Selling a House with a Lien Against It: Your Complete Options

Discovering a lien on your property when you’re ready to sell can feel like hitting a brick wall. The good news? Selling a house with a lien against it is absolutely possible—and you have more options than you might think.

Whether you’re dealing with unpaid taxes, contractor bills, court judgments, or HOA fees, liens don’t have to derail your plans. Thousands of homeowners successfully navigate these challenges every year with the right knowledge and helpful guidance. This comprehensive guide walks you through every option available for selling a house with a lien against it in 2026, from traditional solutions to fast-track alternatives that can close in days.

Key Takeaways

- Liens must typically be resolved at closing, either through sale proceeds or negotiated settlements, but they don’t prevent you from selling

- Different lien types have different priority levels, affecting the order in which they get paid from your sale proceeds

- You have multiple pathways: traditional sales with lien payoff, cash buyers who handle liens, negotiated settlements, or short sales when equity is insufficient

- Disclosure is legally required in most states—hiding liens can result in serious legal consequences and transaction cancellation

- Professional help makes the difference: working with industry experts who understand lien resolution can save thousands and accelerate your timeline significantly

Understanding Property Liens: What You’re Really Dealing With

A lien is a legal claim against your property that gives a creditor the right to receive payment from your home’s sale proceeds. Think of it as a financial “hold” on your house—not ownership, but a guaranteed spot in line when money changes hands.

How Liens Attach to Your Property

Liens attach to property, not just to you personally. This means:

- The lien stays with the house even if you transfer the deed

- New buyers inherit the lien problem unless it’s cleared

- You can’t simply “walk away” from the debt by abandoning the property

- The lien holder has legal recourse to force payment through foreclosure in many cases

Understanding this attachment is crucial because it explains why buyers and title companies insist on clear title before closing.

Common Types of Property Liens

Not all liens are created equal. Here are the most common types homeowners encounter:

