Imagine discovering that your property has a judgment lien attached to it—a legal claim that prevents you from selling, refinancing, or accessing your home's equity. This unwelcome surprise affects thousands of property owners each year, creating obstacles that seem insurmountable. The good news? Understanding how to satisfy a judgment lien: payment, release & removal can transform this challenging situation into a manageable process with clear, actionable steps toward resolution.

A judgment lien represents a creditor's legal right to your property following a court ruling. Whether it stems from unpaid debts, contractor disputes, or legal judgments, this encumbrance clouds your property title and limits your options. However, with helpful guidance and expert service, property owners can navigate the satisfaction process successfully and regain control of their real estate assets.

This comprehensive guide walks through every aspect of judgment lien satisfaction—from understanding what these liens mean to executing payment strategies, obtaining proper releases, and ensuring complete removal from public records. For property owners facing liens and judgments, this information provides the roadmap to clear title and financial freedom.

Key Takeaways

- Judgment liens attach to property after court rulings and must be satisfied before selling or refinancing

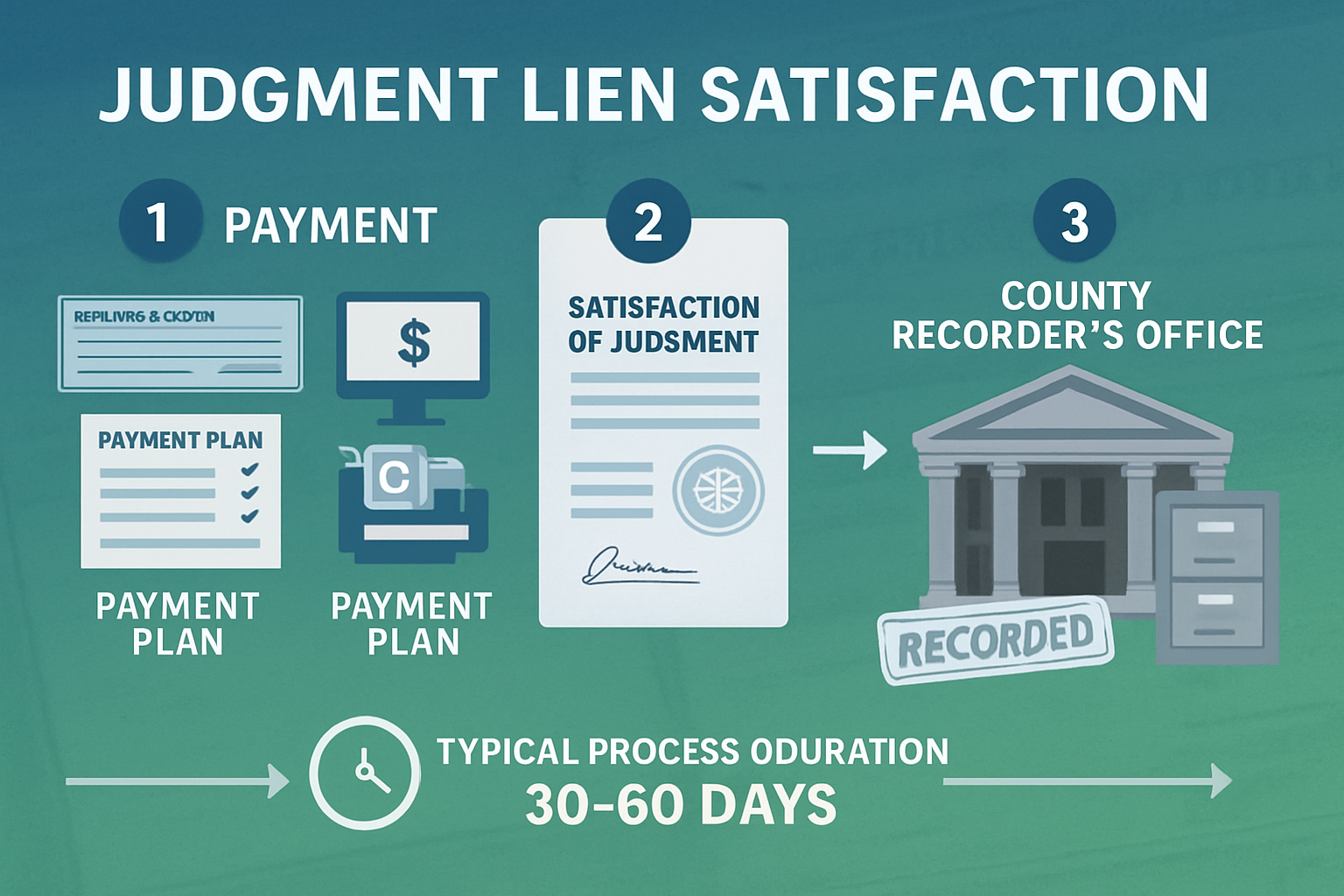

- Three critical steps ensure complete removal: paying the debt, obtaining a satisfaction of judgment, and recording the release with the county

- Multiple payment options exist including full payment, negotiated settlements, payment plans, and using property sale proceeds

- Proper documentation is essential—without recorded satisfaction, the lien remains even after payment

- Professional assistance can expedite the process and prevent costly mistakes that delay resolution

Understanding Judgment Liens and Their Impact on Property

Before diving into how to satisfy a judgment lien: payment, release & removal, property owners need to understand exactly what they're dealing with and why prompt action matters.

