Sell House Fast to Avoid Foreclosure: Your Emergency Exit Plan

The foreclosure notice arrives in the mail, and suddenly everything changes. Your heart races as you read the timeline—just months before losing your home. But here’s the truth that many homeowners don’t realize: foreclosure is not inevitable, and you have more power than you think.

When mortgage payments become impossible and foreclosure looms, time becomes your most valuable asset. Every day that passes brings you closer to losing your home, damaging your credit for years, and potentially facing a deficiency judgment. The good news? A strategic emergency exit plan can help you sell your house fast to avoid foreclosure, preserve your equity, and move forward with dignity intact.

This comprehensive guide walks through every step of creating and executing an emergency exit plan when foreclosure threatens your home. Whether you’re one payment behind or already received a notice of default, understanding your options and acting quickly can make the difference between financial devastation and a fresh start.

Key Takeaways

- Time is critical: The foreclosure timeline varies by state, but acting within the first 90 days provides the most options and best outcomes

- Multiple exit strategies exist: Traditional sales, short sales, cash buyers, and deed in lieu each offer different timelines and benefits depending on your situation

- Equity preservation matters: Selling before foreclosure auction protects any remaining equity and prevents deficiency judgments that can haunt you for years

- Professional guidance accelerates solutions: Working with industry experts who understand complicated situations—like liens, title issues, or multiple owners—can expedite the process significantly

- Your credit can be protected: Strategic action before foreclosure completion can minimize long-term credit damage and preserve future homeownership opportunities

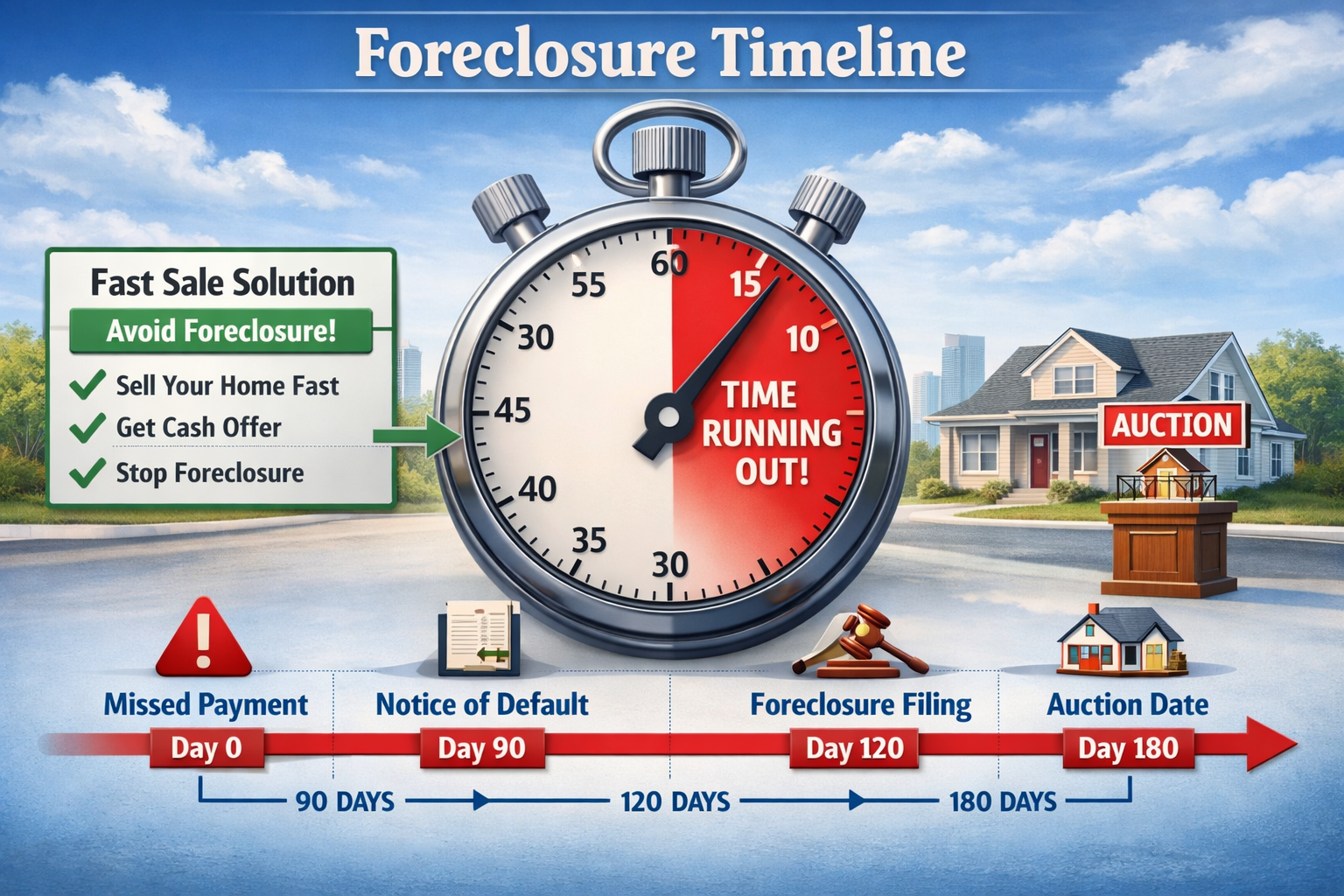

Understanding the Foreclosure Timeline and Your Window of Opportunity

Foreclosure doesn’t happen overnight. The process unfolds in predictable stages, and each stage offers different opportunities for intervention. Understanding this timeline is the foundation of your emergency exit plan.

