Sharing property ownership with another person can feel like navigating a maze with no clear exit. Whether you inherited a house with siblings, purchased investment property with a business partner, or found yourself co-owning real estate through divorce, the day often comes when one owner wants out—or when you want to take full control. Understanding how to execute a Tenants in Common Buyout: How to Buy Out a Co-Owner can transform a complicated shared ownership situation into a clean, straightforward path to sole ownership.

This comprehensive guide walks through every step of the buyout process, from initial valuation to final title transfer, providing helpful solutions for even the most complex co-ownership scenarios.

Key Takeaways

- Tenants in common ownership allows multiple owners to hold different percentage shares of a property with individual rights to sell or transfer their portion

- Property valuation is the critical first step—obtain a professional appraisal to establish fair market value before negotiating a buyout price

- Financing options for buyouts include cash purchases, refinancing, home equity loans, seller financing, or partnership with real estate solution companies

- Legal documentation must be properly executed, including purchase agreements, deed transfers, and title updates to ensure clean ownership transfer

- Professional guidance from real estate experts, attorneys, and title professionals can help navigate complex situations involving liens, judgments, or title issues

Understanding Tenants in Common Ownership

Before diving into the buyout process, it’s essential to understand what tenants in common ownership actually means and how it differs from other co-ownership structures.

What Is Tenants in Common?

