Imagine discovering the perfect opportunity to sell your land, only to realize there’s a lien attached to the property. Your heart sinks as questions flood your mind: Can the sale still happen? Will buyers run away? What happens to the debt? Here’s the good news—Can You Sell Land with a Lien on It? Process & Options exist that make it entirely possible to move forward, even with this complication.

Selling land with a lien isn’t just possible—it happens every day across the country. Whether you’re dealing with tax liens, judgment liens, or contractor claims, understanding your options transforms what seems like an impossible situation into a manageable process. The key lies in knowing how liens work, what buyers expect, and which strategies align with your specific circumstances.

Key Takeaways

- Yes, you can sell land with a lien—liens don’t prevent sales, but they must be addressed during the transaction process

- Liens typically get paid from sale proceeds at closing, protecting both buyer and seller through escrow arrangements

- Multiple options exist including traditional sales with lien payoff, cash buyer transactions, lien negotiation, and subordination agreements

- Professional guidance makes the difference—working with experienced professionals helps navigate title issues and coordinate with lien holders

- Time and transparency are your allies—early disclosure and proper planning lead to smoother transactions and better outcomes

Understanding Property Liens and How They Affect Land Sales

A lien represents a legal claim against your property, giving a creditor the right to receive payment from the property’s sale proceeds. Think of it as a financial “bookmark” that stays with the property until the debt gets satisfied. When someone places a lien on land, they’re essentially saying, “This property owes me money, and I have a legal right to collect.”

What Is a Property Lien?

Property liens come in two main categories: voluntary liens and involuntary liens. Voluntary liens occur when property owners agree to them, such as mortgages taken out to purchase land. Involuntary liens happen without the owner’s consent—tax liens, judgment liens, and mechanic’s liens fall into this category.

Here’s what makes liens particularly important for land sales:

- They attach to the property, not just the owner

- They create a cloud on the title, making it difficult to transfer clean ownership

- They follow a priority order, determining which creditors get paid first

- They remain public record, visible to potential buyers and their lenders

Common Types of Liens on Land

Understanding the specific type of lien affecting your property helps determine the best approach for selling. Each lien type carries different implications, priority levels, and resolution strategies.

Tax Liens 🏛️

Tax liens typically hold the highest priority and include:

- Property tax liens from county or municipal governments

- Federal tax liens from the IRS

- State tax liens for unpaid income or business taxes

These liens demand immediate attention because government entities have powerful collection rights. The good news? Many jurisdictions offer payment plans and settlement options that make resolution more manageable.

Judgment Liens ⚖️

When someone sues and wins a monetary judgment, they can place a judgment lien on property to secure payment. These liens arise from:

- Unpaid credit card debts

- Personal loans in default

- Business disputes

- Divorce settlements

Mechanic’s Liens 🔨

Contractors, subcontractors, and material suppliers can file mechanic’s liens when they don’t receive payment for work performed on the property. These liens protect workers and suppliers but can complicate sales significantly.

Mortgage Liens

Existing mortgages represent the most common voluntary liens. When selling land with a mortgage, the lender must be paid from the sale proceeds or agree to release the lien.

How Liens Impact Your Ability to Sell

Liens don’t prevent you from listing or marketing your land, but they create obstacles that must be addressed before closing. Here’s the reality: most buyers and their lenders require clear title before completing a purchase.

The impact varies based on several factors:

| Factor | Impact on Sale |

|---|---|

| Lien Amount | Small liens relative to property value are easier to handle; large liens may exceed equity |

| Lien Type | Tax liens require immediate resolution; other liens may allow negotiation |

| Buyer Type | Cash buyers offer more flexibility; financed buyers face lender requirements |

| Available Equity | Positive equity allows lien payoff at closing; negative equity requires alternative solutions |

“A lien doesn’t mean you’re stuck with the property forever. It simply means you need a clear plan for addressing the debt as part of the sale process.” — Real Estate Title Expert

The encouraging news? With helpful guidance and the right approach, liens become manageable obstacles rather than insurmountable barriers. The key lies in understanding your specific situation and exploring all available options.

Can You Sell Land with a Lien on It? The Direct Answer

Yes, you absolutely can sell land with a lien on it. This straightforward answer brings relief to many property owners facing complicated situations. The process requires coordination, transparency, and proper handling, but thousands of property owners successfully complete these sales every year.

The Reality of Selling Encumbered Property

Selling land with liens happens more frequently than most people realize. The real estate market accommodates these transactions through established systems designed to protect all parties involved. The critical factor isn’t whether you can sell—it’s how you approach the sale.

Think of it like selling a car with an outstanding loan. The loan doesn’t prevent the sale; it simply means the lender must be paid from the sale proceeds. Property liens work similarly, with title companies and closing attorneys coordinating the payoff process.

Legal Requirements and Disclosure Obligations

Transparency forms the foundation of any successful sale involving liens. Most states require sellers to disclose known liens on property disclosure forms. Attempting to hide liens creates legal liability and can derail transactions at closing when title searches reveal the encumbrances.

Mandatory Disclosures Include:

- All known liens against the property

- Approximate amounts owed

- Identity of lien holders

- Any ongoing disputes or litigation

Honest disclosure actually helps sales succeed. Buyers appreciate transparency, and many remain willing to proceed when they understand how liens will be resolved. Professional buyers and investors often specialize in properties with title issues, viewing them as opportunities rather than problems.

