Sell House with Multiple Liens: We Handle Complex Payoffs

Imagine opening your mailbox to find yet another notice about a lien on your property. First came the tax lien. Then the contractor’s mechanics lien. Now there’s a judgment lien from an old lawsuit. Each piece of paper feels like another chain wrapped around your house, making it impossible to sell or move forward with your life.

You’re not alone in this situation. Thousands of property owners across the country face the overwhelming challenge of selling a house burdened by multiple liens. The good news? Sell House with Multiple Liens: We Handle Complex Payoffs is not just a promise—it’s a practical solution that can free you from this complicated situation faster than you might think.

When multiple liens attach to your property, traditional buyers and real estate agents often walk away. The paperwork becomes too complex. The timeline stretches too long. The risk feels too high. But specialized buyers like Sure Path Property Solutions understand exactly how to navigate these murky waters, coordinating with counties, title companies, and lien holders to create a clear path forward.

Key Takeaways

- Multiple liens don’t prevent a sale when working with experienced buyers who specialize in complex property situations

- Lien priority determines payoff order—understanding which liens get paid first protects you from unexpected financial surprises

- Professional coordination is essential—expert buyers handle negotiations with multiple lien holders simultaneously, saving months of stress

- Net proceeds are calculated after all payoffs—transparent buyers show exactly what you’ll receive before closing

- Speed matters—the right buyer can close in days or weeks, not months, even with complicated lien situations

Understanding Multiple Liens on Your Property

What Are Property Liens?

A property lien is a legal claim against your house or land that secures payment for a debt. Think of it like a bookmark that creditors place on your property, giving them the right to be paid from the sale proceeds before you receive anything.

Liens come in many forms:

- Tax liens from unpaid property taxes, income taxes, or other government debts

- Judgment liens resulting from court decisions in lawsuits

- Mechanics liens filed by contractors or suppliers for unpaid work

- Mortgage liens held by your lender

- HOA liens for unpaid homeowners association fees

Each lien represents a separate creditor with a legal stake in your property. When multiple liens pile up, they create layers of complexity that can feel impossible to untangle.

How Multiple Liens Accumulate

Liens rarely appear all at once. They typically accumulate over time through various circumstances:

Financial hardship often triggers the first lien. Missing property tax payments leads to a tax lien. Falling behind on medical bills might result in a judgment lien after a lawsuit. Each financial setback can add another layer.

Inherited property frequently comes with surprise liens. The previous owner may have left behind unpaid debts that transferred with the property. Back taxes on inherited property are especially common.

Home improvement projects gone wrong create mechanics liens. When contractors don’t receive payment—whether due to disputes or financial problems—they can file liens that remain attached to the property.

Divorce or estate settlements sometimes leave properties with multiple claims from different parties, creating a tangled web of financial obligations.

Why Traditional Sales Fail with Multiple Liens

Most conventional buyers and their lenders require “clear title” before closing. This means the property must be free from liens and other encumbrances. When they discover multiple liens during the title search, several problems emerge:

🚫 Mortgage lenders refuse to finance properties with unresolved liens, eliminating most traditional buyers from the market.

🚫 Title companies won’t insure the property until all liens are satisfied, creating a roadblock to closing.

🚫 Buyers lack funds to pay off liens at closing, especially when liens total thousands or tens of thousands of dollars.

🚫 Timeline uncertainty scares away buyers who need to close by a specific date.

Real estate agents often decline to list properties with multiple liens because they know the challenges ahead. The few who do take these listings frequently struggle to find qualified buyers, leaving properties sitting on the market for months or years.

