alternatives exist

Credit Impact Comparison

The credit consequences of each option vary significantly:

Deed in Lieu: Credit scores typically drop 85-160 points and remain on credit report for 7 years. However, the notation is less severe than foreclosure, and recovery is faster.[7]

Short Sale: Similar impact to deed in lieu, with 85-160 point drop for 7 years. Some lenders view short sales slightly more favorably than deed in lieu.

Foreclosure: Most severe impact with 200-250+ point drop for 7 years. The “foreclosure” notation carries significant stigma with future lenders.

Loan Modification: Minimal credit impact if approved and payments remain current. May show as “partial payment” or “settlement” but far less damaging.

Future Mortgage Eligibility

Government-backed loan programs impose waiting periods after foreclosure alternatives:

Conventional Loans (Fannie Mae/Freddie Mac):

- Foreclosure: 7 years

- Deed in Lieu: 4 years

- Short Sale: 2-4 years (depending on circumstances)

FHA Loans:

- Foreclosure: 3 years

- Deed in Lieu: 3 years

- Short Sale: 3 years

VA Loans:

- Foreclosure: 2 years

- Deed in Lieu: 2 years

- Short Sale: 2 years

These timelines can be reduced with extenuating circumstances documentation and larger down payments.

Pros and Cons of Deed in Lieu of Foreclosure

Like any financial decision, deed in lieu arrangements come with both advantages and disadvantages. Understanding both sides helps homeowners make informed choices.

Advantages of Deed in Lieu

✅ Avoids Public Foreclosure Record

Unlike formal foreclosure, deed in lieu doesn’t create a public court record. This privacy protects homeowners from:

- Neighborhood embarrassment

- Employment background check issues

- Public auction announcements

- Court proceedings and appearances

For many homeowners, this dignity preservation is invaluable during an already difficult time.

✅ Reduced Legal Costs

Foreclosure proceedings involve substantial legal fees for both parties. Deed in lieu eliminates:

- Attorney fees for foreclosure defense

- Court filing fees

- Process server costs

- Potential judgment collection expenses

These savings benefit both homeowner and lender, making cooperation more attractive.

✅ Faster Resolution Timeline

While 90-120 days may seem long, it’s significantly shorter than the 180-360+ days typical foreclosure requires. This faster timeline means:

- Less time in financial limbo

- Quicker credit recovery start

- Reduced stress and uncertainty

- Faster path to housing stability

✅ Potential Relocation Assistance

Many lenders offer cash-for-keys stipends ranging from $2,000-$5,000 to help cover moving and relocation expenses.[8] This financial assistance helps homeowners:

- Secure new housing (deposits, first month’s rent)

- Cover moving costs

- Bridge temporary financial gaps

- Start fresh with some financial cushion

This helpful guidance through the transition makes the process more manageable.

✅ Possible Deficiency Waiver

While not guaranteed, many deed in lieu agreements include deficiency waivers, releasing borrowers from the difference between property value and loan balance. This protection prevents:

- Future collection actions

- Wage garnishment

- Bank account levies

- Additional credit damage

✅ Less Severe Credit Impact

Compared to foreclosure’s 200-250+ point drop, deed in lieu’s 85-160 point impact is significantly less damaging. Credit recovery also occurs faster, with many homeowners qualifying for new mortgages in 2-4 years versus 5-7 years post-foreclosure.

✅ Cooperative Rather Than Adversarial

The deed in lieu process emphasizes cooperation between borrower and lender. This friendly and caring approach creates:

- Better communication

- Mutual understanding

- Reduced stress

- Dignified exit strategy

Disadvantages of Deed in Lieu

❌ Not Guaranteed

Lender approval isn’t automatic. Many requests are denied due to:

- Subordinate liens

- Property condition issues

- Insufficient hardship documentation

- Property value below loan balance

- Lender policy restrictions

This uncertainty means homeowners can’t rely on deed in lieu as definite solution.

❌ Requires Lender Cooperation

Unlike foreclosure (which happens whether borrowers cooperate or not), deed in lieu requires active lender participation. If the lender:

- Doesn’t offer the program

- Has restrictive eligibility criteria

- Prefers foreclosure for policy reasons

- Won’t negotiate favorable terms

…the option simply isn’t available.

