Losing a parent ranks among life's most challenging experiences. When grief intersects with the practical necessity of selling their home, the emotional weight can feel overwhelming. Yet thousands of families navigate this journey every year, transforming what seems like an insurmountable task into a manageable process.

Understanding how to sell deceased parents house: step-by-step guide principles can transform confusion into clarity during an already difficult time. Whether dealing with probate court requirements, coordinating with siblings, or managing property issues like liens or back taxes, having a clear roadmap makes all the difference.

This comprehensive guide walks through every stage of selling an inherited property, from initial legal requirements through closing day. The process involves more moving parts than a typical home sale, but with expert service and helpful guidance, families successfully complete these transactions every day.

Key Takeaways

- Probate is usually required before selling a deceased parent's house, though some states offer simplified processes for smaller estates

- Multiple heirs complicate the process and require unanimous agreement or legal partition actions to proceed with a sale

- Property issues like liens, back taxes, or title problems must be resolved before closing, but professional solutions exist for every scenario

- Three main selling options exist: traditional listing, cash buyers, or auction—each with distinct timelines and financial outcomes

- Tax implications vary significantly based on inheritance laws, capital gains calculations, and how proceeds are distributed among heirs

Understanding the Legal Requirements Before You Sell

The legal framework surrounding estate property sales protects all parties involved but creates necessary hurdles that must be cleared before proceeding. These requirements aren't optional—they form the foundation of a legitimate property transfer.

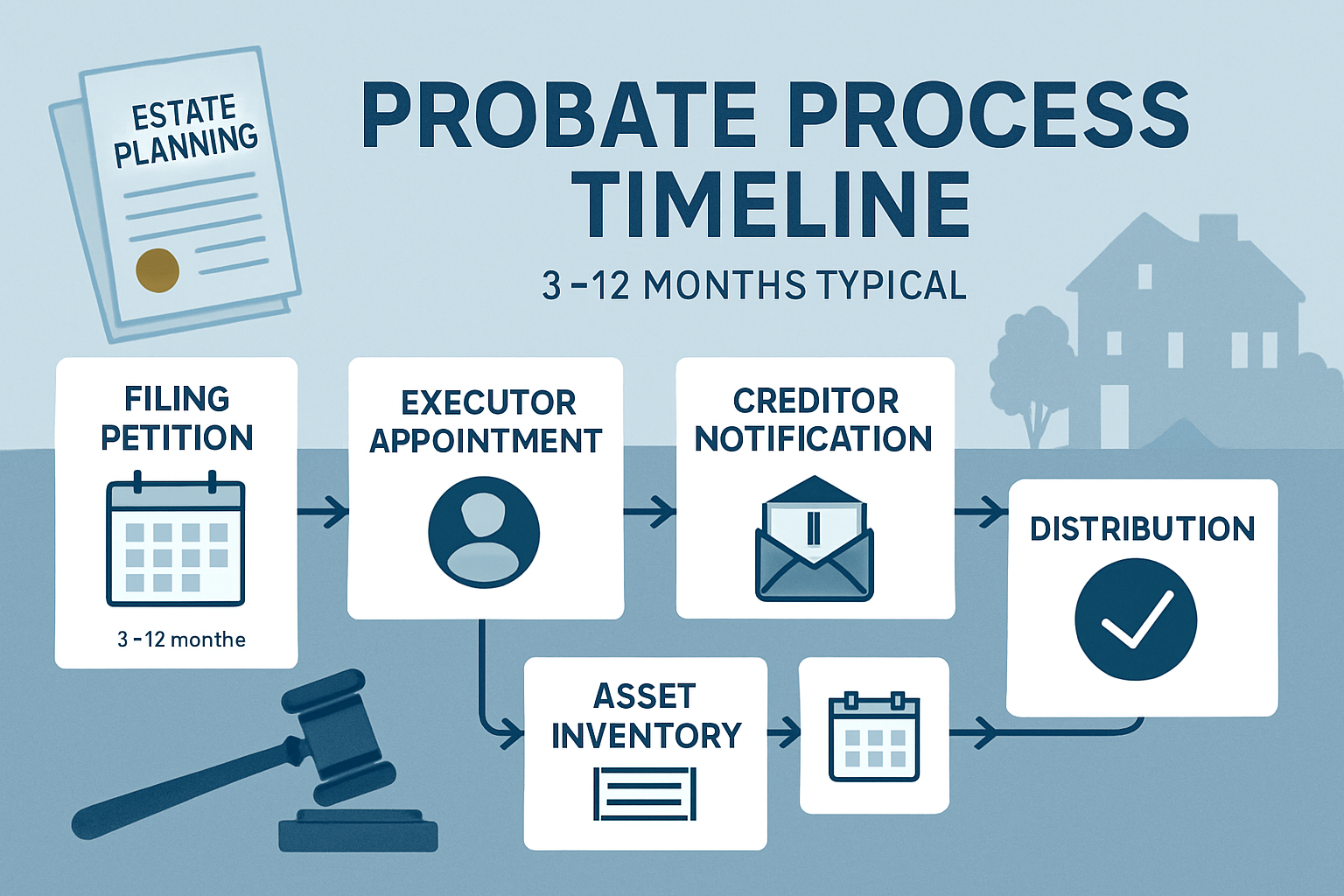

The Probate Process Explained

Probate serves as the legal mechanism for transferring property ownership from deceased individuals to their heirs. Think of it as the court's way of ensuring debts get paid and assets reach their rightful recipients.

The probate timeline typically spans six months to two years, depending on estate complexity and state requirements. During this period, the court validates the will (if one exists), appoints an executor or administrator, inventories assets, pays outstanding debts, and finally distributes remaining property to beneficiaries.

