How to Sell a House with a Lien: Step-by-Step Guide (2025)

![Professional landscape hero image (1536x1024) featuring bold text overlay 'How to Sell a House with a Lien: Step-by-Step Guide [2025]' in ex](https://zsxkvszxbhpwnvzxdydv.supabase.co/storage/v1/object/public/generated-images/kie/41f32d32-3644-43e9-b262-bc747716c5e2/slot-0-1765311067098.png)

Discovering a lien on your property when you’re ready to sell can feel like hitting a brick wall. The phone calls from potential buyers are coming in, you’ve mentally moved on to your next chapter, and suddenly you’re facing unexpected legal claims against your home. Here’s the good news: selling a house with a lien is absolutely possible, and thousands of homeowners successfully navigate this challenge every year.

Understanding how to sell a house with a lien on it doesn’t require a law degree or endless frustration. With helpful guidance and the right approach, you can clear these obstacles and move forward with your sale. This comprehensive guide walks through every step of the process, from identifying what type of lien you’re dealing with to successfully closing your sale and moving on.

Whether you’re facing tax liens, contractor claims, or judgment liens, this step-by-step guide for 2025 provides the expert service and practical solutions you need to sell your property confidently.

Key Takeaways

- Liens don’t prevent sales – You can sell a house with liens, but they must be satisfied before or at closing for the buyer to receive clear title

- Multiple payment options exist – Pay liens upfront, use sale proceeds at closing, or negotiate reduced settlements with creditors

- Professional help matters – Working with experienced real estate agents, title companies, and property solution experts streamlines the entire process

- Title searches reveal all liens – A comprehensive title search identifies every recorded claim against your property early in the process

- Documentation is critical – Obtaining payoff letters and lien release documents ensures proper legal clearance and protects all parties

Understanding Property Liens and How They Affect Your Sale

A property lien represents a legal claim against your house by a creditor who is owed money. Think of it as a financial “hold” on your property that gives creditors security until their debt is paid. Creditors record these liens at the county clerk’s office to protect their interest and notify the world of their claim on the property[1].

When you attempt to sell house with liens, these claims don’t simply disappear. They attach to the property itself, not just to you as the owner. This means any buyer purchasing your home would inherit these financial obligations unless they’re cleared before the sale completes.

Why Liens Must Be Resolved Before Closing

The title must be cleared and all outstanding liens must be satisfied before the buyer can take possession[1]. Here’s why this non-negotiable requirement exists:

- Lenders won’t approve mortgages on properties with clouded titles

- Title insurance companies refuse coverage when liens remain unresolved

- Buyers face legal liability for inherited debts if liens transfer with the property

- Recording offices maintain public records that reveal all claims against the property

A title search will identify any liens recorded against your property, and the title company ensures all liens are satisfied at closing[1]. This protective measure benefits everyone involved in the transaction.

