Sell House Before Foreclosure Date: Last-Minute Solutions

The foreclosure notice arrived. The date is circled in red. Your heart is racing, and the clock is ticking. But here’s the truth that many homeowners don’t realize until it’s almost too late: you still have options to sell your house before the foreclosure date, even in these final critical days. While the situation feels overwhelming, understanding your last-minute solutions can mean the difference between losing everything and walking away with cash in hand.

When facing foreclosure, time becomes your most precious commodity. The good news? Homeowners can successfully sell their properties right up until the actual foreclosure auction date. This comprehensive guide explores proven strategies to Sell House Before Foreclosure Date: Last-Minute Solutions that have helped thousands of property owners avoid the devastating consequences of foreclosure and preserve their financial futures.

Key Takeaways

- Time is critical but not expired: You can sell your house anytime before the actual foreclosure auction, even days before the scheduled date

- Cash buyers offer the fastest path: Traditional sales take 30-60 days, but cash buyers can close in 7-14 days, making them ideal for urgent foreclosure situations

- Multiple solutions exist: Short sales, deed-in-lieu arrangements, and direct cash sales each offer different advantages depending on your specific circumstances

- Selling beats foreclosure: Avoiding foreclosure protects your credit score (preventing a 200-300 point drop), eliminates deficiency judgment risks, and often leaves you with cash proceeds

- Professional guidance matters: Working with experienced professionals who understand complicated property situations can simplify the process and maximize your outcome

Understanding Your Foreclosure Timeline ⏰

Before exploring last-minute solutions, understanding exactly where you stand in the foreclosure process is essential. Foreclosure doesn’t happen overnight—it follows a predictable timeline that varies by state and foreclosure type.

The Foreclosure Process Stages

Pre-Foreclosure Stage (30-120 days)

This period begins when you miss your first mortgage payment. During these initial months, lenders send notices of default and attempt to work out payment arrangements. This is actually the best time to act, though many homeowners don’t realize foreclosure is imminent.

Notice of Default (NOD) or Lis Pendens Filing

After typically 90-120 days of missed payments, the lender files official foreclosure paperwork. In judicial foreclosure states, this means a lawsuit. In non-judicial states, it’s a Notice of Default. This formal notice marks the beginning of the official foreclosure timeline.

Foreclosure Auction Notice (20-90 days)

The lender sets an auction date and publishes notice. This is your final countdown. The specific timeframe depends on your state’s laws—some provide just 20 days notice, others give 90 days or more.

Auction Day

This is the absolute deadline. Once the property sells at auction, your ownership rights are terminated.

How Much Time Do You Actually Have?

The answer depends on several factors:

- Your state’s foreclosure laws: Foreclosure timelines vary dramatically by state, ranging from as little as 60 days in some states to over 800 days in others

- Judicial vs. non-judicial process: Judicial foreclosures (requiring court proceedings) take longer than non-judicial foreclosures

- Your lender’s practices: Some lenders move faster than others

- Your response actions: Filing bankruptcy or requesting mediation can extend timelines

Important: Even if the auction is scheduled for next week, you still have time to sell. The key is acting immediately and choosing the right solution for your timeline.

Why Selling Before Foreclosure Beats Waiting

Many homeowners consider just “letting it go” to foreclosure. This is almost always a costly mistake. Here’s why:

| Outcome | Foreclosure | Selling Before Foreclosure |

|---|---|---|

| Credit Impact | 200-300 point drop, stays 7 years | Minimal impact if caught early |

| Deficiency Judgment | Lender can sue for remaining balance | Usually avoided entirely |

| Tax Consequences | Forgiven debt may be taxable | Potentially avoid tax liability |

| Cash Proceeds | Nothing—you lose everything | Often walk away with money |

| Future Housing | Difficulty renting or buying for years | Much easier to secure housing |

| Emotional Toll | Public auction, eviction, maximum stress | Controlled exit, dignity preserved |

The difference is substantial. Foreclosure represents the worst possible outcome, while selling—even at the last minute—preserves options and protects your financial future.

Last-Minute Solutions to Sell House Before Foreclosure Date 🏠

When time is running out, you need solutions that work quickly. Here are the most effective strategies for selling your house before the foreclosure auction, ranked by speed and effectiveness.

