Sell House Notice of Default: Your Options After NOD

Receiving a Notice of Default (NOD) in your mailbox feels like a punch to the gut. Your heart races, your palms sweat, and suddenly the home you’ve built memories in feels like it’s slipping through your fingers. But here’s the truth that most homeowners don’t realize: a Notice of Default is not the end—it’s actually a warning that gives you time to act. When you need to sell house Notice of Default: Your Options After NOD become critical knowledge that can save your credit, preserve your equity, and help you move forward with dignity. The period after receiving an NOD is when you have the most power to control your outcome, and understanding your options can mean the difference between financial devastation and a fresh start.

Key Takeaways

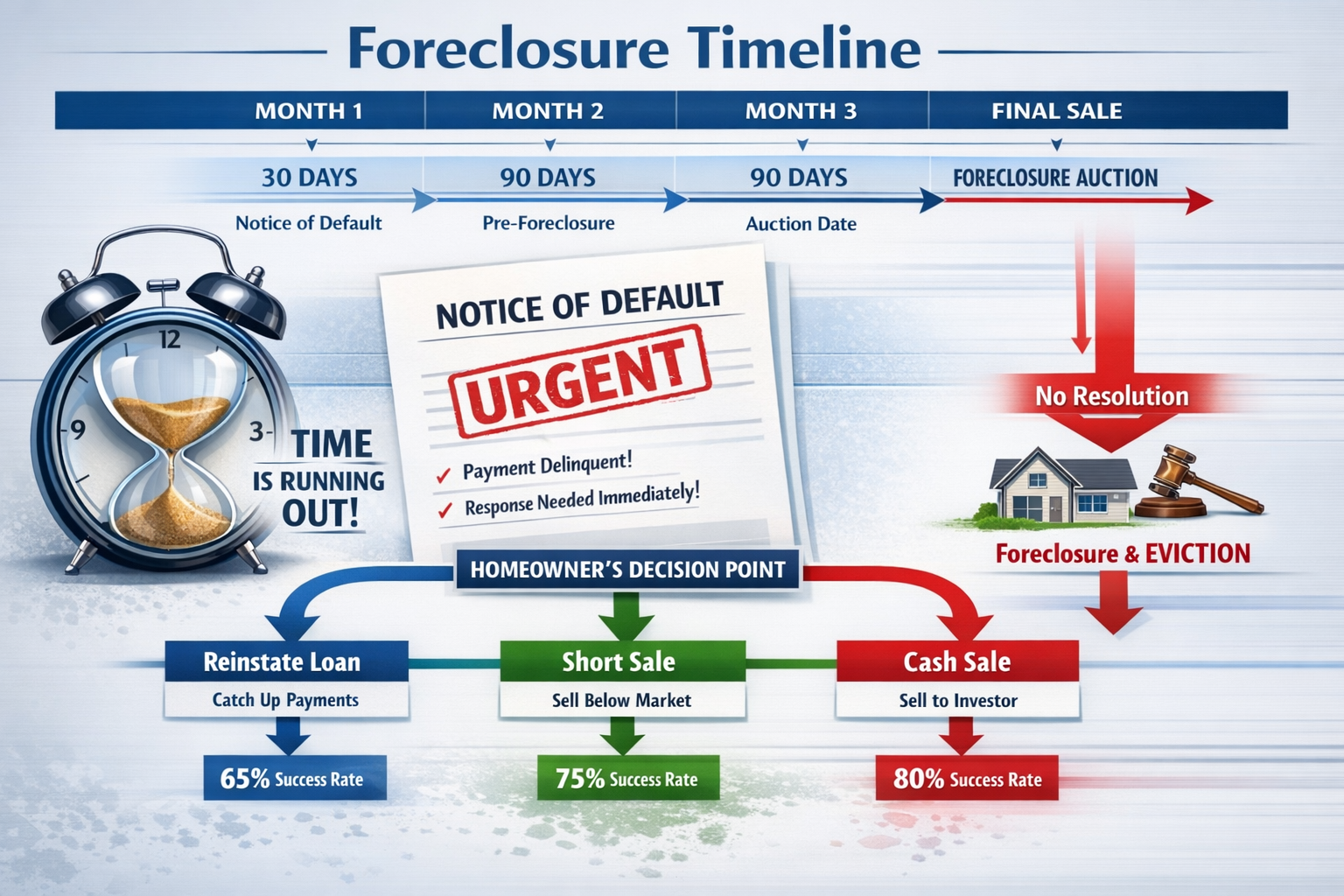

- A Notice of Default gives you 90-120 days before foreclosure proceedings accelerate, providing a critical window to explore alternatives

- Selling your home after NOD is possible and often the best option to preserve equity, avoid foreclosure, and protect your credit score

- Multiple exit strategies exist including loan reinstatement, short sales, deed in lieu, and cash sales to investors who specialize in pre-foreclosure properties

- Time is your most valuable asset after receiving an NOD—taking action within the first 30 days dramatically increases your options

- Professional guidance from industry experts can help navigate complex situations involving liens, judgments, or title issues that complicate traditional sales

Understanding the Notice of Default and What It Means

A Notice of Default is a formal legal document filed by your mortgage lender with the county recorder’s office. It serves as public notice that you’ve failed to make mortgage payments according to your loan agreement—typically after missing three to six consecutive payments.

This document triggers the beginning of the foreclosure process, but it’s important to understand that foreclosure is not immediate.

