How to Do a Short Sale: Complete Step-by-Step Process (2025)

![Professional landscape hero image (1536x1024) featuring bold text overlay 'How to Do a Short Sale: Complete Step-by-Step Process [2025]' in](https://zsxkvszxbhpwnvzxdydv.supabase.co/storage/v1/object/public/generated-images/kie/47d01b56-0e2e-40fb-a176-eb389d5dcf38/slot-0-1765311064899.png)

Facing foreclosure can feel overwhelming, but understanding how to do a short sale might provide the lifeline needed to avoid the devastating impact on credit and financial future. In 2025, approximately 2.5% of homeowners find themselves underwater on their mortgages—owing more than their property is worth—making short sales an increasingly relevant solution for those struggling with mortgage payments[1]. This comprehensive guide walks through the complete step-by-step process of executing a short sale in 2025, offering helpful guidance for homeowners navigating this challenging situation.

Learning how to do a short sale: complete step-by-step process [2025] can mean the difference between a controlled exit from an unaffordable property and the chaos of foreclosure. With the right approach and expert service, homeowners can work with their lenders to sell their property for less than what’s owed while minimizing credit damage and moving forward with dignity.

Key Takeaways

- Short sales allow homeowners to sell property for less than the mortgage balance with lender approval, avoiding foreclosure’s severe credit consequences

- The process typically takes 3-6 months and requires extensive documentation, including a hardship letter, financial statements, and third-party authorization forms

- Working with experienced short sale professionals dramatically increases approval chances and ensures complete submission packages that prevent delays

- All offers must receive lender approval since the bank accepts less than what’s owed, making pricing strategy and negotiation critical

- Multiple liens require separate approvals from each lienholder, adding complexity that industry experts can help navigate successfully