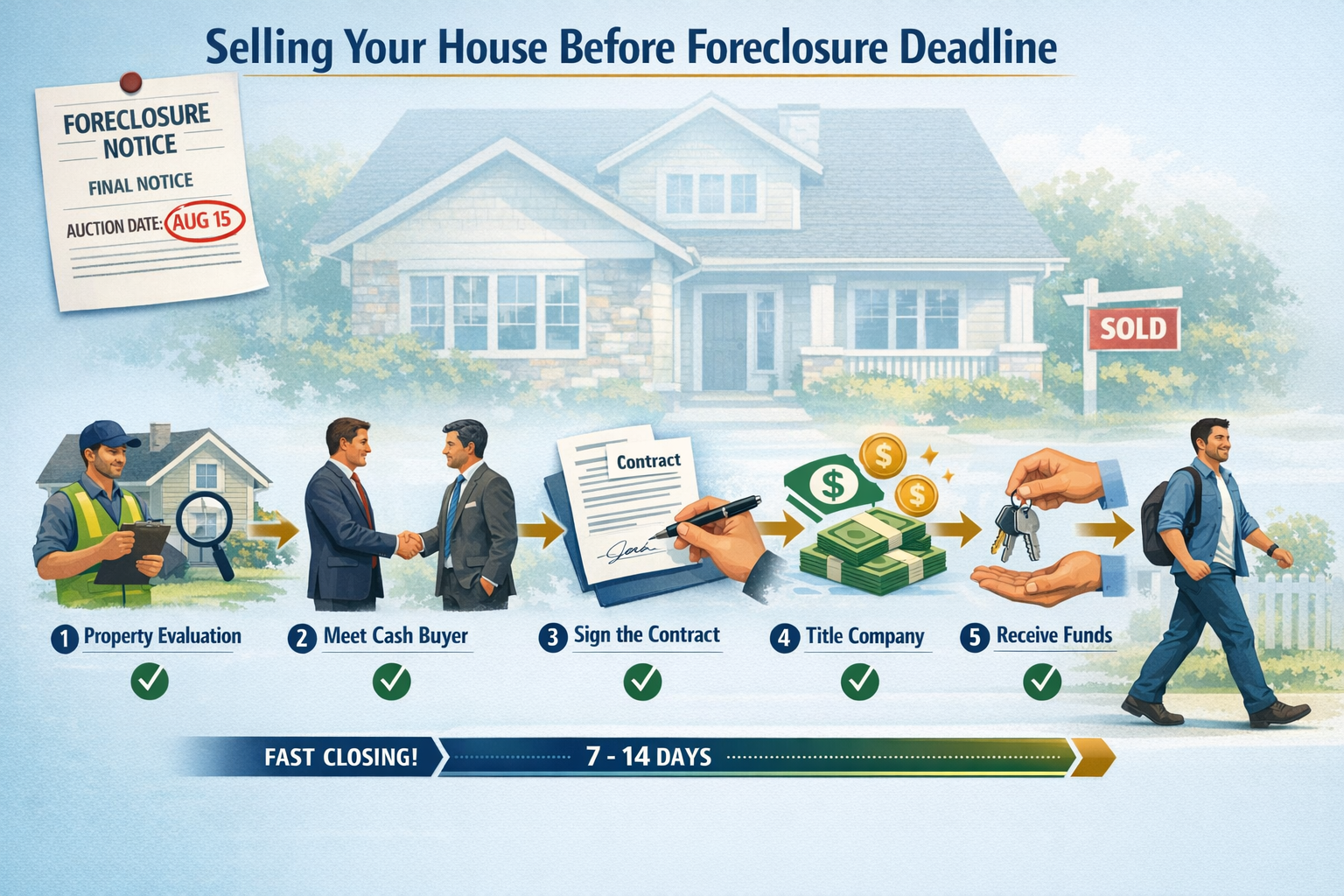

Solution #1: Direct Cash Sale to Investors

Timeline: 7-14 days

Best for: Urgent situations with minimal time remaining

Cash buyers and real estate investors specialize in quick closings because they don’t require mortgage financing, appraisals, or extensive inspections. This makes them the fastest option when you’re racing against a foreclosure deadline.