The Pre-Foreclosure Period: Your Maximum Leverage Phase

The pre-foreclosure period begins the moment you miss your first mortgage payment. This phase typically lasts 90-120 days and represents your golden window of opportunity.

Days 1-30: The Grace Period

Most lenders provide a 15-day grace period before assessing late fees. After 30 days of non-payment, your loan is officially delinquent. During this time, your lender’s loss mitigation department may reach out to discuss options.

This is when you have maximum negotiating power. Your lender hasn’t invested significant resources into the foreclosure process yet, making them more willing to work with you on alternatives.

Days 31-90: The Notice Period

After 90 days of missed payments, most lenders issue a Notice of Default (in non-judicial foreclosure states) or file a foreclosure lawsuit (in judicial foreclosure states). This formal notice starts the official foreclosure clock.

You still have substantial leverage during this period. The property hasn’t been publicly advertised for foreclosure auction, and you can still sell your house in pre-foreclosure with relative ease.

Days 91-120: The Acceleration Phase

The lender declares the entire loan balance due immediately (acceleration). Public notices may be filed, and the foreclosure sale date is typically set. Your window is narrowing, but you can still execute a fast sale strategy.

The Foreclosure Sale Phase: Racing Against the Clock

Once the foreclosure sale date is set, you’re in a race against time. The foreclosure timeline by state varies dramatically:

- Judicial foreclosure states (like Florida, New York, Illinois): 6-12 months or longer

- Non-judicial foreclosure states (like California, Texas, Georgia): 2-4 months

In some states, you have as little as 21 days from the final notice to the auction. In others, you might have several months. Knowing your state’s specific timeline is crucial for planning your exit strategy.

Post-Foreclosure: When Options Disappear

After the foreclosure auction, your ownership rights typically end. In some states, you may have a redemption period allowing you to reclaim the property by paying the full amount owed plus costs, but this is rarely feasible for homeowners already in financial distress.

The key insight? The earlier you act, the more options you have and the better your outcome will be.

Why Selling Fast Beats Letting Foreclosure Complete

Many homeowners facing foreclosure feel paralyzed by shame, denial, or hopelessness. They let the process run its course, thinking they have no alternatives. This is almost always the worst financial decision.

The True Cost of Completed Foreclosure

Foreclosure doesn’t just mean losing your home. The financial and personal consequences extend far beyond moving day:

Credit Score Devastation

A completed foreclosure drops your credit score by 200-400 points and remains on your credit report for seven years. This impacts:

- Future mortgage eligibility (typically 3-7 year waiting period)

- Auto loan interest rates

- Credit card approvals and limits

- Employment opportunities (many employers check credit)

- Rental applications (landlords often reject applicants with foreclosures)

Deficiency Judgments

If your home sells at foreclosure auction for less than you owe, many states allow lenders to pursue you for the difference. A foreclosure deficiency judgment can result in:

- Wage garnishment

- Bank account levies

- Additional credit damage

- Years of collection attempts

Lost Equity

Foreclosure auction sales typically occur at 20-40% below market value. Any equity you’ve built simply evaporates, going to the lender or third-party investors rather than into your pocket.

Tax Consequences

Forgiven debt from foreclosure may be considered taxable income by the IRS, potentially creating a substantial tax bill when you’re already financially struggling.

The Advantages of Selling Before Foreclosure

Selling your house fast to avoid foreclosure flips the script entirely:

✅ Preserve Your Credit: A voluntary sale impacts your credit far less than foreclosure, potentially saving you tens of thousands in higher interest rates over the following years.

✅ Capture Remaining Equity: If you have any equity in your home, selling allows you to keep it rather than losing it at auction.

✅ Avoid Deficiency Judgments: Selling at market value often covers your mortgage balance, eliminating the risk of owing money after losing your home.

✅ Control the Timeline: You choose when to move rather than facing a sheriff’s eviction notice.

✅ Maintain Dignity: Selling proactively demonstrates financial responsibility rather than abandonment.

✅ Faster Recovery: Your path back to homeownership shortens from 7+ years to potentially 2-3 years with proper planning.

“The difference between foreclosure and a strategic sale is the difference between financial catastrophe and a manageable setback. One closes doors for years; the other keeps your options open.” – Real Estate Recovery Specialist

Assessing Your Situation: Can You Sell Fast Enough?