Buyer Expectations and Title Requirements

Understanding what buyers need helps sellers prepare effectively. Most purchase agreements include contingencies requiring the seller to deliver “marketable title” at closing. This means the title must be free from liens and encumbrances—or the buyer must specifically agree to accept certain liens.

Traditional Buyer Requirements:

- Clear title with all liens removed at or before closing

- Title insurance protecting against undisclosed claims

- Proof that all lien holders will be satisfied from sale proceeds

- Proper documentation of lien releases

Cash Buyer Flexibility:

Cash buyers, particularly those who work with properties facing challenges, often offer more flexibility. They may:

- Purchase with liens in place and handle resolution themselves

- Negotiate reduced prices accounting for lien amounts

- Close faster with fewer contingencies

- Accept properties that traditional buyers won’t consider

Companies like Sure Path Property Solutions specialize in helping property owners navigate these exact situations, providing expert service and helpful solutions when traditional sales seem impossible.

The Role of Title Companies and Escrow

Title companies serve as neutral third parties coordinating lien payoffs during closing. They perform several critical functions:

- Conduct thorough title searches identifying all liens and encumbrances

- Calculate exact payoff amounts by contacting lien holders

- Hold funds in escrow ensuring proper distribution

- Coordinate lien releases obtaining satisfaction documents

- Issue title insurance protecting the new owner

This system protects everyone involved. Buyers receive clear title, sellers satisfy their obligations, and lien holders receive payment—all coordinated through a single closing transaction.

The escrow process works like this:

Sale Proceeds → Escrow Account → Priority Order Payoffs → Remaining Funds to Seller

Priority Order Typically Follows:

- Property tax liens (highest priority)

- First mortgage or deed of trust

- Second mortgages or home equity loans

- Federal tax liens

- State tax liens

- Judgment liens (by recording date)

- Mechanic’s liens

Understanding this priority order helps sellers calculate how much they’ll receive after all liens are satisfied. Sometimes the math works favorably; other times, creative solutions become necessary.

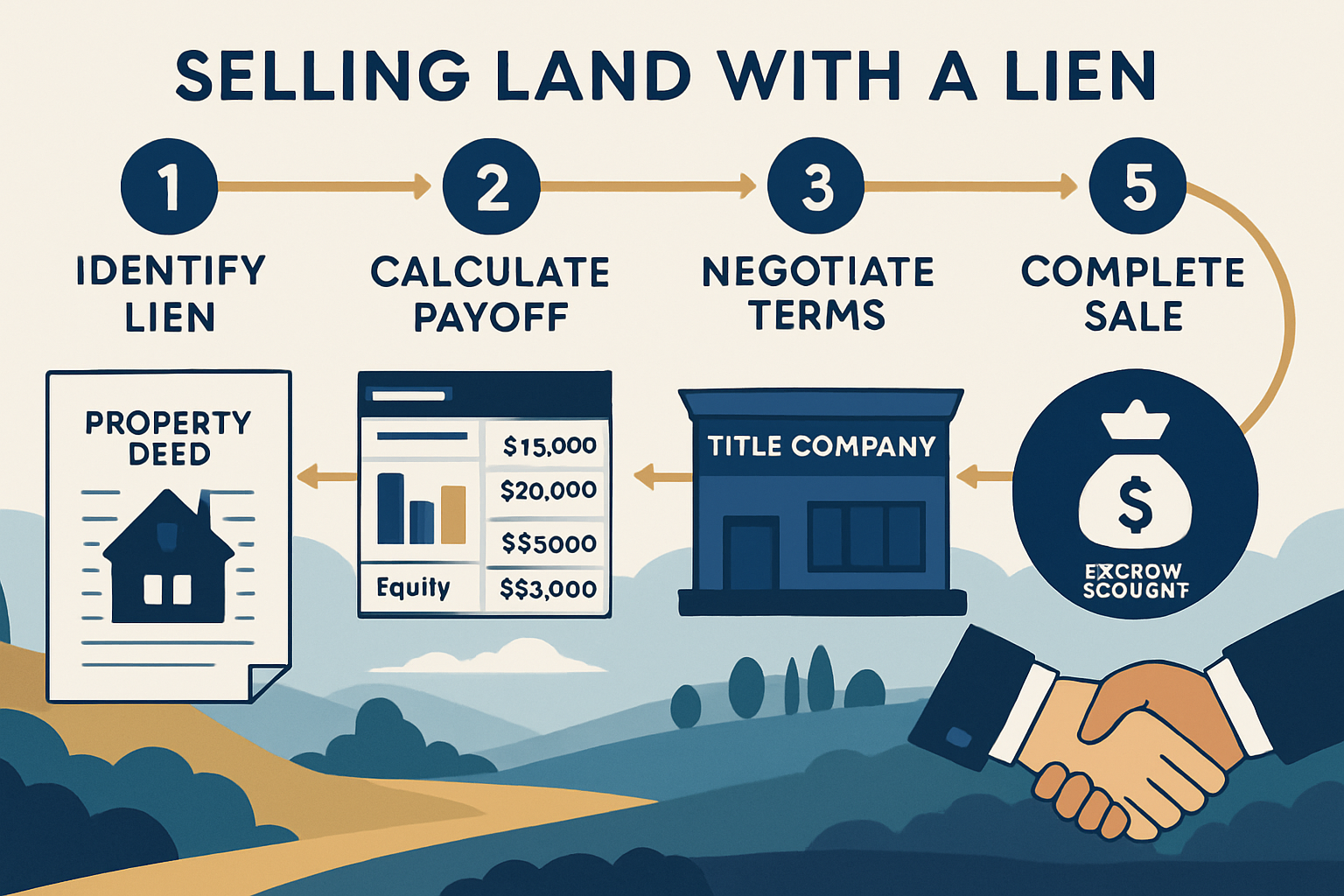

Step-by-Step Process for Selling Land with a Lien

Navigating the sale of land with liens requires a systematic approach. Following these steps helps ensure nothing gets overlooked and maximizes the chances of a successful transaction.