Key probate stages include:

- Filing the petition with probate court

- Notifying heirs and creditors

- Inventorying estate assets

- Paying debts and taxes

- Distributing remaining assets

- Closing the estate

Some states offer simplified probate for smaller estates, potentially reducing both time and costs. California, for example, provides a streamlined process for estates valued under $184,500 in 2025.

"The probate process exists to protect everyone involved—creditors, heirs, and buyers. While it adds time to the sale, it ensures clean title transfer and legal protection for all parties."

When You Can Skip Probate

Certain ownership structures allow property to bypass probate entirely, accelerating the sale timeline significantly. These exceptions represent planning opportunities for property owners and immediate relief for grieving families.

Common probate exceptions include:

- Joint tenancy with right of survivorship: Property automatically transfers to surviving owner(s)

- Transfer-on-death deeds: Available in approximately 30 states, these deeds transfer property directly to named beneficiaries

- Living trusts: Property held in revocable living trusts avoids probate completely

- Community property with right of survivorship: In community property states, surviving spouses receive automatic ownership

Verifying whether probate is necessary should be the first step. Consult the deed, will, or trust documents, and consider speaking with a probate attorney for definitive guidance. This single determination shapes your entire timeline and approach.

Executor Responsibilities and Authority

The executor (or administrator if no will exists) carries significant responsibility and authority throughout the sale process. This person acts as the estate's legal representative, making decisions and signing documents on behalf of the deceased.

Primary executor duties include:

- Securing the property: Maintaining insurance, utilities, and security until sale

- Managing finances: Paying mortgage, taxes, and maintenance costs from estate funds

- Obtaining court approval: Securing permission to sell (requirements vary by state)

- Coordinating with heirs: Communicating decisions and obtaining necessary agreements

- Handling the sale: Selecting selling method, negotiating terms, and completing closing

Executors must act in the estate's best interest, not their personal preferences. This fiduciary duty requires transparency, fairness, and often, difficult decisions that balance competing interests among heirs.

The court grants executors "Letters Testamentary" or "Letters of Administration"—official documents proving their authority to act. These letters become essential when listing property, negotiating with buyers, and signing closing documents.

Preparing the Property for Sale

Physical preparation directly impacts sale price and timeline. A well-presented property attracts more buyers and commands higher offers, while neglected homes languish on the market or require steep discounts.

Securing and Maintaining the Home

Empty homes become targets for vandalism, theft, and deterioration. Immediate security measures protect both the physical asset and its market value.

Essential security steps:

- Change all locks immediately (you don't know who has keys)

- Install motion-sensor lighting around entry points

- Maintain yard appearance to avoid "abandoned" signals

- Forward or stop mail delivery

- Set lights on timers to suggest occupancy

- Notify neighbors and local police of the vacant status

- Continue insurance coverage (vacant home policies may be required)

Utilities present a strategic decision. Maintaining electricity, water, and heat prevents damage from frozen pipes, mold growth, and other deterioration. However, these costs accumulate quickly. Balance preservation needs against carrying costs based on your expected sale timeline.

Regular property visits—weekly if possible—catch problems early. A small roof leak discovered immediately costs hundreds to repair; left undetected for months, it becomes a multi-thousand-dollar disaster that tanks your sale price.

Handling Personal Belongings and Estate Items

Clearing a lifetime of possessions ranks among the most emotionally challenging aspects of selling a parent's home. The process requires balancing sentimental value, practical considerations, and sale timeline pressures.

Strategic approach to estate contents:

- Distribute items per will instructions first

- Allow heirs to select meaningful items before general clearing

- Appraise potentially valuable items (antiques, jewelry, collections)

- Sell valuable items separately through estate sales or specialized dealers

- Donate usable items to charities (obtain receipts for estate tax deductions)

- Dispose of remaining items through junk removal services

Professional estate sale companies handle the entire process for 30-40% of sale proceeds. This option works well when valuable items exist but heirs lack time or energy to manage individual sales.

For properties selling "as-is" to cash buyers, some companies purchase homes with contents included, eliminating this entire burden. This approach sacrifices some value but dramatically reduces stress and timeline.

Making Necessary Repairs vs. Selling As-Is

The repair-versus-as-is decision hinges on property condition, local market dynamics, available capital, and timeline constraints. Neither approach is universally correct—context determines the optimal strategy.

Factors favoring repairs and updates:

- Strong seller's market with competitive bidding

- Property in otherwise good condition with isolated issues

- High-value neighborhood where condition expectations are elevated

- Sufficient estate funds to cover improvement costs

- Flexible timeline allowing for renovation work

Factors favoring as-is sales:

- Extensive deferred maintenance requiring major investment

- Limited estate funds for improvements

- Urgent timeline needs (medical bills, creditor pressure, sibling disputes)

- Properties with title issues or liens complicating traditional sales

- Heirs living far from the property

A hybrid approach often makes sense: address critical safety issues and obvious cosmetic problems while leaving major systems and structural work to buyers. Fresh paint, clean carpets, and functional appliances create positive impressions without massive investment.

Professional home inspections (cost: $300-500) identify issues before listing, allowing strategic decisions about which problems to address and which to disclose and price accordingly.

Navigating Multiple Heirs and Ownership Issues

Shared inheritance creates complexity even among harmonious families. When disagreements arise, the sale process can stall indefinitely without proper legal mechanisms and helpful solutions.

Reaching Agreement Among Siblings

Multiple heirs must unanimously agree to sell unless legal alternatives are pursued. This requirement transforms family dynamics into business negotiations, sometimes surfacing decades-old resentments and conflicts.