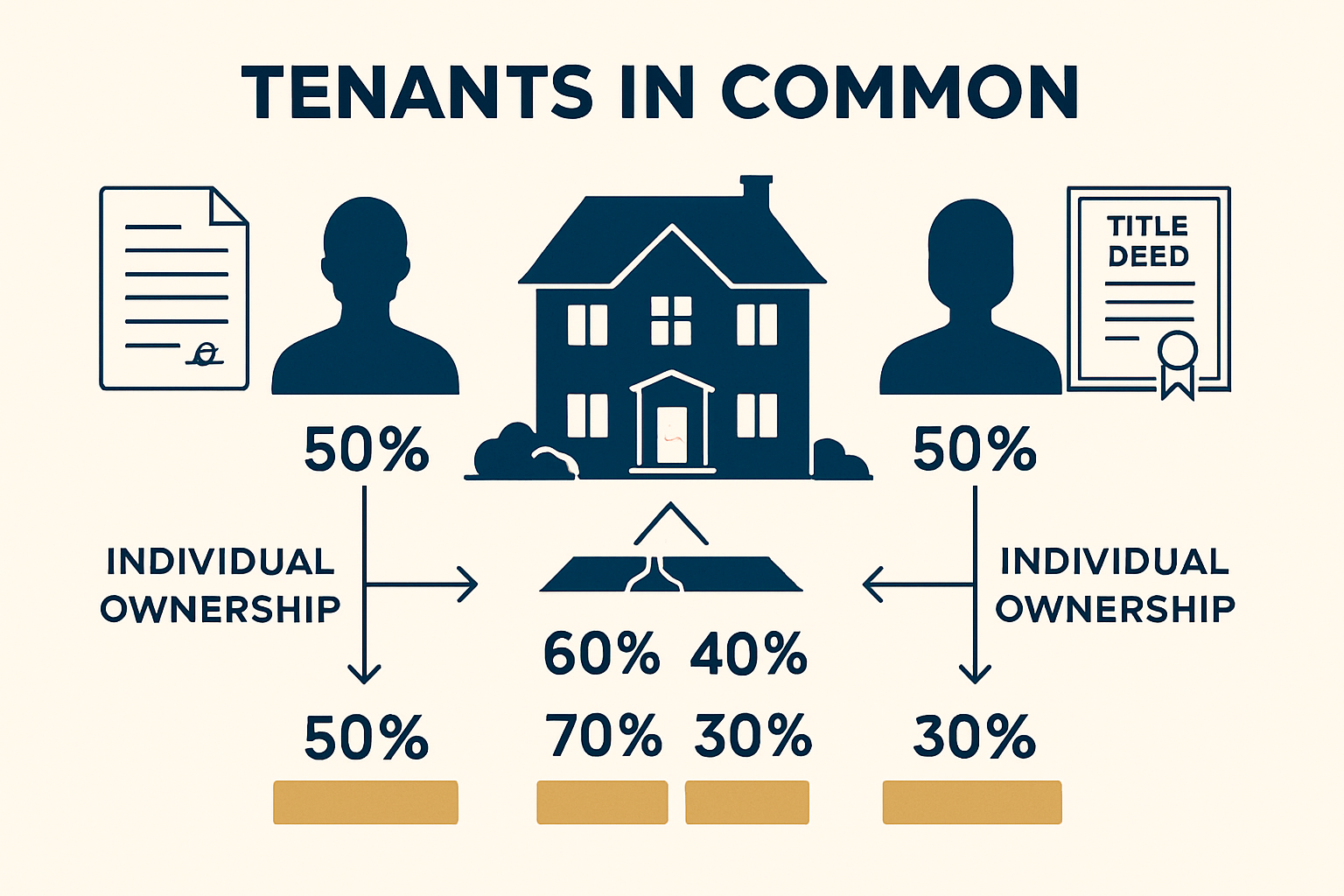

Tenants in common (TIC) is a form of concurrent property ownership where two or more people hold undivided interests in real estate. Unlike joint tenancy, each tenant in common:

- Owns a specific percentage of the property (not necessarily equal shares)

- Can sell, transfer, or mortgage their portion independently

- Can pass their share to heirs through a will or estate

- Has no automatic right of survivorship

Think of it like owning slices of a pie. One person might own 60% while another owns 40%. Each owner has rights to the entire property, but their financial stake differs.

Common Scenarios Leading to TIC Ownership

Several situations frequently result in tenants in common arrangements:

🏠 Inheritance: Multiple siblings inherit a family home and become co-owners

💼 Investment partnerships: Business partners purchase rental property together

💔 Divorce settlements: Former spouses maintain shared ownership temporarily

👨👩👧👦 Family purchases: Parents and adult children buy property together

🤝 Unmarried couples: Partners purchase real estate without marriage

Each scenario brings unique challenges when one party wants to exit the arrangement. That’s where understanding the Tenants in Common Buyout: How to Buy Out a Co-Owner process becomes invaluable.

Why Co-Owners Seek Buyouts

The reasons for pursuing a buyout are as varied as the ownership arrangements themselves:

- Financial strain: One owner can’t afford ongoing expenses like property taxes, insurance, or maintenance

- Disagreements: Co-owners clash over property use, rental decisions, or improvement plans

- Life changes: Relocation, marriage, divorce, or career shifts make continued ownership impractical

- Estate planning: Simplifying assets before retirement or for inheritance purposes

- Investment strategy: One owner wants to liquidate while the other wants to hold long-term

When multiple owners of property can’t agree on the future, a buyout often provides the cleanest resolution.

Preparing for a Tenants in Common Buyout: How to Buy Out a Co-Owner

Successful buyouts don’t happen by accident. They require careful preparation, clear communication, and strategic planning.

Step 1: Review Your Ownership Agreement

Start by examining any existing co-ownership documents:

- Deed: Confirms ownership percentages and how title is held

- Partnership agreements: May outline buyout procedures or first-refusal rights

- Operating agreements: For LLC-owned properties, these govern transfer procedures

- Trust documents: If property is held in trust, review trustee powers

Many co-owners discover they’ve already agreed to specific buyout terms without realizing it. These documents provide the legal framework for your transaction.

Step 2: Communicate Your Intentions

Open, honest communication sets the foundation for a smooth buyout:

Best practices for initial conversations:

✅ Choose a neutral, private setting

✅ Explain your reasons without blame or emotion

✅ Express willingness to negotiate fairly

✅ Propose a timeline for the process

✅ Suggest bringing in professional help

What to avoid:

❌ Making ultimatums or threats

❌ Discussing buyouts during heated arguments

❌ Presenting it as a done deal before negotiation

❌ Involving too many outside parties initially

Remember, the goal is reaching a mutually beneficial agreement. Approaching the conversation with helpful guidance and respect increases the likelihood of success.

Step 3: Determine Property Value

Accurate valuation is the cornerstone of any fair buyout. Without it, negotiations lack a solid foundation.

Valuation methods include:

| Method | Best For | Pros | Cons |

|---|---|---|---|

| Professional appraisal | All situations | Most accurate, legally defensible | Costs $300-$600 |

| Comparative Market Analysis (CMA) | Standard residential | Free from real estate agents | Less formal than appraisal |

| Broker Price Opinion (BPO) | Investment properties | Middle ground on cost/accuracy | Not as detailed as appraisal |

| Online estimators | Initial estimates only | Free, instant | Often inaccurate, not legally valid |

Pro tip: When co-owners disagree on value, consider hiring two independent appraisers and averaging their valuations, or agreeing to use a single appraiser selected jointly.