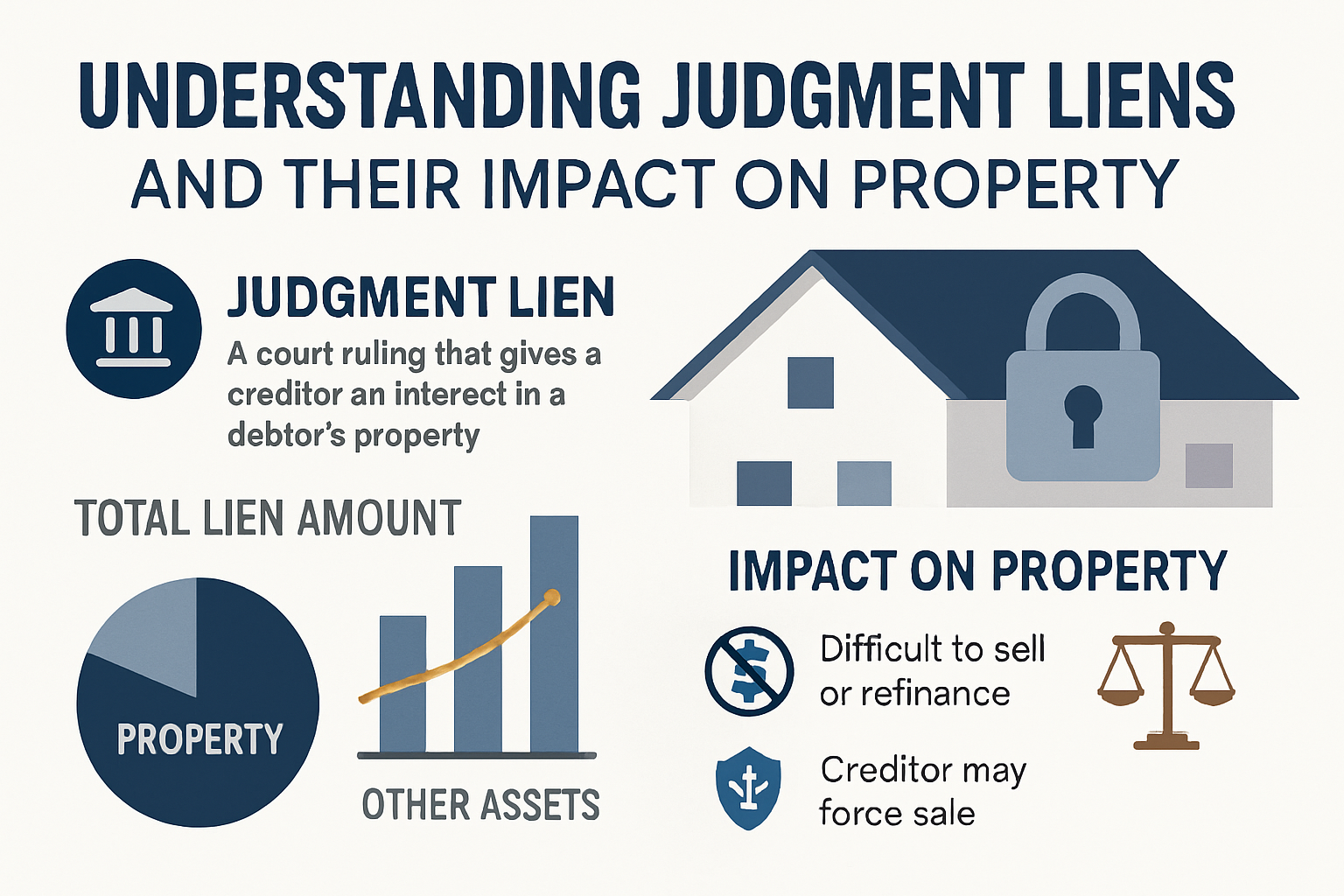

What Is a Judgment Lien?

A judgment lien is a court-ordered claim against your property that results from a lawsuit where a creditor won a monetary judgment against you. Unlike voluntary liens (such as mortgages you agree to), judgment liens are involuntary—they're imposed by the legal system to secure a debt you owe.

These liens typically arise from:

- 💳 Unpaid credit card debts that resulted in lawsuits

- 🏥 Medical bills that went to collections and court

- 🏗️ Contractor disputes where payment wasn't made

- ⚖️ Personal injury judgments from accidents or damages

- 💰 Business debts and commercial obligations

- 🏦 Deficiency judgments after foreclosure

Once a creditor obtains a court judgment, they can file it with the county recorder's office, creating a lien that attaches to any real property you own in that county. This transforms an unsecured debt into a secured claim against your home or land.

How Judgment Liens Affect Property Ownership

The impact of a judgment lien extends far beyond a simple notation on public records. These encumbrances create real, tangible obstacles for property owners:

Selling Becomes Complicated 📉

When you attempt to sell your property, the title search will reveal the judgment lien. Most buyers won't proceed with a purchase until all liens are cleared. The lien must typically be satisfied at closing, with proceeds from the sale going directly to the judgment creditor before you receive any funds.