Strategies for building consensus:

- Hold structured family meetings with clear agendas and decision frameworks

- Share complete financial information about property value, carrying costs, and market conditions

- Consider neutral third-party facilitation when emotions run high

- Calculate exact financial outcomes for each heir under different scenarios

- Address emotional attachments separately from financial decisions

- Set firm deadlines for decision-making to prevent indefinite delays

One common conflict involves heirs who want to keep the property versus those preferring to sell. The "keep it" camp often underestimates carrying costs, maintenance demands, and liability exposure. Presenting concrete numbers—annual taxes, insurance, utilities, maintenance, and opportunity cost of tied-up equity—helps ground emotional positions in financial reality.

Buyout arrangements allow one heir to purchase others' shares, satisfying both camps. This requires property appraisal, financing approval, and formal legal documentation but preserves family relationships while achieving everyone's goals.

Partition Actions When Agreement Fails

When heirs cannot reach consensus, partition actions provide legal resolution. These lawsuits force property sale even when some owners object, though they should be considered a last resort due to costs and family relationship damage.

Two types of partition exist:

- Partition in kind: Physical division of property into separate parcels (rarely practical for houses)

- Partition by sale: Court-ordered sale with proceeds divided among owners

The partition process typically unfolds over 6-18 months and costs $10,000-$50,000 in legal fees. Courts generally order sale by auction, which often yields below-market prices—sometimes 10-30% less than traditional sales.

Despite these drawbacks, partition actions break deadlocks when one heir refuses reasonable offers or blocks legitimate sale attempts. The mere threat of partition sometimes motivates holdout heirs to negotiate in good faith.

For detailed information about this legal process, review our guide on partition action lawsuits.

Dealing with Out-of-State or Difficult Heirs

Geographic distance complicates communication, document signing, and decision-making. Difficult personalities amplify these challenges, sometimes requiring creative solutions and professional intervention.

Managing remote heirs effectively:

- Use video conferencing for family meetings

- Employ digital signature platforms (DocuSign, HelloSign) for documents

- Provide detailed photo and video documentation of property condition

- Share real-time market data and comparable sales

- Consider granting power of attorney to local heirs for specific transactions

- Hire local property managers for maintenance and showing coordination

Difficult heirs—those who are unresponsive, unreasonably demanding, or actively obstructive—require firmer approaches. Document all communication attempts, set reasonable deadlines with stated consequences, and consult attorneys about legal options when cooperation fails.

Professional mediators (cost: $200-400/hour) often resolve conflicts that seem intractable. Their neutral position and conflict-resolution expertise frequently break through emotional barriers that family members cannot overcome alone.

When dealing with jointly owned property complications, understanding all legal options prevents unnecessary delays and expense.

Resolving Title Issues, Liens, and Back Taxes

Property problems that seemed minor during your parents' lifetime become major obstacles at sale time. Buyers and their lenders demand clear title, forcing resolution of issues that may have lingered for years.

Common Title Problems in Inherited Properties

Title issues emerge frequently in estate properties, particularly when owners aged in place for decades without regular title review. These problems must be resolved before any legitimate sale can close.

Frequent title complications include:

- Missing heirs: Undiscovered or unlocated heirs from previous generations

- Unclear ownership chains: Gaps in recorded deed history

- Unreleased mortgages: Paid-off loans never formally released

- Judgment liens: Court judgments against deceased owners

- Mechanic's liens: Unpaid contractor or service provider claims

- Tax liens: Federal, state, or local tax debts

- Easement disputes: Unclear or contested property access rights

Title companies identify these issues during the title search process, typically 2-4 weeks after contract signing. Discovering problems at this stage creates crisis situations, potentially collapsing sales and forcing rushed resolution attempts.

Proactive title examination before listing—through a preliminary title report or attorney opinion—reveals problems early when time pressure doesn't compound complexity. This advance knowledge allows strategic planning and often reduces resolution costs.

For comprehensive information about title complications, explore our resource on clouded title in real estate.

Clearing Liens Before Closing

Liens represent legal claims against property, giving creditors rights to sale proceeds before owners receive anything. These must be satisfied or removed before title can transfer to buyers.

Lien resolution strategies:

- Pay from estate funds: Simplest approach when cash exists

- Negotiate settlements: Many creditors accept reduced payoffs for immediate payment

- Pay at closing: Liens are satisfied from sale proceeds (requires buyer/lender approval)

- Dispute invalid liens: Challenge liens through legal processes when claims lack merit

- Obtain lien releases: Secure formal documentation that liens are satisfied

Different lien types require different approaches. Tax liens often qualify for payment plans or offers in compromise. Judgment liens may be negotiable, especially if the judgment is old or the creditor has written off the debt. Mechanic's liens sometimes expire if not properly renewed.

The key is starting early. Lien resolution takes time—often 30-90 days—and rushing the process limits negotiation leverage and increases costs.

Professional help from real estate attorneys or companies specializing in selling houses with liens can navigate complex situations efficiently, often saving more in negotiated reductions than their fees cost.

Handling Property Tax Delinquencies

Back property taxes create particularly urgent problems because tax authorities hold superior liens—they get paid before anyone else, including mortgage lenders. Accumulated tax debt can equal or exceed property value in extreme cases.

Property tax resolution options:

- Full payment: Clears debt immediately and stops penalty/interest accrual

- Payment plans: Most counties offer installment agreements

- Tax sales redemption: If property has entered tax sale process, redemption periods allow recovery

- Sale proceeds payment: Taxes paid at closing from buyer's funds

- Negotiated reduction: Some jurisdictions reduce penalties/interest for lump-sum payment

Tax debt accumulates quickly due to penalties and interest, often reaching 15-25% annually. A $5,000 tax debt can balloon to $10,000 within 3-4 years. This acceleration makes prompt action critical.

Counties eventually foreclose on tax-delinquent properties through tax deed sales or tax lien certificate sales. These processes vary by state but ultimately result in ownership loss if taxes remain unpaid.

