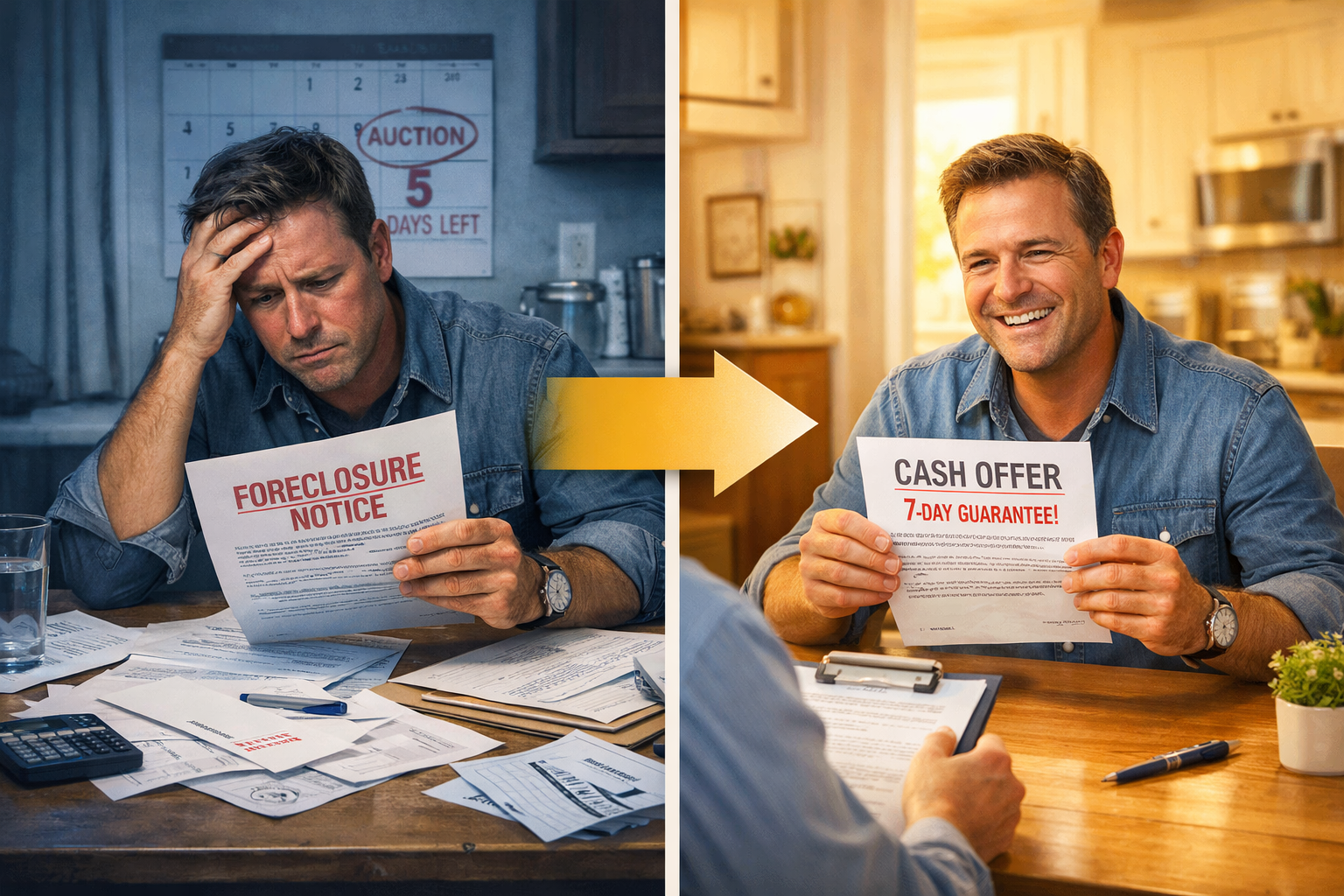

Avoid Foreclosure Sell Quickly: 7-Day Sale Guarantee

The foreclosure notice arrives in the mail, and suddenly the world feels like it’s closing in. The auction date looms just weeks away, traditional buyers want months to close, and real estate agents suggest lengthy listing processes. When facing foreclosure, time becomes the most precious commodity—and most homeowners simply don’t have enough of it. That’s where the Avoid Foreclosure Sell Quickly: 7-Day Sale Guarantee becomes a lifeline, offering a rapid exit strategy that stops the foreclosure process before it destroys credit and financial stability.

Foreclosure doesn’t just threaten housing security. It damages credit scores for seven years, creates potential deficiency judgments, and leaves families scrambling for solutions. Traditional real estate transactions take 30-60 days minimum, but foreclosure auctions wait for no one. The Avoid Foreclosure Sell Quickly: 7-Day Sale Guarantee provides an alternative path—one that prioritizes speed, certainty, and relief over maximum profit.