The Challenge of Selling a House with Multiple Liens

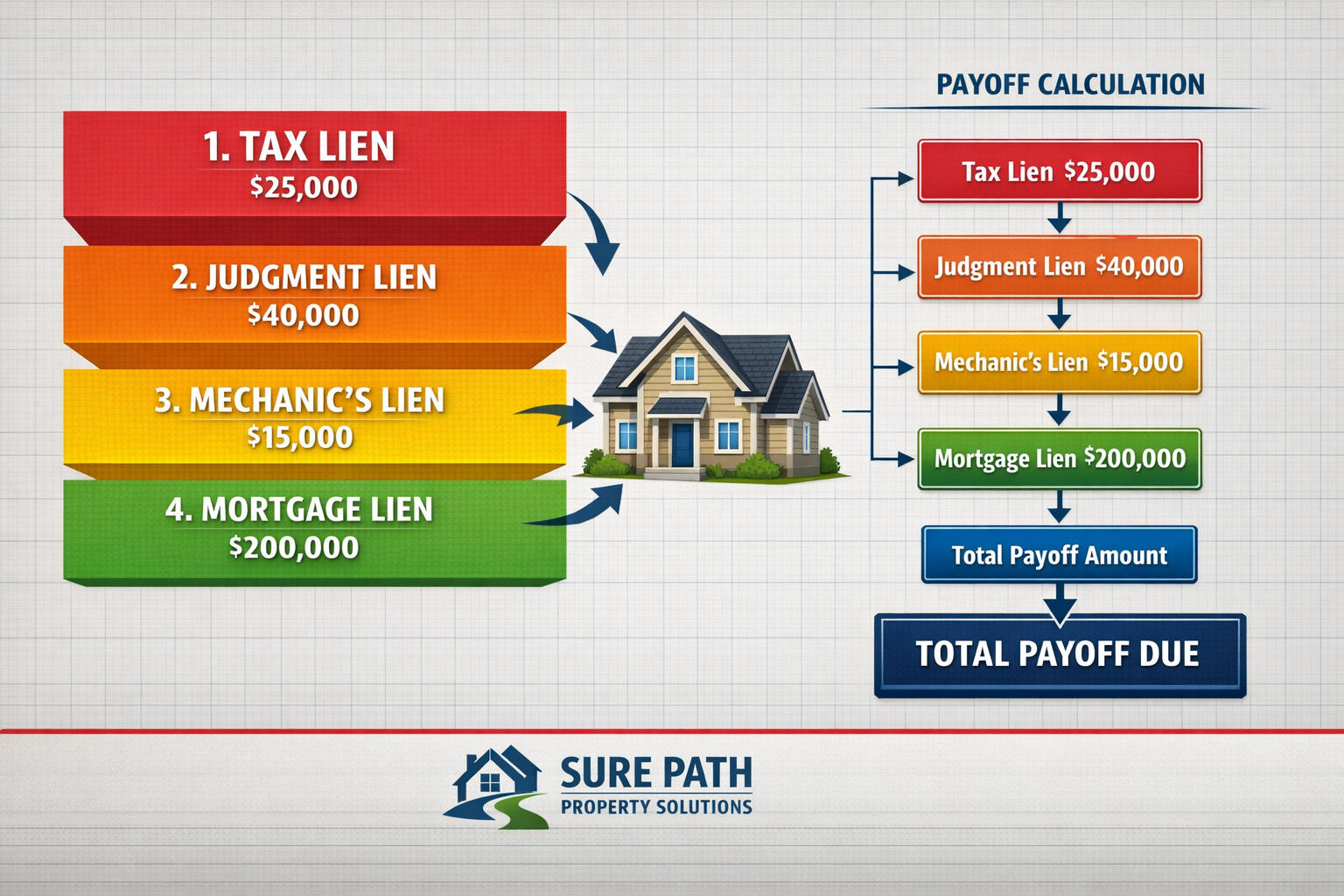

Lien Priority and Payoff Order

Not all liens are created equal. Understanding lien priority is crucial because it determines who gets paid first when your property sells.

Generally, liens follow this hierarchy:

- Property tax liens (almost always first priority)

- First mortgage liens (recorded first)

- Second mortgages or HELOCs (recorded second)

- Federal tax liens (IRS liens)

- Judgment liens (varies by recording date)

- Mechanics liens (can have retroactive priority)

- HOA liens (priority varies by state)

The recording date often determines priority among liens of the same type. A judgment lien recorded in 2023 typically takes priority over one recorded in 2024.