For properties with significant property tax issues, specialized buyers and solutions exist. Companies like Sure Path Property Solutions work with county tax offices to coordinate payoffs and facilitate sales even with substantial back taxes.

Choosing the Right Selling Method

The selling approach dramatically affects timeline, net proceeds, and stress levels. No single method suits every situation—careful evaluation of priorities and constraints guides the optimal choice.

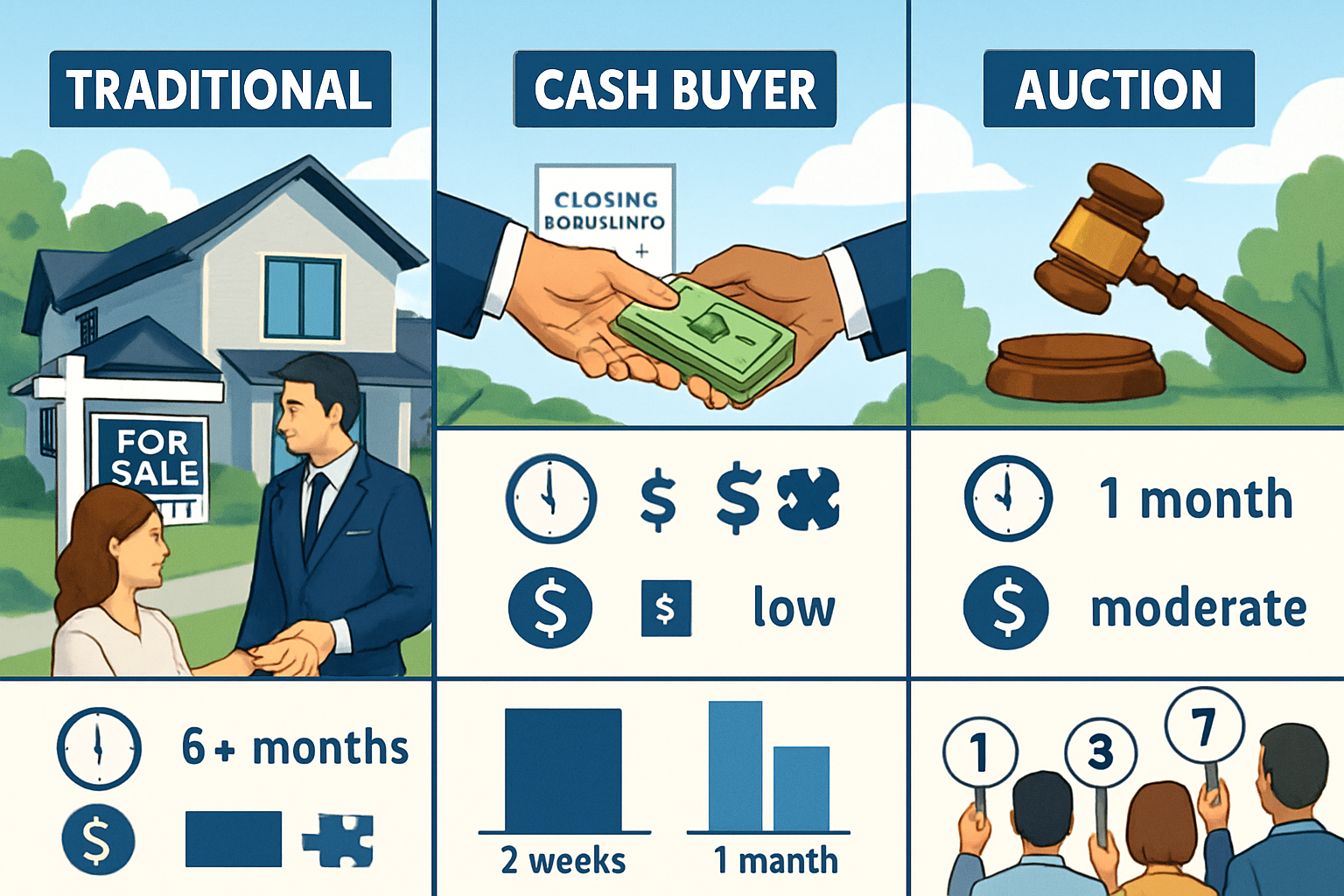

Traditional Real Estate Listing

Listing with a real estate agent represents the conventional approach, offering maximum market exposure and typically the highest sale prices. This method works best when time allows and property condition supports retail marketing.

Traditional listing advantages:

- ✅ Highest potential sale price (typically 10-20% above as-is offers)

- ✅ Maximum buyer pool through MLS exposure

- ✅ Professional marketing, photography, and showing coordination

- ✅ Agent expertise in negotiation and contract management

- ✅ Established transaction processes and legal protections

Traditional listing disadvantages:

- ❌ Longer timeline (average 60-90 days to closing)

- ❌ Commission costs (typically 5-6% of sale price)

- ❌ Preparation requirements (cleaning, repairs, staging)

- ❌ Ongoing carrying costs during marketing period

- ❌ Showing disruptions and property access requirements

- ❌ Potential for deals to fall through during inspection/financing

Agent selection matters enormously. Seek agents with specific estate sale experience who understand probate requirements, heir coordination, and property issue navigation. Interview 3-4 candidates, checking references and recent comparable sales.

Commission rates are negotiable, particularly for higher-value properties or those requiring minimal agent effort. Don't hesitate to discuss reduced rates—many agents prefer some commission to none.

Selling to Cash Buyers or Investors

Cash buyers—investors and companies purchasing properties directly—offer speed and certainty in exchange for below-market prices. This approach shines when timeline, property condition, or situation complexity makes traditional sales impractical.

