How to Sell House with Attachment Lien: Urgent Solutions

Discovering an attachment lien on your property can feel like hitting a brick wall when you’re trying to sell. The phone call from your title company delivering the bad news, the sinking feeling in your stomach, the immediate questions flooding your mind—it’s overwhelming. But here’s the truth: an attachment lien doesn’t have to derail your home sale. Understanding how to sell house with attachment lien: urgent solutions can transform this seemingly impossible situation into a manageable challenge with clear pathways forward.

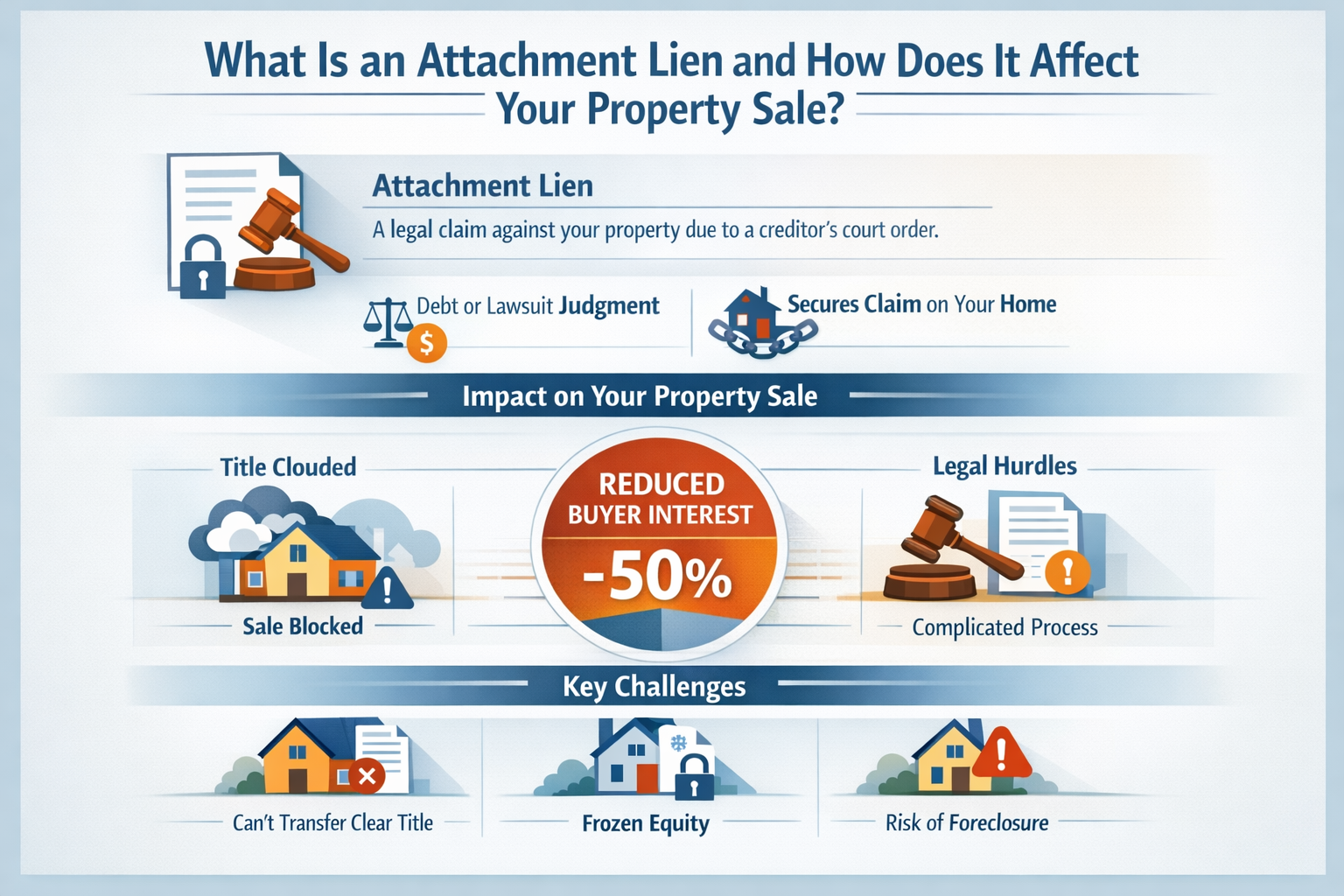

An attachment lien represents a creditor’s legal claim against your property, typically arising from unpaid debts or pending lawsuits. While this creates complications, thousands of homeowners successfully navigate these waters every year. The key lies in understanding your options, acting decisively, and working with industry experts who specialize in complicated real estate situations.