Key Takeaways

✅ Speed matters most: Seven-day sale guarantees can stop foreclosure proceedings before auction dates, protecting credit and preventing deficiency judgments

💰 Cash offers eliminate financing delays: Direct buyers remove the uncertainty of mortgage approvals that cause traditional sales to collapse

📋 Sell as-is without repairs: No need to invest time or money fixing properties when facing imminent foreclosure deadlines

🤝 Professional guidance navigates complexity: Expert service helps coordinate with lenders, title companies, and counties to resolve liens and back taxes

🏡 Multiple exit strategies exist: Understanding all options—short sales, deeds in lieu, and quick cash sales—empowers better decision-making

Understanding Foreclosure: The Timeline That Threatens Homeowners

Foreclosure represents a legal process where lenders reclaim property due to mortgage default. The timeline varies by state, but the pressure remains constant.

How Foreclosure Proceedings Unfold

Most foreclosures follow a predictable pattern. After missing three to six monthly payments, lenders issue a Notice of Default or Demand Letter. This initial warning provides 30-90 days to cure the default by paying overdue amounts plus fees.

When homeowners cannot catch up on payments, lenders file foreclosure actions. In judicial foreclosure states, this means court proceedings that can take 6-12 months. Non-judicial foreclosure states move faster—sometimes completing the process in 90-120 days.

The foreclosure auction represents the final stage. Properties sell on courthouse steps to the highest bidder. Whatever the property brings at auction goes toward the mortgage debt. If the sale price falls short, lenders may pursue a deficiency judgment for the remaining balance.

The Real Cost of Foreclosure

Foreclosure creates devastating financial consequences that extend far beyond losing the home:

- Credit score damage: Foreclosure drops credit scores by 200-300 points and remains on credit reports for seven years

- Future housing challenges: Difficulty qualifying for mortgages, apartments, or even employment requiring credit checks

- Deficiency judgments: Potential liability for the difference between auction price and mortgage balance

- Tax implications: Forgiven debt may count as taxable income under certain circumstances

- Emotional toll: Stress, anxiety, and uncertainty affecting entire families

“Foreclosure isn’t just about losing a house—it’s about losing financial stability for years to come. The seven-year credit impact affects everything from car loans to job opportunities.”

Why Traditional Sales Fail Homeowners Facing Foreclosure

When foreclosure threatens, many homeowners instinctively list with real estate agents. Unfortunately, traditional sales rarely work under time pressure.

Listing challenges include:

| Challenge | Impact on Foreclosure Timeline |

|---|---|

| Market time | 30-90 days average to find buyers |

| Buyer financing | 30-45 days for mortgage approval |

| Inspection contingencies | Delays for repairs or renegotiation |

| Appraisal issues | Deals collapse if value comes in low |

| Total timeline | 60-135+ days minimum |

Foreclosure auctions don’t wait for traditional sales to close. When the auction date arrives in 30-60 days, incomplete sales become worthless. Buyers walk away, and homeowners lose everything.

Understanding foreclosure timelines helps homeowners recognize when they need faster solutions than traditional real estate can provide.

