Reinstate Mortgage After Default: Requirements, Cost & Process

Missing mortgage payments can feel overwhelming. The notices pile up, the phone calls increase, and the fear of losing your home becomes very real. But here’s the good news: mortgage default doesn’t automatically mean foreclosure. In many cases, homeowners have the legal right to reinstate their mortgage and stop the foreclosure process completely.

Understanding how to reinstate mortgage after default—including the requirements, costs, and step-by-step process—can be the difference between losing your home and getting back on track. This comprehensive guide walks through everything property owners need to know about mortgage reinstatement, from eligibility requirements to exact costs and timelines.

Whether facing temporary financial hardship, dealing with liens and judgments, or navigating complex property ownership situations, this article provides helpful guidance to understand your options and take action.

Key Takeaways

- Mortgage reinstatement allows homeowners to cure a default by paying all past-due amounts in a lump sum, stopping foreclosure and restoring the original loan terms

- Reinstatement costs typically include all missed payments, late fees, legal costs, and foreclosure expenses—often ranging from $5,000 to $25,000+ depending on how long the default has continued

- State laws determine reinstatement rights, with some states allowing reinstatement until the foreclosure sale date while others have earlier deadlines

- The reinstatement process requires contacting your lender, requesting a payoff statement, gathering funds, and making payment before the deadline

- Alternative solutions exist if reinstatement isn’t feasible, including loan modification, short sale, or working with industry experts who specialize in complex property situations

What Does It Mean to Reinstate a Mortgage After Default?

Mortgage reinstatement is a legal right that allows homeowners to bring a defaulted loan current by paying all past-due amounts in one lump sum. This process essentially “rewinds the clock” on the foreclosure, restoring the mortgage to its original terms as if the default never happened.

The Difference Between Reinstatement and Other Options

Many homeowners confuse reinstatement with other foreclosure alternatives. Here’s how they differ:

Reinstatement means paying everything owed to catch up completely. The original mortgage continues with the same interest rate, monthly payment, and terms.

Loan modification involves negotiating new loan terms with the lender—potentially a lower interest rate, extended repayment period, or reduced principal balance.

Forbearance provides temporary payment relief, but the missed payments must eventually be repaid through a repayment plan or loan modification.

Repayment plan spreads the past-due amount over several months, adding extra to each regular payment until caught up.

Think of reinstatement like hitting the reset button. One payment brings everything current, and the homeowner continues making regular monthly payments as before.

When Reinstatement Rights Apply

Not every mortgage default situation allows for reinstatement. The right to reinstate depends on several factors:

📋 State law requirements – Some states grant statutory reinstatement rights up until the foreclosure sale, while others have earlier cutoff dates

📋 Loan type and terms – Federal loans (FHA, VA, USDA) typically offer more flexible reinstatement options than conventional mortgages

📋 Stage of foreclosure – Reinstatement becomes more complicated and expensive as foreclosure proceedings advance

📋 Previous defaults – Lenders may limit reinstatement rights for borrowers with multiple default histories

📋 Bankruptcy status – Filing bankruptcy can extend reinstatement deadlines and provide additional protections

Most homeowners have the right to reinstate at least once during the foreclosure process, but timing matters significantly.

Understanding Mortgage Default and Its Consequences

Before exploring the reinstatement process, it’s important to understand what triggers default and what happens next.

What Constitutes Mortgage Default?

Mortgage default occurs when a borrower fails to meet the obligations outlined in the loan agreement. The most common triggers include:

Missed payments – Typically, lenders consider a mortgage in default after 30 days of non-payment, though formal action usually begins after 90 days

Property tax delinquency – Failing to pay property taxes can trigger default even if mortgage payments are current

Homeowners insurance lapse – Allowing insurance coverage to expire violates most mortgage agreements

Property condition violations – Allowing the property to fall into significant disrepair may constitute default

Transfer without lender approval – Selling or transferring property without notifying the lender (violating the due-on-sale clause)

For most homeowners, the issue starts with missed monthly payments due to job loss, medical expenses, divorce, or other financial hardships.

The Foreclosure Timeline

Once default occurs, lenders follow a structured process:

| Timeline | Action | What Happens |

|---|---|---|

| Day 1-15 | Grace period | No penalty; payment still considered on time if received |

| Day 16-30 | Late fee assessed | Late charge added to account; first late notice sent |

| Day 31-90 | Default notices | Multiple collection calls and letters; account marked delinquent |

| Day 90-120 | Breach letter | Formal notice of default; demand for full payment to cure |

| Day 120+ | Foreclosure filing | Legal action begins; notice of default or lis pendens filed |

| Months 4-18 | Foreclosure process | Court proceedings (judicial states) or trustee sale process (non-judicial states) |

| Sale date | Foreclosure auction | Property sold to highest bidder; homeowner must vacate |

The exact timeline varies significantly by state. Judicial foreclosure states (requiring court approval) typically take 6-18 months, while non-judicial states can complete foreclosure in as little as 3-4 months.

Impact on Credit and Future Homeownership

Mortgage default creates serious consequences beyond losing the home:

💳 Credit score damage – A foreclosure can drop credit scores by 200-300 points and remain on credit reports for seven years

💳 Future mortgage challenges – Most lenders require 3-7 years after foreclosure before approving a new mortgage

💳 Deficiency judgments – If the foreclosure sale doesn’t cover the full loan balance, lenders may pursue borrowers for the difference

💳 Tax implications – Forgiven debt may be considered taxable income (though some exemptions apply)

💳 Employment issues – Some employers check credit reports, and foreclosure may impact job prospects in financial industries

These consequences make exploring all options—including reinstatement—critically important for homeowners facing default.