❌ Subordinate Lien Complications

Properties with second mortgages, HELOCs, or other liens face significant challenges. The 90-day second-lien release process often fails because:

- Junior lien holders refuse to release claims

- Settlement amounts can’t be negotiated

- Multiple lien holders create complexity

- Lien holders pursue separate collection actions

❌ Potential Tax Consequences

Forgiven mortgage debt may be considered taxable income by the IRS. While the Mortgage Forgiveness Debt Relief Act provided temporary protection, homeowners may face:

- 1099-C forms reporting forgiven debt

- Tax liability on phantom income

- Need for insolvency documentation

- Complicated tax filing requirements

Consulting a tax professional is essential to understand potential consequences.

❌ Possible Deficiency Liability

Not all deed in lieu agreements include deficiency waivers. Borrowers may remain responsible for the difference between property value and loan balance, potentially facing:

- Collection actions

- Credit damage

- Wage garnishment

- Bank levies

Always ensure the agreement explicitly waives deficiency before signing.

❌ Loss of Property Equity

Any equity in the property transfers to the lender without compensation to the homeowner. If the property has value above the mortgage balance, short sale might yield better financial outcome.

❌ Credit Damage Still Significant

While less severe than foreclosure, the 85-160 point credit drop still creates substantial challenges:

- Difficulty obtaining new credit

- Higher interest rates on future loans

- Potential employment issues (credit-sensitive positions)

- Insurance rate increases

- Security deposit requirements for utilities and rentals

Decision-Making Framework

Consider deed in lieu when:

✔️ Financial hardship is genuine and documented

✔️ Property won’t sell through short sale

✔️ No subordinate liens exist (or can be resolved)

✔️ Lender offers favorable terms with deficiency waiver

✔️ Faster resolution is priority

✔️ Avoiding public foreclosure record is important

Explore alternatives when:

✖️ Property has significant equity

✖️ Multiple liens complicate title transfer

✖️ Lender won’t waive deficiency

✖️ Loan modification might be viable

✖️ Property could sell through short sale

Other Foreclosure Alternatives: Complete Options Guide

Deed in lieu represents just one of several foreclosure alternatives available to struggling homeowners. Understanding all options ensures the best choice for individual circumstances.

1. Loan Modification

What it is: Permanent change to original loan terms to make payments more affordable.

How it works:

Lenders modify one or more loan terms, including:

- Reducing interest rate

- Extending loan term (e.g., 30 to 40 years)

- Converting adjustable rate to fixed rate

- Forbearing or forgiving principal balance

- Capitalizing past-due amounts into new loan

Best for:

- Homeowners who want to keep their home

- Those with temporary hardship now resolved

- Borrowers with income to support modified payment

- Properties with equity or near break-even value

Pros:

✅ Keep the home

✅ Minimal credit impact if approved

✅ Permanent solution

✅ Immediate mortgage eligibility after modification

Cons:

❌ Strict qualification requirements

❌ Lengthy application process

❌ Not guaranteed approval

❌ May extend total interest paid

2. Forbearance Agreement

What it is: Temporary pause or reduction of mortgage payments while borrower recovers financially.

How it works:

Lender agrees to suspend or reduce payments for 3-12 months, with repayment plan for missed amounts through:

- Lump sum payment after forbearance

- Extended repayment period

- Modified loan incorporating missed payments

- Partial claim (government-backed loans)

Best for:

- Temporary hardships (medical leave, short-term job loss)

- Borrowers expecting income recovery

- Those needing breathing room to explore options

- COVID-19 or disaster-related hardships

Pros:

✅ Immediate payment relief

✅ Prevents foreclosure during hardship

✅ Relatively easy to obtain

✅ Minimal credit impact if properly structured

Cons:

❌ Temporary solution only

❌ Missed payments must be repaid

❌ May create large balloon payment

❌ Doesn’t solve long-term affordability issues

3. Short Sale

What it is: Sale of property for less than outstanding mortgage balance with lender approval.

How it works:

- Homeowner lists property with real estate agent

- Buyer makes offer below loan balance

- Lender reviews and approves short sale

- Sale proceeds satisfy (or partially satisfy) debt

- Lender releases lien and may waive deficiency

Best for:

- Properties with some marketable value

- Active real estate markets

- Homeowners comfortable with sale process

- Those wanting to maximize relocation assistance

Pros:

✅ Potentially higher relocation assistance ($3,000-$10,000)

✅ Some control over buyer selection

✅ May preserve more credit than foreclosure

✅ Avoids public foreclosure record

Cons:

❌ Lengthy process (120-180 days)

❌ No guarantee property will sell

❌ Requires active market participation

❌ Deficiency not always waived

❌ Tax consequences on forgiven debt

4. Cash-for-Keys Program

What it is: Lender incentive program offering cash payment for voluntary, timely property vacation.