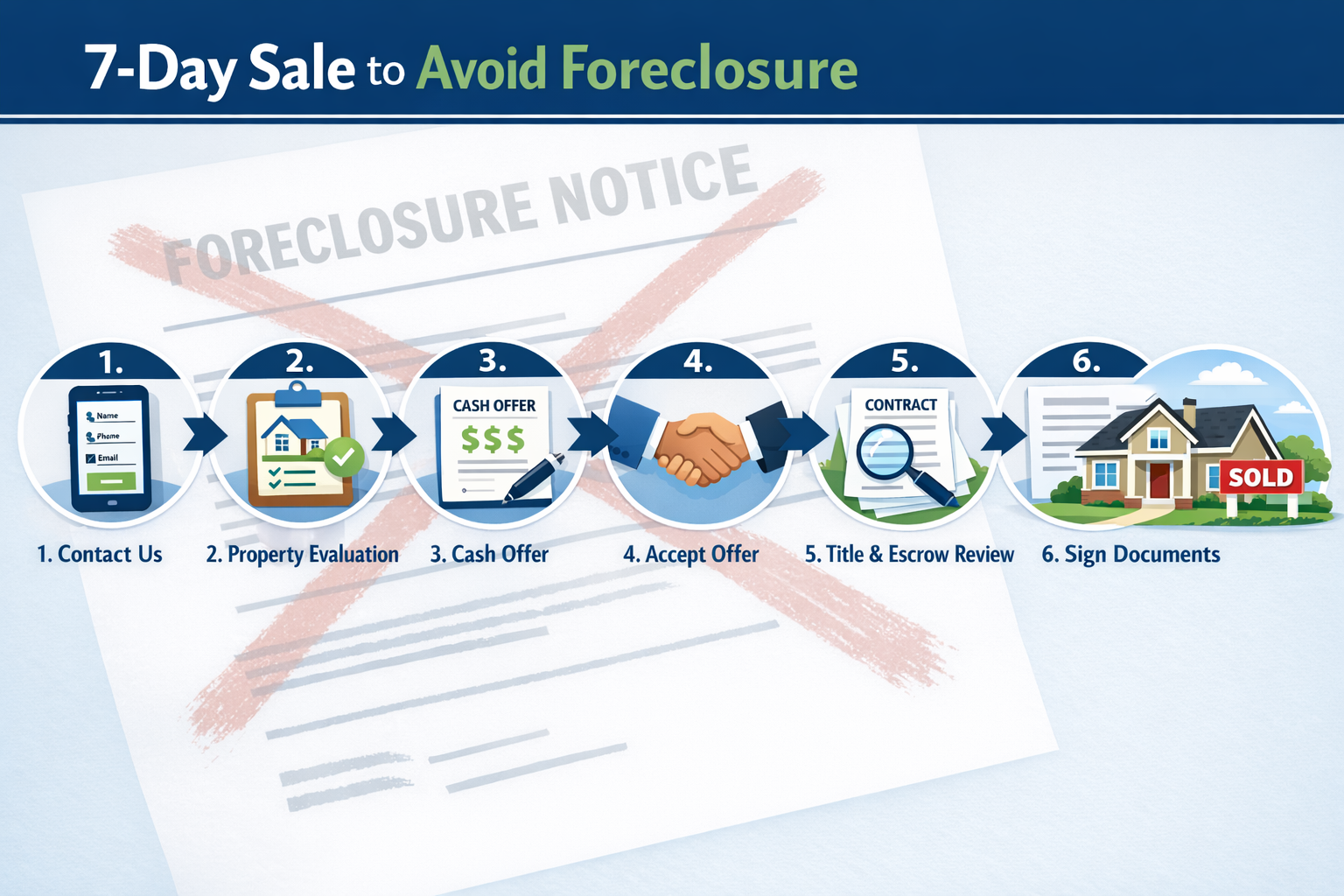

The 7-Day Sale Solution: How Avoid Foreclosure Sell Quickly Programs Work

The Avoid Foreclosure Sell Quickly: 7-Day Sale Guarantee offers a fundamentally different approach than traditional real estate transactions. Instead of hoping buyers secure financing and navigate contingencies, these programs provide certainty and speed.

What Makes Seven-Day Sales Possible

Several factors enable legitimate companies to close property purchases in seven days:

Cash purchasing power eliminates financing delays. Companies maintain capital reserves specifically for purchasing distressed properties. No mortgage applications, no underwriting delays, no appraisal contingencies.

Streamlined due diligence focuses on essential title review rather than exhaustive inspections. Professional buyers understand property conditions and purchase as-is, removing inspection contingencies that derail traditional sales.

Established relationships with title companies, attorneys, and closing agents create efficient workflows. When everyone knows the process and timeline, closings happen faster.

Simplified documentation reduces paperwork complexity. Standard purchase agreements, clear terms, and straightforward processes replace the lengthy contracts typical of traditional sales.

The Seven-Day Timeline Breakdown

Understanding how seven days translates into a completed sale helps homeowners recognize legitimate offers:

Day 1-2: Initial Contact and Property Evaluation

- Homeowner contacts buyer or completes online form

- Brief phone consultation to understand situation

- Property details gathered (address, condition, mortgage balance, foreclosure timeline)

- Preliminary research on title and liens

Day 3: Cash Offer Presentation

- Comprehensive offer presented with clear terms

- Explanation of how offer accounts for liens, back taxes, and closing costs

- No obligation to accept—time to review and ask questions

- Transparency about net proceeds homeowner receives

Day 4-5: Acceptance and Title Work

- Homeowner accepts offer

- Title company orders title search

- Coordination begins with lender on payoff amounts

- Closing date scheduled

Day 6: Final Review and Preparation

- Title issues addressed (if any)

- Final settlement statement prepared

- Closing logistics confirmed

- Any remaining questions answered

Day 7: Closing and Cash Payment

- Documents signed at title company or attorney’s office

- Funds transferred to pay off mortgage and liens

- Homeowner receives any remaining equity

- Foreclosure stopped before auction

This compressed timeline works because professional buyers remove the variables that delay traditional sales. No financing contingencies. No repair negotiations. No buyer cold feet.

As-Is Purchases: No Repairs, No Preparation

One of the most valuable aspects of quick-sale programs is the as-is purchase commitment. Homeowners facing foreclosure rarely have money or time for repairs.

Traditional buyers expect:

- Fresh paint and carpet

- Functional appliances

- Roof and HVAC in good condition

- Updated kitchens and bathrooms

- Landscaping and curb appeal

Professional cash buyers purchase properties regardless of condition:

- ✅ Foundation issues

- ✅ Roof damage

- ✅ Outdated systems

- ✅ Deferred maintenance

- ✅ Code violations

- ✅ Tenant occupied

- ✅ Hoarder situations

This as-is approach saves homeowners thousands in repair costs and weeks in preparation time—neither of which they have when foreclosure looms.

Handling Liens and Back Taxes

Many properties facing foreclosure also carry additional complications: tax liens, judgment liens, HOA liens, or mechanic’s liens. These encumbrances must be resolved before title transfers.

Professional buyers coordinate lien resolution as part of the purchase process:

- Title search identifies all liens: Every claim against the property gets documented

- Payoff amounts requested: Current balances obtained from lien holders

- Settlement statement accounts for liens: Purchase price allocates funds to satisfy all claims

- Liens paid at closing: Title company distributes funds to lien holders, clearing title

- Clean title transfers to buyer: Homeowner walks away free of property obligations

This coordination represents expert service that simplifies what would otherwise require months of negotiation. Companies like Sure Path Property Solutions specialize in navigating these complex situations, providing helpful guidance through every step.