Why priority matters: If your house sells for $200,000 but you have $180,000 in liens, the payoff order determines whether you receive anything. Higher-priority liens get paid in full before lower-priority liens receive a penny.

| Lien Type | Amount | Priority | Payoff Amount |

|---|---|---|---|

| Property Tax Lien | $15,000 | 1st | $15,000 (full) |

| First Mortgage | $150,000 | 2nd | $150,000 (full) |

| Judgment Lien | $25,000 | 3rd | $20,000 (partial) |

| Mechanics Lien | $10,000 | 4th | $0 (insufficient funds) |

In this example, the mechanics lien holder receives nothing because the higher-priority liens consumed all sale proceeds.

Calculating Your Net Proceeds

When you sell house with multiple liens, understanding your potential net proceeds prevents disappointment at closing.

The calculation works like this:

Sale Price – Closing Costs – Lien Payoffs = Your Net Proceeds

Let’s walk through a real-world example:

- Sale price: $175,000

- Closing costs (title, recording, etc.): $3,500

- Tax lien: $8,000

- First mortgage: $120,000

- Judgment lien: $15,000

- Mechanics lien: $6,000

Total liens: $149,000

Available for liens after closing costs: $171,500

Your net proceeds: $22,500

This property owner walks away with money despite having nearly $150,000 in liens. However, if the liens totaled more than $171,500, they would need to bring money to closing or negotiate with lien holders to accept less than the full amount.

Common Complications with Multiple Liens

Several complications frequently arise when dealing with multiple liens:

Subordination issues occur when a lien holder refuses to accept a lower priority position, blocking the sale.

Disputed amounts create delays when you disagree with a lien holder about how much is actually owed, requiring legal resolution.

Missing lien holders make payoff impossible when creditors have moved, gone out of business, or can’t be located.

Expired liens may still appear on title reports even though they’re no longer enforceable, requiring legal action to remove them.

Partial payoffs become necessary when sale proceeds don’t cover all liens, requiring negotiation with junior lien holders to accept reduced payments.

These complications explain why selling a house with a lien requires specialized expertise and patient coordination.

How We Handle Complex Lien Payoffs

Our Specialized Process

At Sure Path Property Solutions, we’ve developed a systematic approach to handle complex payoffs that removes the burden from property owners. Our process transforms what seems impossible into a straightforward transaction.

Step 1: Comprehensive Lien Search

We begin with a thorough title search that uncovers every lien, judgment, and encumbrance attached to your property. Many property owners are surprised to discover liens they didn’t know existed. Our industry experts work with professional title companies to ensure nothing is missed.

Step 2: Lien Verification and Calculation

Next, we verify each lien’s validity, amount, and priority. This involves:

- Contacting each lien holder directly

- Obtaining payoff statements with current balances

- Calculating interest, penalties, and fees through closing

- Identifying any errors or disputes requiring resolution

Step 3: Financial Analysis and Offer

We analyze the complete financial picture to determine what we can offer for your property. Our offers account for:

- Current market value

- All lien payoffs required

- Closing costs and fees

- Our acquisition costs

- Fair compensation for you

This analysis ensures transparency. You’ll know exactly where every dollar goes before you accept our offer.

Step 4: Simultaneous Coordination

Here’s where our expertise truly shines. We coordinate with multiple parties simultaneously:

✅ County tax offices for property tax liens

✅ IRS or state agencies for government liens

✅ Courts and attorneys for judgment liens

✅ Contractors and suppliers for mechanics liens

✅ Mortgage companies for loan payoffs

✅ Title companies for closing coordination

This parallel processing dramatically shortens the timeline compared to handling each lien sequentially.

Step 5: Negotiation When Necessary

Sometimes liens exceed the property’s value, making full payoff impossible. We negotiate with junior lien holders to accept reduced payments, using our experience and industry relationships to reach agreements that allow the sale to proceed.

Step 6: Closing and Payoff Distribution

At closing, the title company distributes funds according to lien priority, pays all required parties, and provides you with your net proceeds. You walk away free from the liens and the property, ready to move forward.

Why Professional Coordination Matters

Attempting to coordinate multiple lien payoffs yourself creates several problems:

Time consumption becomes overwhelming. Each lien holder has different requirements, contact procedures, and processing times. Property owners often spend months making phone calls, sending documents, and waiting for responses.

