Imagine watching the equity in your home disappear like water draining from a bathtub—except this water never stops flowing. You owe more on your mortgage than your house is worth, foreclosure notices are piling up, and traditional real estate agents won’t return your calls. This nightmare scenario affects thousands of homeowners across America in 2026, but there’s a path forward that most people don’t know exists.

When you need to sell underwater house foreclosure: we handle negative equity situations, understanding your options can mean the difference between financial devastation and a fresh start. The combination of being underwater on your mortgage while facing foreclosure creates a perfect storm of stress, but specialized solutions exist for exactly this situation.

Key Takeaways

- Negative equity doesn’t mean you’re trapped: Even when you owe more than your home’s value, multiple exit strategies can help you avoid foreclosure

- Time is your most valuable asset: Acting quickly when facing foreclosure with negative equity opens more doors and preserves more options

- Short sales and cash buyers offer alternatives: These solutions can help you escape foreclosure without waiting for traditional market sales

- Professional guidance simplifies complex situations: Expert service from companies experienced in underwater properties can navigate lender negotiations and title complications

- Foreclosure alternatives protect your financial future: Avoiding foreclosure through strategic property sales minimizes long-term credit damage and potential deficiency judgments

Understanding Underwater Mortgages and Negative Equity

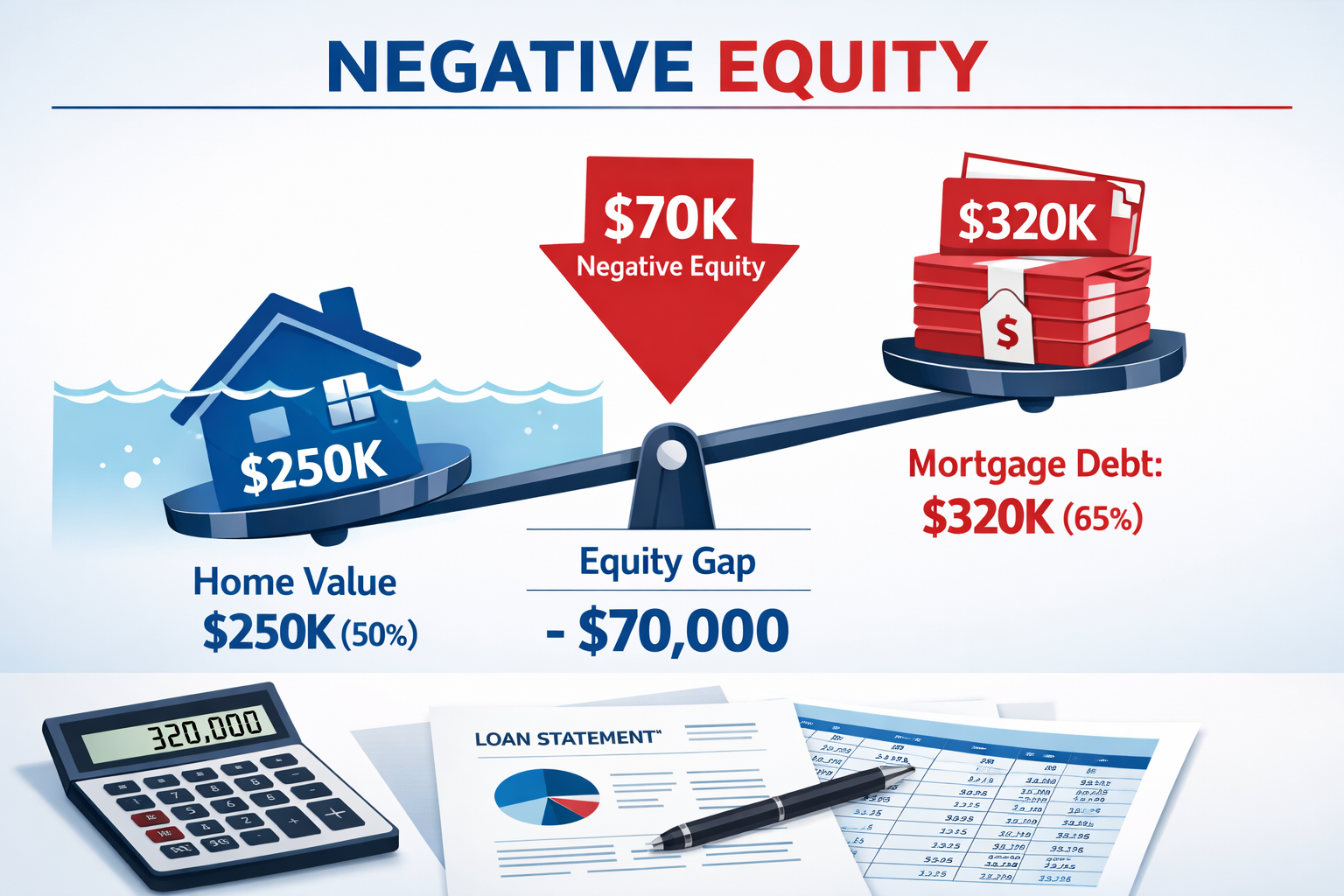

Negative equity occurs when your outstanding mortgage balance exceeds your property’s current market value. Picture a homeowner who purchased a house for $300,000 with a $280,000 mortgage, but the property’s value has dropped to $240,000. That homeowner is now $40,000 underwater—they owe $40,000 more than the house could sell for in today’s market.

What Causes Negative Equity?

Several factors can push a property underwater:

- 📉 Market downturns: Local or national real estate crashes reduce property values

- 🏗️ Neighborhood decline: Economic changes, increased crime, or infrastructure problems

- 💰 High loan-to-value purchases: Buying with minimal down payment leaves little equity cushion

- 🏚️ Property deterioration: Deferred maintenance reduces value faster than mortgage paydown

- 📊 Economic recession: Job losses and foreclosures in your area drag down comparable sales

