How to Negotiate Tax Lien Payoff: Strategies & Settlement Options

Imagine opening your mail to find a tax lien notice attached to your property. Your heart sinks. The amount owed seems insurmountable, and the threat of losing your home or land feels very real. But here’s the good news: tax liens aren’t always set in stone. With the right approach and helpful guidance, many property owners successfully negotiate their tax lien payoffs for significantly less than the original amount owed. Understanding how to negotiate tax lien payoff: strategies & settlement options can transform what feels like an impossible situation into a manageable path forward.

Tax authorities want to collect what they’re owed, but they also recognize that getting something is better than nothing. This creates an opportunity for property owners facing financial hardship to explore settlement options that work for both parties. Whether you’re dealing with federal tax liens, state tax liens, or local property tax debts, negotiation strategies exist that can reduce your burden and help you regain clear title to your property.

Key Takeaways

- Tax liens can often be negotiated for less than the full amount through programs like Offer in Compromise, installment agreements, or penalty abatement

- Documentation is critical – having complete financial records and proof of hardship strengthens your negotiation position significantly

- Multiple settlement options exist including payment plans, lump-sum reductions, currently not collectible status, and innocent spouse relief

- Professional guidance improves outcomes – tax attorneys, enrolled agents, and industry experts understand negotiation strategies that maximize your chances of approval

- Timing matters – acting quickly before liens escalate to foreclosure gives you more negotiation leverage and options

Understanding Tax Liens and Why They’re Negotiable

A tax lien represents the government’s legal claim against your property when you fail to pay tax debts. Unlike other types of liens, tax liens take priority over most other creditors and can severely impact your ability to sell, refinance, or transfer property ownership.

What Makes Tax Liens Different

Tax liens attach to all your current and future assets until the debt is satisfied. They appear on credit reports, damage credit scores, and signal to potential buyers that your property has encumbrances. The IRS, state revenue departments, and local tax collectors all have the authority to place liens and eventually foreclose if debts remain unpaid.

However, tax authorities are also practical. They understand that:

- Collection costs money – pursuing foreclosure involves legal fees, administrative expenses, and time

- Some taxpayers genuinely can’t pay – financial hardship is real, and extracting payment from someone with no resources is impossible

- Partial payment beats no payment – accepting a reduced settlement or payment plan often makes more financial sense than lengthy collection efforts

This practical reality creates the foundation for negotiation. Tax agencies have established formal programs specifically designed to resolve tax debts for less than the full amount or through manageable payment arrangements.

Types of Tax Liens You Can Negotiate

Different tax authorities offer different negotiation programs:

Federal Tax Liens (IRS)

- Offer in Compromise programs

- Installment agreements (short-term and long-term)

- Currently Not Collectible status

- Penalty abatement

- Innocent spouse relief

State Tax Liens

- State-specific settlement programs

- Payment plan options

- Hardship considerations

- Voluntary disclosure agreements

Local Property Tax Liens

- County or municipal payment plans

- Senior citizen exemptions

- Hardship deferrals

- Tax sale redemption periods

Understanding which type of lien you’re facing helps determine which strategies and settlement options will be most effective for your situation.

How to Negotiate Tax Lien Payoff: Core Strategies That Work

Successfully negotiating a tax lien payoff requires strategic planning, thorough documentation, and understanding what tax authorities will accept. These proven strategies have helped countless property owners reduce their tax burdens and move forward with their lives.