Requirements to Reinstate Mortgage After Default

Successfully reinstating a mortgage requires meeting specific legal and financial requirements. Understanding these criteria helps homeowners determine if reinstatement is a viable option.

Legal Eligibility Requirements

The right to reinstate a mortgage depends on both state law and the specific loan terms.

State-Specific Reinstatement Laws

Reinstatement rights vary dramatically by state:

States with statutory reinstatement rights allow homeowners to reinstate up until the foreclosure sale date (or shortly before). These include:

- California

- Colorado

- Illinois

- Michigan

- Minnesota

- Texas

- Washington

States with limited reinstatement periods restrict reinstatement to earlier in the foreclosure process, often requiring action within 30-60 days of the foreclosure filing.

States following mortgage contract terms defer to whatever reinstatement provisions exist in the loan documents themselves.

Homeowners should research their specific state’s laws or consult with a foreclosure attorney to understand their rights. Similar to navigating title issues, understanding state-specific requirements is essential.

Loan Type Considerations

Different loan types offer varying reinstatement protections:

FHA loans – The Federal Housing Administration requires lenders to allow reinstatement throughout the foreclosure process, up until three business days before the foreclosure sale

VA loans – The Department of Veterans Affairs provides similar protections, with generous reinstatement timelines for qualifying veterans

USDA loans – Rural Development loans include borrower-friendly reinstatement provisions

Conventional loans – Reinstatement rights depend on state law and the specific mortgage contract terms

Private/hard money loans – These often have more restrictive reinstatement provisions and shorter timelines

Federal loan programs generally provide the most flexible reinstatement options and longest timelines.

Financial Requirements

Beyond legal eligibility, homeowners must meet financial requirements to successfully reinstate.

Ability to Resume Regular Payments

Reinstatement only makes sense if the homeowner can afford regular monthly payments going forward. Lenders don’t formally verify this ability, but homeowners should honestly assess whether the financial situation that caused the default has been resolved.

Questions to consider:

- Has income stabilized or increased?

- Have the expenses that caused the default been eliminated?

- Is there a realistic budget that includes the full mortgage payment?

- Are there emergency savings to prevent future defaults?

Reinstating the mortgage only to default again within months doesn’t solve the underlying problem and may eliminate future options.

Lump-Sum Payment Capability

The most challenging requirement is securing the full reinstatement amount in one payment. Lenders typically don’t accept payment plans for reinstatement—it’s all or nothing.

Potential funding sources include:

✅ Personal savings – The most straightforward option

✅ Retirement account withdrawals – 401(k) loans or hardship withdrawals (though these have tax implications)

✅ Family loans or gifts – Borrowing from relatives who want to help prevent foreclosure

✅ Home equity line of credit – If available and not already maxed out

✅ Personal loans – Though difficult to obtain with damaged credit

✅ Sale of assets – Selling vehicles, jewelry, or other valuables

✅ Tax refunds – Timing reinstatement with expected refunds

✅ Legal settlements – Using proceeds from insurance claims or lawsuits

✅ Nonprofit assistance – Some housing counseling agencies offer emergency assistance funds

For homeowners who cannot secure the lump sum, alternative solutions like selling a house in pre-foreclosure might be more appropriate.