Missed deadlines occur when you’re juggling multiple moving parts. A delay with one lien holder can derail the entire transaction.

Negotiation challenges arise because individual property owners lack leverage with lien holders. Professional buyers who handle hundreds of transactions have established relationships and credibility.

Legal complexity increases with each additional lien. Understanding lien priority, subordination agreements, and payoff requirements requires specialized knowledge.

Emotional stress takes a toll when dealing with creditors, especially if the liens resulted from difficult life circumstances.

Our team provides helpful guidance through every step, removing the stress and complexity from your shoulders. We’ve handled countless properties with multiple liens, giving us the expertise to anticipate problems and solve them quickly.

Our Track Record with Complex Properties

We specialize in situations that others avoid. Our portfolio includes properties with:

- Five or more simultaneous liens

- Liens exceeding property value requiring negotiation

- Federal and state tax liens requiring IRS coordination

- Judgment liens from multiple lawsuits

- Mechanics liens from defunct contractors

- Properties with title problems and multiple liens combined

One recent client inherited a property with seven different liens totaling $89,000. The property was worth approximately $110,000. Traditional buyers wouldn’t touch it. We coordinated with all seven lien holders, negotiated reduced payoffs on two junior liens, and closed in 23 days. The client received $12,500 and was finally free from the inherited burden.

Another property owner faced foreclosure with multiple liens stacking up. We worked with the mortgage company, two judgment creditors, and the county tax office to sell the house fast in foreclosure, stopping the auction and allowing the owner to walk away without a foreclosure on their record.

Types of Liens We Handle

Tax Liens: Property and IRS

Tax liens represent some of the most challenging situations because government agencies have significant collection powers and first-priority status.

Property tax liens arise when county or municipal property taxes go unpaid. These liens typically take first priority over almost all other liens, including mortgages. Accumulated property taxes can grow quickly with penalties and interest, sometimes reaching tens of thousands of dollars on properties that sat vacant for years.

We work directly with county tax offices to:

- Obtain exact payoff amounts including all penalties

- Negotiate payment plans when possible

- Coordinate closing timing to minimize additional interest

- Ensure proper lien release documentation

IRS and state tax liens result from unpaid income taxes, business taxes, or other government obligations. Federal tax liens can attach to all property you own, making them particularly troublesome.

Our experience with cash buyers for tax lien properties means we understand IRS procedures, subordination requests, and discharge applications that may reduce the payoff amount or remove the lien from your specific property.

Judgment Liens from Lawsuits

Judgment liens result from court decisions in civil lawsuits. Common sources include:

- Medical debt lawsuits

- Credit card judgments

- Personal injury awards

- Business debt litigation

- Contract disputes

Once a creditor obtains a judgment, they can record it as a lien against your property in the county where it’s located. These liens can remain enforceable for many years, with some states allowing renewal that extends them indefinitely.

Challenges with judgment liens:

- Creditors may be difficult to locate years after the judgment

- Interest continues accumulating on the judgment amount

- Some judgment creditors refuse to negotiate

- Multiple judgments from the same lawsuit can appear as separate liens

We handle the detective work of locating judgment creditors, obtaining current payoff amounts, and negotiating settlements when appropriate. Our help selling house with liens includes managing these often-frustrating situations.

Mechanics Liens from Contractors

Mechanics liens (also called construction liens) protect contractors, subcontractors, and material suppliers who provided labor or materials for property improvements but weren’t paid.

These liens have unique characteristics:

Retroactive priority: In many states, mechanics liens can claim priority from the date work began, not when the lien was filed. This means a mechanics lien filed in 2026 might have priority over a mortgage recorded in 2025 if the work started before the mortgage.

Time limitations: Contractors must file mechanics liens within specific timeframes after completing work or they lose lien rights. However, once properly filed, these liens can be difficult to remove.

Verification challenges: Sometimes mechanics liens are filed incorrectly or for inflated amounts, requiring legal action to challenge them.

We investigate each mechanics lien to verify its validity, determine its actual priority, and negotiate with contractors who may be willing to accept less than the full claimed amount to receive payment.