How It Works:

- Contact a reputable cash buyer or investor (companies like Sure Path Property Solutions specialize in these situations)

- Receive a property evaluation—often within 24-48 hours

- Get a cash offer with no obligation

- Accept the offer and set a closing date that beats your foreclosure deadline

- Close quickly—sometimes in as little as 7 days

- Receive cash proceeds and walk away

Advantages:

- ✅ Fastest possible solution for urgent situations

- ✅ No repairs needed—sell the house as-is in any condition

- ✅ No showings or staging required

- ✅ Certainty of closing—no financing fall-through risk

- ✅ Flexible closing dates to meet your specific deadline

- ✅ Works even with liens or title issues that would block traditional sales

Considerations:

- Cash offers typically come in below full market value (usually 70-85% of after-repair value)

- The trade-off is speed and convenience versus maximum price

- For homeowners facing foreclosure, this trade-off usually makes financial sense

Real Example:

Maria received her foreclosure auction notice with just 18 days until the sale date. She contacted a cash buyer on day 1, received an offer on day 3, accepted it on day 4, and closed on day 14—four days before the auction. She walked away with $23,000 after paying off her mortgage balance, avoiding foreclosure entirely.

Solution #2: Short Sale with Lender Approval

Timeline: 30-90 days (sometimes faster with pre-approval)

Best for: Properties worth less than the mortgage balance

A short sale occurs when your lender agrees to accept less than the full mortgage balance as payment in full. This option works when you owe more than the house is worth—a common situation for homeowners facing foreclosure.

How It Works:

- Contact your lender and request short sale consideration

- Submit a hardship letter explaining your financial situation

- Provide financial documentation (pay stubs, bank statements, tax returns)

- List the property for sale (often with a Realtor experienced in short sales)

- Submit offers to the lender for approval

- Lender reviews and either approves, counters, or denies

- Close the sale with lender’s approved terms

Advantages:

- ✅ Avoids foreclosure and its severe credit consequences

- ✅ May eliminate deficiency judgment (debt forgiveness)

- ✅ Less credit damage than foreclosure (typically 100-150 point drop vs. 200-300)

- ✅ Can potentially get relocation assistance from the lender

- ✅ Allows you to sell even when underwater on your mortgage

Challenges:

- ⚠️ Time-consuming process—lenders can take weeks or months to approve

- ⚠️ Requires lender cooperation—not all lenders readily agree

- ⚠️ Still impacts credit, though less severely than foreclosure

- ⚠️ May have tax implications if debt is forgiven

- ⚠️ Requires finding a buyer willing to wait for lender approval

Important Timing Note:

If your foreclosure auction is less than 30 days away, a short sale probably won’t work unless your lender has already pre-approved the process. However, requesting a short sale can sometimes convince lenders to postpone the auction date, buying you additional time.

Solution #3: Deed in Lieu of Foreclosure

Timeline: 30-60 days

Best for: Cooperative lenders when sale isn’t possible

A deed in lieu of foreclosure means voluntarily transferring your property deed to the lender in exchange for being released from the mortgage obligation. It’s essentially handing the keys back to avoid foreclosure.

How It Works:

- Contact your lender and request deed in lieu consideration

- Demonstrate you’ve attempted to sell the property unsuccessfully

- Provide financial hardship documentation

- Negotiate terms, including potential deficiency waiver

- Sign the deed transfer documents

- Vacate the property by the agreed date

- Mortgage obligation is satisfied

Advantages:

- ✅ Less credit damage than foreclosure (similar to short sale impact)

- ✅ Faster than foreclosure process

- ✅ More dignified exit than forced auction

- ✅ May include deficiency waiver (no remaining debt)

- ✅ Potential relocation assistance from lender

- ✅ Avoids public foreclosure auction

Disadvantages:

- ⚠️ Not always accepted by lenders (they often prefer foreclosure)

- ⚠️ Requires property to be lien-free (no second mortgages or other liens)

- ⚠️ Still damages credit (reported as “deed in lieu” or “settled for less”)

- ⚠️ You receive no proceeds from the transaction

- ⚠️ May have tax consequences on forgiven debt

When This Makes Sense:

Deed in lieu works best when you have no equity, can’t find a buyer quickly enough, and your lender is cooperative. It’s a last resort before foreclosure, not a first choice if selling is possible.

Solution #4: Selling to a “Subject-To” Investor

Timeline: 7-21 days

Best for: Properties with significant equity but no time for traditional sale

In a “subject-to” transaction, an investor purchases your property by taking over your existing mortgage payments without formally assuming the loan. The mortgage stays in your name, but the investor makes the payments and takes ownership.

