Imagine standing at the finish line of your property sale, keys in hand, ready to close the deal—only to have your title company drop a bombshell: there’s a problem with your property title. This scenario plays out more often than most property owners realize. In fact, approximately 36% of title files are classified as ‘difficult’ and require extensive curative work before closing can proceed[1]. Understanding title problems at closing: common issues & how to resolve them can mean the difference between a minor delay and a complete transaction collapse.

The good news? Most title issues are solvable with the right knowledge and expert service. Whether dealing with inherited property, back taxes, liens, or judgments, property owners can navigate these challenges successfully with helpful guidance and a clear action plan.

Key Takeaways

- Title problems affect more than one-third of real estate transactions, with difficult files requiring an average of 45 hours of curative work compared to 22 hours for standard files[1]

- Common title issues include tax liens, judgment liens, missing heirs, boundary disputes, and unpaid mortgages—each requiring specific resolution strategies

- Early detection is critical: ordering title searches immediately and reviewing title commitments thoroughly can prevent last-minute closing disasters

- Most title problems are resolvable through payoffs, releases, quiet title actions, or corrective documentation when addressed promptly

- Professional help from industry experts dramatically reduces resolution time and increases the likelihood of successful closing

Understanding Title Problems at Closing

A title problem represents any issue that prevents clear ownership transfer from seller to buyer. These complications create what title professionals call a “cloud on title”—legal uncertainties that must be resolved before a property can change hands legally.

Title companies spend considerable time investigating these issues. Standard title files require approximately 22 hours of work, while difficult files demand 45 hours or more of detailed examination and curative efforts[1]. This intensive process protects both buyers and lenders from inheriting someone else’s legal problems.

Why Title Problems Matter

Clear title isn’t just a formality—it’s the foundation of property ownership. Without it:

- Buyers cannot obtain mortgage financing

- Title insurance companies refuse coverage

- Property ownership remains legally questionable

- Future sales become impossible

- Legal liability transfers to new owners

Think of clear title like a car’s title certificate. Just as you wouldn’t buy a vehicle without proper documentation proving ownership, real estate transactions require the same certainty.

Common Title Problems at Closing

Understanding the specific title issue with property helps determine the fastest resolution path. Here are the most frequent complications that derail closings:

🏛️ Tax Liens and Back Taxes

The Problem: Unpaid property taxes create automatic liens against real estate. These liens take priority over almost all other claims, including mortgages.

Why It Happens: Property owners facing financial hardship often fall behind on tax payments. Inherited properties frequently accumulate years of back taxes when heirs don’t realize their responsibility.

Resolution Steps:

- Request a tax payoff statement from the county treasurer

- Calculate total amount including penalties and interest

- Negotiate payment from sale proceeds at closing

- Obtain tax clearance certificate before closing date

- Ensure title company verifies lien release recording

Timeline: 5-10 business days for standard tax payoffs; 2-4 weeks if negotiating payment plans or settlements.

⚖️ Judgment Liens

The Problem: Court judgments for unpaid debts attach to all real property owned by the debtor in that county.

Common Sources:

- Credit card lawsuits

- Medical bills

- Contractor disputes

- Homeowner association (HOA) violations

- Child support obligations

Resolution Steps:

- Identify all judgment creditors through title search

- Contact creditors or their attorneys for payoff amounts

- Negotiate settlements (often accepting less than full amount)

- Obtain satisfaction of judgment documents

- Record releases with county recorder

- Verify removal from title commitment

Timeline: 2-6 weeks depending on creditor responsiveness and negotiation complexity.

👨👩👧👦 Missing Heirs and Estate Issues

The Problem: When property passes through inheritance, all legal heirs must be identified and either sign off on the sale or have their interests legally resolved.

Common Scenarios:

- Deceased owner never probated

- Unknown or estranged family members

- Multiple heirs with conflicting interests

- Unclear will provisions

- Missing death certificates or estate documents

Resolution Steps:

- Conduct comprehensive heir search

- Open probate proceedings if necessary

- Obtain court orders establishing ownership

- Secure signatures from all identified heirs

- File quiet title action if heirs cannot be located

- Obtain title insurance for remaining risk

Timeline: 3-12 months for probate; 6-18 months for quiet title actions.