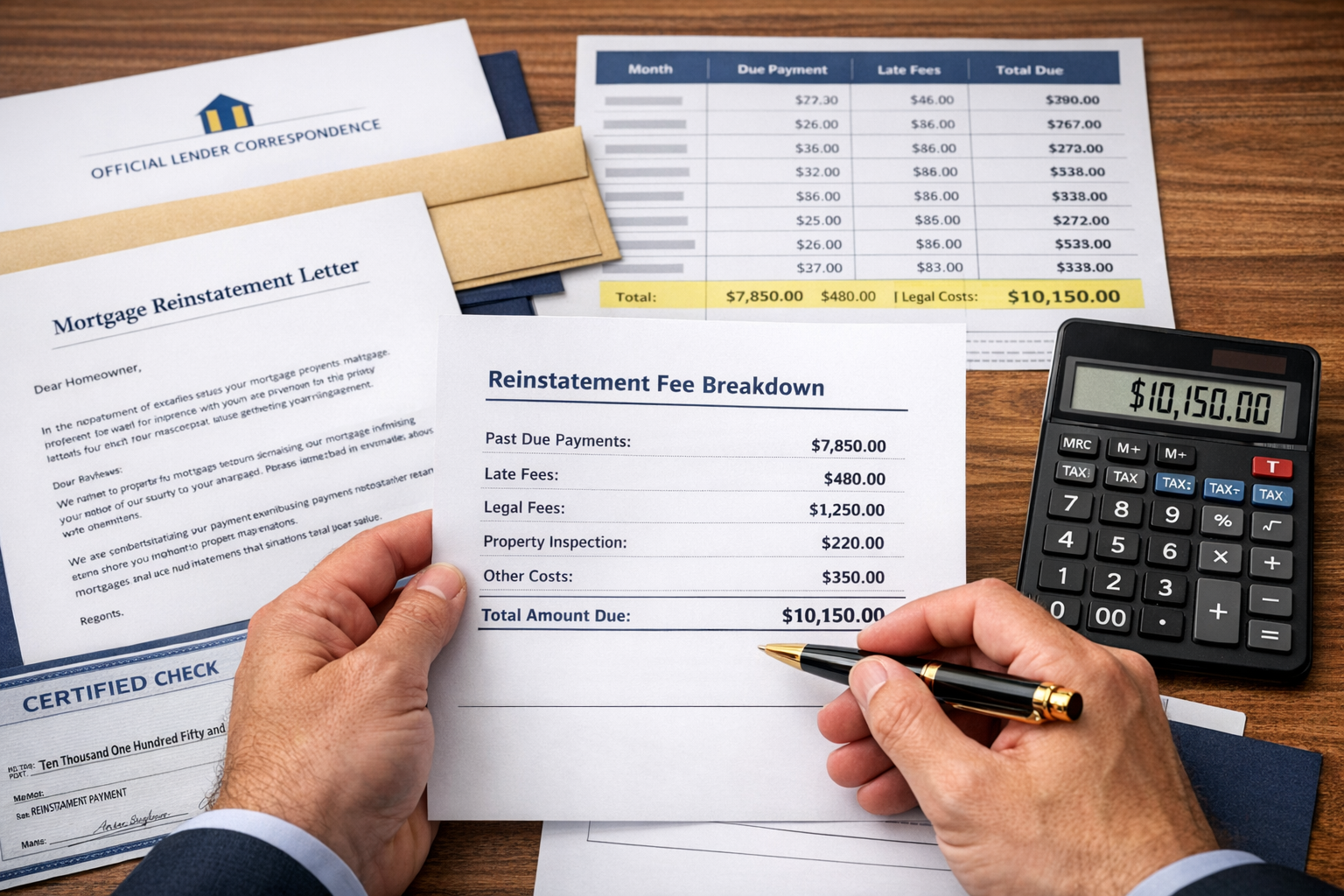

Complete Cost Breakdown: What You’ll Pay to Reinstate

Understanding the exact costs involved in mortgage reinstatement helps homeowners plan and secure adequate funding. The total amount varies based on how long the default has continued and what fees the lender has incurred.

Components of Reinstatement Costs

A complete reinstatement payment includes multiple components:

1. Past-Due Principal and Interest

This is the core amount—all missed monthly payments including both the principal and interest portions.

Example calculation:

- Monthly payment: $1,500

- Missed payments: 6 months

- Past-due principal and interest: $9,000

2. Late Fees and Penalties

Most mortgages assess late fees for each missed payment, typically 4-5% of the payment amount.

Example calculation:

- Monthly payment: $1,500

- Late fee (5%): $75 per month

- Six months of late fees: $450

Some loans also include escalating penalties for extended defaults.

3. Property Tax Advances

If property taxes went unpaid during the default period, the lender may have paid them to protect their interest in the property. These advances must be reimbursed.

Example:

- Annual property taxes: $3,600

- Lender advanced payment: $3,600

- Amount owed to lender: $3,600

Understanding property tax issues becomes especially important when taxes compound the default situation.

4. Insurance Premiums

Similarly, if homeowners insurance lapsed, the lender may have purchased force-placed insurance (which is significantly more expensive than standard policies).

Example:

- Standard annual insurance: $1,200

- Force-placed insurance: $3,500

- Additional cost: $2,300

5. Legal and Foreclosure Costs

Once foreclosure proceedings begin, legal costs accumulate quickly:

- Attorney fees – $1,500-$5,000+ depending on how far the process has advanced

- Filing fees – $200-$500 for court filings and notices

- Publication costs – $300-$800 for required legal notices in newspapers

- Title search fees – $300-$500

- Process server fees – $50-$150 per service

- Trustee fees – $300-$1,000 in non-judicial foreclosure states

The longer foreclosure continues, the higher these costs become.

6. Property Inspection and Preservation Costs

Lenders often conduct property inspections during default to ensure the collateral isn’t being damaged or abandoned.

- Inspection fees – $50-$150 per inspection (may occur monthly)

- Lawn maintenance – If property appears abandoned, lenders may hire services and charge borrowers

- Winterization – $200-$500 if property is vacant during winter

- Securing property – Changing locks, boarding windows if property appears abandoned

7. Additional Interest Accrual

Interest continues accruing on the unpaid balance throughout the default period, even beyond the regular monthly payment amount.

Sample Reinstatement Cost Scenarios

Here are realistic examples showing total reinstatement costs:

Scenario 1: Early Default (3 months)

| Cost Component | Amount |

|---|---|

| Past-due payments (3 × $1,500) | $4,500 |

| Late fees (3 × $75) | $225 |

| Property tax advance | $0 |

| Insurance costs | $0 |

| Legal/foreclosure costs | $500 |

| Inspection fees | $150 |

| Additional interest | $125 |

| Total Reinstatement Cost | $5,500 |

Scenario 2: Mid-Stage Default (6 months)

| Cost Component | Amount |

|---|---|

| Past-due payments (6 × $1,800) | $10,800 |

| Late fees (6 × $90) | $540 |

| Property tax advance | $4,200 |

| Force-placed insurance | $2,800 |

| Legal/foreclosure costs | $3,200 |

| Inspection fees | $450 |

| Property preservation | $600 |

| Additional interest | $380 |

| Total Reinstatement Cost | $22,970 |

Scenario 3: Advanced Default (12 months)

| Cost Component | Amount |

|---|---|

| Past-due payments (12 × $2,200) | $26,400 |

| Late fees (12 × $110) | $1,320 |

| Property tax advance | $6,500 |

| Force-placed insurance | $4,200 |

| Legal/foreclosure costs | $7,800 |

| Inspection fees | $900 |

| Property preservation | $1,500 |

| Additional interest | $1,150 |

| Total Reinstatement Cost | $49,770 |

As these examples show, reinstatement costs increase dramatically the longer default continues. Early action saves thousands of dollars.

