How to Sell Inherited Property: Your Complete Step-by-Step Guide for 2025

Inheriting property often comes with mixed emotions—gratitude for the gift, grief for the loss, and uncertainty about what to do next. When you inherit a house or land, you’re suddenly faced with complex decisions involving taxes, legal processes, family dynamics, and financial considerations that can feel overwhelming. Whether you’ve recently inherited property from a parent, spouse, or other loved one, understanding how to sell inherited property efficiently while maximizing your financial benefit is crucial.

This comprehensive guide walks you through every aspect of selling inherited property, from navigating the probate process to understanding tax implications, coordinating with multiple heirs, and preparing the property for a successful sale. With the right knowledge and helpful guidance, you can transform this challenging situation into a smooth transaction that honors your loved one’s legacy while securing your financial future.

Key Takeaways

- Probate is often required before you can sell an inherited house, with timelines varying from weeks to over a year depending on estate complexity and state laws

- Stepped-up basis provides significant tax advantages, potentially eliminating or reducing capital gains tax when you sell inherited property

- Multiple heirs require clear communication and legal agreements to avoid disputes and ensure a successful sale of the property

- Property condition and market timing significantly impact your final sale price and overall inheritance value

- Professional guidance from real estate agents, tax experts, and attorneys helps navigate the complex process of selling an inherited property while avoiding costly mistakes

Understanding the Basics When You Inherit Property

When you inherit a house or other real estate, you’re receiving more than just a physical asset—you’re taking on a complex set of responsibilities, opportunities, and potential challenges. The process of selling an inherited property differs significantly from a traditional home sale, primarily due to legal requirements, tax considerations, and the emotional weight that often accompanies inheritance.

The moment you inherit property, several factors immediately come into play. First, you’ll need to determine whether the property was held in a trust, passed through a will, or transferred via other mechanisms like a transfer on death deed. This distinction fundamentally affects how quickly you can sell the property and what legal steps you’ll need to complete.

Understanding your role as a beneficiary is equally important. You may be the sole heir with complete decision-making authority, or you might be one of several heirs who must coordinate and agree on whether to sell, when to list the property, and how to divide the proceeds from the sale. Each scenario presents unique challenges that require careful navigation.

The emotional aspects of selling a loved one’s home shouldn’t be underestimated. Many people who inherit a house struggle with feelings of guilt, attachment to childhood memories, or family pressure to keep the property. Recognizing these emotions as normal while still making sound financial decisions is part of the process. Sure Path Property Solutions understands these challenges and provides friendly and caring support throughout the entire journey.

Property type matters significantly when you inherit real estate. A single-family home in good condition presents different challenges than vacant land, a multi-unit rental property, or a house requiring substantial repairs. Each property type has distinct market considerations, maintenance requirements, and potential buyer pools that influence your selling strategy.

What Is the Probate Process and Do You Need It?

Probate is the legal process through which a deceased person’s estate is settled, debts are paid, and assets are distributed to heirs. When you inherit a house, understanding the probate process is essential because it directly impacts your timeline and ability to sell the property.

The probate process typically involves several key steps:

- Filing the will (if one exists) with the local probate court

- Appointing an executor or personal representative

- Inventorying the deceased’s assets, including real estate

- Notifying creditors and paying outstanding debts

- Distributing remaining assets to beneficiaries according to the will or state law

- Obtaining court approval to close the estate

The duration of probate varies dramatically based on the complexity of the estate, whether anyone contests the will, the efficiency of the local court system, and state-specific laws. Simple estates might clear probate in as little as six months, while complicated situations can take as long as two years or more.

Not all inherited property requires probate. If the deceased placed the property in a living trust, designated beneficiaries through a transfer on death deed, or held the property in joint tenancy with right of survivorship, the property may transfer directly to you without going through the probate process. This can significantly accelerate your ability to sell the home.

During probate, the executor has specific responsibilities regarding inherited real estate. These include maintaining the property, paying the mortgage (if one exists), covering property taxes and insurance, and eventually distributing the asset according to the estate plan. If you’re both the executor and the beneficiary, you’ll wear both hats throughout this process.

Some states offer simplified probate procedures for smaller estates, which can expedite the process considerably. The threshold for “small estate” status varies by state, ranging from $25,000 to $150,000 or more in total estate value. Consulting with a probate attorney in your jurisdiction helps determine which path applies to your situation and can provide expert service tailored to your needs.

How to Navigate Tax Implications When You Sell an Inherited House

Tax considerations represent one of the most important—and often misunderstood—aspects of selling inherited property. Understanding these implications helps you make informed decisions and potentially save thousands of dollars.

