Multiple Heirs One Property: How to Navigate Shared Inheritance

Inheriting property should feel like a blessing, not a burden. Yet when multiple siblings, cousins, or family members suddenly share ownership of a single house or piece of land, what begins as a gift can quickly become a source of stress, confusion, and conflict. Multiple Heirs One Property: How to Navigate Shared Inheritance situations affect thousands of families across America every year, creating complex legal and emotional challenges that require careful navigation.

The reality is stark: 67% of inherited properties with multiple heirs experience some form of family disagreement within the first year. One sibling wants to sell immediately. Another hopes to keep the family home. A third needs cash but can’t afford a buyout. Meanwhile, property taxes keep accumulating, maintenance issues arise, and nobody knows who’s responsible for what.

This comprehensive guide provides helpful solutions for families facing shared inheritance challenges. Whether you’re dealing with a childhood home, rental property, or vacant land, understanding your options and legal rights is the first step toward resolution.

Key Takeaways

- Shared ownership creates equal rights and responsibilities among all heirs, requiring unanimous agreement for major property decisions

- Four primary resolution paths exist: buyout agreements, selling together, creating rental arrangements, or pursuing partition actions

- Communication and documentation are essential to prevent conflicts and protect everyone’s interests

- Professional guidance from industry experts can save families thousands in legal fees and preserve relationships

- Acting quickly on property taxes and maintenance prevents additional complications and financial penalties

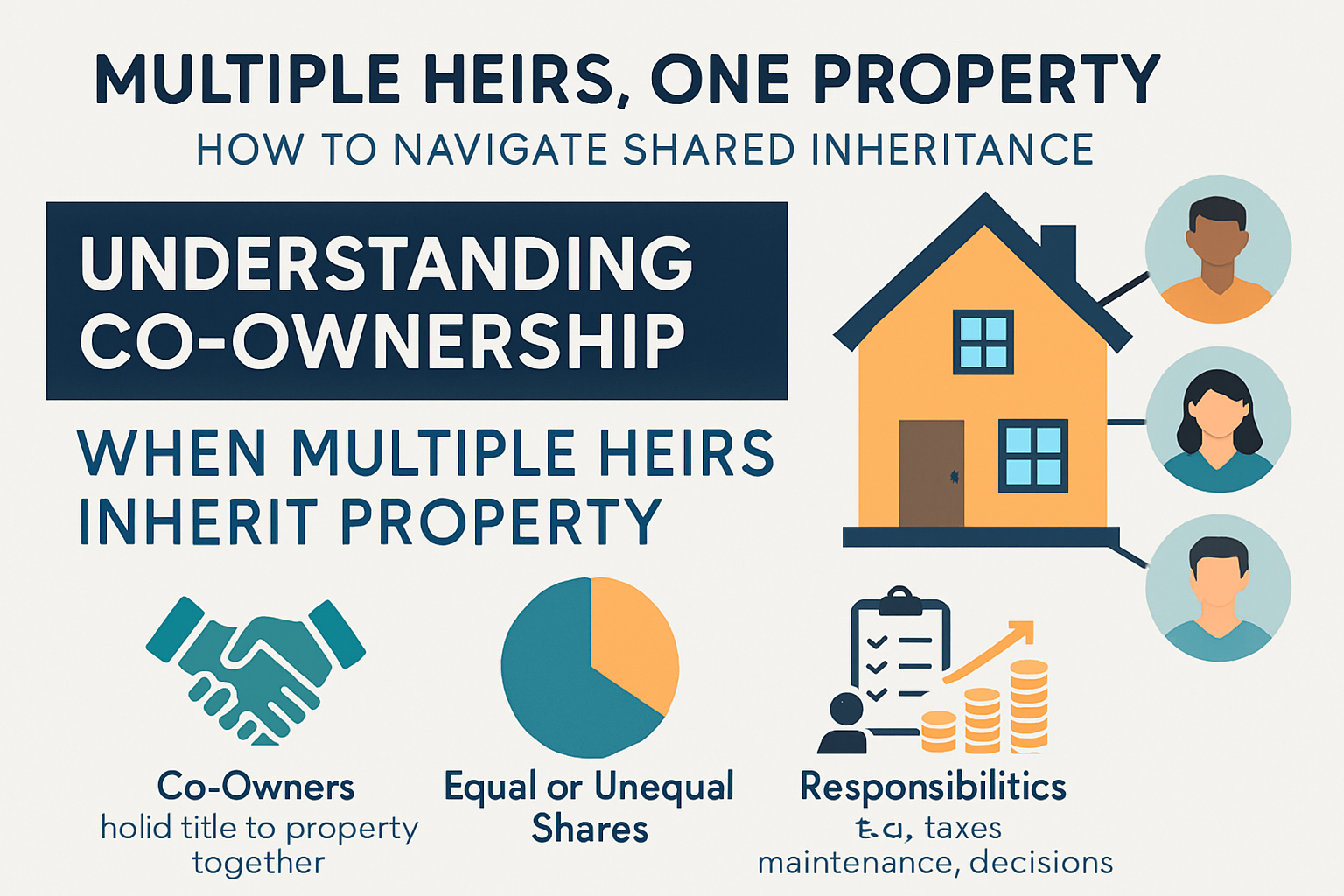

Understanding Co-Ownership When Multiple Heirs Inherit Property

When someone passes away and leaves property to multiple heirs, the legal landscape becomes immediately complex. Each heir doesn’t own a specific portion of the house—like one person owning the kitchen and another the bedroom. Instead, everyone owns an undivided interest in the entire property.