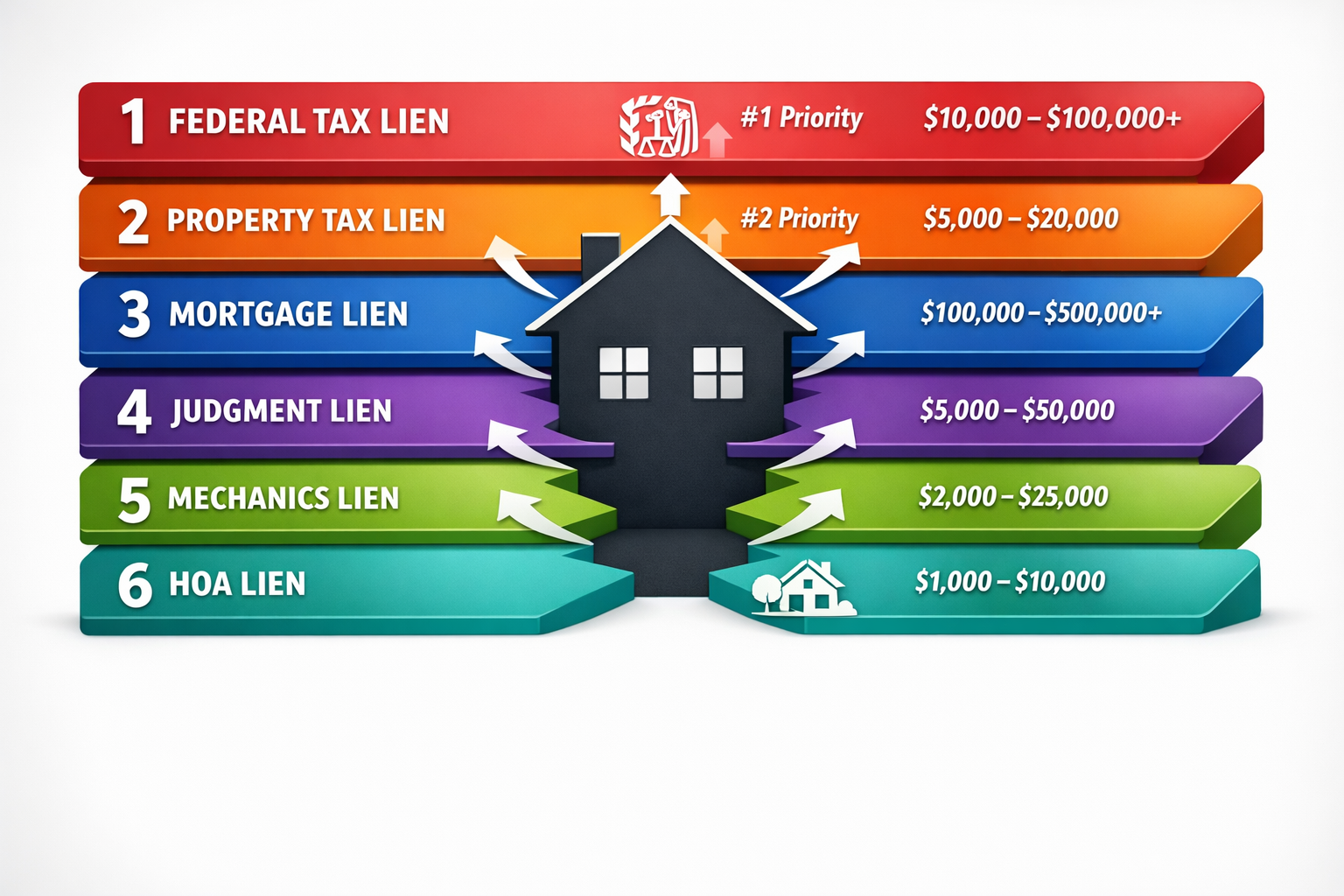

| Lien Type | How It Happens | Typical Priority |

|---|---|---|

| Property Tax Lien | Unpaid county/municipal taxes | Highest priority (often first) |

| Federal Tax Lien | Unpaid IRS taxes | Very high priority |

| Mortgage Lien | Your home loan | Priority by recording date |

| Judgment Lien | Court-ordered debt payment | Varies by state |

| Mechanics Lien | Unpaid contractor/supplier bills | High priority (60-120 days to file) |

| HOA Lien | Unpaid association fees | Can have “super priority” in some states |

| Child Support Lien | Unpaid support obligations | High priority |

Each lien type comes with different rules, timeframes, and resolution strategies. For detailed information about specific lien types, check out our guide on debt liens and how they affect property sales.

Lien Priority: Who Gets Paid First?

Lien priority determines the order of payment when your house sells. This becomes critical when sale proceeds don’t cover all debts.

Generally, priority follows this hierarchy:

- Property tax liens (nearly always first)

- Federal tax liens (very high priority)

- Mortgages and deeds of trust (by recording date)

- HOA liens (can have super-priority for certain amounts in some states)

- Judgment liens (by recording date)

- Other liens (by recording date)

Important exception: Mechanics liens often receive special priority treatment, sometimes jumping ahead of mortgages depending on state law and when work began versus when the mortgage was recorded.

Understanding lien priority and hierarchy helps you strategize which liens to negotiate and which must be paid in full.

The Legal Reality: Can You Actually Sell with a Lien?

Yes, you can legally sell a house with a lien against it. The lien doesn’t prevent the sale—it just requires resolution before or at closing.

What the Law Requires

Most states require sellers to:

✅ Disclose all known liens to potential buyers in writing

✅ Provide clear title at closing (or buyer must agree to accept the lien)

✅ Use sale proceeds to satisfy liens in priority order

✅ Obtain lien releases showing debts are paid or settled

Failure to disclose liens can result in:

- Transaction cancellation

- Lawsuits for fraud or misrepresentation

- Financial liability for buyer’s losses

- Criminal penalties in extreme cases

How Title Companies Handle Liens

Title companies conduct thorough searches—typically reviewing records 30-50 years back—to identify all liens. When they find liens, they:

- Require payoff amounts from each lienholder

- Calculate net proceeds after all liens are paid

- Hold funds in escrow to ensure proper distribution

- Obtain lien releases before issuing title insurance

- Record the releases to clear public records

This process protects buyers and ensures they receive clean title. Title companies won’t issue insurance on property with unresolved liens except in rare circumstances.

For properties with complicated title situations, our article on selling houses with title problems offers additional helpful solutions.

Your Complete Options for Selling a House with a Lien Against It

You have several viable pathways forward. The best choice depends on your equity position, timeline, and financial situation.