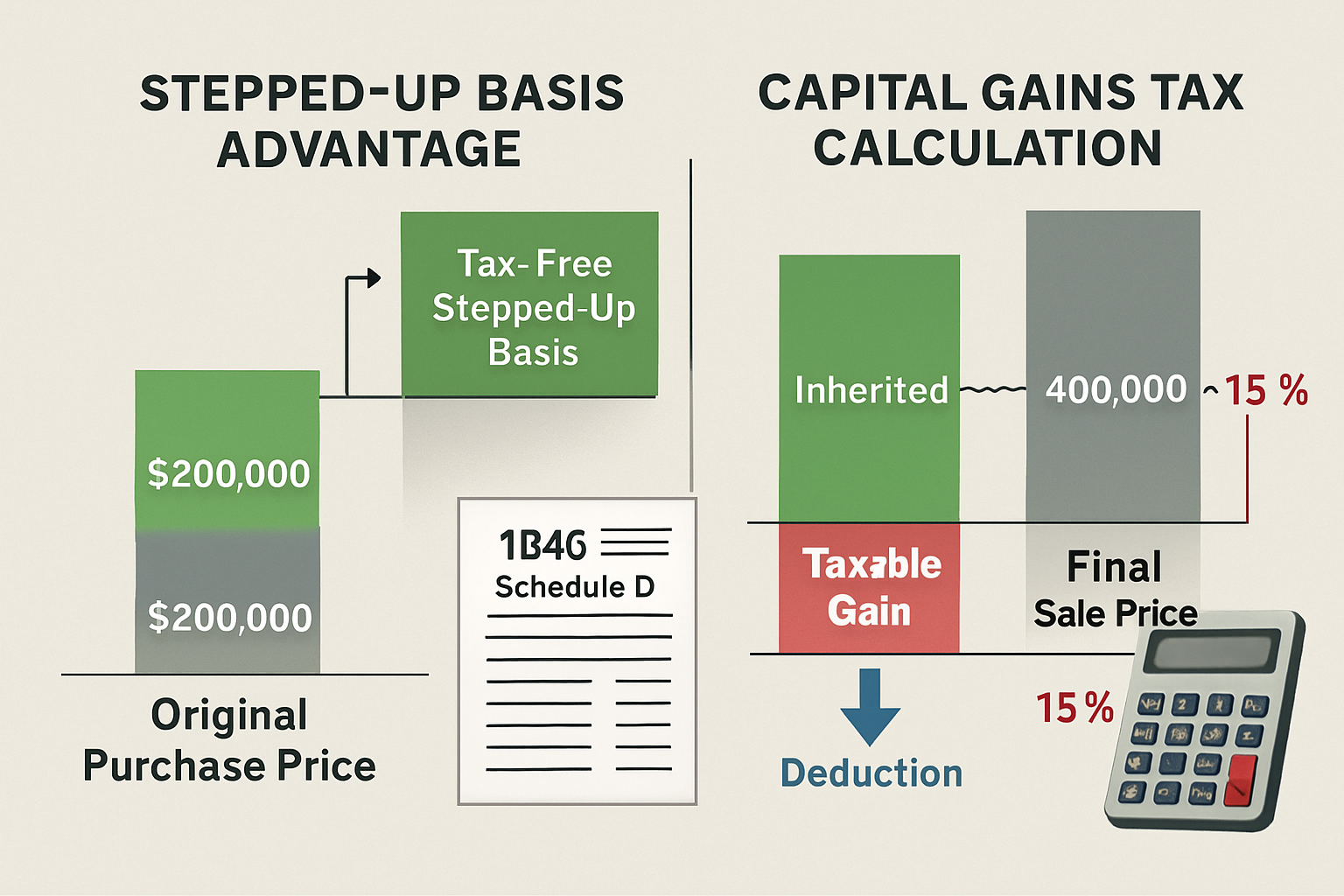

The stepped-up basis is your greatest tax advantage when you inherit property. Unlike property you purchase yourself, inherited real estate receives a “step-up” in cost basis to the fair market value at the time of the owner’s death. This means if your parents bought a house for $50,000 decades ago, but it was worth $300,000 when you inherited it, your cost basis for tax purposes is $300,000—not the original purchase price.

This stepped-up basis dramatically reduces or eliminates capital gains tax when you sell the property. If you sell the inherited home for $310,000 shortly after inheritance, you’d only pay capital gains tax on the $10,000 difference between your stepped-up basis and the final sale price, rather than on the $260,000 in appreciation that occurred during the original owner’s lifetime.

Capital gains tax rates depend on how long you hold the property before selling. Inherited property is automatically considered a long-term capital gain regardless of how quickly you sell, which means you benefit from lower long-term capital gains tax rates (0%, 15%, or 20% depending on your income) rather than higher short-term rates.

To determine capital gains accurately, you’ll need a professional appraisal establishing the property’s fair market value at the time of death. This time of death appraisal becomes your official cost basis for tax purposes. Keep this documentation carefully, as you’ll need it when filing your tax return after the sale.

Inheritance tax differs from estate tax and capital gains tax. Most states don’t impose inheritance tax, and the federal estate tax only applies to estates exceeding $13.61 million in 2025. However, a handful of states do levy inheritance taxes on beneficiaries. Consulting with a tax expert familiar with your state’s laws ensures you understand all potential tax obligations.

If you decide to live in the property as your primary residence for at least two years before selling, you may qualify for the home sale tax exclusion, which allows single filers to exclude up to $250,000 in gains ($500,000 for married couples) from taxable income. This strategy can provide additional tax benefits if you’re willing to delay the sale.

Deductible expenses can reduce your tax burden when you sell inherited property. Costs like real estate agent commissions, legal fees, title insurance, closing costs, and major improvements made before the sale can be added to your cost basis or deducted from proceeds, reducing the amount subject to capital gains tax.

Coordinating with Multiple Heirs: Challenges and Solutions

When property passes to multiple heirs, the complexity of selling increases significantly. Sibling dynamics, differing financial needs, emotional attachments, and conflicting visions for the property can transform what should be a straightforward transaction into a source of family tension.

Clear communication from the outset prevents most heir disputes. Schedule a family meeting early in the process where all heirs can express their preferences, concerns, and expectations. Some may want to sell immediately, others might prefer to rent the property, and some may wish to buy out other heirs and keep the family home. Understanding everyone’s position creates a foundation for productive negotiation.

Legal ownership structure matters when you inherit property along with siblings or other relatives. Most commonly, heirs receive the property as “tenants in common,” meaning each person owns a specific percentage share. All co-owners must typically agree to sell the property, and proceeds are divided according to ownership percentages.

What happens when one heir wants to sell but others don’t? This common scenario has several potential solutions. The heir who wants to keep the property can buy out the others at fair market value. Alternatively, heirs might agree to rent the property for a specified period before selling. If no agreement is possible, any heir can file a partition action lawsuit—a legal proceeding that forces the sale of the property and division of proceeds among heirs.

A partition action should be a last resort, as it’s costly, time-consuming, and often damages family relationships. The court may order a partition sale where the property is sold at auction, often below market value, with legal fees deducted from proceeds before distribution. Understanding partition actions helps heirs recognize why negotiated settlements are almost always preferable.