“Properties with multiple heirs or unclear succession create some of the most challenging title problems, but they’re also among the most rewarding to solve. With helpful solutions and patient coordination, families can successfully navigate these complex situations.” — Title Industry Expert

📏 Boundary Disputes and Survey Issues

The Problem: Disagreements about property lines, encroachments, or easements create title uncertainty.

Examples:

- Neighbor’s fence crosses property line

- Driveway encroaches on adjacent lot

- Undisclosed easements for utilities

- Discrepancies between old and new surveys

- Adverse possession claims

Resolution Steps:

- Order professional boundary survey

- Compare with historical property descriptions

- Negotiate boundary line agreements with neighbors

- Record corrective deeds or easements

- Obtain title insurance endorsements

- Consider quiet title action for disputed areas

Timeline: 4-8 weeks for surveys and negotiations; 6-12 months for litigation.

🏦 Unpaid Mortgages and Prior Liens

The Problem: Previous mortgages or liens that weren’t properly released remain attached to the property.

Why It Happens:

- Lender failed to record satisfaction

- Lost or misfiled release documents

- Merger or acquisition of original lender

- Bankruptcy of lien holder

- Clerical errors in recording

Resolution Steps:

- Contact original lender or successor

- Provide proof of payment if available

- Request re-recording of release

- File affidavit of lost satisfaction if necessary

- Obtain title insurance indemnification

- Consider bonding over small, aged liens

Timeline: 1-4 weeks for cooperative lenders; 2-6 months for defunct institutions.

📝 Deed Errors and Name Discrepancies

The Problem: Mistakes in recorded documents create breaks in the chain of title.

Common Issues:

- Misspelled names

- Incorrect legal descriptions

- Missing signatures or notarizations

- Wrong property identification numbers

- Clerical recording errors

Resolution Steps:

- Identify exact nature of error

- Prepare corrective deed or affidavit

- Obtain signatures from all necessary parties

- Record corrective documents

- Update title commitment

Timeline: 1-3 weeks for simple corrections; longer if original parties are deceased or unavailable.

What Happens When Title Company Found Problems

The moment your title company found problems with your property, a specific process begins. Understanding this workflow helps property owners respond effectively.

Immediate Notification Process

Within 24-48 Hours:

- Title examiner flags issues during search

- Preliminary report lists all discovered problems

- Title company contacts all transaction parties

- Escrow officer assesses impact on closing timeline

Your Title Commitment:

This critical document arrives listing:

- Schedule A: Basic transaction information

- Schedule B-I: Requirements that must be satisfied before closing (the problems)

- Schedule B-II: Exceptions to coverage (items not insured)

Impact Assessment

When the title company discovers issues, three outcomes are possible:

| Severity Level | Impact | Typical Resolution Time |

|---|---|---|

| Minor | Closing delayed 1-2 weeks | 5-10 business days |

| Moderate | Closing delayed 3-6 weeks | 2-6 weeks |

| Severe | Closing cancelled or delayed 3+ months | 3-12 months |

Your Immediate Action Steps

Step 1: Review the Title Commitment Carefully ✅

Don’t panic—read the entire document. Many items listed are standard requirements, not deal-breakers.

Step 2: Contact Your Title Company 📞

Request a detailed explanation of each issue. Ask:

- What exactly is the problem?

- What documentation is needed?

- What is the estimated resolution timeline?

- Who is responsible for resolving it?

- What are the associated costs?

Step 3: Assemble Your Team 👥

Depending on complexity, you may need:

- Real estate attorney

- Estate planning attorney

- Tax specialist

- Survey professional

- Title curative specialist

Step 4: Prioritize Issues 🎯

Work with industry experts to determine which problems must be resolved first and which can be handled simultaneously.

Step 5: Communicate with All Parties 💬

Keep buyers, sellers, agents, and lenders informed. Transparency prevents misunderstandings and maintains trust throughout the resolution process.

How to Resolve Title Issues Quickly

Speed matters when title problems threaten your closing date. These strategies accelerate resolution while maintaining thoroughness.

