Involuntary Lien Examples: Types, Impact & Removal Strategies

Imagine discovering that someone has placed a legal claim on your property—without your permission or signature. This isn’t a nightmare scenario; it’s the reality of involuntary liens, and they affect thousands of property owners across the United States every year. Unlike voluntary liens that property owners agree to (like mortgages), involuntary liens are imposed by creditors, government agencies, or courts to secure unpaid debts or obligations.

Understanding

Involuntary Lien Examples: Types, Impact & Removal Strategies is essential for anyone who owns real estate or plans to buy or sell property. These legal encumbrances can derail property sales, damage credit scores, and create significant financial stress. The good news? With the right knowledge and helpful guidance, property owners can navigate these challenges and find practical solutions.

At

Sure Path Property Solutions, we’ve helped countless property owners work through complicated situations involving liens, judgments, and title issues. This comprehensive guide will walk through real-world involuntary lien examples, explain their impact on property ownership, and provide actionable removal strategies that work in 2026.

Key Takeaways

- Involuntary liens are placed on property without the owner’s consent to secure payment for debts, taxes, or legal judgments—understanding the different types helps property owners respond appropriately.

- Tax liens, judgment liens, mechanic’s liens, HOA liens, and child support liens represent the five most common involuntary lien examples that affect property owners nationwide.

- Involuntary liens create serious obstacles for property sales, refinancing, and ownership transfer while potentially damaging credit and triggering foreclosure proceedings.

- Multiple removal strategies exist including full payment, negotiated settlements, lien disputes, payment plans, and in some cases, bankruptcy protection.

- Professional guidance from industry experts can simplify the removal process and help property owners regain clear title more quickly and cost-effectively.

What Are Involuntary Liens?

An involuntary lien is a legal claim placed against property without the owner’s permission or agreement. These liens serve as security for unpaid debts or obligations, giving creditors a legal right to the property’s value.

Think of an involuntary lien like an invisible chain attached to your property. You still own the property and can live in it, but you cannot sell it or refinance it without addressing the lien first. The chain follows the property, not the person—meaning it stays attached even if ownership changes hands.

How Involuntary Liens Differ from Voluntary Liens

The distinction between voluntary and involuntary liens is straightforward:

Voluntary Liens:

- Created with the property owner’s consent

- Examples include mortgages and home equity loans

- Owner signs documents agreeing to the lien

- Typically used to finance property purchases

Involuntary Liens:

- Imposed without owner’s agreement

- Created through legal processes or statutory authority

- No signature required from property owner

- Used to secure payment for debts or obligations

Legal Authority Behind Involuntary Liens

Involuntary liens don’t appear randomly. They’re created through specific legal mechanisms:

🏛️

Statutory liens arise automatically by law when certain conditions are met (like unpaid property taxes).

⚖️

Judicial liens result from court judgments after legal proceedings.

📋

Equitable liens are imposed by courts based on fairness principles.

Each type of involuntary lien follows established legal procedures, providing some protection for property owners while ensuring creditors can collect legitimate debts.