How it works:

Lender offers $1,000-$5,000+ to borrowers who:

- Vacate property by agreed date

- Leave property in good condition

- Turn over all keys and access

- Complete property in “broom clean” condition

- Sign agreement releasing all claims

Best for:

- Borrowers accepting foreclosure is inevitable

- Those needing relocation funds

- Homeowners willing to cooperate with lender

- Situations where other alternatives failed

Pros:

✅ Cash assistance for moving expenses

✅ Dignified exit with cooperation

✅ Avoids eviction proceedings

✅ May negotiate extended timeline

✅ Lender covers some transition costs

Cons:

❌ Still results in foreclosure

❌ Doesn’t avoid credit damage

❌ Payment amounts vary widely

❌ Must fully vacate and surrender property

❌ No guarantee of offer

5. Refinance

What it is: Replacing existing mortgage with new loan at better terms.

How it works:

Borrower applies for new mortgage to pay off existing loan, potentially:

- Lowering interest rate

- Reducing monthly payment

- Changing loan term

- Accessing equity (cash-out refinance)

- Removing mortgage insurance

Best for:

- Borrowers with improved credit since original loan

- Those with significant equity

- Current on mortgage payments

- Improved income or debt-to-income ratio

- Interest rates lower than original loan

Pros:

✅ Lower monthly payments

✅ No credit damage

✅ Keep the home

✅ Potential cash out for other debts

Cons:

❌ Requires good credit and income

❌ Closing costs ($2,000-$5,000+)

❌ Must qualify under current lending standards

❌ Property must appraise adequately

❌ Not available if already delinquent

6. Bankruptcy

What it is: Legal proceeding providing debt relief and potential foreclosure delay.

How it works:

Chapter 7: Liquidation bankruptcy discharges unsecured debts but doesn’t prevent foreclosure unless combined with other strategies.

Chapter 13: Reorganization bankruptcy creates 3-5 year repayment plan, allowing borrowers to:

- Catch up on missed payments over time

- Keep the home while repaying arrears

- Strip second mortgages (if underwater)

- Delay foreclosure proceedings

Best for:

- Overwhelming unsecured debt alongside mortgage issues

- Homeowners needing time to catch up on arrears

- Those with regular income to support repayment plan

- Properties with second mortgages to strip

Pros:

✅ Immediate automatic stay stops foreclosure

✅ Discharges other debts, freeing income for mortgage

✅ Structured repayment plan

✅ May strip junior liens

Cons:

❌ Severe credit damage (220-240 point drop)

❌ Remains on credit report 7-10 years

❌ Legal fees ($1,500-$3,500+)

❌ Complex legal process

❌ Not all debts dischargeable

❌ Strict budget requirements

7. Sell the Property (Traditional Sale)

What it is: Standard real estate sale at market value to pay off mortgage.

How it works:

List property with real estate agent, sell at market price, use proceeds to:

- Pay off entire mortgage balance

- Cover selling costs (commissions, closing costs)

- Keep any remaining equity

Best for:

- Properties with equity

- Borrowers still current on payments

- Strong real estate markets

- Those wanting to preserve credit

- Homeowners with time for traditional sale process

Pros:

✅ No credit damage

✅ Keep any equity

✅ Clean break from mortgage

✅ No foreclosure or alternative needed

Cons:

❌ Requires property equity

❌ 60-90+ day process

❌ Selling costs (6-10% of sale price)

❌ Must continue mortgage payments during sale

❌ No guarantee of sale

8. Rental Strategy

What it is: Converting primary residence to rental property to generate income covering mortgage.