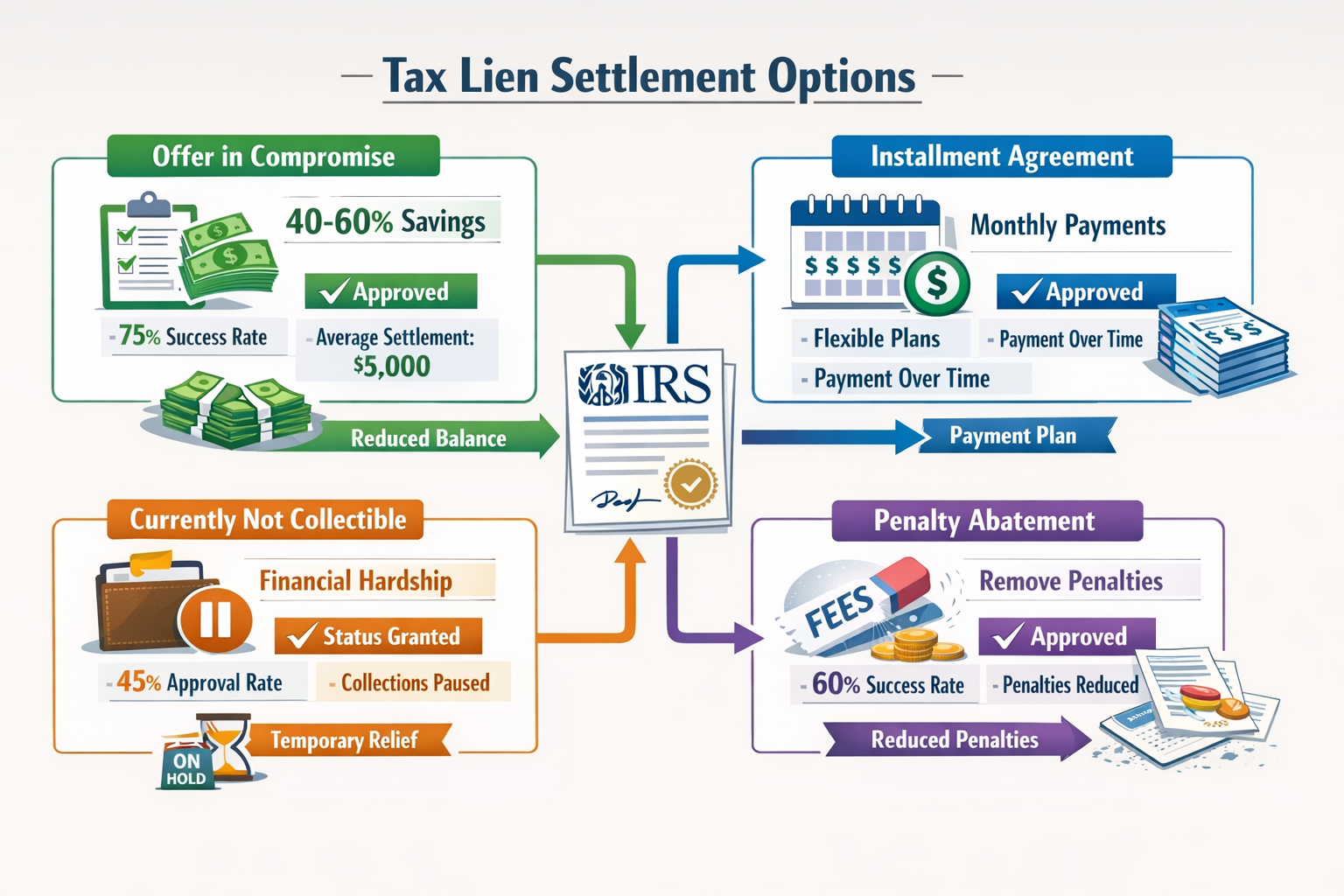

Strategy 1: Offer in Compromise (OIC)

An Offer in Compromise allows you to settle your tax debt for less than the full amount owed. The IRS and many state tax agencies accept OIC applications when they determine that collecting the full amount would create financial hardship or is unlikely to succeed.

How It Works:

The tax authority evaluates your reasonable collection potential (RCP) by analyzing:

- Your income and future earning ability

- Your expenses and necessary living costs

- The equity in your assets (including property)

- Your special circumstances

If your RCP is less than what you owe, you may qualify for a reduced settlement.

Typical Acceptance Criteria:

✅ Doubt as to collectibility – You can’t pay the full amount within the collection statute period

✅ Doubt as to liability – Legitimate questions exist about whether you actually owe the tax

✅ Effective tax administration – Collecting the full amount would create economic hardship or be unfair

Real-World Example:

Sarah owed $45,000 in back taxes with a federal tax lien on her inherited property. After losing her job and facing medical expenses, she submitted an OIC with detailed financial documentation showing she could only afford $12,000. The IRS accepted her offer, and she paid the reduced amount in five monthly installments. Once paid, the lien was released, and she could sell her property with clear title.

Strategy 2: Installment Agreements

If you can’t pay your tax debt immediately but can afford monthly payments, installment agreements provide a structured payment plan that prevents foreclosure while you pay down the debt.

Types of Installment Agreements:

| Agreement Type | Duration | Best For |

|---|---|---|

| Short-term | 120 days or less | Debts under $100,000; temporary cash flow issues |

| Long-term | Up to 72 months | Larger debts; steady income but limited lump-sum capacity |

| Partial payment | Until collection statute expires | When full payment isn’t possible before statute runs out |

| Streamlined | Up to 72 months | Debts under $50,000 (IRS); simplified approval process |

Advantages:

- Stops collection actions and prevents foreclosure

- No extensive financial documentation for streamlined agreements

- Interest and penalties continue but at reduced rates

- Protects your property while you pay down the debt

- Can be combined with penalty abatement requests

Important Considerations:

The lien typically remains in place until the debt is paid in full. However, having an active installment agreement demonstrates good faith and prevents the tax authority from pursuing more aggressive collection actions like seizure or foreclosure.

Strategy 3: Currently Not Collectible (CNC) Status

If you’re experiencing genuine financial hardship where paying your tax debt would prevent you from meeting basic living expenses, you may qualify for Currently Not Collectible status.

How CNC Status Works:

The tax authority temporarily suspends collection activities after determining that you have no ability to pay. The debt doesn’t disappear, but collection efforts stop, giving you breathing room to improve your financial situation.

Qualification Requirements:

- Monthly income barely covers (or doesn’t cover) necessary living expenses

- No assets that could be liquidated to pay the debt

- Detailed financial disclosure proving hardship

- Documentation of expenses (housing, food, medical, transportation)

What Happens During CNC Status:

📌 Collection activities cease

📌 The lien remains but isn’t actively enforced

📌 Interest and penalties continue to accrue

📌 The IRS periodically reviews your financial situation

📌 If your finances improve, collection resumes

CNC status works best as a temporary solution while you rebuild your finances or explore other settlement options. It’s particularly valuable for property owners who need time to arrange a sale or refinance.

Strategy 4: Penalty Abatement

Tax debts often include substantial penalties for late payment, failure to file, or accuracy issues. These penalties can sometimes exceed the original tax owed. Penalty abatement requests can significantly reduce your total debt.