Before committing to a fast-sale strategy, you need an honest assessment of your situation. Three critical factors determine whether selling fast is viable: time remaining, equity position, and property condition.

Factor #1: Time Remaining Until Foreclosure Sale

Calculate exactly how many days you have until the scheduled foreclosure auction. This number dictates which selling strategies are realistic.

90+ Days Available

With three months or more, you have multiple options:

- Traditional listing with a motivated-seller pricing strategy

- Short sale negotiation (if underwater)

- Cash buyer sale

- Lease-option arrangements

30-90 Days Available

Your options narrow to faster strategies:

- Aggressive pricing with traditional listing

- Cash buyers or investors

- Short sale (if lender cooperates quickly)

Less than 30 Days Available

Only the fastest options remain viable:

- Cash buyers who can close in 7-14 days

- Direct sale to investors

- Deed in lieu of foreclosure negotiation

Factor #2: Your Equity Position

Your equity situation fundamentally shapes your strategy and options.

Positive Equity (Home Worth More Than You Owe)

If you have equity, selling fast is straightforward. Price competitively, and you’ll likely receive offers quickly. Your goal is maximizing net proceeds while meeting your timeline.

Even modest equity ($10,000-$30,000) provides motivation to sell rather than walk away. This money can fund your next housing situation and provide a financial cushion.

Underwater/Negative Equity (You Owe More Than Home’s Worth)

If your mortgage balance exceeds your home’s current value, you’ll need to pursue a short sale or bring cash to closing. This complicates the process but doesn’t make it impossible.

Short sales require lender approval, adding 30-90 days to the timeline. However, selling a house with a tax lien or other complications may still be faster than foreclosure.

Break-Even Position

If you’ll roughly break even after paying off your mortgage, closing costs, and any liens, selling still makes sense to avoid foreclosure’s credit damage and potential deficiency judgments.

Factor #3: Property Condition and Complications

The faster you need to sell, the more important condition becomes.

Move-In Ready Properties

Well-maintained homes in good condition attract the broadest buyer pool and sell fastest. Traditional listings can work even on compressed timelines.

Properties Needing Repairs

Homes requiring significant repairs limit your buyer pool to investors and cash buyers. Traditional buyers using financing often can’t close quickly enough or won’t accept properties needing substantial work.

Properties with Title Issues or Liens

Complications like liens and judgments, unclear title, or multiple heirs require expert service to resolve quickly. These situations benefit from working with professionals experienced in complex property issues.

If you’re dealing with back taxes on property, judgment liens, or title problems, specialized buyers who understand these complications can often close faster than traditional buyers who would require clear title.

Your Emergency Exit Plan: Five Pathways to Sell House Fast to Avoid Foreclosure

Not all selling strategies are created equal when time is critical. Here are five proven pathways, ranked from fastest to slowest, with guidance on when each makes sense.

Pathway #1: Direct Sale to Cash Buyers (7-14 Days)

Best for: Homeowners with less than 60 days until foreclosure, properties in any condition, situations with title complications.

Cash buyers—typically investors or investment companies—purchase properties directly without financing contingencies. This eliminates the 30-45 day mortgage approval process that traditional buyers require.

How It Works

- Contact cash buying companies or investors

- Provide basic property information

- Receive cash offer within 24-48 hours

- Accept offer and set closing date

- Close in as little as 7 days

Advantages

- ⚡ Fastest option available: Close in as little as one week

- 🏚️ Sell as-is: No repairs or cleaning required

- 📋 Minimal paperwork: Simplified process

- ✅ Certainty: No financing fall-through risk

- 🔧 Handles complications: Many cash buyers work with properties that have liens, title issues, or other problems

Disadvantages

- 💰 Lower price: Typically 70-85% of market value

- 🔍 Due diligence required: Not all cash buyers are reputable

When to Choose This Path

Cash buyers make sense when speed is paramount and you have limited or no equity. If you’re facing foreclosure in 30-60 days, the price discount is offset by avoiding foreclosure’s devastating consequences.

For properties with complications—liens, title problems, or multiple owners—cash buyers often provide the only realistic fast-sale option.

Pathway #2: Aggressive Traditional Listing (30-60 Days)

Best for: Homeowners with 90+ days until foreclosure, properties in good condition, situations with equity to preserve.

A traditional listing with aggressive pricing and marketing can work if you have sufficient time and your property appeals to conventional buyers.

How It Works

- Hire an experienced agent who understands foreclosure urgency

- Price 5-10% below market value for quick sale

- Prepare home for showings (clean, declutter, minor repairs)

- Accept first reasonable offer

- Close in 30-45 days (typical financing timeline)

Advantages

- 💵 Higher sale price: Market value or close to it

- 🏡 Broader buyer pool: Access to all traditional buyers

- 🤝 Professional guidance: Agent handles negotiations and paperwork

Disadvantages

- ⏰ Slower process: Minimum 30-45 days even with quick offer

- 🔧 Preparation required: Property must show well

- ❌ Uncertainty: Deals can fall through during financing

- 💸 Costs: Agent commissions (typically 5-6%)

When to Choose This Path

Traditional listing makes sense when you have 90+ days until foreclosure and your home is in good condition. The higher sale price justifies the longer timeline and preparation effort.