Key Takeaways

- Attachment liens are court-ordered claims that secure a creditor’s interest in your property but don’t automatically prevent a sale

- Three primary solutions exist: paying off the lien, negotiating a settlement, or working with specialized cash buyers who handle lien complications

- Time sensitivity matters—addressing attachment liens quickly prevents additional legal complications and preserves more selling options

- Professional guidance dramatically improves outcomes—working with experts who understand lien resolution can save thousands of dollars and months of stress

- You have more control than you think—even with an attachment lien, property owners retain significant leverage in determining their property’s future

What Is an Attachment Lien and How Does It Affect Your Property Sale?

An attachment lien is a legal mechanism that allows creditors to secure their claim against your real estate before obtaining a final judgment. Think of it as a creditor’s insurance policy—they’re protecting their ability to collect what they’re owed by placing a hold on your most valuable asset.

The Legal Foundation of Attachment Liens

Courts grant attachment liens when creditors demonstrate a legitimate claim and convince a judge that they need security for potential debt collection. This typically happens in situations involving:

- Unpaid business debts where the creditor fears you might sell assets before judgment

- Contract disputes with significant money at stake

- Personal injury claims where damages are being determined

- Divorce proceedings where property division is contested

- Unpaid professional services from contractors, attorneys, or medical providers

The attachment lien gets recorded with your county recorder’s office, creating a public record that appears during title searches. This public nature is what creates complications when selling.

How Attachment Liens Differ From Other Liens

Unlike mortgage liens (which you agreed to) or tax liens (which government entities impose), attachment liens are court-ordered security interests arising from civil litigation. They share characteristics with judgment liens, but attachment liens can be placed before a final judgment is rendered.

| Lien Type | When Created | Priority Level | Removal Process |

|---|---|---|---|

| Attachment Lien | During litigation | Varies by recording date | Pay, settle, or contest |

| Mortgage Lien | At purchase/refinance | First (usually) | Pay off loan |

| Tax Lien | After tax delinquency | Often supersedes others | Pay taxes or negotiate |

| Judgment Lien | After court judgment | By recording date | Satisfy judgment |

The Impact on Your Ability to Sell

An attachment lien creates what title companies call a “cloud on title”—an unresolved claim that prevents clear ownership transfer. Here’s what happens when you try to sell:

Traditional buyers can’t get financing. Mortgage lenders won’t approve loans on properties with unresolved liens. The buyer’s title insurance company refuses to issue a policy, which kills the deal.

The lien amount comes out of your proceeds. Even if you find a cash buyer, the lien must be addressed at closing. The title company will require the lien to be paid or released before transferring ownership.

Your equity is effectively frozen. The lien amount (plus interest and fees) reduces your available equity. If you owe $150,000 on your mortgage and have a $50,000 attachment lien on a house worth $250,000, your actual available equity drops from $100,000 to $50,000.

Time works against you. Most attachment liens accrue interest. The longer you wait, the more you’ll owe. Additionally, the underlying lawsuit may result in an even larger judgment.

“An attachment lien is like a financial anchor on your property. It doesn’t sink the ship immediately, but it prevents you from sailing forward until you address it. The good news? There are multiple ways to lift that anchor.” — Real Estate Title Expert

Understanding the Urgency: Why Immediate Action Matters

When facing an attachment lien, time is not your friend. The urgency isn’t just about convenience—it’s about protecting your financial interests and preserving your options.