How It Works:

- Investor evaluates your property and mortgage situation

- Investor offers to take over payments and give you cash for your equity

- You deed the property to the investor

- Investor makes mortgage payments (loan remains in your name)

- You receive agreed-upon cash payment for your equity

- Investor eventually refinances or sells, paying off your original loan

Advantages:

- ✅ Very fast closing possible

- ✅ Stops foreclosure immediately

- ✅ Can receive cash for your equity

- ✅ No need to qualify for new financing

- ✅ Works even with poor credit

Significant Risks:

- ⚠️ Loan remains in your name—if investor stops paying, you’re still liable

- ⚠️ Violates most mortgage due-on-sale clauses—lender can demand full payment

- ⚠️ Credit risk—late payments affect YOUR credit

- ⚠️ Difficult to get future mortgages while this loan shows on your credit

- ⚠️ Requires extreme trust in the investor

Important Warning:

Subject-to transactions carry substantial risk and should only be considered with extremely reputable investors who have verifiable track records. Many experts recommend avoiding this option entirely due to the ongoing liability.

Solution #5: Listing with a Traditional Agent (If Time Permits)

Timeline: 30-60+ days

Best for: Properties with at least 45+ days before auction

If you have at least 45-60 days before your foreclosure auction date, listing with a traditional real estate agent might yield a higher sale price than a cash buyer offer.

How It Works:

- Interview and hire an experienced local real estate agent

- Prepare the property (cleaning, minor repairs, staging)

- List on the MLS and market to potential buyers

- Show the property to interested buyers

- Negotiate offers and accept the best one

- Complete inspections, appraisal, and buyer’s financing process

- Close the sale (typically 30-45 days after offer acceptance)

Advantages:

- ✅ Potentially higher sale price (closer to full market value)

- ✅ Access to more buyers through MLS exposure

- ✅ Professional marketing and negotiation

- ✅ Agent handles paperwork and coordination

Disadvantages:

- ⚠️ Much slower process—typically 60-90 days total

- ⚠️ Requires property preparation (cleaning, repairs, staging)

- ⚠️ Showings and disruption to your life

- ⚠️ Risk of buyer financing falling through

- ⚠️ May not close before foreclosure deadline

- ⚠️ Agent commissions reduce net proceeds (typically 5-6%)

Critical Timing Consideration:

Only pursue this option if you have sufficient time. If your auction is less than 45 days away, the risk of not closing in time is too high. A failed traditional sale attempt could leave you with no options as the auction date arrives.

Overcoming Common Obstacles When Selling Before Foreclosure 🚧

Even when you decide to sell before foreclosure, several obstacles might stand in your way. Here’s how to overcome the most common challenges.

Obstacle #1: Property Has Liens or Judgments

The Problem:

Liens and judgments attached to your property must typically be paid at closing before you can transfer clear title. If you owe more than the property is worth, traditional buyers won’t be able to purchase it.

The Solution:

- Work with cash buyers who specialize in properties with liens

- Negotiate lien payoffs for less than full amount (many lienholders will settle)

- Pursue a short sale where the lender agrees to pay off junior liens

- Consider investors who can navigate complex title issues

Experienced companies that handle complicated property situations can coordinate with lienholders, negotiate settlements, and facilitate sales even when multiple liens exist.

Obstacle #2: Property Needs Extensive Repairs

The Problem:

Traditional buyers require properties to be in good condition and often request repairs after inspections. When facing foreclosure, most homeowners lack the time and money for repairs.

The Solution:

- Sell “as-is” to cash buyers who purchase properties in any condition

- Disclose all known issues upfront to avoid delays

- Focus on buyers who specialize in fixer-uppers and distressed properties

- Skip the repair process entirely—many investors prefer to handle renovations themselves

The beauty of as-is sales is that you can sell your house in literally any condition—from minor cosmetic issues to major structural problems—without spending a dollar on repairs.

Obstacle #3: You Owe More Than the House Is Worth

The Problem:

Being “underwater” or “upside-down” on your mortgage means you owe more than the current market value. Traditional sales won’t generate enough proceeds to pay off the loan.