For properties with complications like liens and judgments or property tax issues, professional valuation becomes even more critical. These issues affect both current value and the buyout structure.

Step 4: Calculate the Buyout Amount

Once you have the property value, calculating the buyout amount involves several considerations:

Basic formula:

Buyout Amount = (Property Value × Co-owner's Percentage) - Adjustments

Common adjustments include:

- Outstanding mortgage balance: Who pays what portion?

- Property improvements: Did one owner invest more in upgrades?

- Deferred maintenance: Has one owner neglected their share of upkeep?

- Unpaid expenses: Are there outstanding property taxes, insurance, or HOA fees?

- Rental income: Has one owner collected rent without sharing?

Example calculation:

Property appraised value: $400,000

Co-owner’s share: 50%

Base buyout amount: $200,000

Less: Their share of mortgage ($100,000 × 50%): -$50,000

Less: Unpaid property taxes they owe: -$3,000

Net buyout amount: $147,000

This calculation can become complex quickly. When dealing with inherited property or properties with multiple liens, professional guidance ensures all factors are properly accounted for.

Financing Your Tenants in Common Buyout: How to Buy Out a Co-Owner

Having the funds to complete the buyout is often the biggest hurdle. Fortunately, several financing options exist.

Cash Purchase

The simplest approach is paying cash for your co-owner’s share.

Advantages:

- No loan approval process

- Faster closing

- No interest costs

- Stronger negotiating position

Considerations:

- Requires substantial liquid assets

- May deplete emergency reserves

- Opportunity cost of invested funds

Refinancing the Existing Mortgage

If the property has an existing mortgage, refinancing allows you to pay off the current loan and buy out your co-owner simultaneously.

How it works:

- Apply for a new mortgage in your name only

- New loan amount covers remaining mortgage balance plus buyout amount

- At closing, existing mortgage is paid off and co-owner receives their share

- You become sole owner with a new mortgage

Requirements:

- Sufficient income to qualify alone

- Good credit score (typically 620+)

- Adequate equity in the property

- Debt-to-income ratio under 43-50%

Example:

Current property value: $500,000

Existing mortgage balance: $200,000

Co-owner’s 50% share: $250,000

Less their mortgage portion: -$100,000

Buyout amount needed: $150,000

New mortgage amount: $350,000 ($200,000 existing + $150,000 buyout)

Loan-to-value ratio: 70% (generally acceptable)

Home Equity Loan or HELOC

If you already own other property, tapping that equity can fund the buyout.

Home Equity Loan:

- Lump sum payment

- Fixed interest rate

- Predictable monthly payments

- Typically allows borrowing up to 80-85% combined loan-to-value

Home Equity Line of Credit (HELOC):

- Draw funds as needed

- Variable interest rate

- Interest-only payments during draw period

- More flexibility for staged buyouts

Seller Financing

Sometimes the co-owner being bought out is willing to finance the purchase themselves.

Structure:

- You make a down payment (typically 10-30%)

- Co-owner holds a note for the remaining balance

- You make monthly payments with agreed interest

- After full payment, they sign over their share

Benefits for both parties:

For the buyer:

- Easier qualification than traditional loans

- Potentially lower closing costs

- Flexible terms

For the selling co-owner:

- Earns interest on the sale

- Spreads tax liability over multiple years

- Maintains some security interest until paid

Important: Seller financing arrangements should always be formalized with proper legal documentation to protect both parties.

Partnership with Real Estate Solution Companies

When traditional financing isn’t available or the situation is complex, partnering with companies that specialize in complicated real estate scenarios offers an alternative path.

Sure Path Property Solutions provides expert service for owners facing challenging situations like:

- Properties with significant back taxes

- Multiple heirs with conflicting interests

- Clouded title issues

- Properties in pre-foreclosure

- Situations where traditional buyers can’t or won’t engage

These industry experts can help structure creative solutions, coordinate with counties and title professionals, and provide the helpful guidance needed to navigate complex buyout scenarios.