The Timeline After NOD

The foreclosure timeline varies significantly by state, but most follow a general pattern:

| Timeline Stage | Time Period | What Happens |

|---|---|---|

| Missed Payments | 1-3 months | Lender sends payment reminders and late notices |

| Notice of Default | Month 4-6 | Official NOD filed and sent to homeowner |

| Reinstatement Period | 90-120 days | Homeowner can cure default by paying arrears |

| Notice of Trustee Sale | After reinstatement period | Auction date is set (typically 21-30 days out) |

| Foreclosure Auction | Final stage | Property sold to highest bidder |

During the reinstatement period following your NOD, you maintain significant control over the situation. This is when exploring options to sell your house in pre-foreclosure becomes most advantageous.

How NOD Affects Your Property and Credit

The moment an NOD is filed, several immediate consequences occur:

Public Record Impact: The NOD becomes part of public records, meaning anyone can see that your property is in pre-foreclosure. This attracts investors, but it also signals financial distress.

Credit Score Damage: Your credit score has already taken hits from missed payments (30-60 points per missed payment). The NOD itself adds another 50-100 point drop, though this is less damaging than a completed foreclosure, which can devastate your score by 200-300 points.

Equity Preservation Window: Here’s the silver lining—during the NOD period, you can still sell the property and potentially walk away with your equity intact, unlike after foreclosure when you lose everything.

Common Reasons Homeowners Receive NOD

Understanding why you’re in this situation helps determine the best path forward:

- Job loss or income reduction (40% of cases)

- Medical emergencies and unexpected healthcare costs (25% of cases)

- Divorce or family changes (15% of cases)

- Adjustable-rate mortgage resets (10% of cases)

- Property tax delinquency that triggered acceleration (10% of cases)

If your situation involves back taxes on property, the complexity increases, but helpful solutions still exist.

Sell House Notice of Default: Your Primary Options After NOD

When you receive a Notice of Default, you’re standing at a crossroads with several distinct paths forward. Each option has different timelines, costs, and outcomes. Let’s explore them in detail so you can make an informed decision based on your unique circumstances.

Option 1: Reinstate Your Mortgage Loan

Loan reinstatement means paying all past-due amounts, plus fees and penalties, to bring your mortgage current and stop the foreclosure process.

Requirements for Reinstatement

To successfully reinstate your loan, you’ll need to pay:

- All missed mortgage payments

- Late fees and penalties

- Legal fees incurred by the lender

- Any property tax or insurance payments the lender made on your behalf

- Recording fees for the NOD

Example: If you missed four payments of $2,000 each, you’d need approximately $8,000 plus $500-1,500 in fees—potentially $9,500 total.

Pros and Cons of Reinstatement

✅ Advantages:

- You keep your home

- Foreclosure process stops immediately

- Credit damage is minimized compared to other options

- You maintain your existing interest rate

❌ Disadvantages:

- Requires significant cash immediately

- Doesn’t address underlying financial problems

- May only delay foreclosure if income issues persist

- Lender may be less flexible in future hardships

Reality check: Reinstatement works best when your financial crisis was temporary (like a short-term job loss) and you’ve since recovered stable income. If the underlying problem hasn’t been resolved, you’re likely just postponing the inevitable.

Option 2: Loan Modification and Forbearance

A loan modification permanently changes your mortgage terms—potentially lowering your interest rate, extending the loan term, or even reducing the principal balance. Forbearance temporarily reduces or suspends payments while you recover financially.

How to Request Modification

Contact your lender’s loss mitigation department immediately and:

- Request a loan modification application package

- Gather required financial documents (pay stubs, tax returns, bank statements)

- Write a hardship letter explaining your situation

- Submit complete application before the reinstatement period expires

- Respond promptly to all lender requests for additional information

⚠️ Important: Continue making whatever payments you can during the modification review process. This demonstrates good faith and improves approval chances.

Success Rates and Realistic Expectations

According to 2026 data, approximately 35-40% of loan modification applications are approved. Success depends heavily on:

- Demonstrating genuine hardship beyond your control

- Showing sufficient income to afford modified payments

- Providing complete documentation quickly

- Working with a lender that participates in modification programs

The challenge: The modification process typically takes 60-90 days—consuming most of your reinstatement period. If denied, you’ll have limited time to pursue other options.