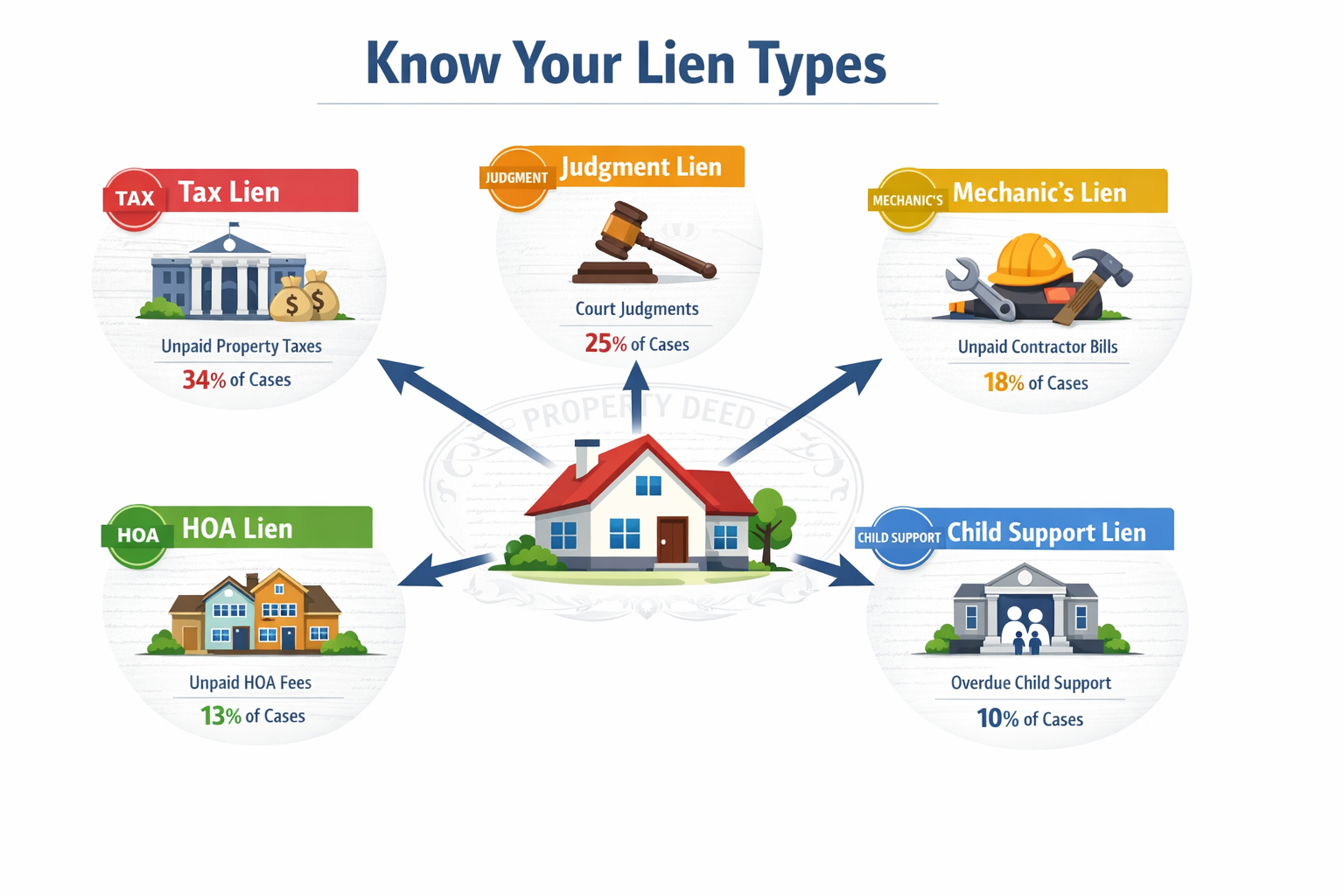

Common Involuntary Lien Examples: The Five Major Types

Understanding the specific types of involuntary liens helps property owners recognize potential problems and take appropriate action. Let’s explore the five most common involuntary lien examples affecting property owners in 2026.

1. Tax Liens: Government Claims for Unpaid Taxes

Tax liens represent one of the most serious involuntary lien examples because government agencies have extraordinary collection powers.

Property Tax Liens

When property owners fall behind on real estate taxes, local governments can place liens on the property. These liens take priority over almost all other claims, including mortgages.

Property tax liens can lead to

tax lien foreclosure if left unresolved. Many counties auction tax lien certificates to investors who pay the back taxes and earn interest when the property owner eventually pays.

Federal Tax Liens (IRS)

The Internal Revenue Service files federal tax liens when taxpayers owe income taxes and don’t pay after receiving notice. These liens attach to all property the taxpayer owns—real estate, vehicles, bank accounts, and even future assets acquired during the lien period.

An IRS tax lien becomes public record, appearing on credit reports and making it nearly impossible to sell property or obtain financing.

State Tax Liens

Similar to federal liens, state revenue departments can file liens for unpaid state income taxes, sales taxes, or other state-level tax obligations. The specific procedures vary by state, but the impact remains severe.

“Tax liens carry tremendous weight in the legal system. They often take priority over other debts, making them particularly challenging for property owners trying to sell or refinance.” — Real Estate Title Expert

2. Judgment Liens: Court-Ordered Claims

Judgment liens result from lawsuits where courts award monetary damages to plaintiffs. Once a creditor obtains a court judgment, they can record it against the debtor’s property.