For properties with back taxes, the process works similarly. Tax obligations get satisfied from sale proceeds, preventing tax foreclosure and eliminating future liability.

Who Benefits Most from Avoid Foreclosure Sell Quickly: 7-Day Sale Guarantee Programs

While anyone facing foreclosure can benefit from quick-sale options, certain situations make these programs particularly valuable.

Homeowners Behind on Mortgage Payments

The most obvious candidates are homeowners who’ve fallen behind on mortgage payments and received foreclosure notices. Common reasons for default include:

- Job loss or income reduction: Layoffs, business closures, or reduced hours

- Medical emergencies: Unexpected healthcare costs draining savings

- Divorce or separation: Household income split between two residences

- Adjustable-rate increases: Payment shock when rates reset higher

- Property tax increases: Rising assessments making total housing costs unaffordable

When catching up on payments isn’t feasible, selling quickly prevents foreclosure from destroying credit. Even if equity is minimal or negative, avoiding foreclosure protects future financial options.

Inherited Property Owners with Tax Problems

Inherited properties often come with unexpected complications. Heirs discover:

- Years of accumulated back taxes

- Deferred maintenance requiring expensive repairs

- Properties in distant locations they cannot manage

- Multiple heirs disagreeing about what to do

- Unclear title due to missing probate steps

When inherited properties face tax foreclosure, quick sales prevent losing the property entirely. The seven-day timeline allows heirs to salvage remaining equity before tax sales occur.

Property Owners with Multiple Liens

Properties encumbered with multiple liens create complex situations that traditional buyers avoid:

- Tax liens from IRS or state agencies

- Judgment liens from lawsuits

- HOA liens from unpaid assessments

- Mechanic’s liens from contractor disputes

- Child support liens

Each lien must be satisfied before title transfers. Professional buyers handle this coordination, making helpful solutions possible when traditional sales would fail.

Owners of Jointly Held Property in Dispute

Jointly owned properties create unique challenges when co-owners disagree. Situations include:

- Siblings inheriting family homes

- Former business partners holding investment property

- Divorced couples maintaining joint ownership

- Family members with fractional interests

When one owner wants to sell but others resist, foreclosure may threaten everyone’s interests. Quick sales can resolve disputes before foreclosure damages all owners’ credit.

Homeowners Relocating for Work or Family

Job transfers, family emergencies, or health issues sometimes require immediate relocation. Homeowners cannot wait months for traditional sales when they need to move across the country or care for aging parents.

The 7-Day Sale Guarantee provides certainty and speed that aligns with urgent timelines. While homeowners might receive less than top market value, they gain the flexibility to move forward with life changes.

People Overwhelmed by Property Maintenance

Some homeowners simply reach a point where property maintenance becomes overwhelming:

- Elderly owners unable to maintain homes physically

- Disabled individuals facing accessibility challenges

- Owners of rental properties tired of tenant issues

- People inheriting properties they never wanted

When properties feel more like burdens than assets, quick sales offer relief. The as-is purchase commitment means walking away without addressing years of deferred maintenance.

Comparing Your Options: Short Sale vs. Deed in Lieu vs. Quick Cash Sale

When foreclosure threatens, homeowners have several potential exit strategies. Understanding the differences helps make informed decisions.

Short Sale: Selling for Less Than Mortgage Balance

A short sale occurs when lenders agree to accept less than the full mortgage balance. The property sells to a third-party buyer, with proceeds going to the lender.

Short Sale Advantages:

- Less credit damage than foreclosure (typically 100-150 point drop vs. 200-300)

- Potential to negotiate deficiency judgment waiver

- Maintains some control over the sale process

- May qualify for relocation assistance from lender

Short Sale Disadvantages:

- Requires lender approval (can take 60-120 days)

- No guarantee lender will approve any offer

- Still appears on credit report for seven years

- Complex paperwork and documentation requirements

- Buyer financing can fall through, restarting the process

- May face tax consequences on forgiven debt

Timeline: 3-6 months minimum, often longer

Short sales work best when homeowners have time before foreclosure and can find qualified buyers willing to wait for lender approval.

Deed in Lieu of Foreclosure: Voluntary Transfer

A deed in lieu involves voluntarily transferring property to the lender instead of going through foreclosure proceedings.

Deed in Lieu Advantages:

- Faster than foreclosure (30-90 days typically)

- Less credit damage than foreclosure

- Avoids public foreclosure auction

- May negotiate relocation assistance

- Typically includes deficiency judgment waiver

Deed in Lieu Disadvantages:

- Lenders not required to accept

- Property must have clear title (no junior liens)

- Still damages credit for 2-4 years

- Must prove inability to sell through other means

- Lender may require listing property first

- Limited negotiating power

Timeline: 1-3 months

Deeds in lieu work when homeowners have clear title, cannot afford payments, and lenders prefer avoiding foreclosure costs.

Quick Cash Sale: The Avoid Foreclosure Sell Quickly Solution

Quick cash sales through programs like the Avoid Foreclosure Sell Quickly: 7-Day Sale Guarantee offer a third option focused on speed and certainty.