Step 1: Identify All Liens on Your Property

Before marketing your land, you need a complete picture of all claims against it. Surprises at closing create delays and complications, so thorough research upfront pays dividends.

How to Find Liens:

- County Recorder’s Office: Visit or search online databases for recorded liens

- Tax Assessor’s Office: Check for unpaid property taxes

- Title Company: Order a preliminary title report (often free when listing with an agent)

- Credit Report: Review for judgments that may have become property liens

- Personal Records: Gather documentation of known debts and legal actions

Many counties now offer online property records searches, making this process easier than ever. Look for documents recorded against your property’s legal description or parcel number.

Step 2: Determine the Total Lien Amount and Payoff Terms

Once you’ve identified all liens, contact each lien holder to obtain current payoff information. Lien amounts can increase over time due to interest, penalties, and fees, so the original amount may not reflect what’s currently owed.

Information to Gather:

- Current principal balance

- Accrued interest and calculation method

- Daily interest rate (per diem)

- Administrative fees or penalties

- Payoff good-through date

- Payment instructions and requirements

- Lien release process and timeline

Create a spreadsheet tracking this information for all liens. This becomes your roadmap for the sale process and helps calculate your net proceeds.

Sample Lien Summary:

| Lien Type | Holder | Original Amount | Current Payoff | Priority | Notes |

|---|---|---|---|---|---|

| Property Tax | County | $8,500 | $9,200 | 1st | Includes 2023-2024 |

| Judgment | ABC Credit | $12,000 | $14,300 | 3rd | 6% annual interest |

| Mechanic’s | XYZ Contractors | $6,000 | $6,450 | 4th | Negotiable |

Step 3: Calculate Your Property’s Equity Position

Understanding your equity position determines which selling options make sense. Equity equals your property’s market value minus all liens and selling costs.

Equity Calculation Formula:

Market Value - Total Liens - Selling Costs = Net Equity

Example Scenario:

- Estimated Market Value: $75,000

- Total Liens: $29,950

- Selling Costs (6% commission + closing): $5,250

- Net Equity: $39,800

This positive equity position offers multiple selling options. However, if liens exceed the property’s value (negative equity), different strategies become necessary.

Step 4: Explore Your Selling Options

With complete information about liens and equity, you can evaluate which approach best fits your situation. Each option carries different advantages, timelines, and outcomes.