The 2008 housing crisis left millions of homeowners underwater, and while markets recovered in many areas, certain neighborhoods and property types never fully rebounded. In 2026, new economic pressures have created pockets of negative equity across different regions.

The Foreclosure Factor

Being underwater becomes critical when combined with foreclosure proceedings. If you could afford your mortgage payments, negative equity would simply be an unfortunate paper loss. But when financial hardship strikes—job loss, medical bills, divorce, or business failure—the inability to sell your way out of the problem creates a true crisis.

Traditional homeowners facing hardship can list their property, sell it, pay off the mortgage, and move forward. Underwater homeowners lack this escape route. Selling would require bringing cash to closing to cover the difference between the sale price and the loan balance—money most distressed homeowners simply don’t have.

The Foreclosure Timeline When You’re Underwater

Understanding the foreclosure process helps you recognize how much time you have to act. Foreclosure doesn’t happen overnight, and each stage presents different opportunities for resolution.

Typical Foreclosure Stages

| Stage | Timeline | What Happens | Your Options |

|---|---|---|---|

| Missed Payments | 1-3 months | Late fees accumulate, lender contacts increase | Loan modification, forbearance, catch up payments |

| Notice of Default | 3-4 months | Formal default notice filed, pre-foreclosure begins | Short sale, deed in lieu, cash sale |

| Pre-Foreclosure | 4-12 months | Property listed as pre-foreclosure, negotiations possible | Short sale approval, quick cash buyers |

| Auction Notice | 30-90 days before sale | Public notice of foreclosure auction date | Emergency cash sale, last-minute negotiations |

| Foreclosure Auction | Auction day | Property sold to highest bidder or bank | Options exhausted |

| Post-Foreclosure | After auction | Eviction proceedings begin | Deficiency judgment risk |

The exact timeline varies significantly by state. Foreclosure timeline by state can range from as little as 60 days in states like Texas to over a year in states like New York or Florida that require judicial foreclosure.

Why Acting Early Matters

The earlier you address an underwater foreclosure situation, the more helpful solutions become available. During the first few months of default, lenders are often willing to discuss alternatives. As the process advances toward auction, options narrow and urgency increases.