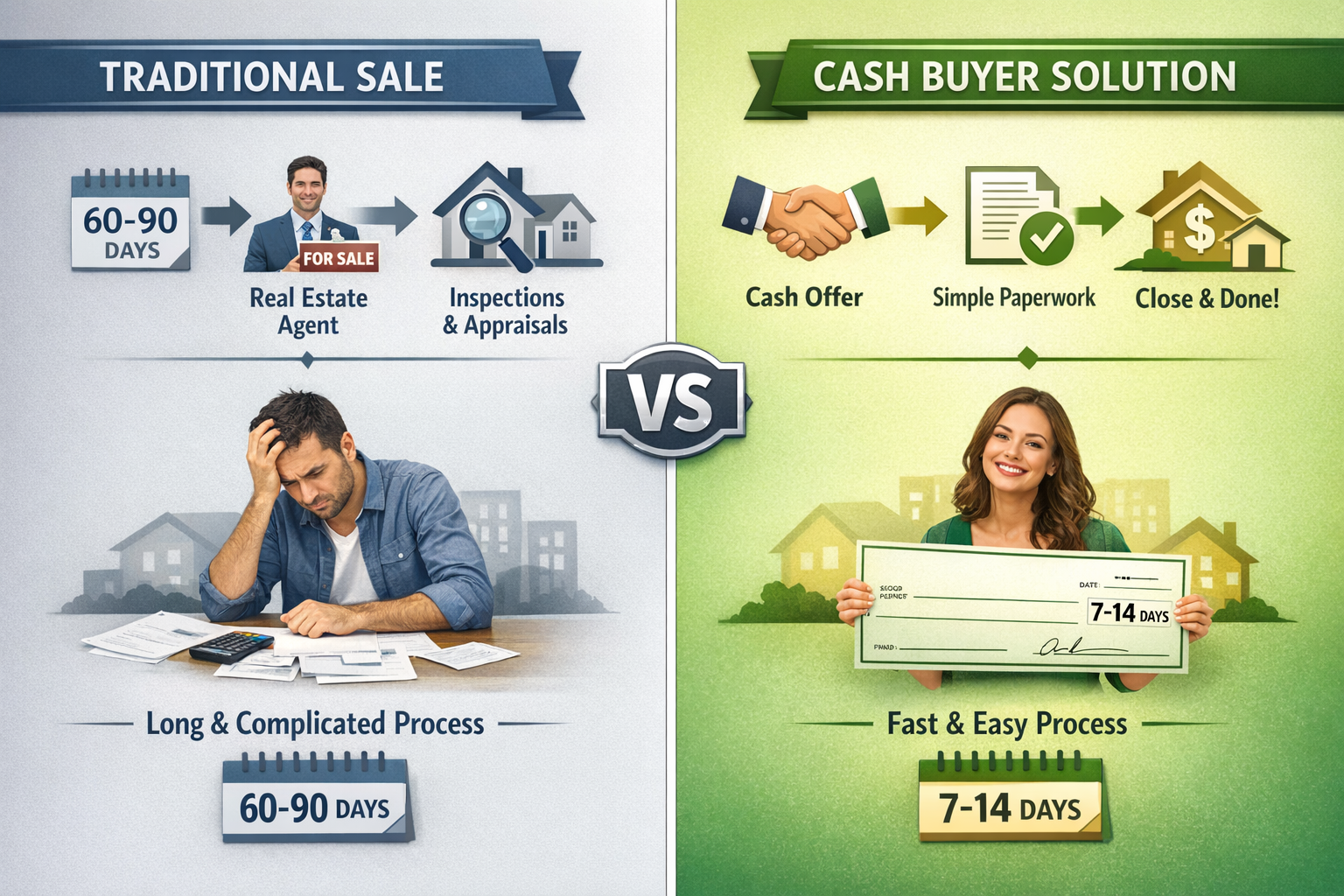

Option 1: Traditional Sale with Lien Payoff at Closing

How it works: List your house with a real estate agent, accept an offer, and use sale proceeds to pay off all liens at closing.