Cash sale advantages:

- ✅ Rapid closing (often 7-14 days)

- ✅ No repairs or cleaning required

- ✅ No showings or marketing period

- ✅ Certainty (no financing contingencies)

- ✅ Solutions for properties with liens, title issues, or code violations

- ✅ Often purchase with contents included

Cash sale disadvantages:

- ❌ Lower sale price (typically 60-80% of retail value)

- ❌ Reduced proceeds to heirs

- ❌ Variable buyer reputation and reliability

Cash buyers serve specific situations exceptionally well: properties needing major repairs, urgent timeline needs, complicated title or lien situations, or when heirs simply want the process finished quickly with minimal involvement.

Vetting cash buyers carefully prevents scams and ensures professional transactions. Verify business registration, check references, review sample contracts, and consult attorneys before signing. Legitimate buyers provide proof of funds, use licensed title companies, and maintain transparent communication throughout.

Sure Path Property Solutions specializes in complicated estate properties, offering helpful solutions for situations involving multiple heirs, liens, back taxes, and title issues. Their expert service navigates complex scenarios that traditional buyers cannot accommodate.

Auction Sales and Other Alternatives

Auctions create competitive bidding environments that sometimes yield surprising prices, though they carry risks of below-market results. Other alternatives—seller financing, lease-options, or donations—suit niche situations.

Auction considerations:

Auctions work well for unique properties, highly desirable locations, or situations requiring absolute sale certainty by a specific date. Reserve prices protect against unreasonably low bids, though they reduce auction appeal.

Costs include auctioneer fees (5-10%), marketing expenses, and preparation requirements. Total auction costs often match or exceed traditional commission rates while introducing price uncertainty.

Alternative selling methods:

- Seller financing: Owner carries the note, receiving monthly payments rather than lump sum

- Lease-option: Tenant-buyer leases with purchase option, building toward eventual sale

- Donation: Charitable donation for tax deduction (requires appraisal and specific property types)

- Land contract: Similar to seller financing but with different legal structure

These alternatives suit specific circumstances but require careful legal structuring and often extend timelines significantly.

For most estate sales, the choice narrows to traditional listing versus cash sale. Evaluate your priorities—maximum price versus speed and certainty—then select the approach aligning with your specific situation and goals.

Step-by-Step Process: How to Sell Deceased Parents House

With legal requirements understood and selling method selected, the actual sale process follows a logical sequence. Each step builds on previous ones, creating momentum toward successful closing.

Step 1: Obtain Legal Authority to Sell

No sale can proceed without proper legal authority. This foundation step determines everything that follows.

Required documentation:

- Letters Testamentary or Letters of Administration from probate court

- Death certificate (certified copies)

- Will or trust documents

- Property deed

- Court order authorizing sale (if required in your state)

Some states require specific court approval before estate property sales; others grant executors broad authority to sell without additional permission. Verify requirements with a probate attorney to avoid costly mistakes.

Processing time for legal authority varies: 2-8 weeks in streamlined probate states, 3-6 months in more formal jurisdictions. This timeline cannot be rushed, making early filing critical.

Step 2: Get Professional Property Valuation

Accurate valuation serves multiple purposes: setting realistic asking prices, distributing proceeds fairly among heirs, calculating taxes, and establishing estate value for probate.

Valuation options:

- Formal appraisal: Licensed appraiser provides detailed report ($400-600)

- Broker price opinion (BPO): Real estate agent estimates value ($100-200 or free when listing)

- Comparative market analysis (CMA): Agent-prepared comparison to recent sales (typically free)

- Automated valuation model (AVM): Computer-generated estimate (free but least accurate)

Formal appraisals provide the most defensible values for tax purposes and heir disputes. They're particularly important for high-value properties or when significant disagreement exists about worth.

Obtain valuations early in the process. Market conditions change, and outdated appraisals lose credibility with buyers, lenders, and courts.

Step 3: Address Property Issues and Prepare for Sale

With authority secured and value established, property preparation begins. The extent of preparation depends on your chosen selling method.

Traditional listing preparation:

- Complete necessary repairs identified in pre-listing inspection

- Deep clean entire property

- Remove or store personal belongings

- Consider professional staging for higher-value homes

- Enhance curb appeal (landscaping, exterior paint, entry improvements)

- Ensure all systems function properly

- Address safety hazards and code violations

As-is sale preparation:

- Secure property and maintain basic safety

- Clear personal belongings (if required by buyer)

- Document property condition through photos

- Gather available property records and disclosures

- Ensure legal access for buyer inspections

Even as-is sales benefit from basic cleaning and security measures. First impressions matter, and minimal effort often yields disproportionate returns.

Step 4: List Property or Accept Offer

Marketing begins once preparation completes. Traditional listings involve photography, MLS entry, signage, online promotion, and showing coordination. Cash sales typically require only basic property information and access for buyer inspection.

Traditional listing timeline:

- Days 1-3: Professional photography and marketing material creation

- Day 4: MLS listing activation and online syndication

- Days 5-30: Showings and open houses

- Days 15-45: Offer receipt and negotiation

- Day 30-60: Contract execution

Cash sale timeline:

- Day 1: Contact buyer and provide property information

- Days 2-5: Buyer inspection and offer preparation

- Days 6-7: Offer review and negotiation

- Day 7-14: Contract execution and closing

Offer evaluation considers more than just price. Terms, contingencies, closing timeline, and buyer qualifications all impact deal quality. A slightly lower all-cash offer with quick closing often beats a higher-priced offer contingent on financing and inspection repairs.

Step 5: Navigate Inspection and Negotiation

Buyer inspections reveal property conditions, often triggering renegotiation requests. How these negotiations proceed depends heavily on initial contract terms and market conditions.