Early action benefits include:

- More time to negotiate short sale approval

- Better chance of avoiding deficiency judgments

- Opportunity to find qualified cash buyers

- Reduced stress and more control over outcomes

- Protection of credit scores (foreclosure causes maximum damage)

Many homeowners wait too long, hoping circumstances will magically improve. This optimism, while understandable, often leads to worse outcomes. Facing the situation head-on with expert guidance creates the best path forward.

How to Sell Underwater House Foreclosure: We Handle Negative Equity Solutions

When you’re underwater and facing foreclosure, several pathways can help you exit the situation with minimal damage. Each approach has specific requirements, timelines, and outcomes.

Short Sale: Negotiating with Your Lender

A short sale allows you to sell your property for less than the outstanding mortgage balance, with the lender agreeing to accept the proceeds as full or partial satisfaction of the debt. This process requires lender approval and coordination between multiple parties.

Short sale advantages:

✅ Avoids foreclosure on your credit report

✅ May eliminate or reduce deficiency judgment

✅ Provides more dignified exit than foreclosure

✅ Can sometimes include relocation assistance

Short sale challenges:

❌ Requires extensive documentation and lender approval

❌ Process can take 3-6 months or longer

❌ No guarantee lender will approve

❌ May still result in taxable forgiven debt

❌ Traditional buyers often lose patience with delays

The complete step-by-step short sale process involves gathering financial hardship documentation, finding a buyer, submitting the short sale package to your lender, and navigating their approval process. Many homeowners find this overwhelming without professional assistance.

Cash Buyers Who Specialize in Underwater Properties

Specialized cash buyers for problem properties offer a faster alternative to traditional short sales. These investors understand negative equity situations and have systems for working with lenders to facilitate quick closings.

How cash buyers help with underwater foreclosures:

- Quick evaluation: Most provide offers within 24-48 hours

- Lender negotiation: Experienced teams handle short sale paperwork and lender communications

- Fast closing: Can close in 7-30 days once lender approves

- As-is purchase: No repairs or improvements required

- Certainty: Cash offers don’t depend on buyer financing falling through

The trade-off is that cash buyers typically offer less than retail market value. However, when facing foreclosure with negative equity, speed and certainty often matter more than maximizing sale price. The goal is escaping the situation, not profit.

Deed in Lieu of Foreclosure

A deed in lieu of foreclosure involves voluntarily transferring your property deed to the lender in exchange for release from the mortgage obligation. Think of it as handing the keys back and walking away.

When deed in lieu makes sense:

- You’ve already tried to sell without success

- Short sale attempts have failed

- You need to avoid foreclosure on your record

- The property has no junior liens or other complications

Deed in lieu limitations:

- Lenders aren’t required to accept

- Only works if property has clear title

- May not eliminate deficiency judgment

- Still impacts credit, though less than foreclosure

- Lender may require you to attempt sale first

Most lenders view deed in lieu as a last resort option. They prefer you attempt a short sale first, as selling to a third party typically recovers more money than the lender taking the property back.

Strategic Default Considerations

Some homeowners consider strategic default—intentionally stopping payments on an underwater mortgage even when they could afford them. This controversial approach aims to force lender negotiation or simply walk away from negative equity.

Important warnings about strategic default:

⚠️ Severely damages credit scores (200+ point drops)

⚠️ May result in deficiency judgments

⚠️ Could trigger tax consequences on forgiven debt

⚠️ Creates legal and ethical complications

⚠️ Not appropriate for most situations

Strategic default should only be considered with legal and financial advice. For most homeowners, working proactively with lenders and exploring legitimate alternatives provides better outcomes.

Working with Sure Path Property Solutions on Underwater Foreclosures

Navigating the intersection of negative equity and foreclosure requires specialized knowledge and experience. Sure Path Property Solutions focuses specifically on complicated real estate situations where traditional methods fall short.