Common Grounds for Penalty Abatement:

🔹 Reasonable cause – Serious illness, death in family, natural disaster, or other circumstances beyond your control

🔹 First-time penalty abatement – Clean compliance history for the previous three years

🔹 Statutory exception – Reliance on incorrect IRS advice or other specific statutory reasons

🔹 Administrative waiver – IRS determines penalties were incorrectly assessed

Success Tips:

Penalty abatement requests succeed when you provide:

- Detailed explanation of circumstances that prevented compliance

- Supporting documentation (medical records, death certificates, disaster declarations)

- Evidence of previous good compliance history

- Demonstration that you’ve now resolved the underlying issue

Even if the IRS or state tax authority won’t reduce the principal tax owed, eliminating penalties can reduce your debt by 25-40%, making the remaining balance much more manageable.

Settlement Options: Choosing the Right Path for Your Situation

Understanding how to negotiate tax lien payoff: strategies & settlement options means matching your specific circumstances to the most effective approach. No single solution works for everyone, so evaluating your financial situation honestly is critical.

Evaluating Your Financial Position

Before approaching tax authorities, complete a thorough financial assessment:

Income Analysis:

- Current monthly income from all sources

- Expected future income (job prospects, retirement, etc.)

- Income stability and reliability

Expense Documentation:

- Necessary living expenses (housing, food, utilities, transportation)

- Medical expenses and insurance

- Dependent care costs

- Court-ordered payments (child support, alimony)

Asset Inventory:

- Real estate equity (current market value minus mortgages)

- Vehicle equity

- Bank accounts and investments

- Retirement accounts

- Other valuable assets

Liability Assessment:

- Total tax debt (principal, interest, penalties)

- Other debts (mortgages, credit cards, medical bills)

- Priority of debts and liens

This assessment reveals your reasonable collection potential and guides which settlement option makes the most sense.

Matching Strategies to Circumstances

Different situations call for different approaches:

Scenario 1: Temporary Financial Hardship

Best Option: Short-term installment agreement or Currently Not Collectible status

Why: Preserves your ability to pay once circumstances improve without accepting a settlement that might not be necessary

Scenario 2: Permanent Inability to Pay Full Amount

Best Option: Offer in Compromise

Why: Settles the debt permanently for a reduced amount based on what you can actually afford

Scenario 3: Ability to Pay Principal but Not Penalties

Best Option: Penalty abatement combined with installment agreement

Why: Reduces total debt significantly while creating manageable payment terms for the remainder

Scenario 4: Need to Sell Property Quickly

Best Option: Lump-sum OIC or subordination request

Why: Clears the lien quickly so the property can be sold, with proceeds potentially funding the settlement

Scenario 5: Disputed Tax Liability

Best Option: Doubt as to liability OIC or formal appeals process

Why: Addresses the fundamental question of whether you actually owe the tax before negotiating payment

Working with Tax Professionals

While you can negotiate directly with tax authorities, professional representation significantly improves outcomes. Tax professionals understand the nuances of negotiation, know what documentation strengthens your case, and can communicate effectively with tax authorities.

Types of Tax Professionals:

Enrolled Agents (EAs)

- Federally licensed tax practitioners

- Authorized to represent taxpayers before the IRS

- Specialize in tax resolution and negotiation

- Often more affordable than attorneys

Tax Attorneys

- Licensed lawyers specializing in tax law

- Can provide legal representation in court

- Handle complex cases involving disputes or litigation

- Attorney-client privilege protects communications

Certified Public Accountants (CPAs)

- Licensed accounting professionals

- Can represent clients before the IRS

- Particularly valuable when tax issues involve business or complex financial situations

Property Solutions Specialists

- Companies like Sure Path Property Solutions that coordinate with tax professionals, title companies, and counties

- Provide helpful solutions for property owners facing liens and tax issues

- Navigate the intersection of tax liens and property sales

Professional representation costs money, but the potential savings often far exceed the fees. A skilled negotiator might secure an OIC acceptance that saves you tens of thousands of dollars or structure a payment plan that prevents foreclosure.