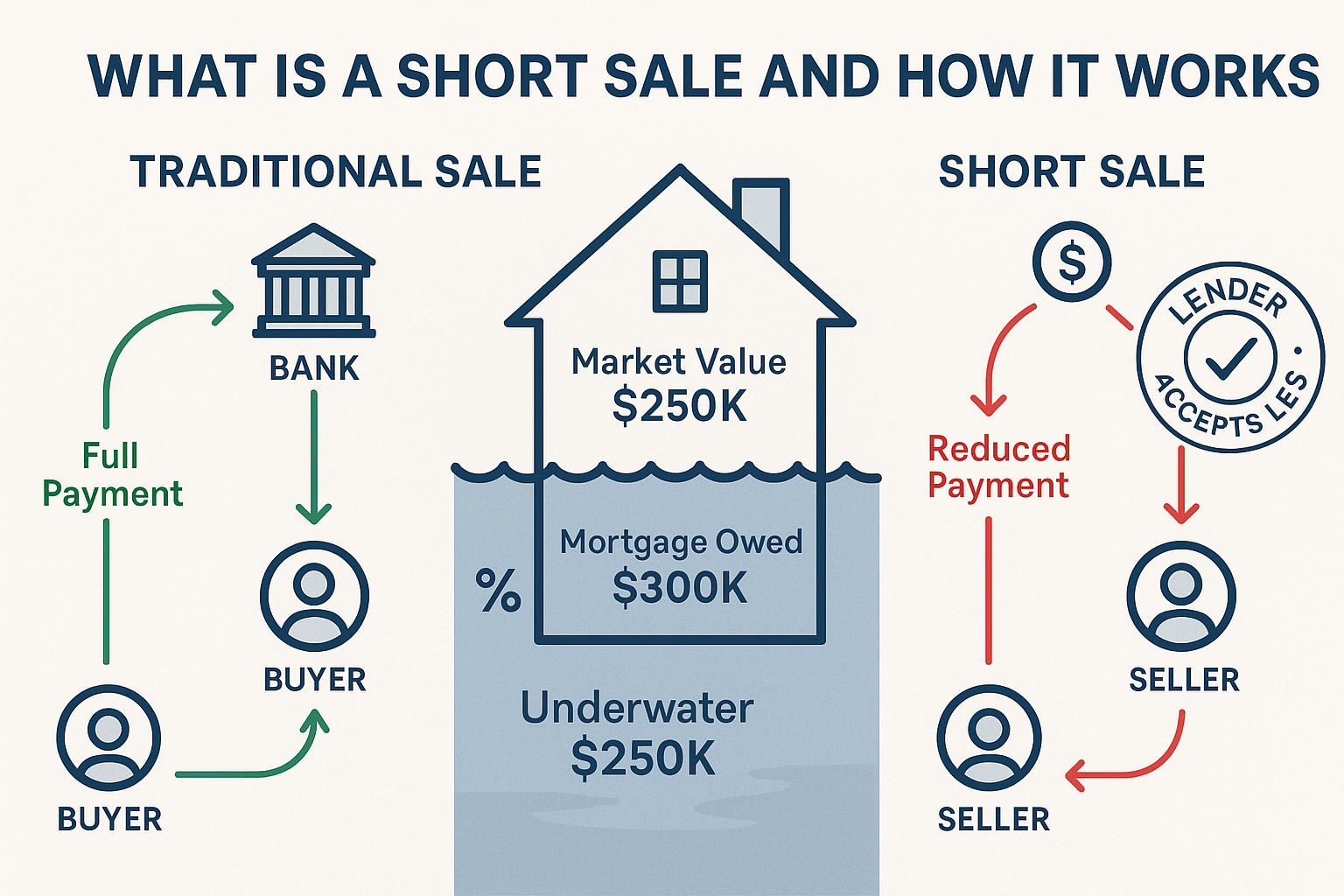

What Is a Short Sale?

A short sale occurs when a homeowner sells their property for less than the outstanding mortgage balance, with the lender agreeing to accept the reduced payoff amount. This arrangement represents a negotiated solution between the homeowner, buyer, and lender to avoid the foreclosure process.

Understanding the Short Sale Concept

In a traditional home sale, the proceeds cover the mortgage balance, closing costs, and provide the seller with remaining equity. With a short sale, the property’s market value has fallen below what the homeowner owes—a situation called being “underwater” or having negative equity.

For example, imagine owing $300,000 on a mortgage while the home’s current market value sits at $250,000. That $50,000 gap represents negative equity. In a short sale, the lender agrees to accept the $250,000 sale price (minus closing costs) even though it doesn’t cover the full debt.

Why Lenders Agree to Short Sales

Banks aren’t in the real estate business. Foreclosure costs lenders significant money through:

- Legal fees and court costs

- Property maintenance and security

- Real estate commissions when reselling

- Extended timeline (often 12-18 months)

- Property deterioration and vandalism risk

A short sale often represents the lesser financial loss for the lender. They recover funds faster and avoid the expenses associated with foreclosure proceedings. This mutual benefit creates the foundation for successful short sale negotiations.

Short Sale vs. Foreclosure: Key Differences

| Aspect | Short Sale | Foreclosure |

|---|---|---|

| Credit Impact | 50-150 point drop | 200-300 point drop |

| Credit Report Duration | 7 years | 7 years |

| Future Mortgage Eligibility | 2-4 years (with exceptions) | 5-7 years |

| Control Over Process | Homeowner participates actively | Lender controls entirely |

| Deficiency Judgment Risk | Negotiable; often waived | More likely |

| Tax Consequences | Potentially reportable as income | Potentially reportable as income |

The credit damage from a short sale, while significant, typically proves less severe than foreclosure. More importantly, short sales demonstrate financial responsibility by attempting to resolve the debt rather than abandoning the property.

How to Qualify for a Short Sale

Not every underwater homeowner qualifies for a short sale. Lenders have specific criteria that must be met before they’ll consider approving this type of transaction.

Financial Hardship Requirement

Lenders require documented financial hardship that makes continuing mortgage payments impossible or unreasonably burdensome. Acceptable hardships include:

✅ Job loss or reduced income – Unemployment, reduced hours, or significant pay cuts

✅ Medical expenses – Serious illness, injury, or disability affecting income

✅ Divorce or separation – Loss of second income or increased expenses

✅ Death of spouse or co-borrower – Sudden loss of household income

✅ Military deployment – Active duty orders affecting ability to maintain property

✅ Job relocation – Transfer requiring move beyond reasonable commuting distance

✅ Adjustable rate increase – Payment shock from ARM adjustment

✅ Business failure – Loss of self-employment income

Simply wanting to sell because the property lost value doesn’t constitute hardship. The situation must genuinely prevent the homeowner from maintaining payments.

Property Value Requirements

The property’s current market value must be less than the total debt secured against it. This includes:

- First mortgage balance

- Second mortgages or HELOCs

- Property tax liens

- HOA liens

- Judgment liens

- Mechanic’s liens

A professional Broker Price Opinion (BPO) or appraisal determines the property’s current market value. The lender typically orders this evaluation after receiving the short sale application.

Homeowner Eligibility Checklist

Before pursuing a short sale, verify these eligibility factors:

- Currently behind on mortgage payments OR facing imminent default

- Documented financial hardship preventing continued payments

- Property value less than total mortgage debt

- No available assets that could resolve the mortgage debt

- Owner-occupied or investment property (guidelines vary)

- Willing to provide complete financial disclosure

- No recent fraudulent activity or misrepresentation

- Cooperative and responsive throughout the process

Important Note: Some lenders require homeowners to be delinquent before considering a short sale, while others accept applications from current borrowers facing imminent hardship. Contact your specific lender to understand their requirements.

How to Do a Short Sale: Complete Step-by-Step Process [2025]

Successfully executing a short sale requires methodical preparation and expert service. This detailed roadmap breaks down each phase of how to do a short sale: complete step-by-step process [2025].