How Judgment Liens Are Created

The process typically follows these steps:

- Creditor sues debtor in court

- Court awards judgment to creditor

- Creditor records judgment with county recorder

- Judgment becomes a lien on debtor’s real property in that county

Common Sources of Judgment Liens

- Unpaid credit card debts

- Medical bills sent to collections

- Personal loans in default

- Business debts

- Breach of contract claims

- Personal injury awards

Judgment liens can remain in effect for years, often 10-20 years depending on state law, with options for renewal in many jurisdictions.

3. Mechanic’s Liens: Construction and Contractor Claims

Mechanic’s liens protect contractors, subcontractors, and material suppliers who perform work or provide materials for property improvements but don’t receive payment.

Who Can File a Mechanic’s Lien?

- General contractors

- Subcontractors (electricians, plumbers, carpenters)

- Material suppliers (lumber yards, hardware stores)

- Equipment rental companies

- Architects and engineers

- Landscapers

The Mechanic’s Lien Process

Mechanic’s liens follow strict procedural requirements that vary by state:

| Step |

Typical Timeframe |

Requirement |

| Preliminary Notice |

Before or shortly after work begins |

Notice to property owner of right to lien |

| Work Completion |

Varies |

Substantial completion of contracted work |

| Lien Filing |

30-120 days after completion |

Recording lien with county |

| Enforcement Action |

90-365 days after filing |

Lawsuit to foreclose on lien |

Missing deadlines can invalidate a mechanic’s lien, providing property owners with potential defenses.

4. HOA Liens: Homeowners Association Claims

Homeowners associations can place liens on properties when owners fall behind on HOA fees, special assessments, or fines for rule violations.

What Triggers HOA Liens?

- Unpaid monthly or annual HOA dues

- Special assessments for community improvements

- Fines for covenant violations

- Legal fees from HOA enforcement actions

HOA liens can be particularly aggressive. Many HOA governing documents give associations “super lien” status, allowing them to foreclose even when a mortgage exists on the property.

HOA Foreclosure Power

In many states, HOAs can initiate foreclosure proceedings after relatively small amounts go unpaid—sometimes as little as a few hundred dollars. This makes HOA liens among the most dangerous involuntary lien examples for property owners.

5. Child Support Liens: Family Court Obligations

When parents fall behind on court-ordered child support payments, state child support enforcement agencies can file liens against their property.

How Child Support Liens Work

Child support liens are particularly powerful because:

- They can be filed administratively without a separate lawsuit

- They attach to real estate, vehicles, and personal property

- They can intercept tax refunds and lottery winnings

- They remain until arrears are paid in full

- They can prevent property sales and refinancing

State child support agencies actively pursue these liens as part of their enforcement toolkit, making them a common involuntary lien example in 2026.

The Impact of Involuntary Liens on Property Owners

Involuntary liens create far-reaching consequences that extend beyond the initial debt. Understanding these impacts helps property owners appreciate the urgency of addressing liens promptly.

Obstacles to Selling Property

Perhaps the most immediate impact:

selling a house with a lien becomes extremely complicated.

Title Company Requirements

Title companies conduct thorough searches before closing any real estate transaction. When they discover liens, they require resolution before issuing title insurance. Without title insurance, most buyers and lenders won’t proceed.

Buyer Concerns

Even cash buyers typically demand clear title. Liens signal financial distress and create legal uncertainty that most buyers simply won’t accept.

Reduced Equity

Liens must be paid from sale proceeds, reducing the seller’s net proceeds. In some cases, liens exceed available equity, creating

underwater property situations.

Refinancing Roadblocks

Mortgage lenders won’t refinance properties with involuntary liens. This prevents property owners from:

- Accessing lower interest rates

- Consolidating debts

- Accessing home equity for emergencies

- Modifying loan terms

The inability to refinance can trap property owners in unfavorable loan terms precisely when they need financial flexibility most.

Credit Score Damage

Most involuntary liens appear on credit reports, causing significant score reductions:

- Tax liens: Can reduce scores by 100+ points

- Judgment liens: Similar severe impact

- Public record status: Remains for 7-10 years

Lower credit scores affect:

- Future borrowing ability

- Interest rates on loans

- Employment opportunities (some employers check credit)

- Insurance premiums

- Rental applications

Foreclosure Risk

Several involuntary lien types carry foreclosure power:

Tax Lien Foreclosure

Property tax liens almost always lead to foreclosure if unpaid long enough. Counties need tax revenue and will sell properties to collect.