Types of Co-Ownership Structures

The way heirs hold title matters significantly. Most inherited properties fall into one of these categories:

Tenancy in Common is the most frequent structure for inherited property. Each heir owns a percentage share (often equal, but not always). These shares can be sold, transferred, or willed to others independently. If one heir passes away, their share goes to their own heirs—not to the other co-owners.

Joint Tenancy with Right of Survivorship includes a critical feature: when one owner dies, their share automatically transfers to the surviving owners. This structure is less common in inheritance situations but may exist if the property was previously owned jointly.

Tenants by the Entirety applies only to married couples in certain states and rarely affects standard inheritance scenarios.

Rights and Responsibilities of Each Heir

Every co-owner possesses specific legal rights, regardless of their ownership percentage:

✅ Right to occupy the entire property (not just their “share”)

✅ Right to receive their proportionate share of rental income

✅ Right to sell or transfer their ownership interest

✅ Right to force a sale through legal partition action

✅ Responsibility to contribute to property taxes, insurance, and maintenance

These rights create natural tension. One heir living in the property rent-free while others pay taxes from afar breeds resentment. One heir making improvements without consent may not recover those costs.

Common Scenarios That Create Complications

Real-world inheritance situations rarely follow simple patterns. Consider these frequent complications:

Unequal Financial Situations: One sibling can afford to maintain the property; others cannot contribute to ongoing costs.

Geographic Distance: Heirs scattered across different states struggle to coordinate property management and decision-making.

Emotional Attachments: The family homestead holds deep sentimental value for some heirs but represents only financial value to others.

Occupancy Disputes: One heir already lives in the property or moves in immediately after inheritance, creating imbalance.

Deferred Maintenance: The inherited property needs significant repairs, but heirs disagree on whether to invest or sell as-is.

Understanding how jointly owned property works provides essential context for navigating these challenges with helpful guidance.

The Legal Framework for Multiple Heirs One Property Situations

Navigating shared inheritance requires understanding the legal mechanisms that govern co-ownership. State laws vary, but certain principles apply broadly across the United States.

Probate and Title Transfer Process

Before heirs can make any decisions about inherited property, the estate must typically pass through probate—the legal process of transferring ownership from the deceased to beneficiaries.

The probate timeline generally spans 6-18 months, depending on estate complexity and state requirements. During this period:

- The court validates the will (or applies intestate succession laws if no will exists)

- An executor or administrator manages the estate

- Debts and taxes are paid from estate assets

- Remaining property transfers to designated heirs

Once probate concludes, a new deed records the heirs as co-owners. This document establishes each person’s ownership percentage and the type of co-ownership.

Important note: Some properties transfer outside probate through mechanisms like living trusts, transfer-on-death deeds, or joint tenancy arrangements. These situations may simplify the process but still result in multiple owners.

Decision-Making Requirements

Here’s where shared inheritance becomes challenging: major property decisions require unanimous consent from all co-owners.

Selling the property, refinancing, or making substantial alterations all need agreement from every heir. One dissenting voice can halt the entire process.

Minor decisions—routine maintenance, paying utilities, basic repairs—fall into a gray area. While individual heirs can technically authorize these actions, disputes often arise over what constitutes “necessary” versus “optional” expenses.

This unanimous consent requirement explains why communication breaks down quickly. Without clear processes for decision-making, families find themselves stuck in limbo.

State-Specific Inheritance Laws

Each state maintains unique laws governing inherited property, particularly regarding:

Homestead Rights: Some states protect a surviving spouse’s right to remain in the family home, even if children are also heirs.

Intestate Succession: When someone dies without a will, state law determines how property divides among heirs. These formulas vary significantly.

Dower and Curtesy Rights: A few states still recognize these traditional spousal inheritance protections.

Community Property States: Arizona, California, Idaho, Louisiana, Nevada, New Mexico, Texas, Washington, and Wisconsin follow community property rules that affect how marital property passes to heirs.

Understanding your state’s specific requirements is crucial. What works in Florida may not apply in Ohio. Consulting with local industry experts familiar with your jurisdiction prevents costly mistakes.

Issues with unclear title or clouded ownership can further complicate the legal framework, requiring additional steps to establish clear ownership.

Challenges Families Face with Shared Property Inheritance

The intersection of money, property, and family relationships creates a perfect storm for conflict. Understanding common challenges helps families prepare and respond effectively.

Emotional and Relationship Dynamics

Grief complicates every decision. Families navigating shared inheritance are simultaneously processing loss while making significant financial choices.

Sentimental value often clashes with practical reality. The dining table where three generations gathered for holidays means everything to one sibling but represents outdated furniture to another. These emotional attachments can’t be quantified on a balance sheet, yet they profoundly influence decision-making.

Old family dynamics resurface with surprising intensity. The sibling rivalry from childhood, the parent’s perceived favoritism, the unresolved conflicts—all emerge during inheritance discussions. One heir may feel entitled to more because they provided caregiving. Another believes their financial success means they should lead decisions.

Communication breakdowns accelerate when families avoid difficult conversations. Assumptions replace dialogue. Resentments build silently until they explode into open conflict.

