Sell House with Judgment Lien Fast: We Pay Off the Judgment

Imagine waking up to discover that your house—your most valuable asset—has a judgment lien attached to it. The stress hits immediately. Can you still sell? Will buyers run away? How long will this take to resolve?

Here’s the good news: you can sell your house even with a judgment lien, and with the right buyer, the process can be surprisingly fast. At Sure Path Property Solutions, we specialize in helping homeowners navigate exactly these complicated situations. We don’t just make offers on properties with judgment liens—we actually pay off the judgment as part of the transaction, clearing your path to a fresh start.

When you need to sell house with judgment lien fast: we pay off the judgment and handle the legal complexity so you don’t have to. This comprehensive guide will walk you through everything you need to know about judgment liens, how they affect property sales, and how working with expert buyers can transform what seems like an impossible situation into a straightforward solution.

Key Takeaways

- Judgment liens don’t prevent sales: You can sell your house with a judgment lien attached, though it complicates traditional sales processes

- Liens must be satisfied at closing: The judgment must typically be paid from sale proceeds before you receive any remaining equity

- Cash buyers offer speed: Companies like Sure Path Property Solutions can close in days and handle lien payoffs directly, eliminating months of uncertainty

- Multiple resolution options exist: From negotiating settlements to having buyers pay the full amount, several pathways can lead to successful sales

- Professional guidance matters: Working with industry experts who understand liens and judgments simplifies the entire process and protects your interests

Understanding Judgment Liens: The Basics

Before diving into how to sell a house with a judgment lien, it’s essential to understand exactly what you’re dealing with.

What Is a Judgment Lien?