HOA Foreclosure

HOAs increasingly use foreclosure to collect relatively small debts, sometimes foreclosing over amounts under $1,000.

Judgment Lien Foreclosure

While less common, judgment creditors can force property sales through judicial foreclosure in many states.

Mechanic’s Lien Foreclosure

Contractors can foreclose to collect payment for completed work, though they must act within statutory timeframes.

Inheritance and Estate Complications

Involuntary liens create special challenges for

inherited property:

- Heirs inherit property subject to existing liens

- Estate assets may need to satisfy liens before distribution

- Multiple heirs may disagree about paying inherited liens

- Probate proceedings become more complex and expensive

Business and Commercial Property Impact

For business owners, involuntary liens on commercial property create additional problems:

- Difficulty obtaining business loans

- Challenges leasing space to tenants

- Partnership disputes over lien responsibility

- Business valuation reductions

- Vendor and supplier relationship damage

Involuntary Lien Examples: Types, Impact & Removal Strategies in Action

Real-world scenarios illustrate how different involuntary lien types affect property owners and the strategies that work for removal.

Case Study 1: Property Tax Lien Resolution

Situation: Maria inherited her grandmother’s house in 2024 but discovered $18,000 in unpaid property taxes spanning three years. The county had already started foreclosure proceedings.

Impact: Maria couldn’t sell the property through traditional means. Real estate agents told her the tax debt would consume any equity, and title companies wouldn’t insure the transaction.

Removal Strategy: Maria contacted

Sure Path Property Solutions for helpful guidance. We worked with the county to:

- Negotiate a payment plan for the back taxes

- Stop the foreclosure proceedings

- Coordinate with a direct buyer willing to purchase subject to the tax lien

- Arrange for lien payoff from sale proceeds at closing

Outcome: Maria successfully sold the property, paid off the tax lien, and received remaining equity—avoiding foreclosure and preserving her credit.

Case Study 2: Judgment Lien from Medical Debt

Situation: Robert suffered a serious accident and incurred $45,000 in medical bills. After his insurance dispute, the hospital sued and obtained a judgment, which they recorded as a lien against his home.

Impact: Robert wanted to refinance to lower his mortgage payment but couldn’t proceed with the judgment lien in place. His credit score dropped 120 points.

Removal Strategy: Robert pursued multiple approaches:

- Negotiated with the hospital’s collection attorney

- Settled the judgment for $22,000 (49% of original amount)

- Obtained a lien release document

- Recorded the release with the county

- Waited 30 days for credit reporting updates

Outcome: The settlement saved Robert over $23,000, removed the lien, and allowed him to refinance successfully.

Case Study 3: Mechanic’s Lien Dispute

Situation: Jennifer hired a contractor for kitchen renovations. Dissatisfied with incomplete work, she withheld final payment of $12,000. The contractor filed a mechanic’s lien against her property.

Impact: Jennifer listed her house for sale but couldn’t close because of the lien. The dispute threatened to derail her job relocation.

Removal Strategy: Jennifer worked with a real estate attorney to:

- Review the mechanic’s lien for procedural defects

- Discover the contractor missed the preliminary notice deadline

- Challenge the lien’s validity in court

- Obtain a court order releasing the invalid lien

Outcome: The court invalidated the lien due to procedural failures, clearing Jennifer’s title without payment. She completed her home sale on schedule.

Case Study 4: Multiple Liens on Inherited Property

Situation: Three siblings inherited their father’s property but discovered it had multiple liens: $8,000 in property taxes, a $15,000 HOA lien, and a $25,000 judgment lien from a business debt.

Impact: The liens totaled $48,000 against a property worth approximately $180,000. The siblings disagreed about whether to pay the liens or walk away from the inheritance.

Removal Strategy: Our team at Sure Path Property Solutions provided expert service by:

- Conducting a complete lien search and title review

- Negotiating settlements with all three lien holders

- Reducing total lien amounts to $32,000

- Coordinating a direct sale to an investor

- Distributing remaining proceeds to the heirs

Outcome: The siblings avoided family conflict, resolved all liens, and each received approximately $49,000 from the sale—a positive outcome they didn’t think possible.