The Legal Process of Buying Out a Co-Owner

Once financing is secured, the legal mechanics of transferring ownership must be executed properly.

Essential Legal Documents

A complete buyout requires several key documents:

1. Purchase Agreement

This contract outlines:

- Purchase price and payment terms

- Closing date

- Contingencies (financing, title review, etc.)

- Representations and warranties

- Who pays closing costs

- Default provisions

2. Quitclaim or Warranty Deed

The transferring co-owner signs a deed conveying their interest:

- Quitclaim deed: Transfers whatever interest the grantor has, with no warranties

- Warranty deed: Guarantees clear title and defends against claims

Most buyouts use quitclaim deeds between co-owners, but warranty deeds provide more protection.

3. Settlement Statement

Documents all financial aspects of the transaction:

- Purchase price

- Prorations (taxes, insurance, HOA fees)

- Payoffs (mortgages, liens)

- Closing costs

- Net proceeds to each party

4. Mortgage Documents

If obtaining new financing:

- Loan application

- Promissory note

- Mortgage or deed of trust

- Disclosure documents

5. Title Insurance Policy

Protects against undiscovered title defects. When buying out a co-owner, obtaining an owner’s title insurance policy in your name alone is wise protection.

Working with Professionals

Attempting a buyout without professional help is like performing surgery on yourself—technically possible but highly inadvisable.

Key professionals to engage:

👨⚖️ Real Estate Attorney

- Reviews and drafts legal documents

- Ensures compliance with state laws

- Handles title issues

- Represents your interests

- Cost: $500-$2,500 depending on complexity

📊 Real Estate Appraiser

- Provides objective property valuation

- Creates detailed appraisal report

- Defends valuation if challenged

- Cost: $300-$600 for residential

🏦 Mortgage Lender or Broker

- Evaluates financing options

- Pre-approves loan applications

- Coordinates closing

- Cost: Paid through loan fees/interest

📋 Title Company

- Conducts title search

- Identifies liens and encumbrances

- Issues title insurance

- Facilitates closing

- Cost: Varies by location, typically $500-$2,000

🏠 Real Estate Solution Specialists

For complicated situations, companies like Sure Path Property Solutions offer comprehensive support, coordinating between all parties and providing trustworthy service throughout the process.

Title Search and Clearing Issues

Before completing the buyout, a thorough title search identifies any problems that could affect ownership:

Common title issues:

- Outstanding liens (tax, judgment, mechanic’s)

- Unpaid property taxes

- Undisclosed heirs or ownership claims

- Errors in prior deeds

- Easements or encroachments

- Unreleased mortgages

If issues are discovered, they must be resolved before clean title can transfer. This might involve:

- Paying off liens

- Obtaining lien releases

- Filing quiet title actions

- Correcting deed errors

- Negotiating with creditors

Properties with judgment liens or tax liens require special attention. These encumbrances typically must be satisfied before or at closing.

Negotiating the Buyout Terms

Even with a fair valuation, negotiation skills can make the difference between a smooth transaction and a contentious battle.

Key Negotiation Points

Purchase price: While the appraisal provides a baseline, the final price is negotiable based on:

- Market conditions

- Property condition

- Urgency of either party

- Comparable sales

- Unique property features

Payment structure:

- Lump sum at closing

- Installment payments over time

- Combination of cash and note

- Assumption of debts in lieu of cash

Closing timeline:

- Immediate (30-45 days)

- Extended (6-12 months to arrange financing)

- Contingent on specific events

Responsibility for costs:

- Closing costs

- Title insurance

- Attorney fees

- Appraisal costs

- Recording fees

- Transfer taxes

Interim property management:

- Who maintains the property during the buyout process?

- How are expenses shared until closing?

- Who collects rent if it’s an investment property?

Strategies for Successful Negotiation

1. Lead with fairness: Approach negotiations seeking a win-win outcome, not trying to “beat” your co-owner.

2. Document everything: Put all agreements in writing, even preliminary ones.

3. Stay objective: Remove emotion from the process. Focus on facts, numbers, and fair market value.

4. Consider their perspective: Understanding what your co-owner truly wants (quick cash, maximum value, tax advantages) helps structure appealing offers.

5. Build in flexibility: Offering options (e.g., “We can close in 30 days for $145,000 or 90 days for $150,000”) often breaks deadlocks.