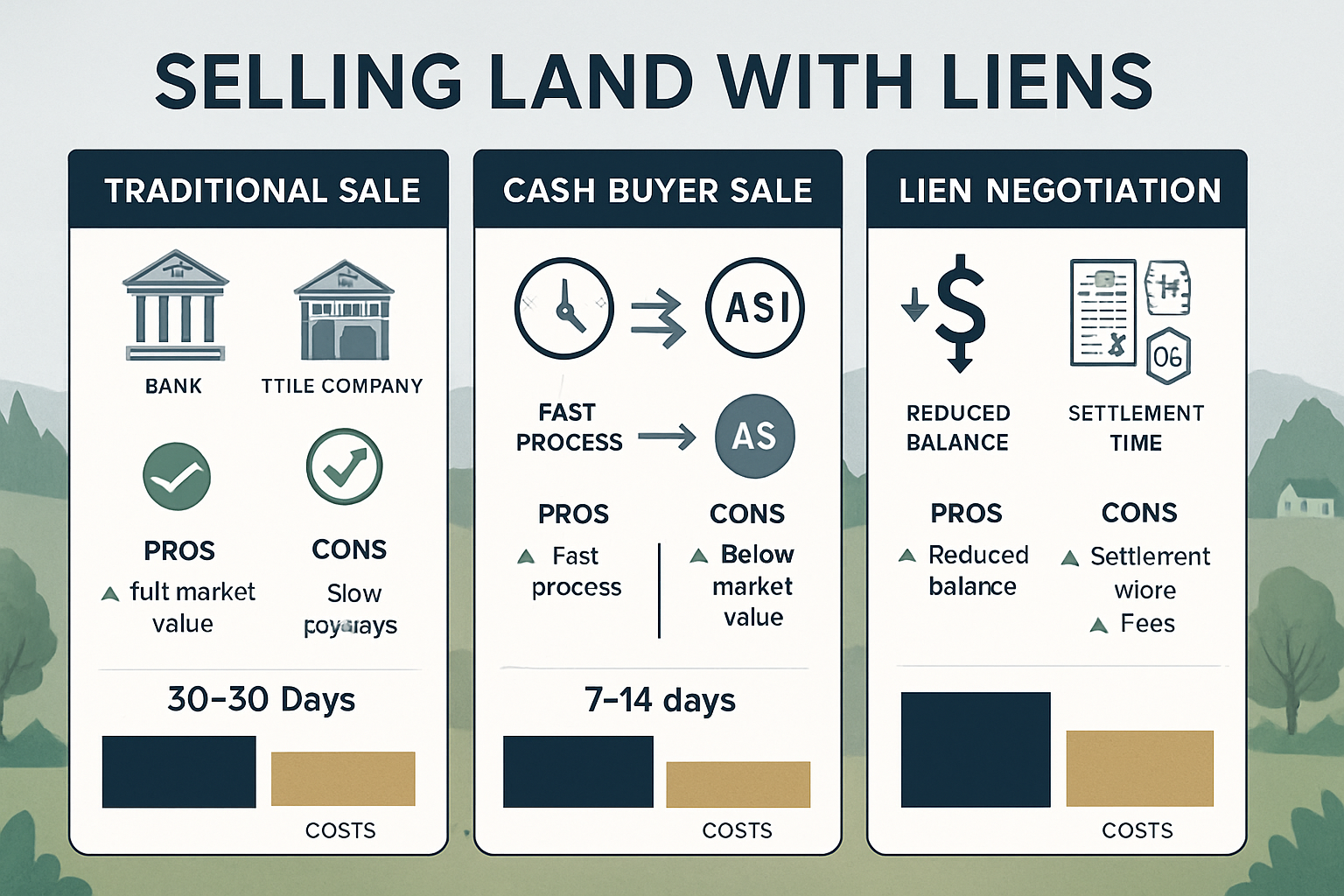

Option A: Traditional Sale with Lien Payoff at Closing

This standard approach works well when you have positive equity and time to market the property properly.

Process:

- List with a real estate agent or sell by owner

- Disclose all liens to potential buyers

- Accept an offer contingent on clear title

- Use sale proceeds to pay liens at closing

- Receive remaining equity after all obligations

Best for: Properties with substantial equity, sellers who want maximum sale price, situations with straightforward liens

Option B: Sell to a Cash Buyer or Investor

Cash buyers specializing in properties with complications offer speed and simplicity. They understand liens and often handle the resolution process themselves.

Advantages:

- ✅ Faster closing (often 7-14 days)

- ✅ Fewer contingencies and inspections

- ✅ No financing fall-through risk

- ✅ Buyer may handle lien negotiations

- ✅ Sell property “as-is” condition

Considerations:

- Offer price typically below retail market value

- Must verify buyer’s legitimacy and funds

- Understand all terms before signing

Working with established companies that help property owners facing challenges provides trustworthy service and peace of mind during the process.

Option C: Negotiate Lien Reduction or Settlement

Some lien holders accept less than the full amount owed, particularly for older debts or when collection seems unlikely. This strategy can improve your equity position significantly.

Negotiation Opportunities:

- Judgment liens: Creditors may settle for 40-70% of balance

- Medical liens: Often negotiable, especially older debts

- Contractor liens: May settle to avoid legal costs

- Tax liens: Some jurisdictions offer hardship programs

Negotiation Tips:

- Document financial hardship if applicable

- Make lump-sum settlement offers

- Get agreements in writing before paying

- Request lien release documents upfront

- Consider professional negotiators for large amounts

Option D: Lien Subordination Agreements

In some cases, lien holders agree to subordinate (lower) their priority position, allowing other liens to be paid first. This advanced strategy requires sophisticated negotiation but can make deals work when equity is tight.

Step 5: Work with Professionals Who Understand Liens

Attempting to navigate lien sales alone increases risks and complications. The right professionals provide helpful guidance and coordinate the complex moving parts.

Essential Team Members:

- Real Estate Attorney: Reviews contracts, negotiates with lien holders, ensures legal compliance

- Title Company: Conducts searches, coordinates payoffs, issues insurance

- Real Estate Agent (if using): Markets property, manages buyer negotiations

- Tax Professional: Advises on tax implications of sale and debt forgiveness

- Specialized Property Buyer: Offers direct purchase solutions for complicated situations

Companies specializing in properties with liens and title issues bring industry experts who handle these situations daily. Their experience navigates obstacles that might derail transactions for general practitioners.

Step 6: Prepare Necessary Documentation

Organization accelerates the process and prevents delays. Gather these documents before listing or accepting offers:

Required Documentation:

- ✔️ Property deed and legal description

- ✔️ Current property tax statements

- ✔️ All lien documentation and payoff letters

- ✔️ Survey or plat map (if available)

- ✔️ HOA documents (if applicable)

- ✔️ Disclosure forms completed honestly

- ✔️ Proof of identity and ownership authority

For Inherited Property:

If you’ve inherited property with liens, additional documentation proves your authority to sell:

- Death certificate

- Will or trust documents

- Letters testamentary or administration

- Heir affidavits

- Probate court orders (if required)

Step 7: Navigate the Closing Process

Once you’ve accepted an offer, the closing process begins. Understanding the timeline and requirements prevents surprises.