Common inspection issues:

- Roof condition and remaining life

- HVAC system age and functionality

- Plumbing problems (leaks, old pipes, water heater)

- Electrical issues (outdated panels, insufficient capacity)

- Foundation concerns

- Pest infestations or damage

- Deferred maintenance accumulation

Buyers typically request repairs, credits, or price reductions after inspection. Sellers can accept, reject, or counter these requests. In strong seller's markets, buyers often accept properties as-is; in buyer's markets, sellers make more concessions.

Estate sales sometimes benefit from pre-negotiated "as-is" contracts where buyers accept all conditions in exchange for reduced prices. This approach eliminates post-inspection surprises and renegotiation stress.

Step 6: Clear Title and Prepare for Closing

Title work proceeds simultaneously with inspection processes. The title company searches public records, identifies issues, and works toward clear title delivery at closing.

Title clearing activities:

- Resolving identified liens through payment or negotiation

- Obtaining releases for satisfied debts

- Correcting deed errors or gaps in ownership chain

- Securing required probate court approvals

- Obtaining heir signatures on required documents

- Clearing tax obligations

This phase often reveals unexpected complications requiring attorney involvement. Budget extra time—2-4 weeks beyond standard closing timelines—when title issues exist.

For properties with complicated situations, companies specializing in inherited property sales provide helpful guidance through these challenges.

Step 7: Complete Closing and Distribute Proceeds

Closing day finalizes the sale, transferring ownership to buyers and proceeds to the estate. This milestone brings relief and closure to what's often been a lengthy, emotional process.

Closing day activities:

- Final walkthrough (buyer confirms property condition)

- Document signing (deed, settlement statement, tax forms)

- Fund transfer (buyer's payment to escrow)

- Lien payoffs (from escrow funds)

- Commission and fee payments

- Net proceeds distribution to estate

Executors receive estate proceeds, not individual heirs. These funds enter the estate account, where they're used to pay remaining debts and expenses before final distribution to beneficiaries according to will terms or state law.

Post-closing responsibilities:

- Obtain and distribute closing documents to all heirs

- Update estate accounting records

- File required tax forms

- Distribute proceeds per will instructions or court order

- Obtain final receipts and releases from heirs

- Petition court for estate closure (when all assets are distributed)

The entire process—from death to final proceeds distribution—typically spans 8-18 months, though simple estates with cooperative heirs sometimes complete in 4-6 months.

Tax Implications and Financial Considerations

Understanding tax consequences prevents costly surprises and enables strategic planning that maximizes net proceeds to heirs.

Capital Gains Tax on Inherited Property

Inherited property receives favorable tax treatment through "step-up in basis"—a significant benefit that often eliminates or minimizes capital gains taxes.

How step-up in basis works:

When someone inherits property, the tax basis (original purchase price for tax purposes) "steps up" to fair market value on the date of death. This reset eliminates taxable gains that accumulated during the deceased owner's lifetime.

Example:

- Parents purchased home in 1985 for $100,000

- Home worth $500,000 at death in 2024

- Heirs sell in 2025 for $510,000

- Taxable gain: $10,000 ($510,000 – $500,000 stepped-up basis)

- Without step-up, gain would be $410,000 ($510,000 – $100,000)

This step-up saves heirs approximately $80,000-$100,000 in federal capital gains taxes in this example (assuming 20% long-term capital gains rate plus 3.8% net investment income tax).

Capital gains calculation factors:

- Date-of-death valuation (establishes new basis)

- Sale price minus selling costs

- Time between inheritance and sale (usually irrelevant due to step-up)

- Heir's income level (affects tax rate)

Primary residence exclusions ($250,000 single, $500,000 married) generally don't apply to inherited properties unless the heir lived there as their primary residence for 2 of the previous 5 years.

Estate Taxes and Inheritance Taxes

Federal estate taxes apply only to estates exceeding $13.61 million per person in 2025 (effectively $27.22 million for married couples). Most estates fall well below these thresholds and owe no federal estate tax.

However, state-level taxes create obligations in some jurisdictions:

States with estate taxes (2025):

- Connecticut, Hawaii, Illinois, Maine, Maryland, Massachusetts, Minnesota, New York, Oregon, Rhode Island, Vermont, Washington, District of Columbia

States with inheritance taxes:

- Iowa, Kentucky, Maryland, Nebraska, New Jersey, Pennsylvania

These state taxes kick in at much lower thresholds—sometimes as low as $1 million—and rates vary from 3-16%. Maryland uniquely imposes both estate and inheritance taxes.

Inheritance taxes are paid by heirs based on their relationship to the deceased. Spouses typically pay nothing; children pay reduced rates; non-relatives pay the highest rates.

Deductible Expenses and Reducing Tax Burden

Numerous expenses reduce taxable estate value or offset capital gains, maximizing net proceeds to heirs.

Deductible estate expenses:

- Funeral and burial costs

- Estate administration fees

- Attorney and accountant fees

- Appraisal costs

- Property maintenance during estate administration

- Property taxes and insurance

- Mortgage interest

- Selling costs (commissions, title fees, transfer taxes)

These deductions reduce the estate's taxable value for estate tax purposes. For capital gains, selling expenses reduce net proceeds and therefore taxable gain.

Strategic tax planning opportunities:

- Timing the sale: Selling quickly after death minimizes appreciation beyond stepped-up basis

- Allocating expenses: Properly categorizing costs maximizes deductions

- Distributing property versus proceeds: Sometimes distributing property to heirs before sale shifts tax obligations

- Installment sales: Spreading proceeds over multiple years can reduce tax rates

- 1031 exchanges: Generally unavailable for inherited property but possible in specific circumstances

Consult tax professionals before finalizing sale strategies. The interplay between estate taxes, inheritance taxes, capital gains taxes, and income taxes creates complexity that generic advice cannot address.