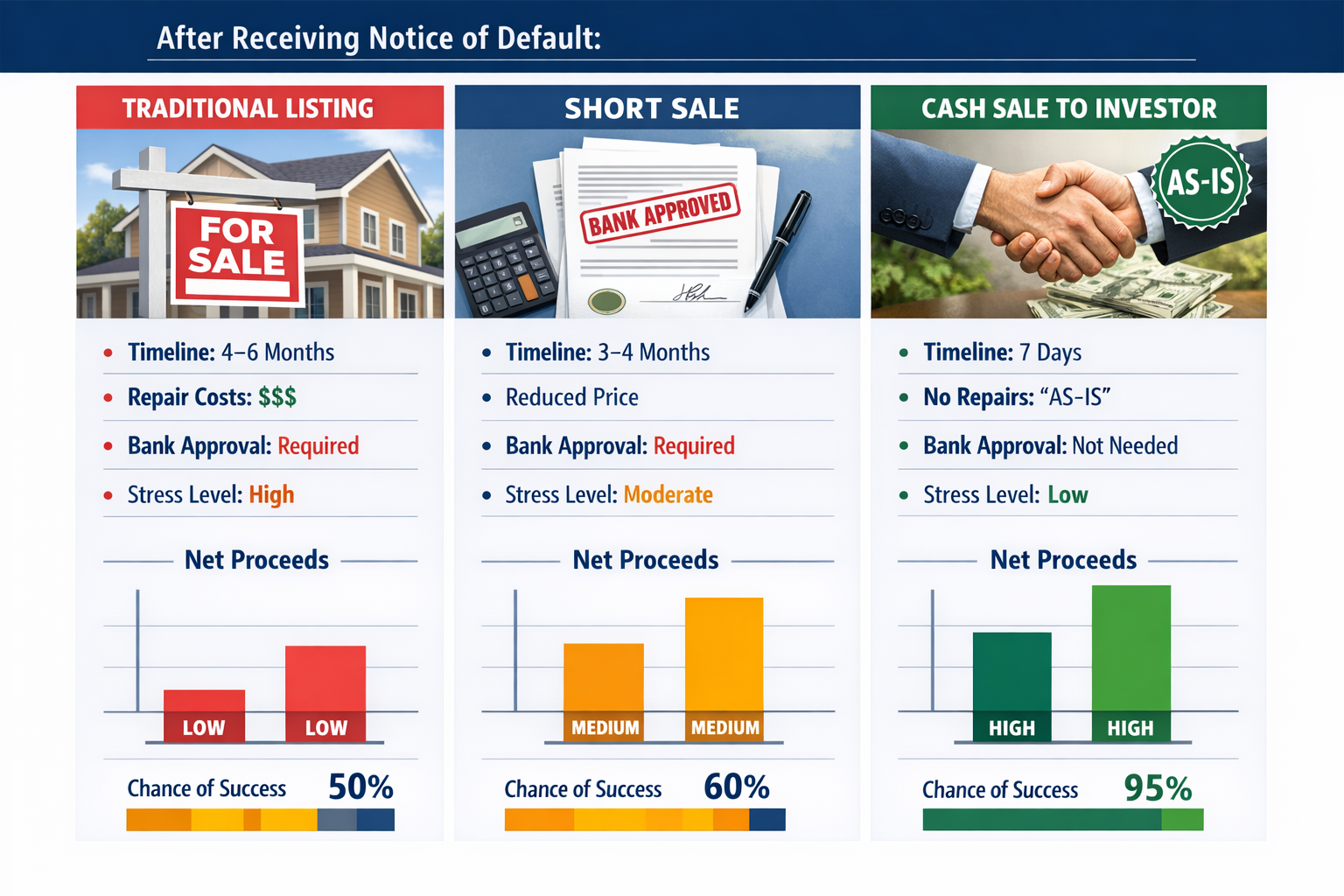

Option 3: Short Sale Your Property

A short sale occurs when your lender agrees to accept less than the full mortgage balance as payment in full, allowing you to sell the property even though the sale price won’t cover what you owe.

Short Sale Process and Timeline

The short sale process typically follows these steps:

- Contact your lender (Week 1): Request short sale approval and obtain their package

- List the property (Week 2-3): Work with a real estate agent experienced in short sales

- Receive an offer (Week 4-12): Marketing time varies by market conditions

- Submit to lender (Week 13): Send offer package with complete financial documentation

- Lender review (Week 14-26): Bank evaluates offer and orders BPO (Broker Price Opinion)

- Negotiation (Week 27-30): Back-and-forth on price and terms

- Closing (Week 31-34): If approved, proceed to closing

Total timeline: 4-8 months on average—which often extends beyond your NOD reinstatement period.

Advantages and Disadvantages

✅ Benefits:

- Avoid foreclosure on your credit report

- May qualify for relocation assistance ($3,000-10,000)

- Potential for lender to waive deficiency judgment

- Less credit damage than foreclosure (100-150 point drop vs. 200-300)

❌ Drawbacks:

- Very lengthy process with no guarantee of approval

- Lender may pursue deficiency judgment for shortfall

- Requires full financial disclosure to lender

- May have tax consequences (forgiven debt counted as income)

- Property must be actively marketed at fair market value

Critical consideration: If you have liens or judgments on your property, the short sale becomes significantly more complex because all lienholders must agree to the sale terms.

Option 4: Deed in Lieu of Foreclosure

A deed in lieu means you voluntarily transfer ownership of the property back to the lender in exchange for release from the mortgage obligation.

Requirements and Process

Lenders typically require:

- Demonstrated inability to sell the property through short sale

- No other liens on the property (or agreement from other lienholders)

- Property in reasonable condition

- Vacant property (in some cases)

The deed in lieu process takes 60-90 days and involves:

- Submitting a formal request with financial documentation

- Lender evaluation of the property condition and value

- Negotiation of terms (especially regarding deficiency balance)

- Signing transfer documents

- Vacating the property

When This Makes Sense

Deed in lieu works best when:

- You have no equity in the property

- The property won’t sell through traditional or short sale methods

- You want to avoid the public nature of foreclosure

- The lender agrees to waive deficiency judgment

- You need a faster resolution than foreclosure provides

The reality: Most lenders view deed in lieu as a last resort and will require you to attempt a short sale first. Additionally, this option still damages your credit significantly (similar to short sale impact).

Option 5: Sell House Notice of Default to a Cash Buyer

Selling your property to a cash investor or company that specializes in pre-foreclosure purchases offers the fastest exit strategy and often the most control over your outcome.

How Cash Sales Work in Pre-Foreclosure

Cash buyers purchase properties “as-is” in their current condition, typically following this streamlined process:

- Contact investor (Day 1): Reach out to reputable cash buyers

- Property evaluation (Day 2-3): Investor assesses property and situation

- Receive cash offer (Day 3-5): Written offer presented, usually within 24-72 hours

- Accept offer (Day 5-7): Review and accept terms

- Title work (Day 8-20): Investor handles title search and clearance

- Closing (Day 21-30): Quick closing, often in as little as 7-14 days

Total timeline: 7-30 days—well within your reinstatement period.