Best for:

- Properties with sufficient equity to cover all liens plus selling costs

- Sellers who can wait 60-90+ days for closing

- Situations where maximum sale price is the priority

The process:

- Order a title search to identify all liens

- Request payoff statements from all lienholders

- Calculate net proceeds (sale price minus liens, mortgage, and costs)

- List the property with full disclosure of liens

- Accept an offer and open escrow

- Title company coordinates payoffs from sale proceeds

- Liens are paid and released at closing

- You receive remaining equity (if any)

Pros:

- Potentially highest sale price through market exposure

- Established process familiar to agents and title companies

- No out-of-pocket payment required if equity exists

Cons:

- Lengthy timeline (typically 60-120 days)

- Requires sufficient equity to cover all debts

- Buyers may be scared off by lien complications

- Agent commissions reduce net proceeds (typically 5-6%)

💡 Pro tip: Get payoff statements early in the process. Lien amounts can include interest and penalties that grow daily, so accurate current figures prevent closing surprises.

Option 2: Sell to Cash Buyers Who Handle Liens

How it works: Specialized cash buyers purchase properties with liens, coordinating payoffs as part of the transaction.

Best for:

- Sellers needing to close quickly (7-14 days typical)

- Properties with complex lien situations

- Situations where traditional financing might fall through

- Owners who want certainty and simplicity

The process:

- Contact cash buyer and provide property details

- Receive cash offer (usually within 24-48 hours)

- Cash buyer orders title search and verifies liens

- Buyer coordinates with lienholders for payoff amounts

- Review settlement statement showing all payoffs

- Close at title company (typically 7-14 days)

- Buyer pays off liens from purchase funds

- You receive net proceeds immediately

Pros:

- Fast closing (as quick as 7 days)

- No repairs or improvements needed

- Buyer handles lien complexity and coordination

- Certainty—cash offers don’t fall through like financed deals

- No agent commissions

- Expert service from industry experts who handle these situations daily

Cons:

- Offer price typically 70-85% of market value

- Lower net proceeds compared to perfect-condition market sale

When this makes sense: If you need speed, certainty, or have multiple liens creating complexity, cash buyers provide helpful solutions that traditional sales can’t match.

Companies like Sure Path Property Solutions specialize in these exact situations, offering friendly and caring service while navigating the technical details. Our expert service includes coordinating with counties, lienholders, and title professionals to create clear pathways forward.

Option 3: Negotiate Lien Settlements

How it works: Contact lienholders directly to negotiate reduced payoff amounts, then sell the property.

Best for:

- Older liens where creditors may accept less

- Judgment liens from creditors willing to negotiate

- Situations where you have some cash to offer but not full amount

- Properties where equity exists but is tight

Negotiation strategies:

For tax liens: Government agencies sometimes accept:

- Installment payment plans

- Offers in compromise (paying less than owed)

- Penalty and interest waivers

- Subordination (moving behind in priority)

Our guide on negotiating tax lien payoffs provides proven strategies and specific approaches.

For judgment liens: Private creditors may accept:

- Lump sum settlements (often 40-70% of balance)

- Structured payment plans

- Trade-offs (release lien for other considerations)

For mechanics liens: Contractors might accept:

- Partial payment to release lien

- Payment plans with lien release upon completion

- Settlement to avoid costly litigation

Pros:

- Can significantly reduce total debt

- Creates pathway when equity is insufficient

- Avoids bankruptcy or foreclosure

- Preserves some proceeds for you

Cons:

- Requires negotiation skills and persistence

- Not all creditors will negotiate

- Can be time-consuming (30-90+ days)

- May require some upfront cash

- Settled debts may have tax consequences (forgiven debt = taxable income)

💡 Pro tip: Always get settlement agreements in writing before making payment, and ensure the agreement includes specific language about lien release and recording the release.

Option 4: Short Sale When Liens Exceed Value

How it works: When total liens exceed property value, negotiate with lienholders to accept less than owed from sale proceeds.

Best for:

- Properties “underwater” (debts exceed value)

- Avoiding foreclosure or bankruptcy

- Situations where walking away isn’t an option

The short sale process:

- Determine property value through appraisal or BPO

- Calculate total liens and shortfall amount

- Find a buyer willing to wait for approval

- Submit short sale package to all lienholders showing:

- Financial hardship documentation

- Property value evidence

- Purchase offer

- Settlement statement showing distribution

- Negotiate with each lienholder for approval

- Obtain written approval from all parties

- Close the sale with approved terms

Pros:

- Avoids foreclosure and its credit impact

- Resolves debt without bankruptcy

- Lienholders often forgive remaining balance

- Less damaging to credit than foreclosure

Cons:

- Lengthy process (often 90-180+ days)

- Requires all lienholders to agree

- You typically receive no proceeds

- Significant credit score impact (though less than foreclosure)

- Forgiven debt may be taxable income

- Not all lienholders will approve

Success factors: Short sales work best when you can demonstrate genuine hardship and when the alternative (foreclosure) would net lienholders even less money.