Common Challenges and How to Overcome Them

Even well-planned estate sales encounter obstacles. Anticipating common challenges and having response strategies ready prevents minor issues from becoming major crises.

Dealing with Underwater Properties or Reverse Mortgages

Properties worth less than outstanding mortgage balances create painful situations requiring specialized solutions.

Underwater property options:

- Short sale: Lender agrees to accept less than full payoff

- Deed in lieu of foreclosure: Voluntarily transfer property to lender

- Estate funds supplement: Use other estate assets to cover shortfall

- Foreclosure: Allow lender to foreclose (damages estate credit but eliminates personal liability)

Short sales require lender approval and typically take 3-6 months. They're particularly common in areas that experienced property value declines or when owners took cash-out refinances near peak values.

Reverse mortgage complications:

Reverse mortgages become due immediately upon the borrower's death. Heirs have several options:

- Pay off loan and keep property

- Sell property and pay loan from proceeds

- Deed property to lender if underwater

- Refinance into traditional mortgage (if qualifying)

Heirs typically have 30 days to decide and 6 months to complete payoff or sale, with possible extensions. Reverse mortgage balances often equal or exceed property values, leaving little or no equity for heirs.

The key is communicating with lenders immediately after death. Early contact establishes timelines, clarifies options, and sometimes yields flexibility that late contact cannot secure.

Managing Emotional Attachments and Family Conflicts

The family home carries decades of memories, making purely financial decisions emotionally difficult. These attachments sometimes override practical considerations, creating conflict and delay.

Strategies for managing emotions:

- Acknowledge feelings explicitly: Create space for grief separate from business decisions

- Document memories before sale: Photos, videos, or written stories preserve what matters

- Remove sentimental items early: Separate keepsakes from the property sale

- Focus on parent's wishes: What would they want for their children?

- Calculate true costs of keeping property: Make decisions based on complete information

- Set firm deadlines: Prevent indefinite emotional processing from stalling necessary actions

Family conflicts often stem from perceived unfairness, poor communication, or historical resentments surfacing during stress. Professional mediators or family therapists sometimes facilitate productive conversations that family members cannot achieve alone.

Remember: selling the house doesn't erase memories. The property is just wood, brick, and drywall—the memories live in hearts and minds regardless of ownership.

Handling Properties in Disrepair or Hoarding Situations

Severe property neglect or hoarding creates both practical and emotional challenges. These situations require specialized approaches and often professional help.

Addressing severely neglected properties:

- Obtain professional assessments: Structural engineers, contractors, and inspectors identify true condition

- Calculate repair costs accurately: Detailed estimates prevent underestimating required investment

- Consider as-is sales: Often more economical than renovation for severely damaged properties

- Explore demolition: Sometimes land value exceeds improved property value

- Investigate code violations: Unpermitted work or violations complicate sales

Hoarding situation protocols:

Hoarding reflects mental health conditions, not character flaws. Approach with compassion while maintaining necessary boundaries.

- Hire specialized cleaning services: Hoarding cleanup requires expertise and safety equipment

- Document valuable items: Don't assume everything is worthless

- Address safety hazards first: Mold, pest infestations, and structural issues require immediate attention

- Allow family members to participate: Some want involvement; others prefer distance

- Budget appropriately: Hoarding cleanup costs $2,000-$10,000+ depending on severity

Properties in extreme disrepair often sell best to investors or companies specializing in distressed properties. Traditional buyers cannot obtain financing for homes failing minimum property standards, limiting your buyer pool to cash purchasers.

Working with Professionals Who Can Help

Estate property sales involve specialized knowledge across multiple disciplines. Building the right professional team dramatically improves outcomes while reducing stress.

When to Hire a Probate Attorney

Probate attorneys specialize in estate administration, providing expertise that general practice attorneys and even real estate attorneys may lack.

Situations requiring probate attorney:

- Complex estates with multiple properties or significant assets

- Will contests or heir disputes

- Unclear title or ownership issues

- Estates with significant debts exceeding assets

- Business interests or unusual assets

- Minor children as heirs

- Blended families with potential conflicts

- Out-of-state property requiring ancillary probate

Probate attorney services:

- Filing probate petitions and required court documents

- Advising executors on legal duties and obligations

- Resolving creditor claims

- Interpreting will provisions

- Representing estate in disputes

- Obtaining court approvals for property sales

- Ensuring proper asset distribution

- Closing estate and obtaining final discharge

Costs vary widely: $3,000-$7,000 for straightforward estates, $10,000-$30,000+ for complex situations. Some attorneys charge hourly ($250-500/hour); others use flat fees for defined services.

This investment often saves far more than it costs through efficient problem resolution, avoided mistakes, and strategic tax planning.

Selecting the Right Real Estate Agent

Not all agents handle estate sales effectively. Seek specialists with specific experience in probate and inherited property transactions.

Essential agent qualifications:

- Probate sale experience (ask for recent examples)

- Knowledge of local probate court requirements

- Patience with extended timelines and multiple decision-makers

- Strong communication skills for coordinating with heirs

- Network of estate sale professionals, attorneys, and contractors

- Marketing expertise for properties in various conditions

Interview multiple agents, asking specific questions about their estate sale experience, typical timeline, marketing approach, and commission structure. Check references from recent estate clients.

Certified Probate Real Estate Specialists (CPRES) or similar credentials indicate advanced training, though practical experience often matters more than certifications.

How Sure Path Property Solutions Can Help

Complex estate situations—multiple heirs, property issues, liens, back taxes, or urgent timelines—often exceed traditional real estate solutions. Specialized companies fill this gap with helpful solutions tailored to challenging circumstances.