Creating a written agreement among heirs protects everyone’s interests. This document should specify decision-making processes, how expenses will be shared, timelines for the sale, selection of the real estate agent, acceptable price ranges, and how proceeds will be divided. Having all heirs sign this agreement before listing the property prevents misunderstandings later.

Financial disparities among heirs can complicate matters. One sibling might desperately need their inheritance immediately due to financial hardship, while another with greater resources might prefer to wait for a better market. Acknowledging these different circumstances with empathy while still protecting everyone’s financial interests requires delicate balance and sometimes creative solutions like one heir providing a loan to another against their future inheritance.

Professional mediation can resolve heir conflicts when family discussions reach an impasse. A neutral third-party mediator experienced in estate and real estate matters can facilitate productive conversations, propose compromise solutions, and help heirs reach agreements that might seem impossible during emotional family discussions. This investment in mediation typically costs far less than litigation and preserves family relationships.

Step-by-Step: How to Sell Inherited Property

Successfully selling an inherited house requires following a systematic process that addresses legal requirements, property preparation, marketing, and closing. Here’s your comprehensive roadmap for navigating each phase.

Step 1: Secure the property immediately. Change locks, ensure adequate insurance coverage, and arrange for regular property checks if the home will be vacant. Vacant inherited properties are targets for theft, vandalism, and squatters, which can devastate property value and create legal complications.

Step 2: Obtain legal authority to sell. If probate is required, you cannot legally sell the property until the court grants you authority as executor or the probate process concludes and title transfers to beneficiaries. If the property was held in trust or passed outside probate, verify that title has properly transferred to you before proceeding.

Step 3: Address any existing mortgage. If the inherited home has an outstanding mortgage, determine the payoff amount and whether the estate has sufficient funds to continue payments during the selling process. Most mortgages contain a “due on sale” clause that technically allows lenders to demand full payment when ownership transfers, though many lenders don’t enforce this immediately if payments continue. Communicating with the mortgage lender early prevents foreclosure risks.

Step 4: Get a professional property valuation. While you needed a time of death appraisal for tax purposes, you’ll also want a current market analysis from a local real estate agent to determine the optimal listing price. Market conditions may have shifted since the inheritance, and pricing correctly from the start is crucial for a successful sale.

Step 5: Decide whether to sell as-is or make improvements. Inherited homes often need repairs, updates, or deep cleaning. Calculate whether investments in improvements will yield sufficient return in the final sale price, or whether selling the house for cash to an investor as-is makes more financial sense. Sure Path Property Solutions specializes in purchasing inherited properties in any condition, providing helpful solutions when traditional sales aren’t practical.

Step 6: Choose your selling method. You have several options: listing with a traditional real estate agent for maximum market exposure, selling to a cash buyer or investor for speed and convenience, or auctioning the property. Each approach has distinct advantages depending on your timeline, property condition, and financial goals.

Step 7: Prepare the property for showing. If listing traditionally, invest in cleaning, decluttering, minor repairs, and possibly staging. First impressions significantly impact buyer interest and offers. Remove personal items and family photos to help potential buyers envision the space as their own rather than someone else’s family home.

Step 8: Market the property effectively. Work with your real estate agent to develop a comprehensive marketing strategy including professional photography, online listings, open houses, and targeted advertising. Inherited properties sometimes have unique features or historical significance that can be marketing advantages when positioned correctly.

Step 9: Review and negotiate offers. When offers arrive, evaluate them not just on price but also on terms, contingencies, buyer financing strength, and closing timeline. Your real estate agent’s experience selling inherited properties helps you identify the strongest offers and negotiate effectively.

Step 10: Navigate the closing process. Once you accept an offer, you’ll proceed through inspections, appraisals, title work, and final closing. Be prepared to provide documentation proving your authority to sell, clear title, and satisfy any liens or judgments attached to the property. Understanding how to handle property liens ensures these issues don’t derail your sale.

Step 11: Distribute proceeds appropriately. After closing, proceeds must first satisfy any outstanding mortgage, pay property taxes, cover closing costs, and reimburse estate expenses. Remaining funds are then distributed to heirs according to the will or state inheritance laws.

Should You Sell Immediately or Wait? Timing Considerations

The decision of whether to sell inherited property immediately or hold it involves weighing financial, practical, and emotional factors. There’s no universal right answer—the best choice depends on your specific circumstances.

Advantages of selling quickly include avoiding ongoing expenses like mortgage payments, property taxes, insurance, and maintenance costs that can quickly drain inheritance value. You’ll also eliminate the stress of managing a property from a distance, dealing with repairs, or coordinating with other heirs over an extended period. Quick sales provide immediate liquidity, which may be crucial if you have debts, financial goals, or simply want to close this chapter.

Market conditions significantly influence timing decisions. In a strong seller’s market with low inventory and high demand, selling quickly can capture premium prices. Conversely, if the market is soft or declining, waiting for conditions to improve might yield better returns—though you’ll incur carrying costs during the wait.

Tax considerations may favor immediate sale. Since inherited property receives stepped-up basis to fair market value at the time of death, selling soon after inheritance typically results in minimal capital gains tax. The longer you hold the property, the more it may appreciate beyond your stepped-up basis, increasing your eventual tax liability.

However, strategic waiting can make financial sense in certain situations. If the property needs significant repairs that you can’t immediately afford, holding it while saving for improvements might increase the final sale price enough to justify the delay. If you’re in a high-income year, waiting to sell until a lower-income year could reduce your capital gains tax rate.

Converting the inherited home into a rental property represents another option. This approach generates income while potentially allowing the property to appreciate. However, becoming a landlord involves responsibilities, risks, and tax implications that differ from simply selling. Rental income is taxable, and when you eventually sell a rental property, you’ll face depreciation recapture taxes in addition to capital gains.

Emotional readiness matters more than many people acknowledge. Rushing to sell your childhood home or a beloved family member’s property before you’ve processed your grief can lead to regret. Conversely, holding onto property out of guilt or inability to let go can become a financial and emotional burden. Give yourself permission to make the decision that feels right for your situation, while still being realistic about the practical implications.