The Resolution Priority Matrix

Handle First (Critical Path Items):

- Tax liens with redemption deadlines

- Judgments with active collection proceedings

- Missing signatures from elderly or ill parties

- Time-sensitive probate requirements

- Lender-required clearances

Handle Second (Important but Flexible):

- Survey corrections

- Name discrepancy affidavits

- Deed corrections

- Easement documentation

- Title insurance endorsements

Handle Last (Can Often Be Insured Over):

- Ancient liens beyond statute of limitations

- Minor boundary encroachments

- Satisfied but unrecorded releases

- Immaterial name variations

- Utility easements of record

Proven Resolution Strategies

Strategy 1: The Payoff Approach

Best For: Tax liens, judgment liens, mortgages

Process:

- Obtain exact payoff amounts in writing

- Negotiate payment from closing proceeds

- Coordinate simultaneous recording of payoff and new deed

- Obtain immediate release documentation

Success Rate: 85-90% when funds are available

Strategy 2: The Negotiation Approach

Best For: Judgment liens, disputed claims, heir agreements

Process:

- Identify all parties’ interests and motivations

- Propose win-win solutions

- Document agreements in legally binding form

- Execute and record simultaneously with closing

Success Rate: 70-80% with skilled negotiators

Strategy 3: The Legal Action Approach

Best For: Missing heirs, boundary disputes, unmarketable title

Process:

- File appropriate legal action (quiet title, partition, etc.)

- Serve all necessary parties

- Obtain court orders establishing clear ownership

- Record judgment and proceed to closing

Success Rate: 90-95% but time-intensive (6-18 months)

Strategy 4: The Insurance Approach

Best For: Minor defects, aged liens, immaterial issues

Process:

- Provide title company with supporting documentation

- Request title insurance coverage over the defect

- Obtain endorsements or affirmative coverage

- Accept slightly higher premium if necessary

Success Rate: 60-70% depending on risk tolerance

Working with Title Curative Specialists

Title companies employ specialists who resolve complex issues daily. These industry experts offer:

- Deep knowledge of county recording systems across all 3,000+ U.S. counties[1]

- Established relationships with county officials, courts, and creditors

- Efficient processes for document retrieval and recording

- Creative solutions for unusual situations

- Trustworthy service that protects all parties’ interests

Leveraging their expertise significantly reduces resolution time and stress.

Understanding Your Title Commitment

The title commitment document holds the roadmap to closing—or the obstacles preventing it. Learning to read this critical document empowers property owners to take control of the situation.

Anatomy of a Title Commitment

Schedule A: The Basics

- Effective date of title search

- Proposed insured (buyer/lender)

- Property legal description

- Current vested owner

- Proposed insurance amount

Schedule B-I: Requirements (The Problems)

This section lists everything that must be completed before the title company will issue insurance:

✅ Standard Requirements (appear on every commitment):

- Proper execution and recording of new deed

- Payment of transfer taxes

- Satisfaction of existing mortgages

- Standard owner affidavits

⚠️ Special Requirements (your specific title problems):

- Tax lien payoffs with specific amounts

- Judgment releases with creditor information

- Estate documents with court case numbers

- Survey requirements with specific concerns

- Corrective deeds with exact language needed

Schedule B-II: Exceptions (Items Not Insured)

Standard exceptions include:

- Rights of parties in possession

- Unrecorded easements

- Matters that would be revealed by survey

- Mechanics’ lien rights

- Governmental regulations (zoning, building codes)

Red Flags to Watch For

🚩 Multiple judgment liens – Suggests financial distress requiring comprehensive creditor negotiation

🚩 Probate required – Indicates 3-12 month minimum delay

🚩 Survey required due to encroachment – Signals potential boundary disputes

🚩 Federal tax liens – More complex than local liens; IRS involvement required

🚩 Lis pendens (pending lawsuit) – Property involved in litigation; resolution required before closing

🚩 Bankruptcy notation – Requires bankruptcy court approval for sale

Questions to Ask Your Title Officer

- Which requirements are seller’s responsibility versus buyer’s?

- What is the realistic timeline for each requirement?

- Which issues can be resolved simultaneously?

- Are any requirements negotiable or insurable?

- What happens if we cannot resolve everything by closing date?

- What are the estimated costs for each resolution?

Delaying vs. Canceling Closing

When title problems emerge, property owners face a critical decision: delay the closing or cancel the transaction entirely.