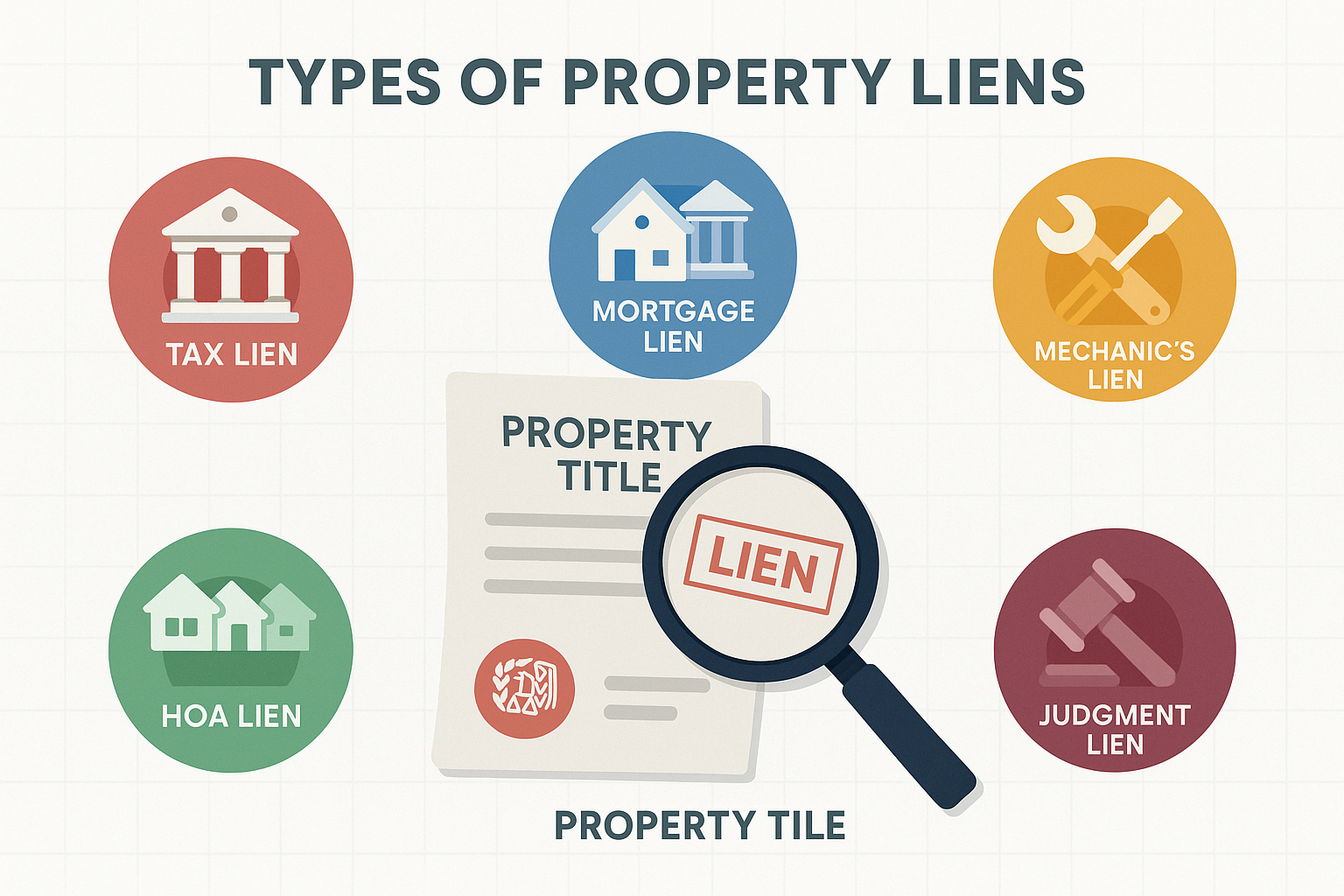

Common Types of Property Liens

Different lien types carry varying levels of urgency and priority:

| Lien Type | Description | Priority Level |

|---|---|---|

| Tax Liens | Government claims for unpaid property taxes, income taxes, or other tax debts | Highest (often supersedes other liens) |

| Mortgage Liens | Claims by your lender secured by the property itself | High (typically first or second position) |

| Mechanic’s Liens | Claims by contractors, subcontractors, or suppliers for unpaid work | Medium (based on filing date) |

| Judgment Liens | Court-ordered claims from lawsuit settlements or unpaid debts | Medium (varies by state) |

| HOA Liens | Homeowners association claims for unpaid dues or assessments | Medium to High (state-dependent) |

| IRS Liens | Federal tax liens for unpaid federal taxes | Highest (federal priority) |

For Texas properties specifically, a lien can be placed on property through a court judgment if you owe money to a creditor or from a personal injury claim[2]. Understanding which type of lien affects your property shapes your resolution strategy.