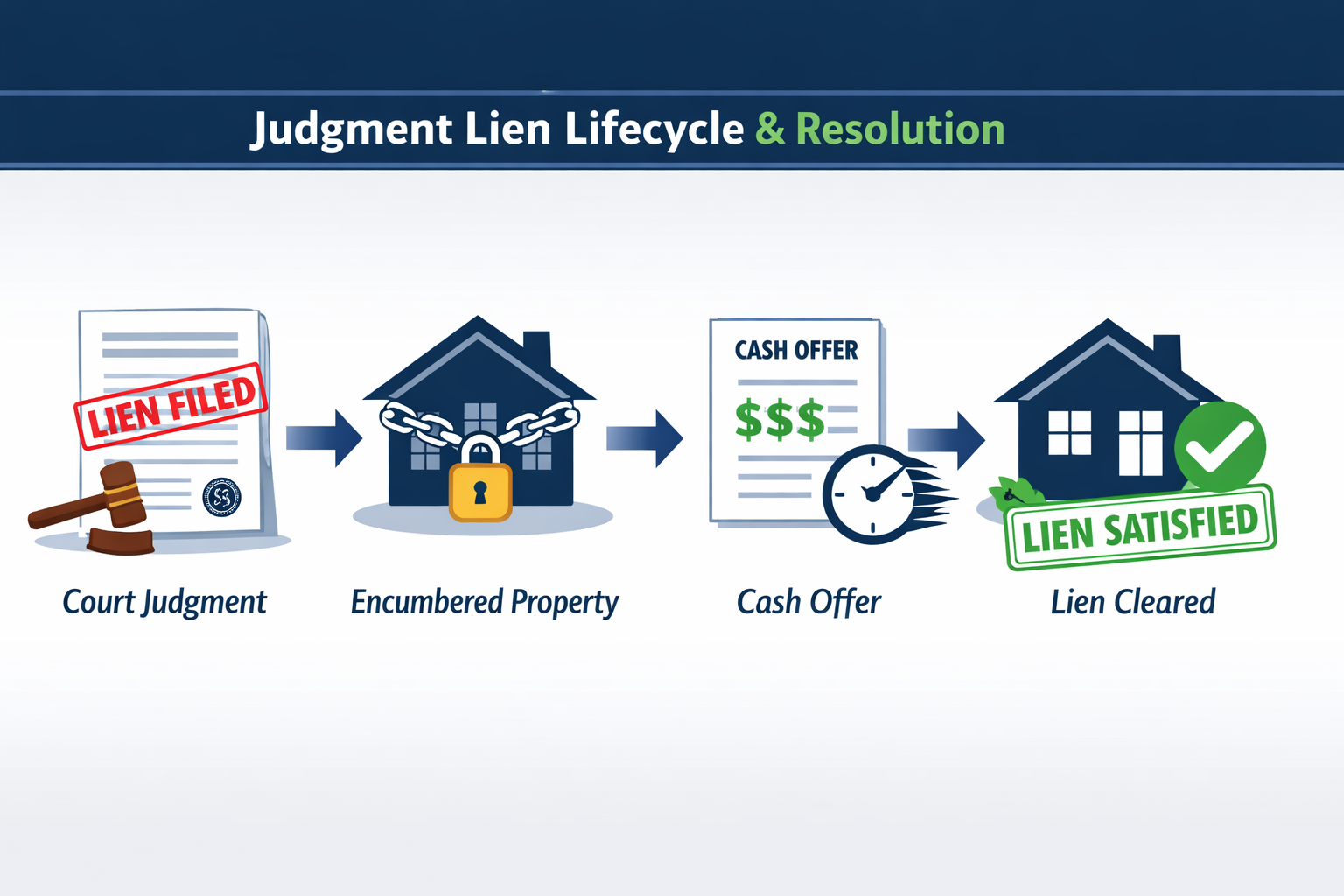

A judgment lien is a court-ordered claim against your property that results from losing a lawsuit. When someone sues you and wins a monetary judgment, they can record that judgment with your county recorder’s office, effectively attaching it to any real estate you own in that jurisdiction.

Common sources of judgment liens include:

- 💳 Credit card debt lawsuits from unpaid balances

- 🏥 Medical bills that went to collections and resulted in court judgments

- 🏢 Business debts where personal guarantees were involved

- 👥 Personal loans from individuals or private lenders

- ⚖️ Breach of contract cases with monetary damages

Once recorded, the judgment lien creates a legal claim against your property. This means the creditor has a secured interest in your home, and they’re entitled to be paid from the proceeds if you sell.

How Judgment Liens Affect Property Ownership

Judgment liens don’t mean you lose your house immediately. You retain ownership and can continue living there. However, they create several significant complications:

Financial Impact:

- The lien amount continues to accrue interest (typically at statutory rates of 5-10% annually)

- Your property equity is effectively reduced by the lien amount

- Credit scores remain damaged as long as the judgment is unsatisfied

Sale Complications:

- Title companies won’t issue clear title insurance with an outstanding judgment

- Traditional buyers typically won’t proceed with purchases on encumbered properties

- Refinancing becomes nearly impossible

- The lien must be addressed before or during any sale transaction

Legal Consequences:

- In some states, judgment creditors can force a sale through judicial foreclosure

- The creditor may be able to place additional liens on other properties you acquire

- Renewal of judgments can extend their life for many years

For detailed information about how different types of liens work, review our guide on judgment liens on property.

The Traditional Challenge of Selling with Judgment Liens

Attempting to sell a house with a judgment lien through conventional methods presents numerous obstacles:

Buyer Concerns: Most retail buyers and their lenders won’t touch properties with title issues. The moment a title search reveals a judgment lien, traditional financing becomes problematic or impossible.

Extended Timelines: Resolving judgment liens through conventional means—negotiating with creditors, obtaining releases, clearing title—can take months or even years.

Legal Complexity: Understanding lien priority, negotiating settlements, and ensuring proper releases requires legal expertise most homeowners don’t possess.

Upfront Costs: Many attorneys and title professionals require payment before they’ll even begin working on lien resolution, creating a catch-22 when you need sale proceeds to pay the judgment.

This is precisely where specialized property buyers make all the difference. When you work with companies that sell house with judgment lien fast: we pay off the judgment, these obstacles disappear.

How We Buy Houses with Judgment Liens: The Process Explained

At Sure Path Property Solutions, we’ve developed a streamlined process specifically designed to help homeowners escape the burden of judgment liens quickly and with minimal stress.

Step 1: Free Property Evaluation and Lien Assessment

The journey begins with a simple conversation. When you contact us, we’ll ask about:

- Your property details (location, size, condition)

- The judgment lien specifics (amount, creditor, age)

- Your timeline and goals

- Any other complications (additional liens, title issues, multiple owners)

No obligation. No pressure. Just helpful guidance.