Our Approach to Negative Equity Situations

When homeowners contact us about underwater foreclosure situations, we provide helpful guidance through a structured process:

Step 1: Situation Assessment

We start by understanding your complete picture:

- Current mortgage balance and payment status

- Property’s estimated market value

- Foreclosure timeline and stage

- Any additional liens or judgments

- Your goals and timeline needs

This assessment is always free and confidential. Our friendly and caring team understands the stress you’re experiencing and approaches every situation with empathy and professionalism.

Step 2: Option Analysis

Based on your specific circumstances, we outline available paths forward:

- Short sale feasibility and timeline

- Cash purchase possibility and terms

- Lender negotiation strategies

- Alternative solutions specific to your situation

We explain each option in plain language, helping you understand the pros, cons, and likely outcomes of different approaches.

Step 3: Implementation Support

Once you choose a direction, our industry experts handle the heavy lifting:

- Coordinating with your lender’s loss mitigation department

- Preparing and submitting required documentation

- Negotiating terms and timelines

- Working with title companies to resolve any title issues

- Facilitating smooth closing process

Why Specialized Help Matters

Underwater foreclosure situations involve multiple complex systems intersecting:

- Mortgage servicing: Understanding how loss mitigation departments operate

- Real estate valuation: Accurately assessing property value in distressed conditions

- Title work: Identifying and addressing liens, judgments, or other encumbrances

- Negotiation: Communicating effectively with institutional lenders

- Timeline management: Coordinating multiple parties to close before auction

Attempting to navigate these systems alone often leads to frustration, missed deadlines, and worse outcomes. Our expert service comes from handling hundreds of similar situations and understanding how to move efficiently through each step.

Real Results for Real People

Consider Maria’s situation: She inherited a house from her parents with a reverse mortgage balance of $185,000, but the property was only worth $160,000 due to deferred maintenance and neighborhood decline. The reverse mortgage company had started foreclosure proceedings.

Maria initially thought she had no options—she couldn’t afford to bring $25,000 to closing, and traditional buyers weren’t interested in a property needing extensive repairs. After contacting our team, we:

- Negotiated with the reverse mortgage servicer for short sale approval

- Made a cash offer that the servicer accepted

- Closed in 21 days, stopping the foreclosure

- Eliminated Maria’s liability for the deficiency

Maria walked away with no debt, no foreclosure on her record, and the emotional relief of resolving her parents’ estate without financial devastation.

Additional Complications That Compound Underwater Foreclosures

Negative equity and foreclosure rarely exist in isolation. Many distressed properties carry additional burdens that complicate resolution.

Property Tax Liens and Back Taxes

Back taxes on property create additional debt that must be addressed during any sale. Property tax liens typically have priority over mortgage liens, meaning they must be paid first from sale proceeds.

When you’re already underwater on your mortgage, adding $15,000 in delinquent property taxes makes the negative equity hole even deeper. The good news: most lenders understand this reality and factor tax debt into short sale negotiations.

We regularly help homeowners sell properties with tax debt by coordinating payoff between the lender, taxing authority, and closing. Our trustworthy service includes ensuring all parties receive proper payment and releases.

Judgment Liens and Other Encumbrances

Judgment liens from unpaid debts, contractor disputes, or legal settlements attach to your property and must be addressed before sale. When combined with negative equity, these liens create additional obstacles.

Common types of liens affecting underwater properties:

- 🏗️ Mechanics liens: From unpaid contractor work

- ⚖️ Judgment liens: From lawsuit awards or unpaid debts

- 🏛️ Tax liens: Federal, state, or local tax debt

- 🏦 HOA liens: Unpaid homeowners association fees

- 💼 Child support liens: From unpaid support obligations

Each lien type has different priority levels and negotiation possibilities. Understanding how to sell a house with a lien requires knowing which liens must be paid in full and which might accept reduced payoffs.

Multiple Owners and Heir Property Issues

Properties with multiple owners or inherited properties add another layer of complexity to underwater foreclosure situations. When siblings inherit a house with negative equity and can’t agree on how to proceed, the foreclosure clock keeps ticking.