The Solution:

- Pursue a short sale with lender approval

- Bring cash to closing to cover the difference (if possible)

- Negotiate with the lender for a deficiency waiver

- Explore deed in lieu as an alternative

- Work with investors who have relationships with lenders and experience negotiating these situations

Many lenders prefer short sales to foreclosure because they recover more money and avoid lengthy legal processes. Being underwater doesn’t mean you can’t sell—it just requires lender cooperation.

Obstacle #4: Multiple Owners or Heirs Disagree

The Problem:

When property is jointly owned or part of an estate with multiple heirs, getting everyone to agree on selling quickly can be challenging, especially under foreclosure pressure.

The Solution:

- Communicate the urgency clearly—foreclosure affects everyone’s credit

- Show the financial comparison: selling proceeds vs. losing everything to foreclosure

- Consider a partition action (though this takes time)

- Work with buyers experienced in complicated ownership situations

- Explore buyout options where one owner purchases others’ shares

Professional guidance from companies experienced in heir property and co-ownership disputes can help navigate these sensitive situations and find solutions that work for everyone involved.

Obstacle #5: You Have No Equity or Cash for Closing Costs

The Problem:

Even when selling, there are closing costs—title fees, recording fees, transfer taxes, and potentially agent commissions. If you have no equity, you might not have money to cover these costs.

The Solution:

- Work with cash buyers who cover all closing costs

- Negotiate with your lender to pay closing costs in a short sale

- Ask the buyer to cover your closing costs (common in investor purchases)

- Request relocation assistance from your lender as part of the agreement

Many cash buyers specifically structure their offers to cover all seller closing costs, allowing you to walk away without bringing any money to the table—and often with cash in hand.

Step-by-Step Action Plan: What to Do Right Now 📋

If you’re facing an imminent foreclosure date, every hour counts. Here’s your action plan for the next 72 hours and beyond.

Immediate Actions (Next 24 Hours)

Hour 1-2: Assess Your Exact Situation

- Locate your foreclosure notice and identify the exact auction date

- Calculate how many days you have until the deadline

- Determine your current mortgage balance

- Research your property’s current market value (Zillow, Realtor.com, recent neighborhood sales)

- Calculate your approximate equity (value minus mortgage and liens)

- Gather all property documents (deed, mortgage, tax bills, lien notices)

Hour 3-4: Contact Your Lender

- Call your mortgage servicer’s loss mitigation department

- Ask about postponement options (even a few weeks helps)

- Inquire about short sale or deed in lieu possibilities

- Request any available foreclosure alternatives

- Document the conversation (name, date, time, what was discussed)

Hour 5-8: Reach Out to Cash Buyers

- Contact 3-5 reputable cash buying companies

- Explain your situation and timeline honestly

- Request property evaluations and offers

- Ask about their typical closing timeline

- Verify they can close before your foreclosure date

Hour 9-24: Evaluate Your Options

- Compare any cash offers received

- Research the companies’ reputations (reviews, BBB ratings, testimonials)

- Calculate your net proceeds from each option

- Consider the timeline certainty of each option

- Discuss with family members or trusted advisors

Days 2-3: Make Your Decision and Move Forward

Choose Your Path:

Based on your timeline, equity situation, and offers received, select the best option:

- 7-14 days until auction: Accept a cash buyer offer immediately

- 15-30 days until auction: Consider cash buyer or possibly short sale if lender pre-approves

- 30-45 days until auction: Short sale or traditional listing might work

- 45+ days until auction: All options available—choose based on maximum net proceeds

Execute Your Choice:

- Accept an offer or list with an agent

- Provide all requested documentation promptly

- Stay in constant communication with all parties

- Be responsive to requests and questions

- Keep your lender informed of your progress

Days 4-14: Navigate the Closing Process

For Cash Sales:

- Complete any required property inspections

- Provide clear access to the property

- Sign all required documents promptly

- Coordinate with the title company

- Prepare to vacate the property by closing date

- Confirm closing date is before foreclosure auction

For Short Sales or Traditional Sales:

- Respond immediately to all lender requests

- Provide complete financial documentation

- Keep the buyer engaged and informed

- Work with your agent on any negotiations

- Monitor the timeline closely

- Request auction postponement if needed

For Deed in Lieu:

- Submit all required hardship documentation

- Negotiate deficiency waiver terms

- Review all documents with an attorney if possible

- Understand the credit reporting implications

- Arrange your moving timeline

- Get all agreements in writing

Final Week Before Closing

- Confirm closing date and time

- Review closing documents in advance

- Arrange for utilities to be transferred

- Complete any required property repairs (if agreed)

- Remove all personal belongings

- Do a final walkthrough

- Bring required identification to closing

- Confirm foreclosure auction has been cancelled

- Get written confirmation that the mortgage is satisfied

Working with Professional Cash Buyers: What to Expect 🤝

When time is critical, professional cash buyers offer the most reliable path to selling before foreclosure. Here’s what the process looks like and how to ensure you’re working with a trustworthy service.