Typical Timeline:

Days 1-7: Title search and examination

- Title company identifies all liens

- Obtains payoff statements

- Discovers any additional encumbrances

Days 8-21: Contingency period

- Buyer conducts due diligence

- Lien payoff amounts finalized

- Any issues addressed or negotiated

Days 22-30: Closing preparation

- Final walkthrough (if applicable)

- Closing documents prepared

- Funds wired to escrow

- Lien payoff confirmations obtained

Day 30+: Closing day

- Documents signed

- Funds distributed to lien holders

- Lien releases recorded

- Remaining proceeds to seller

- Deed transferred to buyer

The title company coordinates most of these activities, but staying informed and responsive keeps things moving smoothly.

Step 8: Ensure Proper Lien Release and Recording

The transaction isn’t complete until all lien releases are properly recorded. This protects you from future claims and ensures the buyer receives clear title.

Post-Closing Requirements:

- Verify all lien holders received payment

- Obtain satisfaction/release documents for each lien

- Ensure releases are recorded with county recorder

- Keep copies of all release documents permanently

- Obtain title insurance policy (buyer’s responsibility, but verify)

Some lien releases take weeks to process. The title company typically handles follow-up, but maintain copies of all documentation for your records.

Alternative Strategies When Traditional Sales Won’t Work

Sometimes the numbers don’t work for a traditional sale. Perhaps liens exceed the property’s value, or you need to sell faster than the market allows. These alternative strategies provide helpful solutions when conventional approaches fall short.

Selling with Negative Equity: Short Sale Considerations

When liens exceed your land’s market value, a short sale might offer the best path forward. In a short sale, lien holders agree to accept less than the full amount owed, allowing the sale to proceed.

How Short Sales Work:

- Obtain property appraisal or broker price opinion

- Prepare hardship letter explaining your situation

- Submit short sale package to all lien holders

- Negotiate acceptance of reduced payoff

- Close sale with lien holders receiving agreed amounts

- Remaining debt may be forgiven (tax implications apply)

Short Sale Requirements:

- Documented financial hardship

- Property value less than total liens

- All lien holders must agree to terms

- Detailed financial disclosure

- Patience (process takes 3-6 months typically)

While similar to short sales on houses, land short sales can be simpler since there’s no occupancy or condition issues to address.

Owner Financing with Lien Subordination

Creative financing arrangements sometimes solve problems that cash sales cannot. If you find a buyer willing to make payments over time, you might structure a deal where:

- Buyer makes down payment sufficient to satisfy highest-priority liens

- Remaining liens are subordinated to the new buyer’s interest

- Monthly payments gradually satisfy remaining liens

- Title transfers when all obligations are met

This strategy requires sophisticated legal documentation and willing lien holders, but it opens possibilities when traditional financing isn’t available.

Partnering with Investors or Lien Buyers

Specialized investors purchase properties with lien complications, often at significant discounts. While you’ll receive less than market value, you gain:

- Speed: Closings in days or weeks, not months

- Certainty: No financing contingencies or buyer backing out

- Simplicity: Investor handles all lien negotiations and resolutions

- Relief: Immediate resolution of a stressful situation

Deed in Lieu or Strategic Default Considerations

When property has become a burden rather than an asset, alternative exit strategies might make sense:

Deed in Lieu of Foreclosure

If a mortgage represents the primary lien and you’re facing foreclosure, a deed in lieu allows you to voluntarily transfer the property to the lender. This approach:

- Avoids foreclosure on your record

- May eliminate deficiency judgment

- Resolves the situation faster

- Potentially reduces credit impact

Important Considerations:

⚠️ Junior liens may remain your responsibility

⚠️ Tax implications of forgiven debt

⚠️ Impact on future borrowing ability

⚠️ Not all lenders accept deed in lieu offers

Bankruptcy Protection and Property Sales

Bankruptcy provides legal protection while you resolve financial difficulties, including property sales. Both Chapter 7 and Chapter 13 bankruptcy affect how property with liens can be sold:

Chapter 7 Bankruptcy:

- Trustee may sell property to satisfy creditors

- Some liens can be stripped or avoided

- Exemptions may protect equity

- Process typically takes 4-6 months

Chapter 13 Bankruptcy:

- Repayment plan addresses liens over 3-5 years

- You retain property while making payments

- Some liens can be reduced to property value

- Requires steady income to fund plan

Bankruptcy represents a serious decision with long-term consequences. Consult with a qualified bankruptcy attorney before proceeding, as it may not be necessary if other solutions exist.

Common Challenges and How to Overcome Them

Even with the best planning, selling land with liens presents obstacles. Understanding common challenges and their solutions helps you navigate the process with confidence.

Challenge 1: Unknown or “Surprise” Liens Discovered During Title Search

The Problem:

Title searches sometimes reveal liens you didn’t know existed—old judgments, tax liens from previous owners, or contractor claims that weren’t properly disclosed.

Solutions:

- Dispute invalid liens: If a lien was improperly filed or already satisfied, file a dispute with the county recorder

- Negotiate rapid settlements: Contact lien holders immediately to negotiate quick payoffs

- Extend closing timeline: Request additional time from the buyer to resolve issues

- Adjust purchase price: Negotiate with the buyer to reduce the price by the lien amount

- Title insurance claims: If the lien should have been discovered earlier, title insurance may provide coverage

Prevention Strategy:

Order a preliminary title report early in the process, before accepting offers. This gives you time to address issues without deadline pressure.

Challenge 2: Lien Holder Won’t Cooperate or Respond

The Problem:

Some lien holders are difficult to locate, unresponsive to communication, or refuse to provide payoff information or releases.