How it works:

Homeowner relocates to more affordable housing and rents current property to tenants, using rental income to:

- Cover mortgage payment

- Pay property taxes and insurance

- Build equity while market recovers

- Potentially sell later when values improve

Best for:

- Properties in strong rental markets

- Homeowners with property management skills

- Those able to relocate to cheaper housing

- Properties near break-even or positive cash flow

Pros:

✅ Preserve property ownership

✅ Build equity over time

✅ Potential appreciation gains

✅ Tax benefits of rental property

✅ No credit damage

Cons:

❌ Landlord responsibilities and risks

❌ Requires property management

❌ Vacancy and maintenance costs

❌ May violate owner-occupancy loan terms

❌ Rental income may not cover all costs

Decision Tree: Choosing the Right Foreclosure Alternative

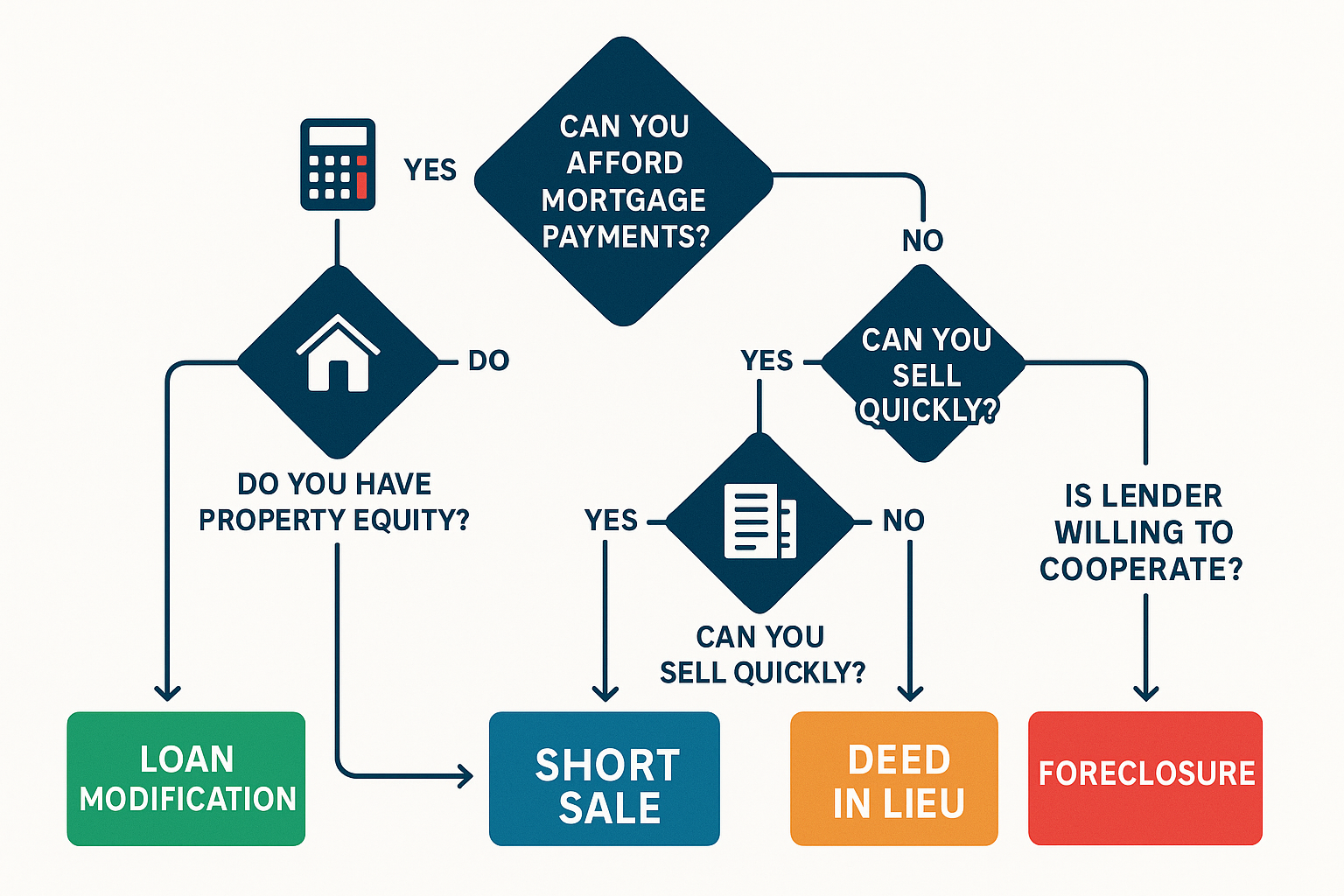

Navigating foreclosure alternatives can feel overwhelming. This decision framework helps homeowners identify the best option based on their specific circumstances.