For properties facing foreclosure, explore our guide on selling houses fast to avoid foreclosure for additional emergency options.

Option 5: Pay Liens from Other Sources Before Selling

How it works: Use savings, loans, or other resources to pay liens before listing, then sell with clear title.

Best for:

- Situations where liens are relatively small

- When clear title will significantly increase sale price

- Sellers with access to funds or credit

- Properties where lien clouds prevent financing

Funding sources:

- Personal savings or emergency funds

- Personal loans from banks or credit unions

- Home equity line of credit (if available)

- Loans from family members

- 401(k) loans (use cautiously—has consequences)

- Sale of other assets

Pros:

- Simplifies sale process dramatically

- Attracts more buyers and better offers

- Faster closing without lien complications

- You control the timeline

Cons:

- Requires significant upfront cash

- Risk if sale falls through or takes longer than expected

- May deplete emergency savings

- Interest costs on borrowed funds

When this makes sense: Small liens (under $5,000-$10,000) that create disproportionate complications may be worth paying upfront if you have the resources and expect the cleared title to increase sale price or speed significantly.

Special Lien Situations and Solutions

Some lien types require specialized approaches and understanding.

Selling with Tax Liens (IRS and State)

Tax liens are particularly challenging because government agencies have powerful collection tools and high priority.

Federal tax liens: The IRS may issue a Certificate of Discharge (Form 14135) that removes the lien from your specific property if:

- Sale proceeds will fully pay the lien

- The government’s interest is protected

- It facilitates collection of the tax debt

State tax liens: Similar to federal liens but governed by state law. Some states are more flexible in negotiating than others.

Key strategies:

- Request payoff statements early (amounts change daily with interest)

- Explore IRS Offer in Compromise programs

- Consider installment agreements that allow sale to proceed

- Work with tax professionals who understand lien discharge procedures

Our comprehensive guide on selling houses with tax liens provides detailed strategies and state-specific considerations.

For properties with significant tax debt, cash buyers who specialize in tax lien properties can provide turnkey solutions.

Selling with Judgment Liens

Judgment liens result from court-ordered debts—credit cards, medical bills, personal loans, or lawsuit damages.

Important characteristics:

- Attach to all real property in the county where recorded

- Typically remain for 10-20 years (varies by state)

- Accrue interest at statutory rates

- Can be renewed/extended in many states

Resolution options:

- Pay in full from sale proceeds

- Negotiate settlement (creditors often accept 50-70%)

- Challenge the judgment if procedural errors occurred

- Wait for expiration (if timeline works)

- Sell to investors who buy houses with judgment liens and handle the complexity

Negotiation leverage: Judgment creditors know that:

- Bankruptcy could eliminate the debt entirely

- Collection is uncertain and expensive

- A settlement today is better than maybe collecting later

This creates room for negotiation, especially on older judgments.

Selling with Mechanics/Contractor Liens

Mechanics liens protect contractors, subcontractors, and suppliers who provided labor or materials.

Critical timeframes:

- Must be filed within 60-120 days of work completion (varies by state)

- Expire after 1-2 years if not enforced through foreclosure

- Can be invalidated if filing procedures weren’t followed exactly

Resolution strategies:

- Verify the lien is valid (many have technical defects)

- Negotiate with contractor (they often prefer settlement to litigation)

- Bond around the lien (insurance company guarantees payment)

- Contest in court if work was defective or lien is fraudulent

- Pay from sale proceeds if amount is reasonable

Common defenses:

- Improper notice procedures

- Work wasn’t authorized

- Lien amount exceeds actual value provided

- Missed filing deadlines

💡 Pro tip: Contractors often file inflated liens knowing they’ll negotiate down. Don’t assume the filed amount is the real settlement number.

Selling with HOA Liens

Homeowners association liens arise from unpaid dues, assessments, or fines.

Super-priority status: Some states give HOA liens priority over even first mortgages for certain amounts (typically 6-12 months of dues). This means the HOA gets paid before your mortgage lender.