Solutions:

- Escalate communication: Use certified mail, phone calls, and email simultaneously

- Involve attorneys: Legal letters often generate faster responses

- File quiet title action: Legal process to clear title when lien holders can’t be located

- Bond around the lien: Purchase a bond that protects the buyer while you resolve the lien

- Use title company resources: Experienced title companies have established contacts and procedures

For particularly stubborn situations, a quiet title action provides a legal remedy, though it adds time and expense to the process.

Challenge 3: Insufficient Equity to Cover All Liens

The Problem:

Your property’s value doesn’t cover all liens plus selling costs, creating negative equity that prevents a traditional sale.

Solutions:

- Bring cash to closing: If you have funds available, pay the difference

- Negotiate lien reductions: Pursue settlements with junior lien holders

- Pursue short sale: Get lien holders to accept less than full payoff

- Sell to specialized buyer: Some investors purchase negative equity properties

- Explore lien discharge programs: Some jurisdictions offer hardship programs

Creative Approach:

Sometimes combining strategies works best—negotiate reduction on one lien while bringing modest cash to closing covers the remaining gap.

Challenge 4: Multiple Lien Holders with Competing Interests

The Problem:

When multiple liens exist, coordinating payoffs and obtaining releases from all parties creates complexity. Lien holders may disagree about priority or payment amounts.

Solutions:

- Establish clear priority order: Work with title company to determine legal priority

- Obtain subordination agreements: Get junior lien holders to agree to payment order

- Use interpleader actions: Legal process where disputed funds are deposited with court

- Negotiate global settlement: Bring all parties together for comprehensive resolution

- Professional mediation: Neutral third party facilitates agreement among lien holders

The title company’s expertise becomes invaluable in these situations, as they handle multi-party closings regularly.

Challenge 5: Buyer Backs Out Due to Lien Complications

The Problem:

Buyers sometimes get cold feet when they learn about liens, even when you have a clear plan to resolve them.

Solutions:

- Educate buyers upfront: Explain how liens will be handled before they make offers

- Provide documentation: Show payoff letters and resolution plan

- Offer price adjustments: Reduce price to account for buyer’s perceived risk

- Target experienced buyers: Work with investors familiar with lien situations

- Consider cash buyers: Eliminate financing contingencies that create additional hurdles

Prevention Strategy:

Full disclosure in marketing materials attracts buyers who understand the situation from the start. This filters out those who won’t proceed and attracts those who will.

Challenge 6: Time-Sensitive Situations (Foreclosure, Tax Sale)

The Problem:

Impending foreclosure or tax sale creates deadline pressure that limits your options.

Solutions:

- Communicate with lien holders: Many will postpone action if a sale is imminent

- Seek emergency buyers: Companies specializing in pre-foreclosure sales can close quickly

- File bankruptcy for automatic stay: Temporarily halts foreclosure while you arrange sale

- Request postponement: Tax authorities often grant extensions when sale is in process

- Accept lower offers: Speed may be worth accepting less than ideal price

When time is critical, working with professionals who understand urgency and have streamlined processes makes all the difference.

Tips for Successfully Selling Land with Liens

Success in selling land with liens comes down to preparation, transparency, and working with the right people. These practical tips increase your chances of a smooth transaction.

Be Transparent About Liens from the Start

Honesty builds trust and prevents deals from falling apart. Disclose all known liens in your marketing materials and initial conversations with buyers. This approach:

- Attracts serious buyers who understand the situation

- Prevents wasted time with buyers who won’t proceed

- Builds credibility and trust

- Reduces legal liability

- Speeds up the due diligence process

Create a simple disclosure statement listing all liens, approximate amounts, and your plan for resolution. Buyers appreciate transparency and respond more positively when they feel informed.

Get Professional Help Early

Don’t wait until problems arise to seek expert assistance. Engaging professionals at the beginning saves time, money, and stress:

- Real estate attorney: Reviews your situation and recommends strategies

- Title company: Conducts preliminary search and identifies all liens

- Tax advisor: Explains tax implications of sale and debt forgiveness

- Experienced real estate professional: Guides you through the process

Companies that specialize in complex property situations bring industry experts who’ve handled hundreds of similar transactions. Their friendly and caring approach combined with technical expertise provides both emotional support and practical solutions.

Understand the True Costs of Selling

Calculate all expenses before committing to a sale strategy. Hidden costs can erode your expected proceeds:

Typical Selling Costs:

- Real estate commissions (5-6% of sale price)

- Title insurance and escrow fees ($500-$2,000)

- Attorney fees ($1,000-$5,000+)

- Recording and transfer fees ($200-$500)

- Property tax prorations

- HOA transfer fees (if applicable)

- Lien payoff fees and interest

- Survey costs (if required)

Cost Comparison Example:

| Sale Price | Commission (6%) | Other Costs | Total Liens | Net to Seller |

|---|---|---|---|---|

| $75,000 | $4,500 | $2,000 | $29,950 | $38,550 |

| $75,000 | $0 (cash buyer) | $1,000 | $29,950 | $44,050 |

This example shows how selling to a cash buyer at a slightly lower price ($70,000) might actually net more money after eliminating commission costs.