Benefits of Working with Professional Cash Buyers

💰 Speed: Close in days or weeks instead of months

🏠 As-Is Purchase: No repairs, cleaning, or staging required

💼 Certainty: No financing contingencies that could fall through

🤝 Expertise: Buyers experienced with liens, judgments, and title issues

📋 Simplicity: Minimal paperwork and hassle

⏰ Flexibility: Close on your timeline

When you work with Sure Path Property Solutions, you’re partnering with industry experts who understand the urgency of your situation and provide helpful guidance throughout the entire process. We coordinate with counties, title professionals, and lienholders to create clear, practical solutions even in complicated situations.

Finding Reputable Cash Buyers

Not all cash buyers are created equal. Look for:

- Established local presence with verifiable address and history

- Transparent process with clear explanations of how offers are calculated

- Professional credentials and positive reviews

- No upfront fees (legitimate buyers don’t charge you)

- Written offers with clear terms and timelines

- Proof of funds demonstrating ability to close

Red flags to avoid:

- Pressure tactics or urgency to sign immediately

- Requests for upfront payments or fees

- Unwillingness to provide references

- Vague or verbal-only offers

- No physical office or local presence

Option 6: Traditional Sale (If Time Permits)

If you’re early in the NOD period and your property is in good condition in a strong market, a traditional sale through a real estate agent might net you the highest sale price.

Realistic Timeline Considerations

A traditional sale typically requires:

- 2-4 weeks: Property preparation, repairs, staging

- 4-8 weeks: Marketing and showing period

- 1-2 weeks: Offer negotiation

- 30-45 days: Buyer’s financing and inspection period

- Total: 3-4 months minimum

The challenge: You only have 90-120 days from NOD to foreclosure auction. Any delays—buyer financing falls through, inspection issues, title problems—can push you past your deadline.

When Traditional Sales Make Sense

Consider traditional listing if:

- You received NOD very early (just filed)

- Your property is in excellent, market-ready condition

- Your local market has very low inventory and high demand

- You have significant equity to preserve

- You can afford to make payments during the sale period

Important: Even with a traditional listing, inform your agent about the NOD immediately. They need to communicate urgency to potential buyers and price accordingly for a quick sale.

Critical Factors to Consider When Deciding Your Path

Choosing the right option after receiving a Notice of Default requires careful evaluation of your unique situation. Let’s examine the key factors that should influence your decision.

Your Available Timeline

Time is your most valuable—and depleting—resource after receiving an NOD.

Calculate your exact timeline:

- Find the date your NOD was filed (on the document itself)

- Determine your state’s reinstatement period (typically 90-120 days)

- Subtract time already elapsed

- Add 30 days buffer for unexpected delays

Example: If your NOD was filed March 1st in a state with a 90-day reinstatement period, your deadline is approximately May 30th. If it’s now March 15th, you have roughly 75 days—but should plan for 45 days to allow cushion.

Decision framework based on timeline:

- 90+ days remaining: Traditional sale or short sale possible

- 60-89 days remaining: Cash sale or loan modification recommended

- 30-59 days remaining: Cash sale strongly recommended

- Under 30 days: Emergency cash sale only viable option

Your Equity Position

Your equity determines which options are financially viable and how much you might walk away with.

Calculate your equity:

Current market value – (Mortgage balance + Liens + Back taxes + Selling costs) = Net equity

Scenarios:

Positive equity (property worth more than you owe):

- Traditional sale or cash sale make sense

- You’ll walk away with money

- Reinstatement may be worth considering if you want to keep the home

Break-even (property worth approximately what you owe):

- Cash sale most practical (no agent commissions)

- Short sale possible but less advantageous

- Focus on avoiding foreclosure to protect credit

Negative equity (underwater—owe more than property worth):

- Short sale or deed in lieu primary options

- Cash sale unlikely unless investor sees unique value

- Reinstatement only if you plan long-term stay and expect appreciation

Your Financial Recovery Prospects

Honestly assess your financial trajectory:

Temporary hardship (job loss but now employed, one-time medical bill now resolved):

- Reinstatement or loan modification worth pursuing

- Keeping the home may be viable

Ongoing financial stress (reduced income, mounting debts, continued instability):

- Selling is likely your best option

- Avoiding foreclosure preserves your ability to recover financially

- Fresh start allows you to rebuild on solid foundation

Complete financial collapse (bankruptcy likely, multiple debts):

- Consult with bankruptcy attorney about timing

- Cash sale may provide funds to settle other debts

- Coordination between bankruptcy and foreclosure timing is critical

Property Condition and Market Factors

Your property’s condition and local market dynamics significantly impact your options.

Property condition assessment:

Excellent condition (move-in ready):

- Traditional sale viable if time permits

- Maximum sale price potential

- Attracts conventional buyers

Average condition (minor issues, dated but functional):

- Traditional sale possible with pricing adjustment

- Cash buyers ideal—no repair requirements

- Quick sale more important than maximum price

Poor condition (needs significant repairs, deferred maintenance):

- Traditional sale very difficult

- Cash buyers often only option

- Repair costs would consume equity anyway

Market conditions impact:

Strong seller’s market (low inventory, high demand):

- Properties sell quickly

- Multiple offers common

- Traditional sale more viable

Balanced or buyer’s market (normal inventory, moderate demand):

- Longer marketing times

- Cash sale provides certainty

- Price competition more intense

Weak market (high inventory, low demand):

- Extended time to sell

- Cash sale strongly recommended

- Traditional sale very risky given timeline

Complexity of Your Situation

Additional complications require specialized expertise and often eliminate certain options.