We’ll conduct a preliminary title search to identify all liens and encumbrances on your property. This comprehensive review ensures we understand the complete picture before making an offer.

Step 2: Cash Offer That Accounts for the Judgment

Within 24-48 hours, we’ll present a fair cash offer for your property. This offer takes into account:

- Current market value of your property

- The judgment lien amount (including accrued interest)

- Any other liens or encumbrances

- Necessary repairs or property condition issues

- Closing costs and transaction expenses

Here’s what makes our approach different: We don’t require you to resolve the judgment before closing. We handle that as part of the transaction, paying off the judgment lien directly from the purchase funds.

Step 3: We Coordinate with All Parties

Once you accept our offer, our team takes over the heavy lifting:

✅ Title Company Coordination: We work with experienced title professionals who specialize in complicated transactions

✅ Creditor Communication: We contact the judgment creditor to obtain payoff amounts and negotiate settlements when possible

✅ Documentation Management: We handle all paperwork, lien releases, and legal requirements

✅ County Recording: We ensure proper satisfaction of judgment is filed with the county recorder

This coordination eliminates the stress and confusion that typically accompanies judgment lien sales. You don’t need to negotiate with creditors, hire attorneys, or navigate complex legal processes.

Step 4: Fast Closing with Lien Payoff Included

We can typically close in as little as 7-14 days, though we’ll work with your timeline if you need more time.