The Professional Cash Buying Process

Step 1: Initial Contact and Information Gathering

When you reach out to a reputable cash buyer, they’ll ask questions about:

- Your property’s location, size, and condition

- Your foreclosure timeline and auction date

- Your mortgage balance and any liens

- Your goals and what you hope to accomplish

- Your ideal closing timeline

This conversation is typically pressure-free and informational. Legitimate buyers want to understand your situation to determine if they can provide helpful solutions.

Step 2: Property Evaluation

The buyer will evaluate your property through:

- Online research and public records review

- Comparable sales analysis in your neighborhood

- Often a brief in-person property visit (15-30 minutes)

- Assessment of needed repairs and renovation costs

- Title search to identify any liens or encumbrances

Step 3: Cash Offer Presentation

Within 24-48 hours, you’ll receive a written cash offer that includes:

- Purchase price

- Proposed closing date

- Any contingencies (usually minimal or none)

- Who pays closing costs

- Explanation of how they calculated the offer

Step 4: Offer Acceptance and Contract

If you accept the offer:

- A purchase agreement is signed

- Earnest money is deposited (typically with a title company)

- The title company begins the closing process

- Any required inspections are scheduled

- The buyer arranges financing (cash) and closing logistics

Step 5: Closing

At closing:

- You sign the deed and transfer documents

- The buyer provides cash payment

- The mortgage and any liens are paid off

- You receive any remaining proceeds

- The foreclosure is stopped

- You hand over the keys

The entire process from first contact to closing typically takes 7-14 days with professional cash buyers.

Red Flags: How to Avoid Scams

Unfortunately, desperate homeowners facing foreclosure are targets for scams. Watch for these warning signs:

🚩 Pressure tactics: Legitimate buyers give you time to consider offers

🚩 Upfront fees: Never pay fees before closing

🚩 Requests to sign blank documents: All documents should be complete when you sign

🚩 Promises that sound too good to be true: Be skeptical of offers significantly above market value

🚩 Requests to make mortgage payments to them: Payments should go to your lender

🚩 No verifiable business presence: Check for physical address, licensing, reviews

🚩 Pressure to move out before closing: You should remain until the sale is complete

Questions to Ask Cash Buyers

Before working with any cash buyer, ask:

- How long have you been buying properties? (Look for established companies)

- Can you provide references from recent sellers? (Verify their track record)

- What is your BBB rating and online reviews? (Check reputation)

- Who pays closing costs? (Many buyers cover these)

- What is your typical closing timeline? (Ensure it meets your needs)

- Can you provide proof of funds? (Verify they can actually close)

- Will you purchase even with liens or title issues? (Important if you have complications)

- What happens if the closing is delayed? (Understand contingency plans)

Why Sure Path Property Solutions Stands Out

When facing foreclosure, working with industry experts who understand complicated situations makes all the difference. Companies specializing in problem properties offer:

- Experience with foreclosure timelines: Understanding exactly how to coordinate with lenders and title companies to close before auction dates

- Solutions for complex title issues: Ability to purchase properties with liens, judgments, or unclear ownership

- Transparent, fair offers: Clear explanation of how offers are calculated

- Flexible closing dates: Ability to close on YOUR timeline

- Compassionate, pressure-free approach: Recognition that you’re going through a difficult situation

- Expert service throughout: Helpful guidance from first contact through closing

The right buyer doesn’t just purchase your property—they provide helpful solutions that address your specific situation with trustworthy service and friendly, caring support.

Life After Selling: Rebuilding and Moving Forward 🌟

Selling your house before foreclosure is just the beginning. Here’s what comes next and how to rebuild your financial life.