Common complications:

Multiple liens or judgments:

- Traditional buyers often walk away

- Cash buyers experienced with liens can navigate complexity

- All lienholders must be satisfied at closing

Title issues (breaks in chain of title, boundary disputes, missing heirs):

- Requires quiet title action or other legal remedies

- Dramatically extends timeline

- Specialized buyers essential

Inherited property with multiple heirs:

- All heirs must agree to sale

- Partition actions may be necessary

- Complex coordination required

Back property taxes:

- Must be paid at closing from proceeds

- Tax liens take priority over other debts

- Reduces net proceeds significantly

When facing complicated situations, working with expert service providers who specialize in problem properties becomes essential. Sure Path Property Solutions has extensive experience coordinating with counties, title professionals, and lienholders to resolve complex issues and create clear paths forward.

Steps to Take Immediately After Receiving NOD

The actions you take in the first 72 hours after receiving your Notice of Default can dramatically impact your outcome. Here’s your immediate action plan.

Day 1: Assess and Document

Hour 1-2: Read the NOD completely

- Note the filing date

- Identify the total amount needed to reinstate

- Find the deadline for reinstatement period

- Note the lender’s contact information

- Identify the trustee handling the foreclosure

Hour 3-4: Gather financial documents

- Recent pay stubs or income documentation

- Bank statements (last 2-3 months)

- Tax returns (last 2 years)

- Current mortgage statement

- Property tax statements

- List of all debts and monthly obligations

Hour 5-6: Calculate your numbers

- Current market value of your property (check Zillow, Redfin, recent sales)

- Total mortgage balance

- Amount in arrears

- Reinstatement amount (arrears + fees)

- Estimated equity position

- Your monthly income vs. expenses

Day 2: Explore Your Options

Morning: Contact your lender

- Call the loss mitigation department (not regular customer service)

- Ask about loan modification programs

- Request forbearance options

- Get reinstatement quote in writing

- Ask about their short sale process

Afternoon: Research sale options

- Contact 2-3 reputable cash buyers for preliminary discussions

- Research real estate agents with foreclosure experience

- Get initial property value estimates

- Understand your realistic timeline

Evening: Consult professionals

- Schedule consultation with foreclosure attorney (many offer free initial consultations)

- Consider HUD-approved housing counselor (free service)

- Research your state’s specific foreclosure laws and timeline

Day 3: Make Your Decision

Based on your timeline, equity, and circumstances, choose your primary path forward:

Decision matrix:

| Your Situation | Recommended Path | Backup Plan |

|---|---|---|

| 90+ days, positive equity, good condition | Traditional sale | Cash sale if no offers in 45 days |

| 60-90 days, positive equity | Cash sale | Short sale if equity is minimal |

| 30-60 days, any equity | Cash sale immediately | None—timeline too tight |

| Negative equity, any timeline | Short sale | Deed in lieu |

| Want to keep home, can afford modified payment | Loan modification | Reinstatement if modification denied |

Week 1: Take Action

Once you’ve chosen your path, act immediately:

If pursuing reinstatement or modification:

- Submit complete application package

- Provide all requested documentation

- Follow up every 3-5 days

- Continue making partial payments if possible

If selling (traditional or cash):

- Sign listing agreement or purchase contract

- Begin title work immediately

- Notify lender of pending sale

- Request payoff statement

- Coordinate with all parties for fastest closing

If pursuing short sale:

- List property with experienced agent

- Submit short sale package to lender

- Price aggressively for quick offers

- Respond immediately to all lender requests

How Sure Path Property Solutions Helps Homeowners in Default

When you’re facing foreclosure, you need more than a transaction—you need a partner who understands the complexity of your situation and provides trustworthy service with genuine care for your outcome.

Our Specialized Approach to NOD Situations

At Sure Path Property Solutions, we’ve built our entire business around helping property owners navigate complicated real estate issues. When you contact us about your Notice of Default, here’s what makes our approach different:

⏰ Speed with Accuracy

We provide cash offers within 24-48 hours, but we don’t rush you. We take time to understand your complete situation, explain your options clearly, and ensure you’re making the best decision for your circumstances.

🔍 Comprehensive Problem-Solving

We don’t just make offers—we solve problems. Whether you’re dealing with back taxes, multiple liens, judgment attachments, or title issues, our team coordinates with all necessary parties to create workable solutions.

💼 Professional Expertise

Our industry experts have handled hundreds of pre-foreclosure situations. We understand the legal requirements, timeline pressures, and negotiation strategies needed to close quickly and protect your interests.

🤝 Transparent Communication

We explain exactly how we calculate our offers, what costs are involved, and what you’ll net at closing. No surprises, no hidden fees, no pressure tactics—just honest, helpful guidance.

Real Solutions for Complex Situations

We specialize in situations that make traditional sales difficult or impossible:

Multiple Liens and Judgments

We negotiate with lienholders to achieve payoffs that allow the sale to proceed. Our established relationships with creditors and understanding of lien priority helps us navigate even the most tangled situations.

Property Tax Delinquency

If your NOD stems from property tax issues, we work directly with county tax offices to determine exact payoff amounts and coordinate payment at closing.

