Sell House to Pay Off Judgment: We Handle the Payoff

When a court judgment threatens your home equity and peace of mind, the stress can feel overwhelming. Legal notices pile up, creditors make demands, and the uncertainty of losing your property through forced sale keeps you awake at night. But here’s the truth: you have more control than you might think. Selling your house to pay off a judgment can be a strategic, voluntary decision that protects your remaining equity and gives you a fresh start.

At Sure Path Property Solutions, we specialize in helping homeowners navigate exactly this situation. We understand that judgments happen to good people facing difficult circumstances—medical debt, business disputes, divorce settlements, or unexpected financial hardships. Our expert service takes the complexity out of the process, coordinating directly with creditors, title companies, and courts to ensure your judgment gets satisfied while you walk away with any remaining equity in your pocket.

Key Takeaways

- Voluntary sales preserve more equity than waiting for forced execution sales or sheriff’s auctions

- Judgment liens must be satisfied at closing, but title companies routinely handle these payoffs from sale proceeds

- Homestead exemptions in many states protect a portion of your home equity from judgment creditors

- Cash buyers can close in 7-14 days, providing fast relief from judgment pressure without repairs or traditional listing delays

- Professional coordination between buyers, title companies, and creditors ensures clean title transfer and proper lien release

Understanding Judgment Liens on Your Property

A judgment lien represents a legal claim against your property following a court ruling in favor of a creditor. When someone sues you and wins, they don’t automatically get access to your house. They must take additional legal steps to secure their judgment against your real estate.

How Judgment Liens Attach to Real Estate

The process typically follows this sequence:

- Creditor files lawsuit and serves you with legal papers

- Court issues judgment after trial or default

- Creditor records judgment with the county recorder’s office

- Lien attaches to any real property you own in that county

Once recorded, the judgment lien becomes part of your property’s public record. It shows up on title searches and must be addressed before you can sell or refinance your home.

Important distinction: A judgment lien is different from a mortgage lien. Mortgage liens are voluntary (you agreed to them when buying your home), while judgment liens are involuntary—imposed by court order.

Types of Judgments That Create Property Liens

Several types of legal judgments can result in liens against your house:

| Judgment Type | Common Sources | Typical Amounts |

|---|---|---|

| Credit Card Debt | Unpaid balances, collection lawsuits | $5,000 – $50,000 |

| Medical Debt | Hospital bills, emergency care | $10,000 – $200,000+ |

| Business Disputes | Contract breaches, partnership dissolution | $25,000 – $500,000+ |

| Personal Injury | Auto accidents, premises liability | $50,000 – $1,000,000+ |

| Divorce Settlements | Property division, support obligations | Varies widely |

| HOA Assessments | Unpaid fees, special assessments | $2,000 – $30,000 |

Each type carries different legal implications, but all create similar challenges when you need to sell your property.

Priority of Liens: What Gets Paid First

Understanding lien priority is crucial when selling a house to satisfy a judgment. Not all liens are equal in the payoff hierarchy.

Standard priority order:

- Property tax liens (almost always first priority)

- First mortgage lien (recorded first in time)

- Second mortgage or HELOC (if applicable)

- Judgment liens (typically subordinate to mortgages)

- HOA liens (varies by state)

- Mechanic’s liens (construction-related)

This priority determines the order creditors get paid from your sale proceeds. If your home sells for $300,000 but you owe $250,000 on your mortgage and have a $75,000 judgment, the mortgage gets paid first, leaving $50,000 to partially satisfy the judgment.

“Understanding lien priority helped me realize I could still walk away with some money after paying off my mortgage and the judgment. I thought I’d lose everything.” — Former client, Dallas, TX

For homeowners dealing with multiple liens on their property, the priority structure becomes even more complex, requiring expert guidance to navigate successfully.

The Reality of Forced Sale: What Happens If You Don’t Act

Many homeowners worry that a judgment automatically means losing their home. While creditors do have legal remedies to collect, the process isn’t immediate or inevitable.

Timeline of Judgment Enforcement

Creditors cannot simply seize your house the day after winning a judgment. The enforcement process involves multiple legal steps:

Typical enforcement timeline:

- Months 0-3: Judgment recorded; creditor sends demand letters

- Months 3-6: Creditor may attempt wage garnishment or bank levies

- Months 6-12: If insufficient assets, creditor files for writ of execution

- Months 12-18: Sheriff’s sale scheduled (varies significantly by state)

- Months 18-24+: Actual forced sale execution

This extended timeline gives homeowners opportunities to take control through voluntary sale. Waiting until the last minute, however, significantly reduces your options and remaining equity.