Consider Timing and Market Conditions

Market timing affects both sale price and likelihood of success. Consider these factors:

- Seasonal patterns: Land often sells better in spring and summer

- Local market trends: Research recent comparable sales

- Interest rate environment: Higher rates reduce buyer pool

- Economic conditions: Recession impacts land values more than housing

- Development activity: Growing areas command premium prices

However, if you’re facing foreclosure or tax sale deadlines, waiting for perfect market conditions may not be realistic. Sometimes accepting a lower price now beats losing the property entirely.

Know When to Accept a Lower Offer

The “best” offer isn’t always the highest price. Consider these factors when evaluating offers:

Offer Evaluation Criteria:

✅ Certainty of closing: Cash offers with no contingencies provide security

✅ Timeline: Faster closing may be worth accepting less

✅ Buyer qualifications: Pre-approved buyers or proof of funds reduce fall-through risk

✅ Contingencies: Fewer conditions mean smoother process

✅ Buyer experience: Investors familiar with liens create less stress

Example Scenario:

- Offer A: $75,000 with financing contingency, 60-day close, first-time buyer

- Offer B: $68,000 cash, 14-day close, experienced investor, no contingencies

Offer B might be the better choice despite the lower price, especially if liens are accruing interest or you face time pressure.

Document Everything

Maintain organized records throughout the process. Proper documentation protects you legally and facilitates smooth transactions:

Essential Documentation:

- All communications with lien holders (emails, letters, notes from calls)

- Payoff statements with dates and confirmation numbers

- Offers and counteroffers with all amendments

- Inspection reports and disclosures

- Closing statements and settlement documents

- Lien release confirmations

- Proof of recording for all releases

Create a dedicated folder (physical or digital) for the transaction and keep everything together. This organization proves invaluable if questions or disputes arise later.

Plan for Tax Implications

Selling property with liens can create unexpected tax consequences. Consult with a tax professional about:

- Capital gains tax: Profit from sale may be taxable

- Cancellation of debt income: Forgiven debt is often taxable as income

- 1099-C forms: Lien holders may issue these for settled debts

- Insolvency exclusion: May reduce or eliminate tax on forgiven debt

- State tax implications: Rules vary by jurisdiction

Understanding tax consequences before closing prevents surprises at tax time and allows you to set aside appropriate funds.

Why Work with Sure Path Property Solutions

Navigating the sale of land with liens requires expertise, patience, and a network of professional relationships. While you can certainly handle the process independently, working with specialists who understand these complications provides significant advantages.

Specialized Expertise in Complex Property Situations

Sure Path Property Solutions focuses specifically on properties facing challenges that make traditional sales difficult. This specialization means:

- Deep experience with liens, judgments, tax issues, and title problems

- Established relationships with title companies, attorneys, and lien holders

- Proven processes for resolving complications efficiently

- Creative solutions for situations that seem impossible

Rather than being one of many transactions for a general real estate agent, your property receives focused attention from industry experts who handle these situations daily.

Comprehensive Support Throughout the Process

From initial consultation through closing and beyond, comprehensive support makes the journey less stressful:

Initial Consultation:

- Free property evaluation

- Lien assessment and analysis

- Discussion of all available options

- No-pressure guidance on best approach

Transaction Management:

- Coordination with all lien holders

- Title search and resolution

- Documentation preparation

- Timeline management

- Regular communication and updates

Closing Support:

- Ensure all liens are properly satisfied

- Verify recording of releases

- Coordinate fund distribution

- Post-closing follow-up

This helpful guidance transforms an overwhelming process into a manageable series of steps.

Fair, Transparent Offers

When purchasing properties directly, Sure Path Property Solutions provides:

- Honest assessments of property value and lien situations

- Clear explanations of how offers are calculated

- No hidden fees or surprise deductions

- Flexible closing timelines to meet your needs

- As-is purchases requiring no repairs or improvements

The goal isn’t to take advantage of difficult situations but to provide helpful solutions that work for property owners facing challenges.

No Obligation Consultations

Understanding your options costs nothing and creates no obligation. The consultation process:

- Share your situation: Describe the property and liens

- Receive expert analysis: Learn about options and likely outcomes

- Get a fair offer (if direct purchase makes sense)

- Make informed decision: Choose the path that works best for you

Whether you decide to work together or pursue another strategy, you’ll leave the consultation with valuable information and clearer understanding of your situation.

Local Knowledge and National Resources

Combining local market expertise with national resources provides the best of both worlds:

- Understanding of local property values and market conditions

- Relationships with local title companies and attorneys

- Knowledge of county-specific lien processes and requirements

- Access to national buyer networks for maximum exposure

- Connections with specialized lien negotiators and resolution experts

This combination ensures your property receives appropriate local context while benefiting from broader resources and expertise.

Frequently Asked Questions

Can I sell land if I don’t know about all the liens?

Yes, but unknown liens will be discovered during the title search process. This is why ordering a preliminary title report early is so important. Unknown liens don’t prevent sales, but they must be addressed before closing. The title company will identify all recorded liens, and you’ll need to either pay them from proceeds or negotiate their resolution.

What happens if the sale price doesn’t cover all the liens?

You have several options when facing negative equity:

- Bring cash to closing to cover the difference

- Negotiate short sale with lien holders to accept less

- Sell to specialized investor who handles negative equity situations

- Pursue lien reduction through settlement negotiations

- Consider bankruptcy protection if overwhelming debt exists

The best approach depends on your financial situation, the amount of negative equity, and your timeline.