Mortgage Liens and HELOCs

Mortgage liens and home equity lines of credit (HELOCs) are voluntary liens you agreed to when borrowing money. While more straightforward than involuntary liens, they still create complications when multiple mortgages exist or when you’re underwater (owing more than the property’s worth).

First mortgages typically have priority over most other liens except property taxes. The payoff amount includes principal, interest through closing, and any fees.

Second mortgages and HELOCs sit in junior positions. When property values decline, these lenders face the risk of receiving nothing at sale. This motivates them to negotiate reduced payoffs rather than receive nothing.

We coordinate with mortgage companies to:

- Obtain accurate payoff quotes

- Request per-diem interest calculations

- Handle short sale negotiations when necessary

- Ensure proper lien release documentation

Our experience with short sales helps when mortgage balances exceed property value, requiring lender approval to accept less than the full amount owed.

HOA Liens and Special Assessments

Homeowners association liens result from unpaid HOA fees, special assessments, or fines. While typically smaller than other liens, HOA liens can be surprisingly aggressive.

Many states give HOA liens “super-priority” status for a portion of unpaid dues, allowing them to take priority even over first mortgages. This unusual priority makes HOA liens more powerful than their dollar amounts suggest.

HOA lien challenges:

- Fees continue accumulating monthly until paid

- Late fees and attorney costs can double the original amount

- HOAs may refuse to negotiate or reduce amounts

- Some HOAs file foreclosure actions quickly for relatively small amounts

We work with HOA management companies to obtain payoff statements, negotiate when possible, and ensure proper release documentation so the lien doesn’t reappear after closing.

Benefits of Working with Lien Resolution Specialists

Speed: Closing in Days, Not Months

Time matters when dealing with multiple liens. Every passing day adds interest to tax liens, increases penalties, and creates more stress.

Traditional sales with multiple liens typically take 4-6 months or longer because:

- Finding a qualified buyer takes months

- Each lien requires separate negotiation

- Financing delays are common

- Title issues require legal resolution

Our streamlined process closes most transactions in 14-30 days, even with complex lien situations. We’ve closed some deals in as few as 7 days when circumstances required speed.

This speed provides several advantages:

💨 Stop accumulating interest and penalties on tax liens and judgments

💨 Avoid foreclosure if you’re facing an auction date

💨 Reduce stress by resolving the situation quickly

💨 Move forward with your life without months of uncertainty

No Out-of-Pocket Costs

One of the biggest misconceptions about selling property with liens is that you need money to pay off the liens before selling. This simply isn’t true when working with the right buyer.

We handle all lien payoffs at closing using the purchase proceeds. You don’t need to:

- Pay liens before listing the property

- Come to closing with cash

- Hire attorneys to negotiate with lien holders

- Pay for title work or lien searches upfront

Everything is coordinated through the closing process, with all costs deducted from the purchase price. You receive your net proceeds check at closing without spending a dollar beforehand.

This approach makes selling possible even when you have no savings or financial resources to address the liens yourself.

Expert Negotiation with Lien Holders

Lien holders respond differently to professional buyers than to individual property owners. Our established relationships and track record give us negotiating leverage that benefits you.

Junior lien holders (those in lower priority positions) often face receiving nothing if the property goes to foreclosure. We can negotiate with them to accept reduced payments, sometimes settling liens for 30-50% of the claimed amount.

Government agencies have specific programs and procedures for lien releases, subordinations, and partial payments. We know these programs and how to navigate the bureaucracy.

Judgment creditors may be willing to settle for less than the full judgment amount when presented with a realistic analysis of their alternatives.

Our expert service includes these negotiations as part of our standard process. We advocate for the best possible outcome while maintaining the ethical standards and professionalism that make these negotiations successful.

Transparent Process and Clear Communication

Confusion and uncertainty create stress. We believe in complete transparency throughout the process.