Refinancing Gets Blocked 🚫

Lenders require clear title before approving refinance applications. A judgment lien signals financial distress and creates a competing claim against the property, making refinancing extremely difficult or impossible until the lien is satisfied.

Equity Access Is Limited 🔒

Home equity lines of credit (HELOCs) and second mortgages become unavailable when judgment liens exist. The lien holder has a claim to your equity, preventing you from accessing it for home improvements, emergencies, or other needs.

Credit Damage Persists 📊

Judgment liens appear on credit reports and public records, significantly damaging credit scores. This impact can last for years, affecting your ability to secure loans, rent apartments, or even obtain employment in certain fields.

For property owners dealing with multiple complications, understanding how these liens interact with other title issues becomes crucial for developing effective solutions.

State-Specific Lien Laws and Timeframes

Judgment lien laws vary significantly by state, affecting how long liens remain valid and what property they can attach to:

| State Characteristic | Typical Range | Impact on Property Owners |

|---|---|---|

| Lien Duration | 5-20 years | Determines how long the lien remains enforceable |

| Renewal Options | Varies by state | Creditors may extend liens beyond initial period |

| Homestead Exemptions | $5,000-$600,000+ | Protects primary residence equity from certain liens |

| Property Types Covered | Real property, sometimes personal | Defines what assets are at risk |

Some states allow judgment liens to attach only to real estate, while others extend them to personal property. Understanding your state's specific rules helps determine the urgency and strategy for satisfaction.

Important consideration: Even if a judgment lien expires, the underlying judgment may remain enforceable, allowing the creditor to renew the lien or pursue other collection methods. This makes proactive satisfaction the most reliable path to resolution.

The Complete Process: How to Satisfy a Judgment Lien: Payment, Release & Removal

Successfully removing a judgment lien requires following a specific sequence of steps. Skipping any stage can leave the lien in place even after you've paid the debt. This section provides helpful solutions for navigating each phase with confidence.

Step 1: Verify the Judgment Details

Before making any payments, confirm exactly what you owe and to whom. This verification prevents overpayment and ensures you're dealing with the legitimate creditor.

Obtain Official Documentation 📄

Contact the court clerk in the county where the judgment was entered. Request certified copies of:

- The original judgment order

- Any modifications or amendments

- Calculation of current balance including interest

- Proof of lien recording

Calculate the Total Amount Due 🧮

Judgment balances grow over time due to:

- Post-judgment interest (rates vary by state, typically 4-10% annually)

- Court costs and filing fees added to the original amount

- Attorney fees if specified in the judgment

- Collection costs that may have accrued

Many property owners are surprised to discover their $10,000 judgment has grown to $15,000 or more over several years. Getting an exact payoff amount prevents the frustration of partial payments that don't fully satisfy the lien.

Confirm the Creditor's Information ✅

Judgments are sometimes sold to collection agencies or assigned to new creditors. Verify:

- Current legal owner of the judgment

- Proper payment address and instructions

- Contact information for obtaining satisfaction documents

- Any special requirements for payment methods

This verification protects against fraudulent payment requests and ensures your payment reaches the right party.

Step 2: Explore Payment Options and Strategies

Understanding how to satisfy a judgment lien: payment, release & removal includes knowing you have multiple payment approaches, each with distinct advantages depending on your financial situation.

Full Payment in Lump Sum

The fastest route to satisfaction involves paying the entire judgment amount at once. This approach:

- ✅ Eliminates ongoing interest accumulation

- ✅ Provides immediate grounds for obtaining release

- ✅ Simplifies the satisfaction process

- ✅ Demonstrates financial responsibility to other creditors

Payment methods typically accepted:

- Cashier's check or certified funds

- Wire transfer to creditor's account

- Attorney trust account check

- Money order for smaller amounts

Pro Tip: Always obtain a detailed receipt showing the judgment case number, payment amount, date, and confirmation that this payment satisfies the judgment in full. This documentation becomes critical if disputes arise later.

Negotiated Settlement for Less Than Full Amount

Many judgment creditors will accept reduced payments rather than risk collecting nothing. Settlement negotiations can reduce your payment by 30-70% in some cases.

When settlements work best:

- The judgment is several years old

- The creditor has had difficulty collecting

- You can offer immediate payment

- The creditor wants to avoid further legal costs

- The judgment was sold to a collection agency at a discount

Negotiation strategy:

- Research the creditor's history with settlements

- Make a realistic initial offer (typically 40-60% of balance)

- Emphasize your willingness to pay immediately upon agreement

- Request settlement terms in writing before sending payment

- Ensure the agreement specifies full satisfaction of the judgment

Critical requirement: Any settlement agreement must explicitly state that the payment satisfies the judgment in full. Without this language, the creditor might accept your payment but claim the remaining balance is still owed.

For property owners considering selling property with liens, negotiated settlements often make financial sense, as the alternative is paying the full amount from sale proceeds anyway.

Payment Plans and Installment Agreements

Some creditors accept monthly payment arrangements, though this approach has limitations for lien satisfaction.