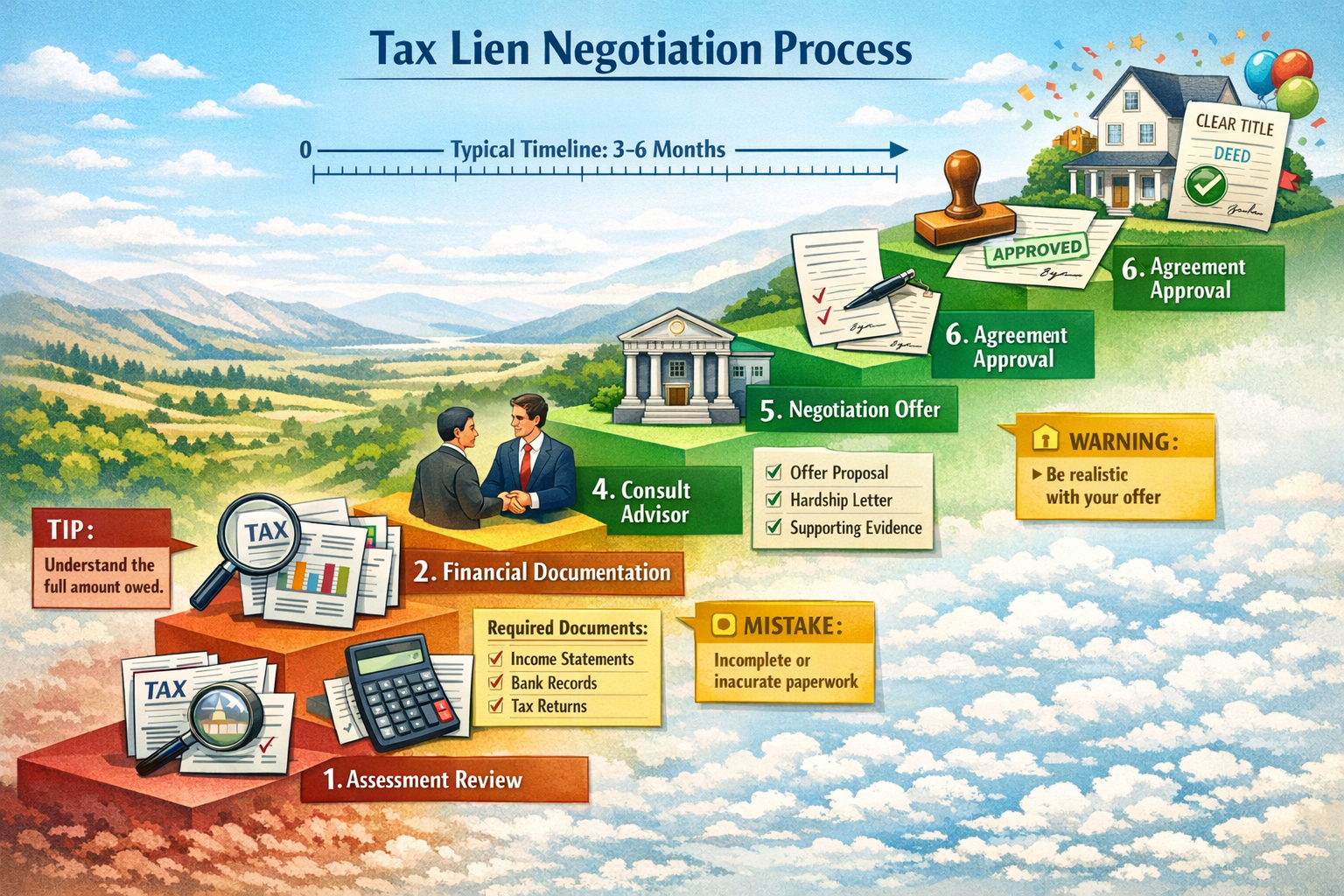

Step-by-Step Process for Negotiating Your Tax Lien Payoff

Knowing the right strategies is only half the battle. Successfully implementing those strategies requires following a systematic process that maximizes your chances of approval.

Step 1: Obtain Complete Tax Records

Before you can negotiate, you need to know exactly what you owe and why.

For Federal Tax Liens:

- Request your IRS account transcript online or by mail

- Review all tax periods with outstanding balances

- Verify the accuracy of assessments, penalties, and interest

- Check the Collection Statute Expiration Date (CSED)

For State and Local Tax Liens:

- Contact your state revenue department or county tax collector

- Request a detailed accounting of all amounts owed

- Verify property tax assessments are accurate

- Check for any exemptions or relief programs you might qualify for

Red Flags to Watch For:

⚠️ Incorrect tax assessments

⚠️ Penalties applied inappropriately

⚠️ Interest calculated incorrectly

⚠️ Payments not properly credited

⚠️ Identity theft or fraudulent returns

If you find errors, address them immediately through the appropriate dispute or correction process. You shouldn’t negotiate payment on debts you don’t actually owe.

Step 2: Gather Financial Documentation

Tax authorities require extensive documentation to evaluate settlement requests. Gathering these documents in advance speeds the process and demonstrates your seriousness.

Required Financial Documents:

📄 Income Verification

- Pay stubs (last 3-6 months)

- Tax returns (last 1-2 years)

- Social Security statements

- Pension or retirement income documentation

- Rental income records

📄 Expense Documentation

- Mortgage statements or rent receipts

- Utility bills

- Insurance policies

- Vehicle payments

- Medical expenses

- Childcare costs

📄 Asset Documentation

- Bank statements (last 3-6 months)

- Investment account statements

- Property deeds and recent appraisals

- Vehicle titles and valuations

- Retirement account statements

📄 Liability Documentation

- Mortgage balances

- Credit card statements

- Other loan documents

- Court-ordered payment obligations

Organization Tips:

Create a comprehensive financial package with clearly labeled sections. Tax authorities process thousands of requests; making their job easier improves your chances of approval. Consider creating a cover sheet that summarizes your financial situation and explains why you qualify for the settlement option you’re requesting.

Step 3: Determine Your Reasonable Collection Potential (RCP)

The IRS and many state tax agencies use RCP formulas to evaluate settlement offers. Understanding how they calculate your RCP helps you make realistic offers they’re likely to accept.

Basic RCP Formula:

RCP = (Monthly Disposable Income × Number of Months) + Net Realizable Equity in Assets

Monthly Disposable Income:

Gross monthly income minus allowable living expenses. Tax authorities use standardized expense allowances for many categories, which may be less than your actual expenses.