You’ll receive:

📋 Detailed breakdown of all liens and their amounts

📋 Clear explanation of lien priority and payoff order

📋 Written offer showing exactly how we calculated our price

📋 Net proceeds estimate showing what you’ll receive

📋 Regular updates on negotiation progress

📋 Closing statement review before signing any documents

Our friendly and caring approach means you can ask questions anytime and receive honest, straightforward answers. We explain complex legal and financial concepts in plain language because we believe you deserve to understand every aspect of your transaction.

This transparency builds trust and ensures no surprises at closing. The net proceeds amount we estimate at the beginning matches what you receive at the end (barring unexpected liens discovered during title search).

Avoiding Foreclosure and Further Damage

Multiple liens often signal financial distress. If you’re also behind on mortgage payments, foreclosure may be looming. Selling before foreclosure provides significant benefits:

✅ Avoid foreclosure on your credit report, which damages credit scores for 7 years

✅ Prevent deficiency judgments that can result from foreclosure

✅ Receive cash proceeds instead of losing everything

✅ Maintain control of the timeline and outcome

✅ Reduce stress by resolving the situation on your terms

We’ve helped many property owners sell fast to avoid foreclosure, coordinating with mortgage companies to stop the foreclosure process while closing the sale.

Even if foreclosure has already been filed, selling remains possible until the actual auction date. The sooner you reach out, the more options we can explore.

Real-World Scenarios: Multiple Lien Success Stories

Case Study: Inherited Property with Seven Liens

The Situation:

Maria inherited her uncle’s house in Dallas after he passed away unexpectedly. She discovered the property had accumulated seven different liens over the previous decade:

- Property tax lien: $23,400

- IRS tax lien: $31,000

- First mortgage: $87,000

- Judgment lien (medical debt): $8,500

- Judgment lien (credit card): $6,200

- Mechanics lien (roof repair): $4,800

- HOA lien: $3,100

Total liens: $164,000

The property’s market value was approximately $185,000, leaving little equity after accounting for liens and closing costs. Traditional buyers wouldn’t consider the property due to the complexity. Real estate agents declined to list it.

Our Solution:

We conducted a comprehensive title search, verified all lien amounts, and analyzed the property’s condition and value. We made an offer of $182,000, which would cover all liens and provide Maria with net proceeds.

We coordinated with:

- The county tax office for property tax payoff

- The IRS for federal tax lien discharge

- The mortgage company for loan payoff

- Two judgment creditors

- The roofing contractor

- The HOA management company

The mechanics lien holder agreed to accept $3,500 instead of the claimed $4,800 when presented with proof of the lien priority and available funds. One judgment creditor accepted $5,000 instead of $6,200 for the same reason.

The Outcome:

We closed in 26 days. All seven liens were satisfied and released. Maria received $11,200 in net proceeds and was free from the inherited burden. She later told us, “I thought I’d be stuck with that house forever. You made the impossible possible.”

Case Study: Divorce Property with Competing Claims

The Situation:

Robert and Jennifer were divorcing after 15 years of marriage. Their marital home had become a battleground, with neither party willing to continue paying the mortgage or other obligations. The property accumulated multiple liens:

- First mortgage: $198,000

- Second mortgage (HELOC): $45,000

- Property tax lien: $11,000

- Mechanics lien (unpaid pool contractor): $18,000

- Judgment lien (business debt in Robert’s name): $22,000

Total liens: $294,000

The property was worth approximately $310,000. Both parties wanted to sell but couldn’t agree on repairs, listing price, or how to handle the liens. The situation was deteriorating, with foreclosure becoming likely.

Our Solution:

We met with both parties and their attorneys separately, then together. We explained how our process would resolve all liens, divide the net proceeds according to their divorce decree, and free both parties to move forward.

Our offer of $305,000 was below market value but eliminated the need for repairs, carrying costs, and months of uncertainty. Both parties agreed this was preferable to foreclosure or continued conflict.

We negotiated with the HELOC lender to accept $38,000 instead of the full $45,000 balance. The pool contractor accepted $15,000 to release the mechanics lien. The judgment creditor, understanding the property was being sold in a divorce situation with limited equity, accepted $18,000.

The Outcome:

We closed in 19 days. All liens were satisfied. After paying closing costs, Robert and Jennifer each received approximately $8,000, split according to their divorce agreement. Both were relieved to close this chapter of their lives and move forward separately.