Homestead Exemptions: Your Legal Protection

Most states provide homestead exemptions that protect a portion of your home equity from judgment creditors. These exemptions vary dramatically by location:

Homestead exemption examples (2026):

- Florida: Unlimited for primary residence (with acreage limits)

- Texas: Unlimited for primary residence (with acreage limits)

- California: $300,000 – $600,000 depending on circumstances

- New York: $165,550 – $550,000 depending on county

- Georgia: $21,500 per person

- Pennsylvania: None (no homestead exemption)

If your home equity falls below the exemption threshold, judgment creditors may not be able to force a sale at all. However, the lien remains attached to your property, creating problems when you eventually want to sell or refinance.

The Cost of Waiting: Accumulating Interest and Fees

Judgments don’t remain static. They grow over time through:

- Post-judgment interest (typically 4-10% annually, depending on state)

- Attorney fees for collection efforts

- Court costs for enforcement proceedings

- Sheriff’s fees if execution sale occurs

A $50,000 judgment can easily become $65,000 or more within just a few years of inaction. Taking proactive steps to sell your house with a judgment against it stops this financial bleeding.

Why Selling Voluntarily Makes Financial Sense

Choosing to sell your house on your own terms—rather than waiting for forced sale—offers significant advantages that protect your financial future.

Preserving Your Equity Through Strategic Sale

Forced sales through sheriff’s auctions typically yield 60-80% of fair market value. Voluntary sales through traditional or cash buyer channels typically achieve 90-100% of market value (or fair cash value for as-is condition).

Example equity comparison:

House fair market value: $350,000

Mortgage balance: $220,000

Judgment amount: $60,000

Scenario 1: Sheriff’s Auction (forced sale)

- Sale price: $245,000 (70% of value)

- Mortgage payoff: -$220,000

- Judgment payoff: -$25,000 (partial)

- Remaining to homeowner: $0

- Deficiency judgment: $35,000 (still owed)

Scenario 2: Voluntary Cash Sale

- Sale price: $315,000 (90% as-is value)

- Mortgage payoff: -$220,000

- Judgment payoff: -$60,000

- Closing costs: -$5,000

- Remaining to homeowner: $30,000

- Deficiency judgment: $0

The difference is substantial. Voluntary sale preserves equity and avoids ongoing liability.

Avoiding Additional Legal Costs and Complications

Once creditors begin enforcement proceedings, additional costs accumulate rapidly:

- Writ of execution filing: $500 – $1,500

- Sheriff’s fees: $1,000 – $3,000

- Publication costs: $300 – $800

- Attorney fees (creditor’s): $2,000 – $10,000+

These costs get added to your judgment balance, reducing your equity further. Voluntary sale eliminates these unnecessary expenses entirely.

Controlling the Timeline and Terms

When you initiate the sale process, you maintain control over:

✅ When to sell (before additional interest accumulates)

✅ How to sell (traditional listing vs. cash buyer)

✅ Property preparation (repairs, staging, or as-is)

✅ Buyer selection (best offer vs. fastest close)

✅ Moving timeline (coordinated to your needs)

This control reduces stress and allows you to plan your next steps thoughtfully rather than reacting to court deadlines and sheriff’s schedules.

For homeowners facing judgment liens in Florida, understanding state-specific timelines and exemptions becomes particularly important when planning a strategic voluntary sale.

How the Judgment Payoff Process Works at Closing

The mechanics of paying off a judgment through property sale are well-established and routine for title companies. Understanding the process removes much of the mystery and anxiety.

The Title Company’s Critical Role

Title companies serve as neutral third parties that ensure all liens get properly satisfied before ownership transfers to the buyer. Their responsibilities include:

Pre-closing activities:

- Conducting comprehensive title search

- Identifying all recorded liens and judgments

- Calculating exact payoff amounts (including per diem interest)

- Requesting payoff letters from judgment creditors

- Preparing settlement statements showing all distributions

At closing:

- Collecting sale proceeds from buyer

- Disbursing funds according to lien priority

- Obtaining lien releases and satisfactions

- Recording deed transfer and lien releases

- Providing final settlement statement to all parties

This professional coordination means you don’t negotiate directly with judgment creditors or handle complex legal paperwork. The title company manages everything according to established legal protocols.

Required Documentation for Judgment Payoff

To facilitate smooth closing, title companies typically require:

📄 Certified copy of judgment (from court records)

📄 Payoff statement from judgment creditor

📄 Satisfaction of judgment form (prepared for recording)

📄 W-9 form from creditor (for tax reporting)

📄 Wire instructions or check delivery details

📄 Authorization from seller to pay from proceeds

Experienced cash buyers like Sure Path Property Solutions coordinate with title companies to gather these documents efficiently, minimizing delays and ensuring accurate payoffs.

Settlement Statement: Where Your Money Goes

The HUD-1 or closing disclosure shows exactly how sale proceeds get distributed. Here’s a typical breakdown:

Sample settlement statement:

| Item | Amount |

|---|---|

| Gross sale price | $300,000 |

| First mortgage payoff | -$195,000 |

| Judgment lien payoff | -$52,000 |

| Property taxes (prorated) | -$1,800 |

| Title insurance | -$1,200 |

| Recording fees | -$300 |

| HOA transfer fees | -$250 |

| Net proceeds to seller | $49,450 |

This transparency ensures everyone understands exactly where funds are allocated and confirms proper satisfaction of all liens.