Start Here: Can You Afford Current Mortgage Payments?

YES → You likely don’t need foreclosure alternatives. Consider:

- Refinancing for better terms

- Continuing current mortgage

- Paying down principal faster

NO → Continue to next question

Is Your Financial Hardship Temporary or Permanent?

TEMPORARY (job loss with new employment pending, short-term medical issue, temporary income reduction):

- Best Option: Forbearance Agreement

- Alternative: Loan Modification

PERMANENT (permanent disability, long-term unemployment, business closure):

- Continue to next question

Do You Want to Keep Your Home?

YES → Consider:

- Loan Modification (if income supports modified payment)

- Chapter 13 Bankruptcy (if overwhelming other debts exist)

- Refinance (if credit and equity permit)

NO → Continue to next question

Does Your Property Have Equity?

YES (property value exceeds mortgage balance):

- Best Option: Traditional Sale

- Keep equity and preserve credit

NO (underwater or break-even):

- Continue to next question

Can Your Property Sell Within 90-120 Days?

YES (active market, good condition, marketable property):

- Best Option: Short Sale

- Potentially higher relocation assistance

- More control over process

NO (slow market, condition issues, previous listing failed):

- Continue to next question

Are There Second Mortgages or Other Liens on the Property?

YES (HELOC, second mortgage, tax liens, judgment liens):

- Best Option: Short Sale (liens resolved through sale proceeds)

- Alternative: Bankruptcy (may strip junior liens)

- Challenge: Deed in Lieu (requires 90-day lien release process)

NO (only first mortgage):

- Continue to next question

Will Your Lender Approve Deed in Lieu?

YES (lender offers program, you meet qualifications, property condition acceptable):

- Best Option: Deed in Lieu of Foreclosure

- Faster than short sale

- Simpler process

- Potential cash-for-keys assistance

NO (lender denies request or doesn’t offer program):

- Remaining Options:

- Cash-for-Keys Program

- Strategic Foreclosure

- Bankruptcy

Special Considerations

If you have significant unsecured debt (credit cards, medical bills, personal loans):

- Consider: Bankruptcy alongside foreclosure alternative

- Discharging other debts may free income for housing

If you’re facing immediate foreclosure sale (auction date scheduled):

- Urgent Options: Bankruptcy (automatic stay), emergency loan modification, cash-for-keys

- Time is critical—seek expert service immediately

If you have multiple properties:

- Strategic decisions differ

- Consider which properties to preserve

- Consult with real estate attorney

Working with Professionals: When to Seek Expert Help

Navigating the Deed in Lieu of Foreclosure: Complete Guide, Process & Requirements is complex. While some homeowners successfully manage the process independently, professional guidance often improves outcomes significantly.

Real Estate Attorneys

When to hire:

- Complex lien situations involving multiple creditors

- Deficiency judgment concerns

- Reviewing deed in lieu agreements before signing

- Lender disputes or unfair practices

- Bankruptcy considerations

- State-specific legal requirements

What they provide:

- Legal protection and representation

- Contract review and negotiation

- Title issue resolution

- Court representation if needed

- Strategic advice on best alternatives

Cost: $150-$400 per hour or flat fees of $1,500-$3,500 for full representation

HUD-Approved Housing Counselors

When to consult:

- Early in the financial hardship process

- Exploring all available options

- Need for free or low-cost guidance

- Assistance with lender negotiations

- Understanding government programs

What they provide:

- Free or low-cost counseling

- Option analysis and recommendations

- Lender communication assistance

- Budget and financial planning

- Application preparation help

Cost: Free or minimal fees (usually under $50)

Find HUD-approved counselors at: www.hud.gov/findacounselor

Real Estate Agents (Short Sale Specialists)

When to hire:

- Pursuing short sale option

- Need property valuation and marketing

- Lender negotiation for sale approval

- Maximizing relocation assistance

What they provide:

- Property marketing and showings

- Buyer negotiations

- Lender short sale package preparation

- Relocation assistance negotiation

- Transaction coordination

Cost: Typically paid from sale proceeds (no out-of-pocket cost to seller)

Tax Professionals (CPAs or Enrolled Agents)

When to consult:

- Understanding tax consequences of forgiven debt

- Insolvency calculations

- 1099-C form preparation

- Tax return implications

- Minimizing tax liability

What they provide:

- Tax consequence analysis

- Insolvency documentation

- Tax return preparation

- IRS representation if needed

- Strategic tax planning

Cost: $200-$500 for consultation and planning; $300-$1,000+ for full tax preparation

Property Solutions Companies

Companies like Sure Path Property Solutions offer industry experts who specialize in complex property situations, including:

- Properties with back taxes

- Multiple heir situations

- Clouded title issues

- Lien and judgment resolution

- Coordinating with counties and title professionals

When to contact:

- Complex ownership situations

- Multiple liens or judgments

- Back tax complications

- Inherited property with multiple owners

- Difficulty selling through traditional means

These specialists provide helpful solutions and trustworthy service for homeowners facing complicated real estate challenges that make traditional foreclosure alternatives difficult to navigate.

Red Flags: Avoiding Foreclosure Rescue Scams

Unfortunately, desperate homeowners often become targets for predatory scams. Watch for these warning signs:

🚩 Upfront fees before any services are provided

🚩 Guaranteed outcomes or promises that seem too good to be true

🚩 Pressure to sign documents immediately without review

🚩 Requests to sign over deed to third party

🚩 Instructions to stop communicating with lender

🚩 Rent-to-buy-back schemes requiring deed transfer

🚩 Unlicensed individuals claiming to provide legal services

Legitimate professionals:

✅ Provide clear fee structures

✅ Encourage document review

✅ Are properly licensed and credentialed

✅ Have verifiable references and reviews

✅ Explain all options honestly

✅ Never guarantee specific outcomes

Frequently Asked Questions

How long does deed in lieu stay on credit report?

A deed in lieu of foreclosure remains on your credit report for 7 years from the date of completion. However, its impact on your credit score diminishes over time, especially if you rebuild credit responsibly through timely payments on other accounts.

Can I buy another home after deed in lieu?

Yes, but waiting periods apply. For conventional loans, you typically must wait 4 years. FHA, VA, and USDA loans generally require 2-3 years. These timelines can be reduced with extenuating circumstances documentation and larger down payments (20%+).

Will I owe taxes on forgiven mortgage debt?

Possibly. Forgiven debt may be considered taxable income and reported on IRS Form 1099-C. However, you may qualify for exclusions if:

- The property was your primary residence

- You were insolvent at the time of forgiveness

- The debt was discharged in bankruptcy

- Certain disaster relief provisions apply

Consult a tax professional to understand your specific situation.

What happens if I have a second mortgage?

Second mortgages and other subordinate liens must be resolved before deed in lieu can proceed. The junior lien holder must provide a Second-Lien Release, which typically takes 90 days to negotiate. If they refuse, deed in lieu cannot proceed, and you’ll need to explore other alternatives like short sale or bankruptcy.

Can my lender force me to do a deed in lieu?

No. Deed in lieu is a voluntary agreement. Lenders cannot force borrowers to transfer property ownership. However, if you don’t cooperate with foreclosure alternatives, the lender will proceed with formal foreclosure proceedings.

Is deed in lieu better than foreclosure?

Generally yes, for several reasons:

- Less credit damage (85-160 points vs. 200-250+ points)

- Faster resolution (90-120 days vs. 180-360+ days)

- No public foreclosure record

- Potential relocation assistance

- More dignified, cooperative process

However, individual circumstances vary. Some situations may benefit from allowing foreclosure to proceed (particularly if bankruptcy is planned or significant deficiency exists).

Conclusion: Making the Right Decision for Your Situation

Facing potential foreclosure ranks among life’s most stressful financial challenges. The uncertainty, fear, and complexity can feel paralyzing. However, understanding the Deed in Lieu of Foreclosure: Complete Guide, Process & Requirements empowers homeowners to make informed decisions and take control of difficult circumstances.

A deed in lieu of foreclosure offers a viable middle ground for homeowners who can no longer afford their mortgage but want to avoid the public record and severe credit consequences of formal foreclosure. While not perfect for every situation, it provides helpful solutions for those who qualify.