Financial Costs That Accumulate Daily

Interest compounds relentlessly. Most attachment liens include provisions for interest, often at statutory rates ranging from 5% to 10% annually. On a $40,000 lien at 8% interest, you’re accumulating approximately $8.77 per day—over $3,200 per year.

Legal fees multiply. The creditor’s attorney fees often get added to the lien amount. As litigation progresses, these fees grow. What starts as a $30,000 debt can balloon to $45,000 or more when legal costs are factored in.

Property value can decline. While you’re frozen by the lien, market conditions might shift. A property worth $300,000 today might be worth $280,000 in six months if the market softens.

Legal Complications Intensify Over Time

Attachment liens can convert to judgment liens. If the underlying lawsuit concludes with a judgment against you, the attachment lien typically converts to a judgment lien, which may carry additional consequences including wage garnishment possibilities.

Additional liens may attach. Other creditors, seeing the attachment lien as a sign of financial distress, may accelerate their collection efforts and seek their own liens.

Foreclosure becomes possible. In some jurisdictions, judgment lien holders can eventually force a sale of your property through judicial foreclosure if the debt remains unpaid long enough.

Your Options Narrow With Delay

Negotiating leverage decreases. Early in the process, creditors may be more willing to negotiate settlements. As time passes and their legal investment grows, they become less flexible.

Cash reserves deplete. If you’re using savings to cover ongoing mortgage payments while the property can’t be sold, you’re burning through resources that could be used to settle the lien.

Emotional toll increases. The stress of an unresolved lien affects health, relationships, and decision-making ability. Quick resolution restores peace of mind and allows you to move forward with your life.

Comprehensive Solutions: How to Sell House with Attachment Lien

The pathway to selling your house despite an attachment lien depends on your specific circumstances, but three primary strategies offer viable solutions. Each has distinct advantages and considerations.

Solution 1: Pay Off the Attachment Lien at Closing

The most straightforward approach involves satisfying the lien from your sale proceeds. This works well when you have sufficient equity to cover both the lien and your other obligations.

How the process works:

- Obtain a payoff statement from the creditor or their attorney detailing the exact amount owed, including principal, interest, and fees

- List your property with a real estate agent or pursue a direct sale

- Negotiate the sale with potential buyers, disclosing the lien situation upfront

- Coordinate with the title company to ensure the lien payoff is included in the closing statement

- Close the transaction with the lien amount paid directly to the creditor from proceeds

Best for: Homeowners with adequate equity who want to pursue maximum sale price through traditional marketing.

Advantages:

- ✅ Cleanest resolution with no lingering debt

- ✅ Allows traditional marketing for best possible price

- ✅ No ongoing legal complications after closing

- ✅ Preserves credit rating better than alternatives

Challenges:

- ❌ Requires sufficient equity to cover all liens and closing costs

- ❌ Takes longer (typically 60-120 days for traditional sale)

- ❌ Buyers may be hesitant when liens are disclosed

- ❌ No immediate relief from financial pressure

Solution 2: Negotiate a Lien Settlement or Reduction

Creditors often accept less than the full amount owed, particularly when they recognize that forcing a sale might yield even less after legal fees and delays.

Negotiation strategies that work:

Lump sum settlement: Offer a reduced amount paid immediately. Creditors frequently accept 50-70% of the debt to avoid continued litigation costs and uncertainty. A $50,000 lien might settle for $30,000-$35,000 cash.

Structured settlement: Propose paying a portion at closing with the remainder in installments. This works when equity is tight but you’ll have post-sale resources.

Hardship demonstration: Document financial difficulties showing the creditor they’re unlikely to collect the full amount. Evidence of job loss, medical issues, or other debts strengthens your negotiating position.

Short sale approach: If you owe more than the property’s worth, work with the creditor to accept whatever the sale generates, similar to how mortgage lenders handle short sales.