How long does it take to sell land with liens?

Timeline varies significantly based on several factors:

- Cash buyer, simple liens: 7-14 days

- Traditional sale, straightforward liens: 30-60 days

- Complex lien situations: 60-90 days

- Short sales or negotiations: 90-180 days

- Quiet title actions: 6-12 months

Working with experienced professionals and being organized with documentation accelerates the process significantly.

Will selling land with liens hurt my credit?

The sale itself doesn’t hurt your credit—it actually helps by eliminating debt. However:

- Lien settlements for less than full amount may be reported as “settled” rather than “paid in full”

- Short sales may impact credit, though less severely than foreclosure

- Paying liens through sale proceeds generally helps credit by removing negative marks

Consult with a credit counselor if credit impact is a primary concern.

Can I sell land with a tax lien to a family member?

Yes, but proceed carefully. Selling to family members with liens requires:

- Arms-length transaction pricing: Must be fair market value to avoid IRS issues

- Proper documentation: Formal purchase agreement and closing process

- Lien payoff or assumption: Liens must still be addressed

- Gift tax considerations: Below-market sales may trigger gift tax

Using a title company and attorney ensures the transaction is handled properly and protects both parties.

Do all liens have to be paid at closing?

Most liens must be paid or released at closing to provide clear title to the buyer. However, exceptions exist:

- Buyer may agree to take title subject to certain liens

- Liens may be bonded around with title insurance

- Some liens can be subordinated to new financing

- Assumable mortgages may transfer to buyer

The buyer’s lender (if financing) typically requires all liens be cleared. Cash buyers have more flexibility to accept properties with liens intact.

What if a lien holder won’t release the lien after being paid?

This frustrating situation requires persistence:

- Document payment with canceled checks, wire confirmations, or receipts

- Send formal demand for release via certified mail

- Contact title company to leverage their relationships and experience

- File complaint with state attorney general or consumer protection agency

- Pursue legal action to compel release if necessary

- Use title insurance to protect buyer while pursuing release

Most lien holders release promptly when paid, but having title insurance provides protection for the rare exceptions.

Conclusion: Your Path Forward

Discovering liens on your land might feel like hitting a roadblock, but it’s actually just a detour on your path to a successful sale. The question “Can You Sell Land with a Lien on It? Process & Options” has a clear answer: absolutely yes, with the right approach and support.

Key Points to Remember

Throughout this guide, we’ve explored how liens work, the various options available for selling encumbered property, and strategies for navigating common challenges. The most important takeaways include:

🔑 Liens don’t prevent sales—they simply require addressing as part of the transaction

🔑 Multiple pathways exist—from traditional sales with closing payoffs to creative solutions for negative equity situations

🔑 Transparency accelerates success—honest disclosure attracts serious buyers and prevents deals from falling apart

🔑 Professional expertise matters—experienced guidance navigates complications that derail DIY attempts

🔑 Time and preparation are allies—early action provides more options and better outcomes

Taking Action Today

The worst approach to liens is ignoring them and hoping they’ll disappear. They won’t. Instead, take these actionable steps right now:

Immediate Actions (This Week):

- Order a title search to identify all liens on your property

- Contact lien holders to obtain current payoff amounts

- Calculate your equity position to understand available options

- Research property values through recent comparable sales

- Consult with professionals who specialize in lien situations

Short-Term Actions (This Month):

- Develop a resolution strategy based on your equity and timeline

- Begin lien negotiations if settlements seem possible

- Prepare disclosure documents with complete lien information

- Interview potential professionals (agents, attorneys, buyers)

- Make a decision on which selling approach to pursue

Long-Term Commitment:

Stay organized, maintain open communication with all parties, and remain flexible as the process unfolds. Unexpected obstacles may arise, but with persistence and expert support, you’ll navigate them successfully.

You’re Not Alone in This Journey

Thousands of property owners successfully sell land with liens every year. What separates successful sales from failed attempts isn’t luck—it’s preparation, transparency, and working with people who understand the process.

Whether you’re dealing with tax liens, judgment liens, or multiple encumbrances, solutions exist. The complexity of your situation doesn’t determine the outcome—your willingness to take action and seek helpful guidance does.

Ready to Explore Your Options?

If you’re ready to move forward with selling your land, or if you simply want to understand your options better, professional guidance is available. Sure Path Property Solutions specializes in helping property owners navigate exactly these situations.

Get Started Today:

- Free consultation with no obligation or pressure

- Expert analysis of your specific lien situation

- Clear explanation of all available options

- Fair offer if direct purchase makes sense for your situation

Contact Sure Path Property Solutions to discuss your property and discover the best path forward. Whether you ultimately work together or pursue another strategy, you’ll gain valuable insights and a clearer understanding of your options.

Your land with liens isn’t a problem without solutions—it’s an opportunity to work with industry experts who provide trustworthy service, helpful solutions, and the expert guidance you need to move forward with confidence.

Don’t let liens hold you hostage. Take the first step today toward resolving your property situation and moving forward with your life. The path may have obstacles, but with the right support, you’ll navigate them successfully and reach your goal.

Sure Path is a family-owned, curative-title cash buyer. We handle the paperwork and pay what’s owed at closing — no fees, no repairs, no pressure.