Key Takeaways to Remember

✅ Deed in lieu is voluntary cooperation between borrower and lender to transfer property ownership and satisfy mortgage debt

✅ The process takes 90-120 days and requires financial hardship documentation, property evaluation, and lien resolution

✅ Qualification isn’t guaranteed – lenders maintain strict eligibility criteria including property condition, lien status, and demonstration of unsuccessful alternatives

✅ Credit impact is significant but less severe than foreclosure – expect 85-160 point drop for 7 years versus 200-250+ points for foreclosure

✅ Multiple alternatives exist – loan modification, forbearance, short sale, bankruptcy, and traditional sale may better fit specific circumstances

Actionable Next Steps

If you’re considering deed in lieu or other foreclosure alternatives, take these steps immediately:

1. Contact your lender’s loss mitigation department – Start the conversation early, before missing multiple payments. Document all communications.

2. Gather financial documentation – Collect pay stubs, tax returns, bank statements, and expense receipts to demonstrate hardship.

3. Explore all alternatives – Don’t limit yourself to one option. Evaluate loan modification, forbearance, and short sale alongside deed in lieu.

4. Consult with professionals – HUD-approved housing counselors offer free guidance. Consider real estate attorneys for complex situations.

5. Understand your timeline – Know when foreclosure proceedings begin in your state and work backward to ensure adequate time for alternatives.

6. Address subordinate liens early – If second mortgages or other liens exist, begin negotiating releases immediately as this process takes 90+ days.

7. Maintain the property – Keep the home in reasonable condition to improve lender approval chances and maximize outcomes.

8. Review all agreements carefully – Never sign documents without understanding terms, especially regarding deficiency liability and tax consequences.

When Traditional Solutions Don’t Work

For homeowners facing complicated situations – back taxes, multiple heirs, liens, judgments, or unclear title – traditional foreclosure alternatives may not address all challenges. These complex scenarios require specialized expertise.

Sure Path Property Solutions provides expert service and helpful guidance for property owners navigating complicated real estate issues. Our industry experts simplify complex situations, coordinate with counties and title professionals, and guide property owners toward clear, practical solutions with friendly and caring support.

Whether you’re dealing with inherited property with multiple owners, properties encumbered by liens and judgments, or difficulty selling through traditional means, professional assistance can make the difference between overwhelming confusion and successful resolution.

Final Thoughts

No one plans to face foreclosure. Financial hardship can strike anyone through job loss, medical emergencies, divorce, or business failure. What matters most is how you respond to the challenge.

Deed in lieu of foreclosure represents one tool in a larger toolkit of foreclosure alternatives. It’s not the right choice for everyone, but for qualified homeowners seeking a faster, more dignified exit from an unaffordable mortgage, it offers significant advantages over formal foreclosure.

The key is acting early, understanding your options, gathering proper documentation, and seeking trustworthy service from qualified professionals who can guide you through the process.

Your current situation doesn’t define your future. With the right information, professional guidance, and proactive approach, you can navigate this challenge and emerge with your financial future intact.

Take the first step today. Your path to resolution begins with a single conversation with your lender or a trusted advisor who can help you evaluate which foreclosure alternative best fits your unique circumstances.

References

[1] Consumer Financial Protection Bureau. (2024). “What is a deed in lieu of foreclosure?” CFPB Housing Resources. https://www.consumerfinance.gov/

[2] Federal Housing Finance Agency. (2024). “Foreclosure Alternative Timelines and Requirements.” FHFA Borrower Assistance Programs.

[3] U.S. Department of Housing and Urban Development. (2024). “Subordinate Lien Resolution in Loss Mitigation.” HUD Handbook 4000.1.

[4] Fannie Mae. (2025). “Deed in Lieu of Foreclosure: Servicing Guide.” Fannie Mae Single-Family Servicing Guide, Section D2-3.2-01.

[5] Freddie Mac. (2024). “Workout Options for Borrowers in Default.” Freddie Mac Seller/Servicer Guide, Chapter 9202.

[6] American Bar Association. (2024). “Second Lien Release Procedures and Timeline.” ABA Real Property, Trust and Estate Law Section.

[7] FICO. (2024). “Understanding Your FICO Score: Impact of Foreclosure Alternatives.” myFICO Consumer Education Resources.

[8] National Association of Realtors. (2024). “Cash for Keys Programs: Industry Standards and Practices.” NAR Research and Statistics.

Sure Path is a family-owned, curative-title cash buyer. We handle the paperwork and pay what’s owed at closing — no fees, no repairs, no pressure.