Case Study: Pre-Foreclosure with Stacked Liens

The Situation:

David fell behind on his mortgage after losing his job in 2024. By early 2026, his property faced foreclosure with an auction date set for 45 days away. Multiple liens had accumulated:

- First mortgage (including arrears): $156,000

- Property tax lien: $8,900

- IRS tax lien: $28,000

- Judgment lien (car accident): $15,000

Total liens: $207,900

The property was worth approximately $215,000. David had found a new job but couldn’t catch up on the missed payments. He wanted to avoid foreclosure but didn’t know how to handle the multiple liens.

Our Solution:

Time was critical with the foreclosure auction approaching. We immediately contacted the mortgage company to request a postponement of the auction while we worked toward closing.

We verified all lien amounts and made an offer of $212,000. This would cover all liens and provide David with a small amount of cash to help with his move.

We worked with the IRS to obtain a lien discharge (removing the lien from this specific property while keeping it in effect against David personally for other assets). The judgment creditor agreed to accept $12,000 instead of $15,000.

The Outcome:

We closed in 17 days, just before the scheduled auction. The foreclosure was cancelled. All liens were satisfied. David received $3,800 and avoided foreclosure on his credit report. He later said, “You saved my credit and gave me a fresh start. I can’t thank you enough.”

Frequently Asked Questions

Can I sell my house if the liens exceed its value?

Yes, but the process requires negotiation with lien holders. When liens exceed property value, junior lien holders (those in lower priority positions) face receiving nothing. We can often negotiate with them to accept reduced payments, making the sale possible.

This process is called a “short sale” when it involves mortgage lenders, but the same principle applies to other lien holders. Our experience with investors who buy houses with liens means we understand how to structure these deals successfully.

How long does it take to sell a house with multiple liens?

With our process, most sales close in 14-30 days, even with multiple liens. Traditional sales with liens typically take 4-6 months or longer.

The timeline depends on several factors:

- Number and type of liens

- Responsiveness of lien holders

- Whether negotiations are required

- Complexity of title issues

- Your timeline needs

We prioritize speed while ensuring all legal requirements are met properly.

Will I receive any money if my house has multiple liens?

In many cases, yes. If your property’s value exceeds the total liens plus closing costs, you’ll receive the difference as net proceeds.

Even when liens are substantial, our negotiation expertise often creates equity where none seemed to exist. We’ve helped property owners receive proceeds in situations where they assumed they’d get nothing.

We provide a detailed net proceeds estimate before you commit to selling, so you’ll know exactly what to expect.

Do I need to hire an attorney to sell a house with liens?

Not when working with us. We coordinate the entire process, including working with title companies and lien holders. The title company handles the legal aspects of lien payoffs and releases.

However, if you have concerns about specific liens or want independent legal advice, consulting an attorney is always your right. We support whatever makes you comfortable.

What happens if a lien holder won’t negotiate?

Lien holders in senior positions (like property tax liens or first mortgages) rarely need to negotiate—they’ll be paid in full from the sale proceeds.

Junior lien holders sometimes refuse to negotiate, believing they’ll receive more through other collection methods. In these cases, we analyze their actual alternatives:

- If the property goes to foreclosure, what would they receive?

- Can they collect through wage garnishment or bank levies?

- How much would litigation cost them?

This realistic analysis often motivates negotiation. In rare cases where a junior lien holder refuses reasonable settlement, we may need to adjust the sale price or structure to accommodate their demands, or in some situations, the sale may not be possible.

Can you help with properties in other states?

Yes. We work with properties throughout multiple states and have established relationships with title companies, attorneys, and lien resolution specialists nationwide. Our process adapts to state-specific lien laws and requirements.

Whether your property is in Texas, Oklahoma, or other states, we can help you sell house with multiple liens through our network of resources and expertise.

Taking the Next Step: Your Path to Freedom

Getting Started is Simple

Selling a house with multiple liens might seem overwhelming, but getting started is straightforward:

Step 1: Contact Us

Reach out through our website, phone, or email. Share basic information about your property and situation. This initial conversation is completely free and confidential, with no obligation.