Step 1: Assess Your Financial Situation

Begin by conducting an honest evaluation of your financial circumstances with a qualified professional.

Action items:

- Calculate total debt secured against the property

- Obtain a preliminary property valuation through online tools or a real estate agent

- Review monthly income versus expenses

- Identify the specific hardship preventing continued payments

- Consult with a short sale specialist or real estate agent experienced in short sales[1][6]

This assessment determines whether a short sale represents the best option or if alternatives like loan modification, forbearance, or traditional sale might work better.

Step 2: Contact Your Lender’s Loss Mitigation Department

Early communication with the lender establishes the foundation for the entire process.

What to do:

- Call your mortgage servicer and ask for the Loss Mitigation Department or Short Sale Department

- Request the name and direct contact information for the specific person who will process your application[3]

- Ask for the short sale application package and complete list of required documentation

- Inquire about their specific timeline expectations and approval process

- Request information about potential deficiency judgments and their policies

Document every conversation with date, time, representative name, and discussion summary. This record proves invaluable if disputes arise later.

Step 3: Hire an Experienced Short Sale Agent

Working with a real estate professional who specializes in short sales dramatically increases success rates.

What to look for:

- Proven track record with short sale transactions (ask for specific numbers)

- Certifications such as Short Sale and Foreclosure Resource (SFR) designation

- Established relationships with local lenders

- Understanding of BPO and appraisal processes

- Strong negotiation skills

- Patience and communication throughout the lengthy process

The right agent provides helpful solutions by managing lender communications, pricing strategy, marketing, and buyer qualification—all while keeping the process moving forward.

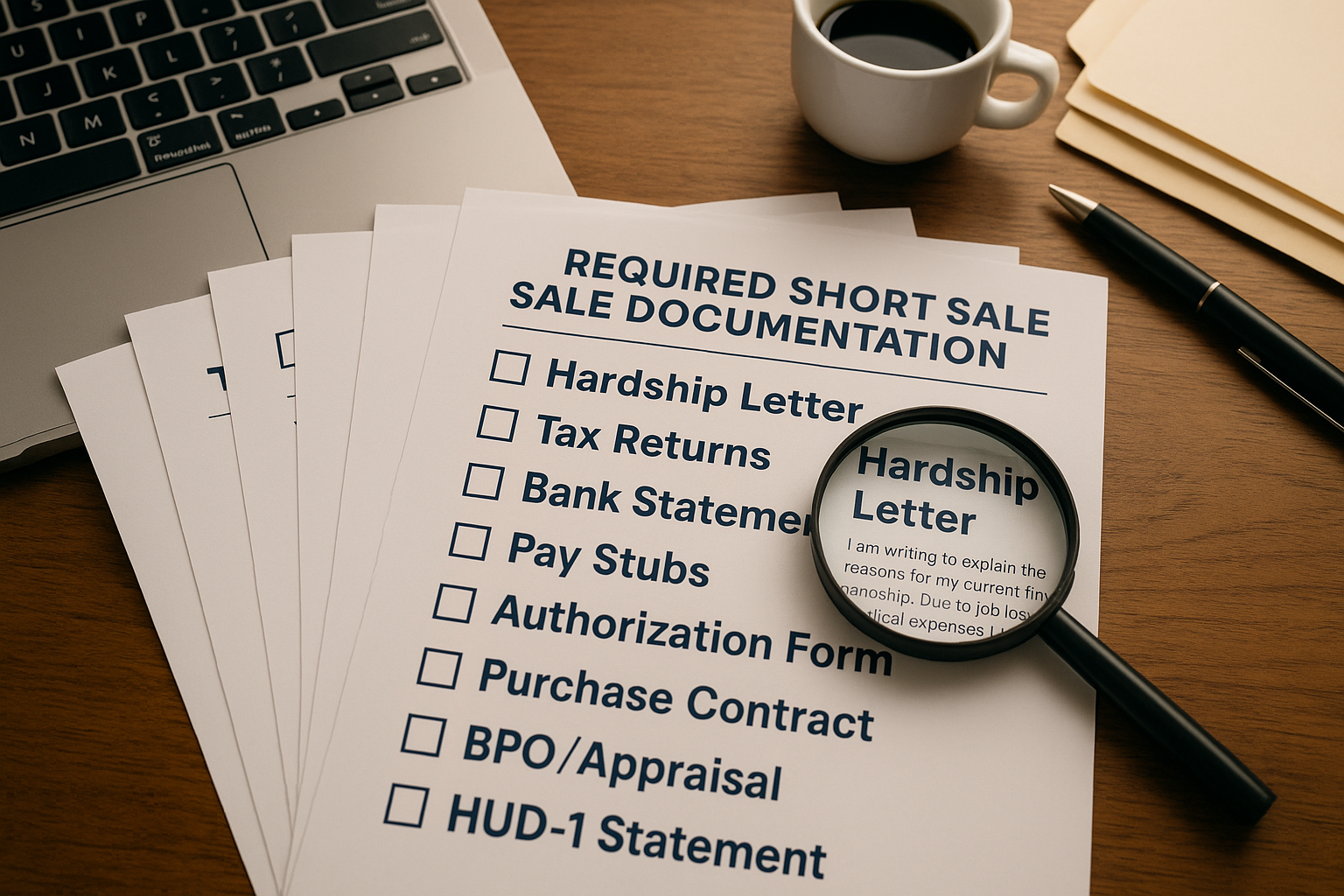

Step 4: Gather Required Documentation

Compile a comprehensive documentation package before listing the property. This preparation prevents delays once an offer arrives.