Getting an Exact Reinstatement Quote

The only way to know the precise reinstatement amount is to request an official payoff statement from the lender. This document, sometimes called a “reinstatement quote” or “cure amount,” itemizes every cost and provides a specific deadline.

How to request:

- Call the lender’s loss mitigation or foreclosure department

- Request a “reinstatement payoff statement” in writing

- Provide the loan number and property address

- Ask for the statement to be sent via email and postal mail

- Verify the deadline for the quoted amount (usually valid for 30 days)

“The reinstatement quote is a legally binding document that locks in the exact amount needed to cure the default. Get it in writing and verify every line item.” – Foreclosure Prevention Specialist

Step-by-Step Process to Reinstate Mortgage After Default

Successfully reinstating a mortgage requires following a specific process within tight deadlines. Here’s the complete step-by-step guide.

Step 1: Assess Your Situation and Timeline

Before beginning the reinstatement process, homeowners need to understand where they stand.

Determine your foreclosure stage:

- Review all notices received from the lender

- Check county records for foreclosure filings

- Identify the foreclosure sale date if scheduled

- Calculate how much time remains to act

Evaluate financial capability:

- Calculate available funds for reinstatement

- Assess ability to resume regular payments

- Consider whether reinstatement is the best solution or if alternatives like deed in lieu of foreclosure might be more appropriate

Understand your rights:

- Research state-specific reinstatement laws

- Review your mortgage documents for reinstatement provisions

- Note any deadlines or restrictions

This assessment determines whether to proceed with reinstatement or explore other options.

Step 2: Contact Your Lender Immediately

Time is critical in foreclosure situations. Contact the lender’s loss mitigation department as soon as possible.

What to say:

- State your intention to reinstate the mortgage

- Request the exact reinstatement amount

- Ask about the deadline for reinstatement

- Inquire about acceptable payment methods

- Request written confirmation of all information

Get the right department:

- Don’t speak with general customer service

- Ask specifically for “loss mitigation,” “foreclosure prevention,” or “default services”

- Get the direct phone number and extension

- Obtain the name and employee ID of your contact person

Document everything:

- Record the date and time of each call

- Write down the name of everyone you speak with

- Take notes on what was discussed

- Request written confirmation via email

- Keep copies of all correspondence

Many lenders have dedicated foreclosure prevention programs and may even offer alternatives if reinstatement isn’t feasible.

Step 3: Request and Review the Reinstatement Statement

The official reinstatement statement is the most important document in this process.

What the statement should include:

- Complete itemization of all amounts due

- Breakdown of principal, interest, fees, and costs

- The effective date (when the quote is valid)

- The expiration date (deadline for payment)

- Acceptable payment methods

- Payment submission instructions

- Contact information for questions

Review carefully for:

- Accuracy of the past-due payment count

- Reasonable late fees (check your mortgage contract)

- Legitimate legal costs (request itemization if needed)

- Property tax and insurance advances (verify with county records)

- Any unexplained charges or fees

If you find errors:

- Contact the lender immediately

- Provide documentation supporting your position

- Request a corrected statement

- Don’t delay—dispute while also preparing to pay

Errors are more common than many homeowners realize, and challenging incorrect charges can save hundreds or thousands of dollars.

Step 4: Secure Funding for the Reinstatement Amount

With the exact amount and deadline known, homeowners must secure funding quickly.

Funding strategies:

Immediate sources (1-7 days):

- Savings or checking accounts

- Cash advances from credit cards (expensive but fast)

- Borrowing from family or friends

- Selling valuable items for quick cash

Short-term sources (1-2 weeks):

- 401(k) loans (if employer plan allows)

- Home equity line of credit

- Personal loans from banks or credit unions

- Peer-to-peer lending platforms

Medium-term sources (2-4 weeks):

- Hardship withdrawals from retirement accounts

- Tax refund advances

- Selling vehicles or other assets

- Liquidating investments

Assistance programs:

- State and local homeowner assistance funds

- Nonprofit housing counseling agencies

- Emergency assistance from religious organizations

- Employer hardship loans or advances

Creative solutions:

- Borrowing against life insurance cash value

- Advance on inheritance or trust distributions

- Legal settlement advances

- Crowdfunding from community support

For homeowners who cannot secure the full amount, working with industry experts who understand complex property situations can provide alternative solutions.

Step 5: Submit Payment Before the Deadline

Once funding is secured, submitting payment correctly and on time is crucial.