Step 2: Property Evaluation

We’ll ask questions about your property’s location, condition, and the liens you know about. This helps us provide an accurate preliminary assessment.

Step 3: Title Search

We’ll order a comprehensive title search to uncover all liens and encumbrances. This ensures nothing is missed and we can provide an accurate offer.

Step 4: Receive Your Offer

Within days, we’ll present a detailed written offer showing:

- Purchase price

- All liens and their payoff amounts

- Closing costs

- Your estimated net proceeds

Step 5: Review and Decide

Take time to review the offer. Ask questions. Consult with family, attorneys, or advisors. We want you to feel completely comfortable with your decision.

Step 6: Accept and Close

If you accept our offer, we’ll coordinate everything from that point forward. You’ll sign documents at closing and receive your check. We handle all lien payoffs and releases.

What to Prepare

When you contact us, having the following information ready helps us serve you better:

📝 Property address and basic details

📝 Known liens (tax bills, judgment documents, etc.)

📝 Current mortgage statement (if applicable)

📝 Recent property tax statement

📝 Your timeline and goals

Don’t worry if you don’t have all this information. We can work with whatever you have and obtain missing details through our research.

Why Choose Sure Path Property Solutions

We’re not just cash buyers—we’re problem solvers who specialize in complex situations. Our trustworthy service is built on:

Experience: We’ve successfully closed hundreds of transactions involving multiple liens, title issues, and complicated situations.

Transparency: We explain everything in plain language and provide detailed documentation showing exactly how we calculated our offer.

Speed: Our streamlined process closes in weeks, not months, getting you to resolution quickly.

Compassion: We understand that liens often result from difficult life circumstances. We treat every client with respect and dignity.

Expertise: Our team includes industry experts who understand lien law, title issues, and real estate transactions at a deep level.

Results: We’ve helped property owners in seemingly impossible situations find helpful solutions and move forward with their lives.

The Cost of Waiting

Every day you wait to address multiple liens on your property, the situation typically worsens:

⏰ Interest and penalties accumulate on tax liens

⏰ Additional liens may be filed

⏰ Foreclosure moves closer

⏰ Stress takes a toll on your health and relationships

⏰ Property condition may deteriorate

⏰ Market conditions may change

Taking action now—even if you’re just exploring options—puts you in control of the situation rather than letting it control you.

Conclusion: Your Fresh Start Awaits

Multiple liens on your property don’t have to mean the end of your options. While traditional buyers and real estate agents may walk away from complex situations, specialized buyers like Sure Path Property Solutions see these challenges as opportunities to provide helpful solutions.

Sell House with Multiple Liens: We Handle Complex Payoffs is more than a service—it’s a pathway to freedom from the burden of accumulated debt, complicated legal situations, and overwhelming stress.

You’ve learned how lien priority works, why professional coordination matters, and how our process transforms what seems impossible into a straightforward transaction. You’ve seen real-world examples of property owners who faced seven liens, divorce battles, and foreclosure threats—yet found resolution and received cash proceeds.

The expertise, speed, and transparent process we provide make selling possible even when:

- Liens exceed your property’s value

- Multiple creditors are involved

- Time is running out before foreclosure

- Traditional options have failed

- You have no money to pay liens upfront

Your situation is unique, but you’re not alone. Thousands of property owners face similar challenges every year. The difference between those who find resolution and those who don’t often comes down to one decision: reaching out for expert help.

Take Action Today

The first step toward resolving your multiple lien situation is simple: contact us. There’s no cost, no obligation, and no pressure. We’ll listen to your situation, answer your questions honestly, and help you understand your options.

Whether you decide to work with us or pursue another path, you’ll have clarity about your situation and what’s possible. That clarity alone is valuable.

Ready to move forward? Contact Sure Path Property Solutions today for a free, confidential consultation. Let’s explore how we can help you sell house with multiple liens and start your fresh chapter.

Your property doesn’t have to remain a burden. Your liens don’t have to control your future. With the right partner and proven process, you can resolve even the most complex situations and move forward with confidence.

The path to resolution starts with a conversation. Let’s have that conversation today.