Steps to successful negotiation:

- Gather documentation of your financial situation, property value, and other obligations

- Calculate maximum offer based on realistic sale proceeds minus senior liens

- Make initial contact with creditor’s attorney presenting your situation professionally

- Submit written offer with supporting documentation

- Negotiate terms including release language and timing

- Get agreement in writing before proceeding with sale

- Execute at closing with title company ensuring proper lien release

“Creditors are businesses making calculated decisions. When you present a compelling case showing they’ll receive more money faster through settlement than litigation, they often accept. It’s not about begging—it’s about presenting sound business logic.” — Debt Settlement Specialist

Best for: Homeowners with limited equity or those facing financial hardship who need to reduce the total debt burden.

Solution 3: Work With Specialized Cash Buyers

Companies like Sure Path Property Solutions specialize in purchasing properties with complicated title issues, including attachment liens. This approach offers speed and certainty when traditional sales aren’t viable.

How cash buyer solutions work:

Rapid assessment: Expert buyers evaluate your property and lien situation within 24-48 hours, providing clear guidance on viable solutions.

Direct lien negotiation: Experienced buyers often handle creditor negotiations directly, leveraging their industry expertise and relationships to secure favorable settlements.

Fast closing: Cash transactions can close in as little as 7-14 days, providing immediate relief from the burden of the attachment lien.

As-is purchase: No repairs, cleaning, or preparation required—the buyer accepts the property in current condition, saving time and money.

Comprehensive coordination: The buyer manages all aspects of title clearance, working with attorneys, title companies, and creditors to resolve the lien at closing.

When this solution makes sense:

- ⏰ Time pressure: Facing foreclosure, additional legal action, or personal circumstances requiring quick resolution

- 💰 Limited equity: The property value minus debts leaves little room for traditional sale costs

- 🔧 Property condition: The house needs significant repairs that you can’t afford to address

- 😰 Stress reduction: The emotional toll of managing the situation has become overwhelming

- 🏃 Need to relocate: Job transfer, family emergency, or other circumstances requiring immediate move

What to expect from the process:

- Initial consultation: Discuss your situation, property details, and lien specifics with a specialist

- Property evaluation: Quick assessment (often virtual) of property condition and value

- Lien analysis: Review of the attachment lien amount, creditor, and negotiation potential

- Cash offer presentation: Receive a written offer typically within 24-48 hours

- Lien resolution strategy: The buyer proposes how they’ll handle the lien (payoff or negotiation)

- Acceptance and closing: Choose your closing date and let the buyer coordinate all details

The team at Sure Path Property Solutions has helped hundreds of homeowners navigate complex lien situations, providing helpful solutions that restore peace of mind and financial stability.

Step-by-Step Process: Executing Your Chosen Solution

Regardless of which solution you select, following a structured process increases your chances of success and minimizes complications.

Phase 1: Information Gathering and Assessment

Document the attachment lien thoroughly:

- Obtain a certified copy of the lien from the county recorder’s office

- Request a detailed payoff statement from the creditor or their attorney

- Review the underlying lawsuit or claim that generated the lien

- Calculate total amount owed including principal, interest, fees, and costs

- Determine the lien’s recording date to understand its priority

Assess your property and equity position:

- Get a professional property valuation or comparative market analysis

- List all other liens and encumbrances (mortgages, tax liens, HOA liens)

- Calculate your net equity: Property Value – All Liens – Selling Costs

- Determine if you have positive equity, break-even, or negative equity situation

Understand your legal standing:

- Consult with a property lien attorney to review the lien’s validity

- Determine if grounds exist to contest or challenge the attachment

- Understand your state’s specific laws regarding attachment liens

- Review any defenses available in the underlying lawsuit

Phase 2: Strategy Selection and Planning

Match your situation to the optimal solution:

Choose payoff strategy if:

- You have sufficient equity to cover all liens and costs

- You want maximum sale price and can wait 60-120 days

- Your credit preservation is a high priority

- The property is in good condition for traditional marketing

Choose negotiation strategy if:

- Equity is limited but you have some cash for settlement

- You can demonstrate financial hardship

- The creditor has indicated willingness to negotiate

- You have time to work through the negotiation process

Choose cash buyer strategy if:

- You need to close quickly (under 30 days)