Number of Months:

- Lump-sum cash offers: 12 months (paid within 5 months) or 24 months (paid within 24 months)

- Periodic payment offers: Number of months remaining on collection statute

Net Realizable Equity:

Current market value of assets minus loans secured by those assets, minus costs of sale (typically 20% for real estate), minus an asset protection allowance.

Example Calculation:

John owes $60,000 in back taxes. His calculation:

- Monthly income: $4,500

- Allowable expenses: $3,800

- Disposable income: $700

- Months remaining on statute: 60 months

- Income component: $700 × 60 = $42,000

- Home equity: $80,000 market value – $70,000 mortgage – $16,000 cost of sale = -$6,000 (no equity)

- Vehicle equity: $8,000 value – $6,000 loan = $2,000

- Total RCP: $42,000 + $2,000 = $44,000

John could potentially offer $44,000 to settle his $60,000 debt, representing a $16,000 reduction.

Step 4: Submit Your Formal Request

Once you’ve determined the appropriate strategy and gathered documentation, submit your formal request using the correct forms and procedures.

For IRS Offers in Compromise:

- Complete Form 656 (Offer in Compromise)

- Complete Form 433-A (Collection Information Statement for Wage Earners and Self-Employed) or Form 433-B (for businesses)

- Include application fee ($205 as of 2026) unless you qualify for low-income waiver

- Include initial payment (20% for lump-sum offers, first payment for periodic payment offers)

- Submit to the appropriate IRS office based on your location

For IRS Installment Agreements:

- Apply online through IRS.gov (fastest method)

- Complete Form 9465 (Installment Agreement Request)

- For streamlined agreements under $50,000, minimal documentation required

- For larger amounts, complete Form 433-F (Collection Information Statement)

For State and Local Tax Settlements:

- Contact your state revenue department or county tax collector

- Request information about available settlement programs

- Complete required state-specific forms

- Provide documentation similar to IRS requirements

Submission Best Practices:

✅ Make copies of everything before submitting

✅ Send via certified mail with return receipt

✅ Keep detailed records of all communications

✅ Follow up if you don’t receive acknowledgment within 30 days

✅ Continue making any required payments while the request is pending

Step 5: Respond to Requests for Additional Information

Tax authorities almost always request additional documentation or clarification. Responding promptly and completely is critical to keeping your request moving forward.

Common Additional Requests:

- Updated financial information if processing takes several months

- Explanation of specific expenses that seem high

- Verification of asset values through appraisals

- Documentation of hardship circumstances

- Proof of income sources

Response Guidelines:

Treat every request as urgent. Tax authorities often set deadlines for responses (typically 10-30 days). Missing a deadline can result in your request being rejected without further consideration.

Provide exactly what’s requested—no more, no less. Additional unsolicited information can sometimes raise new questions or concerns. If you’re working with a tax professional, let them handle all communications to ensure consistency and appropriate framing.

Step 6: Negotiate and Finalize the Agreement

If the tax authority makes a counteroffer or requests modifications to your proposal, you’ve entered the negotiation phase. This is where expert guidance proves most valuable.

Negotiation Tactics:

🎯 Start with a reasonable offer – Lowball offers waste time and damage credibility

🎯 Justify every number – Explain why your offer represents fair value based on RCP

🎯 Be prepared to compromise – Meeting in the middle often leads to acceptance

🎯 Emphasize collection difficulties – Remind them that your offer may be their best opportunity to collect

🎯 Highlight special circumstances – Age, health issues, or economic conditions that support your position

If Your Request Is Denied:

Don’t give up. You have options:

- Request reconsideration – Provide additional documentation addressing the reasons for denial

- Appeal the decision – Formal appeals processes exist for most tax settlement programs

- Reapply later – If your financial situation worsens, you may qualify in the future

- Explore alternative strategies – If an OIC is denied, try an installment agreement or CNC status

Once Accepted:

Get everything in writing. Your acceptance letter should clearly state:

- The agreed-upon settlement amount or payment terms

- Payment due dates and methods

- Conditions you must meet (filing future returns on time, staying current on payments)

- When the lien will be released

- Consequences of defaulting on the agreement

Follow the terms precisely. Defaulting on a settlement agreement reinstates the full original debt plus any additional interest and penalties that accrued.

Special Considerations When Selling Property with Tax Liens

Many property owners need to negotiate tax lien payoffs specifically because they want to sell their property. The intersection of tax liens and property sales creates unique challenges and opportunities.

Understanding Lien Priority and Payoff at Closing

Tax liens typically take priority over other liens, including mortgages in many cases. This means they must be satisfied before you can transfer clear title to a buyer.

How Liens Are Handled at Closing:

When you sell property with a tax lien, the closing process typically works like this:

- Title search reveals the lien – Buyers’ title companies discover the lien during their examination

- Payoff amount is requested – The title company contacts the tax authority for an official payoff amount

- Funds are held in escrow – Sale proceeds are set aside to satisfy the lien

- Lien is paid at closing – The title company pays the tax authority directly from sale proceeds

- Release is obtained – The tax authority issues a lien release, clearing the title

- Remaining proceeds go to seller – After paying the lien and other closing costs, you receive the balance

This process works smoothly when sale proceeds exceed all liens and costs. But what if they don’t?