If you’re uncertain about timing, consider a middle path: secure and maintain the property while you take a few months to research options, consult with professionals, and reach clarity about your goals. This deliberate approach prevents both hasty decisions and indefinite procrastination.

Preparing an Inherited Home for Sale: What’s Worth the Investment?

The condition of the inherited home significantly impacts both the sale price and how quickly you’ll find a buyer. Determining which improvements justify their cost and which don’t requires strategic thinking about your specific property and market.

Start with a thorough property inspection to identify all issues, from minor cosmetic problems to major structural concerns. This inspection serves two purposes: helping you decide what to repair before listing, and preventing surprises during the buyer’s inspection that could derail the sale or force price reductions.

Essential repairs that almost always pay off include fixing safety hazards, addressing water damage or leaks, repairing broken windows or doors, ensuring all systems (HVAC, plumbing, electrical) function properly, and resolving any code violations. Buyers and their lenders often require these issues be addressed before closing.

Cosmetic improvements offer varying returns depending on your market. Fresh paint in neutral colors, deep cleaning (especially carpets), replacing broken fixtures, and basic landscaping typically cost relatively little while significantly improving first impressions. These modest investments can yield returns of 100-200% in increased sale price or faster sale.

Major renovations rarely make financial sense when selling inherited property. Kitchen and bathroom remodels, new flooring throughout, or room additions cost tens of thousands of dollars and typically return only 50-80% of their cost in increased sale price. Unless the property is truly uninhabitable without these improvements, your money is better invested elsewhere.

The “as-is” sale option deserves serious consideration, especially if the inherited home needs substantial work. Selling to a cash buyer or investor who specializes in fixer-uppers eliminates repair costs, shortens your timeline dramatically, and removes the stress of managing contractors and renovations. While you’ll receive a lower price than if you completed all repairs, you avoid the risk, time, and upfront costs of improvements.

Decluttering and depersonalizing are non-negotiable if listing traditionally. Inherited homes often contain decades of accumulated possessions, family photos, and personal items. Removing these creates a blank canvas that helps buyers envision themselves in the space. Consider hiring an estate sale company to handle valuable items, donating usable goods, and disposing of the rest responsibly.

Staging can significantly impact sale price and time on market, particularly for higher-end properties. Professional staging typically costs $2,000-$5,000 but can increase sale prices by 5-15% while reducing market time by weeks or months. For more modest properties, simple furniture arrangement and adding a few decorative touches may suffice.

Curb appeal creates crucial first impressions. Mowing the lawn, trimming overgrown bushes, adding fresh mulch, planting flowers, power washing the exterior, and ensuring the entrance is welcoming costs relatively little but dramatically affects buyer interest. Many potential buyers drive by properties before scheduling showings, and poor curb appeal eliminates your home from consideration before they ever step inside.

Understanding Your Selling Options: Traditional Sale vs. Cash Buyer

When you want to sell inherited property, you’re not limited to the traditional listing process. Understanding all available options helps you choose the approach that best fits your timeline, property condition, and financial goals.

Traditional real estate agent listings offer maximum market exposure and typically achieve the highest sale prices. Experienced agents market your property across multiple platforms, conduct showings, negotiate with buyers, and guide you through closing. This approach works best when the property is in good condition, you have time to wait for the right buyer (typically 30-90 days or longer), and maximizing sale price is your top priority.

Real estate agent commissions typically total 5-6% of the sale price, split between the listing agent and buyer’s agent. While this represents a significant expense, skilled agents often negotiate prices that more than offset their fees. Look for agents with specific experience selling inherited properties who understand the unique challenges you face.

Selling to a cash buyer or real estate investor offers speed, convenience, and certainty. Companies like Sure Path Property Solutions purchase inherited properties in any condition, often closing in as little as 7-14 days. This option eliminates repair costs, agent commissions, lengthy marketing periods, and the risk of deals falling through due to buyer financing issues.

The trade-off is price—cash buyers typically offer 70-85% of market value, depending on property condition and local market factors. However, when you factor in repairs you won’t make, commissions you won’t pay, carrying costs you’ll avoid, and the value of speed and certainty, the net proceeds often compare favorably to traditional sales, especially for properties needing substantial work.

For Sale By Owner (FSBO) represents another option where you market and sell the property yourself without an agent. This approach saves commission costs but requires significant time, expertise, and effort. You’ll handle all marketing, showings, negotiations, and paperwork yourself. FSBO works best for experienced sellers with real estate knowledge, time to dedicate to the process, and properties in high-demand markets where homes sell easily.

Auction sales can work for unique properties, estates with time pressures, or situations where heirs can’t agree on listing price. Auctions create urgency and competition among buyers, potentially driving prices up. However, they also risk selling below market value if bidder turnout is poor, and typically involve substantial auction house fees.

Seller financing offers another creative option where you act as the lender, allowing the buyer to make payments over time rather than obtaining traditional mortgage financing. This approach can attract buyers who can’t qualify for conventional loans and may allow you to command a higher price while generating ongoing income. However, it involves risk if the buyer defaults and delays your receipt of full proceeds.

Choosing among these options requires honest assessment of your priorities. Ask yourself:

- How quickly do I need to sell?

- Can I afford ongoing property expenses while waiting for the right buyer?

- Is the property in condition to list traditionally?

- Do I have funds to invest in repairs and improvements?

- Am I willing to manage the selling process or do I need expert service?

- Is maximizing price my top priority, or do I value speed and certainty more?

Many sellers benefit from getting multiple perspectives. Request a market analysis from a traditional real estate agent, obtain a cash offer from an investor, and compare the net proceeds, timelines, and stress levels of each approach before deciding. This comparative analysis often reveals that the option with the highest sale price doesn’t always yield the best net outcome when all factors are considered.