Proven Strategies for Removing Involuntary Liens

Removing involuntary liens requires understanding available options and choosing the right approach for each situation. Here are the most effective removal strategies used successfully in 2026.

Strategy 1: Full Payment and Lien Release

The most straightforward removal method is paying the debt in full and obtaining a formal lien release.

Steps for Full Payment:

- Verify the exact amount owed including interest, penalties, and fees

- Request a payoff statement in writing with a specific payoff date

- Make payment via certified check or wire transfer (keep proof)

- Obtain a lien release document signed by the creditor

- Record the release with the county recorder’s office

- Verify removal from title records and credit reports

When This Works Best:

- Property sale is imminent

- Sufficient equity exists to pay from sale proceeds

- Refinancing will provide payoff funds

- Inheritance or other windfall becomes available

Strategy 2: Negotiated Settlement

Many creditors accept less than the full amount owed, especially for older debts or when collection seems unlikely.

Settlement Negotiation Tips:

💡

Start low: Initial offers of 30-50% often lead to settlements at 50-70% of the debt.

💡

Emphasize hardship: Creditors settle more readily when they understand financial difficulties.

💡

Request lien release language: Ensure settlement agreements specifically state the lien will be released.

💡

Get everything in writing: Never make payments without written settlement agreements.

💡

Understand tax implications: Forgiven debt over $600 may be taxable income.

Best Candidates for Settlement:

- Judgment liens from credit card or medical debt

- Older liens approaching statute of limitations

- Situations where creditors face collection challenges

- Debts sold to collection agencies

Strategy 3: Disputing Invalid Liens

Not all liens are valid. Procedural errors, expired deadlines, or incorrect information can invalidate liens.

Common Grounds for Disputing Liens:

- Procedural defects: Missed notice requirements or filing deadlines

- Incorrect amounts: Inflated balances or improper fee calculations

- Statute of limitations: Liens filed after time limits expired

- Identity errors: Liens filed against wrong person or property

- Paid debts: Liens remaining after debt satisfaction

- Fraudulent liens: False claims filed maliciously

Dispute Process:

- Review lien documents for errors

- Research applicable state statutes and requirements

- Gather evidence supporting the dispute

- File formal challenge with appropriate court or agency

- Attend hearings and present evidence

- Obtain court order releasing invalid lien

Working with industry experts who understand

title issues can significantly improve dispute success rates.

Strategy 4: Payment Plans and Installment Agreements

When immediate payment isn’t possible, structured payment plans can prevent foreclosure while gradually eliminating liens.

Tax Lien Installment Agreements

The IRS and most state tax agencies offer payment plans for tax liens:

- Short-term plans: 120 days or less, no setup fee

- Long-term plans: Up to 72 months, with setup fees

- Partial payment plans: For taxpayers who can’t pay full amount

Property tax payment plans vary by county but often allow 12-36 month repayment periods.

Judgment Lien Payment Arrangements

Judgment creditors may agree to payment plans, though they’re not required to do so. Offering secured payments or automatic withdrawals increases acceptance likelihood.

HOA Lien Payment Plans

Many HOAs will accept payment plans to avoid costly foreclosure proceedings, especially if owners demonstrate good faith.

Strategy 5: Lien Subordination

Subordination doesn’t remove liens but changes their priority, which can enable refinancing or property sales.

How Subordination Works:

A senior lien holder agrees to move to a junior position, allowing a new loan to take first priority. This is common when refinancing properties with second mortgages.

Subordination Applications:

- Refinancing primary mortgages when second liens exist

- Obtaining new financing for property improvements

- Restructuring debt to improve cash flow

Lien holders subordinate when they believe their security won’t be compromised by the new arrangement.

Strategy 6: Bankruptcy Protection

Bankruptcy provides powerful tools for addressing involuntary liens, though it carries significant consequences.

Chapter 7 Bankruptcy

- Discharges underlying debts (except taxes, child support)

- Doesn’t automatically remove liens from property

- May allow lien avoidance for certain judgment liens

- Provides fresh start but impacts credit for 10 years

Chapter 13 Bankruptcy

- Creates 3-5 year repayment plan

- Can strip wholly unsecured junior liens

- Allows catching up on tax arrears

- Less severe credit impact (7 years)

Lien Stripping

In Chapter 13, wholly unsecured liens (where property value doesn’t cover senior liens) can be “stripped” and treated as unsecured debt, receiving pennies on the dollar.