Immediate Post-Sale Steps

Confirm the Foreclosure is Cancelled

- Get written confirmation from your lender that the foreclosure has been withdrawn

- Verify with the county that no auction will proceed

- Keep all documentation showing the sale and mortgage satisfaction

- Monitor your credit report to ensure foreclosure is not reported

Address Any Remaining Debts

If you had a short sale or deed in lieu:

- Obtain written confirmation of any deficiency waiver

- Understand any tax implications of forgiven debt

- Consult with a tax professional about Form 1099-C (Cancellation of Debt)

- Keep all documentation for at least seven years

Secure Your Housing

- If you received proceeds, use them wisely for housing deposits

- Be upfront with landlords about your situation

- Consider renting from private landlords rather than large companies

- Provide references from employers, previous landlords (before the foreclosure situation)

- Offer a larger security deposit if needed to secure housing

Credit Recovery Timeline

Immediate Impact (Months 0-6)

- Your credit score will reflect the late payments leading up to the sale

- Short sale or deed in lieu will appear on your credit report

- Score impact: 100-150 points typically (vs. 200-300 for foreclosure)

- Focus on paying all other bills on time

Short-Term Recovery (Months 6-24)

- Establish new positive payment history

- Consider a secured credit card to rebuild credit

- Keep credit utilization below 30%

- Avoid applying for new credit unnecessarily

- Monitor your credit reports for accuracy

Long-Term Recovery (Years 2-7)

- Short sale/deed in lieu impact diminishes over time

- Positive payment history increasingly outweighs the negative event

- After 2-3 years, you may qualify for FHA financing

- After 4 years, conventional mortgage financing becomes possible

- After 7 years, the event is removed from your credit report entirely

Financial Lessons and Future Planning

Build an Emergency Fund

- Start small—even $500-1,000 provides a buffer

- Automate savings to make it consistent

- Keep funds in a separate, easily accessible account

- Aim for 3-6 months of expenses eventually

Create a Realistic Budget

- Track all income and expenses

- Identify areas to reduce spending

- Prioritize needs over wants

- Build in savings as a non-negotiable expense

Understand Housing Affordability

- Follow the 28/36 rule: housing costs should be no more than 28% of gross income

- Consider all costs: mortgage/rent, utilities, insurance, maintenance, taxes

- Don’t overextend to buy again too quickly

- Rent until you’re financially stable

Consider Financial Counseling

- Many non-profit organizations offer free financial counseling

- HUD-approved counselors can provide guidance

- Learn from the experience to avoid future difficulties

- Develop a long-term financial plan

The Emotional Recovery Journey

Losing a home—even by selling before foreclosure—is emotionally difficult. It’s important to acknowledge the feelings and move forward:

Allow Yourself to Grieve

It’s normal to feel loss, shame, anger, or sadness. These feelings are valid. Give yourself permission to experience them without judgment.

Reframe the Narrative

You didn’t “lose” your house—you made a strategic decision to protect your financial future. Selling before foreclosure shows wisdom and courage.

Focus on What You Gained

- You avoided the worst-case scenario

- You protected your credit from maximum damage

- You may have received cash proceeds

- You maintained control of the situation

- You can recover much faster than from foreclosure

Look Forward, Not Back

- This is a chapter in your life, not the whole story

- Many successful people have faced financial setbacks

- Your housing situation doesn’t define your worth

- You now have knowledge and experience to avoid future problems

Seek Support

- Talk with trusted friends or family

- Consider counseling if you’re struggling emotionally

- Connect with others who’ve faced similar situations

- Remember that this situation is temporary

“Selling my house before foreclosure felt like failure at first. But six months later, I realized it was actually the smartest decision I could have made. I walked away with $15,000, avoided foreclosure on my credit, and now I’m renting a nice apartment and rebuilding. If I had let it go to auction, I’d have nothing and my credit would be destroyed for years.” — Jennifer M., former homeowner

Frequently Asked Questions ❓

Can I really sell my house the week before the foreclosure auction?

Yes! You can sell your property anytime before the actual auction occurs. Many homeowners successfully sell just days before their scheduled auction date. The key is working with cash buyers who can close quickly and don’t require financing approvals. However, the earlier you start the process, the more options you’ll have.

Will I get any money from selling before foreclosure?

It depends on your equity situation. If your property is worth more than you owe (including all liens and closing costs), you’ll receive the difference as cash proceeds. If you’re underwater, you might not receive proceeds, but you’ll avoid foreclosure’s severe consequences. Even breaking even is better than foreclosure, which leaves you with nothing and destroys your credit.