- The property needs significant repairs

- You’re facing additional legal pressure or foreclosure

- The stress of managing the situation is overwhelming

- Traditional sale attempts have failed

Phase 3: Execution and Coordination

For payoff strategy:

- List property with agent experienced in lien sales or contact cash buyers

- Disclose lien to all potential buyers upfront

- Obtain updated payoff statement as closing approaches

- Coordinate with title company to include lien payoff in closing

- Ensure lien release is recorded immediately after payment

For negotiation strategy:

- Prepare comprehensive settlement proposal with documentation

- Submit formal offer to creditor’s attorney

- Engage in back-and-forth negotiation maintaining professional communication

- Secure written settlement agreement specifying exact terms

- Coordinate settlement payment with property sale closing

- Verify lien release is properly recorded

For cash buyer strategy:

- Contact reputable buyers like Sure Path Property Solutions

- Provide complete information about property and lien situation

- Review and accept cash offer

- Allow buyer to coordinate lien resolution and title clearance

- Select closing date that works for your timeline

- Sign documents and receive proceeds

Phase 4: Closing and Verification

Critical closing day tasks:

- Review closing statement carefully ensuring lien payoff amount is correct

- Verify funds distribution showing payment going directly to creditor

- Obtain lien release documentation signed by creditor or their attorney

- Confirm recording of release with county recorder within days of closing

- Keep complete records of all payoff documentation and releases

Post-closing follow-up:

- Monitor your credit report to ensure lien is removed (60-90 days)

- Retain copies of all closing documents permanently

- Verify no remaining balance or claims from the creditor

- Update your records showing clear title transfer

Common Challenges and How to Overcome Them

Even with a solid strategy, obstacles can emerge. Anticipating these challenges and knowing how to address them keeps your sale on track.

Challenge 1: Creditor Refuses to Negotiate

Why this happens: Some creditors have policies against settlements, or they believe they have strong leverage to collect the full amount.

Solutions that work:

- Present hard evidence of limited collectibility through financial statements and property valuations

- Involve a mediator or attorney who specializes in debt negotiation

- Wait for strategic timing such as end-of-quarter when creditors want to close accounts

- Consider bankruptcy consultation (the mere possibility often motivates negotiation)

- Work with cash buyers who have established creditor relationships and negotiation expertise

Challenge 2: Multiple Liens Create Complexity

When your property has an attachment lien plus other liens (mortgage, tax liens, mechanic’s liens), coordinating payoffs becomes complicated.

Priority matters: Liens are typically paid in order of recording date, with some exceptions (tax liens often have super-priority). Understanding lien priority is crucial for determining how sale proceeds will be distributed.

Solutions for multiple lien situations:

- Work with experienced title companies that handle complex closings regularly

- Create a detailed payoff timeline coordinating all creditors

- Consider selling to investors who specialize in properties with multiple liens

- Negotiate with junior lien holders who might accept less to avoid being wiped out

- Explore whether any liens can be contested or removed

Challenge 3: Insufficient Equity to Cover All Obligations

This represents the most challenging scenario—when your property value minus all liens leaves you short.

Example scenario:

- Property value: $200,000

- First mortgage: $150,000

- Attachment lien: $60,000

- Selling costs: $15,000

- Total obligations: $225,000 (exceeds value by $25,000)

Viable approaches:

Short sale with all creditors: Negotiate with both mortgage lender and attachment lien holder to accept less than full payoff. This requires demonstrating hardship and getting all parties to agree.

Bring cash to closing: If you have savings or can borrow from family, bringing $25,000 to closing resolves all obligations. While painful, it provides clean resolution.

Deed in lieu or foreclosure: As a last resort, allowing foreclosure may eliminate the attachment lien if it’s junior to the mortgage. Consult an attorney about your state’s specific laws.

Cash buyer creative solutions: Some specialized buyers can structure transactions that address shortfalls through creative approaches. Companies that buy tax lien properties often have experience with complex negative equity situations.

Challenge 4: Time Constraints and Urgent Deadlines

When facing foreclosure, additional legal action, or personal emergencies, time pressure intensifies.