When Delaying Makes Sense

Delay the closing if:

✅ Problems are clearly resolvable with defined timelines

✅ All parties remain committed to the transaction

✅ Buyers can extend financing commitments

✅ Resolution costs are reasonable and agreed upon

✅ Delay period is definite (30, 60, or 90 days)

✅ Progress can be monitored with specific milestones

When Canceling Might Be Necessary

Consider cancellation if:

❌ Resolution timeline exceeds 6-12 months

❌ Resolution costs exceed property value

❌ Buyer or lender withdraws due to complications

❌ Legal obstacles prove insurmountable

❌ Multiple title issues compound complexity

❌ Property owner lacks resources for curative work

The Extension Agreement

When delaying, formalize the arrangement:

Include:

- Specific new closing date

- Milestones for issue resolution

- Party responsibilities clearly defined

- Cost allocation agreements

- Consequences for missing deadlines

- Earnest money handling

- Financing commitment extensions

Example Timeline Extension:

“Closing date extended from March 15, 2025 to May 15, 2025. Seller to obtain tax lien release by April 1, 2025, judgment satisfaction by April 15, 2025, and corrective deed by May 1, 2025. Buyer’s financing commitment extended through May 20, 2025. Earnest money remains in escrow. If seller fails to meet milestones, buyer may cancel with full refund of earnest money.”

Protecting Your Interests During Delays

For Sellers:

- Maintain property insurance and taxes

- Continue property maintenance

- Keep all parties informed of progress

- Document all resolution efforts

- Consider backup offers if permitted

For Buyers:

- Secure financing extension in writing

- Monitor resolution progress actively

- Maintain inspection contingency if applicable

- Document all communications

- Protect earnest money through proper escrow

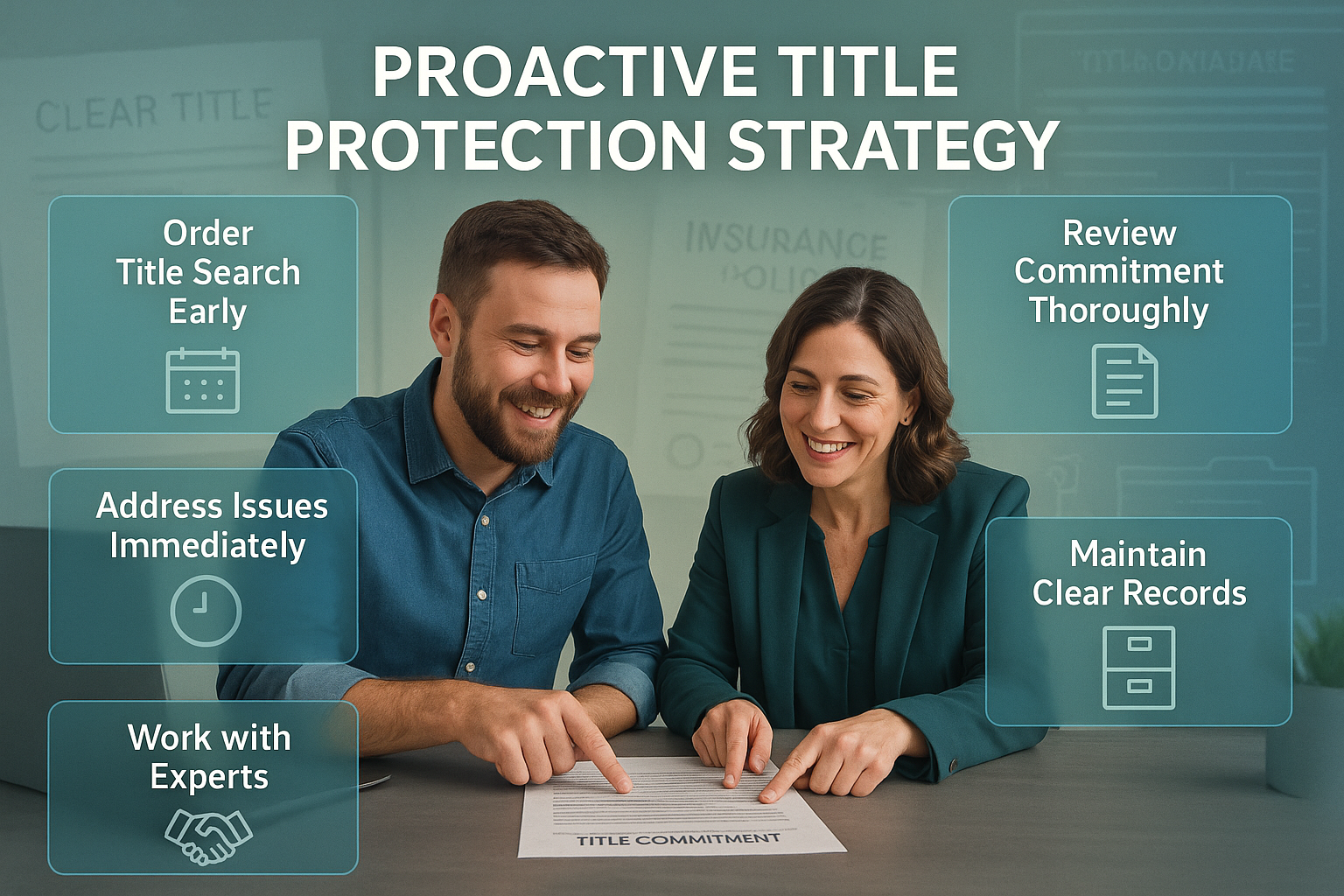

Preventing Title Problems Before They Happen

The best resolution strategy is prevention. Property owners can avoid most title complications through proactive measures and helpful guidance from professionals.

Early Title Search Strategy

⏰ Timing Matters:

Order title searches immediately when considering sale:

- 60-90 days before listing provides resolution time

- Identifies problems before buyers are involved

- Allows unhurried resolution without closing pressure

- Prevents last-minute surprises

Cost: $200-500 for preliminary title search—a small investment compared to lost deals.

Maintain Clean Property Records

📋 Best Practices:

For All Property Owners:

- Keep all deeds, mortgages, and releases in safe location

- File satisfaction of mortgage immediately upon payoff

- Update ownership after life events (marriage, divorce, death)

- Pay property taxes on time, every time

- Respond promptly to legal notices

For Inherited Properties:

- Probate estate promptly after death

- Record death certificates and estate documents

- Transfer title to heirs formally

- Update tax assessor records

- Maintain continuous insurance coverage

For Properties with Multiple Owners:

- Document all ownership agreements in writing

- Record partition agreements if dividing property

- Establish clear decision-making authority

- Maintain communication among all owners

- Plan exit strategies before conflicts arise

Work with Professionals from Day One

🤝 Build Your Expert Team:

Real Estate Attorney:

- Reviews contracts before signing

- Identifies potential title issues early

- Provides helpful solutions for complex situations

- Represents interests in negotiations

- Handles legal filings efficiently

Title Company:

- Conducts thorough title searches

- Provides expert service throughout transaction

- Offers title insurance protection

- Coordinates with all parties

- Delivers friendly and caring customer support

Tax Specialist:

- Resolves back tax issues

- Negotiates payment plans with counties

- Obtains tax clearances

- Advises on tax implications of sale

- Provides helpful guidance on complex tax situations

Survey Professional:

- Establishes accurate boundary lines

- Identifies encroachments early

- Provides documentation for title insurance

- Resolves disputes before they escalate

Address Known Issues Immediately

Don’t wait for a buyer to appear before resolving known problems:

Common Proactive Fixes:

- Pay off small liens immediately – $500-2,000 liens are often negotiable for less; eliminate them now

- Correct deed errors – File corrective deeds for name misspellings or description errors

- Resolve estate matters – Complete probate even if not selling immediately

- Establish clear boundaries – Order survey if any uncertainty exists

- Satisfy old judgments – Many creditors settle for pennies on the dollar after several years

The Title Insurance Advantage

Title insurance protects against undiscovered defects, but prevention remains superior:

What Title Insurance Covers:

- Forgery and fraud

- Unknown heirs

- Recording errors

- Undisclosed liens

- Survey mistakes

What It Doesn’t Cover:

- Known defects listed in Schedule B-II

- Issues arising after policy date

- Governmental actions (eminent domain)

- Environmental hazards

2025 Market Context:

Title insurance premiums reached $4.5 billion in Q2 2025, with volume up 13.2% compared to 2024[4]. This increase reflects both growing transaction volume and increasing complexity of title issues requiring professional resolution.

Special Considerations for Complex Situations

Certain property situations create unique title challenges requiring specialized approaches.