Financial Pressures and Obligations

Money matters create immediate, tangible stress for co-owners.

| Ongoing Expense | Annual Cost Range | Who Pays? |

|---|---|---|

| Property Taxes | $1,200 – $15,000+ | All heirs proportionally |

| Homeowners Insurance | $800 – $3,500 | All heirs proportionally |

| Utilities (if vacant) | $600 – $2,400 | Often one heir fronts costs |

| Maintenance & Repairs | $1,000 – $10,000+ | Disputed among heirs |

| HOA Fees (if applicable) | $500 – $6,000 | All heirs proportionally |

These costs don’t pause while heirs decide what to do. Property taxes accrue. Insurance lapses create liability. Deferred maintenance leads to deterioration.

The challenge intensifies when heirs have vastly different financial capacities. One sibling earning $200,000 annually views a $5,000 tax bill differently than another struggling on a fixed income.

Carrying costs for an inherited property can easily exceed $10,000-$20,000 annually. For a property that might sell for $200,000, these expenses represent 5-10% of the total value each year. Delay becomes expensive.

Some families discover the inherited property has existing liens or judgments that must be resolved before any sale can proceed, adding another layer of financial complexity.

Disagreements About Property Use

What should happen with the inherited property? This question sparks the most heated debates.

Common positions include:

🏠 Keep it as a family gathering place – One or more heirs want to preserve the property for reunions, vacations, or sentimental purposes

💰 Sell immediately and split proceeds – Heirs need liquidity and want to convert the asset to cash

🏘️ Convert to rental income – Some heirs see investment potential and want to generate ongoing revenue

🏡 One heir buys out others – A single family member wants to keep the property but needs others to sell their shares

Each position makes sense from different perspectives. The heir who lives nearby and can manage a rental sees opportunity. The heir across the country dealing with their own mortgage sees burden. The heir with young children envisions summer vacations at grandma’s lake house. The heir facing medical bills needs cash now.

Without compromise, these disagreements lead to stalemate. The property sits vacant, deteriorating and accumulating costs while family relationships fracture.

Maintenance and Management Responsibilities

Who mows the lawn? Who pays when the roof leaks? Who handles tenant complaints if the property is rented?

Shared responsibility often means no responsibility. Everyone assumes someone else will handle it. Meanwhile, the property suffers.

Distance creates practical challenges. An heir living 1,000 miles away can’t easily inspect the property, meet with contractors, or respond to emergencies. This burden typically falls on the geographically closest heir—who may resent doing all the work while others share equally in any eventual proceeds.

Decision authority becomes murky. If the water heater fails, can one heir authorize a $1,200 replacement without consulting others? What if one heir wants to invest $15,000 in updates to increase sale value, but others disagree?

These day-to-day management questions create constant friction and require clear agreements from the outset.

Practical Solutions for Multiple Heirs One Property Scenarios

Fortunately, families have several viable paths forward. The key is understanding options, communicating openly, and selecting the approach that best serves everyone’s interests.

Option 1: One Heir Buys Out the Others

A buyout arrangement allows one heir (or multiple heirs together) to purchase the ownership shares of other co-owners. This solution works well when:

- One heir has emotional attachment and financial capacity

- Other heirs prefer cash over continued ownership

- The property’s value is clearly established

- Financing is available or the buying heir has sufficient liquid assets

The buyout process typically follows these steps:

- Obtain a professional appraisal to establish fair market value

- Calculate each heir’s share based on ownership percentages

- Determine buyout price (often the appraised value minus estimated selling costs)

- Arrange financing through conventional mortgage, home equity loan, or private financing

- Execute the transaction with proper legal documentation transferring ownership

Advantages of buyouts:

✅ Preserves the property within the family

✅ Provides immediate cash to heirs who want to sell

✅ Avoids real estate commissions and closing costs

✅ Resolves disputes quickly with willing participants

✅ Allows the purchasing heir complete control

Challenges to consider:

⚠️ Requires significant capital or financing approval

⚠️ Determining “fair” value can spark disagreement

⚠️ May create tax implications for both buyer and sellers

⚠️ Can breed resentment if one heir feels pressured to sell

Pro tip: Consider seller financing, where the buying heir pays other heirs over time with interest. This arrangement can benefit both parties—the buyer avoids bank qualification requirements, while sellers receive interest income above typical savings rates.

Option 2: Sell the Property and Split Proceeds

Selling the inherited property and dividing the proceeds equally often represents the cleanest resolution, especially when:

- Heirs cannot agree on other arrangements

- No single heir has the financial capacity for a buyout

- The property requires substantial repairs or updates

- Ongoing carrying costs create financial strain

- Heirs live far away and cannot manage the property

The collaborative sale process:

- Reach unanimous agreement to sell (required for traditional sale)

- Prepare the property by addressing necessary repairs and cleaning

- Select a real estate agent together or obtain multiple opinions

- Set a realistic listing price based on market analysis

- Review and accept offers with all heirs participating in decisions

- Navigate closing and distribute proceeds according to ownership shares

Important considerations for selling inherited property:

💡 Capital gains taxes: Heirs typically receive a “stepped-up basis” equal to the property’s value at the date of death. This means selling shortly after inheritance usually generates minimal capital gains tax. Waiting years before selling may create significant tax liability on appreciation.

💡 Selling costs: Factor in real estate commissions (typically 5-6%), closing costs, title insurance, and any repairs or updates. These expenses reduce net proceeds by 8-12% on average.

💡 Timing pressures: Markets fluctuate. Selling during a down market may cost heirs tens of thousands compared to waiting for better conditions—but waiting extends the period of shared ownership and ongoing costs.