Essential documents include:

- Hardship letter explaining why mortgage payments cannot continue

- Financial statement or worksheet (lender-provided form)

- Two years of tax returns

- Two months of pay stubs (or proof of unemployment)

- Two months of bank statements (all accounts)

- Monthly expense breakdown

- Comparative Market Analysis (CMA) from your agent

- Repair estimates if property needs significant work

- HOA statements showing any dues owed

- Signed third-party authorization form allowing your agent to communicate with the lender[1]

The third-party authorization proves particularly important. Without it, lenders cannot discuss your loan details with your agent or attorney, creating frustrating communication barriers.

Step 5: List the Property for Sale

With documentation prepared, list the property on the market like a traditional sale.

Pricing strategy considerations:

- Set asking price based on current market conditions and comparable sales[5]

- Price competitively to attract qualified buyers quickly

- Understand that lender has final approval on any accepted offer

- Consider pricing slightly below market to generate multiple offers

- Include “Short Sale” disclosure in all marketing materials

Marketing the property effectively remains crucial. The faster a qualified buyer emerges, the sooner the lender approval process begins. Professional photography, online listings, open houses, and targeted marketing all contribute to attracting serious buyers.

Step 6: Review and Negotiate Offers

When offers arrive, the process differs significantly from traditional sales.

Key considerations:

- Evaluate buyer’s financial strength (pre-approval letter, proof of funds)

- Assess offer terms beyond just price (contingencies, timeline, earnest money)

- Understand that all offers require lender approval[6]

- Stronger buyers with fewer contingencies often win over higher-priced offers with uncertain financing

- Cash buyers or conventional financing typically close faster than FHA/VA loans

Work with your agent to select the offer most likely to receive lender approval and successfully close. The highest offer doesn’t always represent the best choice if the buyer can’t perform.

Step 7: Compile the Complete Short Sale Package

Once an acceptable offer is in hand, assemble the comprehensive submission package for the lender.

Complete package includes:

- Executed purchase contract

- Buyer’s pre-approval letter or proof of funds

- Updated hardship letter

- Current financial documentation

- Third-party authorization form

- Comparative Market Analysis or BPO

- Preliminary HUD-1 Settlement Statement prepared by escrow/title company[3]

- Repair estimates (if applicable)

- Any additional lender-specific forms

Critical Success Factor: Submit the entire package at once rather than piece by piece. Lenders penalize incomplete files by moving them to the back of the processing queue[1]. A complete submission from the start dramatically reduces approval timeline.

Step 8: Submit Package and Await Lender Response

With the complete package assembled, submit it through the lender’s preferred method (online portal, fax, email, or mail).

Timeline expectations:

- Fannie Mae loans: Written response within 5 business days of initial offer, or within 30 calendar days if complete BPO required[4]

- Conventional loans: Typically 30-90 days for initial response

- FHA loans: 30-60 days average

- Portfolio loans: Varies widely by lender

During this waiting period, respond immediately to any lender requests for additional information. Delays in providing requested documentation restart the review timeline.

Step 9: Negotiate Lender Counter-Offers

Lenders frequently counter the submitted offer with different terms.

Common lender counter-offers:

- Higher sales price requirement

- Seller contribution to closing costs eliminated

- Specific repair requirements before closing

- Shortened closing timeline

- Promissory note for partial deficiency balance

- Cash contribution from seller at closing

Your agent negotiates these counter-terms with both the lender and buyer. Finding acceptable middle ground that keeps the deal together requires skill and persistence—hallmarks of trustworthy service from experienced professionals.

Step 10: Obtain Approval for All Liens

Properties with multiple loans or liens require separate approvals from each lienholder[3].

Multiple lien considerations:

- First mortgage holder must approve first

- Second mortgages/HELOCs receive only remaining proceeds after first lien

- Junior lienholders often receive minimal payoff, making negotiation challenging

- Tax liens may require separate payment arrangements

- HOA liens must be satisfied or negotiated

Second lien holders pose particular challenges since they receive little or nothing from the sale proceeds. Experienced short sale professionals understand negotiation strategies to secure junior lienholder approval, including offering small cash settlements to release their liens.

Step 11: Review and Sign Short Sale Agreement

Before final approval, review the short sale agreement carefully.