Obtaining Lien Release Documentation

After the judgment gets paid, obtaining proper release documentation is essential. The title company typically handles this, but sellers should verify:

✅ Satisfaction of judgment recorded with county

✅ Release of lien notation on property records

✅ Confirmation letter from creditor acknowledging full payment

✅ Updated credit report showing satisfied judgment (may take 30-60 days)

These documents prove the judgment has been satisfied and protect against future collection attempts. Keep copies permanently in your records.

When working with companies that specialize in buying houses with judgment liens, they typically ensure all release documentation gets properly completed and recorded as part of their standard closing process.

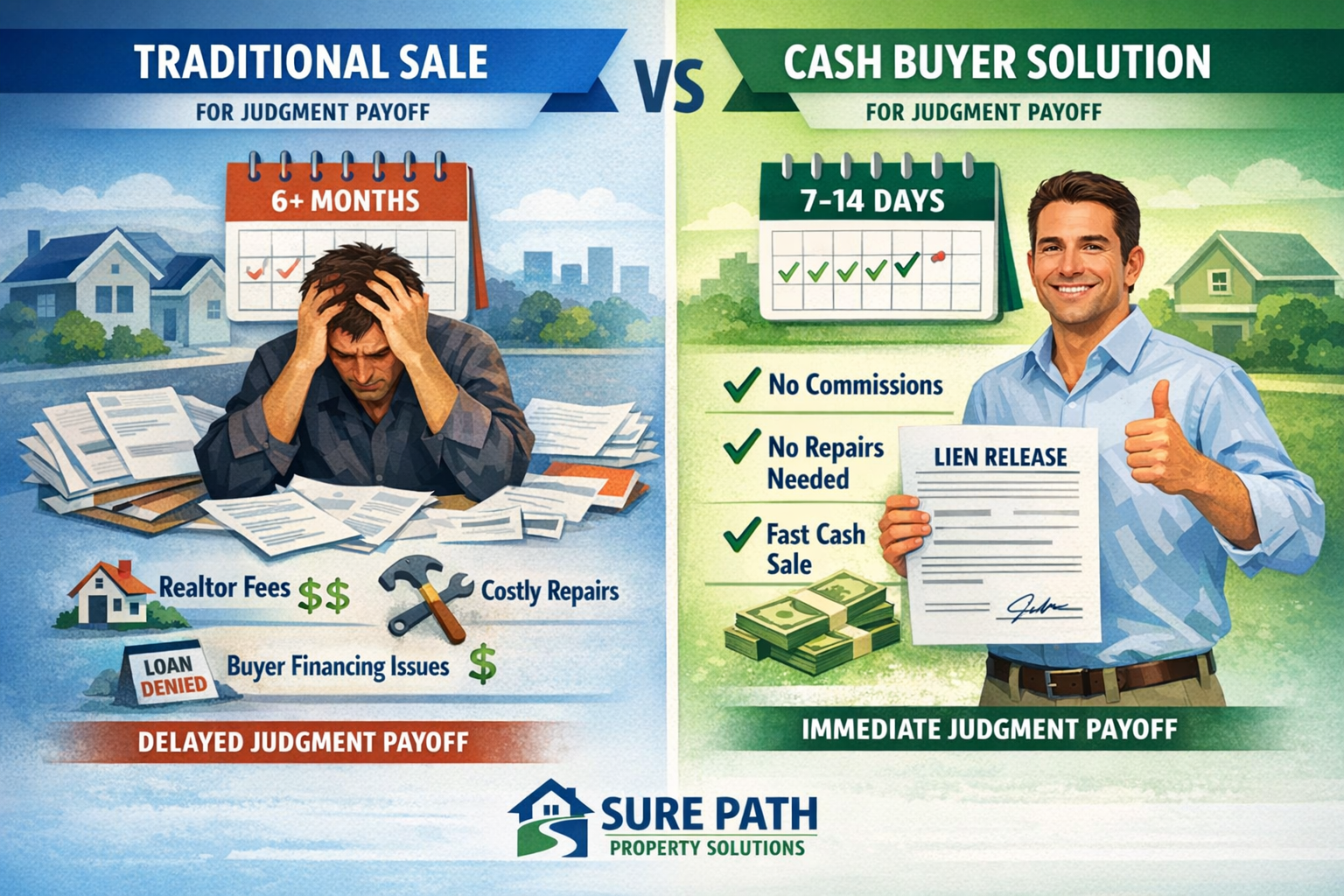

Sell House to Pay Off Judgment: Traditional Sale vs. Cash Buyer

Homeowners facing judgment liens have two primary paths for voluntary sale: traditional listing with a real estate agent or direct sale to a cash buyer. Each approach offers distinct advantages depending on your circumstances.