💡 Property condition: Inherited properties often need updates. Heirs must decide whether to invest in improvements or sell as-is at a lower price. This decision requires unanimous agreement and shared financial contribution.

For properties with complications like tax liens or other title issues, working with experienced professionals who understand complex situations can streamline the selling process significantly.

Alternative selling approaches:

When traditional listing seems too complicated or time-consuming, heirs might consider:

- Direct sale to investors who buy properties as-is, eliminating repair costs and lengthy marketing periods

- Auction for unique properties or when heirs want certainty of sale date

- Lease-option arrangements that generate income while finding a buyer

Option 3: Create a Co-Ownership Agreement for Rental Income

Some families choose to keep inherited property as a shared investment, generating rental income that benefits all heirs. This approach works when:

- The property is in a strong rental market

- At least one heir can manage day-to-day operations

- All heirs agree on investment strategy

- The property is in good condition or heirs can fund necessary improvements

- Family relationships are strong enough to sustain ongoing partnership

Essential elements of a co-ownership rental agreement:

📋 Management structure: Designate one heir as property manager (with compensation) or hire professional management. Clearly define decision-making authority for various scenarios.

📋 Income distribution: Specify how rental income distributes among heirs (typically proportional to ownership shares) and the frequency of distributions.

📋 Expense allocation: Detail how costs are shared, including routine maintenance, major repairs, property taxes, insurance, and management fees.

📋 Capital improvements: Establish a process for approving and funding significant upgrades or repairs, including what happens if some heirs cannot or will not contribute.

📋 Exit strategy: Define how heirs can sell their shares, whether to other co-owners or outside parties, and the process for eventually selling the entire property.

📋 Dispute resolution: Include mediation or arbitration clauses to handle disagreements without litigation.

Financial projections for rental scenarios:

Before committing to rental arrangements, heirs should create realistic financial projections:

| Item | Monthly Amount | Annual Amount |

|---|---|---|

| Rental Income | $1,800 | $21,600 |

| Property Taxes | -$350 | -$4,200 |

| Insurance | -$150 | -$1,800 |

| Maintenance (10% of rent) | -$180 | -$2,160 |

| Property Management (8%) | -$144 | -$1,728 |

| Vacancy Reserve (5%) | -$90 | -$1,080 |

| Net Operating Income | $886 | $10,632 |

For three heirs sharing equally, this scenario generates approximately $3,544 annually per heir—before accounting for major repairs or capital improvements.

Realistic expectations: Rental property ownership involves ongoing responsibilities, tenant issues, maintenance emergencies, and market fluctuations. The fantasy of passive income rarely matches reality, especially with multiple decision-makers.

Option 4: Partition Action (Legal Property Division)

When heirs cannot reach agreement through negotiation, partition action provides a legal remedy. This court process forces the sale or physical division of property.

Two types of partition exist:

Partition in Kind: The court physically divides the property into separate parcels, with each heir receiving a distinct portion. This option rarely works for residential properties but may apply to large land tracts that can be subdivided.

Partition by Sale: The court orders the property sold, with proceeds divided among heirs according to ownership shares. This is the most common outcome for houses and small properties.

The partition action process:

- One or more heirs file a partition lawsuit in the county where the property is located

- The court notifies all co-owners of the action

- Heirs may present arguments for or against partition

- The court appoints a referee or commissioner to oversee the sale

- The property is marketed and sold (often at auction or through a court-supervised process)

- Proceeds are distributed to heirs after deducting legal fees, court costs, and sale expenses

Costs and timeline:

⏱️ Duration: 6-18 months from filing to final distribution

💰 Legal fees: $5,000-$25,000+ depending on complexity and whether heirs contest

💰 Court costs: $1,000-$5,000 for filing fees, referee fees, and administrative expenses

💰 Sale discounts: Court-ordered sales often achieve 10-20% below market value

When partition makes sense:

- Communication has completely broken down among heirs

- One or more heirs refuse to cooperate with buyout or sale

- Heirs are deadlocked with no path to compromise

- The property is deteriorating due to neglect and inaction

Drawbacks of partition:

❌ Expensive legal process reduces everyone’s net proceeds

❌ Court-supervised sales typically achieve lower prices

❌ Permanently damages family relationships

❌ Removes control from heirs over timing and terms

❌ Creates public record of family dispute

Partition should be the last resort after exhausting other options. The financial and emotional costs make it an expensive way to resolve disagreement. However, it provides certainty when cooperation proves impossible.

Understanding partition action in detail helps heirs make informed decisions about whether this path serves their interests.

Step-by-Step Guide to Resolving Multiple Heirs One Property Challenges

Successfully navigating shared inheritance requires a structured approach. Following these steps increases the likelihood of reaching resolution while preserving family relationships.

Step 1: Open Communication Among All Heirs

Begin with honest, respectful dialogue. Schedule a family meeting—in person if possible, or via video conference for geographically dispersed heirs.

Meeting agenda should include:

- Each heir’s preferences and concerns

- Financial capacity of each heir to contribute to ongoing costs

- Timeline considerations (who needs resolution quickly versus who can wait)

- Emotional attachments and sentimental concerns

- Practical constraints (distance, time availability, expertise)

Ground rules for productive discussion:

🗣️ Everyone gets heard without interruption or judgment

🗣️ Focus on interests, not positions (understand the “why” behind each preference)

🗣️ Acknowledge emotions as valid while seeking practical solutions

🗣️ Avoid blame for past decisions or family dynamics

🗣️ Document agreements in writing, even preliminary ones

Consider using a neutral facilitator—a family friend, mediator, or counselor—if tensions run high. The cost of professional mediation ($200-$400 per session) is minimal compared to litigation expenses.