6. Know your limits: Determine your maximum price and minimum terms before negotiating.

7. Use professional mediators: If direct negotiation stalls, a neutral mediator can facilitate productive discussions.

When Negotiations Fail: Legal Alternatives

Sometimes, despite best efforts, co-owners can’t reach agreement. Legal remedies include:

Partition Action

A partition action lawsuit forces the sale or physical division of property when co-owners can’t agree.

Two types:

- Partition in kind: Physical division of the property (rare for residential)

- Partition by sale: Court-ordered sale with proceeds divided

Downsides:

- Expensive (often $10,000-$50,000+ in legal fees)

- Time-consuming (6-18 months or more)

- Court-supervised sale often yields below-market prices

- Damages relationships permanently

When it makes sense:

- All other negotiation attempts have failed

- One co-owner refuses to engage

- Ownership percentages are disputed

- The property is generating losses

Partition should be a last resort. The costs and stress usually exceed what either party would lose by compromising.

Tax Implications of a Tenants in Common Buyout

Understanding the tax consequences helps both parties make informed decisions and avoid surprises.

For the Selling Co-Owner

Capital Gains Tax

When selling their share, the co-owner may owe capital gains tax on any profit.

Calculation:

Capital Gain = Sale Price - (Original Cost Basis + Improvements - Depreciation)

Tax rates (2025):

- Short-term (owned less than 1 year): Ordinary income rates (10-37%)

- Long-term (owned more than 1 year): 0%, 15%, or 20% depending on income

Example:

Original purchase price (50% share): $100,000

Improvements paid by this owner: $15,000

Buyout price received: $150,000

Capital gain: $150,000 – $115,000 = $35,000

Tax (15% bracket): $5,250

Primary residence exclusion: If the property was the seller’s primary residence for 2 of the last 5 years, they may exclude up to $250,000 ($500,000 married) of gain.

Installment sale treatment: If receiving payments over time, taxes can be spread across multiple years using installment sale reporting.

For the Buying Co-Owner

New cost basis: The buying owner’s new basis includes:

- Their original ownership share cost

- Amount paid for co-owner’s share

- Acquisition costs (legal fees, title insurance, etc.)

This higher basis reduces future capital gains if the property is later sold.

No immediate tax: Simply buying out a co-owner doesn’t trigger taxable income for the buyer.

Mortgage interest deduction: Interest on loans used to buy out a co-owner may be deductible if the property is:

- Your primary residence

- A qualified second home

- A rental property (deducted as business expense)

Gift Tax Considerations

If the buyout price is below fair market value, the IRS may consider the difference a gift.

2025 gift tax rules:

- Annual exclusion: $18,000 per recipient

- Lifetime exemption: $13.61 million

- Gifts exceeding annual exclusion require filing Form 709

Example: If a property share worth $200,000 is sold to a co-owner for $150,000, the $50,000 difference could be considered a gift.

Professional Tax Advice

Tax rules are complex and change frequently. Both parties should consult with tax professionals before finalizing buyout terms to:

- Optimize tax treatment

- Understand reporting requirements

- Structure the transaction tax-efficiently

- Avoid unexpected tax bills

Special Situations in Tenants in Common Buyouts

Certain scenarios add layers of complexity to the buyout process.

Inherited Property with Multiple Heirs

When siblings or other heirs inherit property as tenants in common, emotions often run high.

Common challenges:

- Sentimental attachment: One heir wants to keep the family home while others want to sell

- Unequal financial capacity: Some heirs can afford buyouts, others can’t

- Geographic distance: Heirs live in different states or countries

- Family dynamics: Old conflicts resurface during negotiations

Helpful solutions:

✅ Establish clear communication: Regular family meetings (in person or virtual) keep everyone informed

✅ Hire a neutral appraiser: Removes accusations of favoritism in valuation

✅ Consider creative structures: One heir might buy the property but grant others lifetime visitation rights

✅ Explore estate loans: Some lenders specialize in loans to heirs for buyout purposes

✅ Work with specialists: Companies experienced in inherited property situations can mediate and facilitate solutions

Properties with Existing Liens or Judgments

Liens complicate buyouts because they must be addressed before clear title can transfer.