Agreement typically includes:

- What the short sale processor/agent will do

- How they’ll be compensated

- Confirmation they’re not providing legal or tax advice[1]

- Any seller obligations (promissory notes, cash contributions)

- Deficiency waiver status

- Timeline for closing

Consider having a real estate attorney review this agreement, especially regarding deficiency judgment waivers and tax implications.

Step 12: Close the Transaction

With all approvals secured, proceed to closing.

Final steps:

- Schedule closing date coordinating all parties

- Conduct final walk-through (buyer)

- Sign closing documents

- Transfer property title to buyer

- Vacate property by agreed-upon date

- Receive written confirmation of satisfied mortgage debt

Obtain written documentation that the lender considers the debt satisfied and will not pursue a deficiency judgment. This protection proves critical for future financial planning.

Required Documentation for a Short Sale

Thorough documentation separates successful short sales from rejected applications. Understanding what lenders need and why helps homeowners prepare complete packages.

The Hardship Letter: Your Most Important Document

The hardship letter explains in personal terms why continuing mortgage payments has become impossible. This narrative document should:

Include these elements:

- Brief background on property purchase and initial circumstances

- Specific hardship that occurred (job loss, medical crisis, divorce, etc.)

- Timeline of when hardship began

- Steps already taken to resolve the situation

- Current financial reality preventing continued payments

- Explanation of why selling traditionally isn’t possible

- Request for lender’s consideration of short sale

Writing tips:

- Keep it to 1-2 pages maximum

- Be honest and factual without excessive emotion

- Provide specific dates and numbers

- Avoid blaming the lender or making demands

- Maintain respectful, professional tone

- Proofread carefully for errors

The hardship letter humanizes the transaction for the lender’s decision-maker. A well-crafted letter demonstrates genuine hardship while showing responsibility and cooperation.

Financial Documentation Checklist

Lenders verify hardship through comprehensive financial disclosure:

Income verification:

- Two most recent pay stubs (all jobs)

- Two years of federal tax returns with all schedules

- Profit and loss statement (self-employed)

- Social Security/disability award letters

- Unemployment benefits documentation

- Pension or retirement income statements

Asset documentation:

- Two months of bank statements (all accounts)

- Investment account statements

- Retirement account statements (401k, IRA)

- Vehicle titles and valuations

- Other real estate ownership documentation

Liability documentation:

- Current mortgage statement

- Second mortgage/HELOC statements

- Credit card statements

- Personal loan documentation

- Medical bills

- Other debt obligations

Property documentation:

- Homeowner’s insurance declaration page

- Property tax statements

- HOA statements and bylaws

- Repair estimates for needed work

- Recent utility bills

Transaction-Specific Documents

Once an offer is received, additional documents join the package:

- Purchase and Sale Agreement – Fully executed contract with buyer

- Buyer’s Financial Qualification – Pre-approval letter or proof of funds

- Preliminary Title Report – Showing all liens and encumbrances

- Comparative Market Analysis – Agent-prepared valuation

- Preliminary HUD-1 Settlement Statement – Estimated closing costs and proceeds distribution[3]

- Listing Agreement – Proving property actively marketed

- Marketing Activity Report – Showing days on market, showings, previous offers

The preliminary HUD-1 proves particularly important as many lenders reference this document heavily in their acceptance or rejection decisions[3].

Timeline and Expectations for Short Sales

Understanding realistic timeframes helps manage expectations and reduce frustration during the short sale process.

Typical Short Sale Timeline

| Phase | Duration | Key Activities |

|---|---|---|

| Preparation | 2-4 weeks | Gather documents, hire agent, contact lender |

| Listing & Marketing | 2-8 weeks | List property, show to buyers, receive offers |

| Package Submission | 1 week | Compile and submit complete package to lender |

| Lender Review | 4-12 weeks | BPO ordered, file reviewed, decision made |

| Negotiation | 1-4 weeks | Counter-offers, junior lien negotiations |

| Closing Preparation | 2-4 weeks | Title work, buyer financing, inspections |

| Total Timeline | 3-6 months | From initial contact to closing |

This timeline assumes a complete package submission and responsive communication. Incomplete submissions or communication delays can extend the process to 9-12 months or longer.

Factors That Affect Timeline

Accelerating factors:

- Complete documentation submitted initially

- Experienced short sale agent managing process

- Single lien holder (no junior mortgages)

- Responsive lender with clear procedures

- Qualified cash buyer or strong financing

- Competitive pricing attracting quick offers

Delaying factors:

- Incomplete or incorrect documentation

- Multiple lien holders requiring separate approvals

- Lender backlogs or staffing changes

- Buyer financing issues or contingencies

- Property condition problems discovered during inspection

- Homeowner unresponsiveness to lender requests

What to Expect During the Waiting Period

The weeks between submission and lender decision test patience. During this time:

Homeowners should:

- Continue making payments if financially possible (improves approval odds)

- Maintain property in good condition

- Respond immediately to any lender requests

- Keep utilities on and property insured

- Communicate regularly with agent

- Avoid making major financial changes (new debt, job changes)

What’s happening behind the scenes:

- Lender orders BPO or appraisal to verify value

- File reviewed by loss mitigation specialist

- Investor approval obtained (if loan is securitized)

- Junior lien holders contacted for approval

- Title review conducted

- Automated valuation models run

- Comparative foreclosure cost analysis performed

Understanding this background activity helps explain why the process takes months rather than weeks.