Traditional Listing: Timeline and Challenges

Selling through a real estate agent involves the familiar process most homeowners understand:

Traditional sale timeline:

- Week 1-2: Interview agents, sign listing agreement

- Week 2-4: Property preparation, repairs, staging

- Week 4-8: Active marketing, showings, open houses

- Week 8-12: Offer negotiation, buyer financing approval

- Week 12-18: Inspection, appraisal, title work, closing

Total timeline: 3-6 months (or longer in slow markets)

Challenges with judgment liens:

❌ Disclosure requirements may deter traditional buyers

❌ Financing complications if judgment affects title insurability

❌ Buyer concerns about lien payoff coordination

❌ Appraisal issues if property needs repairs

❌ Deal failures if buyer financing falls through

❌ Accumulating interest on judgment during extended marketing

Traditional sales work best when you have time, your property is in good condition, and you want to maximize sale price in a strong market.

Cash Buyer Solution: Speed and Simplicity

Cash buyers like Sure Path Property Solutions offer a dramatically different approach designed specifically for complicated situations:

Cash buyer timeline:

- Day 1: Contact buyer, describe situation

- Day 2-3: Property evaluation (often virtual)

- Day 3-5: Receive written cash offer

- Day 5-7: Accept offer, open escrow

- Day 7-21: Title work, judgment payoff coordination, closing

Total timeline: 7-21 days from initial contact to closing

Advantages for judgment situations:

✅ No repairs required (sold as-is)

✅ No showings or staging needed

✅ No buyer financing to fall through

✅ Expert lien coordination included

✅ Minimal interest accumulation due to speed

✅ Certainty of closing (no contingencies)

✅ Professional guidance through complex payoffs

The trade-off is typically receiving 70-85% of retail market value. However, when you factor in repair costs, agent commissions (5-6%), holding costs, and continued judgment interest, the net proceeds often compare favorably—while delivering certainty and speed.

Cost Comparison: All-In Analysis

Understanding total costs helps you make informed decisions:

Traditional sale costs:

- Agent commission: 5-6% ($15,000-$18,000 on $300k sale)

- Repairs/improvements: $5,000-$25,000

- Staging: $2,000-$5,000

- Holding costs (6 months): $3,000-$6,000

- Closing costs: $2,000-$4,000

- Judgment interest (6 months): $1,500-$3,000

- Total costs: $28,500-$61,000

Cash buyer sale costs:

- Agent commission: $0

- Repairs/improvements: $0

- Staging: $0

- Holding costs (2 weeks): $200-$400

- Closing costs: $1,000-$2,000 (often covered by buyer)

- Judgment interest (2 weeks): $100-$200

- Total costs: $1,300-$2,600

The cash buyer discount (typically 10-30% below retail) must be weighed against these substantial cost savings and the certainty of closing.

When Each Option Makes Sense

Choose traditional listing when:

- Property is in excellent condition

- You have 4-6 months available

- Market conditions strongly favor sellers

- Judgment amount is small relative to equity

- You want to maximize gross sale price

Choose cash buyer when:

- Time pressure exists (enforcement proceedings advancing)

- Property needs significant repairs

- You want certainty and speed

- Judgment interest is accumulating rapidly

- You prefer simplicity over maximum price

- Traditional buyers are deterred by lien complexity

For many homeowners, the peace of mind and speed of working with cash buyers who specialize in lien payoffs outweighs the potential for slightly higher proceeds through traditional sale.

We Handle the Payoff: What This Really Means

When Sure Path Property Solutions says “we handle the payoff,” this isn’t marketing language—it’s a comprehensive service that removes the burden from your shoulders.

Coordinating with Judgment Creditors

Our expert service includes direct communication with your judgment creditors to:

🤝 Verify exact payoff amounts including all interest and fees

🤝 Negotiate payoff terms when appropriate

🤝 Request payoff letters with per diem interest calculations

🤝 Coordinate payment timing to minimize interest

🤝 Obtain satisfaction documents immediately upon payment

🤝 Confirm release recording with county offices

This coordination eliminates the stress of dealing directly with creditors who may be adversarial or difficult to work with. Our industry experts understand the legal requirements and have established relationships with title companies and creditors.

Working with Title Companies and Attorneys

Complex lien situations require experienced title professionals. We partner with title companies that specialize in:

⚖️ Curative title work for complicated lien scenarios

⚖️ Multi-lien priority analysis and payoff sequencing

⚖️ Judgment satisfaction procedures specific to your state

⚖️ Escrow management for disputed or uncertain amounts

⚖️ Recording services for all release documents

When necessary, we also coordinate with real estate attorneys to address unique legal issues, ensuring your interests are protected throughout the transaction.