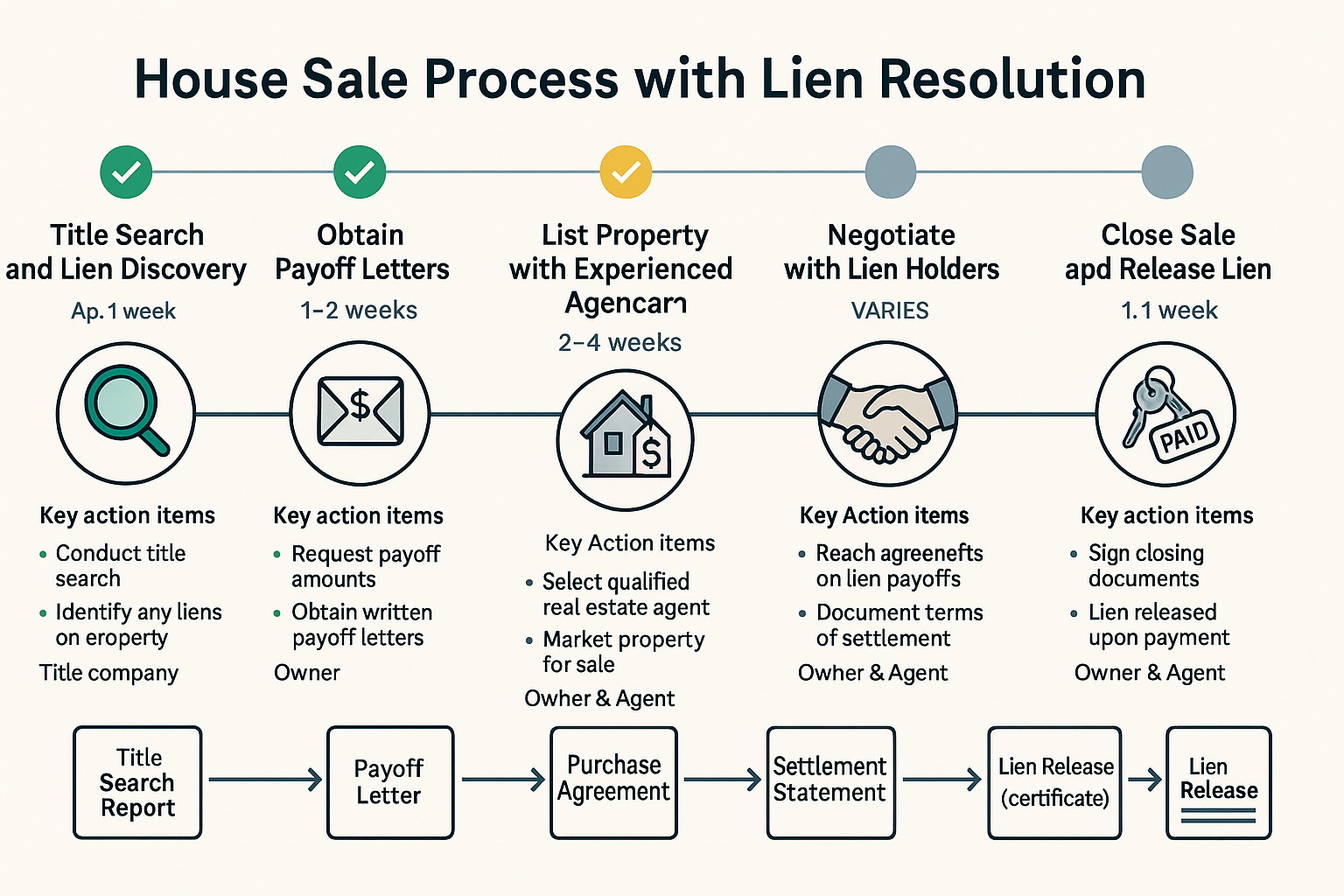

Step 1: Identify All Liens on Your Property

Before you can develop a plan for selling a house with a lien on it, you need a complete picture of what you’re dealing with. This discovery phase prevents surprises later and helps you budget appropriately for the sale.

Ordering a Comprehensive Title Search

The most reliable way to identify liens is through a professional title search. Title companies specialize in examining public records to uncover:

- ✅ All recorded liens against the property

- ✅ The lien holder’s name and contact information

- ✅ The original lien amount and filing date

- ✅ The lien’s priority position (which gets paid first)

- ✅ Any subordinate or junior liens

Cost and timeline: Title searches typically cost $75-$200 and take 3-5 business days to complete. This small investment provides invaluable clarity and prevents costly mistakes.

Checking County Records Yourself

For a preliminary investigation, visit your county clerk’s office or check their online portal. Most counties now offer digital access to recorded documents. Search for:

- Your property’s legal description or parcel number

- Your name as the property owner

- The property address

Look for documents labeled as “Notice of Lien,” “Abstract of Judgment,” “Lis Pendens,” or similar terms. Keep in mind that self-searches may miss liens recorded under variations of your name or property description.

Understanding Lien Priority and Payment Order

Not all liens are equal. Priority determines the order in which liens get paid from your sale proceeds. Generally, priority follows this hierarchy:

- Property tax liens (almost always first)

- First mortgage lien (the original purchase loan)

- Second mortgages or HELOCs (home equity loans)

- Mechanic’s liens (based on when work began)

- Judgment liens (based on recording date)

- Other liens (based on recording date)

“Understanding lien priority isn’t just academic—it directly affects whether you’ll have enough equity to sell your house and walk away with any proceeds.” — Real Estate Title Expert

In Texas, property liens must include a lawsuit filed within one year of the lien filing to proceed to foreclosure[5]. This provides some breathing room for property owners developing their resolution strategy.

Step 2: Determine the Exact Lien Amounts and Payoff Requirements

Knowing a lien exists is only half the battle. You need precise payoff figures to accurately calculate your home’s net equity and determine if a traditional sale makes financial sense.

Requesting Official Payoff Letters

A payoff letter (also called a payoff statement or demand letter) provides the exact amount required to satisfy the lien as of a specific date. This document is essential because:

- Interest and fees continue accumulating on most liens

- The original lien amount rarely matches the current payoff amount

- Creditors may have added penalties, attorney fees, or collection costs

- Payoff amounts include a “good through” date after which the figure changes

How to request a payoff letter:

- Contact the lien holder directly (phone number from title search)

- Provide your property address and lien reference number

- Explain you’re selling the property and need a payoff statement

- Request the letter include per diem interest (daily interest charges)

- Ask for a 30-60 day payoff window to accommodate closing timelines

Obtain a payoff letter from the creditor and provide it to your escrow agent, who will handle the lien payment from sale proceeds[1].

Calculating Total Lien Obligations

Once you’ve gathered payoff letters for all liens, create a comprehensive calculation:

Example Calculation:

- Primary mortgage payoff: $185,000

- Property tax lien: $12,500

- Contractor’s mechanic’s lien: $8,750

- HOA lien: $3,200

- Total lien obligations: $209,450

Now compare this to your home’s realistic market value:

- Estimated home value: $275,000

- Total liens: -$209,450

- Selling costs (6-8%): -$19,250

- Estimated net proceeds: $46,300

This calculation reveals whether selling through traditional means provides sufficient funds to clear all liens and cover transaction costs.