Managing Stress During the Process

Short sales create significant emotional strain. These strategies help maintain perspective:

🧘 Practice patience – The process simply takes time; frustration doesn’t accelerate it

📞 Maintain communication – Regular updates from your agent reduce anxiety

📋 Focus on controllables – Keep property maintained and respond promptly to requests

🤝 Seek support – Talk with family, friends, or counselors about the stress

📚 Stay informed – Understanding the process reduces fear of the unknown

🎯 Remember the goal – Short sale avoids foreclosure’s worse consequences

Organizations like Sure Path Property Solutions specialize in providing helpful guidance through these complex situations, offering friendly and caring support when homeowners feel overwhelmed by the process.

Alternatives to Short Sales

Before committing to a short sale, explore these alternatives that might better fit specific situations.

Loan Modification

What it is: Permanent change to loan terms making payments more affordable.

Modifications may include:

- Reduced interest rate

- Extended loan term (30 to 40 years)

- Principal forbearance (portion set aside interest-free)

- Principal reduction (rare but possible)

Best for: Homeowners who want to keep the property and whose income can support modified payments.

Pros: Keep the home, avoid selling, less credit damage

Cons: Not all qualify, still owe full debt, may increase total interest paid

Forbearance Agreement

What it is: Temporary pause or reduction in payments while recovering from short-term hardship.

How it works: Lender agrees to accept reduced payments or no payments for 3-12 months, with missed amounts added to loan balance or due as lump sum after forbearance ends.

Best for: Temporary hardships with clear recovery timeline (short-term job loss, medical recovery).

Pros: Keeps home, provides breathing room, avoids foreclosure

Cons: Debt still owed, payments resume eventually, may include lump sum requirement

Deed in Lieu of Foreclosure

What it is: Voluntarily transferring property deed to lender in exchange for release from mortgage obligation.

How it works: Homeowner signs over property ownership; lender cancels debt and avoids foreclosure process.

Best for: Homeowners unable to sell property who want to avoid foreclosure.

Pros: Faster than foreclosure, less credit damage than foreclosure, may include relocation assistance

Cons: Still significant credit impact, must vacate property, not available with junior liens

Traditional Sale with Seller Contribution

What it is: Selling property at market value while bringing cash to closing to cover the shortfall.

Example: Property worth $250,000, mortgage balance $270,000, seller brings $20,000 plus closing costs to closing.

Best for: Homeowners with available savings who want to avoid short sale or foreclosure credit impact.

Pros: Minimal credit impact, faster process, clean break

Cons: Requires significant cash, may deplete emergency savings

Bankruptcy

What it is: Legal process providing debt relief through Chapter 7 (liquidation) or Chapter 13 (reorganization).

How it affects mortgages:

- Chapter 7: May discharge other debts, freeing income for mortgage

- Chapter 13: Creates payment plan potentially including mortgage arrears

Best for: Overwhelming debt beyond just the mortgage.

Pros: Stops foreclosure temporarily, may discharge other debts, provides fresh start

Cons: Severe credit impact (7-10 years), legal costs, public record, complex process

Rental Conversion

What it is: Converting primary residence to rental property generating income to cover mortgage.

Considerations:

- Rental income must cover mortgage, taxes, insurance, maintenance

- Landlord responsibilities and risks

- Lender approval may be required

- Alternative housing costs for owner

Best for: Properties in strong rental markets where income covers all costs.

Pros: Keep property, build equity, potential appreciation

Cons: Landlord responsibilities, maintenance costs, vacancy risk, still owe full debt

Working with Professionals: The Value of Expert Guidance

Successfully navigating how to do a short sale: complete step-by-step process [2025] rarely succeeds as a solo endeavor. The right professionals provide helpful solutions that dramatically increase approval odds.

Short Sale Specialists and Real Estate Agents

What they provide:

- Accurate pricing strategy based on lender expectations

- Professional marketing attracting qualified buyers

- Buyer screening and qualification

- Lender communication and negotiation

- Documentation package preparation

- Timeline management and follow-up

- Problem-solving when obstacles arise

Questions to ask potential agents:

- How many short sales have you successfully closed?

- What’s your approval rate with lenders?

- How do you communicate with clients during the waiting period?

- What’s your strategy for dealing with junior lien holders?

- Can you provide references from past short sale clients?

- What happens if the lender denies the short sale?