Price aggressively from day one. In foreclosure situations, you can’t afford to “test the market” at a higher price and reduce later. Every week counts.

Pathway #3: Short Sale (60-120 Days)

Best for: Underwater homeowners who owe more than the home is worth, situations where lender cooperation is possible.

A short sale occurs when your lender agrees to accept less than the full mortgage balance, allowing you to sell without bringing cash to closing.

How It Works

- Hire an agent experienced in short sales

- Contact lender’s loss mitigation department

- Submit short sale package (hardship letter, financials, listing agreement)

- List property and find buyer

- Submit buyer’s offer to lender for approval

- Negotiate with lender

- Close once lender approves

Advantages

- 💰 Avoid bringing cash to closing: Sell even when underwater

- 📉 Less credit damage than foreclosure: Impact similar to late payments

- 🚫 May avoid deficiency judgment: Lender often waives remaining balance

Disadvantages

- ⏳ Time-consuming: 60-120+ days typical

- 📋 Complex process: Extensive documentation required

- ❓ Uncertain outcome: Lender may reject offers or demand too much

- 💳 Credit impact: Still damages credit, though less than foreclosure

When to Choose This Path

Short sales work when you’re underwater, have 90+ days until foreclosure, and your lender indicates willingness to cooperate. Learn more about how to do a short sale to understand the complete process.

Not all lenders process short sales efficiently. Some drag the process out until foreclosure becomes unavoidable. Get clear timelines from your lender before committing to this path.

Pathway #4: Deed in Lieu of Foreclosure (30-60 Days)

Best for: Homeowners with no equity, no other options working, and cooperative lenders.

A deed in lieu involves voluntarily transferring your property deed to the lender in exchange for release from the mortgage obligation.

How It Works

- Contact lender’s loss mitigation department

- Request deed in lieu consideration

- Submit financial documentation proving hardship

- Lender evaluates property value

- Negotiate terms (moving assistance, deficiency waiver)

- Sign deed transfer documents

- Vacate property by agreed date

Advantages

- 🏃 Faster than foreclosure: Typically 30-60 days

- 💳 Less credit damage: Impacts credit less than completed foreclosure

- 🚫 Deficiency waiver possible: Lender may waive remaining balance

- 💵 Relocation assistance: Some lenders offer moving money

Disadvantages

- 🏠 Lose the property: No equity preservation

- 📋 Not always accepted: Lenders may prefer foreclosure

- 💳 Still damages credit: Significant negative impact

- 🔍 Junior liens complicate: Lenders won’t accept with second mortgages/liens

When to Choose This Path

Deed in lieu makes sense as a last resort when you have no equity, can’t sell fast enough, and want to minimize foreclosure’s impact. It’s essentially a negotiated surrender that’s less damaging than forced foreclosure.

Pathway #5: Lease-Option or Owner Financing (Variable Timeline)

Best for: Homeowners with equity and time (90+ days), properties in good condition, situations where traditional financing is challenging.

Creative financing strategies can attract buyers who can’t get traditional mortgages but can make monthly payments.

How It Works

Lease-Option:

- Find tenant-buyer who wants to purchase eventually

- Structure lease with option to buy within 1-3 years

- Collect option fee (typically 3-5% of purchase price)

- Tenant makes monthly payments covering your mortgage

- Tenant exercises option and purchases, or you keep option fee and re-lease

Owner Financing:

- Find buyer who can make down payment but can’t get traditional financing

- Structure seller-financed note (you act as the bank)

- Collect down payment

- Buyer makes monthly payments to you

- You use payments to cover your mortgage

- Buyer refinances to traditional mortgage within agreed timeframe

Advantages

- 💵 Immediate cash from option fee/down payment: Can catch up on mortgage

- 📈 Higher sale price: Often above market value

- 🏡 Broader buyer pool: Attracts buyers who can’t get traditional financing

- 💰 Ongoing income: Monthly payments may exceed your mortgage

Disadvantages

- ⏰ Doesn’t immediately solve foreclosure: You remain on mortgage

- ❌ Buyer may not complete purchase: Option may not be exercised

- 📋 Complex legal structure: Requires attorney guidance

- 🎯 Requires equity: Doesn’t work if underwater

When to Choose This Path

Creative financing works when you have equity, sufficient time (90+ days minimum), and can catch up on missed payments with the option fee or down payment. It’s not a true emergency exit but rather a strategy to stabilize the situation.

Step-by-Step: Executing Your Emergency Exit Plan

Once you’ve chosen your pathway, execution requires methodical action. Here’s your step-by-step implementation guide.