Acceptable payment methods typically include:

✅ Certified check or cashier’s check – Most common and widely accepted

✅ Wire transfer – Fastest method, usually same-day processing

✅ Money order – Acceptable to some lenders, though less common for large amounts

❌ Personal checks – Rarely accepted due to clearance time

❌ Cash – Almost never accepted for large reinstatement amounts

❌ Credit cards – Not accepted by most lenders

Submission best practices:

- Use the fastest method – Wire transfer if possible, overnight certified check if not

- Get written confirmation – Request receipt showing payment received and credited

- Submit early – Don’t wait until the last day; allow processing time

- Follow instructions exactly – Use the account numbers and references provided

- Keep proof – Retain wire transfer confirmations, tracking numbers, and receipts

- Confirm posting – Call to verify payment was received and properly applied

“Missing the reinstatement deadline by even one day can result in the lender rejecting the payment and proceeding with foreclosure. Submit payment at least 3-5 business days before the deadline whenever possible.”

Step 6: Obtain Written Confirmation

After submitting payment, don’t assume everything is complete. Get written proof that the reinstatement was successful.

Request from the lender:

- Written confirmation that the loan is current

- Updated account statement showing zero past-due balance

- Confirmation that foreclosure proceedings have been dismissed

- Documentation of the next regular payment due date

- Verification that credit reporting will be updated

Verify with the court (if applicable):

- In judicial foreclosure states, confirm the case has been dismissed

- Obtain a copy of the dismissal order

- Check that the lis pendens has been released from county records

Update your records:

- File all reinstatement documentation

- Set up automatic payments to prevent future defaults

- Create a budget ensuring you can afford ongoing payments

- Build an emergency fund to handle future financial challenges

Step 7: Resume Regular Payments

Reinstatement brings the loan current, but homeowners must resume making regular monthly payments on time.

Post-reinstatement checklist:

📌 Mark the next payment due date on your calendar

📌 Set up automatic payments if available

📌 Ensure adequate funds are in your account before the due date

📌 Monitor your account online to confirm payments post correctly

📌 Address any issues immediately if payments don’t process

📌 Build a cushion to prevent future defaults

📌 Consider refinancing if the current payment is unaffordable long-term

Remember, most lenders won’t allow multiple reinstatements. This is likely your one opportunity to cure the default and keep the home, so maintaining current status going forward is essential.

Challenges and Obstacles in the Reinstatement Process

While reinstatement can save a home from foreclosure, the process isn’t always straightforward. Understanding common challenges helps homeowners prepare and overcome obstacles.

Lender Resistance or Delays

Some lenders create unnecessary hurdles in the reinstatement process.

Common issues:

Slow response times – Lenders may take weeks to provide reinstatement quotes, eating into the available timeline

Incorrect calculations – Reinstatement amounts may include inflated or unauthorized fees

Changing amounts – The quoted amount may increase between request and payment due to additional fees

Payment processing delays – Even after receiving payment, lenders may delay crediting the account

Lost paperwork – Documents get “lost” requiring resubmission and further delays

Strategies to overcome:

- Make all requests in writing with delivery confirmation

- Follow up every 3-5 business days

- Escalate to supervisors if representatives are unhelpful

- File complaints with the Consumer Financial Protection Bureau (CFPB) if necessary

- Consult with a foreclosure attorney for serious obstacles

- Document everything meticulously

Similar to resolving liens on property, persistence and documentation are key when dealing with lender bureaucracy.

Insufficient Funds or Funding Delays

The most common obstacle is simply not having enough money to reinstate or not getting it in time.

When funding falls short:

If the available funds don’t cover the full reinstatement amount, homeowners have limited options:

- Negotiate a partial payment – Some lenders may accept a substantial partial payment to extend the foreclosure timeline, though this isn’t guaranteed

- Request a repayment plan – Instead of reinstatement, ask about a formal repayment plan spreading the arrearage over several months

- Seek additional assistance – Contact housing counseling agencies, local government programs, or charitable organizations for emergency funds

- Consider alternatives – If reinstatement isn’t feasible, explore loan modification, short sale, or deed in lieu of foreclosure

- Sell the property – Working with professionals who understand selling houses with legal problems may provide a solution

When funding is delayed:

If money is coming but won’t arrive before the deadline:

- Request an extension – Explain the situation and ask for additional time (success varies by lender)

- Provide proof – Show documentation of incoming funds (pending loan approval, expected inheritance, etc.)

- Make a partial payment – Demonstrate good faith by paying what’s currently available

- File bankruptcy – As a last resort, bankruptcy filing immediately stops foreclosure and may provide additional time

Multiple Owners or Inherited Property Complications

When property has multiple owners or was inherited, reinstatement becomes more complex.

Challenges with multiple owners:

- Disagreement on reinstatement – Co-owners may disagree about whether to reinstate or let foreclosure proceed

- Unequal financial contribution – One owner may be willing to pay the reinstatement amount while others cannot or will not contribute

- Unclear ownership percentages – Determining each owner’s share of the reinstatement cost

- Future payment responsibility – Deciding who will make ongoing mortgage payments after reinstatement

For situations involving multiple owners of inherited property, legal counsel may be necessary to navigate ownership disputes and financial responsibilities.

Solutions for multi-owner situations:

- Written agreement – Create a formal agreement outlining each owner’s financial contribution and future payment responsibility

- Buyout arrangement – One owner pays the reinstatement and buys out the other owners’ interests

- Partition action – Legal proceeding to force sale or division of the property

- Sell the property – All owners agree to sell and split proceeds after paying off the mortgage

- Professional mediation – Hire a mediator to help owners reach agreement

Title Issues and Legal Complications

Certain property situations create additional reinstatement challenges.