Negotiating Short Payoffs for Property Sales

If your property’s value has declined or you owe more in liens than the property is worth, you may need to negotiate a short payoff—accepting less than the full amount to facilitate the sale.

Why Tax Authorities Accept Short Payoffs:

Tax authorities recognize that:

- A property in poor condition may not sell for enough to cover all debts

- Foreclosure costs them money and time

- Getting partial payment now is better than uncertain future collection

- Allowing the sale prevents further deterioration of the property

How to Propose a Short Payoff:

📋 Obtain a professional appraisal – Document the current market value

📋 Get a purchase offer – A legitimate buyer’s offer proves market value

📋 Calculate net proceeds – Show what will be available after senior liens and closing costs

📋 Submit a formal request – Explain why accepting less facilitates resolution

📋 Emphasize collection alternatives – Describe the poor condition or limited marketability

Example:

Maria inherited a property worth $150,000 with a $120,000 mortgage and a $45,000 tax lien. After closing costs, the sale would net $140,000—not enough to pay both liens. She negotiated with the tax authority, showing that accepting $20,000 from the sale was better than waiting for uncertain future collection. They agreed, allowing the sale to proceed.

Subordination Agreements

Sometimes you don’t need to pay off the tax lien entirely—you just need to move it behind another lien temporarily.

What Is Subordination?

A subordination agreement allows another creditor (typically a new mortgage lender) to move ahead of the tax lien in priority. This is useful when you’re refinancing to get cash to pay the lien or when a buyer needs financing.

When to Request Subordination:

- Refinancing to pull out equity to pay the tax debt

- Buyer needs a mortgage, but lender won’t lend with a senior tax lien

- Restructuring debts to improve your ability to pay

Tax authorities may agree to subordination if it increases the likelihood of collection. For example, if subordinating allows you to refinance and use the proceeds to pay the tax debt, they’ll often agree.

Working with Property Solutions Companies

Navigating tax liens while trying to sell property can be overwhelming. Companies specializing in complex property situations provide helpful solutions by coordinating between tax authorities, title companies, and buyers.

How Property Solutions Companies Help:

🏠 Coordinate with multiple parties – Handle communications with tax collectors, title companies, and buyers

🏠 Navigate complex title issues – Address liens alongside other title problems

🏠 Provide expert service – Industry experts who understand both tax resolution and real estate transactions

🏠 Offer alternative solutions – When traditional sales won’t work, explore other options

🏠 Simplify the process – Take the burden off property owners facing overwhelming situations

This approach is particularly valuable for inherited properties with multiple issues or properties with several types of liens that need to be resolved simultaneously.

Common Mistakes to Avoid When Negotiating Tax Liens

Even with the best intentions, property owners often make mistakes that jeopardize their negotiation success. Avoiding these common pitfalls improves your chances significantly.

Mistake 1: Waiting Too Long to Act

The biggest mistake is ignoring tax liens and hoping they’ll go away. They won’t. Tax liens grow larger over time as interest and penalties compound, and tax authorities become less willing to negotiate as debts age.

Why Timing Matters:

- Collection statutes eventually expire, but tax authorities accelerate enforcement as expiration approaches

- The longer you wait, the more aggressive collection actions become

- Early intervention provides more options and better negotiating leverage

- Some settlement programs have time limits or deadlines

Action Step:

Address tax liens as soon as you become aware of them. Even if you can’t pay immediately, contacting the tax authority and exploring options prevents the situation from deteriorating.

Mistake 2: Providing Incomplete or Inaccurate Information

Tax authorities base their decisions on the information you provide. Incomplete applications get rejected, and inaccurate information can result in accusations of fraud.

Common Documentation Errors:

❌ Omitting bank accounts or assets

❌ Understating income

❌ Overstating expenses without documentation

❌ Failing to disclose all tax years with liabilities

❌ Submitting outdated financial information

Action Step:

Be thorough, honest, and accurate. If you’re unsure about something, seek professional guidance rather than guessing. Tax authorities can verify most financial information independently, so dishonesty always backfires.

Mistake 3: Making Unrealistic Offers

Offering to settle a $100,000 tax debt for $5,000 when you have $80,000 in home equity wastes everyone’s time and damages your credibility.

How to Make Realistic Offers:

- Calculate your RCP using the tax authority’s methodology

- Offer an amount close to your RCP (slightly lower is acceptable)

- Provide clear documentation supporting your calculations

- Explain any special circumstances that justify a lower amount

Action Step:

Research the tax authority’s acceptance criteria and historical acceptance rates. The IRS publishes annual Offer in Compromise acceptance data that shows average accepted offers by income and asset levels.

Mistake 4: Defaulting on Accepted Agreements

Getting a settlement approved is a major victory—but defaulting on the agreement reinstates the full original debt and eliminates future negotiation opportunities.

Common Default Triggers:

- Missing installment payments

- Failing to file future tax returns on time

- Incurring new tax debts

- Not reporting significant income increases (for some agreements)

Action Step:

Treat your settlement agreement as your highest financial priority. Set up automatic payments if possible, and mark all filing deadlines on your calendar. If you anticipate difficulty meeting the terms, contact the tax authority immediately to discuss modifications.

Mistake 5: Not Seeking Professional Help When Needed

While simple installment agreements can often be handled independently, complex situations benefit enormously from professional representation.