Properties with Back Taxes

The Challenge:

Back taxes create super-priority liens that must be satisfied before any other claims. Properties with multiple years of unpaid taxes face:

- Accumulating penalties and interest (often 10-18% annually)

- Tax sale or foreclosure proceedings

- Redemption deadlines

- Multiple taxing authorities (county, city, school district)

The Solution Path:

- Obtain comprehensive tax statement from county treasurer showing all amounts owed

- Verify redemption deadlines to avoid tax sale

- Negotiate payment plans if immediate full payment impossible

- Request penalty abatement based on hardship circumstances

- Coordinate closing to pay taxes from sale proceeds

- Secure tax clearance before deed recording

Expert Assistance:

Companies like Sure Path Property Solutions specialize in coordinating with counties and title professionals to resolve complex back tax situations, providing helpful solutions that simplify the process for property owners.

Properties with Multiple Heirs

The Challenge:

When multiple family members inherit property, complications multiply:

- All heirs must agree to sale terms

- Some heirs may be unreachable or uncooperative

- Ownership percentages may be disputed

- Estate was never properly probated

- Generational transfers create numerous potential heirs

The Solution Path:

- Identify all legal heirs through genealogical research if necessary

- Open probate proceedings if estate was never administered

- Obtain court orders establishing ownership percentages

- Negotiate heir buyouts if some want to keep property

- File partition action if heirs cannot agree

- Secure all necessary signatures with proper notarization

Timeline Reality:

Properties with heir issues require patience. Expect 6-18 months for complex situations, but the result—clear, marketable title—makes the effort worthwhile.

Properties with Liens and Judgments

The Challenge:

Multiple liens create a hierarchy of claims against property:

- Property tax liens (first priority)

- Federal tax liens

- Mortgage liens (by recording date)

- Judgment liens (by recording date)

- HOA liens (varies by state)

- Mechanics liens (relate back to work commencement)

The Solution Path:

- Create comprehensive lien list from title search

- Prioritize by urgency and legal priority

- Negotiate settlements (many creditors accept less than full amount)

- Obtain written payoff agreements before payment

- Coordinate simultaneous releases at closing

- Verify recording of all satisfactions

Negotiation Leverage:

Creditors often settle for 40-70% of judgment amount when:

- Judgment is several years old

- Debtor has limited assets

- Property sale provides only recovery opportunity

- Legal collection costs would be substantial

Cybersecurity and Fraud Concerns

Emerging Threats in 2025:

Business Email Compromise (BEC) fraud reached $2.9 billion in losses in 2023, with a 42% increase in 2024[3]. Seller impersonation fraud particularly targets vacant and rental properties[3].

Protection Strategies:

🔒 Verify all wire transfer instructions by phone using known numbers, never email

🔒 Confirm identity of all parties through in-person or video verification

🔒 Use secure communication platforms for sensitive information

🔒 Monitor property records for unauthorized filings

🔒 Work with title companies implementing strong cybersecurity measures[5]

When to Consult an Attorney

While many title issues resolve through title company curative work, certain situations demand legal representation.

Situations Requiring Legal Counsel

Immediate Attorney Consultation Needed:

⚖️ Quiet title actions – Court proceedings to establish clear ownership

⚖️ Probate proceedings – Estate administration and heir determination

⚖️ Partition actions – Forcing sale when co-owners disagree

⚖️ Boundary disputes – Litigation over property lines

⚖️ Fraud allegations – Claims of forged documents or misrepresentation

⚖️ Lien priority disputes – Conflicts over which creditor gets paid first

⚖️ Adverse possession claims – Someone claiming ownership through long-term possession

⚖️ Contract disputes – Disagreements over sale terms or contingencies

Choosing the Right Attorney

Look for:

✅ Real estate specialization (not general practice)

✅ Local county experience and relationships

✅ Title issue expertise specifically

✅ Reasonable fee structures (flat fee vs. hourly)

✅ Responsive communication style

✅ Proven track record with similar issues

Questions to Ask:

- How many cases like mine have you handled?

- What is the typical timeline for resolution?

- What are total estimated costs including filing fees?

- What is my likelihood of success?

- What alternatives exist to litigation?

- How will we communicate throughout the process?

Cost Considerations

Typical Attorney Fees for Title Work:

| Service | Typical Cost Range |

|---|---|

| Simple deed correction | $500 – $1,500 |

| Judgment lien negotiation | $1,000 – $3,000 |

| Probate (uncontested) | $3,000 – $8,000 |

| Quiet title action | $5,000 – $15,000 |

| Boundary dispute litigation | $10,000 – $50,000+ |

| Partition action | $5,000 – $20,000 |

Cost-Benefit Analysis:

Compare attorney fees against:

- Property value

- Potential sale proceeds

- Cost of not resolving (lost sale, continued carrying costs)

- Alternative resolution options

- Likelihood of success

Last-Minute Title Problem Checklist

Despite best efforts, sometimes title problems emerge days before closing. This emergency checklist helps navigate crisis situations.