When Liens Exceed Property Value

If your liens total more than your home’s value, you’re facing an “underwater” or “upside-down” situation. Don’t panic—you still have options:

- Short sale: Negotiate with lien holders to accept less than owed

- Lien negotiation: Request reduced payoff amounts (covered in Step 4)

- Cash buyer sale: Work with investors who handle lien complications

- Bankruptcy consideration: Consult an attorney about Chapter 7 or 13

Sure Path Property Solutions specializes in these complex scenarios, offering helpful solutions when traditional sales aren’t viable. Our industry experts coordinate with counties and title professionals to find practical paths forward.

Step 3: Explore Your Payment Options for Clearing Liens

Understanding how to sell a house with a lien centers on one critical question: How will you pay off the liens? Fortunately, several viable pathways exist, each with distinct advantages depending on your financial situation.

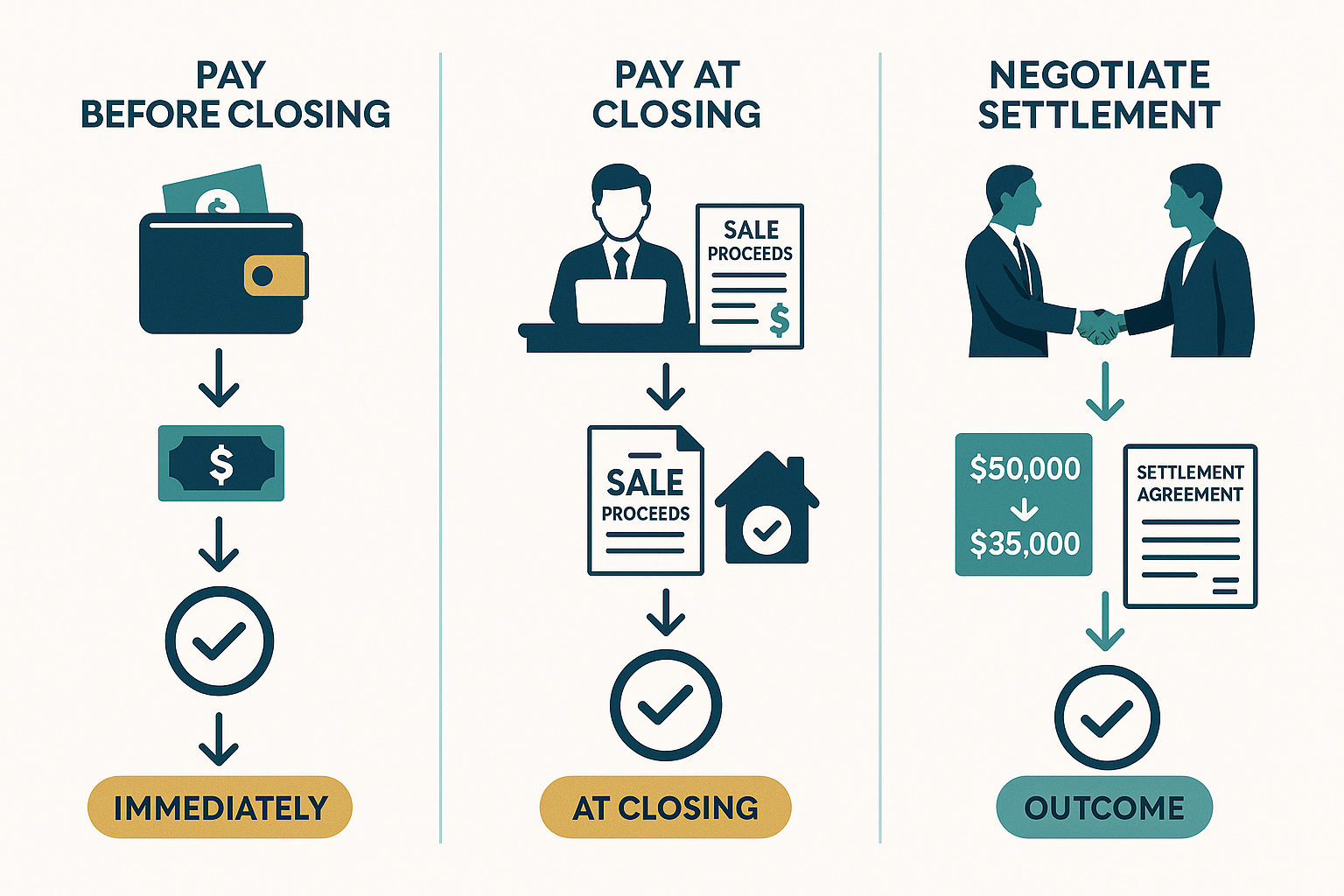

Option A: Pay Liens Before Listing the Property

The most straightforward approach to selling is paying the lien debt in full upfront, which clears the title immediately[1][2]. This strategy offers significant benefits:

Advantages:

- ✅ Clean title attracts more buyers and better offers

- ✅ Faster sales process without lien complications

- ✅ Stronger negotiating position

- ✅ No surprises at closing

- ✅ Simpler transaction for all parties

Disadvantages:

- ❌ Requires substantial cash reserves

- ❌ Money tied up before receiving sale proceeds

- ❌ Risk if sale falls through after paying liens

Best for: Homeowners with savings, access to personal loans, or family assistance who want the cleanest, fastest sale process.