Important reality: Most creditors won't release the judgment lien until you've paid in full, even if they agree to installment payments. The lien remains attached to your property throughout the payment period.

Payment plan considerations:

- Interest continues accruing during the payment period

- The lien blocks property transactions until final payment

- Missed payments may trigger immediate full balance demands

- Written agreements are essential to protect both parties

Payment plans work best when you're not immediately selling or refinancing and need time to gather funds for eventual lump-sum satisfaction.

Using Property Sale Proceeds

When selling property with a judgment lien, the lien is typically satisfied at closing using sale proceeds. This approach:

- Ensures the lien is paid before you receive any funds

- Provides clear title to the buyer

- Simplifies the satisfaction process

- Protects all parties through escrow handling

How it works:

- The title company identifies all liens during the title search

- Lien payoff amounts are calculated as of closing date

- Settlement statement shows lien payments as deductions from seller proceeds

- Title company pays creditors directly and obtains satisfaction documents

- Releases are recorded, clearing title for the new owner

This method provides peace of mind that the lien satisfaction is handled correctly by professionals. For those exploring how to sell a house with a lien, this represents the most common and reliable approach.

Step 3: Obtain a Satisfaction of Judgment

Payment alone doesn't remove a judgment lien. You must obtain official documentation confirming the judgment has been satisfied.

The Satisfaction of Judgment Document 📋

This legal document, also called an "Acknowledgment of Satisfaction" or "Release of Judgment," officially states that:

- The judgment has been paid in full (or settled)

- The creditor releases all claims against the debtor

- The lien should be removed from the property

Who prepares it:

- The judgment creditor or their attorney typically prepares the document

- Some courts provide standard satisfaction forms

- Your attorney can draft it if the creditor is uncooperative

Essential elements:

- Case number and court where judgment was entered

- Names of all parties (plaintiff/creditor and defendant/debtor)

- Original judgment amount and date

- Statement that judgment is satisfied in full

- Date of satisfaction

- Creditor's signature (must be notarized in most states)

Timeline expectations:

Most states require creditors to provide satisfaction documents within 14-30 days after receiving full payment. If the creditor delays or refuses, you can petition the court to enter satisfaction and compel the creditor to comply.

Step 4: Record the Satisfaction with the County

The final critical step in how to satisfy a judgment lien: payment, release & removal involves recording the satisfaction document with the same county recorder's office where the original lien was filed.

Why recording matters:

Until the satisfaction is recorded in public records, the lien technically remains attached to your property. Title searches will continue showing the lien, blocking transactions even though you've paid the debt.

Recording process:

- Obtain the original or certified copy of the satisfaction document

- Visit or mail documents to the county recorder's office where the lien was recorded

- Pay the recording fee (typically $15-50)

- Request a recorded copy for your records

- Verify the lien shows as released in the county's online records (usually updates within 1-2 weeks)

Multiple properties consideration:

If you own property in several counties and the creditor recorded the judgment in multiple locations, you must record the satisfaction in each county where the lien appears. A satisfaction recorded in one county doesn't automatically clear liens in other counties.

Documentation to keep:

- Proof of payment to the creditor

- Original satisfaction of judgment document

- Recorded satisfaction with county stamp

- Correspondence with creditor regarding the satisfaction

These documents protect you if questions arise later about whether the lien was properly satisfied and released.

Common Challenges and Solutions in Lien Satisfaction

Even with the best intentions, property owners encounter obstacles when satisfying judgment liens. Recognizing these challenges and knowing how to address them provides helpful guidance through the process.

When the Creditor Can't Be Located

Judgment creditors sometimes disappear—businesses close, individuals move without forwarding addresses, or collection agencies go out of business. This creates a frustrating situation where you want to pay but can't find who to pay.

Solutions for missing creditors:

Court Petition for Satisfaction ⚖️

File a motion with the court that entered the original judgment, requesting:

- Declaration that you've made good-faith efforts to locate the creditor

- Evidence of the creditor's disappearance

- Court order declaring the judgment satisfied

- Authorization to record the satisfaction

Courts generally grant these petitions when you can demonstrate reasonable efforts to find the creditor and willingness to pay the debt.

Deposit Funds with the Court 💰

Some jurisdictions allow you to deposit the judgment amount with the court clerk, who holds the funds for the creditor. Once deposited, the court enters satisfaction of the judgment, releasing the lien even though the creditor hasn't been located.

Title Insurance Solutions 🛡️

When selling property, title companies may issue title insurance covering the old judgment lien if:

- The lien is very old (10+ years)

- The amount is relatively small

- You provide an indemnity agreement

- Evidence suggests the creditor is defunct

This doesn't technically satisfy the lien but allows the transaction to proceed with the buyer protected.

Disputing Incorrect or Invalid Liens

Sometimes judgment liens appear on property records incorrectly—wrong property, wrong person, or judgments that were already paid.