72 Hours Before Closing

If title problems appear:

☑️ Immediately contact all parties – Buyer, seller, agents, lender, title company

☑️ Assess severity – Can this be resolved in 72 hours or does closing need delay?

☑️ Identify responsible party – Whose obligation is resolution?

☑️ Mobilize resources – Attorney, title curative specialist, county officials

☑️ Establish communication protocol – Hourly updates until resolution

☑️ Prepare extension agreement – Draft now in case delay becomes necessary

☑️ Protect earnest money – Ensure proper handling if closing cancels

☑️ Document everything – Email confirmations of all conversations and agreements

Rapid Resolution Tactics

For Tax Liens:

- Request emergency payoff from county (often available same-day)

- Arrange wire transfer of funds

- Obtain electronic release if county offers

- Accept title insurance coverage if release recording delayed

For Judgment Liens:

- Contact creditor attorney directly

- Offer immediate payment for satisfaction

- Request expedited satisfaction document

- Use overnight courier for document delivery

- Arrange simultaneous closing and recording

For Missing Documents:

- Check with all previous title companies

- Request emergency county search

- Prepare affidavit of lost document

- Obtain title insurance indemnification

- Consider bonding over small amounts

For Survey Issues:

- Order rush survey (2-3 day delivery available)

- Negotiate survey exception with buyer

- Obtain survey endorsement from title company

- Prepare indemnity agreement if appropriate

The Role of Title Insurance in Problem Resolution

Title insurance serves dual purposes: protection against unknown defects and facilitation of closing despite known issues.

How Title Insurance Enables Closing

Coverage Options:

- Standard Coverage – Protects against defects not listed in Schedule B-II

- Extended Coverage – Includes additional protections for survey matters, mechanics liens, and other risks

- Endorsements – Specific coverage additions for identified concerns

Problem-Solving Through Insurance:

Title companies may agree to insure over certain defects rather than requiring full resolution:

Commonly Insurable Issues:

- Ancient liens beyond statute of limitations (typically 10-20 years)

- Satisfied mortgages with lost release documents

- Minor name discrepancies with supporting affidavits

- Immaterial survey encroachments

- Gaps in chain of title with supporting documentation

Non-Insurable Issues:

- Current tax liens

- Active judgments

- Known boundary disputes

- Unresolved estate matters

- Fraudulent conveyances

The Underwriting Decision

Title underwriters assess risk based on:

📊 Age of defect – Older issues carry less risk

📊 Dollar amount – Small liens more easily insured

📊 Supporting documentation – Strong evidence reduces risk

📊 Legal precedent – How courts have treated similar issues

📊 Statute of limitations – Whether claims are time-barred

📊 Practical likelihood – Probability someone will actually make claim

Industry Challenges Affecting Title Resolution in 2025

Understanding current industry dynamics helps set realistic expectations for title problem resolution.

Workforce Shortage Impact

The title industry faces significant staffing challenges, with 10-40% of the workforce expected to retire within the next decade without adequate replacement personnel[8]. This shortage means:

- Longer turnaround times for title searches

- Reduced availability of experienced examiners

- Increased reliance on technology and automation

- Premium pricing for rush services

- Greater importance of early title ordering

Jurisdictional Complexity

The U.S. has over 3,000 counties with vastly different recording systems[1]:

- Fully digitized systems – Online access, same-day searches

- Partially digitized – Mixed online and physical records

- Manual systems – Handwritten archives requiring in-person research

This fragmentation creates:

- Inconsistent turnaround times

- Variable data quality

- Geographic expertise requirements

- Higher costs for multi-county searches

Regulatory Evolution

Title companies navigate increasing regulatory complexity in 2025:

- Enhanced data privacy laws requiring stronger information protection

- Anti-money laundering (AML) regulations demanding additional verification[2]

- CFPB disclosure requirements increasing transparency around fees and policies[5]

- Cybersecurity mandates protecting against fraud and data breaches[5]

These regulations protect consumers but may extend processing timelines.