Option B: Pay Liens at Closing Using Sale Proceeds

If you lack sufficient funds, you can use the sale proceeds to pay off the lien at closing, with the amount deducted from your home sale proceeds like other closing costs[1][3]. This is the most common approach for selling house with liens.

How it works:

- Provide payoff letters to your title company or closing attorney

- The title company calculates exact payoff amounts as of closing date

- At closing, proceeds are distributed in priority order:

- First: Property taxes and government liens

- Second: First mortgage

- Third: Secondary liens by priority

- Finally: Remaining proceeds to you as the seller

The escrow agent handles the lien payment from sale proceeds, ensuring creditors receive payment and file proper release documents[1].

Advantages:

- ✅ No upfront cash required from you

- ✅ Automated process managed by professionals

- ✅ Simultaneous payment and lien release

- ✅ Protected transaction with escrow oversight

Disadvantages:

- ❌ Reduces your net proceeds from the sale

- ❌ Requires sufficient equity to cover all liens

- ❌ May complicate buyer’s financing approval

- ❌ Longer closing process for lien coordination

Best for: Homeowners with adequate equity who need to use sale proceeds to satisfy liens.

Option C: Negotiate a Reduced Lien Payoff

Creditors are typically willing to negotiate based on the sale circumstances[1][4]. Many lien holders prefer receiving partial payment over lengthy collection processes or receiving nothing if you file bankruptcy.

Negotiation strategies:

- Lump sum discount: Offer immediate payment for 50-70% of the balance

- Financial hardship: Demonstrate inability to pay full amount

- Time value argument: Emphasize quick resolution versus years of collection efforts

- Competitive pressure: Mention other liens that take priority over theirs

Best for: Homeowners with limited equity, multiple liens, or financial hardship who need debt reduction to make the sale viable.

Creating Your Payment Strategy

Work with an experienced real estate agent who understands how the lien payment affects the asking price and ensures sufficient sale proceeds to cover both the mortgage and lien[3]. Your strategy should account for:

- Total lien amounts and priority order

- Your available cash reserves

- Home’s realistic market value

- Estimated selling costs (agent commissions, title fees, repairs)

- Your desired net proceeds

A professional agent with expertise in complicated real estate issues can model different scenarios and recommend the optimal approach for your situation.

Step 4: Negotiate with Lien Holders for the Best Resolution

Negotiating with creditors might seem intimidating, but remember: they want to get paid, and you’re offering them a concrete path to payment through your home sale. This shared interest creates room for productive discussions.

Preparing for Successful Negotiations

Before contacting lien holders, gather your documentation and develop your strategy:

Essential preparation steps:

- Document your financial situation with bank statements, income proof, and expense records

- Calculate maximum affordable payment based on realistic sale proceeds

- Research the creditor’s typical settlement patterns (some are more flexible than others)

- Prepare a written settlement proposal outlining your offer

- Identify your walk-away point if negotiations fail

Effective Negotiation Techniques

When contacting lien holders, use these proven approaches:

Start with empathy and honesty:

“I understand I owe this debt, and I want to resolve it. I’m selling my property and want to ensure you receive payment, but I need to discuss the payoff amount.”

Present concrete numbers:

“Based on my home’s value of $275,000 and my first mortgage of $185,000, I have approximately $70,000 in equity before selling costs. With your lien and two others totaling $24,000, I’m asking if you’d accept $X to settle this matter.”

Emphasize mutual benefits:

“Accepting this settlement gives you immediate payment without further collection costs or the risk of bankruptcy, where you might receive significantly less or nothing.”

Request written confirmation:

“If you agree to this settlement amount, I’ll need a written agreement stating that payment of $X fully satisfies the lien, with no remaining balance.”

Getting Settlement Agreements in Writing

Never rely on verbal agreements. Insist on written documentation that includes:

- ✅ Original lien amount and reference number

- ✅ Agreed settlement amount

- ✅ Statement that payment constitutes “full and final settlement”

- ✅ Commitment to file lien release within specific timeframe

- ✅ Authorized signature from someone with settlement authority

- ✅ Contact information for follow-up

Once a lien is paid, obtain a recorded lien release document (also called satisfaction of mortgage, lien discharge, or lien termination) proving the debt is satisfied[1].

Special Considerations for Different Lien Types

Different creditors have varying flexibility:

Tax liens (IRS, state, county): Government liens rarely negotiate on amount but may offer payment plans or subordination agreements allowing the sale to proceed.

Mechanic’s liens: Contractors often negotiate, especially if the work was disputed or the amount includes inflated costs.

Judgment liens: Creditors who’ve already won lawsuits may be more rigid, but many still prefer settlement over continued collection efforts.

HOA liens: Homeowners associations typically require full payment of dues but may waive some penalties and interest.

To release a lien in Texas, the lienholder must sign a Release of Lien, Lien Release, or Deed of Reconveyance document to officially remove the lien[2]. Ensure you understand your state’s specific requirements.