Step 1: Gather Critical Information (Day 1)

Before you can make informed decisions or present your property to buyers, collect these essential documents and details:

📄 Mortgage Information

- Current loan balance(s)

- Missed payment amounts

- Foreclosure sale date (if scheduled)

- Lender contact information

- Loan account numbers

📄 Property Information

- Property deed

- Recent property tax statement

- Homeowners insurance policy

- HOA information (if applicable)

- Recent mortgage statements

📄 Title Information

- Any known liens or judgments

- Property tax arrears

- Homeowners association dues owed

- Contractor liens or mechanic’s liens

📄 Financial Documentation

- Recent pay stubs or income documentation

- Bank statements

- Hardship explanation (job loss, medical bills, divorce, etc.)

If you’re dealing with property tax issues or other complications, gathering this information upfront accelerates the process significantly.

Step 2: Determine Your Property’s Value (Days 1-3)

You need an accurate understanding of your home’s current market value to make informed decisions.

Quick Valuation Methods

- Online estimators: Zillow, Redfin, Realtor.com (use as rough guides only)

- Comparative Market Analysis (CMA): Request from local real estate agents

- Professional appraisal: Most accurate but costs $300-500

- Cash buyer estimates: Many provide free valuations within 24 hours

Calculate Your Net Position

Once you know the value, calculate your equity position:

Property Value: $250,000

Minus Mortgage Balance: -$230,000

Minus Liens/Judgments: -$5,000

Minus Selling Costs (6-8%): -$18,000

═══════════════════════════

Net Proceeds: -$3,000 (underwater by $3,000)

This calculation determines which pathways are viable. Positive equity means you can sell traditionally or to cash buyers. Negative equity means you need a short sale or must bring cash to closing.

Step 3: Contact Your Lender Immediately (Day 2)

Many homeowners avoid their lender out of shame or fear. This is counterproductive. Lenders prefer solutions that avoid foreclosure’s expensive legal process.

What to Say

“I’m experiencing financial hardship due to [job loss/medical emergency/divorce] and cannot continue making my mortgage payments. I want to explore alternatives to foreclosure. Can you connect me with your loss mitigation department?”

What to Ask

- How much time do I have before foreclosure sale?

- Will you postpone the foreclosure sale while I pursue a sale?

- What programs or alternatives do you offer?

- Will you consider a short sale if I’m underwater?

- Can I get approval for a deed in lieu?

Document Everything

Keep detailed records of every conversation:

- Date and time

- Representative’s name and ID number

- What was discussed

- What was promised

- Follow-up required

Step 4: Choose Your Selling Strategy (Days 3-5)

Based on your timeline, equity position, and property condition, commit to the pathway that best fits your situation.

Decision Matrix

| Time Available | Equity Position | Best Strategy |

|---|---|---|

| Under 30 days | Any | Cash buyer |

| 30-60 days | Positive equity | Cash buyer or aggressive listing |

| 30-60 days | Negative equity | Cash buyer or deed in lieu |

| 60-90 days | Positive equity | Aggressive listing |

| 60-90 days | Negative equity | Short sale |

| 90+ days | Positive equity | Traditional listing |

| 90+ days | Negative equity | Short sale |

Step 5: Implement Your Chosen Strategy (Days 5-7)

Take immediate action on your selected pathway.

For Cash Buyer Sales:

- Contact 3-5 reputable cash buying companies

- Provide property details and timeline

- Compare offers and terms

- Verify buyer’s proof of funds

- Select buyer and set closing date

For Traditional Listings:

- Interview and hire experienced agent

- Sign listing agreement

- Prepare property for showing

- Price aggressively for quick sale

- Begin marketing immediately

For Short Sales:

- Hire short sale specialist agent

- Submit short sale package to lender

- List property

- Find buyer

- Submit offer to lender for approval

For Deed in Lieu:

- Submit formal request to lender

- Provide financial documentation

- Negotiate terms

- Arrange moving timeline

Step 6: Navigate the Closing Process (Variable Timeline)

Once you have a buyer or lender agreement, focus on getting to the closing table as quickly as possible.

Stay in Communication

- Respond immediately to all requests

- Provide documents promptly

- Be available for inspections, appraisals, showings

- Keep your lender informed of progress

Prepare for Moving

Don’t wait until the last minute. Begin:

- Researching new housing options

- Packing non-essential items

- Arranging moving logistics

- Transferring utilities

Understand Closing Costs

Even in distress sales, you’ll face some closing costs:

- Title search and insurance

- Recording fees

- Transfer taxes (varies by state)

- Prorated property taxes

- HOA fees

Some buyers (especially cash buyers) will cover these costs. Negotiate this upfront.

Step 7: Close and Move Forward (Closing Day and Beyond)

At closing, you’ll sign documents transferring ownership and releasing you from the mortgage obligation.