Fast-track strategies:

- Contact cash buyers immediately who can close in 7-14 days

- Request expedited payoff statements from all creditors

- Use experienced closing attorneys who can accelerate the process

- Prepare all documentation in advance (deed, identification, property documents)

- Communicate urgency clearly to all parties involved

What’s realistically possible:

- Cash sale with simple lien: 7-10 days minimum

- Cash sale with negotiation needed: 14-21 days

- Traditional sale with clear lien: 45-60 days minimum

- Traditional sale requiring negotiation: 60-90 days

Legal Considerations and Protections

Understanding your legal rights and obligations protects you throughout the process and prevents future complications.

Your Rights as a Property Owner

Right to contest the lien: If you believe the attachment lien is invalid, improperly filed, or based on a disputed claim, you can challenge it in court. Grounds for contest include:

- Improper service of legal documents

- Lack of jurisdiction

- Lien amount exceeds the underlying claim

- Procedural errors in obtaining the attachment order

Right to redeem: In most states, you retain the right to pay off liens and redeem your property even after judgment, though time limits apply.

Right to proceeds: If sale proceeds exceed all liens and costs, you’re entitled to the surplus. The title company holds these funds for you.

Right to representation: You can hire an attorney at any stage to protect your interests, negotiate on your behalf, or challenge improper actions.

Disclosure Obligations

To potential buyers: Most states require disclosure of known liens. Failing to disclose can result in:

- Buyer lawsuit for fraud or misrepresentation

- Unwinding of the sale transaction

- Liability for buyer’s damages and legal fees

To your lender: If you have a mortgage, review your loan documents. Some require notification of liens or legal actions affecting the property.

To title company: Complete honesty with your title company is essential. They’ll discover liens during the title search anyway, and early disclosure allows them to plan for resolution.

Protecting Yourself From Liability

Get written agreements: All settlement negotiations and agreements should be in writing, signed by authorized representatives of the creditor.

Verify authority: Ensure the person negotiating has actual authority to settle the debt and release the lien.

Obtain proper releases: The lien release must be properly executed, notarized, and recorded with the county recorder. Don’t rely on verbal promises.

Use escrow or title company: Never pay creditors directly outside of closing. Payment through the title company provides documentation and ensures proper handling.

Keep permanent records: Retain copies of all lien releases, settlement agreements, and closing documents indefinitely. These protect you if questions arise years later.

Working With Sure Path Property Solutions: Your Partner in Complex Sales

When you’re facing the challenge of how to sell house with attachment lien: urgent solutions, having an experienced partner makes all the difference. Sure Path Property Solutions specializes in exactly these complicated situations.

Why Specialized Expertise Matters

Industry experts understand lien mechanics: The team has handled hundreds of lien situations and understands the legal, financial, and practical aspects of resolution. This expertise translates to better outcomes for property owners.

Established creditor relationships: Through repeated interactions, specialized buyers develop working relationships with creditors and their attorneys, facilitating smoother negotiations.

Creative problem-solving: Every situation is unique. Expert service means tailoring solutions to your specific circumstances rather than applying one-size-fits-all approaches.

Coordinated resolution: Managing multiple parties—creditors, attorneys, title companies, county offices—requires organizational skills and persistence. Professional buyers handle this coordination, removing the burden from your shoulders.

The Sure Path Difference

Compassionate, helpful guidance: Facing an attachment lien is stressful. The friendly and caring approach at Sure Path Property Solutions means you’re treated with respect and empathy, not as just another transaction.

Transparent communication: You’ll receive clear explanations of your options, realistic assessments of outcomes, and honest guidance about the best path forward.

Fast, trustworthy service: When time matters, Sure Path delivers. Quick evaluations, prompt offers, and rapid closings provide the relief you need.

No-obligation consultation: Discussing your situation costs nothing. You’ll gain valuable insights and options even if you choose a different path.

Proven track record: Hundreds of satisfied clients have successfully resolved their property challenges through Sure Path’s helpful solutions.