Step 2: Assess the Property’s Condition and Value

Informed decisions require accurate information. Obtain a professional appraisal to establish fair market value and conduct a thorough property inspection.

Key evaluation factors:

🏠 Current market value via professional appraisal

🏠 Needed repairs with cost estimates from licensed contractors

🏠 Deferred maintenance that affects value or safety

🏠 Outstanding debts including mortgages, liens, or judgments

🏠 Tax obligations including property taxes and potential capital gains

🏠 Rental potential if considering income-generation strategy

Investment analysis:

If heirs are considering keeping the property, create a detailed financial analysis:

- Estimated rental income (research comparable properties)

- All carrying costs (taxes, insurance, maintenance, management)

- Required capital improvements to make property rentable

- Expected return on investment compared to alternative investments

- Risk factors and worst-case scenarios

This objective assessment helps heirs move beyond emotional reactions to data-driven decisions.

Step 3: Explore All Available Options Together

Present each resolution option with its advantages, disadvantages, costs, and timeline. Use the framework outlined earlier in this guide.

Create a comparison matrix:

| Option | Timeline | Upfront Cost | Pros | Cons | Best For |

|---|---|---|---|---|---|

| Buyout | 1-3 months | Appraisal fee | Quick resolution, keeps in family | Requires financing | One heir wants to keep property |

| Sell Together | 3-6 months | Repairs, commissions | Clean break, equal proceeds | Market dependent | Heirs want liquidity |

| Rental Agreement | 1-2 months setup | Repairs, legal fees | Ongoing income | Management burden | Strong rental market |

| Partition Action | 6-18 months | $10,000-$30,000+ | Forces resolution | Expensive, adversarial | Complete deadlock |

Voting or consensus process:

Determine how the family will make the final decision. Options include:

- Unanimous consent: Everyone must agree (required for sale, but can be applied to other decisions)

- Majority vote: Weighted by ownership percentage

- Facilitator recommendation: A neutral third party suggests the best path after hearing all perspectives

Document the decision-making process to avoid later disputes about whether proper procedures were followed.

Step 4: Formalize Agreements in Writing

Verbal agreements among family members often lead to misunderstandings and conflict. Every agreement should be documented in writing, regardless of how trustworthy everyone seems.

Essential documentation includes:

📄 Co-ownership agreement detailing rights, responsibilities, and decision-making processes

📄 Buyout agreement specifying price, payment terms, and transfer timeline

📄 Property management agreement if pursuing rental strategy

📄 Sale agreement with all heirs’ signatures authorizing listing and accepting offers

Legal review is essential. Have an attorney experienced in real estate and estate matters review all documents before signing. The cost ($500-$2,000 typically) is minimal insurance against future disputes.

Key provisions to include:

- Specific timelines and deadlines

- Financial obligations of each party

- Consequences for non-compliance

- Dispute resolution procedures

- Conditions that would trigger renegotiation

Step 5: Execute the Chosen Solution

Once agreement is reached and documented, move forward decisively. Delays create opportunities for second-guessing and changing circumstances.

For buyouts:

- Secure financing approval

- Order title work and title insurance

- Schedule closing with all parties present or represented

- Execute deed transfer and record with county

- Distribute funds to selling heirs

For sales:

- Interview and select real estate agent together

- Prepare property for market (repairs, cleaning, staging)

- Review and approve listing agreement

- Establish communication protocol for offers and negotiations

- Coordinate closing and fund distribution

For rental arrangements:

- Make necessary property improvements

- Establish LLC or other business entity (recommended)

- Set up business bank account for rental income and expenses

- Hire property manager or designate managing heir

- Market property and screen tenants

- Implement systems for income distribution and expense tracking

For partition actions:

- Hire experienced partition attorney

- File petition with appropriate court

- Participate in court proceedings as required

- Cooperate with court-appointed referee

- Attend sale and closing processes

Step 6: Address Tax Implications

Inherited property creates various tax considerations that heirs must understand and plan for.

Stepped-up basis: When someone inherits property, the tax basis “steps up” to the fair market value on the date of death. This eliminates capital gains tax on appreciation that occurred during the deceased’s ownership.

Example: Mom bought a house in 1985 for $50,000. It’s worth $300,000 when she passes in 2025. Heirs receive a stepped-up basis of $300,000. If they sell for $305,000, they owe capital gains tax only on the $5,000 gain, not the $250,000 appreciation during Mom’s ownership.

Capital gains considerations:

- Selling within a year of inheritance typically generates minimal capital gains

- Holding property for years before selling creates potential tax liability on post-inheritance appreciation

- Improvements and selling costs increase basis, reducing taxable gains

- Each heir reports their proportionate share of gains on individual tax returns

Estate tax: Most estates don’t owe federal estate tax (2025 exemption is $13.61 million per person). However, some states impose estate or inheritance taxes at lower thresholds.

Property tax reassessment: Some states reassess property value upon transfer, potentially increasing annual property taxes.

Consult a tax professional: The complexity of inheritance taxation makes professional guidance valuable. A CPA or tax attorney can help heirs minimize tax liability and avoid costly mistakes.

Working with Professionals: When and Why to Seek Expert Help

Navigating Multiple Heirs One Property situations often exceeds most families’ expertise. Knowing when to engage professionals can save money, time, and relationships.