When to Hire a Professional:

- Tax debt exceeds $25,000

- Multiple tax years are involved

- You’re facing imminent foreclosure or levy

- Your financial situation is complex (business income, multiple properties, etc.)

- Previous settlement requests were denied

- You’re dealing with multiple liens or complicated title issues

Action Step:

Consult with at least one tax professional before submitting complex settlement requests. Many offer free initial consultations where they evaluate your situation and explain whether professional representation would be cost-effective.

Protecting Your Property During the Negotiation Process

While you’re negotiating your tax lien payoff, protecting your property from foreclosure or levy is critical. Several strategies can buy you time and prevent loss of your property.

Request a Collection Due Process Hearing

When the IRS files a Notice of Federal Tax Lien or issues a Final Notice of Intent to Levy, you have the right to request a Collection Due Process (CDP) hearing.

Benefits of CDP Hearings:

✅ Temporarily suspends collection actions

✅ Provides opportunity to propose alternative collection methods

✅ Independent review by IRS Appeals Office

✅ Right to appeal to Tax Court if you disagree with the decision

✅ Protects your property while the hearing is pending

How to Request:

File Form 12153 (Request for a Collection Due Process or Equivalent Hearing) within 30 days of receiving the lien notice or levy notice. The hearing request must be timely—late requests may receive an “equivalent hearing” without the same protections.

Apply for Currently Not Collectible Status

As discussed earlier, CNC status temporarily suspends collection activities when you can prove financial hardship. This protection extends to preventing foreclosure on your property.

Strategic Use of CNC:

CNC status works well as a bridge strategy while you:

- Improve your financial situation to qualify for an installment agreement

- Gather documentation for an Offer in Compromise

- Arrange to sell the property and pay the lien from proceeds

- Wait for the collection statute to expire (though this is risky)

The key is using CNC status as part of a broader strategy, not as a permanent solution.

Explore Bankruptcy Protection

While bankruptcy doesn’t eliminate tax liens that have already attached to property, it can provide temporary protection and reorganize your debts.

Chapter 13 Bankruptcy:

Allows you to create a 3-5 year repayment plan that includes tax debts. The automatic stay prevents foreclosure while you’re in bankruptcy and making plan payments.

Chapter 7 Bankruptcy:

May discharge certain older income tax debts (generally more than three years old, with specific requirements met). However, tax liens survive bankruptcy and remain attached to property.

Important Note:

Bankruptcy is a serious step with long-term consequences. Consult with both a bankruptcy attorney and a tax professional to understand how it would affect your specific situation. In many cases, negotiating directly with tax authorities produces better outcomes without the severe credit impact of bankruptcy.

Maintain Communication with Tax Authorities

Regular communication demonstrates good faith and keeps you informed about the status of your case.

Communication Best Practices:

📞 Document every conversation (date, time, person you spoke with, what was discussed)

📞 Follow up phone conversations with written confirmation

📞 Respond promptly to all correspondence

📞 Update the tax authority if your financial situation changes significantly

📞 Request extensions if you need more time to gather documentation

Tax authorities are more willing to work with taxpayers who are responsive and engaged in the process. Ignoring their communications signals that you’re not serious about resolving the debt.

Life After Settlement: Moving Forward with Clear Title

Successfully negotiating your tax lien payoff is a major accomplishment. Understanding what happens next ensures you maintain your progress and avoid future problems.

Obtaining Your Lien Release

Once you’ve satisfied the terms of your settlement, the tax authority should release the lien. However, releases don’t always happen automatically or quickly.

Steps to Ensure Lien Release:

- Make final payment – Ensure the payment clears and is properly credited

- Request release documentation – Ask for Form 668-Z (IRS) or equivalent state/local release

- Verify release is filed – Check with the county recorder’s office where the lien was filed

- Obtain certified copies – Get official copies of the release for your records

- Update credit reports – Dispute any credit report entries that don’t reflect the release

Timeline Expectations:

- IRS typically releases liens within 30 days of full payment

- State and local authorities vary (10-60 days is common)

- Recording the release at the county level may take additional time

If the release doesn’t appear within the expected timeframe, follow up persistently. Having the lien released is essential for selling your property or refinancing.

Rebuilding Your Credit

Tax liens filed before 2018 may still appear on credit reports (newer liens generally don’t appear, but the underlying tax debt might affect credit indirectly).

Credit Rebuilding Steps:

💳 File all future tax returns on time

💳 Pay all taxes when due

💳 Make all installment payments as agreed

💳 Monitor credit reports for accuracy

💳 Dispute any errors or outdated information

💳 Establish positive credit history through responsible use of credit

The impact of tax issues on credit diminishes over time, especially when you demonstrate consistent responsible financial behavior.

Preventing Future Tax Problems

The best way to avoid future tax liens is preventing tax debts from accumulating.

Prevention Strategies:

🛡️ Adjust withholding – Ensure enough tax is withheld from paychecks

🛡️ Make estimated payments – If you’re self-employed or have investment income

🛡️ File on time even if you can’t pay – Failure to file penalties are much higher than failure to pay

🛡️ Request payment plans immediately – If you owe at filing, set up payments before the debt becomes delinquent

🛡️ Keep good records – Maintain documentation for deductions and income

🛡️ Consult tax professionals – Get help with complex tax situations before problems develop

Planning for Property Transactions

With your lien released and title clear, you can finally move forward with property transactions that were previously impossible.