What to Expect When You Reach Out

- Initial conversation: A brief discussion about your property, the attachment lien, and your goals

- Information gathering: Providing details about the lien amount, property condition, and timeline needs

- Expert evaluation: Professional assessment of your situation and viable solutions

- Written offer: Clear, written cash offer typically within 24-48 hours

- Solution explanation: Detailed explanation of how the lien will be handled

- Your decision: Time to review, ask questions, and decide if the solution works for you

- Smooth closing: If you accept, coordinated closing process handling all details

Frequently Asked Questions

Can I sell my house if there’s an attachment lien on it?

Yes, absolutely. You can sell a house with an attachment lien through several methods: paying off the lien from sale proceeds, negotiating a settlement with the creditor, or working with specialized cash buyers who handle the lien resolution. The lien must be addressed at closing, but it doesn’t prevent the sale.

How much will an attachment lien reduce my sale proceeds?

The lien amount plus any accrued interest and fees will be deducted from your proceeds at closing. If you successfully negotiate a settlement for less than the full amount, you’ll save the difference. Working with experienced negotiators can potentially save thousands of dollars.

Will buyers be scared away by an attachment lien?

Traditional buyers seeking financing may be deterred because lenders won’t approve loans on properties with unresolved liens. However, cash buyers and investors who specialize in properties with liens are not deterred—they view liens as solvable problems and make offers accordingly.

How long does it take to sell a house with an attachment lien?

Timeline varies by approach: cash sales can close in 7-14 days once an agreement is reached; traditional sales typically take 60-120 days. Negotiating lien settlements adds 2-6 weeks depending on creditor responsiveness. Working with experienced buyers who handle negotiations can significantly accelerate the process.

What happens if I just ignore the attachment lien?

Ignoring an attachment lien worsens your situation. The debt continues accruing interest, the underlying lawsuit may result in a larger judgment, and eventually the creditor may force a sale of your property through judicial foreclosure. Additionally, your credit suffers, and you lose control over the outcome. Early action preserves more options and better outcomes.

Can I remove an attachment lien without selling?

Yes, if you have funds available, you can pay off the lien directly without selling. Alternatively, you might refinance to access equity for payoff, negotiate a settlement for less than the full amount, or contest the lien in court if you have valid grounds. However, many people facing attachment liens lack the liquid resources for these options, making a sale the most practical solution.

Do I need an attorney to sell a house with an attachment lien?

While not legally required in most cases, consulting a property lien attorney is highly advisable. An attorney can review the lien’s validity, negotiate with creditors, protect your interests, and ensure proper handling of the transaction. If you work with specialized cash buyers, they often coordinate with attorneys as part of their service, reducing your need to hire separate counsel.

Real Success Stories: How Homeowners Resolved Attachment Liens

Sarah’s Story: Business Debt Becomes Manageable

Sarah owned a small consulting business that failed, leaving her with $75,000 in unpaid vendor debts. One vendor obtained an attachment lien on her home valued at $280,000. She owed $180,000 on her mortgage, leaving $100,000 in equity—but the lien consumed most of it.

Sarah contacted Sure Path Property Solutions, which evaluated her situation and negotiated directly with the creditor. Through persistent negotiation and demonstrating the property’s actual equity position, they secured a settlement for $42,000—a savings of $33,000. Sarah sold her home, paid off all obligations, and walked away with $45,000 to start fresh. The entire process took 28 days.

Michael’s Story: Lawsuit Lien Resolved Through Fast Sale

Michael was involved in a business partnership dispute that resulted in an attachment lien for $95,000 on his property. With the lawsuit ongoing and legal fees mounting, he needed to relocate for a new job opportunity. Traditional sale wasn’t viable due to the uncertain lien amount and his tight timeline.

He reached out to a cash buyer specializing in lien properties. The buyer made an offer accounting for the lien, handled all creditor negotiations, and closed in 12 days. Michael received his equity, avoided continued legal stress, and started his new position on time. The expert service and friendly and caring approach made a stressful situation manageable.