Resolution approaches:

- Pay current to avoid additional penalties

- Negotiate payment plans

- Challenge improper fees or fines

- Include payoff in sale closing

- Work with cash buyers experienced in HOA lien situations

Warning: HOAs can foreclose relatively quickly in many states, sometimes in as little as 90 days. Don’t ignore these liens.

The Step-by-Step Process: Selling a House with a Lien Against It

Regardless of which option you choose, follow this systematic approach:

Step 1: Identify All Liens (Complete Title Search)

Don’t rely on memory—get a professional title search that reveals:

- All recorded liens (public record)

- Lien amounts and recording dates

- Lienholder contact information

- Priority order

Cost: $100-$300 for owner’s title search

Timeline: 2-5 business days

Many title companies provide preliminary title reports free when you commit to using them for closing.

Step 2: Request Payoff Statements

Contact each lienholder and request:

- Current payoff amount (principal, interest, penalties, fees)

- Per diem interest rate (daily accrual amount)

- Payoff good-through date

- Payment instructions and requirements

- Lien release procedures

Important: Payoff amounts change daily due to interest. Get statements dated as close to your expected closing as possible.

Step 3: Calculate Your Equity Position

Create a simple calculation:

Estimated Sale Price: $________

Minus:

- Mortgage payoff: $________

- Property tax lien: $________

- Judgment lien: $________

- Mechanics lien: $________

- HOA lien: $________

- Selling costs (6-10%): $________

Equals Net Proceeds: $________

This number determines your strategy:

- Positive equity: Traditional sale or cash buyer

- Minimal equity: Cash buyer or negotiate some liens

- Negative equity: Short sale or settlement negotiations

Step 4: Choose Your Selling Strategy

Based on your equity, timeline, and priorities, select:

- ✅ Traditional listing (maximum price, longer timeline)

- ✅ Cash buyer (speed and certainty)

- ✅ Negotiate settlements first (reduce debt load)

- ✅ Short sale (underwater properties)

- ✅ Hybrid approach (negotiate some, pay others)

Step 5: Execute Your Chosen Strategy

For traditional sales:

- Hire experienced real estate agent

- Disclose all liens in listing and to buyers

- Include lien payoffs in closing calculations

- Coordinate with title company

For cash buyer sales:

- Contact reputable cash buying companies

- Provide property details and lien information

- Review offer and settlement statement

- Schedule quick closing

For negotiations:

- Contact lienholders in writing

- Present settlement offers with documentation

- Get agreements in writing before payment

- Ensure lien releases are recorded

Step 6: Close the Transaction

At closing, the title company:

- Receives purchase funds from buyer

- Pays off liens in priority order

- Obtains lien releases from each creditor

- Records the releases in public records

- Disburses remaining funds to you

- Transfers clear title to buyer

You should receive:

- Final closing statement (HUD-1 or ALTA)

- Copies of all lien releases

- Proof of recording

- Your net proceeds (check or wire)

Step 7: Verify Lien Releases Are Recorded

Don’t assume—verify. After closing:

- Check county records (usually online) to confirm releases are recorded

- Keep copies of all release documents permanently

- Follow up if releases aren’t recorded within 30 days

- Consider ordering a new title search 60 days post-closing for peace of mind

Unrecorded releases can cause problems years later if you’re ever connected to the property.

State-Specific Considerations

Lien laws vary significantly by state. Here are key differences:

Community Property States

In Arizona, California, Idaho, Louisiana, Nevada, New Mexico, Texas, Washington, and Wisconsin:

- Liens against one spouse may attach to community property

- Both spouses may need to consent to lien resolution

- Separate property liens don’t affect community property (generally)

Homestead Protection States

Some states (Florida, Texas, Kansas, others) provide homestead exemptions protecting primary residences from certain judgment liens. This can affect:

- Which liens actually attach to your home

- Negotiating leverage with judgment creditors

- Whether forced sale is possible

HOA Super-Priority States

Nevada, Colorado, and several others give HOAs priority over first mortgages for certain amounts. This dramatically changes negotiating dynamics.

Foreclosure Timeline States

Judicial foreclosure states (slower, court-supervised):

- Florida, New York, New Jersey, Pennsylvania, others

- Timeline: 6-24+ months

Non-judicial foreclosure states (faster, trustee sale):

- California, Texas, Georgia, Arizona, others

- Timeline: 3-6 months

This affects urgency when facing tax or HOA foreclosure.