What if I have liens or judgments on the property?

Liens must typically be paid at closing from the sale proceeds. However, experienced buyers who handle properties with liens can often negotiate settlements for less than the full amount. They coordinate with lienholders, title companies, and your mortgage lender to facilitate the sale even with complex title issues.

Can I sell if I’m already in bankruptcy?

Yes, but you’ll need bankruptcy court approval. If you’ve filed Chapter 13, the court must approve the sale. If you’re in Chapter 7, the trustee controls the property. Work with an attorney and inform potential buyers about the bankruptcy so they understand the additional approval requirements and timeline.

What happens to my credit if I sell before foreclosure?

Your credit will show the late payments leading up to the sale, but not a foreclosure. If you complete a regular sale, the impact is minimal—just the late payments. A short sale or deed in lieu shows on your credit but causes significantly less damage than foreclosure (typically 100-150 points vs. 200-300 points). You’ll also recover much faster.

Do I need a real estate agent to sell before foreclosure?

No. When time is critical, working directly with cash buyers is often faster and more effective. Agents add value in traditional sales with longer timelines, but their commission (5-6%) reduces your proceeds, and the process takes much longer. For urgent foreclosure situations, direct cash sales typically make more sense.

What if my house needs major repairs?

Sell it as-is to a cash buyer. You don’t need to make any repairs. Professional investors purchase properties in any condition—from minor cosmetic issues to major structural problems. They factor repair costs into their offer and handle all renovations themselves after closing.

Can I stay in the house after I sell it?

This depends on the buyer. Some investors offer rent-back arrangements where you can remain as a tenant for a specified period after closing. However, most buyers will require you to vacate at or shortly after closing. Discuss your needs during negotiations—flexibility might be possible.

What if I can’t find the deed or other documents?

Don’t worry. Title companies can obtain copies of recorded documents from county records. Your lender can provide mortgage documents. Missing paperwork shouldn’t prevent the sale—the title company handles obtaining necessary documentation as part of the closing process.

How do I know if a cash buyer is legitimate?

Research thoroughly: check their BBB rating, read online reviews, verify they have a physical business address, ask for references, and confirm they’ve been in business for several years. Legitimate buyers never charge upfront fees, don’t pressure you, and provide clear written offers. Trust your instincts—if something feels wrong, it probably is.

Conclusion: Your Path Forward Starts Today

Facing foreclosure feels overwhelming, but you’ve taken the most important step by seeking information about your options. The truth is simple: Sell House Before Foreclosure Date: Last-Minute Solutions exist, they work, and thousands of homeowners have successfully used them to avoid foreclosure’s devastating consequences.

Time is your most valuable asset right now. Every day you wait is one less day to execute a solution. Whether your auction is scheduled for next week or next month, acting immediately gives you the best possible outcome.

Your Action Steps Right Now

- Calculate your exact timeline: Find your foreclosure notice and identify the auction date

- Assess your situation: Determine your equity, liens, and property condition

- Contact cash buyers today: Reach out to 3-5 reputable companies for evaluations

- Compare your options: Evaluate offers and timelines realistically

- Make a decision: Choose the path that best fits your timeline and goals

- Execute immediately: Move forward without delay

Remember These Key Points

- You have options until the actual auction occurs

- Selling beats foreclosure in every measurable way

- Cash buyers offer the fastest, most reliable solution for urgent timelines

- Even complex situations with liens, judgments, or title issues can be resolved

- Professional guidance makes the process simpler and less stressful

- Your financial future can recover—this setback doesn’t define you

Get Expert Help Today

If you’re facing foreclosure and need helpful solutions delivered with trustworthy service, contact Sure Path Property Solutions today. Our team of industry experts specializes in complicated property situations—foreclosures, liens, judgments, title issues, and more. We provide friendly and caring, expert service that guides you toward clear, practical solutions.

We understand you’re facing a difficult situation. Our approach is professional yet approachable, focused on helpful guidance rather than pressure. We’ll evaluate your property quickly, provide a fair cash offer, and close on your timeline—often in as little as 7-14 days.

Don’t let foreclosure happen when solutions exist. Your path forward starts with a simple conversation. Reach out today and discover how we can help you sell your house before the foreclosure date, protect your financial future, and move forward with confidence.

The clock is ticking, but hope isn’t lost. Take action now—your future self will thank you for the decision you make today.