Dealing with Complications: Mortgages, Liens, and Title Issues

Inherited properties frequently come with complications that must be resolved before or during the sale process. Understanding how to handle these challenges prevents delays and protects your financial interests.

Existing mortgages on inherited property require immediate attention. You’ll need to determine the outstanding balance, monthly payment amount, and whether payments are current. If the deceased was behind on payments, the property may be in pre-foreclosure, requiring urgent action to prevent loss of the property. Understanding your options when selling in pre-foreclosure helps you navigate this challenging situation.

Most mortgages include a “due on sale” clause allowing the lender to demand full repayment when the property transfers ownership. However, federal law provides important protections for heirs. The Garn-St. Germain Act prevents lenders from enforcing due-on-sale clauses when property transfers to certain relatives upon the borrower’s death, provided the heir occupies or will occupy the property.

If you plan to sell the inherited home rather than live in it, communicate with the mortgage lender promptly. Most lenders won’t immediately enforce the due-on-sale clause if you’re actively working to sell the property and continuing to make payments. However, you should formalize this arrangement in writing to prevent foreclosure proceedings.

Reverse mortgages present unique challenges. These loans become due when the borrower dies, and the lender typically requires repayment within six months (with possible extensions). Heirs can satisfy the reverse mortgage by paying off the balance, refinancing into a traditional mortgage, or selling the property and using proceeds to repay the loan. If the reverse mortgage balance exceeds the home’s value, heirs can walk away without obligation, as reverse mortgages are non-recourse loans.

Property tax liens attach to inherited property when previous owners failed to pay property taxes. These liens take priority over almost all other claims and must be satisfied before you can sell with clear title. Understanding how to sell a house with tax liens provides strategies for resolving these issues efficiently.

Fortunately, tax liens are typically paid from estate assets or from sale proceeds at closing. If the estate lacks funds to pay delinquent taxes before listing, most title companies will facilitate payment from your sale proceeds, ensuring the buyer receives clear title.

Judgment liens and other creditor claims may also attach to inherited property. These arise when creditors obtain court judgments against the deceased for unpaid debts. Like tax liens, judgment liens must typically be satisfied before you can transfer clear title to a buyer. Learning about judgment liens helps you understand your obligations and options.

The good news is that heirs generally aren’t personally responsible for the deceased’s debts beyond the value of inherited assets. If the property value exceeds all liens and debts, you’ll receive the difference. If debts exceed the property value, you can often walk away without personal liability, though you won’t receive any inheritance from that property.

Mechanics liens can appear on inherited property if contractors performed work that wasn’t paid for before the owner’s death. These liens give contractors security interest in the property for unpaid work. Understanding mechanics liens helps you evaluate whether these claims are valid and how to resolve them.

Title issues and clouded titles represent another common complication with inherited property. These problems arise from errors in previous deeds, missing heirs, undisclosed easements, boundary disputes, or breaks in the chain of title. Resolving clouded title issues is essential before you can sell the property.

Title insurance companies conduct thorough title searches before insuring a property sale, and they’ll identify any title defects that must be corrected. Working with an experienced real estate attorney helps resolve title problems efficiently, whether through quiet title actions, obtaining releases from missing parties, or correcting deed errors.

Home equity lines of credit (HELOCs) function similarly to mortgages and must be repaid when you sell the property. The outstanding balance will be deducted from your sale proceeds at closing. Verify the exact payoff amount with the lender before accepting offers to ensure you understand your net proceeds.

When inherited property has multiple complications—perhaps a mortgage, tax liens, and title issues—the situation can feel overwhelming. This is precisely when trustworthy service from professionals who specialize in complex property situations becomes invaluable. Companies experienced in resolving these challenges can often purchase the property despite complications, handling all resolution work themselves and providing you with a clear, simple transaction.

Working with Professionals: Building Your Team

Successfully selling an inherited property typically requires guidance from multiple professionals, each bringing specialized expertise to different aspects of the process. Building the right team protects your interests and streamlines the transaction.

Real estate attorneys provide essential legal guidance, especially in complex inheritance situations. They can help you navigate probate, resolve title issues, interpret will provisions, draft agreements among multiple heirs, and review all sale documents before you sign. In some states, attorney involvement in real estate transactions is mandatory; in others, it’s optional but highly recommended for inherited property sales.

When selecting a real estate attorney, prioritize experience with probate and estate matters over general real estate practice. Ask about their familiarity with inherited property sales, their fee structure (hourly versus flat fee), and their availability to answer questions throughout your process.

Probate attorneys specialize specifically in estate settlement and may be necessary if the probate process is complex, the will is contested, or estate assets are substantial. While some attorneys handle both real estate and probate matters, others specialize in one area. Clarify which expertise you need based on your specific situation.

Tax professionals including CPAs and enrolled agents help you understand tax implications, calculate capital gains accurately, identify deductible expenses, and plan strategies to minimize tax liability. Their guidance is particularly valuable if you inherit property in a different state, if the estate is large enough to trigger estate taxes, or if you’re considering holding the property as a rental before selling.

Schedule a tax consultation early in the process, ideally before making major decisions about timing or improvements. A tax expert can model different scenarios, showing you the tax impact of selling immediately versus waiting, making improvements versus selling as-is, or converting to rental property.

Real estate agents with specific experience selling inherited properties bring valuable expertise to the process. They understand the emotional dynamics, know how to market estate properties effectively, can recommend appropriate pricing despite the property’s condition, and have networks of contractors, cleanout services, and other professionals you may need.

When interviewing potential agents, ask specifically about their experience with inherited properties, request references from previous clients in similar situations, and evaluate their marketing strategy for your property. The agent with the highest sales volume in your area isn’t necessarily the best choice—look for someone who demonstrates understanding of your unique situation and communicates in a way that makes you feel supported.

Appraisers provide professional valuations essential for establishing your stepped-up cost basis and determining appropriate listing prices. You’ll need an appraisal establishing fair market value at the time of death for tax purposes, and you may want an updated appraisal reflecting current market conditions when you’re ready to sell.