“Bankruptcy should be considered carefully and only after exploring other options. While it provides powerful debt relief, the long-term credit consequences affect future borrowing, employment, and housing opportunities.”

Strategy 7: Selling to Direct Buyers

When traditional sales aren’t possible due to liens, selling to direct buyers or investors offers an alternative path.

How Direct Sales Work with Liens:

Companies like

Sure Path Property Solutions purchase properties subject to liens by:

- Conducting thorough lien searches

- Calculating available equity after lien payoffs

- Making cash offers that account for lien amounts

- Coordinating lien payoffs at closing

- Providing sellers with remaining equity

Advantages of Direct Sales:

✅ No need to resolve liens before listing

✅ Fast closings (often 7-30 days)

✅ No repairs or improvements required

✅ Professional coordination with lien holders

✅ Certainty of closing

When Direct Sales Make Sense:

- Multiple liens create complex situations

- Time pressure exists (foreclosure, relocation)

- Property needs significant repairs

- Traditional buyers won’t accept lien complications

- Owners lack funds to pay liens before selling

For property owners wondering “

can you sell land with a lien on it,” direct buyers provide viable solutions.

State-Specific Considerations for Involuntary Liens

Lien laws vary significantly across states, affecting both how liens are created and how they can be removed.

Statute of Limitations by Lien Type

Different states impose different time limits on lien enforcement:

| Lien Type |

Typical Duration |

State Variations |

| Judgment Liens |

10-20 years |

Renewable in most states |

| Mechanic’s Liens |

90-365 days to enforce |

Strict deadlines vary widely |

| Tax Liens |

Until paid |

No expiration in most states |

| HOA Liens |

Until paid |

Some states limit enforcement |

Homestead Exemptions and Lien Protection

Many states provide homestead exemptions that protect primary residences from certain judgment liens:

- Texas: Unlimited homestead protection (with acreage limits)

- Florida: Unlimited value protection for primary residence

- California: $600,000+ depending on county

- New York: $165,550-$250,000 depending on location

Homestead exemptions typically don’t protect against:

- Tax liens

- Mortgage liens

- Mechanic’s liens

- HOA liens

Super Lien States

Some states grant HOA liens “super lien” status, giving them priority over first mortgages for certain amounts:

- Nevada: HOA super lien for up to 9 months of dues

- Washington: Priority for 6 months of assessments

- Oregon: Priority for certain assessment amounts

Understanding state-specific lien laws helps property owners develop effective removal strategies.

Preventing Involuntary Liens: Proactive Measures

While this guide focuses on

Involuntary Lien Examples: Types, Impact & Removal Strategies, prevention deserves attention. Avoiding liens in the first place saves time, money, and stress.

Financial Management Best Practices

🏠

Pay property taxes on time: Set up automatic payments or escrow accounts through mortgage lenders.

🏠

Maintain HOA compliance: Pay dues promptly and address violation notices immediately.

🏠

Address tax debts quickly: Contact the IRS or state agencies at the first sign of tax problems.

🏠

Resolve disputes before litigation: Mediation and negotiation prevent judgments.

Construction Project Protection

When hiring contractors, protect against mechanic’s liens:

- Use written contracts specifying payment terms and project scope

- Require lien waivers before making progress payments

- Verify contractor licensing and insurance coverage

- Research contractor reputation through reviews and references

- Consider payment bonds for large projects

Regular Title Monitoring

Periodically checking property title helps catch liens early:

- Order annual title reports

- Monitor county recorder websites

- Review credit reports quarterly

- Address discrepancies immediately

Early detection allows faster, less expensive resolution.

Working with Professionals: When to Seek Expert Help

While some lien situations can be handled independently, complex cases benefit from professional assistance.

Real Estate Attorneys

Attorneys provide valuable help with:

- Disputing invalid liens

- Negotiating settlements

- Navigating foreclosure proceedings

- Reviewing complex title issues

- Representing clients in court

Legal fees vary but typically range from $200-500 per hour, with some attorneys offering flat fees for specific services.