What to Bring to Closing

- Government-issued ID

- Keys to the property

- Garage door openers, gate remotes

- Mailbox keys

- Security system codes

- Appliance manuals and warranties

Verify Foreclosure Cancellation

Ensure your lender files the necessary paperwork to cancel the foreclosure proceedings. Request written confirmation that:

- The foreclosure is withdrawn

- The mortgage is satisfied

- No deficiency judgment will be pursued

Begin Credit Repair

While selling before foreclosure minimizes damage, you’ll still need to rebuild:

- Monitor your credit reports for accuracy

- Dispute any errors

- Establish new positive payment history

- Keep credit utilization low

- Consider a secured credit card if needed

Working with Professionals Who Understand Complex Situations

Not all real estate professionals are equipped to handle foreclosure situations, especially when complicated by liens, title issues, or ownership disputes. The right expert service can mean the difference between success and failure.

When to Seek Specialized Help

Consider working with professionals experienced in complex property situations if you’re dealing with:

🔴 Multiple Liens or Judgments

Properties with tax liens, mechanic’s liens, or judgment liens require coordination with multiple parties to clear title. Professionals who regularly handle properties with liens understand the negotiation and payment priority process.

🔴 Title Issues

Unclear ownership, breaks in chain of title, or missing heirs complicate sales significantly. Specialists who work with title problems can navigate these challenges efficiently.

🔴 Multiple Owners or Heirs

When property has multiple owners who disagree on selling, or inherited property with several heirs, specialized guidance becomes essential.

🔴 Tax Complications

Back taxes, tax liens, or IRS liens require specific expertise to resolve. Understanding how to sell property with tax issues prevents delays and complications.

What to Look for in a Foreclosure Specialist

The right professional brings helpful solutions and expert service to your situation:

✅ Proven Experience: Look for professionals who have successfully closed foreclosure-avoidance sales, not just traditional transactions.

✅ Lien Resolution Expertise: They should understand lien priority, negotiation strategies, and payment coordination.

✅ Title Company Relationships: Strong relationships with title companies expedite problem-solving when issues arise.

✅ County and Legal Connections: Professionals who regularly work with county offices and attorneys can navigate bureaucratic processes faster.

✅ Transparent Communication: You need someone who explains options clearly, sets realistic expectations, and maintains helpful guidance throughout.

✅ Flexible Solutions: The best professionals offer multiple pathways rather than pushing a one-size-fits-all approach.

The Sure Path Property Solutions Approach

At Sure Path Property Solutions, we specialize in helping property owners navigate exactly these complicated situations. Our friendly and caring approach combines industry expertise with practical problem-solving.

We understand that foreclosure doesn’t happen in isolation. Often, homeowners facing foreclosure also deal with:

- Back taxes they can’t pay

- Liens from contractors or creditors

- Inherited property complications

- Multiple owners with conflicting interests

- Title issues that traditional buyers won’t accept

Our team coordinates with counties, title professionals, and lien holders to create clear pathways forward. We provide trustworthy service that simplifies complex situations, offering helpful solutions tailored to your specific circumstances.

Whether you need to sell quickly to a cash buyer or require time to resolve title issues before listing traditionally, we can guide you toward the approach that best serves your situation.

Common Obstacles and How to Overcome Them

Even with a solid plan, obstacles can derail your emergency exit strategy. Here’s how to navigate the most common challenges.

Obstacle #1: Lender Won’t Postpone Foreclosure Sale

The Problem: You’ve found a buyer or are close to closing, but the foreclosure sale date arrives first.

Solutions:

- Request a formal postponement in writing, explaining you have a pending sale

- Have your buyer or agent contact the lender directly to confirm the transaction

- File for temporary bankruptcy protection (Chapter 13) to trigger automatic stay—this immediately halts foreclosure but should be a last resort

- Explore whether your state offers redemption rights allowing you to reclaim the property post-auction

Obstacle #2: Property Won’t Appraise for Loan Amount

The Problem: Your buyer’s lender orders an appraisal that comes in below the purchase price, jeopardizing the sale.

Solutions:

- Reduce the price to match the appraisal (if timeline permits)

- Request the buyer increase their down payment to cover the gap

- Challenge the appraisal with comparable sales data

- Switch to a cash buyer who doesn’t require an appraisal

- Consider seller financing to bridge the gap

Obstacle #3: Title Issues Discovered During Closing Process

The Problem: The title search reveals liens, judgments, or ownership questions that must be resolved before closing.

Solutions:

- Work with a title company experienced in complex situations

- Negotiate with lien holders for reduced payoffs (many accept less than full amount)

- Use sale proceeds to pay liens at closing (title company coordinates)

- Seek quiet title action if ownership is unclear (time-consuming but sometimes necessary)

- Consider selling to buyers who purchase properties with title problems

Obstacle #4: Co-Owner Won’t Agree to Sell

The Problem: You own the property with someone else (spouse, sibling, ex-partner) who refuses to cooperate with the sale.