Industry experts with proven track records transform the complex short sale process into a manageable journey with clear milestones and realistic expectations.

Real Estate Attorneys

While not always required, real estate attorneys provide valuable protection in complex situations:

When to consult an attorney:

- Multiple liens or complicated title issues

- Deficiency judgment concerns

- Divorce involving property division

- Inheritance or estate situations

- Lender requesting cash contribution or promissory note

- Tax implications requiring clarification

Attorneys review short sale agreements, negotiate deficiency waivers, and ensure homeowners understand all legal implications before signing documents.

Tax Professionals

Short sales create potential tax consequences requiring expert advice.

Tax considerations:

- Canceled debt income: Forgiven mortgage debt may be taxable as income

- Mortgage Forgiveness Debt Relief Act: Previously provided exclusions (verify current status for 2025)

- Insolvency exception: May exclude canceled debt if liabilities exceed assets

- Form 1099-C: Lenders issue this form for canceled debt over $600

- State tax implications: Vary by jurisdiction

Consult a CPA or tax attorney before completing a short sale to understand potential tax liability and planning strategies.

Companies Specializing in Complex Property Situations

Organizations like Sure Path Property Solutions offer comprehensive support for homeowners facing complicated real estate challenges including:

- Properties with back taxes

- Multiple heirs or ownership disputes

- Existing liens and judgments

- Unclear or clouded title

- Properties difficult to sell through traditional means

These specialists coordinate with counties, title professionals, and lenders to navigate complex situations that would overwhelm typical real estate agents. Their expert service provides friendly and caring guidance through processes that seem impossibly complicated.

When facing multiple challenges simultaneously—underwater mortgage plus tax liens plus unclear title—working with professionals who specialize in these exact situations provides the helpful solutions needed to reach resolution.

Common Short Sale Mistakes to Avoid

Learning from others’ mistakes prevents costly errors during your short sale journey.

❌ Waiting Too Long to Start the Process

The mistake: Hoping the situation improves while falling further behind on payments.

Why it’s problematic: Lenders need time to process short sales. Starting when foreclosure is imminent leaves insufficient time for approval.

The solution: Contact the lender and begin the process as soon as hardship becomes apparent and continuing payments seems impossible.

❌ Submitting Incomplete Documentation

The mistake: Sending partial packages or missing required forms.

Why it’s problematic: Incomplete files move to the back of the processing queue, adding months to the timeline[1].

The solution: Gather every required document before submission. Use a checklist and verify completeness with your agent before sending.

❌ Overpricing the Property

The mistake: Listing significantly above market value hoping to reduce the shortfall.

Why it’s problematic: Overpriced properties don’t attract buyers. Time wasted on market increases foreclosure risk.

The solution: Price competitively based on current market conditions and comparable sales. Generate buyer interest quickly rather than waiting months for the “perfect” offer.

❌ Failing to Communicate with the Lender

The mistake: Avoiding lender calls or ignoring correspondence.

Why it’s problematic: Lenders interpret non-communication as non-cooperation, leading to denials.

The solution: Respond promptly to all lender requests. Maintain regular contact through your authorized agent. Document all communications.

❌ Not Obtaining Third-Party Authorization

The mistake: Forgetting to submit the authorization form allowing your agent to communicate with the lender.

Why it’s problematic: Without authorization, lenders cannot discuss your loan with your agent, creating communication barriers and delays[1].

The solution: Submit the third-party authorization form immediately when starting the process. Verify the lender has it on file.

❌ Accepting the First Buyer Without Proper Qualification

The mistake: Accepting an offer from an unqualified buyer excited about the price.

Why it’s problematic: Unqualified buyers can’t close, wasting months of processing time when their financing falls through.

The solution: Verify buyer qualification thoroughly. Strong pre-approval letters or proof of funds for cash buyers. Consider buyer’s track record and contingencies.

❌ Making Major Financial Changes During the Process

The mistake: Taking on new debt, changing jobs, or making large purchases while the short sale is pending.

Why it’s problematic: Lenders verify financial information at multiple points. Changes raise red flags about hardship legitimacy.

The solution: Maintain financial status quo throughout the process. Delay major changes until after closing.

❌ Neglecting Property Maintenance

The mistake: Allowing the property to deteriorate during the process.

Why it’s problematic: Buyers walk away from properties in poor condition. Lenders order BPOs showing diminished value due to neglect.

The solution: Maintain the property in showing condition. Keep utilities on, lawn mowed, and basic repairs current.

❌ Assuming Deficiency Waiver Without Confirmation

The mistake: Believing the lender automatically waives the deficiency balance.

Why it’s problematic: Without explicit written waiver, lenders may pursue deficiency judgments after closing.

The solution: Negotiate deficiency waiver as part of the short sale approval. Obtain written confirmation before closing. Consult an attorney if the lender won’t provide a waiver.

❌ Ignoring Tax Implications

The mistake: Not consulting a tax professional about canceled debt income.