Ensuring Clean Title Transfer

Our ultimate goal is delivering clean, marketable title to the buyer while ensuring you receive any remaining equity. This requires:

✔️ Comprehensive title search identifying all encumbrances

✔️ Resolution of all liens through proper payoff procedures

✔️ Title insurance protecting the buyer’s ownership

✔️ Recorded releases clearing public records

✔️ Final title commitment showing clear ownership transfer

This meticulous process protects everyone involved and prevents future disputes or claims against the property.

Transparent Communication Throughout

You receive regular updates at every stage:

- Initial evaluation: Clear explanation of your situation and options

- Offer presentation: Detailed breakdown of payoff amounts and net proceeds

- Contract signing: Review of all terms and timeline

- Title work: Updates on lien verification and payoff coordination

- Pre-closing: Final settlement statement review

- Post-closing: Confirmation of all releases and recordings

This transparency builds trust and ensures you understand exactly what’s happening with your property and your money.

Homeowners dealing with court judgments on their property benefit from this comprehensive approach that treats judgment payoff as a routine part of the transaction rather than an obstacle.

Special Situations: When Judgment Payoff Gets Complicated

While most judgment payoffs follow standard procedures, certain situations require additional expertise and creative solutions.

Insufficient Equity to Cover Judgment

What happens when your home’s value doesn’t cover all liens and the judgment?

Example scenario:

- Home value: $200,000

- First mortgage: $175,000

- Judgment: $50,000

- Available equity: $25,000

Options in this situation:

- Negotiate judgment reduction: Creditors often accept partial payment in exchange for full release, especially when forced sale would yield even less

- Short sale with lien release: Some creditors agree to release liens for less than owed when property sells

- Buyer advances funds: Specialized buyers may advance funds to satisfy liens in exchange for lower purchase price

- Bankruptcy consideration: Chapter 7 or 13 may discharge or restructure judgment debt

Our helpful guidance includes analyzing which option best serves your long-term financial interests. Sometimes selling a house with multiple liens requires negotiating with several creditors simultaneously to achieve full release.

Multiple Judgments from Different Creditors

Managing multiple judgment creditors adds complexity to the payoff process:

Coordination challenges:

- Different payoff procedures for each creditor

- Varying interest rates and calculation methods

- Priority disputes between creditors

- Timeline coordination for simultaneous payoffs

- Ensuring all releases get recorded properly

Our industry experts handle these multi-party negotiations, ensuring all creditors receive proper payment according to their priority and legal entitlement.

Disputed or Appealed Judgments

If you’re actively disputing or appealing a judgment, selling becomes more complex:

Escrow solutions:

- Disputed amounts held in escrow pending resolution

- Partial payoff of undisputed amounts at closing

- Buyer protection through title insurance endorsements

- Seller protection through escrow agreements

We work with title companies and attorneys to structure transactions that protect everyone’s interests while allowing the sale to proceed.

Out-of-State Judgments and Sister State Recognition

Judgments from other states may affect your property through “sister state” recognition:

Domestication process:

- Creditor files judgment in your state’s courts

- Judgment becomes enforceable under local laws

- Lien attaches to property in new jurisdiction

We verify whether out-of-state judgments have been properly domesticated and ensure they’re addressed appropriately at closing.

Tax Liens Combined with Judgments

When property tax liens combine with judgment liens, priority and payoff become more complex:

Tax lien considerations:

- Property tax liens typically have super-priority status

- IRS liens follow specific federal procedures

- State tax liens vary by jurisdiction

- Combined payoff coordination requires expertise

Our friendly and caring approach includes working with tax authorities and judgment creditors simultaneously to ensure proper payoff sequencing and complete lien release.

State-Specific Considerations for Judgment Liens

Judgment lien laws vary significantly by state, affecting your options and timeline when selling to satisfy debt.

Florida Judgment Lien Rules

Florida provides strong homestead protection but specific judgment lien procedures:

Key Florida provisions:

- Homestead exemption: Unlimited for primary residence (up to 0.5 acres in municipality, 160 acres elsewhere)

- Judgment lien duration: 20 years (can be renewed)

- Recording requirements: Must record in each county where property located

- Execution timeline: Minimum 6 months from judgment to forced sale

Florida’s generous homestead protection means many judgment creditors cannot force sale of your primary residence. However, the lien remains attached and must be satisfied when you voluntarily sell.

For homeowners throughout the state, our Florida-specific lien expertise ensures compliance with all state requirements and maximum protection of your rights.

Texas Judgment Lien Procedures

Texas offers even stronger homestead protection with unique judgment lien rules:

Key Texas provisions:

- Homestead exemption: Unlimited for primary residence (up to 10 acres urban, 100-200 acres rural)

- Judgment lien duration: 10 years (renewable)

- Abstract of judgment: Must file in county where property located

- Forced sale restrictions: Very limited for homestead property

Texas homestead laws prevent forced sale for most judgment types (except mortgage foreclosure, property taxes, home equity loans, and specific other exceptions). However, liens still attach and must be cleared for sale.