Next Steps for Property Owners:

If you negotiated the lien to sell your property, you can now:

- Market the property with clear title

- Accept offers without lien complications

- Close sales smoothly through normal processes

If you negotiated the lien to keep your property, you can now:

- Refinance to get better terms or access equity

- Transfer ownership to family members if desired

- Use the property as collateral for other purposes

Working with experienced property professionals ensures your transaction proceeds smoothly and all title issues are properly resolved.

Frequently Asked Questions About Tax Lien Negotiation

Can I negotiate a tax lien myself, or do I need professional help?

You can absolutely negotiate tax liens yourself, especially for straightforward situations like simple installment agreements or first-time penalty abatement. The IRS and most state tax authorities provide detailed instructions and forms for taxpayers to use independently.

However, professional help becomes valuable for:

- Complex financial situations

- Large tax debts (over $25,000)

- Offers in Compromise

- Cases involving multiple tax years or types of taxes

- Situations where previous requests were denied

Tax professionals understand the nuances of negotiation and know how to present your case most effectively.

How long does the negotiation process take?

Timelines vary significantly based on the settlement option and the tax authority involved:

- Installment agreements: 30-60 days for approval

- Offer in Compromise: 6-12 months on average (sometimes longer)

- Penalty abatement: 30-90 days

- Currently Not Collectible: 30-60 days for initial determination

The process takes longer when:

- Your case is complex

- You submit incomplete documentation

- The tax authority requests additional information

- You’re working with state or local authorities with limited staff

Will negotiating a tax lien hurt my credit score?

The negotiation itself doesn’t hurt your credit. However, the underlying tax debt and lien (if filed before 2018) may already be affecting your credit.

Successfully resolving the tax lien through settlement actually helps your credit long-term by:

- Removing the lien from public records

- Preventing foreclosure or levy

- Demonstrating responsible debt resolution

- Allowing you to move forward with positive financial behaviors

What happens if I can’t afford the settlement amount?

If you can’t afford the settlement amount proposed or accepted, you have several options:

- Request Currently Not Collectible status – Temporarily suspend collection until your finances improve

- Propose a longer payment plan – Extend the term to reduce monthly payments

- Wait and reapply – If your financial situation worsens, you may qualify for a better settlement later

- Explore partial payment installment agreements – Pay what you can afford until the collection statute expires

The worst option is agreeing to terms you can’t meet and then defaulting. Be realistic about what you can afford.

Can I negotiate property tax liens the same way as income tax liens?

Property tax liens work differently from income tax liens. Local governments have different procedures and often less flexibility because property taxes fund essential services.

However, many counties and municipalities offer:

- Payment plans for delinquent property taxes

- Senior citizen or hardship exemptions

- Tax sale redemption periods

- Installment arrangements

Contact your local tax collector to ask about available programs. Some jurisdictions are surprisingly flexible, especially when property owners demonstrate good faith efforts to pay.

Conclusion: Taking Control of Your Tax Lien Situation

Understanding how to negotiate tax lien payoff: strategies & settlement options transforms what seems like an insurmountable problem into a manageable challenge with real solutions. Tax liens don’t have to mean losing your property or facing financial ruin. With the right approach, thorough documentation, and persistence, most property owners can negotiate settlements that work for their circumstances.

The key principles to remember:

Act quickly – The sooner you address tax liens, the more options you have and the better your negotiating position.

Be thorough – Complete, accurate documentation is the foundation of successful negotiations. Take the time to gather everything the tax authority needs to evaluate your request fairly.

Be realistic – Understanding your reasonable collection potential and making offers that align with tax authority guidelines dramatically improves your approval chances.

Get help when needed – Complex situations benefit from professional expertise. The cost of representation often pales in comparison to the savings achieved through successful negotiation.

Follow through – Once you’ve negotiated a settlement, meeting the terms precisely is essential. Defaulting reinstates the full debt and eliminates future negotiation opportunities.

Your Next Steps

If you’re facing a tax lien on your property, take action today:

- Gather your tax records – Obtain complete information about what you owe and why

- Assess your finances – Complete a thorough inventory of income, expenses, assets, and liabilities

- Research your options – Determine which settlement strategy best fits your situation

- Seek guidance – Consult with tax professionals or property solutions experts who can provide helpful guidance

- Submit your request – Don’t delay—begin the negotiation process before the situation worsens

Remember, tax authorities want to collect what they’re owed, but they’re also practical. They recognize that accepting reasonable settlements is often better than pursuing costly, uncertain collection actions. This creates opportunity for property owners who approach negotiations strategically and professionally.

Your property represents significant value—financial, sentimental, or both. Don’t let tax liens force you into losing it when negotiation options exist. With the strategies and settlement options outlined in this guide, you have the knowledge to move forward confidently toward resolution.

The path from tax lien to clear title may seem long, but thousands of property owners successfully navigate it every year. With determination, proper documentation, and the right approach, you can join them in resolving your tax issues and reclaiming control of your property and your financial future.

For personalized assistance navigating tax liens and other complex property issues, reach out to industry experts who provide friendly and caring, trustworthy service designed to help property owners find practical solutions to challenging situations.