Challenges with multiple ownership:

- All owners must typically agree to short sale

- One owner’s financial problems affect all owners

- Disagreements delay decision-making

- Partition lawsuits add cost and time

- Communication breakdowns stall progress

We’ve helped numerous families navigate these situations by facilitating communication, explaining options clearly to all parties, and providing solutions that work for everyone involved. Our approach recognizes that helpful solutions must address both financial and family dynamics.

Protecting Yourself from Deficiency Judgments

One of the biggest fears homeowners have about short sales and foreclosures is the deficiency judgment—when the lender sues you for the difference between what you owed and what the property sold for.

Understanding Deficiency Judgment Risk

If you owe $300,000 but your house sells at foreclosure auction for $220,000, the lender lost $80,000. In many states, they can pursue a deficiency judgment to recover that loss from you personally.

Factors affecting deficiency judgment risk:

- State laws: Some states prohibit or limit deficiency judgments

- Loan type: Purchase money mortgages often have different rules than refinances

- Lender policies: Some lenders routinely pursue deficiencies, others rarely do

- Your financial situation: Lenders assess collectability before pursuing judgments

- Negotiated terms: Short sale agreements can include deficiency waivers

Strategies to Minimize Deficiency Risk

1. Negotiate Deficiency Waivers

During short sale negotiations, explicitly request that the lender waive their right to pursue deficiency judgment. Many lenders agree to this, especially when:

- The borrower has limited assets

- Pursuing judgment would be costly relative to potential recovery

- The short sale offer is reasonable and well-documented

2. Choose States with Anti-Deficiency Protection

If you’re considering walking away from an underwater property, understand your state’s laws. California, Arizona, and several other states have strong anti-deficiency protections for purchase money loans on primary residences.

3. Consider Bankruptcy Protection

In severe financial distress situations, bankruptcy can discharge deficiency judgments. This is a serious step requiring legal counsel, but it provides a complete financial reset for those who qualify.

4. Document Financial Hardship

Lenders are more likely to waive deficiencies when borrowers demonstrate genuine hardship rather than strategic default. Thorough documentation of job loss, medical issues, divorce, or other hardship strengthens your negotiating position.

Tax Implications of Underwater Property Sales

Selling an underwater property through short sale or foreclosure can trigger tax consequences that catch homeowners by surprise.

Cancellation of Debt Income

When a lender forgives debt through a short sale or foreclosure, the IRS generally considers that forgiven amount as taxable income. If your lender forgives $50,000 in debt, you might receive a 1099-C form reporting $50,000 in income—potentially triggering a significant tax bill.

Exceptions and protections:

- 🏠 Primary residence exclusion: The Mortgage Forgiveness Debt Relief Act (extended through 2025, check 2026 status) allows exclusion of forgiven debt on principal residences up to certain limits

- 💰 Insolvency exception: If you were insolvent (debts exceeded assets) when the debt was forgiven, you may exclude the income

- 📋 Bankruptcy discharge: Debt forgiven in bankruptcy isn’t taxable

- 🏚️ Property abandonment: Different rules apply to abandoned properties

Capital Gains Considerations

Ironically, even with negative equity, you might face capital gains questions. If you purchased your home for $150,000 many years ago, made improvements, and now owe $280,000 on a property worth $240,000, the tax calculation considers your original basis, not your current loan amount.

Most homeowners avoid capital gains through:

- Primary residence exclusion ($250,000 single, $500,000 married)

- Losses offsetting gains

- Proper documentation of improvements and selling costs

Professional Tax Guidance

Tax implications of distressed property sales are complex and individual. Always consult with a qualified tax professional before completing a short sale or foreclosure to understand your specific situation and plan accordingly.

When to Sell vs. When to Fight Foreclosure

Not every underwater foreclosure situation requires selling the property. Understanding when to fight and when to exit helps you make the best decision for your circumstances.

Situations Where Selling Makes Sense

✓ Sell when:

- You’ve experienced permanent income reduction

- The property needs major repairs you can’t afford

- You’re relocating for employment

- Family circumstances have changed (divorce, death, etc.)