Problematic scenarios:

Clouded title – Unresolved title issues may prevent reinstatement until cleared

Pending litigation – Lawsuits involving the property may complicate the process

Bankruptcy – Current or recent bankruptcy affects reinstatement rights and procedures

Divorce proceedings – Ongoing divorce may create uncertainty about who has authority to reinstate

Estate issues – If the borrower has died, estate proceedings may be required before heirs can reinstate

Tax liens – Multiple property tax liens or other liens may need resolution

These situations often require legal expertise to navigate successfully. Working with professionals experienced in complex property situations provides helpful solutions when standard reinstatement isn’t straightforward.

Alternatives to Reinstatement

While reinstatement can be the ideal solution, it’s not always feasible or the best option. Understanding alternatives helps homeowners make informed decisions.

Loan Modification

A loan modification changes the original mortgage terms to make payments more affordable.

How it works:

- Lender agrees to modify interest rate, loan term, or principal balance

- Past-due amounts may be added to the principal balance

- New payment is calculated based on modified terms

- Homeowner makes affordable payments going forward

Advantages:

- No lump sum required

- Can significantly reduce monthly payments

- Keeps homeowner in the property

- May be available when reinstatement isn’t

Disadvantages:

- Lengthy application process (3-6 months)

- No guarantee of approval

- May extend loan term significantly

- Could result in paying more interest over time

Best for: Homeowners who cannot afford the lump-sum reinstatement but have steady income to support modified payments.

Repayment Plan

A repayment plan spreads the past-due amount over several months while resuming regular payments.

How it works:

- Homeowner pays regular monthly payment plus an additional amount

- Additional amount covers past-due balance over 6-24 months

- Once repayment plan is complete, loan is current

Example:

- Regular payment: $1,500

- Past-due amount: $9,000

- Repayment period: 12 months

- Monthly payment during repayment: $1,500 + $750 = $2,250

Advantages:

- No lump sum required

- Keeps foreclosure on hold during repayment

- Simpler than loan modification

- Shorter timeline than modification

Disadvantages:

- Temporarily higher monthly payments

- Requires consistent income to afford increased payment

- Not all lenders offer repayment plans

- Default on the plan may result in immediate foreclosure

Best for: Homeowners experiencing temporary financial hardship who can afford higher payments for a limited time.

Forbearance Agreement

Forbearance temporarily reduces or suspends mortgage payments during financial hardship.

How it works:

- Lender agrees to reduce or pause payments for 3-12 months

- Homeowner must demonstrate temporary hardship

- After forbearance ends, missed payments must be repaid through reinstatement, repayment plan, or loan modification

Advantages:

- Provides immediate payment relief

- Prevents foreclosure during forbearance period

- Gives time to resolve financial issues

- Relatively easy to obtain during qualifying hardships

Disadvantages:

- Temporary solution only

- Missed payments still must be repaid

- May accrue additional interest

- Doesn’t solve long-term affordability issues

Best for: Homeowners facing temporary hardship (job loss, medical issue) who expect to recover financially within several months.

Short Sale

A short sale involves selling the property for less than the mortgage balance with lender approval.

How it works:

- Homeowner lists property for sale

- Buyer makes offer below the mortgage payoff amount

- Lender agrees to accept the sale proceeds as full satisfaction of the debt

- Homeowner avoids foreclosure but loses the property

Advantages:

- Less credit damage than foreclosure

- Eliminates mortgage debt (in most cases)

- Homeowner may receive relocation assistance

- More dignified exit than foreclosure

Disadvantages:

- Lose the property

- Lengthy process (6-12 months)

- No guarantee lender will approve

- May still owe deficiency in some states

- Tax implications on forgiven debt

Best for: Homeowners who cannot afford the property long-term and owe more than it’s worth. Learn more about how to do a short sale.

Deed in Lieu of Foreclosure

The homeowner voluntarily transfers property ownership to the lender in exchange for release from the mortgage debt.

How it works:

- Homeowner offers to deed the property to the lender

- Lender evaluates the property condition and title

- If accepted, homeowner signs deed transferring ownership

- Mortgage debt is satisfied

Advantages:

- Faster than foreclosure or short sale

- Less credit damage than foreclosure

- Avoids public foreclosure process

- May negotiate relocation assistance

Disadvantages:

- Lose the property

- Lender may still pursue deficiency

- Not all lenders accept deed in lieu

- Must have clear title

- Tax implications on forgiven debt

Best for: Homeowners who cannot afford the property and want to avoid foreclosure proceedings. Review the complete deed in lieu process for details.

Selling to a Direct Buyer

Working with a direct buyer who purchases properties in challenging situations provides another alternative.

How it works:

- Homeowner contacts a professional buyer

- Buyer evaluates the property and mortgage situation

- Buyer makes a cash offer

- Sale closes quickly (often 7-30 days)

- Proceeds pay off mortgage and any liens

Advantages:

- Very fast process

- No repairs or preparations needed

- Buyer handles complex title and lien issues

- Certainty of closing

- May receive cash above mortgage payoff

Disadvantages:

- Offer may be below retail market value

- Must find reputable, trustworthy buyer

- Lose the property

Best for: Homeowners who need to sell quickly, have equity in the property, or face complex situations like multiple liens, title issues, or inherited property complications.