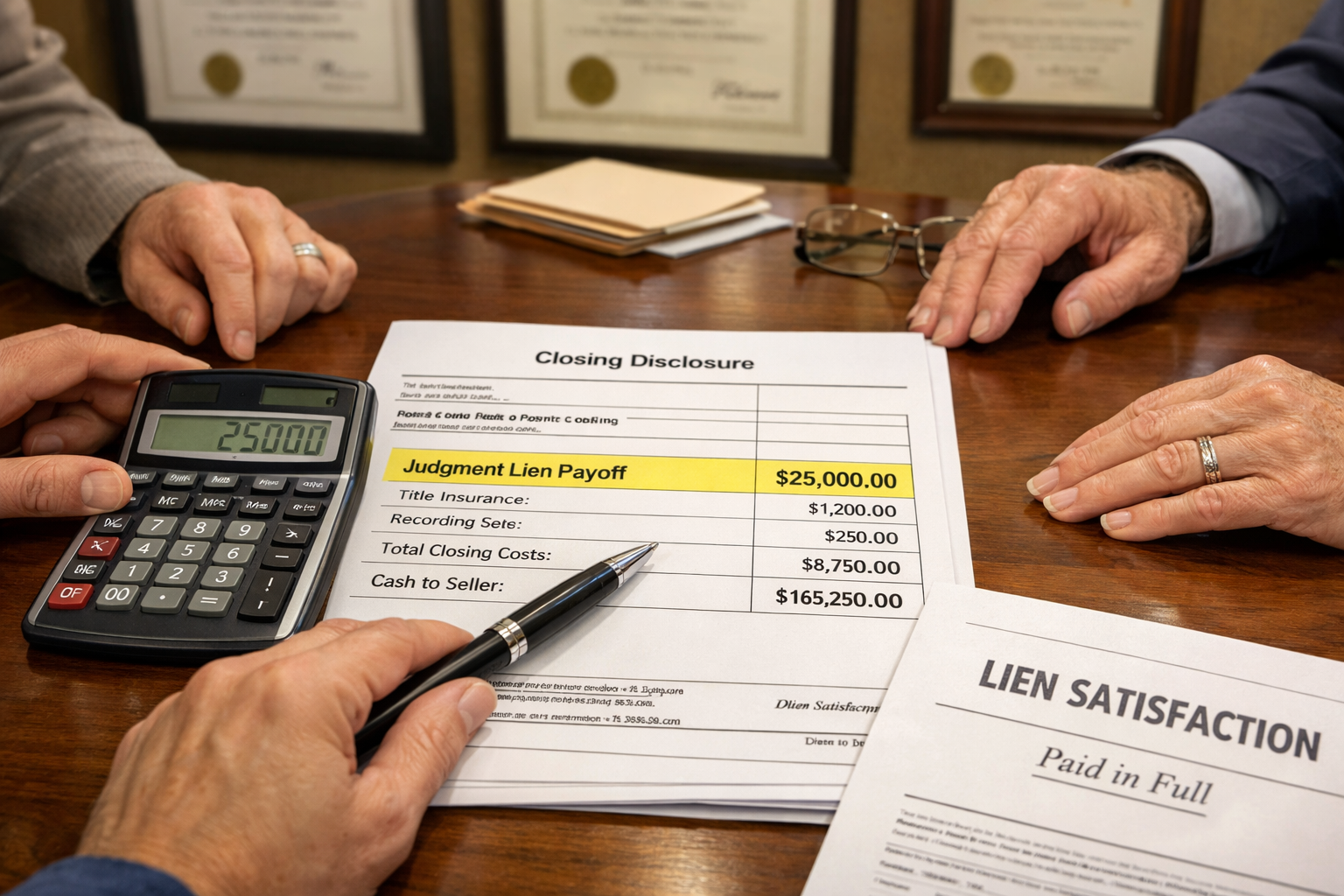

At closing, here’s what happens:

- Purchase funds are distributed according to the settlement statement

- The judgment lien is paid in full (or according to negotiated settlement)

- Lien satisfaction documents are recorded with the county

- You receive your remaining equity via check or wire transfer

- The property transfers with clear title to us

You walk away free from the judgment lien and with cash in hand. No more collection calls. No more worry about forced sales. No more damage to your credit from the unpaid judgment.

Why This Approach Works

The sell house with judgment lien fast: we pay off the judgment model works because it aligns everyone’s interests:

- You get speed and certainty: No months of uncertainty waiting for traditional buyers

- Creditors get paid: They receive their money without expensive collection efforts

- Title companies get clean transactions: All liens are satisfied, allowing them to issue clear title insurance

- We get properties: We’re able to purchase properties other buyers can’t or won’t touch

This creates a win-win-win situation that resolves complicated problems efficiently.

Options for Resolving Judgment Liens During Sale

When selling a property with a judgment lien, several resolution strategies exist. Understanding these options helps you make informed decisions about your situation.

Full Payoff from Sale Proceeds

The most straightforward approach involves paying the judgment in full from the sale proceeds.

How it works:

- The title company calculates the exact payoff amount (principal + interest + costs)

- At closing, funds are distributed to satisfy the judgment before you receive proceeds

- The creditor issues a satisfaction of judgment

- The lien is released and recorded as satisfied

Advantages:

- Clean, complete resolution

- No ongoing liability

- Creditor cooperation is usually immediate

- Simplest documentation process

Considerations:

- Reduces your net proceeds by the full judgment amount

- May not be feasible if the judgment exceeds your equity

This is the most common approach when working with cash buyers who sell house with judgment lien fast: we pay off the judgment.

Negotiated Settlement for Less Than Full Amount

In many cases, judgment creditors will accept less than the full amount owed, especially if:

- The judgment is old (several years)

- Collection efforts have been unsuccessful

- The creditor is a debt buyer who purchased the judgment at a discount

- Your property equity is limited

Typical settlement ranges: 40-70% of the original judgment amount

How negotiations work:

- We contact the creditor with a settlement proposal

- We explain the sale transaction and available funds

- We negotiate the lowest acceptable amount

- We obtain written settlement agreement

- We pay the agreed amount at closing

- The creditor releases the lien completely

Benefits of settlements:

- 💰 Saves you money by reducing the total payoff

- ⚡ Often speeds up the process as creditors want quick payment

- 📄 Results in complete lien release despite partial payment

Our team has extensive experience negotiating with judgment creditors. We understand what motivates them and how to structure offers they’ll accept. This expertise can save you thousands of dollars.

For more information about negotiating with creditors, see our article on how to satisfy a judgment lien.