Solutions:

- Negotiate a buyout if you can afford to purchase their share

- Explore partition action lawsuit to force the sale (court-ordered)

- Demonstrate how foreclosure harms them too (credit damage, lost equity)

- Offer concessions (larger share of proceeds, covering moving costs)

- Consult an attorney about your specific ownership structure and rights

Obstacle #5: Property in Severe Disrepair

The Problem: Your home needs substantial repairs that you can’t afford, limiting buyer interest.

Solutions:

- Target investor and cash buyers who purchase as-is properties

- Price significantly below market to account for needed repairs

- Obtain repair estimates and provide to buyers upfront (transparency builds trust)

- Consider selling to wholesalers who specialize in distressed properties

- Disclose all known issues to avoid legal complications later

Obstacle #6: Emotional Paralysis

The Problem: Shame, denial, or overwhelm prevents you from taking action.

Solutions:

- Reframe the situation: Selling proactively is responsible, not shameful

- Focus on the future: This is a temporary setback, not a permanent identity

- Seek support: Talk to a counselor, trusted friend, or financial advisor

- Take small steps: Break the process into manageable daily tasks

- Remember: Millions of Americans have faced foreclosure; you’re not alone

Protecting Yourself: Red Flags and Scams to Avoid

Unfortunately, homeowners in foreclosure are targets for scammers and predatory operators. Protect yourself by recognizing these red flags.

Foreclosure Rescue Scams

The Scam: A “rescuer” offers to save your home if you sign over the deed temporarily, promising to secure refinancing and deed the property back to you. They collect rent from you, pocket the money, and never return the property.

Red Flags:

- Requests to sign over your deed

- Promises of guaranteed refinancing

- Asks you to make payments to them instead of your lender

- Pressures you to sign documents without attorney review

- Charges large upfront fees before providing services

Protection: Never sign over your deed to anyone unless you’re intentionally selling the property. Consult an attorney before signing any documents you don’t fully understand.

Equity Skimming

The Scam: A buyer offers to purchase your property and let you stay as a renter, promising to help you buy it back later. They take your equity, collect rent, never make mortgage payments, and the home goes to foreclosure anyway.

Red Flags:

- Promises you can stay in the home and buy it back

- Offers to “take over” your mortgage payments

- Requests you move out temporarily

- Provides vague or confusing contracts

Protection: If selling, plan to move out. Don’t enter arrangements where you remain in the home after selling unless structured through legitimate attorney-drafted agreements.

Phantom Help Scams

The Scam: Companies charge large upfront fees to negotiate with your lender or file paperwork on your behalf, then provide no actual services.

Red Flags:

- Demands large upfront fees before providing services

- Guarantees they can stop foreclosure

- Tells you not to contact your lender directly

- Isn’t licensed or accredited

- Has no verifiable track record

Protection: Legitimate housing counselors approved by HUD provide free assistance. Never pay large upfront fees for foreclosure help.

Lowball Cash Buyer Scams

The Scam: Not all cash buyers are scammers, but some prey on desperate homeowners by offering extremely low prices and using high-pressure tactics.

Red Flags:

- Offers 40-50% or less of market value without justification

- Pressures you to sign immediately without time to consider

- Discourages you from getting other opinions

- Uses scare tactics about your foreclosure timeline

- Won’t provide references or proof of funds

Protection: Get multiple offers. Legitimate cash buyers typically offer 70-85% of market value. Lower offers should be justified by specific property conditions or complications.

Frequently Asked Questions

Q: How much time do I have once I receive a foreclosure notice?

A: This varies dramatically by state and foreclosure type. In judicial foreclosure states, you may have 6-12 months. In non-judicial states, as little as 90-120 days from the initial notice to the auction. Contact your lender immediately to understand your specific timeline.

Q: Can I sell my house if foreclosure proceedings have already started?

A: Yes, absolutely. You can sell at any point before the foreclosure auction is completed. In fact, selling in pre-foreclosure is one of the best ways to avoid foreclosure’s consequences.

Q: Will I owe money after selling my house to avoid foreclosure?

A: It depends on your equity position. If your home sells for more than you owe (including the mortgage, liens, and selling costs), you won’t owe anything and may receive proceeds. If you’re underwater and pursue a short sale, the lender may waive the deficiency, but this must be negotiated and confirmed in writing.

Q: How does selling before foreclosure affect my credit compared to letting foreclosure complete?

A: Selling before foreclosure is significantly less damaging. A completed foreclosure drops your credit score 200-400 points and remains for seven years. A strategic sale before foreclosure may only impact your credit by 50-100 points (from the late payments), and you can begin rebuilding immediately.

Q: Can I sell my house if I have liens or back taxes?

A: Yes. Liens don’t prevent selling; they just must be addressed during the sale process. Typically, liens are paid from the sale proceeds at closing. If proceeds don’t cover all liens, you may need to negotiate reduced payoffs or bring cash to closing. Learn more about selling with liens.