Steps to dispute invalid liens:

- Gather evidence proving the lien is incorrect (payment records, identity documents, property records)

- Contact the creditor with documentation requesting voluntary release

- File a motion to vacate or release the lien in the court that entered the judgment

- Present evidence at a hearing demonstrating the error

- Obtain court order directing release of the lien

- Record the court order with the county recorder

Common scenarios requiring disputes:

- Identity confusion: Lien filed against someone with a similar name

- Property misidentification: Wrong parcel number or address

- Already satisfied: Payment made but satisfaction never recorded

- Expired liens: Judgment exceeded the statutory enforcement period

- Bankruptcy discharge: Judgment was discharged but lien not released

Professional assistance from attorneys experienced in title issues can expedite dispute resolution and prevent costly delays.

Dealing with Multiple Judgment Liens

Property owners sometimes face several judgment liens simultaneously, creating complex prioritization decisions.

Lien priority matters:

Judgment liens generally take priority based on recording date—the first recorded has first claim to property proceeds. However, certain liens (like property tax liens) may have "super priority" that places them ahead of earlier-recorded judgment liens.

Strategic approach to multiple liens:

Assess total lien amounts versus property value 📊

If total liens exceed property value, you're in a negative equity situation. Consider:

- Bankruptcy options that might discharge some judgments

- Short sale possibilities if selling

- Lien negotiation leveraging limited equity available

Prioritize liens blocking immediate goals 🎯

If you need to sell or refinance quickly:

- Focus first on liens that must be cleared for the transaction

- Negotiate with lower-priority lien holders who might receive nothing in foreclosure

- Determine which liens the title company requires satisfied

Negotiate package settlements 💼

Some creditors offer better settlement terms when you're satisfying multiple obligations simultaneously. This demonstrates serious commitment to resolving debts and may yield better overall savings.

For property owners navigating complex situations with multiple liens and title problems, professional guidance helps prioritize actions and maximize available resources.

Handling Liens During Property Sales

Selling property with judgment liens requires coordination between multiple parties and careful timing.

The closing process with liens:

Title Search Reveals All Liens 🔍

Early in the transaction, the title company conducts a comprehensive search identifying all recorded liens. This typically occurs within days of opening escrow.

Payoff Demands Are Requested 📨

The title company contacts each lien holder requesting an official payoff statement showing the exact amount required to satisfy the lien as of the anticipated closing date.

Settlement Statement Shows Deductions 📑

The HUD-1 or closing disclosure itemizes all lien payoffs as deductions from the seller's proceeds, ensuring transparency about where funds are going.

Simultaneous Satisfaction and Recording ⏱️

At closing, the title company:

- Disburses payment to lien holders

- Obtains satisfaction documents

- Records satisfactions with the county

- Ensures clear title transfers to the buyer

Potential complications:

- Insufficient proceeds: When sale price doesn't cover all liens, you may need to bring money to closing or negotiate short payoffs

- Creditor delays: Slow response to payoff requests can delay closing

- Last-minute liens: New liens recorded just before closing require quick resolution

Working with experienced professionals who understand the complete process of selling with liens helps avoid these pitfalls and ensures smooth transactions.

Alternative Approaches to Judgment Lien Resolution

While direct payment represents the most straightforward path, other legal mechanisms can resolve judgment liens depending on your circumstances.

Bankruptcy and Judgment Discharge

Bankruptcy offers powerful tools for dealing with judgment liens, though the specifics depend on the bankruptcy chapter filed.

Chapter 7 Bankruptcy 🏛️

Chapter 7 liquidation bankruptcy can:

- Discharge the underlying debt that led to the judgment

- Eliminate your personal liability for the judgment amount

- Prevent future collection efforts on the discharged debt

However: Chapter 7 doesn't automatically remove judgment liens already recorded against property. The lien survives bankruptcy and remains attached to the property even though you no longer personally owe the debt.

Lien avoidance in Chapter 7:

You can petition the bankruptcy court to "avoid" (remove) certain judgment liens if:

- The lien impairs your homestead exemption

- The property is your primary residence

- The lien is a judicial lien (not a mortgage or tax lien)

When successful, lien avoidance removes the judgment lien entirely, even though the property wasn't sold.

Chapter 13 Bankruptcy 📋

Chapter 13 reorganization bankruptcy allows you to:

- Include judgment debts in your repayment plan

- Pay reduced amounts (sometimes pennies on the dollar)

- Strip off wholly unsecured judgment liens in some cases

- Protect property from foreclosure while catching up on payments

After completing a Chapter 13 plan (typically 3-5 years), remaining balances on judgment debts are discharged, and liens must be released.

Important consideration: Bankruptcy has significant credit implications and should be carefully evaluated with legal counsel. For some property owners, particularly those with multiple financial challenges, bankruptcy provides the fresh start needed to move forward.

Waiting for Lien Expiration

Judgment liens don't last forever. Each state sets a specific enforcement period, after which liens become unenforceable.

Typical expiration periods:

- 5-7 years: Shorter duration states

- 10 years: Most common timeframe

- 20+ years: Longer duration states

Renewal provisions:

Many states allow creditors to renew judgment liens before expiration, extending them for another full term. This means a 10-year lien could potentially last 20 years if renewed.

When waiting makes sense:

- The judgment amount is small relative to property value

- You're not planning to sell or refinance soon

- The creditor appears inactive and unlikely to renew

- The lien is approaching expiration

Risks of waiting:

- Interest continues accumulating, increasing the debt

- Creditors may pursue other collection methods

- Renewed liens extend the problem for years

- Uncertainty affects financial planning

For most property owners, proactive satisfaction provides more certainty and control than hoping liens expire.