Title Problems

Clouded titles, breaks in chain of title, missing heirs, or boundary disputes don’t stop us. We have the resources and expertise to resolve title issues or purchase subject to resolving them post-closing.

Inherited Properties

When multiple heirs are involved or probate complications exist, we coordinate with all parties and provide solutions that work for everyone.

As-Is Condition

We purchase properties in any condition—from pristine to severely distressed. You won’t spend a dollar on repairs, cleaning, or improvements.

Our Process: Simple, Fast, and Supportive

Step 1: Initial Contact (Day 1)

Call us or submit your property information online. We’ll have a friendly, no-pressure conversation about your situation.

Step 2: Property Evaluation (Day 1-2)

We’ll schedule a convenient time to view the property (or in urgent situations, can make offers based on photos and description).

Step 3: Cash Offer (Day 2-3)

We present a written cash offer with clear explanation of our calculation and what you’ll net at closing.

Step 4: Your Decision (Your Timeline)

Take the time you need to review the offer, consult with family or advisors, and ask questions. We’re here to help, not pressure.

Step 5: Title and Coordination (Day 4-14)

Once you accept, we immediately order title work, coordinate with your lender for payoff, and handle all communication with lienholders, tax offices, and other parties.

Step 6: Closing (Day 7-30)

We close on your timeline—as fast as 7 days if needed, or we can accommodate a longer timeline if that serves you better.

Step 7: You Move Forward

You receive your proceeds, avoid foreclosure, and begin your fresh start with your credit protected and the stress behind you.

Why Homeowners Choose Us

Our clients consistently tell us these factors made the difference:

✅ Compassionate, caring approach during a stressful time

✅ Clear communication and patient explanation of options

✅ Fast, reliable closings that meet urgent deadlines

✅ Fair offers based on honest evaluation

✅ Problem-solving expertise for complicated situations

✅ No fees, no commissions charged to sellers

✅ Professional service from experienced industry experts

One recent client shared: “I was 45 days from foreclosure auction with two liens and back taxes. Every agent I contacted said it was too complicated. Sure Path took the time to understand everything, negotiated with all my creditors, and we closed in 18 days. They literally saved my credit and my sanity.”

Protecting Your Credit and Financial Future

While avoiding foreclosure is the immediate goal, protecting your long-term financial health should guide your decision-making process.

Credit Score Impact Comparison

Understanding the relative credit damage of each option helps you make informed decisions:

| Option | Credit Score Impact | Duration on Credit Report | Long-term Implications |

|---|---|---|---|

| Reinstatement | Minimal (late payments only: -30 to -90 points) | 7 years | Least damaging; can recover quickly |

| Loan Modification | Moderate (-50 to -100 points) | 7 years | May show as “partial payment agreement” |

| Short Sale | Significant (-100 to -150 points) | 7 years | Better than foreclosure; shows cooperation |

| Deed in Lieu | Significant (-100 to -150 points) | 7 years | Similar to short sale impact |

| Cash Sale (Pre-Foreclosure) | Moderate (-50 to -100 points from late payments only) | 7 years | Stops damage; no foreclosure notation |

| Foreclosure | Severe (-200 to -300 points) | 7 years | Most damaging; affects future lending significantly |

Key insight: Selling your property before foreclosure—whether through traditional sale, short sale, or cash sale—prevents the most severe credit damage. Your credit report will show late payments, but not foreclosure, which carries much more stigma with future lenders.

Timeline to Financial Recovery

How soon can you buy another home after each option?

After Reinstatement: Immediately eligible (loan never defaulted completely)

After Cash Sale in Pre-Foreclosure:

- FHA loan: 3 years with extenuating circumstances

- Conventional loan: 4 years

- VA loan: 2 years

After Short Sale:

- FHA loan: 3 years

- Conventional loan: 4 years (2 years with extenuating circumstances and 20% down)

- VA loan: 2 years

After Deed in Lieu:

- FHA loan: 3 years

- Conventional loan: 4 years

- VA loan: 2 years

After Foreclosure:

- FHA loan: 3 years (with extenuating circumstances and housing counseling)

- Conventional loan: 7 years (4 years with extenuating circumstances)

- VA loan: 2 years

The advantage is clear: Avoiding foreclosure by selling—especially to a cash buyer who can close quickly—reduces your waiting period for future home ownership by up to 3 years compared to foreclosure.

Tax Implications to Consider

When debt is forgiven, the IRS may consider it taxable income. Understanding these implications helps you plan appropriately.

Mortgage Forgiveness Debt Relief Act:

While this act expired in 2020, similar provisions may be available. Consult with a tax professional about current law and whether forgiven debt on your primary residence may be excluded from income.

Short Sale and Deed in Lieu Tax Consequences:

If your lender forgives part of your mortgage debt, they’ll issue a 1099-C form reporting the forgiven amount as income. This could result in significant tax liability.

Example: If you owe $300,000 but sell via short sale for $250,000, the $50,000 forgiven amount may be taxable. At a 22% tax bracket, that’s $11,000 in taxes owed.

Insolvency Exception: If you were insolvent (debts exceeded assets) at the time of forgiveness, you may exclude the forgiven debt from income. This requires Form 982 and careful documentation.

Cash Sale Advantage: When you sell to a cash buyer who pays off your mortgage completely, there’s no forgiven debt and therefore no tax consequence from the sale itself.

Action step: Consult with a tax professional or CPA before finalizing any option that involves debt forgiveness to understand your specific tax implications.

Deficiency Judgments and How to Avoid Them

A deficiency judgment occurs when the foreclosure sale price doesn’t cover your full mortgage debt, and the lender sues you personally for the difference.