The Rodriguez Family: Multiple Liens Untangled

The Rodriguez family inherited a property with both an attachment lien from a contractor dispute ($38,000) and delinquent property taxes ($12,000). As multiple heirs, coordinating decisions was challenging, and none had funds to clear the liens.

Working with Sure Path Property Solutions, they received a cash offer that accounted for both liens. The buyer coordinated with the county tax office and the contractor’s attorney, negotiated settlements on both obligations, and purchased the property. Each heir received their share of the remaining proceeds, and the complicated situation was resolved in 21 days without any family member paying out-of-pocket.

Taking Action: Your Next Steps Forward

Understanding how to sell house with attachment lien: urgent solutions empowers you to move forward confidently. The path ahead becomes clearer when you break it into concrete steps.

Immediate Actions (Within 24-48 Hours)

- Gather your documentation:

- Copy of the attachment lien from county records

- Recent mortgage statement showing balance owed

- Property tax records

- Any correspondence from the creditor or their attorney

- Assess your property value:

- Research recent comparable sales in your neighborhood

- Consider requesting a professional valuation

- Calculate your approximate equity position

- Contact specialized help:

- Reach out to Sure Path Property Solutions for a no-obligation consultation

- Discuss your situation with a property lien attorney if the lien seems questionable

- Connect with a title company to understand the lien’s impact

Short-Term Actions (Within 1-2 Weeks)

- Request payoff information:

- Contact the creditor or their attorney for a detailed payoff statement

- Ask about interest rates and how quickly the amount is growing

- Inquire about settlement possibilities

- Evaluate your options:

- Compare the three main strategies (payoff, negotiation, cash buyer)

- Consider your timeline, financial resources, and stress tolerance

- Discuss options with family members or advisors

- Make your strategic decision:

- Choose the approach that best fits your circumstances

- Commit to following through rather than continuing to delay

- Set a target timeline for resolution

Execution Phase (Ongoing)

- Implement your chosen solution:

- If pursuing traditional sale, list with an experienced agent

- If negotiating, prepare and submit your settlement proposal

- If working with cash buyers, accept an offer and coordinate closing

- Stay organized and responsive:

- Respond promptly to requests for information or documentation

- Keep all parties informed of developments

- Maintain a file with all correspondence and documents

- Follow through to completion:

- Attend closing prepared with required identification and documents

- Review all closing documents carefully before signing

- Verify lien release is properly recorded after closing

Moving Forward After Resolution

- Rebuild and plan ahead:

- Learn from the experience to avoid future lien situations

- Address any underlying financial issues that contributed to the problem

- Celebrate resolving a difficult situation and moving forward

Conclusion: Your Path to Resolution Starts Now

Facing an attachment lien on your property feels overwhelming, but you’ve now discovered that viable solutions exist. Whether you choose to pay off the lien from sale proceeds, negotiate a settlement, or work with specialized cash buyers, you have options that lead to resolution.

The key to success lies in taking action quickly rather than hoping the problem resolves itself. Every day of delay costs money through accruing interest and potentially narrows your options. But with the right guidance and support, you can navigate this challenge successfully.

Remember these essential truths:

- An attachment lien is a solvable problem, not a permanent obstacle

- You retain more control and options than you might think

- Professional expertise dramatically improves outcomes and reduces stress

- Thousands of homeowners successfully sell properties with liens every year

- The sooner you act, the better your results will be

Sure Path Property Solutions stands ready to provide the helpful solutions, expert service, and trustworthy guidance you need. The friendly and caring team understands the stress you’re experiencing and has the industry expertise to resolve even the most complicated situations.

Your next step is simple: Reach out for a no-obligation consultation. Within 24-48 hours, you’ll have clarity about your options, a potential cash offer, and a clear path forward. The burden you’ve been carrying can be lifted, allowing you to move forward with your life.

Don’t let an attachment lien hold you hostage any longer. The solution to how to sell house with attachment lien: urgent solutions is within reach. Take that first step today—your future self will thank you.

Contact Sure Path Property Solutions now to discuss your situation and discover your best path forward. Freedom from your attachment lien is closer than you think.