Title Companies and Title Attorneys

Title professionals specialize in:

Tax Professionals

CPAs and enrolled agents help with:

- IRS and state tax lien resolution

- Offer in compromise applications

- Installment agreement negotiations

- Innocent spouse claims

- Tax debt settlement strategies

Property Solutions Companies

Companies like Sure Path Property Solutions offer comprehensive assistance:

- Evaluating properties with multiple liens

- Coordinating with various lien holders

- Providing direct purchase options

- Offering helpful solutions for complex situations

- Delivering trustworthy service throughout the process

Our team of industry experts understands that dealing with liens feels overwhelming. We provide friendly and caring support while navigating the technical and legal complexities.

For property owners facing

liens and judgments, professional guidance often means the difference between successful resolution and foreclosure.

Common Mistakes to Avoid When Dealing with Involuntary Liens

Learning from others’ mistakes helps property owners avoid costly errors.

❌ Ignoring Lien Notices

The Mistake: Hoping liens will disappear or assuming they’re not serious.

The Consequence: Liens don’t expire on their own (except mechanic’s liens). Ignoring them leads to foreclosure, credit damage, and increased collection costs.

The Solution: Address lien notices immediately, even if full payment isn’t possible. Communication often leads to workable solutions.

❌ Making Partial Payments Without Agreements

The Mistake: Sending payments without written settlement agreements.

The Consequence: Creditors can accept payments without releasing liens or crediting them properly. Partial payments may restart statute of limitations.

The Solution: Always obtain written agreements before making payments, specifying exactly how payments will be applied and when liens will be released.

❌ Failing to Record Lien Releases

The Mistake: Assuming creditors will record releases after payment.

The Consequence: Unreleased liens remain on title indefinitely, blocking future transactions even after debts are paid.

The Solution: Obtain signed release documents and personally record them with the county recorder. Follow up to verify recording.

❌ Attempting DIY Legal Challenges

The Mistake: Disputing liens without understanding legal procedures and requirements.

The Consequence: Missed deadlines, procedural errors, and unsuccessful challenges that waste time and money.

The Solution: Consult with attorneys for lien disputes. Legal expertise significantly improves success rates.

❌ Accepting First Settlement Offers

The Mistake: Immediately accepting initial settlement proposals.

The Consequence: Paying more than necessary. Most creditors expect negotiation and build room into first offers.

The Solution: Counter-offer at lower amounts. Multiple negotiation rounds often yield better results.

❌ Neglecting Tax Implications

The Mistake: Forgetting that settled debts may create taxable income.

The Consequence: Unexpected tax bills when the IRS treats forgiven debt as income.

The Solution: Consult tax professionals before settling large debts. Certain exceptions (insolvency, bankruptcy) can eliminate tax liability.

Frequently Asked Questions About Involuntary Liens

Q: Can I sell my house if it has an involuntary lien?

Yes, but the lien must be addressed during the sale process. Most commonly, liens are paid from sale proceeds at closing.

Selling a house with a lien requires coordination between sellers, buyers, title companies, and lien holders.

Q: How long do involuntary liens last?

Duration varies by type:

- Tax liens: Until paid (no expiration)

- Judgment liens: 10-20 years (renewable in most states)

- Mechanic’s liens: Must be enforced within 90-365 days or expire

- HOA liens: Until paid

- Child support liens: Until arrears are satisfied

Q: Do involuntary liens affect my credit score?

Tax liens and judgment liens typically appear on credit reports and can reduce scores by 100+ points. Mechanic’s liens and HOA liens may not appear on credit reports but still affect property transactions.

Q: Can bankruptcy remove involuntary liens?

Bankruptcy discharges the underlying debt but doesn’t automatically remove liens from property. However, certain liens can be avoided or stripped in bankruptcy, particularly wholly unsecured junior liens in Chapter 13.

Q: What happens if I inherit property with liens?

You inherit the property subject to existing liens. The liens must be satisfied before you can sell with clear title. Some heirs choose to

sell inherited property to direct buyers who handle lien complications.

Q: Can I remove a lien by transferring property to someone else?

No. Liens attach to property, not people. Transferring ownership doesn’t eliminate liens—they remain attached to the property regardless of who owns it.

Q: How much does it cost to remove an involuntary lien?

Costs vary widely:

- Payment/settlement: The debt amount (or negotiated percentage)

- Legal fees: $200-500/hour for attorney assistance

- Filing fees: $25-100 for recording releases

- Title search: $200-400 for comprehensive searches

Q: What’s the difference between a lien and a judgment?