Lien Subordination Agreements

In some situations, a judgment creditor might agree to subordinate their lien, meaning they accept a lower priority position. This is less common in sale transactions but can be useful when:

- You’re refinancing to pay off the judgment

- Multiple liens exist and priority needs adjustment

- The creditor believes subordination increases their likelihood of payment

When subordination makes sense:

- You have sufficient equity to pay all liens

- The first-position lienholder requires subordination

- The judgment creditor sees strategic advantage in cooperation

This is a more complex strategy that requires legal expertise, but it can provide helpful solutions in specific circumstances.

Bonding Off the Lien

Some states allow property owners to “bond off” a judgment lien by posting a surety bond equal to the judgment amount. This removes the lien from the property and transfers it to the bond.

How bonding works:

- You (or the buyer) purchase a surety bond for the judgment amount

- The bond is filed with the court

- The lien is released from the property

- The creditor can pursue the bond instead

Limitations:

- Requires creditworthiness to obtain the bond

- Involves ongoing premium costs

- Not available in all states

- Doesn’t eliminate the underlying debt

This approach is rarely used in fast sale situations but can be valuable in specific scenarios where other options aren’t feasible.

Advantages of Selling to Cash Buyers Who Handle Judgment Liens

Working with specialized buyers who understand how to sell house with judgment lien fast: we pay off the judgment offers numerous benefits compared to traditional sale methods.

⚡ Speed: Close in Days, Not Months

Traditional sale timeline with judgment lien:

- 2-4 weeks: List property, wait for buyers

- 1-2 weeks: Negotiate with interested parties

- 2-4 weeks: Buyer’s financing and inspection period

- 4-8 weeks: Negotiate with judgment creditor

- 2-4 weeks: Obtain lien releases and clear title

- Total: 3-6 months or more

Cash buyer timeline:

- 24-48 hours: Receive cash offer

- 7-14 days: Close and receive funds

- Total: Under 2 weeks

This dramatic difference in speed matters tremendously when you’re facing:

- Foreclosure proceedings

- Additional legal actions from creditors

- Financial emergencies requiring quick access to equity

- Relocation for work or family reasons

💼 No Repairs or Preparations Needed

Traditional buyers typically require:

- Professional inspections

- Repairs to address inspection findings

- Cosmetic improvements to compete with other listings

- Deep cleaning and staging

- Ongoing maintenance during listing period

Cash buyers purchase as-is, meaning:

- No inspection contingencies

- No repair negotiations

- No need to invest money you don’t have

- No ongoing utility and maintenance costs during a long sale process

This is especially valuable when the judgment lien has already strained your finances.

🤝 Expert Handling of Complex Title Issues

Judgment liens are just one type of title complication. Many properties have multiple issues:

- Tax liens (federal, state, or local)

- Mechanic’s liens from unpaid contractors

- HOA liens from unpaid assessments

- Multiple judgments from different creditors

- Divorce-related claims

- Heir property complications

Companies like Sure Path Property Solutions specialize in untangling these complex situations. We coordinate with:

- Title companies experienced in difficult transactions

- Attorneys who understand lien priority and resolution

- County recorders to ensure proper documentation

- Multiple creditors to negotiate comprehensive settlements

This expert service means you don’t need to become an expert yourself or hire expensive professionals out-of-pocket.

📊 Certainty and Transparency

Traditional sales involve numerous uncertainties:

- Will the buyer’s financing be approved?

- Will inspection issues kill the deal?

- Will the judgment creditor cooperate?

- Will title insurance be available?

Cash offers provide certainty:

- ✅ No financing contingencies

- ✅ No inspection contingencies

- ✅ Clear understanding of lien resolution process

- ✅ Guaranteed closing date

- ✅ Known net proceeds amount

You’ll receive a detailed settlement statement showing exactly how funds will be distributed, including the judgment payoff. No surprises. No last-minute complications.

🛡️ Protection from Forced Sales

If you don’t address a judgment lien proactively, the creditor may eventually force a sale through judicial foreclosure. This process:

- Typically yields lower sale prices (often 60-80% of market value)

- Involves additional legal fees and costs

- Damages credit even further

- Provides no control over timing

- May result in deficiency judgments for remaining debt

Proactive sale to a cash buyer prevents forced sale, allowing you to:

- Maximize your proceeds

- Control the timing

- Avoid additional legal complications

- Walk away with a clean slate

Common Questions About Selling Houses with Judgment Liens

Can I sell my house if there’s a judgment lien against me personally?