Our Texas property expertise includes understanding county-specific procedures in major markets like Houston, Dallas, Austin, and San Antonio.

California Judgment Enforcement

California’s judgment lien system includes specific timelines and procedures:

Key California provisions:

- Homestead exemption: $300,000 – $600,000 depending on circumstances (2026)

- Judgment lien duration: 10 years from entry

- Abstract of judgment: Creates automatic lien on real property in county

- Renewal requirements: Must renew before 10-year expiration

California’s moderate homestead exemptions mean many homeowners have equity vulnerable to judgment enforcement, making voluntary sale an important option to preserve value.

Other State Variations

Other states have unique provisions affecting judgment lien sales:

New York:

- 20-year judgment lien duration

- Varying homestead exemptions by county ($165,550 – $550,000)

- Specific execution sale procedures

Georgia:

- 7-year judgment lien duration (renewable)

- Limited homestead exemption ($21,500 per person)

- Relatively quick execution timeline

Pennsylvania:

- 20-year judgment lien duration

- No homestead exemption

- Vulnerable equity for most homeowners

Understanding your state’s specific rules is essential for making informed decisions about timing and strategy when selling to satisfy judgments.

Protecting Your Credit and Financial Future

Selling your house to pay off a judgment isn’t just about resolving the immediate problem—it’s about protecting your long-term financial health.

How Judgments Affect Your Credit Score

Judgments impact credit scores significantly:

Credit score impact:

- Initial judgment: 50-150 point drop typically

- Duration on report: 7 years from filing date (varies by state)

- Public record status: Visible to all creditors and lenders

- Ongoing impact: Diminishes over time but remains visible

Paying off the judgment through property sale changes the status from “unsatisfied” to “satisfied,” which improves your credit profile even though the record remains.

The Value of Satisfied vs. Unsatisfied Judgments

The difference between satisfied and unsatisfied judgments matters for future credit:

Unsatisfied judgment:

- ❌ Active collection risk

- ❌ Growing balance (interest and fees)

- ❌ Maximum credit score impact

- ❌ Barrier to new credit approval

- ❌ Possible wage garnishment or bank levies

Satisfied judgment:

- ✅ No collection risk

- ✅ Fixed balance (no more interest)

- ✅ Reduced credit score impact

- ✅ Better credit approval odds

- ✅ No garnishment or levy risk

While both remain on your credit report, satisfied judgments demonstrate responsibility and significantly improve your creditworthiness.

Rebuilding After Judgment Payoff

Once you’ve satisfied the judgment through property sale, focus on rebuilding:

Immediate steps (0-3 months):

- Verify satisfaction recorded on credit reports

- Dispute any inaccuracies in reporting

- Establish emergency savings fund

- Create realistic budget for new housing situation

Short-term rebuilding (3-12 months):

- Obtain secured credit card to rebuild payment history

- Make all payments on time (most important factor)

- Keep credit utilization below 30%

- Monitor credit reports quarterly

Long-term recovery (12-36 months):

- Diversify credit types (installment and revolving)

- Maintain consistent payment history

- Gradually increase available credit

- Consider credit counseling if needed

Selling your property to eliminate judgment debt provides a clean slate for financial recovery—a fresh start that’s impossible while the judgment remains unsatisfied and growing.

Tax Implications of Judgment Payoff

Understanding tax consequences helps you plan appropriately:

Potential tax issues:

- Cancellation of debt income: If creditor accepts less than full amount, difference may be taxable income

- Capital gains: Sale may trigger capital gains tax depending on profit and holding period

- Form 1099-C: Creditors must issue if $600+ debt canceled

- Insolvency exception: May exclude canceled debt from income if insolvent

Consult with a tax professional before finalizing any judgment settlement to understand your specific tax situation and plan accordingly.

Common Questions About Selling to Pay Off Judgments

Homeowners facing judgment liens often have similar concerns and questions. Here are answers to the most common inquiries.

Can I Sell My House If There’s a Judgment Against Me?

Yes, absolutely. Judgment liens don’t prevent you from selling your property. They simply must be satisfied from the sale proceeds before you receive any remaining equity.

The title company coordinates the payoff as part of the standard closing process. Buyers receive clear title, creditors receive their judgment amount, and you receive any remaining proceeds.

Will I Get Any Money After Paying Off the Judgment?

It depends on your equity position. Calculate your potential proceeds:

Formula:

Sale Price – Mortgage Balance – Judgment Amount – Closing Costs = Your Net Proceeds

If this calculation yields a positive number, you’ll receive money at closing. If negative, you’ll need to negotiate judgment reduction or consider other options.