Q: What if I inherited the property and there are multiple owners?

A: Multiple ownership complicates sales but doesn’t prevent them. All owners must typically agree to sell, or one owner can pursue a partition action to force the sale. Working with professionals experienced in inherited property with multiple owners streamlines this process.

Q: Should I just walk away and let the bank take the house?

A: Walking away is almost always the worst option. You lose any equity, damage your credit severely, risk deficiency judgments, and may face tax consequences. Selling proactively—even for less than you hoped—produces better outcomes in virtually every scenario.

Q: How do I know if a cash buyer is legitimate?

A: Legitimate cash buyers provide:

- Proof of funds (bank statements or letters)

- References from previous sellers

- Clear, written offers with no hidden fees

- Professional contracts reviewed by attorneys

- Reasonable timelines and expectations

Get multiple offers and don’t feel pressured to accept the first one.

Q: What happens if my house doesn’t sell before the foreclosure auction date?

A: If the auction occurs before you close on a sale, you lose the property. This is why choosing the right selling strategy for your timeline is critical. Cash buyers can close in 7-14 days, while traditional sales take 30-60 days minimum.

Taking Action: Your Next Steps Today

Knowledge without action won’t save your home. Here’s exactly what to do today to begin executing your emergency exit plan.

Immediate Actions (Today)

- Calculate Your Timeline: Determine exactly how many days until your foreclosure sale date. If you don’t know the date, call your lender immediately to find out.

- Assess Your Equity: Use online estimators or contact local agents for a quick property valuation. Calculate whether you have positive equity, are underwater, or will break even.

- Gather Your Documents: Collect mortgage statements, foreclosure notices, property tax records, and any lien information you have.

- Contact Your Lender: Call the loss mitigation department and explain your intention to sell. Ask about postponement options and timelines.

- Research Your Options: Based on your timeline and equity position, identify which selling pathway makes most sense for your situation.

This Week

- Get Multiple Property Valuations: Contact 2-3 cash buyers for offers, request CMAs from local agents, or order an appraisal.

- Interview Professionals: If your situation involves complications (liens, title issues, multiple owners), contact specialists who handle these scenarios regularly.

- Choose Your Strategy: Commit to the selling pathway that best fits your timeline, equity position, and property condition.

- Take First Action: List with an agent, contact cash buyers, submit a short sale package, or request deed in lieu—whatever your chosen strategy requires.

- Create a Moving Plan: Begin researching new housing options and preparing for transition.

This Month

- Execute Your Plan: Follow through on your chosen selling strategy with urgency and focus.

- Maintain Communication: Stay in constant contact with your lender, buyer, agent, or other professionals involved.

- Prepare the Property: Make your home as presentable as possible given your timeline and resources.

- Respond Quickly: Answer all requests for information, documents, or access immediately.

- Finalize Moving Arrangements: Secure your next housing situation and arrange logistics.

Conclusion: From Crisis to Fresh Start

Facing foreclosure ranks among life’s most stressful experiences. The fear, shame, and uncertainty can feel overwhelming. But here’s the empowering truth: you have more control than you think, and foreclosure is not inevitable.

Selling your house fast to avoid foreclosure transforms you from a passive victim of circumstances into an active problem-solver taking charge of your financial future. While you can’t change the past events that led to this moment, you absolutely can control what happens next.

The strategies outlined in this emergency exit plan—from cash buyer sales to strategic listings to short sales—provide proven pathways out of foreclosure. The key is matching the right strategy to your specific situation and acting with urgency.

Remember these critical principles:

Time is your most valuable asset. Every day you delay narrows your options and reduces your leverage. The homeowners who successfully avoid foreclosure are those who act immediately upon recognizing the problem.

You don’t have to navigate this alone. Professional guidance from industry experts who understand complicated property situations can accelerate your timeline and improve your outcome. Whether you’re dealing with liens, title issues, multiple owners, or other complications, helpful solutions exist.

This is not a permanent failure. Millions of Americans have faced foreclosure and recovered to achieve financial stability and even homeownership again. This is a temporary setback, and how you handle it determines how quickly you recover.

Proactive selling beats passive foreclosure every time. The difference in credit impact, equity preservation, and future opportunities is profound. Choosing to sell strategically demonstrates financial responsibility and protects your future.

If you’re facing foreclosure and need expert service to navigate complex property issues—back taxes, liens, judgments, unclear title, or multiple heirs—Sure Path Property Solutions provides the trustworthy service and helpful guidance you need. Our team coordinates with counties, title professionals, and other stakeholders to create clear pathways forward, even in the most complicated situations.

Your emergency exit plan starts today. Take the first step, and you’ll be amazed at how quickly a seemingly impossible situation becomes manageable. The path forward exists—you just need the courage to take it.

Ready to explore your options? Contact us for a confidential consultation about your specific situation. We’re here to help you navigate this challenge and move toward a brighter future.