Types of liens affecting buyouts:

- Mortgage liens: Must be paid or assumed

- Tax liens: Federal, state, or local tax debts

- Judgment liens: From lawsuit judgments

- Mechanic’s liens: From unpaid contractor work

- HOA liens: Unpaid homeowner association fees

Resolution strategies:

- Pay at closing: Liens are satisfied from buyout proceeds

- Negotiate payoff: Sometimes creditors accept less than full amount

- Dispute invalid liens: Challenge liens that shouldn’t exist

- Structure around them: Buyer assumes certain liens with price adjustment

Understanding how to sell a house with a lien provides valuable insights applicable to buyout situations.

For properties with multiple complications, working with industry experts who specialize in liens ensures nothing is overlooked.

Investment Properties with Tenants

When the property being divided has tenants, additional considerations arise:

Lease obligations: Existing leases typically transfer with ownership and must be honored

Security deposits: Must be properly transferred or accounted for in the buyout

Rental income: How is income divided during the transition period?

Property management: Who handles tenant issues until closing?

Tenant notification: In some states, tenants must be notified of ownership changes

Best practice: Include lease assignments and security deposit transfers in the buyout agreement.

Properties in Foreclosure or Pre-Foreclosure

When a property faces foreclosure, time pressure intensifies.

Challenges:

- Limited time before foreclosure sale

- Damaged credit for all owners

- Reduced property value

- Difficulty obtaining traditional financing

Options:

- Quick buyout with cash: If one owner has funds available

- Short sale: Both owners agree to sell to third party with lender approval

- Loan modification: Bring loan current and refinance into one owner’s name

- Deed in lieu: Transfer property to lender to avoid foreclosure

Properties in pre-foreclosure require immediate action. Consulting with professionals who understand foreclosure timelines and alternatives is critical.

Step-by-Step Process: Executing Your Buyout

Here’s a practical timeline for completing a Tenants in Common Buyout: How to Buy Out a Co-Owner:

Weeks 1-2: Initial Planning

- Review ownership documents (deed, agreements)

- Have initial conversation with co-owner

- Consult with real estate attorney

- Order professional appraisal

- Assess your financing options

Weeks 3-4: Valuation and Offer

- Receive appraisal report

- Calculate fair buyout amount

- Prepare written offer

- Present offer to co-owner

- Begin negotiations

Weeks 5-6: Agreement and Due Diligence

- Reach agreement on price and terms

- Execute purchase agreement

- Order title search

- Apply for financing (if needed)

- Review title report for issues

Weeks 7-8: Resolving Issues

- Address any title problems

- Obtain lien releases if necessary

- Finalize loan approval

- Review all closing documents

- Schedule closing date

Weeks 9-10: Closing

- Conduct final walkthrough (if applicable)

- Wire funds or confirm cashier’s check

- Sign all closing documents

- Co-owner signs deed transferring interest

- Record new deed with county

- Receive title insurance policy

- Update property insurance

- Celebrate sole ownership! 🎉

Note: This timeline assumes a relatively straightforward transaction. Complex situations may take 3-6 months or longer.

Common Mistakes to Avoid

Learning from others’ errors can save time, money, and relationships.

1. Skipping Professional Appraisal

The mistake: Using online estimates or “gut feelings” about value

Why it’s problematic: Creates disputes and undermines negotiation credibility

The solution: Invest in a professional appraisal from a licensed, independent appraiser

2. Ignoring Hidden Costs

The mistake: Focusing only on the buyout price

Overlooked expenses:

- Closing costs (2-5% of purchase price)

- Attorney fees

- Title insurance

- Recording fees

- Loan origination fees

- Appraisal costs

- Inspection fees

- Prorated property taxes and insurance

The solution: Create a comprehensive budget including all transaction costs

3. Verbal Agreements Only

The mistake: Relying on handshake deals or verbal promises

Why it fails: Memories differ, circumstances change, and verbal agreements are difficult to enforce

The solution: Document everything in writing, even preliminary agreements

4. Neglecting Title Issues

The mistake: Assuming title is clear without verification

Potential problems:

- Undisclosed liens

- Judgment attachments

- Tax delinquencies

- Easement disputes

- Prior deed errors

The solution: Order a title search early and address issues before closing

5. Poor Communication

The mistake: Avoiding difficult conversations or communicating through third parties

Consequences: Misunderstandings, hurt feelings, and failed negotiations

The solution: Maintain direct, respectful, honest communication throughout the process

6. Unrealistic Timelines

The mistake: Expecting to complete a buyout in days or weeks

Reality: Most buyouts take 2-4 months, complex situations take longer

The solution: Set realistic expectations and build buffer time into your timeline

7. Ignoring Tax Implications

The mistake: Failing to consider tax consequences until after closing

Potential issues: Unexpected tax bills, missed deductions, inefficient structuring

The solution: Consult tax professionals before finalizing terms

Alternatives to Buying Out a Co-Owner

Sometimes a buyout isn’t the best solution. Consider these alternatives:

Option 1: Sell to a Third Party

Instead of one co-owner buying out the other, sell the property to an outside buyer and split proceeds.