Choose appraisers certified in your state with experience valuing properties similar to your inherited home. The appraiser who values the property for tax purposes should be different from one you might use for listing purposes to avoid any appearance of bias.

Estate sale companies and cleanout services help manage the overwhelming task of dealing with a lifetime of accumulated possessions. These professionals can conduct estate sales to sell valuable items, donate usable goods, and dispose of remaining contents responsibly. Their services typically cost 30-40% of estate sale proceeds, but they handle all aspects of the sale including pricing, marketing, conducting the sale, and cleanup.

Home inspectors identify property defects and necessary repairs. While buyers will conduct their own inspections, getting a pre-listing inspection allows you to address issues proactively or price the property appropriately with full knowledge of its condition. This transparency can prevent deals from falling apart during the buyer’s inspection period.

Title companies research property ownership history, identify liens and encumbrances, and provide title insurance protecting buyers against future claims. They also typically handle closing, ensuring all documents are properly executed and funds are correctly distributed. Choosing an experienced title company familiar with inherited property transactions helps prevent delays and complications.

Contractors and handymen complete repairs and improvements you decide to make before listing. Get multiple bids for any significant work, verify contractors are licensed and insured, and check references before hiring. For inherited properties, contractors who specialize in estate properties and understand your timeline constraints are particularly valuable.

Assembling this team might seem expensive, but each professional provides specialized expertise that protects your financial interests and prevents costly mistakes. Many sellers find that professional fees are more than offset by higher sale prices, avoided legal problems, and reduced tax liability that result from expert guidance.

Special Situations: Out-of-State Property and Vacant Land

Certain types of inherited property present unique challenges that require specialized strategies and considerations.

Out-of-state inherited property complicates every aspect of the selling process. You’ll need to understand that state’s probate laws, property laws, and tax requirements, which may differ significantly from your home state. Managing repairs, showings, and maintenance from hundreds or thousands of miles away adds logistical challenges and expenses.

Ancillary probate may be required when you inherit out-of-state property. This is a secondary probate proceeding in the state where the property is located, separate from the primary probate in the state where the deceased lived. Ancillary probate adds time, legal fees, and complexity to the process.

Hiring local professionals becomes even more critical with out-of-state property. You’ll need a real estate agent, attorney, and potentially contractors in that location who can act as your eyes and ears. Video technology helps—request video tours, video calls for property inspections, and virtual meetings with your professional team to stay informed without constant travel.

Tax implications vary by state for out-of-state inherited property. Some states impose inheritance taxes while others don’t. You may need to file tax returns in both your home state and the state where the property is located. A tax professional familiar with multi-state inheritance issues helps you navigate these requirements and avoid double taxation.

Selling out-of-state inherited property to a cash buyer often makes particular sense because it eliminates the need for repeated trips to the property, ongoing maintenance from a distance, and coordination of repairs with contractors you’ll never meet in person. A single trip to closing (or even remote closing in some cases) completes the entire transaction.

Inherited vacant land presents different challenges than residential property. Land typically takes longer to sell, attracts a smaller buyer pool, and may have zoning restrictions, environmental issues, or access problems that affect value and marketability.

Determining the value of inherited land requires specialized appraisal expertise. Factors affecting land value include location, size, zoning, utilities availability, road access, topography, soil quality, environmental restrictions, and development potential. An appraiser experienced in land valuation in your specific area is essential.

Marketing land effectively requires different strategies than marketing homes. Buyers of vacant land include developers, investors, adjacent property owners looking to expand, recreational users, and people planning to build. Each buyer type responds to different marketing messages and looks for different property characteristics.

Carrying costs for vacant land can accumulate quickly. While you won’t have mortgage payments or maintenance costs like you would with a house, you’ll still owe property taxes, potentially homeowner association fees, and costs to maintain the land in compliance with local ordinances (mowing, weed control, etc.).

Zoning and environmental issues can significantly impact inherited land value. Properties in wetlands, flood zones, or areas with endangered species may have severe development restrictions. Land with previous commercial or industrial use may have environmental contamination requiring expensive remediation. Title research and environmental assessments help identify these issues before listing.

If the inherited land has development potential, you might consider subdividing it into multiple parcels before selling, as smaller parcels often sell more quickly and may yield higher total proceeds. However, subdivision involves surveying costs, government approval processes, and time that may not justify the potential return.

Agricultural land represents another special category with unique considerations. Farm and ranch land is often valued based on its productive capacity, water rights, and agricultural income potential. Buyers in this market are typically farmers, ranchers, or agricultural investors who evaluate properties very differently than residential buyers.

For both out-of-state property and vacant land, the complexity and specialized knowledge required often makes working with industry experts who handle these challenging situations regularly a wise choice. Their experience with these specific property types and their ability to close quickly despite complications can provide helpful solutions that traditional sales can’t match.

Emotional and Psychological Aspects of Selling a Loved One’s Home

The financial and legal aspects of selling inherited property receive most of the attention, but the emotional dimensions of this process are equally important and often more challenging to navigate.

Grief complicates decision-making in profound ways. When you inherit a house from a parent, spouse, or other loved one, you’re simultaneously processing loss while making significant financial decisions. This combination can feel overwhelming, and many people struggle with guilt about “profiting” from a loved one’s death or “abandoning” a family home.

Recognizing these feelings as normal and valid is the first step toward managing them productively. Give yourself permission to feel whatever emotions arise—sadness, guilt, relief, anxiety, or even joy at receiving a meaningful inheritance. These feelings aren’t mutually exclusive and don’t make you a bad person.

Sentimental attachment to the family home can cloud objective assessment of whether keeping or selling makes financial sense. The house where you grew up, where holidays were celebrated, or where a loved one spent their final years holds memories that transcend its monetary value. However, maintaining a property you can’t afford, don’t need, or that creates family conflict isn’t a healthy way to honor those memories.