Quick Cash Sale Advantages:

- ✅ Fastest option (7 days vs. months)

- ✅ Guaranteed closing (no financing contingencies)

- ✅ As-is purchase (no repairs needed)

- ✅ Handles liens and title issues

- ✅ Stops foreclosure before auction

- ✅ Preserves remaining equity for homeowner

- ✅ No listing, showings, or marketing needed

- ✅ Professional guidance through entire process

Quick Cash Sale Considerations:

- Offer price typically below retail market value

- Works best when speed matters more than maximum price

- Requires finding reputable buyer

Timeline: 7 days

Quick cash sales excel when foreclosure dates loom close and homeowners prioritize stopping foreclosure over maximizing sale price.

Decision Matrix: Which Option Fits Your Situation?

| Your Situation | Best Option | Why |

|---|---|---|

| Auction in 30-45 days | Quick cash sale | Only option fast enough |

| Auction in 60-90 days | Quick cash sale or short sale | Cash sale provides certainty |

| Auction in 120+ days | Short sale possible | Time to navigate lender approval |

| Property has junior liens | Quick cash sale | Buyers handle lien complications |

| Need to preserve credit | Quick cash sale | Stops foreclosure before credit damage |

| Have significant equity | Short sale or traditional listing | Time to maximize value |

| Minimal/negative equity | Quick cash sale or deed in lieu | Fastest exit with least hassle |

| Property needs major repairs | Quick cash sale | As-is purchase saves money and time |

The right choice depends on individual circumstances. However, when time runs short, the Avoid Foreclosure Sell Quickly: 7-Day Sale Guarantee often represents the only viable option.

Red Flags: Identifying Legitimate vs. Predatory Quick-Sale Companies

Unfortunately, homeowners facing foreclosure become targets for scams and predatory practices. Recognizing red flags protects vulnerable homeowners from making bad situations worse.

Warning Signs of Predatory Buyers

🚩 Pressure tactics and urgency manipulation

Legitimate buyers understand homeowners need time to make informed decisions. Predatory operators create artificial urgency:

- “This offer expires in 24 hours”

- “Sign now or lose this opportunity”

- “Other buyers are interested—decide immediately”

Trustworthy service provides reasonable time to review offers, consult attorneys, and ask questions without pressure.

🚩 Requests for upfront fees

Legitimate cash buyers never charge homeowners fees. They profit from purchasing and reselling properties, not from charging desperate homeowners.

Red flags include:

- “Processing fees” to review your situation

- “Title search fees” before making offers

- “Administrative costs” to prepare paperwork

Reputable companies cover all costs associated with purchasing properties.

🚩 Requests to sign over the deed before closing

Some scammers ask homeowners to deed property immediately with promises of future payment. Once the deed transfers, homeowners lose all leverage.

Legitimate transactions close simultaneously:

- Deed transfers at closing

- Payment occurs at closing

- Everything happens together through title company or attorney

🚩 Offers significantly below market value without explanation

Professional buyers make below-market offers for valid reasons:

- Property condition requiring extensive repairs

- Liens and back taxes reducing equity

- Market conditions and holding costs

- Profit margin for business sustainability

Legitimate buyers explain their offers clearly, showing how they calculated the price. Predatory buyers make lowball offers without justification, hoping desperate homeowners accept anything.

🚩 Lack of verifiable business presence

Reputable companies have:

- ✅ Physical business addresses

- ✅ Professional websites with educational content

- ✅ Verifiable reviews and testimonials

- ✅ Business licenses and registrations

- ✅ Clear contact information

- ✅ Established track records

Scammers operate from P.O. boxes, use only cell phones, and disappear after transactions.

Questions to Ask Potential Buyers

Protect yourself by asking direct questions:

- “How long have you been in business?” Established companies have track records. New operations may lack experience or legitimacy.

- “Can you provide references from recent sellers?” Legitimate buyers gladly connect you with satisfied clients.

- “What are your company’s credentials and licenses?” Professional buyers maintain proper business registrations.

- “How did you calculate your offer?” Transparent buyers explain their numbers clearly.

- “What costs will I pay?” The answer should be “none” or only standard seller-paid closing costs.

- “Who handles the closing?” Reputable buyers use independent title companies or attorneys, not their own paperwork.

- “What happens if you can’t close in seven days?” Understand contingencies and guarantees.

Verifying Legitimacy: Due Diligence Steps

Before accepting any offer:

Research the company online

- Check Better Business Bureau ratings

- Read Google reviews and testimonials

- Search for complaints or legal actions

- Verify business registration with state authorities

Consult professionals

- Have a real estate attorney review any contracts

- Ask a CPA about tax implications

- Discuss options with a HUD-approved housing counselor

Trust your instincts

- If something feels wrong, it probably is

- Don’t let desperation override caution

- Take time to understand all terms

Verify the closing process

- Ensure closing occurs through independent third party

- Confirm you’ll receive settlement statement in advance

- Understand exactly what you’ll net from the sale

Legitimate companies welcome scrutiny. They want informed sellers who understand and feel comfortable with transactions. Sure Path Property Solutions exemplifies this approach, providing friendly and caring service that prioritizes homeowner understanding and comfort.

The Process: What to Expect When Choosing Avoid Foreclosure Sell Quickly: 7-Day Sale Guarantee

Understanding the step-by-step process removes uncertainty and helps homeowners feel confident moving forward.