Why it’s problematic: Surprise tax bills can create new financial hardship after resolving the mortgage problem.

The solution: Consult a CPA or tax attorney before completing the short sale. Understand potential tax liability and plan accordingly.

Frequently Asked Questions About Short Sales

How much does a short sale hurt your credit?

Short sales typically reduce credit scores by 50-150 points, compared to 200-300 points for foreclosure[2]. The exact impact depends on your starting score and overall credit profile. Higher credit scores often see larger point drops. The short sale remains on your credit report for seven years, but its impact diminishes over time, especially with responsible credit management afterward.

Can you buy another home after a short sale?

Yes, but waiting periods apply. Conventional loans typically require 2-4 years after a short sale, FHA loans require 3 years, and VA loans require 2 years. Some programs offer exceptions with extenuating circumstances and larger down payments. Rebuilding credit during the waiting period improves qualification chances when ready to purchase again.

Do you owe money after a short sale?

It depends on whether the lender agrees to a deficiency waiver. Without a waiver, lenders can pursue the remaining balance through deficiency judgments. Some states prohibit deficiency judgments on primary residence purchase-money mortgages. Always negotiate a deficiency waiver as part of the short sale approval and obtain written confirmation.

How long does a short sale take in 2025?

The typical short sale timeline ranges from 3-6 months from initial lender contact to closing. Factors affecting duration include documentation completeness, number of lien holders, lender processing speed, buyer qualification, and property condition. Complex situations with multiple liens or lender backlogs can extend the process to 9-12 months.

Can you do a short sale if you’re current on payments?

Some lenders accept short sale applications from current borrowers facing imminent hardship—situations where default is inevitable even though payments are currently being made. Examples include upcoming job loss, medical diagnosis affecting income, or ARM adjustment making future payments unaffordable. Lender policies vary; some require actual delinquency before considering short sales.

What happens if the lender denies the short sale?

If the lender denies the short sale, options include:

- Requesting reconsideration with additional documentation

- Finding a buyer willing to pay a higher price

- Pursuing alternative solutions (loan modification, deed in lieu)

- Allowing foreclosure to proceed

- Filing bankruptcy to delay foreclosure

Working with experienced professionals increases approval odds and provides alternative strategies if initial attempts are denied.

Conclusion: Taking Control of a Difficult Situation

Understanding how to do a short sale: complete step-by-step process [2025] empowers homeowners facing financial hardship to take control of their situation rather than becoming victims of foreclosure. While the process requires patience, thorough documentation, and expert guidance, it provides a dignified exit from an unaffordable property while minimizing credit damage and future financial impact.

The journey begins with honest assessment of the financial situation and early communication with the lender. Gathering complete documentation, working with experienced short sale professionals, and maintaining realistic expectations about timelines all contribute to successful outcomes. Remember that lenders prefer short sales to foreclosure—the mutual benefit creates opportunity for negotiated solutions.

Your Next Steps

If facing mortgage difficulties and considering a short sale, take these actions today:

- Assess your situation honestly – Calculate your property’s current value versus total debt

- Contact your lender immediately – Ask for the Loss Mitigation Department and request short sale information

- Consult with short sale specialists – Interview experienced agents with proven track records

- Gather documentation – Begin compiling financial records and drafting your hardship letter

- Explore all alternatives – Consider loan modification, forbearance, and other options alongside short sales

- Seek professional guidance – Consult with real estate attorneys and tax professionals about implications

For homeowners facing complex situations—properties with back taxes, multiple liens, inheritance issues, or unclear title—specialized companies like Sure Path Property Solutions provide the expert service and helpful guidance needed to navigate these challenging circumstances. Their friendly and caring approach, combined with deep industry expertise, helps property owners find practical solutions even in seemingly impossible situations.

The path forward may feel overwhelming, but trustworthy service from qualified professionals transforms the complex short sale process into manageable steps. Taking action today prevents worse outcomes tomorrow and opens the door to financial recovery and a fresh start.

Remember: facing financial hardship doesn’t reflect personal failure. Economic conditions, medical emergencies, job loss, and life changes affect millions of homeowners. What matters is responding responsibly, seeking helpful solutions, and moving forward with dignity. A short sale, when appropriate, provides exactly that opportunity.

References

[1] National Association of Realtors – Short Sale Processing Guidelines and Best Practices (2024)

[2] Experian Credit Bureau – Credit Impact Analysis: Short Sales vs. Foreclosures (2024)

[3] Federal Housing Finance Agency – Servicer Guidelines for Loss Mitigation and Short Sale Approvals (2024)

[4] Fannie Mae – Servicing Guide: Short Sale Timeline Requirements and Response Standards (2024)

[5] National Association of Realtors – Pricing Strategies for Distressed Property Sales (2024)

[6] Consumer Financial Protection Bureau – Understanding Short Sales: A Guide for Homeowners (2024)