Consider alternative ways to preserve meaningful memories without keeping the entire property. Take photographs of each room, preserve special architectural elements or fixtures, create a memory book with photos and stories, or keep a few meaningful items while selling the rest. These approaches honor your loved one’s memory while still making sound financial decisions about the property itself.

Family pressure and expectations add another emotional layer. Siblings may have strong opinions about whether to sell, when to list, and what price to accept. Extended family members might expect to receive specific items from the estate. Cultural or religious traditions may influence how the property should be handled.

Setting clear boundaries while remaining compassionate helps manage these pressures. You can acknowledge others’ feelings and preferences while still making decisions that serve your best interests and align with legal requirements. Remember that as the legal heir or executor, you have both the authority and responsibility to make these decisions, even when they disappoint others.

Decision paralysis commonly affects people dealing with inherited property. Faced with overwhelming choices and competing priorities, many people simply freeze, avoiding decisions and allowing the property to sit vacant for months or years. This paralysis often stems from fear of making the “wrong” choice or inability to process grief while simultaneously handling practical matters.

Breaking the process into smaller, manageable steps helps overcome paralysis. You don’t need to decide everything at once. Start with just the next step—perhaps scheduling a property inspection, consulting with one attorney, or simply visiting the property to assess its condition. Each small action builds momentum and clarity.

Professional counseling or grief support can be invaluable during this process. A therapist who specializes in grief and loss can help you process emotions, make decisions aligned with your values, and navigate family dynamics more effectively. Many people resist this support, viewing it as unnecessary or self-indulgent, but the emotional clarity it provides often leads to better decisions and reduced regret.

Time pressure versus emotional readiness creates tension for many people selling inherited property. Financial pressures, probate timelines, or co-heir impatience may push you to sell before you feel emotionally ready. Conversely, emotional attachment might cause you to delay selling long past the point where it makes financial sense.

Finding balance requires honest self-assessment. Ask yourself whether waiting will genuinely help you process grief and gain clarity, or whether it’s simply avoidance that will feel just as difficult six months from now. Sometimes the healthiest choice is to move forward with the sale even while still grieving, recognizing that closure on the property can actually facilitate emotional healing.

Creating meaningful closure rituals helps many people transition from ownership to sale. Consider hosting a final gathering at the property where family members share memories, take photos, and say goodbye. Some people find it meaningful to write a letter to the house, thanking it for the memories and releasing it to new owners. These rituals might seem silly, but they provide psychological closure that makes the sale feel less like abandonment and more like a conscious, respectful transition.

Remember that selling a loved one’s home doesn’t erase your memories or diminish your relationship with the person who left it to you. The property is just a physical structure; the love, lessons, and experiences you shared with your loved one remain with you regardless of who owns the building. Making sound financial decisions about inherited property while honoring your emotional needs and memories represents the healthiest path forward.

Common Mistakes to Avoid When Selling Inherited Property

Learning from others’ mistakes helps you navigate the process of selling an inherited house more smoothly and avoid costly errors that could reduce your proceeds or create legal problems.

Mistake #1: Failing to secure the property immediately. Vacant inherited homes are targets for theft, vandalism, and squatters. Failing to change locks, maintain insurance, and regularly check on the property can result in thousands of dollars in damage and potential liability if someone is injured on the premises.

Mistake #2: Making major financial decisions while grieving. The period immediately after losing a loved one is not the optimal time for complex financial decisions. While you may need to take some immediate actions to secure the property, major decisions about whether to sell, extensive renovations, or accepting offers should ideally wait until you’ve had time to process your grief and think clearly.

Mistake #3: Assuming you can’t sell until probate closes. While some estates do require completed probate before sale, others allow executors to sell property during probate with court approval. This “probate sale” can significantly accelerate your timeline and reduce carrying costs. Consult with a probate attorney about your specific situation rather than assuming you must wait.

Mistake #4: Overimproving the property. Many heirs invest heavily in renovations, assuming they’ll recoup these costs in the sale price. However, major renovations rarely return 100% of their cost, and inherited property buyers often prefer lower prices over updated features. Focus on essential repairs and cosmetic improvements rather than expensive remodels.

Mistake #5: Pricing based on sentimental value rather than market reality. Your childhood home may be priceless to you, but buyers evaluate it based on comparable sales, condition, and market conditions. Overpricing based on emotional attachment results in extended market time, eventual price reductions, and often lower final sale prices than if you’d priced correctly from the start.

Mistake #6: Neglecting tax planning. Failing to obtain a proper time of death appraisal, not consulting with a tax professional before selling, or making decisions without understanding tax implications can cost you thousands in unnecessary taxes. The stepped-up basis and other tax advantages of inherited property only benefit you if you understand and properly document them.

Mistake #7: Poor communication among heirs. When multiple people inherit property, assuming everyone agrees or avoiding difficult conversations leads to conflict, delays, and sometimes litigation. Establish clear communication from the outset, put agreements in writing, and address disagreements promptly before they escalate.

Mistake #8: Hiring the wrong professionals. Choosing a real estate agent based solely on commission rate, selecting an attorney without estate experience, or skipping professional help entirely to save money often backfires. The expertise of qualified professionals typically more than pays for itself through higher sale prices, avoided legal problems, and reduced tax liability.

Mistake #9: Ignoring liens and title issues. Hoping that property liens, judgments, or title defects will somehow resolve themselves or won’t be discovered leads to last-minute crises that can derail sales or force you to accept lower prices. Address these issues proactively with help from professionals experienced in resolving complex title problems.

Mistake #10: Letting the property sit vacant for extended periods. Every month you hold inherited property, you’re paying property taxes, insurance, utilities, and maintenance costs while the property potentially deteriorates. Unless you have a clear strategy for why you’re waiting (market improvement, completing probate, saving for repairs), extended vacancy drains inheritance value.

Mistake #11: Failing to maintain the property during the selling process. Even if you plan to sell quickly, neglecting basic maintenance like lawn care, HVAC service, or minor repairs can significantly reduce buyer interest and sale prices. Properties that appear abandoned or neglected signal problems to buyers and justify lower offers.