Step 1: Initial Contact and Consultation

The process begins with a simple phone call or online form submission. During initial contact, expect:

Information gathering:

- Property address and basic details

- Current mortgage balance and payment status

- Foreclosure timeline and auction date

- Property condition overview

- Liens, judgments, or title issues

- Homeowner’s goals and timeline

No-pressure conversation:

Legitimate buyers use this call to understand situations, not pressure decisions. The consultation should feel helpful and informative, not pushy or aggressive.

Preliminary assessment:

Based on initial information, buyers can often provide ballpark estimates of potential offers. This helps homeowners understand whether quick sales make sense for their situations.

Step 2: Property Evaluation

Most buyers conduct brief property evaluations, either through:

Drive-by assessment:

External evaluation of property condition, neighborhood, and comparable sales

Interior walkthrough:

15-30 minute visit to assess condition, needed repairs, and overall property status

Virtual evaluation:

In some cases, photos and video tours suffice for initial assessments

Unlike traditional buyer inspections that take hours and generate lengthy repair lists, quick-sale evaluations focus on overall condition and major systems.

Step 3: Cash Offer Presentation

Within 24-48 hours of evaluation, buyers present formal cash offers. Professional offers include:

Clear purchase price:

The total amount buyer will pay for the property

Breakdown of costs:

- Mortgage payoff amount

- Property taxes owed

- HOA fees or assessments

- Lien payoffs

- Title and closing costs

- Net proceeds to homeowner

Timeline commitment:

Specific closing date (typically 7 days from acceptance)

Terms and conditions:

Any contingencies or requirements (usually minimal)

Explanation and transparency:

Professional buyers walk through offers line by line, answering questions and ensuring understanding. This represents the expert service that separates legitimate companies from predatory operators.

Step 4: Offer Acceptance and Title Work

If homeowners accept offers, several things happen simultaneously:

Purchase agreement execution:

Both parties sign binding purchase agreements outlining all terms

Title company engagement:

Independent title companies or real estate attorneys get engaged to handle closings

Title search ordered:

Comprehensive title searches identify all liens, judgments, and encumbrances

Mortgage payoff requested:

Title companies contact lenders for exact payoff amounts

Lien payoff quotes obtained:

All lien holders provide current payoff amounts

This phase typically takes 2-3 days as various parties gather information and prepare closing documents.

Step 5: Title Issue Resolution

Title searches sometimes reveal unexpected issues:

- Unknown liens or judgments

- Estate or probate complications

- Boundary disputes

- Missing signatures on previous deeds

Professional buyers work with title companies to resolve these issues quickly. This might involve:

- Negotiating lien releases

- Obtaining missing documentation

- Filing corrective deeds

- Coordinating with attorneys on legal issues

Companies specializing in problem properties have experience navigating complex title situations that would derail traditional sales.

Step 6: Closing Preparation

As the closing date approaches:

Settlement statement prepared:

Detailed accounting of all money in and out of the transaction

Final walkthrough (optional):

Some buyers conduct final property checks

Document preparation:

Deeds, affidavits, and closing documents prepared

Funds arranged:

Buyers ensure cash available for closing

Closing scheduled:

Specific time and location confirmed

Homeowners receive settlement statements 24 hours before closing, allowing time to review and ask questions.

Step 7: Closing and Payment

The closing appointment typically takes 30-60 minutes:

Document signing:

- Deed transferring property to buyer

- Affidavits regarding property condition

- IRS forms for tax reporting

- Settlement statement acknowledgment

Fund disbursement:

Title company distributes funds:

- Mortgage payoff sent to lender

- Lien payoffs sent to creditors

- Property taxes paid to county

- Remaining proceeds to homeowner

Payment to homeowner:

Homeowners receive remaining equity via:

- Cashier’s check

- Wire transfer

- Cash (for small amounts)

Keys and possession:

Property keys transferred to buyer

Foreclosure stopped:

With mortgage paid off, foreclosure proceedings end immediately

The relief homeowners feel at this moment—knowing foreclosure is stopped and the burden is lifted—represents the true value of the Avoid Foreclosure Sell Quickly: 7-Day Sale Guarantee.

Maximizing Your Outcome: Tips for Getting the Best Quick-Sale Deal

While quick sales prioritize speed over maximum price, homeowners can still optimize outcomes.

Be Honest About Property Condition

Transparency benefits everyone. Accurately describing property condition helps buyers make fair offers and prevents closing delays when issues surface.

Disclose known problems:

- Foundation or structural issues

- Roof leaks or damage

- Plumbing or electrical problems

- Environmental hazards

- Permit violations

Buyers expect issues with distressed properties. Honesty builds trust and leads to smoother transactions.

Gather Documentation in Advance

Having documents ready accelerates the process:

- 📄 Recent mortgage statements

- 📄 Property tax bills

- 📄 HOA documents and fee information

- 📄 Foreclosure notices and timeline

- 📄 Title insurance policy (if available)

- 📄 Lien or judgment documentation

- 📄 Utility bills showing account current or past due

Organized documentation demonstrates seriousness and helps buyers assess situations accurately.