Yes, absolutely. Even if the judgment lien is against you personally (rather than specifically against the property), it typically attaches to any real estate you own in the county where it’s recorded.

When you sell, the lien must be addressed because:

- Title searches will reveal the judgment

- Title insurance companies won’t issue policies with outstanding judgments

- Buyers (or their lenders) won’t proceed with unclear title

The good news: selling provides the perfect opportunity to resolve the judgment. The sale proceeds pay off the lien, and you’re free from both the property and the judgment.

What if the judgment is larger than my home equity?

This is a challenging but not uncommon situation. If you owe more on your mortgage and judgment liens than your house is worth, you have several options:

Option 1: Short Sale

If your mortgage lender agrees, you can sell for less than the total debt. Both the mortgage lender and judgment creditor must agree to accept less than full payment. Learn more about how short sales work.

Option 2: Negotiated Settlements

Judgment creditors often accept significant discounts (50-70% off) when they understand the alternative is receiving nothing if the property goes to foreclosure.

Option 3: Strategic Negotiation

Experienced buyers can sometimes negotiate with all parties to structure a deal that works for everyone, even with negative equity.

Option 4: Walk Away Strategically

In some cases, allowing foreclosure while negotiating separate judgment settlement may be the most practical path.

We evaluate each situation individually to identify the best strategy for your specific circumstances.

How long does the judgment lien sale process take?

With cash buyers: 7-14 days from accepted offer to closing

Traditional sale: 3-6 months or more

The difference comes down to:

- No financing contingencies (eliminates 30-45 days)

- No inspection periods (eliminates 10-14 days)

- Experienced lien resolution (eliminates months of negotiation)

- Direct creditor coordination (eliminates communication delays)

If you need to close faster or slower based on your circumstances, most cash buyers can accommodate your timeline.

Will I owe taxes on the judgment lien payoff?

Generally, no. When a judgment lien is paid as part of a property sale, it’s treated as a debt payoff, not taxable income.

However, tax situations vary based on:

- Whether the judgment was related to business or personal debt

- Your overall financial situation

- State-specific tax laws

Consult with a tax professional about your specific situation. The peace of mind is worth the consultation fee.

Can the judgment creditor stop me from selling?

No. Judgment creditors cannot prevent you from selling your property. However, they have rights:

What they CAN do:

- Require their lien be paid from sale proceeds

- Refuse to release the lien without payment

- Object to settlements they consider inadequate

- In some states, force a sale through judicial foreclosure

What they CANNOT do:

- Prevent you from selling to a willing buyer

- Take possession of your property (without court-ordered foreclosure)

- Demand payment before you’ve sold (though they can pursue other collection methods)

When you work with experienced buyers who sell house with judgment lien fast: we pay off the judgment, they handle creditor negotiations professionally, ensuring all parties’ rights are respected while moving the transaction forward efficiently.

What if there are multiple judgment liens?

Multiple judgments are common and don’t prevent sales—they just require more coordination.

How multiple liens are handled:

- Title search identifies all liens and their priority

- Payoff amounts are obtained from each creditor

- Negotiations occur simultaneously with all creditors

- Settlement statement allocates funds according to lien priority

- All liens are satisfied at closing

Lien priority matters: Generally, liens are paid in the order they were recorded. First recorded = first paid. However, certain liens (like IRS tax liens) have super-priority status.

Our team has extensive experience managing multiple-lien situations. We coordinate with all parties to ensure everyone is paid appropriately and all releases are obtained. For more details about lien priority, read our guide on priority of tax liens.

Real-World Example: How We Helped Sarah Sell Her House with a Judgment Lien

The Situation:

Sarah inherited her mother’s house in 2023, but she also inherited significant credit card debt that resulted in a $45,000 judgment lien against her personally. The judgment automatically attached to the inherited property.