For Florida-specific guidance, see our detailed article on selling houses with liens in Florida.

Working with Professionals: Who Can Help

Navigating liens requires expertise. Consider building a team:

Real Estate Attorneys

When you need one:

- Complex lien situations with multiple creditors

- Disputed or contested liens

- Short sales requiring legal documentation

- Potential litigation with lienholders

Cost: $200-$500/hour or flat fees for specific services

Tax Professionals (CPAs, Enrolled Agents)

When you need one:

- IRS or state tax liens

- Offer in Compromise applications

- Tax consequences of forgiven debt

- Installment agreement negotiations

Cost: $150-$400/hour or project-based fees

Real Estate Agents Experienced with Liens

Not all agents understand lien complications. Look for:

- Experience with distressed properties

- Knowledge of lien disclosure requirements

- Relationships with investor buyers

- Track record with complicated closings

Cost: Standard commission (5-6% of sale price)

Title Companies and Escrow Officers

Essential for:

- Identifying all liens through title search

- Coordinating payoffs at closing

- Ensuring proper lien releases

- Providing title insurance

Cost: Usually paid from sale proceeds (1-2% of sale price)

Cash Buying Companies (Like Sure Path Property Solutions)

Specialized in:

- Properties with multiple liens

- Tax lien situations

- Quick closings (7-14 days)

- Handling all coordination and paperwork

- Providing trustworthy service and helpful guidance

Cost: Built into purchase price (no separate fees)

The advantage of working with industry experts who handle these situations daily is the peace of mind and simplified process. Companies like Sure Path Property Solutions coordinate with counties, title companies, and lienholders, removing the burden from your shoulders.

Common Mistakes to Avoid

❌ Hiding Liens from Buyers

Why it fails: Title searches reveal everything. Hiding liens:

- Kills deals at closing

- Creates legal liability

- Damages your credibility

- May constitute fraud

Do instead: Disclose everything upfront and position it as “already factored into price.”

❌ Ignoring Lien Notices

Why it’s dangerous: Ignoring liens leads to:

- Foreclosure proceedings

- Increased penalties and interest

- Loss of negotiating opportunities

- Reduced options over time

Do instead: Address liens immediately, even if you can’t pay them now. Communication keeps options open.

❌ Accepting First Lien Payoff Quote

Why it’s costly: Initial payoff quotes often include:

- Inflated interest calculations

- Unnecessary fees

- Penalties that might be waived

- Errors in calculation

Do instead: Review payoff statements carefully, question charges, and negotiate when possible.

❌ Trying to Sell FSBO with Complex Liens

Why it’s risky: For-Sale-By-Owner with liens requires:

- Legal expertise you probably don’t have

- Title company relationships

- Negotiating skills with creditors

- Understanding of closing procedures

Do instead: Use professionals—agents, attorneys, or cash buyers who specialize in problem properties—to navigate complexity.

❌ Waiting Until the Last Minute

Why it backfires: Rushed lien resolution leads to:

- Missed opportunities for negotiation

- Higher interest and penalties

- Forced acceptance of bad terms

- Deal failures at closing

Do instead: Start the process early. Even if you’re not ready to sell immediately, understanding your lien situation creates options.

❌ Assuming All Liens Are Valid

Why it’s wrong: Many liens have defects:

- Improper filing procedures

- Missed deadlines

- Incorrect amounts

- Expired enforcement periods

Do instead: Have an attorney review liens for validity, especially mechanics liens and older judgments.

Frequently Asked Questions

Can I sell my house if I have a lien on it?

Yes, absolutely. Liens don’t prevent sales—they just require resolution (payment, settlement, or buyer acceptance) before or at closing. Thousands of houses with liens sell successfully every year.

Will a lien stop me from getting a buyer?

Not necessarily. Cash buyers and investors regularly purchase properties with liens. Traditional buyers using financing may be more hesitant, but proper disclosure and pricing can attract buyers willing to wait for lien resolution.

How long does it take to sell a house with a lien?

Timeline varies by method:

- Cash buyers: 7-14 days

- Traditional sale with simple lien: 60-90 days

- Short sale with multiple liens: 90-180+ days

- Sales requiring negotiated settlements: 45-120 days

Do I need to pay the lien before listing?