Understand Your Numbers

Know your financial position before negotiating:

Calculate your equity:

Current market value – mortgage balance – liens – selling costs = equity

Determine your minimum acceptable net:

What amount do you need to walk away from closing to move forward?

Consider alternatives:

What happens if you don’t sell? Foreclosure? Bankruptcy? Continuing to struggle with payments?

Understanding your numbers provides clarity about whether offers make sense for your situation.

Get Multiple Offers When Possible

If time permits, contact 2-3 reputable buyers for competitive offers. This helps ensure fair pricing.

Compare offers based on:

- Net proceeds to you

- Closing timeline certainty

- Company reputation and reviews

- Terms and contingencies

- Your comfort level with the buyer

The highest offer isn’t always the best if it comes with contingencies or from questionable operators.

Consult Professionals

Before accepting any offer:

Real estate attorney:

Have attorneys review purchase agreements, especially if terms seem unclear or unusual

Tax professional:

Understand tax implications of sales, forgiven debt, or capital gains

HUD housing counselor:

Free counseling available through HUD-approved agencies to discuss all options

Professional advice costs far less than mistakes made in desperation.

Negotiate Terms Beyond Price

While purchase prices may have limited flexibility, other terms might be negotiable:

Closing timeline:

If you need slightly more or less time, ask

Possession date:

Some buyers allow sellers to remain briefly after closing

Personal property:

Clarify what stays and goes

Rent-back arrangements:

Occasionally buyers allow short-term rent-back periods

Professional buyers want win-win outcomes. Reasonable requests often receive consideration.

Maintain the Property Until Closing

Even though buyers purchase as-is, maintaining properties through closing protects value:

- Keep utilities on

- Maintain basic cleanliness

- Secure the property

- Don’t remove fixtures or appliances

- Continue insurance coverage

Properties that deteriorate between offer and closing may trigger price renegotiations.

Life After Quick Sale: Rebuilding and Moving Forward

Selling quickly to avoid foreclosure solves the immediate crisis, but homeowners still face the task of rebuilding financial stability.

Understanding Credit Impact

Quick sales that pay off mortgages before foreclosure minimize credit damage:

Best case scenario:

If the sale occurs before any missed payments report, credit remains largely intact

Typical scenario:

Some missed payments reported (30-60-90 days late) cause moderate credit score drops of 60-110 points

Recovery timeline:

- Recent payment history matters most

- Scores begin recovering within 6-12 months

- Full recovery possible within 2-3 years with responsible credit use

Compare this to foreclosure’s 200-300 point drop and seven-year recovery period, and the advantage becomes clear.

Tax Considerations

Consult tax professionals about potential implications:

Capital gains:

If properties sold for more than purchase price, capital gains taxes may apply (though primary residence exclusions often eliminate this)

Cancellation of debt income:

If short sales forgive debt, that forgiven amount may count as taxable income (though insolvency and primary residence exceptions often apply)

Deductible expenses:

Some selling costs may be tax deductible

Tax laws change frequently, making professional advice essential.

Finding New Housing

After quick sales, homeowners need new housing:

Rental options:

- Explain situation honestly to landlords

- Offer larger deposits if needed

- Provide references from previous landlords

- Consider private landlords over large management companies

Rebuilding toward ownership:

- Focus on credit repair

- Build emergency savings

- Research FHA loans (available 3 years after foreclosure alternatives)

- Consider homeownership counseling programs

Financial Recovery Steps

Use the experience as a learning opportunity:

- Create realistic budgets based on actual income

- Build emergency funds to weather future setbacks

- Address underlying issues that led to financial distress

- Seek financial counseling if needed

- Monitor credit reports for accuracy

- Establish positive payment history on all remaining obligations

Emotional Recovery

The stress of foreclosure and rapid sale takes emotional tolls:

- Allow yourself to grieve the loss

- Recognize the courage it took to act

- Focus on the fresh start ahead

- Seek support from friends, family, or counselors

- Celebrate stopping foreclosure before it destroyed your credit

The Avoid Foreclosure Sell Quickly: 7-Day Sale Guarantee provides more than financial relief—it offers peace of mind and the opportunity to move forward.

Frequently Asked Questions About Quick Foreclosure Sales

Will I owe money after the sale?

If the sale pays off your mortgage and all liens completely, you owe nothing further. Any remaining proceeds belong to you. This represents a key advantage over foreclosure, which may result in deficiency judgments.

How much will I net from a quick sale?

Net proceeds depend on:

- Property value

- Mortgage balance

- Liens and back taxes

- Selling costs

Many homeowners facing foreclosure have little or no equity. The primary benefit is stopping foreclosure and avoiding credit damage rather than receiving large cash proceeds.

Can I sell if I’m already in foreclosure?

Yes, you can sell anytime before the foreclosure auction occurs. Once the auction happens and the property sells, you lose ownership and can no longer sell. This makes timing critical.

What if my property is worth less than I owe?

This situation requires a short sale, where lenders agree to accept less than the full mortgage balance. Some quick-sale companies handle short sale negotiations as part of their service.

Do I need an attorney?

While not legally required in all states, having an attorney review documents provides valuable protection. Many attorneys offer flat-fee services for reviewing purchase agreements.

What happens to my belongings?