Bonding Around the Lien

In some situations, you can post a bond that substitutes for the judgment lien, allowing property transactions to proceed while the underlying dispute continues.

How lien bonds work:

- You purchase a surety bond equal to the judgment amount

- The bond replaces the property lien as security for the creditor

- Your property is released from the lien

- The creditor can claim against the bond if they ultimately prevail

When bonds are useful:

- You're disputing the judgment's validity

- You need to sell property quickly

- The judgment amount is moderate (bonds become expensive for large amounts)

- You have good credit to qualify for bonding

Costs and requirements:

Surety bonds typically cost 1-15% of the bond amount annually, depending on your creditworthiness. You'll need to qualify financially and may need to pledge collateral to the bonding company.

Professional Help: When to Seek Expert Assistance

While some judgment lien satisfactions are straightforward, many situations benefit from professional guidance. Knowing when to seek expert service can save time, money, and frustration.

Situations Requiring Legal Assistance

Complex multi-lien scenarios 🏗️

When multiple judgment liens, tax liens, and mortgages create competing claims, an attorney can:

- Determine proper lien priority

- Negotiate with multiple creditors simultaneously

- Identify which liens must be satisfied for your goals

- Protect your interests in complex transactions

Disputed or contested judgments ⚖️

If you believe the judgment was entered incorrectly or unfairly:

- Legal expertise is essential for filing appeals or motions to vacate

- Attorneys understand procedural requirements and deadlines

- Professional representation increases success rates significantly

Uncooperative creditors 🚧

When creditors refuse to provide satisfaction documents after payment or can't be located:

- Attorneys can file court petitions compelling satisfaction

- Legal pressure often motivates creditor cooperation

- Court orders provide alternative paths to lien release

Bankruptcy considerations 💼

The intersection of bankruptcy and judgment liens requires specialized knowledge:

- Bankruptcy attorneys understand which liens can be avoided

- Timing of bankruptcy filing affects lien treatment

- Strategic planning maximizes debt relief while protecting property

How Property Solutions Companies Can Help

Companies specializing in complicated real estate situations, like Sure Path Property Solutions, offer valuable assistance for property owners dealing with judgment liens.

Comprehensive situation assessment 🔍

Industry experts can evaluate your complete situation, including:

- All liens and encumbrances affecting the property

- Property value and equity position

- Your financial goals and timeline

- Available resolution strategies

This holistic approach identifies solutions that address multiple challenges simultaneously rather than focusing narrowly on a single lien.

Coordination with multiple parties 🤝

Resolving judgment liens often requires coordinating with:

- Creditors and their attorneys

- Title companies

- County recorder's offices

- Courts and court clerks

- Real estate professionals

Property solutions companies handle this coordination, saving you countless phone calls and follow-ups while ensuring nothing falls through the cracks.

Creative problem-solving 💡

Experienced professionals have seen numerous variations of lien situations and can suggest helpful solutions you might not have considered:

- Alternative transaction structures

- Negotiation strategies based on creditor behavior patterns

- Timing strategies that maximize available options

- Resource connections for specialized needs

Transaction facilitation 🏡

If selling property represents your best path forward, property solutions companies can:

- Purchase properties with liens directly

- Handle all lien satisfaction at closing

- Provide certainty and speed compared to traditional sales

- Eliminate the stress of managing the process yourself

For property owners feeling overwhelmed by judgment liens and other complications, reaching out for expert guidance can transform a seemingly impossible situation into a manageable path forward.

Preventing Future Judgment Liens

Once you've successfully navigated how to satisfy a judgment lien: payment, release & removal, taking steps to prevent future liens protects your property and financial stability.

Responding to Lawsuits Promptly

Never ignore legal notices ⚠️

Many judgment liens result from default judgments—court rulings entered when defendants fail to respond to lawsuits. Even if you can't pay the debt immediately:

- File a response to the lawsuit within the deadline

- Appear at scheduled hearings

- Communicate with the creditor about payment arrangements

- Consider legal representation for significant claims

Engaging with the legal process provides opportunities to:

- Negotiate settlements before judgment

- Challenge incorrect claims

- Establish payment plans that avoid liens

- Reduce the final judgment amount

Maintaining Open Communication with Creditors

Proactive contact prevents escalation 📞

When facing financial difficulties:

- Contact creditors before accounts go to collections

- Explain your situation honestly

- Propose realistic payment arrangements

- Request hardship programs if available

Most creditors prefer receiving some payment over pursuing costly litigation. Open communication often yields manageable solutions that prevent judgment liens entirely.

Understanding Your Rights

Fair debt collection practices 📜

Federal and state laws protect consumers from abusive collection practices. Understanding these rights helps you:

- Identify illegal collection tactics

- Demand proper documentation of debts

- Challenge incorrect information

- Protect your property from improper liens

Statute of limitations ⏰

Each state sets time limits for filing lawsuits on different types of debts. Once the statute of limitations expires, creditors can't obtain new judgments (though they may still attempt collection).