- The neighborhood is declining with no recovery in sight

- Stress is affecting your health and wellbeing

- You have no emotional attachment to the property

- Better housing options exist for your current needs

Situations Where Fighting Foreclosure May Work

✓ Fight foreclosure when:

- Your income disruption is temporary

- Loan modification could make payments affordable

- You have significant equity that will return when market recovers

- The property is your long-term family home

- You’re close to retirement and need housing stability

- Refinancing options exist that you haven’t explored

- Government assistance programs apply to your situation

- You can catch up on missed payments within 3-6 months

Making the Decision

This decision is deeply personal and depends on factors beyond pure financial calculation. Consider:

Financial factors:

- How far underwater are you?

- What’s the realistic timeline for recovering equity?

- Can you afford current or modified payments?

- What are your other debts and obligations?

Personal factors:

- How is the stress affecting your health?

- What’s best for your family?

- What are your housing alternatives?

- How important is this specific property to you?

Future factors:

- What are your career prospects?

- Are you planning other major life changes?

- How will this decision affect your goals?

- What’s your timeline for financial recovery?

Our team provides helpful guidance without pressure. We help you think through these questions and make the decision that’s right for your unique situation.

The Sure Path Process: From First Contact to Closing

Understanding what to expect when working with us helps reduce anxiety and uncertainty during an already stressful time.

Initial Contact and Consultation

Day 1: Reach Out

Contact us through our website, phone, or email. You’ll speak with a real person who listens to your situation without judgment. We ask questions to understand:

- Your property location and type

- Current mortgage situation

- Foreclosure status and timeline

- Additional complications (liens, co-owners, etc.)

- Your goals and concerns

This conversation typically takes 15-30 minutes and is completely confidential.

Day 1-2: Preliminary Assessment

Our team researches your property:

- Public records review

- Mortgage and lien search

- Property value estimation

- Foreclosure timeline verification

- Title issue identification

Offer and Option Presentation

Day 2-3: Options Discussion

We present your realistic options with honest pros and cons:

- Cash purchase: If we can make an offer that works

- Short sale assistance: If that’s the better path

- Lender negotiation support: To explore modification or other alternatives

- Referrals: If another solution better fits your needs

We never pressure you toward any particular option. Our goal is trustworthy service that puts your interests first.

Day 3-7: Offer Details

If a cash purchase makes sense, we provide:

- Written purchase offer

- Explanation of terms and timeline

- Clear breakdown of how proceeds will be distributed

- Next steps and requirements

Lender Coordination and Approval

Week 1-4: Short Sale Package

For underwater properties, we prepare and submit the short sale package to your lender:

- Hardship letter

- Financial documentation

- Purchase agreement

- Comparative market analysis

- Repair estimates (if applicable)

- Title report

Week 2-8: Lender Review

Your lender’s loss mitigation department reviews the package. We follow up regularly, respond to requests for additional information, and keep you updated on progress.

This is typically the longest part of the process. Lender timelines vary significantly, but our experience helps us navigate their systems efficiently.

Closing and Resolution

Final Week: Closing Preparation

Once the lender approves the short sale:

- Title company prepares closing documents

- Final walkthrough scheduled

- Closing date confirmed

- Moving arrangements finalized

Closing Day: Resolution

At closing:

- Documents are signed

- Funds are distributed per lender approval

- Mortgage is satisfied

- Additional liens are paid per agreement

- You receive any approved relocation assistance

- Keys are transferred

Post-Closing: Fresh Start

After closing:

- Foreclosure is stopped

- You’re released from mortgage obligation

- Credit impact is minimized

- You can begin rebuilding your financial future

Frequently Asked Questions About Underwater Foreclosures

Can I sell my house if I’m upside down on my mortgage?

Yes, through a short sale where your lender agrees to accept less than the full loan balance. You can also work with cash buyers who specialize in negotiating these situations with lenders.

How long does a short sale take?