Advantages:

- Neither owner needs financing

- Market determines price (less dispute)

- Clean break for both parties

- Potentially higher sale price

Disadvantages:

- Both owners must agree to sell

- Transaction costs reduce net proceeds

- Neither retains the property

- May trigger larger capital gains

Option 2: Continue Co-Ownership with New Agreement

Sometimes the relationship can be salvaged with clearer terms.

Create a formal co-ownership agreement addressing:

- Decision-making processes

- Expense sharing formulas

- Property use schedules

- Maintenance responsibilities

- Exit strategies

- Dispute resolution procedures

When this works:

- The property is profitable

- Disagreements are about process, not fundamental goals

- Both owners want to retain ownership

- The relationship can be repaired

Option 3: Lease Your Share

If you want out but your co-owner can’t buy you out, consider leasing your ownership interest to them.

Structure:

- Co-owner pays you monthly rent for your share

- They have exclusive use of the property

- You retain ownership and appreciation potential

- Option to revisit buyout later

Considerations:

- Requires careful legal documentation

- You remain liable for your share of mortgage and taxes

- Creates landlord-tenant relationship with co-owner

Option 4: Exchange Properties

If both co-owners have other real estate, consider trading assets.

Example: You own 50% of Property A together. Your co-owner also owns Property B alone. They transfer Property B to you in exchange for your share of Property A.

Advantages:

- No cash needed

- Both parties get sole ownership

- Potential tax advantages through 1031 exchange

Challenges:

- Properties must have similar values

- Complex tax implications

- Requires both properties to be investment/business use for 1031 treatment

Working with Sure Path Property Solutions

When your co-ownership situation involves complications like back taxes, liens, judgments, or unclear title, partnering with specialists can make all the difference.

Sure Path Property Solutions provides friendly and caring support for property owners facing challenging circumstances:

How We Help with Complex Buyouts

Situation assessment: We evaluate your unique circumstances and identify the best path forward

Title resolution: Our team coordinates with counties and title professionals to clear title issues

Creative solutions: We structure deals that work when traditional approaches fail

Multiple owner coordination: We facilitate communication and agreement among multiple co-owners

Back tax resolution: We help navigate property tax issues that complicate ownership

Lien negotiation: We work with creditors to resolve liens that block clean transfers

Who We Serve

Our expert service is particularly valuable for:

- Properties with significant delinquent taxes

- Multiple heirs who can’t agree on property disposition

- Co-owners facing foreclosure

- Properties with clouded or defective title

- Situations where traditional buyers won’t engage

- Owners who need to sell quickly due to financial hardship

Our Approach

We believe in providing helpful guidance with transparency and integrity. Our process:

- Free consultation: Discuss your situation with no obligation

- Comprehensive evaluation: We research title, liens, taxes, and ownership structure

- Clear options: We present solutions in plain language

- Coordinated execution: We handle details and keep all parties informed

- Clean closing: We ensure proper documentation and title transfer

When you’re facing a complicated co-ownership situation, you don’t have to navigate it alone. Contact our team to discuss how we can help.

Frequently Asked Questions

Can I force my co-owner to sell their share to me?

No, you cannot force a co-owner to sell to you specifically. However, you can file a partition action to force a sale of the entire property, with proceeds divided among owners. This is expensive and should be a last resort.

What if my co-owner refuses to cooperate at all?

If a co-owner completely refuses to engage, your options include:

- Hiring a mediator to facilitate communication

- Having an attorney send a formal proposal

- Filing a partition lawsuit

- Selling your share to a third-party investor (though this may be at a discount)

How long does a typical buyout take?

A straightforward buyout typically takes 60-90 days from initial agreement to closing. Complex situations involving title issues, difficult financing, or legal disputes can take 6-12 months or longer.