No. Most liens are paid from sale proceeds at closing. However, paying small liens upfront can simplify the process and attract more buyers.

What if the lien amount is more than my house is worth?

You have options:

- Short sale (negotiate with lienholders to accept less)

- Deed in lieu of foreclosure

- Bankruptcy (consult attorney)

- Sell to cash buyer who negotiates with lienholders

For properties with tax debt exceeding value, our guide on selling houses with tax debt provides specific strategies.

Can a buyer assume my liens?

Rarely. Most lienholders won’t agree to transfer liens to a new owner. Exceptions might include assumable mortgages or specific negotiated agreements, but these are uncommon.

What happens if I can’t pay off all the liens?

Options include:

- Negotiate settlements for less than owed

- Short sale with lienholder approval

- Bring cash to closing to cover shortfall

- Sell to investor who handles complex payoffs

How do I find out what liens are on my property?

- Order a title search from a title company ($100-$300)

- Check county recorder’s office (often online)

- Review your property tax records

- Contact a title company for preliminary report

Will selling with a lien hurt my credit?

The sale itself doesn’t hurt credit. However:

- Unpaid liens already damage credit

- Short sales impact credit (less than foreclosure)

- Settled liens may show as “settled for less than owed”

- Paying liens in full through sale proceeds helps credit

Why Sure Path Property Solutions Is Your Best Partner

When you’re facing the stress of selling a house with a lien against it, you need more than just a buyer—you need a partner who understands the complexity and provides helpful solutions.

Our Expert Service Includes:

✅ Free property evaluation within 24-48 hours

✅ Coordination with all lienholders to obtain payoffs

✅ Work with counties and title professionals to resolve complications

✅ Cash offers that account for lien payoffs

✅ Fast closings (7-14 days typical)

✅ No repairs, cleaning, or improvements required

✅ Friendly and caring approach to stressful situations

✅ Trustworthy service from industry experts with proven track records

Our Process Is Simple:

- Contact us with your property details and lien situation

- We research all liens and calculate payoffs

- You receive a fair cash offer accounting for all debts

- We coordinate everything with lienholders and title company

- You close quickly and walk away with your net proceeds

We’ve helped hundreds of homeowners navigate complicated situations—from multiple liens to tax problems to inherited properties with unclear title. We provide helpful guidance every step of the way.

Take Action Today: Your Next Steps

Selling a house with a lien against it doesn’t have to be overwhelming. Here’s what to do right now:

Immediate Actions (Today):

- Order a title search to identify all liens

- Request payoff statements from known lienholders

- Calculate your equity position using the formula above

- Contact Sure Path Property Solutions for a free consultation and cash offer

This Week:

- Review your options based on equity and timeline

- Consult with professionals (attorney, tax advisor, or cash buyer)

- Develop your strategy for lien resolution

- Begin negotiations if pursuing settlements

This Month:

- Execute your chosen strategy (list, accept cash offer, or negotiate)

- Coordinate with title company for closing

- Verify lien releases are properly recorded

- Move forward with your life, free from the burden

Conclusion: You Have More Options Than You Think

Discovering liens on your property can feel like a crisis, but it’s a challenge with clear solutions. Whether you have sufficient equity for a traditional sale, need the speed and certainty of a cash buyer, or face complex negotiations with multiple lienholders, selling a house with a lien against it is absolutely achievable.

The key is taking action rather than hoping the problem disappears. Liens don’t go away on their own—they grow larger with interest and penalties. But with the right approach and helpful guidance from industry experts, you can resolve these obligations and move forward.

Remember these core principles:

- Liens complicate sales but don’t prevent them

- Full disclosure protects you legally and builds buyer trust

- Professional help saves time, money, and stress

- Multiple pathways exist—choose the one that fits your situation

- Speed often works in your favor (less interest accrual, fewer complications)

At Sure Path Property Solutions, we’ve built our reputation on providing trustworthy service and expert solutions for exactly these situations. We understand the stress you’re facing, and we’re here to help with friendly and caring support backed by deep expertise.

Don’t let liens keep you trapped in a property you need to sell. Contact us today for a free, no-obligation consultation and cash offer. We’ll review your specific situation, explain your options clearly, and provide a straightforward path forward.

Your fresh start is closer than you think. Let’s make it happen together.