Purchase agreements specify when you must vacate and remove personal property. Typically, you have until closing or shortly after. Clarify this timeline in your agreement.

Can I sell if there are multiple owners?

Yes, but all owners must agree to the sale and sign the deed. Properties with multiple owners require coordination among all parties.

What if I have tenants?

Properties can sell with tenants in place. Buyers either honor existing leases or negotiate tenant relocation. Disclose tenant situations upfront.

How do I know if the offer is fair?

Compare the offer to:

- Recent comparable sales in your area

- Your property’s condition

- Costs you’re avoiding (repairs, holding costs, realtor fees)

- Your alternatives (foreclosure consequences)

Fair doesn’t always mean top dollar—it means reasonable given circumstances and timeline.

What if I change my mind?

Purchase agreements are binding contracts. Once signed, backing out may have legal and financial consequences. Take time to feel certain before signing.

Taking Action: Your Next Steps to Avoid Foreclosure

Knowledge without action doesn’t stop foreclosure. If you’re facing foreclosure, the time to act is now.

Assess Your Timeline

Determine exactly how much time remains:

- When is the foreclosure auction scheduled?

- How many days until that date?

- What options fit within that timeline?

If the auction occurs in less than 60 days, quick-sale options may be your only realistic choice.

Research Reputable Buyers

Identify 2-3 legitimate companies:

- Search for “cash home buyers” in your area

- Read reviews and check Better Business Bureau ratings

- Verify business credentials and track records

- Look for companies specializing in foreclosure situations

Companies like Sure Path Property Solutions focus specifically on helping homeowners navigate complex situations with helpful solutions and trustworthy service.

Gather Your Documentation

Collect the documents buyers will need:

- Mortgage statements

- Foreclosure notices

- Property tax information

- Lien documentation

- Property details

Having these ready accelerates the evaluation process.

Make Contact

Reach out to reputable buyers:

- Complete online forms or call directly

- Be honest about your situation

- Ask questions about their process

- Request preliminary assessments

Initial consultations cost nothing and create no obligations.

Evaluate Offers Carefully

When offers arrive:

- Review all terms thoroughly

- Calculate your net proceeds

- Understand the timeline

- Ask about any unclear terms

- Consult professionals if needed

Make an Informed Decision

Consider:

- Does this offer solve my immediate problem?

- Are the terms fair given my circumstances?

- Do I trust this company?

- What happens if I don’t accept?

Move Forward with Confidence

Once you’ve made a decision:

- Sign the purchase agreement

- Cooperate with the closing process

- Maintain the property until closing

- Prepare for your transition

- Focus on your fresh start

The Avoid Foreclosure Sell Quickly: 7-Day Sale Guarantee exists to help homeowners in crisis situations. It’s not the right choice for everyone, but for those facing imminent foreclosure with limited time and options, it can be a lifeline.

Conclusion: Speed, Certainty, and Relief When You Need It Most

Foreclosure represents one of life’s most stressful financial crises. The anxiety of impending auctions, the shame of financial struggles, and the uncertainty about the future create overwhelming pressure. Traditional real estate solutions—listing with agents, hoping for qualified buyers, waiting months for closings—simply don’t work when foreclosure dates loom weeks away.

The Avoid Foreclosure Sell Quickly: 7-Day Sale Guarantee offers a different path. It prioritizes what matters most in crisis situations: speed, certainty, and relief. While quick sales may not maximize property value, they accomplish something far more important—they stop foreclosure before it destroys credit, creates deficiency judgments, and eliminates future housing options.

Professional cash buyers provide helpful guidance through the entire process. They handle complicated title issues, coordinate lien payoffs, navigate back taxes, and simplify what would otherwise be impossibly complex situations. Companies specializing in problem properties bring industry experts who’ve seen every complication imaginable.

The seven-day timeline isn’t magic—it’s the result of eliminating the variables that delay traditional sales. No financing contingencies. No inspection negotiations. No buyer cold feet. Just straightforward transactions that close quickly and provide certainty when homeowners need it most.

For homeowners facing foreclosure, the most important step is acting quickly. Every day that passes brings the auction date closer. Every week of inaction reduces options. The Avoid Foreclosure Sell Quickly: 7-Day Sale Guarantee works, but only if homeowners reach out before it’s too late.

If foreclosure threatens your property, don’t wait. Research reputable buyers. Get professional guidance. Understand your options. Make informed decisions. Take control of your situation before the situation controls you.

The path forward exists. Quick-sale programs provide friendly and caring service designed to help homeowners navigate their darkest financial moments. They offer not just transactions, but transformation—from crisis to relief, from uncertainty to fresh starts, from foreclosure to freedom.

Your situation may feel hopeless, but solutions exist. The Avoid Foreclosure Sell Quickly: 7-Day Sale Guarantee has helped thousands of homeowners stop foreclosure, preserve their credit, and move forward with their lives. It can help you too—but only if you take that first step and reach out for help.

The auction date doesn’t care about your circumstances. It doesn’t wait for better times or easier solutions. But you don’t have to face it alone. Professional help is available, ready to provide the expert service and helpful solutions that turn foreclosure nightmares into manageable transitions.

Take action today. Your future self will thank you.