Real Estate Attorneys

When you need legal counsel:

- Drafting or reviewing co-ownership agreements

- Navigating complex title issues or liens

- Pursuing partition action

- Resolving disputes among heirs

- Understanding state-specific inheritance laws

- Executing buyout transactions

What to expect: Real estate attorneys typically charge $200-$500 per hour or offer flat fees for specific services like document review ($500-$1,500) or partition representation ($5,000-$25,000+).

How to find qualified counsel: Seek attorneys specializing in real estate and estate law. Ask for referrals from the estate’s probate attorney or check your state bar association’s referral service.

Estate Planners and Probate Attorneys

If the inherited property is still in probate or estate administration, the executor’s attorney can provide helpful guidance on the transfer process and heir rights.

Services provided:

- Clarifying ownership structure and percentages

- Explaining probate timeline and requirements

- Addressing estate debts that affect the property

- Coordinating with title companies for ownership transfer

Real Estate Agents and Appraisers

Professional appraisers provide unbiased property valuations essential for buyouts, estate tax returns, and informed decision-making. Cost: $300-$600 for residential properties.

Real estate agents bring market expertise, marketing resources, and negotiation skills when heirs decide to sell. Choose agents experienced with inherited property and estate sales who understand the unique dynamics of multiple decision-makers.

Interview multiple agents and ask:

- Experience with inherited property and multiple heirs

- Marketing strategy for this specific property

- Comparable sales analysis and pricing recommendation

- Commission structure and services included

- Communication protocols with multiple heirs

Tax Professionals

CPAs and tax attorneys help heirs understand and minimize tax implications of inheritance decisions.

Services include:

- Calculating stepped-up basis

- Projecting capital gains tax scenarios

- Advising on timing of sale to optimize tax outcomes

- Preparing tax returns reporting sale proceeds

- Structuring transactions to minimize tax liability

Cost: $200-$400 per hour for consultation, or project-based fees for comprehensive tax planning.

Property Management Companies

If heirs choose rental income strategy, professional property management removes much of the operational burden.

Services provided:

- Tenant screening and placement

- Rent collection and distribution

- Maintenance coordination and emergency response

- Financial reporting and tax documentation

- Lease enforcement and eviction if necessary

Cost: Typically 8-12% of monthly rental income, plus leasing fees (often one month’s rent for new tenant placement).

Mediators and Family Counselors

When communication breaks down but heirs want to avoid litigation, professional mediators facilitate productive dialogue.

Mediation process:

- Neutral third party guides structured discussions

- Each heir presents their perspective and interests

- Mediator helps identify common ground and creative solutions

- Agreements are documented for legal review

Cost: $200-$400 per hour, with most inheritance mediations requiring 4-8 hours total.

Success rate: Mediation resolves 70-80% of disputes without litigation, at a fraction of the cost.

Specialized Property Solution Companies

Companies like Sure Path Property Solutions specialize in complex property situations, including multiple heir scenarios. These industry experts offer:

✨ Direct purchase options that eliminate the need for heir consensus on repairs, timing, and marketing

✨ Coordination with title professionals to resolve liens, judgments, and ownership issues

✨ Simplified processes that reduce stress and timeline

✨ Fair, transparent pricing based on property condition and market value

✨ Expert service navigating complicated situations with friendly and caring support

This approach particularly benefits families when:

- Heirs want quick resolution without lengthy marketing periods

- The property needs substantial repairs heirs cannot fund

- Geographic distance makes traditional selling difficult

- Family dynamics make coordination challenging

- Title issues or liens complicate traditional sales

Working with trustworthy service providers who understand the emotional and practical challenges of inheritance creates helpful solutions that serve everyone’s interests.

Preventing Future Inheritance Conflicts

While this guide focuses on resolving current Multiple Heirs One Property challenges, families can take proactive steps to prevent similar situations in the future.

Estate Planning Best Practices

Clear, updated wills that specify exactly how property should be distributed prevent ambiguity and potential disputes.

Consider these strategies:

🎯 Specific bequests: Instead of leaving “all property to be divided equally among my children,” specify which child receives which property, or direct that property be sold with proceeds divided.

🎯 Unequal distributions with explanation: If circumstances justify unequal inheritance (one child provided caregiving, another received financial support during life), document the reasoning to prevent hurt feelings.

🎯 Trustee authority: Establish a trust with a designated trustee who has authority to manage or sell property, removing decision-making from heirs who may disagree.

🎯 Right of first refusal: Give specific heirs the option to purchase property at appraised value before it’s sold to others.

🎯 Mandatory sale provisions: Direct that property must be sold within a specific timeframe after death, preventing indefinite co-ownership.

Family Communication During Estate Planning

The best time to discuss inheritance preferences is while the property owner is alive and can participate in the conversation.

Family meetings about estate plans allow:

- Parents to explain their intentions and reasoning

- Children to express preferences and concerns

- Everyone to understand financial realities

- Potential conflicts to be identified and addressed proactively

- Alternative solutions to be explored while options remain flexible

Transparency prevents surprises that breed resentment. When heirs learn about inheritance plans only after death, they may feel blindsided or treated unfairly.

Considering Life Insurance Solutions

Life insurance proceeds can equalize inheritance when property can’t be divided equally.

Example: A parent owns a $400,000 home and wants one child to inherit it (perhaps that child lives there or has special attachment). The parent purchases a $400,000 life insurance policy naming the other child as beneficiary, creating equal inheritance value.