Knowing these timeframes helps you:

- Understand your vulnerability to new lawsuits

- Make informed decisions about old debts

- Avoid inadvertently restarting expired limitation periods

Exemption protections 🛡️

State and federal laws exempt certain property from creditor claims:

- Homestead exemptions protect primary residence equity

- Personal property exemptions cover essential items

- Retirement account protections shield certain savings

Understanding these exemptions helps you protect assets while resolving debts responsibly.

Real-World Examples: Judgment Lien Satisfaction Success Stories

Seeing how others have successfully navigated judgment lien satisfaction provides helpful guidance and encouragement for property owners facing similar challenges.

Case Study 1: Medical Debt Judgment Settlement

The situation: Sarah inherited her grandmother's home but discovered a $23,000 judgment lien from a hospital bill her grandmother had incurred years earlier. The lien prevented Sarah from selling the property to settle the estate.

The challenge: Sarah didn't have $23,000 plus accumulated interest to pay the judgment, and the estate had limited liquid assets.

The solution:

- Sarah contacted the collection agency holding the judgment

- She explained the estate situation and offered $8,000 for full satisfaction

- The agency initially countered at $15,000

- After negotiation, they agreed to $10,000 paid within 30 days

- Sarah used a portion of estate funds to make the payment

- The creditor provided satisfaction documents within two weeks

- The satisfaction was recorded, clearing title for the estate sale

The outcome: Sarah saved $13,000 plus interest through negotiation, allowing the estate to be settled and the property sold. The entire process took six weeks from initial contact to recorded satisfaction.

Key lesson: Creditors often accept reduced payments rather than risk collecting nothing, especially when dealing with estates or older judgments.

Case Study 2: Contractor Lien Through Property Sale

The situation: James needed to sell his property quickly for a job relocation but discovered a $47,000 judgment lien from a contractor dispute three years earlier.

The challenge: The judgment amount exceeded James's available cash, and the creditor refused to negotiate a settlement.

The solution:

- James listed the property with full disclosure of the lien

- The title company calculated the exact payoff including interest

- At closing, the lien was paid directly from sale proceeds

- The title company obtained and recorded the satisfaction

- James received his remaining equity after all liens were satisfied

The outcome: While James received less from the sale than hoped, the transaction proceeded smoothly, and he avoided the lien following him to his new state. The title company's handling of the satisfaction ensured proper documentation and recording.

Key lesson: Property sale proceeds provide a reliable method for satisfying liens when cash isn't available, and professional handling by title companies ensures proper completion.

Case Study 3: Bankruptcy Lien Avoidance

The situation: Maria faced $85,000 in judgment liens against her home from credit card lawsuits, plus other unsecured debts totaling $120,000. Her home was worth $200,000 with a $140,000 mortgage.

The challenge: The judgment liens prevented refinancing to a lower interest rate, and Maria couldn't afford to pay them while managing other debts.

The solution:

- Maria consulted a bankruptcy attorney who evaluated her situation

- She filed Chapter 7 bankruptcy, discharging the underlying debts

- Her attorney filed motions to avoid the judgment liens as they impaired her homestead exemption

- The bankruptcy court granted the motions, removing all judgment liens

- The underlying debts were discharged, and the liens were eliminated

The outcome: Maria emerged from bankruptcy with no judgment liens, no personal liability for the discharged debts, and the ability to refinance her mortgage, saving $400 monthly.

Key lesson: Bankruptcy provides powerful tools for removing judgment liens when they impair homestead exemptions, offering a fresh start for overwhelmed homeowners.

Frequently Asked Questions About Judgment Lien Satisfaction

How long does it take to remove a judgment lien after payment?

The timeline varies but typically includes:

- Immediate to 30 days: Creditor provides satisfaction documents after receiving payment

- 1-3 days: Recording the satisfaction with the county

- 1-2 weeks: County records update to reflect the release

Total timeline: 2-6 weeks in most cases, though delays can extend this if creditors are slow to provide satisfaction documents.

Can I sell my house with a judgment lien on it?

Yes, you can sell property with judgment liens, but the lien must be satisfied from the sale proceeds before closing. The title company handles this process, ensuring the creditor is paid and the lien is released so clear title transfers to the buyer.

What happens if I pay the judgment but the creditor won't provide a satisfaction?

If a creditor refuses to provide satisfaction documents after receiving full payment:

- Send a formal written demand citing your state's laws requiring satisfaction

- File a motion with the court requesting an order compelling satisfaction

- The court can enter satisfaction and order the creditor to comply

- You may be entitled to attorney fees and damages for the creditor's refusal

Most states impose penalties on creditors who wrongfully refuse to acknowledge satisfaction.

Do judgment liens affect my credit score?

Yes, judgment liens negatively impact credit scores by:

- Appearing in public records sections of credit reports

- Signaling financial distress to lenders

- Remaining on credit reports for 7 years from the filing date

- Reducing creditworthiness for loans and credit applications

Satisfying the lien doesn't immediately remove it from credit reports, but it changes the status to "satisfied," which is less damaging than an outstanding judgment.

Can a judgment lien force the sale of my home?