Sure Path Property Solutions specializes in helping property owners navigate these complex situations, providing expert service and helpful solutions for properties with liens, judgments, tax issues, or unclear title.

Protecting Your Rights During the Reinstatement Process

Understanding and protecting legal rights is essential when dealing with mortgage default and reinstatement.

Federal and State Consumer Protections

Several laws protect homeowners during foreclosure:

Regulation X (RESPA) – Requires mortgage servicers to:

- Respond to borrower inquiries within specific timeframes

- Provide loss mitigation options before foreclosure

- Maintain accurate account records

- Avoid dual tracking (pursuing foreclosure while reviewing loss mitigation)

Fair Debt Collection Practices Act (FDCPA) – Prohibits:

- Harassment or abusive collection practices

- False or misleading statements

- Unfair collection tactics

State foreclosure laws – Vary by state but may include:

- Required notice periods before foreclosure

- Mandatory mediation programs

- Reinstatement rights and timelines

- Redemption periods after foreclosure sale

Servicemembers Civil Relief Act (SCRA) – Provides special protections for active-duty military members, including:

- Reduced interest rates during active duty

- Protection from foreclosure during deployment

- Extended reinstatement timelines

When to Consult an Attorney

Legal representation may be necessary in certain situations:

🔑 The lender refuses to accept reinstatement despite your legal right

🔑 Reinstatement calculations appear inflated or include unauthorized fees

🔑 The foreclosure timeline seems accelerated or doesn’t follow state law

🔑 You’re facing complex ownership issues like divorce, inheritance, or multiple owners

🔑 The lender violated consumer protection laws during the collection or foreclosure process

🔑 You’re considering bankruptcy to stop foreclosure

🔑 The property has significant title issues or liens

Many foreclosure defense attorneys offer free consultations and may work on contingency or flat-fee arrangements for homeowners facing financial hardship.

Housing Counseling Resources

HUD-approved housing counseling agencies provide free or low-cost assistance:

Services offered:

- Reviewing your financial situation

- Explaining available options

- Helping prepare loss mitigation applications

- Negotiating with lenders on your behalf

- Providing foreclosure prevention education

- Connecting you with emergency assistance funds

Finding a counselor:

- Call the HUD Counseling Hotline: 1-800-569-4287

- Visit the HUD website: www.hud.gov/findacounselor

- Contact local nonprofit housing organizations

- Ask your lender for referrals to approved counselors

Housing counselors are trained industry experts who provide friendly and caring assistance to homeowners navigating complex situations. Their services are particularly valuable for those unfamiliar with the foreclosure process or overwhelmed by the options.

Preventing Future Default After Reinstatement

Successfully reinstating a mortgage is only the first step. Preventing future default ensures the investment in reinstatement pays off.

Creating a Sustainable Budget

A realistic budget is essential for maintaining mortgage payments.

Budget essentials:

- Calculate true monthly income – Use after-tax income, not gross pay

- List all fixed expenses – Mortgage, insurance, taxes, car payments, utilities

- Identify variable expenses – Groceries, gas, entertainment, clothing

- Build in savings – Emergency fund contributions should be a budget line item

- Ensure mortgage is affordable – Housing costs shouldn’t exceed 30-35% of gross income

- Cut unnecessary expenses – Eliminate or reduce discretionary spending

- Track actual spending – Monitor whether you’re following the budget

Red flags that suggest the mortgage may not be sustainable:

- Regularly using credit cards for basic expenses

- No money left after paying bills

- Unable to save anything monthly

- Frequently late on other bills

- Stress and anxiety about finances

If the budget reveals the mortgage truly isn’t affordable long-term, it may be better to sell the property voluntarily rather than face another default.

Building an Emergency Fund

An emergency fund prevents minor financial setbacks from causing mortgage default.

Emergency fund guidelines:

💰 Target amount: 3-6 months of essential expenses (including mortgage)

💰 Starting goal: $1,000 minimum for immediate emergencies

💰 Where to keep it: High-yield savings account (accessible but separate from checking)

💰 How to build it: Automatic transfers from each paycheck

💰 When to use it: Job loss, medical emergencies, major home repairs, car breakdowns

💰 When NOT to use it: Vacations, gifts, non-emergency purchases

Even small monthly contributions add up. Saving $100 monthly creates a $1,200 cushion within a year—enough to cover one mortgage payment if needed.

Setting Up Payment Safeguards

Automated systems help ensure payments are never missed.

Payment protection strategies:

✅ Automatic payments – Set up autopay from checking account

✅ Payment reminders – Calendar alerts 5 days before due date

✅ Backup payment method – Have a secondary account or credit line available

✅ Bi-weekly payments – Some lenders allow splitting monthly payment into two smaller payments

✅ Grace period awareness – Know your grace period and use it if needed

✅ Servicer contact information – Keep lender contact details easily accessible

✅ Online account access – Monitor account regularly to confirm payments post correctly

Addressing Financial Challenges Early

When financial difficulties arise, early action prevents default.

Warning signs to act on immediately:

⚠️ Reduced income or job loss

⚠️ Major unexpected expenses

⚠️ Difficulty making full payment

⚠️ Using savings to make payments

⚠️ Juggling which bills to pay

Immediate actions to take:

- Contact the lender – Explain the situation before missing a payment

- Ask about options – Inquire about forbearance, modification, or repayment plans

- Reduce expenses – Cut discretionary spending immediately

- Increase income – Seek additional work, sell unnecessary items

- Seek assistance – Contact housing counselors or local assistance programs

- Evaluate long-term viability – Honestly assess whether keeping the home is realistic

Lenders are much more willing to work with borrowers who communicate proactively rather than those who simply stop paying.