Do I need an attorney for a buyout?

While not legally required in all states, hiring a real estate attorney is highly recommended. The cost ($500-$2,500) is minimal compared to the protection and expertise provided.

Can I buy out a co-owner if there’s an existing mortgage?

Yes, but the existing mortgage must be addressed. Options include:

- Refinancing in your name alone

- Assuming the existing mortgage (if lender allows)

- Paying off the mortgage as part of the buyout

- Having the co-owner remain on the mortgage temporarily (risky for them)

What happens if we can’t agree on the property value?

If co-owners dispute value, solutions include:

- Each hiring an appraiser and averaging the results

- Agreeing to use a single appraiser chosen jointly

- Using a mediator to facilitate agreement

- One owner offering the other first right to buy at their stated price

Are buyout proceeds taxable?

For the selling co-owner, proceeds may be subject to capital gains tax on any profit over their cost basis. The primary residence exclusion may apply if they lived in the property. Consult a tax professional for your specific situation.

Can I buy out a co-owner with seller financing?

Yes, if the co-owner agrees. You would make a down payment and pay the balance over time with interest. This arrangement should be formalized with a promissory note and recorded mortgage or deed of trust.

What if the property has more debt than value?

If the property is underwater (mortgage exceeds value), a traditional buyout may not work. Options include:

- Negotiating a short sale with the lender

- Both owners contributing to pay down the mortgage

- Walking away and allowing foreclosure (damages credit for both)

- One owner taking over payments and assuming the negative equity

How do I remove my co-owner from the deed?

Your co-owner must voluntarily sign a quitclaim or warranty deed transferring their interest to you. This deed must be properly executed, notarized, and recorded with the county recorder’s office. They won’t do this until they receive their buyout payment.

Conclusion: Taking Control of Your Property Future

Navigating a Tenants in Common Buyout: How to Buy Out a Co-Owner can feel overwhelming, especially when emotions, finances, and legal complexities intersect. But with the right approach, professional guidance, and commitment to fairness, you can successfully transition from shared ownership to sole control of your property.

Key Steps to Remember

✅ Start with accurate valuation from a professional appraiser

✅ Explore all financing options including refinancing, home equity, seller financing, or partnership with solution specialists

✅ Document everything in writing from initial offers through final closing

✅ Address title issues early to avoid delays and surprises

✅ Engage qualified professionals including attorneys, title companies, and real estate experts

✅ Communicate openly and respectfully with your co-owner throughout the process

✅ Consider tax implications and consult with tax professionals before finalizing terms

✅ Be patient but persistent as the process takes time but yields valuable results

Your Next Steps

If you’re ready to move forward with buying out your co-owner:

- Gather your documents: Collect your deed, mortgage statements, and any co-ownership agreements

- Assess your situation: Identify any complicating factors like liens, back taxes, or title issues

- Get professional help: Consult with a real estate attorney and consider ordering an appraisal

- Explore financing: Talk to lenders about your options or consider alternative solutions

- Reach out for expert guidance: If your situation involves complications, contact Sure Path Property Solutions for a free consultation

When You Need Specialized Help

Co-ownership situations involving multiple heirs, significant back taxes, liens, judgments, or unclear title require specialized expertise. Sure Path Property Solutions has helped countless property owners navigate these exact challenges with trustworthy service and practical solutions.

We understand that every co-ownership situation is unique, and cookie-cutter approaches don’t work for complex scenarios. Our team takes time to understand your specific circumstances, research all aspects of your property, and present clear options that work for your situation.

Whether you’re trying to buy out siblings from an inherited property, dealing with a co-owner who’s stopped paying their share of expenses, or facing foreclosure on a jointly-owned property, we provide the helpful solutions and expert service you need.

Don’t let a complicated co-ownership situation prevent you from moving forward. The path to sole ownership—or a fair exit from shared ownership—is clearer than you might think with the right guidance.

Visit our blog for more helpful resources on property ownership challenges, or reach out to our team today to discuss your specific situation.

Your property future is too important to leave to chance. Take control today with a clear plan for your Tenants in Common Buyout: How to Buy Out a Co-Owner.

Sure Path is a family-owned, curative-title cash buyer. We handle the paperwork and pay what’s owed at closing — no fees, no repairs, no pressure.

See how we help with selling a property with multiple heirs →