Government Funding Impacts

Government shutdowns affect title clearance through:

- NFIP disruptions – Flood insurance unavailability delaying thousands of closings daily[7]

- IRS delays – Federal tax lien releases and subordinations suspended

- Court closures – Probate and quiet title proceedings halted

- Recording office closures – Document recording suspended in some jurisdictions

Finding Expert Help for Title Problems

Navigating title problems at closing: common issues & how to resolve them becomes significantly easier with the right professional support.

When to Seek Specialized Assistance

Consider expert help if:

🔍 Multiple complex issues exist simultaneously

🔍 Property has been in family for generations

🔍 Inherited property with numerous heirs

🔍 Significant back taxes have accumulated

🔍 Multiple liens and judgments are present

🔍 Previous sale attempts failed due to title issues

🔍 Time is critical and expertise is limited

🔍 Emotional factors complicate family decisions

What Expert Title Resolution Services Provide

Comprehensive Support:

- Title research and analysis – Identifying all issues thoroughly

- County coordination – Working directly with government offices

- Creditor negotiation – Settling liens and judgments favorably

- Document preparation – Creating all necessary legal paperwork

- Timeline management – Coordinating simultaneous resolutions

- Professional relationships – Leveraging industry connections

- Problem-solving expertise – Finding creative solutions to unique situations

Sure Path Property Solutions Approach:

Companies specializing in complex property situations offer:

✨ Helpful solutions tailored to each unique situation

✨ Trustworthy service protecting property owner interests

✨ Helpful guidance through confusing legal processes

✨ Friendly and caring support during stressful times

✨ Expert service from industry experts with deep experience

✨ Coordination with counties, title companies, and legal professionals

✨ Practical solutions that move properties toward successful closing

Conclusion: Moving Forward with Confidence

Title problems at closing: common issues & how to resolve them need not derail property sales or create insurmountable obstacles. While approximately 36% of title files encounter difficulties requiring extensive curative work[1], the vast majority of these issues resolve successfully with proper knowledge, timely action, and expert assistance.

Your Action Plan

If facing title problems now:

- Don’t panic – Most issues are resolvable with time and expertise

- Review your title commitment carefully – Understand exactly what needs resolution

- Assemble your professional team – Attorney, title company, specialists as needed

- Prioritize issues strategically – Address critical path items first

- Communicate transparently – Keep all parties informed of progress

- Set realistic timelines – Allow adequate time for proper resolution

- Document everything – Maintain records of all efforts and agreements

If planning to sell:

- Order title search early – 60-90 days before listing

- Address known issues immediately – Don’t wait for buyers

- Maintain clean records – Keep all property documents organized

- Pay obligations timely – Taxes, HOA fees, mortgages

- Resolve estate matters promptly – Complete probate when necessary

- Work with professionals – Leverage industry experts from the start

The Path Forward

Property ownership comes with responsibilities, and clear title represents the foundation of that ownership. Whether dealing with inherited property, back taxes, liens, judgments, or any other complication, solutions exist.

The key lies in taking action early, seeking helpful guidance from industry experts, and maintaining realistic expectations about timelines and processes. With the right approach and trustworthy service from experienced professionals, even the most complex title problems become manageable challenges rather than insurmountable obstacles.

Remember: you don’t have to navigate these waters alone. Expert service providers specialize in exactly these situations, offering friendly and caring support combined with practical expertise. Their helpful solutions can transform a stressful situation into a successful closing, allowing property owners to move forward with confidence toward their real estate goals.

The title problems that seem overwhelming today become tomorrow’s success stories when approached with knowledge, patience, and the right professional support.

References

[1] Title Industry Operational Challenges and File Complexity Data, 2024-2025

[2] Title Company Regulatory Compliance Requirements, Anti-Money Laundering Regulations, 2025

[3] Business Email Compromise and Real Estate Fraud Statistics, FBI Internet Crime Report, 2023-2024

[4] Title Insurance Premium Volume Data, Q2 2025, Industry Financial Reports

[5] Consumer Financial Protection Bureau (CFPB) Regulatory Guidance and Cybersecurity Requirements for Title Companies, 2025

[7] National Flood Insurance Program (NFIP) Government Shutdown Impact Analysis, 2025

[8] Title Industry Workforce Shortage and Retirement Projections, Industry Association Data, 2025

Sure Path is a family-owned, curative-title cash buyer. We handle the paperwork and pay what’s owed at closing — no fees, no repairs, no pressure.