Short sales typically take 2-6 months from initial submission to closing, though timelines vary by lender. Some banks respond in 30-45 days, while others take 3-4 months. Working with experienced professionals speeds the process.

Will I owe money after a short sale?

It depends on whether your lender agrees to waive the deficiency. Many short sale agreements include deficiency waivers, especially for primary residences. Always negotiate this explicitly and get it in writing.

Is short sale better than foreclosure?

Generally yes. Short sales typically damage credit scores less than foreclosure (50-150 points vs. 200-300 points), allow you to avoid foreclosure on your record, and may eliminate deficiency judgment risk. You also maintain more control and dignity through the process.

Can I buy another house after a short sale?

Yes, though waiting periods apply. FHA loans may be available after 3 years, conventional loans after 4 years, and VA loans after 2 years. These timelines assume you’ve rebuilt credit and can document the hardship that caused the short sale.

What if my lender won’t approve a short sale?

If your lender denies a reasonable short sale offer, options include: requesting reconsideration with additional documentation, exploring deed in lieu of foreclosure, or allowing foreclosure to proceed while understanding the consequences. Sometimes lenders become more flexible as auction dates approach.

Do I need a real estate agent for a short sale?

While not legally required, having representation helps. However, traditional agents often lack experience with short sales and may not have the lender relationships necessary to navigate the process efficiently. Specialized companies like Sure Path Property Solutions combine purchase capability with short sale expertise.

Taking Action: Your Next Steps

If you’re facing the stress of an underwater mortgage combined with foreclosure proceedings, taking action today opens more doors than waiting and hoping things improve.

Immediate Actions You Can Take

1. Assess Your Timeline

Determine exactly where you are in the foreclosure process:

- Review all notices you’ve received

- Note important dates (auction date, response deadlines)

- Calculate how many payments you’ve missed

- Understand your state’s foreclosure timeline

2. Gather Your Documentation

Collect the information you’ll need for any solution:

- Current mortgage statement showing balance

- Recent property tax statement

- List of any other liens or judgments

- Documentation of financial hardship

- Recent pay stubs or income documentation

- Bank statements

3. Stop Ignoring Your Lender

While it’s tempting to avoid calls from your mortgage servicer, communication is important. Let them know you’re exploring options. Ask about their loss mitigation department and what programs might be available.

4. Get Professional Assessment

Contact specialists who understand underwater foreclosure situations. Reach out to our team for a free, no-obligation consultation about your specific circumstances.

What to Expect When You Contact Us

When you reach out to Sure Path Property Solutions:

✅ No pressure: We provide information and options, never high-pressure sales tactics

✅ Confidential consultation: Your situation remains private

✅ Honest assessment: We tell you what’s realistic, not what you want to hear

✅ Multiple options: We explore all possibilities, not just those that benefit us

✅ Fast response: We understand urgency and respond quickly

✅ Clear communication: Plain language explanations without confusing jargon

Making the Decision

Only you can decide the right path for your situation. Our role is providing the information, expertise, and support you need to make that decision with confidence.

Consider these questions:

- What outcome would give you the most peace of mind?

- What’s most important to you—avoiding foreclosure, minimizing credit damage, or moving forward quickly?

- What resources (time, money, energy) do you have available?

- What does your gut tell you about the right direction?

Trust yourself. You know your situation better than anyone else. We’re here to provide expert service and helpful solutions, but the final decision is always yours.

Regional Considerations: Where You Live Matters

Foreclosure laws, timelines, and protections vary significantly by state. Understanding your local context helps set realistic expectations.

Judicial vs. Non-Judicial Foreclosure States

Judicial foreclosure states (like Florida, New York, New Jersey) require lenders to go through court proceedings. This typically takes longer—often 12-24 months—giving homeowners more time to explore alternatives.

Non-judicial foreclosure states (like Texas, California, Georgia) allow lenders to foreclose without court involvement, often completing the process in 2-4 months. Speed is critical in these states.