Many homeowners are pleasantly surprised to discover they have more equity than expected, especially when working with buyers who minimize closing costs and expedite the process to reduce interest accumulation.

How Long Does the Process Take?

Timeline varies by sale method:

- Cash buyer: 7-21 days from offer acceptance to closing

- Traditional sale: 3-6 months from listing to closing

- Complex situations: May add 2-4 weeks for title work

The judgment payoff itself adds minimal time to the closing process—usually just a few days for the title company to obtain payoff letters and prepare satisfaction documents.

What If the Judgment Amount Is Disputed?

Several solutions exist:

- Escrow disputed amount: Hold contested portion in escrow while proceeding with sale

- Bond substitution: Replace property lien with surety bond

- Settlement negotiation: Resolve dispute as part of sale transaction

- Court resolution: Obtain court order clarifying amount before closing

We work with title companies and attorneys to structure transactions that protect your interests while allowing the sale to proceed despite disputes.

Can Creditors Force Me to Sell Below Market Value?

Not in voluntary sales. When you control the sale process, you determine the acceptable price. Forced sales through sheriff’s auctions typically yield below-market results, but voluntary sales achieve fair market value (or fair as-is value for cash buyers).

This is precisely why selling voluntarily makes financial sense—you preserve maximum equity by controlling the process rather than waiting for forced execution.

What Happens to Remaining Judgment Debt?

Depends on sale proceeds:

- Full payoff: If proceeds cover entire judgment, debt is completely satisfied with no remaining liability

- Partial payoff: If proceeds insufficient, creditor may pursue deficiency judgment for remainder (state laws vary)

- Negotiated settlement: Creditors often accept partial payment as full satisfaction when property sale is involved

Our expert service includes negotiating with creditors to achieve full release whenever possible, even when proceeds don’t cover the entire judgment amount.

Why Choose Sure Path Property Solutions

When facing the stress of judgment liens and potential property loss, you need more than just a buyer—you need a partner with expertise, integrity, and a proven track record.

Our Expertise in Complex Lien Situations

Sure Path Property Solutions specializes in exactly the complicated situations that intimidate traditional buyers:

🏆 Judgment liens of all types and amounts

🏆 Multiple creditors requiring coordinated payoffs

🏆 Title defects and clouded ownership

🏆 Tax liens combined with judgments

🏆 Foreclosure prevention through quick sale

🏆 Probate complications with inherited property

🏆 Multiple owners with conflicting interests

Our industry experts have successfully closed hundreds of transactions involving judgment payoffs, giving us the knowledge and relationships to navigate even the most complex situations smoothly.

Transparent Process, Fair Offers

We believe in complete transparency throughout the process:

Our commitment:

- ✅ Clear explanation of how we calculate offers

- ✅ Detailed breakdown of all payoffs and costs

- ✅ No hidden fees or surprise deductions

- ✅ Written offers with specific terms and timeline

- ✅ Regular updates throughout the process

- ✅ Honest assessment of your best options

Fair doesn’t always mean highest price—it means honest evaluation of your property’s as-is value and transparent disclosure of how proceeds will be distributed. Our helpful solutions focus on your net outcome, not just gross sale price.

No Upfront Costs, No Obligations

Getting started with Sure Path Property Solutions involves zero financial risk:

What we don’t charge:

- ❌ No evaluation fees

- ❌ No consultation charges

- ❌ No obligation to accept our offer

- ❌ No upfront costs of any kind

- ❌ No pressure or aggressive sales tactics

You receive a written cash offer based on thorough evaluation of your situation. Accept it if it makes sense for your circumstances. Decline it if you prefer to pursue other options. Either way, you’ve gained valuable information about your situation at no cost.

Testimonials from Homeowners We’ve Helped

“I was terrified of losing my house to the sheriff’s sale. Sure Path explained everything clearly, made a fair offer, and handled all the coordination with my creditor. I walked away with $28,000 and a huge weight off my shoulders.” — Marcus T., Houston, TX

“Three different judgment liens made selling seem impossible. Traditional agents wouldn’t even list my property. Sure Path coordinated payoffs with all three creditors and closed in 12 days. Professional, caring, and expert service throughout.” — Jennifer L., Orlando, FL

“The judgment interest was adding $150 per month to what I owed. Every month I waited cost me more money. Sure Path’s quick closing saved me thousands in accumulating interest and gave me a fresh start.” — Robert K., Atlanta, GA

These real experiences reflect our commitment to helpful guidance and trustworthy service for homeowners navigating difficult property situations.

Our Service Areas

Sure Path Property Solutions helps homeowners throughout major markets including:

- Florida: Jacksonville, Orlando, Miami

- Texas: Houston, Dallas, Austin, San Antonio

- Georgia: Atlanta

- California: Los Angeles, San Diego

We also work with homeowners in other markets facing judgment liens and complex property situations. Contact us to discuss your specific location and circumstances.