In most states, judgment lien holders cannot directly force the sale of your primary residence. However:

- They can wait until you sell and collect from the proceeds

- In some states, they can force a judicial sale after the homestead exemption is exceeded

- The lien remains attached until satisfied, limiting your options

Mortgage lenders and tax authorities have stronger foreclosure rights than general judgment creditors.

What if the judgment lien is in the wrong amount?

If the recorded lien shows an incorrect amount:

- Contact the creditor with documentation of the correct amount

- Request an amended satisfaction or correction

- If the creditor refuses, file a motion with the court to correct the judgment

- Present evidence of the proper amount

- Obtain a court order correcting the lien amount

Never pay an incorrect amount without resolving the discrepancy first, as this can create confusion about whether the judgment is fully satisfied.

Taking Action: Your Next Steps Toward Lien-Free Property

Understanding how to satisfy a judgment lien: payment, release & removal empowers property owners to take control of their situation and move forward with confidence. The path from discovery to complete removal follows clear steps, and helpful solutions exist for even the most complicated scenarios.

Immediate Actions to Take Today

1. Gather all documentation 📁

Collect every document related to the judgment lien:

- Original judgment paperwork

- Lien recording information

- Payment records if any payments were made

- Correspondence with creditors

- Property records and title reports

Having complete information provides the foundation for effective action.

2. Calculate your exact payoff amount 🧮

Contact the creditor or court clerk to determine:

- Current principal balance

- Accumulated interest through today

- Any additional fees or costs

- Acceptable payment methods

- Contact information for satisfaction documents

Knowing the precise amount prevents partial payments that don't fully resolve the lien.

3. Assess your financial options 💰

Review your available resources:

- Cash savings that could pay the judgment

- Property equity that could be accessed through sale

- Settlement negotiation potential

- Payment plan possibilities

- Bankruptcy as a last resort option

Honest assessment of your financial position guides strategy selection.

4. Consult with professionals 🤝

Reach out for expert guidance from:

- Real estate attorneys for legal advice

- Property solutions companies for transaction assistance

- Title companies if selling property

- Bankruptcy attorneys if considering that option

Professional input often reveals solutions and strategies you hadn't considered, potentially saving thousands of dollars and months of time.

Why Professional Guidance Makes a Difference

Navigating judgment lien satisfaction involves legal procedures, negotiation skills, and detailed documentation. While some property owners successfully handle the process independently, many benefit from trustworthy service and expert guidance.

Sure Path Property Solutions specializes in helping property owners facing complicated situations including judgment liens, tax issues, and title problems. With industry experts who understand the challenges and friendly and caring professionals who prioritize your goals, the path to resolution becomes clearer and more manageable.

Whether you're dealing with a single judgment lien or multiple encumbrances affecting your property, professional assistance can:

- Simplify complex situations by handling coordination and paperwork

- Expedite resolution through established relationships with creditors and courts

- Maximize your financial outcome through skilled negotiation

- Reduce stress by managing the process on your behalf

- Prevent costly mistakes that could delay satisfaction or create new problems

The Path Forward: From Burden to Opportunity

A judgment lien may seem like an insurmountable obstacle, but thousands of property owners successfully satisfy these liens every year and move forward with their real estate goals. The key lies in understanding the process, taking prompt action, and seeking helpful guidance when needed.

Your property represents significant value—both financial and personal. Don't let a judgment lien prevent you from accessing that value or achieving your goals. With the right approach and expert service, you can transform this challenge into a resolved issue and a clear path forward.

Conclusion

Understanding how to satisfy a judgment lien: payment, release & removal transforms what initially appears as an overwhelming obstacle into a manageable process with clear, actionable steps. From verifying judgment details and exploring payment options to obtaining proper satisfaction documents and recording releases with the county, each phase builds toward the ultimate goal: clear title and unrestricted property ownership.

The journey requires attention to detail, patience with bureaucratic processes, and often negotiation skills to achieve optimal outcomes. Whether you choose full payment, negotiated settlement, bankruptcy alternatives, or satisfaction through property sale proceeds, the essential elements remain constant—proper documentation, timely recording, and verification that the lien has been completely removed from public records.

For property owners facing judgment liens alongside other complications such as inherited property challenges, tax issues, or multiple ownership situations, the complexity can feel overwhelming. This is precisely when professional assistance provides the greatest value, offering helpful solutions tailored to your unique circumstances and expert service that navigates the legal and administrative requirements efficiently.

Remember that judgment liens, while serious, represent solvable problems. Every day, property owners successfully satisfy these liens and regain control of their real estate assets. With the information provided in this guide and access to industry experts who specialize in complicated property situations, you have the foundation needed to move forward confidently.

Don't let a judgment lien continue limiting your options or preventing you from achieving your property goals. Take the first step today—whether that's contacting the creditor, consulting with professionals, or reaching out to Sure Path Property Solutions for a comprehensive evaluation of your situation. The path to lien-free property ownership begins with a single action, and helpful guidance is available every step of the way.

Your property deserves a clear title, and you deserve the peace of mind that comes with complete lien satisfaction. The knowledge, resources, and professional support exist to make that outcome a reality. Take action today and begin your journey toward unrestricted property ownership.

Sure Path is a family-owned, curative-title cash buyer. We handle the paperwork and pay what’s owed at closing — no fees, no repairs, no pressure.