Step 5: Work with Your Title Company and Real Estate Professionals

Successfully selling a house with a lien on it requires coordination among multiple professionals. The title company serves as the central hub, ensuring all legal requirements are met and all parties receive proper payment.

The Title Company’s Critical Role

Title companies provide essential services throughout the lien resolution process:

Pre-closing services:

- Conducting comprehensive title searches

- Identifying all liens and encumbrances

- Calculating exact payoff amounts as of closing date

- Coordinating with lien holders for payoff instructions

- Preparing settlement statements showing all disbursements

At closing:

- Holding funds in escrow for secure distribution

- Disbursing payments to lien holders in priority order

- Ensuring all parties sign required documents

- Recording the deed transfer and lien releases

- Issuing title insurance to the buyer

Post-closing:

- Following up on lien release recordings

- Providing copies of all recorded documents

- Resolving any post-closing title issues

The title company ensures all liens are satisfied at closing[1], protecting both you and the buyer from future claims.

Choosing the Right Real Estate Agent

Not all agents have experience with complicated property situations. When selling house with liens, seek an agent who demonstrates:

- Proven experience with lien sales and complex transactions

- Strong relationships with title companies and attorneys

- Realistic pricing strategy that accounts for lien obligations

- Excellent communication to keep you informed throughout the process

- Problem-solving skills when unexpected issues arise

- Patience and persistence through extended timelines

An experienced agent understands how the lien payment affects the asking price and ensures sufficient sale proceeds to cover both the mortgage and lien[3]. They’ll help you price the property to attract buyers while ensuring adequate equity for lien satisfaction.

Coordinating with Attorneys When Necessary

Some lien situations benefit from legal counsel:

- Multiple complex liens with priority disputes

- Litigation-related liens requiring court involvement

- Foreclosure proceedings already initiated

- Title defects beyond standard liens

- Bankruptcy considerations affecting lien treatment

Sure Path Property Solutions maintains relationships with experienced real estate attorneys who provide helpful guidance through these complicated scenarios. Our trustworthy service includes coordinating all necessary professionals to guide property owners toward clear, practical solutions.

Creating a Professional Team Timeline

Coordinate your team with a clear timeline:

| Week | Activity | Responsible Party |

|---|---|---|

| 1-2 | Title search and lien identification | Title Company |

| 2-3 | Obtain payoff letters | Seller/Agent |

| 3-4 | Negotiate lien reductions | Seller/Attorney |

| 4-5 | List property | Real Estate Agent |

| 5-8 | Marketing and showings | Real Estate Agent |

| 8-9 | Accept offer and open escrow | Agent/Title Company |

| 9-10 | Buyer inspections and financing | Buyer/Lender |

| 10-11 | Final lien payoff coordination | Title Company |

| 11-12 | Closing and lien satisfaction | All Parties |

This timeline assumes no major complications. Complex situations may require additional time, particularly for lien negotiations or title issues.

Step 6: Successfully Close Your Sale and Obtain Lien Releases

The closing process for a house with liens requires extra attention to detail, but with proper preparation, it proceeds smoothly and results in a clean transfer of ownership.

Preparing for Closing Day

In the days before closing, confirm these critical items:

Documentation checklist:

- ✅ All payoff letters with current amounts

- ✅ Written settlement agreements (if liens were negotiated)

- ✅ Government-issued ID

- ✅ Property keys and garage door openers

- ✅ HOA documents and contact information

- ✅ Utility account information for final readings

- ✅ Forwarding address for remaining proceeds

Financial preparation:

- Review the settlement statement (HUD-1 or Closing Disclosure) carefully

- Verify all lien payoff amounts match your payoff letters

- Confirm the distribution priority is correct

- Calculate your expected net proceeds

- Arrange wire transfer information if proceeds exceed check limits

Understanding the Closing Settlement Statement

Your settlement statement itemizes every dollar in the transaction:

Example Settlement Statement (Simplified):

SALE PRICE: $275,000.00

SELLER DEBITS (amounts you owe):

First Mortgage Payoff -$185,000.00

Property Tax Lien Payoff -$12,500.00

Mechanic's Lien Payoff -$8,750.00

HOA Lien Payoff -$3,200.00

Real Estate Commission (6%) -$16,500.00

Title Insurance (seller portion) -$1,250.00

Recording Fees -$175.00

Prorated Property Taxes -$850.00

Transfer Tax -$1,375.00

____________

TOTAL SELLER DEBITS: -$229,600.00

NET PROCEEDS TO SELLER: $45,400.00

Review this document carefully and ask questions about any items you don’t understand. The title company should explain each line item clearly.

Ensuring Proper Lien Release Documentation

Payment alone doesn’t remove liens from public records. You must obtain and record official release documents.

Critical lien release requirements:

- Immediate release: Request the lien holder provide a signed release at closing or within 24-48 hours

- Proper format: The release must meet your state’s legal requirements (in Texas, this is a Release of Lien, Lien Release, or Deed of Reconveyance[2])

- Recording: The release must be recorded with the same county office where the original lien was filed

- Verification: Confirm recording by checking county records 2-3 weeks after closing

Once a lien is paid, obtain a recorded lien release document proving the debt is satisfied[1]. Keep copies of all release documents permanently in your records.