Frequently Asked Questions

Can I reinstate my mortgage more than once?

Most lenders limit reinstatement to once per loan, though this varies by state law and loan terms. Some states grant statutory reinstatement rights for each foreclosure filing, potentially allowing multiple reinstatements if foreclosure is filed multiple times. However, lenders may modify loan terms after the first reinstatement to limit future reinstatement rights. Review your mortgage documents and state laws, or consult with a foreclosure attorney to understand your specific situation.

How long do I have to reinstate after receiving a foreclosure notice?

The timeframe varies significantly by state and foreclosure type. In judicial foreclosure states, homeowners typically can reinstate until shortly before the foreclosure sale date—often up to five days before the sale. In non-judicial foreclosure states, reinstatement deadlines may be earlier, sometimes 30-90 days after the initial notice of default. Federal loans (FHA, VA) generally allow reinstatement up to three business days before the foreclosure sale. Always verify the exact deadline with your lender and state law.

What happens if I can’t pay the full reinstatement amount?

If you cannot pay the full amount, contact your lender immediately to discuss alternatives. Options may include a repayment plan (spreading the arrearage over several months), loan modification (changing loan terms to make payments affordable), forbearance (temporary payment reduction), or other loss mitigation options. If keeping the home isn’t feasible, consider a short sale or deed in lieu of foreclosure to avoid the more severe credit impact of foreclosure. Working with housing counselors or property solution experts can help identify the best path forward.

Does reinstating my mortgage remove the foreclosure from my credit report?

Reinstating the mortgage stops the foreclosure process, but the late payments and foreclosure filing may still appear on your credit report. The foreclosure status should be updated to show the loan is current after reinstatement, but the history of late payments typically remains for seven years. However, successfully reinstating and maintaining current payments going forward demonstrates financial recovery to future lenders and will gradually improve your credit score.

Can I negotiate the reinstatement amount with my lender?

While the principal, interest, and contractual late fees are generally non-negotiable, some costs may be negotiable. Review the reinstatement statement carefully and challenge any fees that seem excessive or unauthorized. Legal fees, property preservation costs, and inspection fees should be reasonable and documented. If you find errors or questionable charges, contact the lender with supporting documentation. Some lenders may waive certain fees, particularly if you can demonstrate financial hardship or errors in their calculations.

What if I’m in bankruptcy—can I still reinstate my mortgage?

Yes, bankruptcy can actually extend reinstatement rights. When you file Chapter 13 bankruptcy, the automatic stay immediately stops foreclosure proceedings, and you can reinstate the mortgage through your bankruptcy repayment plan. Chapter 13 allows you to catch up on missed payments over 3-5 years while making current payments. Chapter 7 bankruptcy also stops foreclosure temporarily, though it doesn’t provide a long-term mechanism to cure the default. Consult with a bankruptcy attorney to understand how bankruptcy affects your specific situation.

Conclusion: Taking Action to Save Your Home

Facing mortgage default and potential foreclosure is one of the most stressful situations a homeowner can experience. But understanding how to reinstate mortgage after default—including the requirements, costs, and step-by-step process—empowers property owners to take control and potentially save their homes.

Key points to remember:

✔ Reinstatement is a legal right in most states, allowing homeowners to cure default by paying all past-due amounts in a lump sum

✔ Time is critical – The longer default continues, the more expensive reinstatement becomes and the fewer options remain

✔ Exact costs vary but typically include missed payments, late fees, legal costs, and any advances the lender made for taxes or insurance

✔ The process requires action – Contact your lender immediately, request a reinstatement quote, secure funding, and submit payment before the deadline

✔ Alternatives exist if reinstatement isn’t feasible, including loan modification, repayment plans, short sale, or working with professionals who specialize in complex property situations

✔ Prevention is essential – After successfully reinstating, create a sustainable budget, build an emergency fund, and address financial challenges early

Your Next Steps

If you’re facing mortgage default, take these actions today:

- Assess your timeline – Determine how much time you have before foreclosure sale

- Contact your lender – Request an official reinstatement quote and understand your deadline

- Evaluate your options – Honestly assess whether reinstatement is financially feasible

- Seek professional guidance – Contact HUD-approved housing counselors for free assistance

- Explore all solutions – If reinstatement isn’t possible, investigate alternatives before time runs out

For homeowners dealing with complex property situations—including liens, judgments, title issues, or inherited property with multiple owners—professional assistance can make the difference between losing everything and finding a workable solution.

Sure Path Property Solutions provides expert service to property owners navigating complicated real estate challenges. With trustworthy service and helpful guidance, the team coordinates with counties, title professionals, and other industry experts to help property owners find clear, practical solutions—even in the most challenging situations.

Whether you choose to reinstate your mortgage, pursue an alternative solution, or need help navigating the complexities of property ownership, remember that options exist. Taking action today, rather than waiting until options disappear, gives you the best chance of protecting your interests and moving toward financial stability.

Don’t face this challenge alone. Reach out to housing counselors, legal professionals, or property solution experts who can provide the friendly and caring support you need during this difficult time. Your home and financial future are worth the effort to explore every available option.