Example: You owe $280,000. The property sells at foreclosure auction for $220,000. The lender may pursue a $60,000 deficiency judgment against you.

State Laws Vary:

- Non-recourse states (Alaska, Arizona, California, etc.): Lenders cannot pursue deficiency judgments on purchase-money mortgages

- Recourse states: Lenders can pursue deficiencies, though many choose not to due to cost and collection difficulty

- Anti-deficiency protections: Some states limit or prohibit deficiency judgments under certain circumstances

How to Avoid Deficiency Judgments:

- Sell before foreclosure: No foreclosure means no deficiency judgment

- Negotiate release: In short sales or deed in lieu, negotiate written release of deficiency

- Cash sale: Paying off the loan completely eliminates any deficiency

- Bankruptcy: Chapter 7 bankruptcy can discharge deficiency judgments

- Settlement: If judgment is entered, negotiate settlement for less than full amount

Best protection: Selling your property through a cash sale before foreclosure eliminates the possibility of deficiency judgment entirely.

Frequently Asked Questions About Selling After NOD

Can I sell my house after receiving a Notice of Default?

Absolutely yes. You maintain full ownership of your property until the foreclosure auction actually occurs. During the reinstatement period (typically 90-120 days after NOD), you have every legal right to sell the property.

In fact, selling during this period is often your best option because:

- You can preserve your equity

- You avoid foreclosure on your credit report

- You maintain control over the process and timeline

- You can choose your buyer and terms

The key is acting quickly. The earlier in the NOD period you list or accept an offer, the more options you have and the less pressure you face.

How long do I have to sell after receiving NOD?

The timeline varies by state, but generally you have 90-120 days from the NOD filing date until the lender can schedule a foreclosure auction.

State-specific reinstatement periods:

- California: 90 days

- Texas: Varies (typically 20 days notice before auction)

- Florida: 120 days (judicial foreclosure state)

- Arizona: 90 days

- Nevada: 115 days

Critical timeline consideration: While you technically have the full reinstatement period, practical selling timelines require you to act much sooner:

- Traditional sale: Start immediately; needs 90+ days

- Short sale: Start within first 30 days; needs 120-180 days

- Cash sale: Can start anytime; needs 7-30 days

Best practice: Treat the NOD as an emergency requiring immediate action, not a distant deadline.

Will selling affect my credit score?

Selling your property after NOD will not add additional credit damage beyond what’s already occurred from missed payments.

Credit impact breakdown:

Already occurred (before you sell):

- Missed payments: -30 to -120 points (depending on number of missed payments)

- Notice of Default filing: -50 to -100 points

If you sell before foreclosure:

- The sale itself: No additional impact

- Final credit report notation: “Paid” or “Settled” rather than “Foreclosure”

If you don’t sell and foreclosure completes:

- Additional damage: -200 to -300 points total

- Credit report notation: “Foreclosure”

- Lasting impact: Much harder to recover

Bottom line: Selling stops the bleeding. Your credit has already been damaged by the missed payments and NOD, but selling prevents the catastrophic damage of completed foreclosure.

Recovery advantage: Homeowners who sell before foreclosure typically see credit score recovery within 12-24 months, while foreclosure can suppress scores for 5-7 years.

What if I owe more than my house is worth?

Being “underwater” or “upside down” on your mortgage doesn’t prevent you from selling, but it does change your options.

Option 1: Short Sale

If you owe more than the property’s market value, a short sale allows your lender to accept less than the full payoff. The lender must approve both the sale price and the terms.

Option 2: Bring Cash to Closing

If the shortfall is small and you have savings, you can pay the difference at closing to complete the sale.

Option 3: Negotiate with Lender

Some lenders will accept a deed in lieu of foreclosure or negotiate a settlement on the deficiency.

Option 4: Explore Cash Buyers

Some investors may see value others don’t (rental potential, development opportunity, etc.) and might offer more than you expect. It’s always worth getting an evaluation.

Important: Even if you’re underwater, selling is almost always better than foreclosure. A short sale damages your credit less, may qualify you for relocation assistance, and allows you to move forward with dignity.

Can I still live in my house while trying to sell?

Yes, you should continue living in your property while it’s listed for sale or while you’re pursuing other options. You maintain full ownership and occupancy rights until the foreclosure auction occurs.

Benefits of staying:

- Property appears occupied and maintained

- You can show the property to potential buyers

- You avoid additional housing costs

- You maintain homeowner’s insurance coverage

Responsibilities while staying:

- Keep property clean and showable

- Maintain basic upkeep and repairs

- Allow reasonable access for showings

- Continue homeowner’s insurance

- Maintain utilities

When to move out:

- After closing on a sale (per the agreement terms)

- If you pursue deed in lieu (lender may require vacancy)

- After foreclosure auction (you’ll receive notice to vacate)

Never abandon the property before selling or foreclosure completion. Abandonment can lead to additional complications, vandalism, insurance issues, and potential personal liability.

Taking Action: Your Next Steps

You’ve received a Notice of Default. You understand your options. Now it’s time to act decisively to protect your financial future and move forward with confidence.