This strategy works well for family businesses, farms, or properties with unique significance to specific heirs.

Regular Property and Estate Reviews

Estate plans should be reviewed and updated every 3-5 years or after major life events:

- Marriage or divorce of property owner or heirs

- Birth of grandchildren

- Significant changes in property value

- Changes in financial circumstances

- Changes in family relationships

- Moves to different states with different laws

Property maintenance during the owner’s lifetime also prevents inheritance complications. A well-maintained property in good condition is easier to sell or manage than one requiring extensive repairs.

Real-World Success Stories: How Families Resolved Shared Inheritance

Learning from others’ experiences provides valuable perspective. Here are composite examples based on common scenarios (details changed to protect privacy).

The Johnson Family: Successful Buyout

Situation: Three siblings inherited their parents’ home valued at $360,000. Sarah lived nearby and wanted to keep the family home. Michael and Jennifer lived out of state and preferred cash.

Solution: Sarah obtained a home equity loan on her own residence to fund the buyout. After deducting estimated selling costs (8%), the buyout price was set at $331,200, or $110,400 per sibling share. Sarah paid Michael and Jennifer $110,400 each and received sole ownership.

Outcome: Michael and Jennifer received immediate liquidity. Sarah kept the family home at a price below market purchase. Everyone avoided real estate commissions and the stress of preparing the home for sale. The transaction closed in 45 days.

Key success factors: Clear communication, professional appraisal, documented agreement, and Sarah’s financial capacity to execute the buyout.

The Martinez Family: Collaborative Sale

Situation: Four cousins inherited their grandmother’s property valued at $280,000. The property needed $35,000 in repairs. None of the heirs had emotional attachment or financial capacity to fund improvements.

Solution: The cousins agreed to sell as-is. They interviewed three real estate agents together, selected one with estate sale experience, and listed at $265,000 (reflecting the needed repairs). The property sold in 23 days for $260,000.

Outcome: After selling costs of approximately $20,000, net proceeds of $240,000 were distributed equally: $60,000 per heir. The entire process from decision to closing took 11 weeks.

Key success factors: Aligned interests, realistic pricing, willingness to sell as-is, and collaborative decision-making.

The Williams Family: Rental Income Agreement

Situation: Two brothers inherited a duplex generating $2,400 monthly rental income. Both saw investment potential but lived in different states.

Solution: They created a formal co-ownership LLC, hired a property management company (10% fee), and established a detailed operating agreement specifying income distribution, expense allocation, and decision-making authority.

Outcome: After expenses (taxes, insurance, management, maintenance reserve), the property generates approximately $1,200 monthly net income, split equally. They review financial statements quarterly and make major decisions by mutual agreement. The arrangement has functioned successfully for three years.

Key success factors: Professional property management, clear written agreement, aligned investment philosophy, and strong communication.

The Thompson Family: Partition Resolution

Situation: Three siblings inherited a property valued at $400,000. One wanted to keep it, one wanted to sell immediately, and one wanted to rent it. After 18 months of disagreement and accumulating costs, communication had completely broken down.

Solution: The sibling wanting to sell filed a partition action. After $18,000 in combined legal fees and eight months of court proceedings, the court ordered the property sold. It sold at auction for $365,000.

Outcome: After legal fees, court costs, and selling expenses totaling approximately $45,000, net proceeds of $320,000 were distributed: approximately $106,667 per heir. Everyone received less than if they had cooperated initially, and family relationships were permanently damaged.

Key lesson: Partition works as a last resort but costs everyone significantly. Early professional mediation might have prevented this outcome.

Frequently Asked Questions About Multiple Heirs and Property Inheritance

Can one heir force the sale of inherited property?

Yes, through partition action. Any co-owner can petition the court to force a sale, regardless of other heirs’ preferences. The court will typically order the property sold with proceeds divided proportionally. However, this process is expensive and time-consuming, making it a last resort.

What happens if one heir lives in the inherited property?

The occupying heir doesn’t automatically owe rent to other co-owners, but this creates obvious inequity. Best practice is to formalize an arrangement where the occupying heir either:

- Pays fair market rent divided among other heirs

- Buys out other heirs’ shares

- Receives a reduced inheritance share to account for exclusive use

Without formal agreement, resentment builds and often leads to partition action.

How are property expenses divided among heirs?

Typically, expenses are divided proportionally to ownership shares. If three heirs each own one-third, each pays one-third of taxes, insurance, and maintenance. However, heirs can agree to different arrangements in writing.

If one heir pays expenses others refuse to cover, that heir may have a legal claim for contribution or reimbursement—but enforcing these claims requires legal action.

What if heirs disagree on the property’s value?

Obtain a professional appraisal from a licensed, certified appraiser. Most heirs accept this objective valuation. If disagreement persists, consider:

- Getting multiple appraisals and averaging them

- Agreeing to list at one price and adjusting if the market doesn’t respond

- Using the appraised value minus estimated selling costs for buyout scenarios

Can inherited property be sold with a mortgage or liens?

Yes, but these debts must be paid from sale proceeds before heirs receive anything. If the property has existing liens or judgments, these must be resolved during the sale process. Working with professionals experienced in selling properties with liens ensures these complications are properly addressed.

How long do heirs have to make decisions about inherited property?

There’s no legal deadline for most decisions, but practical considerations create urgency:

- Property taxes and insurance continue accruing

- Vacant properties deteriorate

- Market conditions change

- Family relationships strain under prolonged uncertainty

Most experts recommend reaching resolution within 6-12 months of inheritance to minimize carrying costs and stress.