The Complications:

- The house needed $30,000 in repairs

- Sarah lived out of state and couldn’t manage renovations

- She had already missed several months of property tax payments

- Traditional buyers wouldn’t touch the property due to the judgment lien

- The judgment was accruing interest at 8% annually ($3,600/year)

The Traditional Path Would Have Required:

- Hiring an attorney ($3,000-5,000)

- Negotiating with the judgment creditor (2-3 months)

- Making property repairs ($30,000)

- Listing with a realtor (3-6 months to sell)

- Paying realtor commissions (6% of sale price)

- Total timeline: 6-12 months

- Total upfront costs: $33,000-35,000 Sarah didn’t have

Our Solution:

- Day 1: Sarah contacted Sure Path Property Solutions

- Day 2: We conducted a title search and property evaluation

- Day 3: We presented a cash offer of $185,000 (accounting for repairs needed and lien payoff)

- Days 4-7: We negotiated with the judgment creditor, settling for $31,500 (30% discount)

- Day 12: We closed on the property

The Results:

- ✅ Judgment lien paid and satisfied: $31,500

- ✅ Property taxes brought current: $4,200

- ✅ Closing costs covered: $2,800

- ✅ Sarah’s net proceeds: $146,500

- ✅ Total timeline: 12 days

- ✅ Sarah’s out-of-pocket costs: $0

Sarah’s Testimonial:

“I was overwhelmed and didn’t know where to start. Sure Path made everything simple. They handled the judgment creditor, paid off the lien, and I walked away with money in my pocket. I couldn’t have asked for a better experience.”

This is exactly the kind of helpful solution we provide every day. When you need to sell house with judgment lien fast: we pay off the judgment, we make the complex simple.

Alternative Options: When Cash Sale Might Not Be Best

While selling to a cash buyer who handles judgment liens offers tremendous advantages, it’s important to consider all options. Here are alternatives that might work better in specific situations:

Fighting the Judgment in Court

If you believe the judgment was:

- Obtained improperly

- Based on incorrect information

- Beyond the statute of limitations

- Already paid but not properly released

You might consider appealing or challenging the judgment. This requires:

Pros:

- Potential to eliminate the lien entirely

- No payment required if successful

- Vindication if you were wronged

Cons:

- Expensive legal fees ($5,000-15,000+)

- Time-consuming (6-18 months)

- Uncertain outcome

- Judgment continues accruing interest during appeal

Best for: Situations where you have strong legal grounds and the judgment amount is substantial enough to justify legal costs.

Bankruptcy

Filing Chapter 7 or Chapter 13 bankruptcy can discharge certain judgment debts and eliminate associated liens.

Pros:

- May eliminate the judgment debt entirely

- Stops collection actions immediately

- Provides fresh financial start

Cons:

- Severely damages credit (7-10 years)

- Costs $1,500-3,500 in legal fees

- Not all judgments are dischargeable

- May still require property sale

- Involves complex legal process

Best for: Situations with overwhelming debt beyond just the judgment lien, where comprehensive debt relief is needed.

Paying Off the Judgment Before Selling

If you have access to funds from other sources, you could pay off the judgment before listing the property traditionally.

Pros:

- Clears title for traditional sale

- May allow higher sale price

- Eliminates lien interest accrual

Cons:

- Requires significant upfront cash

- No guarantee of successful sale afterward

- Property must be in good condition

- Still involves 3-6 month traditional sale timeline

Best for: Situations where you have available cash, your property is in excellent condition, and you’re not facing time pressure.

Keeping the Property and Paying Over Time

If you want to keep the property, you might negotiate a payment plan with the judgment creditor.

Pros:

- Retain property ownership

- Spread payments over time

- May negotiate reduced total amount

Cons:

- Lien remains until fully paid

- Ongoing monthly payment obligation

- Continued credit impact

- Property can’t be sold or refinanced easily

Best for: Situations where you want to keep the property long-term and have stable income to make payments.

Why Sure Path Property Solutions Is Your Best Choice

When you’re ready to sell house with judgment lien fast: we pay off the judgment, choosing the right buyer makes all the difference. Here’s why homeowners across the region trust Sure Path Property Solutions:

🎯 Specialized Expertise in Complex Properties

We don’t just buy houses—we specialize in complicated situations that traditional buyers can’t handle:

- Judgment liens and legal judgments

- Tax liens and back taxes

- Multiple heirs and inheritance issues

- Title problems and clouded titles

- Properties in pre-foreclosure

- Houses with code violations

This specialization means we’ve seen it all and know how to resolve virtually any complication.