A judgment is a court decision awarding money to a creditor. A judgment lien is created when that judgment is recorded against property. Not all judgments become liens—creditors must take the additional step of recording them.

Resources for Property Owners Dealing with Liens

Government Resources

- IRS: Taxpayer Advocate Service for tax lien assistance

- State Revenue Departments: Tax lien information and payment plans

- County Recorder Offices: Lien search and recording services

- Legal Aid Societies: Free legal assistance for qualifying individuals

Professional Organizations

- American Bar Association: Attorney referral services

- National Association of Consumer Advocates: Consumer rights attorneys

- American Land Title Association: Title professional resources

Educational Resources

The

Sure Path Property Solutions blog offers extensive articles about liens, title issues, and property challenges, providing helpful guidance for property owners navigating complex situations.

Taking Action: Your Next Steps

Understanding

Involuntary Lien Examples: Types, Impact & Removal Strategies provides the foundation for addressing lien problems effectively. Knowledge alone isn’t enough—action is required.

Immediate Action Steps

Step 1: Identify All Liens

Order a comprehensive title search to discover all liens against your property. County recorder websites provide some information, but professional title searches reveal details that might be missed.

Step 2: Verify Lien Amounts

Contact each lien holder to obtain current payoff amounts, including interest, penalties, and fees. Get everything in writing with specific payoff dates.

Step 3: Assess Your Options

Review the removal strategies outlined in this guide and determine which approaches fit your situation:

- Can you pay liens in full?

- Is settlement negotiation possible?

- Are there grounds to dispute lien validity?

- Would payment plans prevent foreclosure?

- Should you consider selling to a direct buyer?

Step 4: Develop a Timeline

Create a realistic timeline for lien resolution, accounting for:

- Foreclosure deadlines (if applicable)

- Statute of limitations on enforcement

- Personal financial circumstances

- Property sale or refinance goals

Step 5: Seek Professional Guidance

Complex lien situations benefit from expert service. Consider consulting:

- Real estate attorneys for legal issues

- Tax professionals for tax lien resolution

- Title companies for comprehensive title work

- Property solutions companies for direct purchase options

When to Contact Sure Path Property Solutions

Our team provides helpful solutions for property owners facing challenging lien situations:

- Multiple liens creating overwhelming complexity

- Foreclosure pressure requiring fast action

- Inherited property with unknown lien problems

- Insufficient equity to pay liens through traditional sales

- Title issues preventing conventional transactions

We offer friendly and caring assistance combined with industry expertise, helping property owners navigate from problem to solution.

Contact our team to discuss your specific situation and explore available options. We provide free consultations and honest assessments—even if we’re not the right solution, we’ll point you in the right direction.

Conclusion

Involuntary liens represent serious challenges for property owners, but they’re not insurmountable obstacles. Understanding the common

Involuntary Lien Examples: Types, Impact & Removal Strategies empowers property owners to take control of difficult situations.

The five major involuntary lien types—tax liens, judgment liens, mechanic’s liens, HOA liens, and child support liens—each carry unique characteristics and removal strategies. While their impacts can be severe, including blocked property sales, credit damage, and foreclosure risk, multiple proven removal strategies exist.

Whether through full payment, negotiated settlement, legal disputes, payment plans, subordination, bankruptcy protection, or direct sales, property owners have options. The key is taking action early, understanding available strategies, and seeking professional guidance when situations become complex.

Remember these essential principles:

✅

Act quickly when liens appear—delays only increase costs and complications

✅

Communicate proactively with lien holders—many are willing to negotiate

✅

Document everything in writing—verbal agreements provide no protection

✅

Verify removals by recording releases and checking title records

✅

Seek expert help for complex situations—professional guidance saves time and money

At

Sure Path Property Solutions, we’ve built our reputation on providing trustworthy service to property owners facing complicated situations. Whether dealing with

back taxes, multiple liens, inheritance complications, or title problems, our industry experts deliver helpful solutions with friendly and caring support.

Your property challenges have solutions. The first step is reaching out for help.

Contact us today to discuss your situation and discover the path forward.

Don’t let involuntary liens control your property’s future. With the right knowledge, strategies, and professional support, you can resolve lien problems and move forward with confidence.