Taking Action: Your Next Steps

Knowledge without action doesn’t solve problems. If you’re facing judgment liens on your property, now is the time to take control of your situation.

Immediate Actions You Can Take Today

Within the next 24 hours:

- Gather documentation: Locate your judgment paperwork, property deed, mortgage statements, and recent property tax bills

- Calculate equity: Estimate your property value and subtract all known liens to understand your equity position

- Contact Sure Path: Reach out for a no-obligation consultation and property evaluation

- Request payoff letters: Contact judgment creditors to request current payoff amounts (or let us handle this)

- Review your options: Consider both traditional sale and cash buyer approaches

Within the next week:

- Get property evaluation: Allow us to assess your property and situation

- Review written offer: Examine our cash offer and detailed breakdown

- Compare alternatives: Weigh cash sale against traditional listing based on your timeline and goals

- Consult professionals: Speak with a real estate attorney or tax advisor if needed

- Make decision: Choose the path that best serves your financial interests

How to Get Started with Sure Path Property Solutions

Beginning the process is simple and completely risk-free:

Step 1: Contact Us

- Phone: [Your phone number]

- Online form: [Your website contact form]

- Email: [Your email address]

Step 2: Brief Consultation

We’ll ask about your property, judgment situation, timeline, and goals. This conversation typically takes 10-15 minutes and provides us with the information needed to evaluate your situation.

Step 3: Property Evaluation

We’ll assess your property’s condition and value, either through:

- Virtual evaluation (photos and video)

- In-person visit (scheduled at your convenience)

- Public records and comparable sales analysis

Step 4: Written Offer

Within 24-48 hours, you’ll receive a detailed written offer including:

- Cash purchase price

- Estimated closing timeline

- Breakdown of judgment payoffs

- Your estimated net proceeds

- Terms and conditions

Step 5: Your Decision

Review the offer with no pressure. Accept it if it works for your situation. Decline if you prefer other options. Ask questions until you’re completely comfortable with the process.

Step 6: Smooth Closing

If you accept, we coordinate everything:

- Title company selection and coordination

- Judgment creditor communication

- Payoff amount verification

- Closing date scheduling

- Document preparation

- Final settlement and fund distribution

Questions to Ask Any Cash Buyer

If you’re considering multiple cash buyers, ask these important questions:

❓ How do you calculate your offers?

❓ What closing costs will I pay?

❓ How quickly can you close?

❓ Do you have experience with judgment payoffs?

❓ Will you coordinate directly with my creditors?

❓ Can you provide references from similar situations?

❓ What happens if title issues arise during closing?

❓ Are there any circumstances where you wouldn’t close?

Quality buyers provide clear, confident answers to all these questions. Evasive or vague responses should raise concerns.

The Cost of Delay

Every month you wait to address judgment liens costs you money:

Monthly costs of inaction:

- Judgment interest accumulation ($200-$1,000+)

- Property taxes and insurance ($300-$800)

- Mortgage payments ($1,000-$3,000)

- Maintenance and utilities ($200-$500)

- Stress and uncertainty (priceless)

More importantly, delay increases the risk of:

- Creditor enforcement proceedings

- Additional legal costs

- Forced sale at below-market value

- Further credit damage

- Loss of control over the process

Taking action now—even if just gathering information—puts you back in control and stops the financial bleeding.

Conclusion: Your Path to Freedom from Judgment Liens

Facing a judgment lien on your property feels overwhelming, but you have more power than you might realize. Selling your house to pay off a judgment isn’t admitting defeat—it’s taking strategic control of your financial future.

The key insights to remember:

✅ Voluntary sale preserves significantly more equity than waiting for forced execution

✅ Judgment payoff at closing is routine for experienced title companies and cash buyers

✅ Speed matters because judgment interest accumulates daily

✅ Professional coordination eliminates the stress of dealing with creditors directly

✅ You can walk away with money if you have sufficient equity after payoffs

✅ Satisfied judgments improve your credit profile and financial options

Whether you choose traditional listing or a cash buyer depends on your specific circumstances—timeline pressure, property condition, equity position, and personal preferences. Both paths can successfully resolve judgment liens, but cash buyers offer speed, certainty, and expertise specifically designed for complicated situations.

At Sure Path Property Solutions, we’ve built our reputation on friendly and caring service for homeowners facing exactly your situation. Our industry experts understand the legal complexities, coordinate with all parties, and guide you toward the solution that best serves your interests.

You don’t have to navigate this alone. Our helpful solutions and trustworthy service have helped hundreds of homeowners escape the burden of judgment liens and move forward with their lives.

The first step is simply reaching out. No cost, no obligation, no pressure—just honest information and expert guidance to help you make the best decision for your circumstances.

Take control today. Contact Sure Path Property Solutions for your free property evaluation and discover exactly how much equity you can preserve by selling your house to pay off your judgment.

Your fresh start is closer than you think.