What Happens If a Lien Holder Doesn’t Release?

Occasionally, lien holders delay filing releases despite receiving payment. If this occurs:

- Contact the lien holder immediately with proof of payment

- Request the title company intervene on your behalf

- Send a formal demand letter (via certified mail) requiring release within 30 days

- File a complaint with your state’s attorney general or consumer protection office

- Consult an attorney about legal remedies, including potential damages for wrongful refusal

Most states impose penalties on creditors who fail to release liens after receiving payment, giving you legal recourse if necessary.

Post-Closing Follow-Up

After closing, complete these final steps:

- Verify lien releases were recorded by checking county records online

- Obtain copies of all recorded documents from the title company

- Keep permanent records of the entire transaction

- Update your credit reports to reflect satisfied liens (may take 30-60 days)

- Notify relevant parties of your address change

Congratulations! You’ve successfully navigated the complex process of selling a house with liens and can now move forward to your next chapter.

Real-World Case Studies: Successful Lien Resolutions

Learning from others who’ve successfully sold properties with liens provides valuable insights and encouragement. Here are three real examples demonstrating different approaches:

Case Study #1: Tax Lien Resolution Through Sale Proceeds

Situation: Maria inherited a house in Houston with $18,500 in delinquent property taxes spanning three years. She didn’t have cash to pay the lien but needed to sell quickly to settle the estate among four heirs.

Solution: Maria worked with a real estate agent experienced in tax lien sales. They:

- Ordered a title search confirming only the tax lien existed

- Obtained a payoff letter from the county tax office

- Priced the property accounting for the lien payoff

- Listed the home with full disclosure of the tax situation

- Found a cash buyer willing to close quickly

- Used sale proceeds to pay the tax lien at closing

Outcome: The property sold for $195,000. After paying the $18,500 tax lien, $7,800 in selling costs, and distributing the remaining $168,700 among the four heirs, each received $42,175. The entire process took 47 days from listing to closing.

“I thought the tax lien would prevent us from selling, but our agent showed us it was just another closing cost. The helpful guidance made a stressful situation manageable.” — Maria H.

Case Study #2: Multiple Lien Negotiation

Situation: Robert faced foreclosure on a property with a $142,000 mortgage, a $23,000 second mortgage, and a $9,500 contractor’s lien from disputed work. The property’s value was only $165,000, leaving insufficient equity to pay all liens and selling costs.

Solution: Robert contacted Sure Path Property Solutions for expert service. The team:

- Conducted a comprehensive title search revealing all three liens

- Negotiated with the second mortgage holder, securing a settlement for $11,500 (50% reduction)

- Disputed the mechanic’s lien amount, negotiating down to $6,000 (37% reduction)

- Coordinated a short sale with the first mortgage lender

- Found a buyer willing to purchase despite the complexity

Outcome: Through professional negotiation and coordination, Robert avoided foreclosure and resolved all liens. While he received no proceeds, he eliminated $175,500 in debt and protected his credit from foreclosure damage. The alternative—foreclosure—would have resulted in a deficiency judgment for the remaining balance.

Case Study #3: Pre-Sale Lien Payment Strategy

Situation: Jennifer and Tom wanted to sell their home to relocate for work. They discovered a $7,200 HOA lien for unpaid dues and special assessments they’d disputed. They had savings and wanted the cleanest possible sale.

Solution: The couple chose to pay the lien before listing:

- Negotiated with the HOA, reducing penalties from $1,800 to $600

- Paid the $6,000 settlement from savings

- Obtained and recorded the lien release before listing

- Listed the property with a clear title

Outcome: The property sold in 12 days for $15,000 over asking price. The clean title attracted multiple offers and eliminated buyer financing concerns. Their net proceeds were $89,300 after all costs—significantly more than if they’d disclosed the lien and paid it at closing, which likely would have reduced buyer interest and offers.

Frequently Asked Questions About Selling Houses with Liens

Can I sell my house if it has a lien on it?

Yes, absolutely. You can sell a house with liens, but the liens must be satisfied before or at closing for the buyer to receive clear title[1]. The sale can proceed as long as sufficient proceeds exist to pay the liens, or you arrange alternative payment.

What if I don’t have enough equity to pay off all the liens?

You have several options:

- Negotiate reduced payoffs with lien holders

- Pursue a short sale (if the first mortgage holder agrees)

- Bring cash to closing to cover the shortage

- Sell to a cash buyer or investor who specializes in lien situations

- Work with companies like Sure Path Property Solutions that handle complex scenarios

How long does it take to sell a house with a lien?

The timeline varies based on complexity:

- Simple single lien: 45-60 days (similar to standard sales)

- Multiple liens requiring negotiation: 90-120 days

- Complex situations with disputes: 120-180 days

Starting the process early and working with experienced professionals minimizes delays.

Do I need to disclose liens to potential buyers?