State-Specific Protections

Some states offer stronger homeowner protections:

- Anti-deficiency laws: Limiting or prohibiting deficiency judgments

- Redemption periods: Allowing homeowners to reclaim property after foreclosure

- Mediation programs: Requiring lenders to participate in foreclosure mediation

- Notice requirements: Mandating specific warnings and timelines

Local Market Conditions

Real estate markets vary dramatically by region. What’s considered underwater in one market might be normal in another:

- Declining markets: Areas with ongoing population loss or economic challenges

- Recovering markets: Regions rebounding from previous downturns

- Stable markets: Areas with consistent values and demand

- Volatile markets: Locations with boom-bust cycles

We work across multiple states and understand regional differences. Whether you’re facing foreclosure in Texas, Florida, or anywhere else, we adapt our approach to your local context.

Hope and Help: Moving Forward from Underwater Foreclosure

Financial distress feels isolating and overwhelming. When you’re underwater on your mortgage and facing foreclosure, it’s easy to believe you’re alone in this struggle. You’re not.

Thousands of homeowners face similar situations every year. The 2008 crisis taught us that market forces beyond individual control can create these circumstances. Job losses, medical emergencies, divorces, and economic downturns happen to good people who made reasonable decisions with the information they had.

You didn’t fail. The situation failed you.

The good news: solutions exist. Whether through short sale, cash purchase, lender negotiation, or other alternatives, pathways forward are available. The key is taking action before options narrow.

The Emotional Component

Beyond the financial calculations, underwater foreclosure carries emotional weight:

- 😟 Shame and embarrassment: Feeling like you’ve failed

- 😰 Stress and anxiety: Constant worry about the future

- 😢 Grief: Losing a home you love

- 😤 Anger: At circumstances, lenders, or yourself

- 😔 Depression: Feeling hopeless and stuck

These feelings are normal and valid. Acknowledging them is part of moving forward. Many homeowners report that taking action—even difficult action like accepting a short sale—brings relief. The uncertainty and waiting often feel worse than making a decision and moving forward.

Your Financial Future

One question we hear frequently: “Will this ruin my financial future forever?”

The answer is no. While short sales and foreclosures impact credit scores and create waiting periods for new mortgages, these effects are temporary. People rebuild credit, buy homes again, and create financial stability after distressed property sales.

Timeline for recovery:

- Credit score: Begins improving immediately as you rebuild positive history

- New mortgage: Possible in 2-4 years depending on loan type

- Rental approval: Often possible immediately with explanation letter

- Employment: Most employers don’t check credit; those who do often understand hardship

- Overall financial health: Can improve quickly once you’re free from underwater debt

Many people report that their financial situation actually improves after resolving an underwater property. The stress, negative cash flow, and mounting debt disappear, allowing them to focus on building positive financial habits.

Conclusion: Your Path Forward Starts Here

Standing at the intersection of negative equity and foreclosure feels like being trapped in a maze with no exit. But walls that seem solid often have doors—you just need someone who knows where to look.

Sell underwater house foreclosure: we handle negative equity isn’t just a service description—it’s a commitment to homeowners facing one of the most stressful situations in real estate. Whether through short sale negotiation, cash purchase, or connecting you with the right resources, solutions exist for your specific circumstances.

The most important step is the first one: reaching out for help. Every day you wait, options narrow and stress increases. Every day you act, you move closer to resolution and relief.

Take Action Today

Don’t let another sleepless night pass wondering what to do. Contact Sure Path Property Solutions today for a free, confidential consultation about your underwater foreclosure situation.

What you’ll receive:

- Honest assessment of your situation

- Clear explanation of available options

- No-obligation cash offer (if applicable)

- Guidance on next steps

- Support from experienced professionals who care

You don’t have to navigate this alone. Our team has helped hundreds of homeowners escape underwater foreclosure situations and move forward to better circumstances. We can help you too.

Ready to explore your options? Contact us now or call to speak with a specialist who understands exactly what you’re facing and how to help.

Your fresh start is closer than you think. Let’s take that first step together.

Sure Path is a family-owned, curative-title cash buyer. We handle the paperwork and pay what’s owed at closing — no fees, no repairs, no pressure.