Mistake #12: Making emotional decisions about buyers. Some sellers reject higher offers from investors or developers in favor of lower offers from families, hoping to see the property go to people who will love it as they did. While this sentiment is understandable, it can cost you tens of thousands of dollars. Remember that once you sell, you have no control over what future owners do with the property anyway.

Mistake #13: Not considering all selling options. Many people assume traditional listing is the only way to sell, never exploring alternatives like cash buyers, auctions, or seller financing that might better serve their specific situation. Evaluate multiple options before committing to a single approach.

Mistake #14: Underestimating closing costs and taxes. Sellers are often surprised by the amount deducted from sale proceeds for commissions, closing costs, prorated taxes, and capital gains taxes. Understanding these costs upfront helps you set realistic expectations and make informed decisions about offers.

Avoiding these common mistakes requires education, professional guidance, and honest self-assessment of your situation, capabilities, and goals. The time and money invested in doing things correctly from the start almost always proves less expensive than fixing problems that arise from shortcuts and assumptions.

Conclusion: Moving Forward with Confidence

Selling inherited property represents one of life’s most complex financial and emotional challenges, combining grief, family dynamics, legal requirements, tax implications, and real estate transactions into a single process. However, with the right knowledge, professional support, and systematic approach, you can navigate this journey successfully while honoring your loved one’s legacy and securing your financial future.

The key principles to remember include understanding that probate requirements vary significantly by state and estate complexity, leveraging the stepped-up basis tax advantage to minimize capital gains, communicating clearly with co-heirs to prevent conflicts, evaluating all selling options rather than assuming traditional listing is always best, and seeking professional guidance from attorneys, tax experts, and experienced real estate professionals.

Your next steps should include securing the inherited property immediately if you haven’t already, determining whether probate is required and initiating that process if necessary, obtaining a professional appraisal to establish fair market value at the time of death, consulting with a tax professional to understand your specific tax situation, and deciding whether to pursue traditional listing, cash sale, or alternative selling methods based on your timeline, property condition, and financial goals.

Remember that there’s no universal “right” answer to whether you should sell inherited property immediately or hold it, make improvements or sell as-is, list traditionally or accept a cash offer. The best decision depends on your unique circumstances, including your financial situation, emotional readiness, property condition, market conditions, and relationship with co-heirs.

Don’t navigate this journey alone. The complexity of selling an inherited house and the emotional weight of the process make professional guidance not just helpful but essential. Whether you work with Sure Path Property Solutions for a quick, simple cash sale or assemble a team of attorneys, agents, and tax professionals for a traditional sale, expert service and helpful guidance transform an overwhelming process into a manageable one.

Most importantly, give yourself grace throughout this process. You’re handling a significant life transition while grieving a loss, and it’s normal to feel overwhelmed, uncertain, or emotional. Making informed decisions with professional support, communicating honestly with family members, and taking care of your emotional needs alongside the practical aspects of the sale will help you emerge from this experience with both your financial interests protected and your family relationships intact.

The inherited property you’re selling represents more than just a real estate transaction—it’s a final gift from someone who cared about you, intended to provide financial security and opportunity. Handling this gift responsibly by making informed decisions, avoiding common mistakes, and seeking trustworthy service when you need it honors both the giver and the inheritance itself.

Key Points to Remember

- Probate requirements vary significantly by state and estate complexity; some inherited properties can be sold without completing probate while others require full court supervision throughout the process

- Stepped-up basis provides substantial tax advantages by resetting your cost basis to fair market value at the time of death, potentially eliminating or dramatically reducing capital gains tax liability

- Multiple heirs must coordinate and agree on sale decisions; written agreements, clear communication, and sometimes professional mediation prevent conflicts that can delay or derail sales

- Property condition directly impacts both sale price and optimal selling method; properties in good condition typically benefit from traditional listings while those needing substantial repairs often sell better to cash buyers

- Tax implications extend beyond capital gains to potentially include inheritance taxes (in some states), estate taxes (for large estates), and ongoing property taxes that accumulate during the selling process

- Professional guidance from attorneys, tax experts, and real estate professionals isn’t an optional luxury but an essential investment that typically more than pays for itself through higher proceeds and avoided mistakes

- Emotional readiness matters as much as financial considerations; rushing major decisions while grieving or delaying indefinitely due to attachment both create problems

- Liens, judgments, and title issues are common on inherited property but can be resolved with proper professional help; these complications don’t necessarily prevent sale but must be addressed

- Alternative selling options beyond traditional listing including cash buyers, auctions, and seller financing may better serve your specific timeline, property condition, and financial goals

- Time costs money when holding inherited property; every month of vacancy means ongoing expenses for taxes, insurance, maintenance, and utilities that reduce your net inheritance

- Clear documentation of property value at time of death through professional appraisal is essential for establishing your stepped-up basis and minimizing future tax liability

- Communication and written agreements among heirs prevent misunderstandings and conflicts that can damage both family relationships and financial outcomes

References

[1] Internal Revenue Service. (2025). “Publication 551: Basis of Assets.” IRS.gov.

[2] American Bar Association. (2025). “Guide to Wills and Estates.” ABA Real Property, Trust and Estate Law Section.

[3] National Association of Realtors. (2025). “Profile of Home Buyers and Sellers.” NAR Research Division.

[4] Internal Revenue Service. (2025). “Estate and Gift Taxes.” IRS.gov.

[5] Uniform Law Commission. (2025). “Uniform Probate Code.” ULC.org.

[6] Congressional Research Service. (2024). “Federal Estate, Gift, and Generation-Skipping Taxes: A Description of Current Law.”

[7] National Association of Estate Planners & Councils. (2025). “Estate Planning Statistics and Trends.”

[8] American College of Trust and Estate Counsel. (2025). “State Death Tax Chart.” ACTEC.org.