Yes, in most states you’re legally required to disclose known liens. However, the title search will reveal them anyway, so transparency builds trust and prevents deals from falling apart during due diligence.

Will a lien on my house affect my credit?

Many liens (especially tax liens and judgment liens) already appear on your credit report. Successfully paying them through your home sale typically improves your credit over time as the liens are marked “satisfied” or “released.”

Can a buyer assume my liens instead of me paying them?

This is extremely rare. Most buyers won’t accept a property with existing liens because:

- Lenders won’t approve mortgages on properties with clouded titles

- They’d become responsible for debts they didn’t incur

- Title insurance won’t be available

The only exception might be certain assumable mortgage situations, but even these require lender approval.

When to Seek Professional Help: Sure Path Property Solutions

Some lien situations exceed the scope of traditional real estate transactions. If you’re facing any of these circumstances, professional assistance can make the difference between success and failure:

Situations Requiring Expert Intervention

- Multiple overlapping liens creating priority disputes

- Liens exceeding property value requiring complex negotiations

- Inherited properties with unknown or disputed liens

- Properties with multiple owners who disagree on resolution strategy

- Tax liens with pending foreclosure requiring immediate action

- Title defects beyond standard liens

- Properties you can’t sell traditionally due to condition or lien complications

How Sure Path Property Solutions Helps

Sure Path Property Solutions specializes in helping owners navigate complicated real estate issues—back taxes, multiple heirs, liens, judgments, or unclear title. The company provides:

Comprehensive lien resolution services:

- Complete title research identifying all claims

- Coordination with counties and title professionals

- Negotiation with multiple lien holders simultaneously

- Creative solutions when traditional sales aren’t viable

- Direct purchase options for properties others won’t buy

The Sure Path difference:

- ✅ Industry experts with decades of combined experience

- ✅ Friendly and caring approach to stressful situations

- ✅ Helpful solutions tailored to your specific circumstances

- ✅ Trustworthy service with transparent communication

- ✅ Practical guidance toward clear resolution

Getting Started with Professional Help

If your situation feels overwhelming, reach out for a no-obligation consultation. Sure Path Property Solutions offers:

- Free property evaluation to understand your specific situation

- Comprehensive lien analysis identifying all claims and options

- Multiple solution pathways including traditional sale assistance or direct purchase

- Coordination of all professionals needed for resolution

- Clear timeline and expectations so you know what to expect

The company’s expert service simplifies complex situations and guides property owners toward practical solutions, even when the path forward seems unclear.

Conclusion: Your Path Forward to Successfully Selling Your House with a Lien

Selling a house with a lien doesn’t have to derail your plans or create endless frustration. As this comprehensive guide demonstrates, thousands of homeowners successfully navigate this process every year by following a systematic approach and working with the right professionals.

Your Action Plan Summary

Here’s your roadmap for moving forward:

Immediate next steps (Week 1-2):

- Order a comprehensive title search to identify all liens

- Request payoff letters from all lien holders

- Calculate your total obligations versus property value

- Decide whether to pursue traditional sale, negotiation, or professional assistance

Short-term actions (Week 3-6):

5. Interview and select an experienced real estate agent (or contact Sure Path Property Solutions for complex situations)

6. Begin lien negotiations if needed

7. Develop your pricing strategy accounting for lien obligations

8. Prepare the property for sale

Closing phase (Week 7-12+):

9. List the property or accept a direct offer

10. Coordinate with title company on lien payoffs

11. Review settlement statements carefully

12. Close the sale and obtain lien release documents

Remember These Key Principles

✅ Liens are obstacles, not roadblocks – With the right approach, they can be overcome

✅ Professional help accelerates success – Experienced agents, title companies, and solution providers like Sure Path Property Solutions provide invaluable expertise

✅ Negotiation often works – Many lien holders prefer reduced payment over lengthy collection processes

✅ Documentation protects everyone – Insist on written agreements and proper lien releases

✅ Multiple pathways exist – If one approach doesn’t work, alternatives are available

Take the First Step Today

The longest journey begins with a single step. Whether you choose to tackle this process independently or seek helpful guidance from industry experts, taking action today moves you closer to resolution.

If you’re facing complicated real estate issues—back taxes, multiple heirs, liens, judgments, or unclear title—Sure Path Property Solutions stands ready to provide friendly and caring support. The company’s trustworthy service and expert guidance help property owners find clear, practical solutions even in the most challenging situations.

Don’t let liens keep you trapped in a property you need to sell. With the step-by-step approach outlined in this guide and the right professional support, you can successfully sell your house with a lien and move forward to your next chapter with confidence.

Ready to explore your options? Contact Sure Path Property Solutions today for a free, no-obligation consultation about your specific situation. The path to resolution is clearer than you think.

References

[1] Title company procedures and lien satisfaction requirements in real estate transactions

[2] Texas Property Code provisions regarding lien placement, requirements, and release procedures

[3] Real estate agent best practices for pricing and selling properties with lien encumbrances

[4] Creditor negotiation strategies and settlement practices in real estate transactions

[5] Texas foreclosure law requirements for liens, including lawsuit filing timelines