What are the tax implications of inheriting property?

Heirs receive a “stepped-up basis” equal to the property’s fair market value at the date of death, which typically eliminates capital gains tax on appreciation during the deceased’s ownership. Selling shortly after inheritance usually generates minimal tax liability.

However, if heirs hold the property for years before selling, they’ll owe capital gains tax on appreciation occurring after the inheritance. Each heir reports their proportionate share of gains on individual tax returns.

Do all heirs need to agree to sell inherited property?

Yes, for traditional sales. All co-owners must sign the listing agreement and deed transferring ownership to the buyer. One dissenting heir can prevent a sale.

However, individual heirs can sell their ownership share to other co-owners or third-party investors without unanimous consent—though finding buyers for partial interests is challenging and typically requires significant discounts.

What happens if one heir can’t afford their share of property expenses?

This common situation requires negotiation. Options include:

- Other heirs cover the shortfall and receive increased ownership percentage

- The property is sold to eliminate ongoing expense obligations

- The financially struggling heir sells their share to others

- Formal loan arrangements among heirs with repayment terms

Without resolution, the property may face tax foreclosure or deterioration that harms everyone’s interests.

Taking Action: Your Next Steps for Resolving Shared Inheritance

Facing Multiple Heirs One Property challenges can feel overwhelming, but taking systematic action creates momentum toward resolution.

Immediate Actions (This Week)

✅ Schedule a family meeting with all heirs to discuss the property and preferences

✅ Gather essential documents: deed, recent property tax statements, insurance information, any existing mortgage or lien documentation

✅ Take photos documenting current property condition

✅ Research property value using online tools like Zillow or Realtor.com for preliminary estimates

✅ List ongoing expenses to understand monthly carrying costs

Short-Term Actions (This Month)

✅ Obtain professional appraisal to establish accurate fair market value

✅ Conduct property inspection to identify needed repairs and maintenance

✅ Consult with professionals: real estate attorney, tax advisor, or real estate agent

✅ Research comparable sales if considering selling

✅ Investigate rental market if considering income strategy

✅ Review estate documents to confirm ownership structure and percentages

Medium-Term Actions (Next 2-3 Months)

✅ Present all options to heirs with detailed analysis of each path

✅ Facilitate decision-making through voting, consensus, or mediation

✅ Formalize agreements in writing with legal review

✅ Begin execution of chosen strategy (listing property, pursuing buyout, establishing rental agreement, or filing partition if necessary)

✅ Address title issues or liens that might complicate the chosen path

Resources and Support

Navigating complex inheritance situations doesn’t have to be a solo journey. Sure Path Property Solutions provides expert service for families dealing with multiple heirs, title issues, liens, and other complications that make traditional property sales challenging.

The team offers:

- Free consultations to assess your specific situation

- Helpful guidance through complex title and ownership issues

- Direct purchase options that eliminate the need for repairs and lengthy marketing

- Coordination with attorneys, title companies, and other professionals

- Friendly and caring support during difficult family transitions

- Trustworthy service focused on fair, transparent solutions

Whether you’re ready to move forward with a sale or simply need helpful solutions to understand your options, reaching out to industry experts who specialize in complicated property situations provides clarity and direction.

Conclusion: Finding Resolution While Preserving Family Relationships

Multiple Heirs One Property: How to Navigate Shared Inheritance situations test families in unique ways. The intersection of grief, money, property, and family dynamics creates complexity that extends far beyond simple real estate transactions.

Yet thousands of families successfully navigate these challenges every year by following the principles outlined in this guide:

🏡 Open, honest communication that acknowledges both practical and emotional concerns

🏡 Professional guidance from attorneys, appraisers, agents, and specialized property solution companies

🏡 Documented agreements that protect everyone’s interests and prevent misunderstandings

🏡 Realistic timelines that balance thoughtful decision-making with the costs of delay

🏡 Flexibility and compromise that honor different perspectives and needs

The path forward depends on your family’s unique circumstances, the property’s characteristics, each heir’s financial situation, and everyone’s willingness to work together toward resolution.

Remember these key principles:

- No single “right” answer exists—the best solution is the one that works for your specific situation

- Speed matters—carrying costs and property deterioration make delay expensive

- Professional help pays for itself—expert guidance prevents costly mistakes

- Relationships matter more than property—preserve family bonds while resolving practical issues

- Solutions exist for every situation—even seemingly impossible deadlocks can be resolved

Whether you choose a buyout arrangement, collaborative sale, rental income strategy, or even partition action, taking informed action moves you toward resolution. The worst choice is inaction—allowing the property to sit in limbo while costs accumulate and relationships deteriorate.

If you’re facing Multiple Heirs One Property challenges and need helpful guidance from professionals who understand complex inheritance situations, Sure Path Property Solutions stands ready to help. With expert service, trustworthy advice, and friendly and caring support, the team can help you navigate even the most complicated shared inheritance scenarios.

Your inherited property represents your loved one’s legacy. Honor that legacy by finding a resolution that serves everyone’s interests while preserving the family relationships that matter most.

Take the first step today. Whether that means scheduling a family meeting, consulting with an attorney, obtaining an appraisal, or reaching out to property solution experts, action creates momentum toward the resolution you need.

The path through shared inheritance may be challenging, but with the right information, professional support, and commitment to communication, families can successfully navigate these complex situations and move forward with clarity and confidence.