Immediate Action Checklist

Print this checklist and complete each item within the next 72 hours:

☐ Day 1 Actions:

- Read your NOD completely and note all critical dates

- Calculate your exact timeline (reinstatement deadline minus today)

- Gather all financial documents (mortgage statements, tax returns, pay stubs)

- Determine your property’s current market value (Zillow, Redfin, recent comparable sales)

- Calculate your equity position (market value minus all debts and liens)

☐ Day 2 Actions:

- Contact your lender’s loss mitigation department

- Request written reinstatement quote

- Ask about loan modification and forbearance programs

- Contact 2-3 reputable cash buyers for preliminary discussions

- Research foreclosure attorneys or HUD-approved housing counselors in your area

☐ Day 3 Actions:

- Make your decision about which path to pursue

- If selling: Contact Sure Path Property Solutions or other cash buyers

- If modifying: Submit complete loan modification application

- If listing traditionally: Interview and hire experienced agent

- Create your action timeline with specific deadlines

Making the Right Choice for Your Situation

There’s no one-size-fits-all answer to handling a Notice of Default. The right choice depends on your unique circumstances.

Choose REINSTATEMENT if:

- You have access to the full reinstatement amount

- Your financial crisis was temporary and is now resolved

- You have stable income to resume payments

- You want to keep your home long-term

Choose LOAN MODIFICATION if:

- You have some income but can’t afford current payments

- You want to keep your home

- You have time to wait for approval (60-90 days)

- You can document genuine hardship

Choose TRADITIONAL SALE if:

- You have 90+ days remaining

- Your property is in excellent condition

- Your market is very strong

- You have significant equity to preserve

- You can afford to wait for the right buyer

Choose CASH SALE if:

- You have limited time (under 90 days)

- Your property needs repairs

- You want certainty and speed

- You have liens, judgments, or title issues

- You want to avoid the stress of traditional selling

Choose SHORT SALE if:

- You’re underwater on your mortgage

- You have time for the lengthy process

- Your lender is willing to negotiate

- You want to avoid foreclosure

Choose DEED IN LIEU if:

- You’re underwater with no equity

- You’ve tried to sell without success

- You want to avoid foreclosure

- Your lender agrees to waive deficiency

How to Contact Sure Path Property Solutions

If you’re ready to explore a fast, certain cash sale solution, we’re here to provide helpful guidance and expert service.

📞 Call us: Speak directly with our friendly and caring team who understand the urgency of your situation

💻 Visit our website: Sure Path Property Solutions to learn more about our process and submit your property information

📧 Email us: Reach out with your questions and property details

🏢 Schedule a consultation: We offer no-pressure, no-obligation consultations to discuss your specific situation

What to expect when you contact us:

- Immediate response: We typically respond within 2-4 hours during business hours

- Friendly conversation: We’ll ask about your property and situation without pressure or sales tactics

- Clear explanation: We’ll explain how we can help and what the process looks like

- Fast offer: Most clients receive written cash offers within 24-48 hours

- Your timeline: We work on your schedule, closing as quickly as 7 days or accommodating longer timelines if needed

No obligations, no fees, no pressure—just honest, helpful solutions from industry experts who care about your outcome.

Resources for Additional Support

You don’t have to navigate this alone. These resources provide additional support and information:

🏛️ HUD-Approved Housing Counselors: Free, confidential advice from certified counselors

- Find counselors: www.hud.gov/findacounselor

- Services: Budget counseling, foreclosure prevention advice, option evaluation

⚖️ Legal Aid Organizations: Free or low-cost legal assistance for qualifying homeowners

- Services: Legal representation, document review, negotiation support

- Find local legal aid: www.lawhelp.org

📚 State-Specific Foreclosure Information: Understanding your state’s specific laws and timeline

- Check your state’s Attorney General website

- Review state bar association resources

💼 Financial Counseling: Credit counseling and debt management assistance

- National Foundation for Credit Counseling: www.nfcc.org

- Services: Budget planning, debt management, credit repair guidance

🏦 Lender Assistance Programs: Many major lenders offer proprietary assistance programs

- Contact your lender’s loss mitigation department directly

- Ask specifically about proprietary modification programs

Conclusion: Moving Forward with Confidence

Receiving a Notice of Default feels overwhelming, but it’s not the end of your story—it’s a critical turning point where the decisions you make today shape your financial future tomorrow.

The most important truths to remember:

✅ You still have options. The NOD is a warning, not a final judgment. You maintain control over the outcome if you act quickly.

✅ Time is precious. Every day you delay is a day lost from your already limited timeline. The homeowners who achieve the best outcomes are those who treat the NOD as an emergency requiring immediate action.

✅ Selling before foreclosure protects your future. Whether you pursue a traditional sale, short sale, or cash sale, avoiding completed foreclosure on your credit report dramatically improves your financial recovery timeline.

✅ You don’t have to navigate this alone. Professional help is available—from housing counselors to foreclosure attorneys to companies like Sure Path Property Solutions that specialize in exactly these complicated situations.

✅ There’s life after foreclosure crisis. Thousands of homeowners face NODs every year. Those who act decisively, explore all options, and make informed choices move forward to financial recovery and eventually homeownership again.

Your action plan starting today:

- Assess your timeline and options using the frameworks in this guide

- Contact professionals who can provide expert guidance specific to your situation

- Make a decision within 72 hours about which path you’ll pursue

- Take immediate action on your chosen path

- Follow through consistently until you reach resolution

If speed, certainty, and expert problem-solving are what you need, Sure Path Property Solutions stands ready to help. We’ve guided hundreds of homeowners through pre-foreclosure sales, coordinating with lenders, lienholders, and counties to create clear paths forward even in the most complicated situations.

You’ve already taken the most important step by educating yourself about your options. Now it’s time to take the next step and turn knowledge into action.

Your fresh start begins with a single decision to move forward. Make that decision today.