Sure Path Property Solutions focuses specifically on complicated property situations that traditional buyers and agents cannot accommodate. Their expert service addresses:

- Multiple heir coordination: Managing communication and agreement among dispersed family members

- Lien and title issue resolution: Working directly with creditors and counties to clear obstacles

- Back tax situations: Coordinating with tax authorities to resolve delinquencies

- Properties in disrepair: Purchasing as-is regardless of condition

- Urgent timeline needs: Closing in days when necessary

- Probate complexity: Understanding court requirements and executor obligations

Their friendly and caring approach recognizes that estate sales involve grief and stress beyond typical transactions. This trustworthy service provides helpful guidance through processes that feel overwhelming to families handling them for the first time.

The industry experts at Sure Path Property Solutions have navigated thousands of complicated situations, bringing solutions to scenarios that seem impossible to families facing them alone.

For situations involving traditional sales challenges, their blog offers extensive resources on topics from liens to title issues to inheritance complications.

Frequently Asked Questions

How long does it take to sell a deceased parent's house?

Timeline varies significantly based on probate requirements, property condition, and selling method. Expect 8-18 months for traditional probate sales, 4-6 months for simplified probate, or as little as 2-4 weeks for as-is cash sales to investors. Court approval processes, heir coordination, and title issues extend timelines beyond typical home sales.

Can I sell my parents' house before probate is complete?

Generally no—legal authority to sell requires probate court approval and executor appointment. Some exceptions exist: properties held in living trusts, joint tenancy with right of survivorship, or transfer-on-death deeds can sell without probate. Attempting to sell without proper authority creates legal liability and title defects that prevent legitimate closing.

What if siblings disagree about selling the inherited house?

Unanimous agreement among heirs is typically required unless one heir has been granted sole authority through will provisions or court order. When agreement fails, partition actions force sale through court order, though this process costs $10,000-$50,000 and takes 6-18 months. Mediation, buyout arrangements, or detailed financial analysis often resolve disagreements more efficiently than litigation.

Do I have to pay capital gains tax when selling inherited property?

Usually minimal or no capital gains tax due to "step-up in basis." The property's tax basis resets to fair market value on the date of death, eliminating accumulated gains. You only pay tax on appreciation between inheritance and sale. If selling quickly after death, taxable gain is typically small or zero. Consult tax professionals for specific situations.

Can I sell an inherited house with a mortgage?

Yes, but the mortgage must be paid at closing from sale proceeds. If proceeds don't cover the mortgage (underwater property), short sales or deed-in-lieu arrangements may be necessary. Reverse mortgages become due immediately upon death, requiring payoff or sale within 6-12 months. Contact lenders immediately after death to understand obligations and options.

What happens if the inherited property has liens or back taxes?

Liens must be satisfied before clear title can transfer to buyers. Options include paying from estate funds, negotiating settlements, or paying from sale proceeds at closing. Properties with liens can still sell—specialized buyers and solutions exist for complicated situations. Tax liens receive priority payment, but most counties work with estates to coordinate payoff through sale proceeds.

Should I repair the house before selling or sell as-is?

Depends on property condition, available funds, timeline urgency, and local market. Properties in good condition with isolated issues often benefit from strategic repairs in strong markets. Extensively neglected properties, urgent timeline situations, or limited estate funds favor as-is sales to investors. Calculate expected return on repair investment before committing funds.

How are sale proceeds divided among multiple heirs?

According to will provisions or state intestacy laws if no will exists. Proceeds go to the estate first, where debts and expenses are paid, then remaining funds distribute to heirs per legal requirements. Executors cannot distribute proceeds until all estate obligations are satisfied and court approval obtained. Unequal distributions require specific will language; otherwise, heirs typically receive equal shares.

Conclusion

Selling a deceased parent's house represents one of life's most challenging transitions—combining grief, family dynamics, legal complexity, and financial decisions into a process that feels overwhelming. Yet thousands of families successfully navigate this journey every year, transforming what seems impossible into accomplished reality.

The key lies in understanding the process, building the right professional team, and taking systematic action rather than becoming paralyzed by the magnitude of the task.

Essential steps for success:

- ✅ Secure legal authority through probate or trust administration

- ✅ Assess property condition and value accurately

- ✅ Resolve title issues, liens, and tax obligations early

- ✅ Build consensus among heirs or pursue legal alternatives

- ✅ Select selling method matching your priorities and constraints

- ✅ Work with experienced professionals who understand estate sales

- ✅ Understand tax implications and plan strategically

- ✅ Maintain clear communication with all stakeholders throughout

Remember that this process has a definite end. The house will sell, proceeds will distribute, and the estate will close. The overwhelming complexity you feel today becomes a completed chapter tomorrow.

For situations involving complications—multiple heirs, property issues, liens, back taxes, or urgent timelines—specialized help exists. Sure Path Property Solutions brings expert service and helpful solutions to scenarios that traditional approaches cannot accommodate. Their friendly and caring team understands that estate sales involve more than transactions; they involve families navigating loss while managing practical necessities.

Whether pursuing traditional listing, as-is sale, or alternative approaches, the fundamental principle remains constant: take informed action, seek professional guidance when needed, and maintain focus on honoring your parents' legacy while protecting all heirs' interests.

The journey may be challenging, but it's entirely navigable with the right knowledge, support, and resources. Your parents built something of value—ensuring that value transfers properly to the next generation represents a final act of love and responsibility.

Ready to move forward? Contact Sure Path Property Solutions for a confidential consultation about your specific situation. Their industry experts provide trustworthy service and helpful guidance tailored to your unique circumstances, transforming complicated estate sales into clear, manageable processes.

Sure Path is a family-owned, curative-title cash buyer. We handle the paperwork and pay what’s owed at closing — no fees, no repairs, no pressure.