💰 Fair, Transparent Offers

We provide detailed written offers that clearly show:

- Property valuation methodology

- Lien payoff calculations

- Estimated closing costs

- Your net proceeds

No hidden fees. No surprises. Just honest, trustworthy service.

🤝 Friendly, Caring Approach

Dealing with judgment liens is stressful. We understand you’re going through a difficult time, and we treat you with:

- Respect and dignity

- Patience and understanding

- Clear communication

- Helpful guidance throughout the process

We’re not just buying your property—we’re helping you solve a problem and move forward with your life.

⚡ Proven Track Record

We’ve successfully helped hundreds of homeowners resolve judgment liens and other property complications. Our industry experts have:

- Decades of combined real estate experience

- Established relationships with title companies and attorneys

- Deep knowledge of local laws and procedures

- Proven negotiation skills with creditors

This experience translates directly into better outcomes for you.

🏆 No-Obligation Consultation

Not sure if selling is right for you? We offer free consultations to:

- Evaluate your situation

- Explain your options

- Answer your questions

- Provide helpful guidance—even if you don’t sell to us

There’s no pressure, no obligation, and no cost. Just expert advice when you need it most.

Taking the Next Step: How to Get Started

If you’re ready to explore how to sell house with judgment lien fast: we pay off the judgment, getting started is simple.

Step 1: Contact Us

Reach out through any of these methods:

- 📞 Phone: Call us directly for immediate assistance

- 💻 Website: Fill out the simple form on our contact page

- 📧 Email: Send us your information and we’ll respond within 24 hours

Step 2: Share Your Situation

During our initial conversation, we’ll ask about:

- Your property location and basic details

- The judgment lien specifics

- Your timeline and goals

- Any other complications or concerns

This information helps us provide the most accurate evaluation and helpful solutions.

Step 3: Receive Your Cash Offer

Within 24-48 hours, we’ll present a fair cash offer that accounts for:

- Current market conditions

- Property condition

- Judgment lien amount

- Other liens or encumbrances

- Closing costs

The offer will clearly show your estimated net proceeds after all liens are satisfied.

Step 4: Accept and Close

If you accept our offer:

- We’ll open escrow with a reputable title company

- Our team will coordinate all lien payoffs and releases

- You’ll review and sign closing documents

- We’ll close in as little as 7-14 days (or on your timeline)

- You’ll receive your funds and walk away free from the judgment lien

It’s that straightforward. No complications. No stress. Just helpful solutions from industry experts who care about your situation.

Frequently Asked Questions About Our Process

Do I need to hire an attorney?

No. We handle all aspects of the transaction, including lien resolution. However, you’re always welcome to have an attorney review documents if that provides peace of mind.

What if I’m behind on mortgage payments too?

We can help with that as well. We frequently work with homeowners facing both judgment liens and mortgage default. We can coordinate with your lender to bring payments current or negotiate payoffs. Learn more about selling houses in pre-foreclosure.

Can you help if the judgment is from the IRS or state taxes?

Yes. Tax liens require special handling, but we have extensive experience resolving them. Tax liens often have super-priority status, but they can still be negotiated and satisfied through property sales. See our guide on selling property with tax debt.

What if the property is in another state?

We work with properties in multiple states and have established networks of title professionals and attorneys nationwide. Distance doesn’t prevent us from helping you.

Will this affect my credit?

Satisfying a judgment lien through property sale actually helps your credit by:

- Showing the judgment as “satisfied” rather than “outstanding”

- Stopping ongoing interest accrual

- Eliminating collection actions

- Demonstrating debt resolution

While the judgment will remain on your credit report for the statutory period (typically 7 years from the judgment date), showing it as satisfied is significantly better than leaving it unpaid.

Can I sell if there’s also a divorce involved?

Yes. We frequently help with properties involved in divorce proceedings. We can work with both spouses, their attorneys, and the court to facilitate sales that satisfy all parties and resolve judgment liens. Check out our article on selling jointly owned property.

Understanding Your Rights as a Property Owner with a Judgment Lien

Knowledge is power. Understanding your rights helps you make informed decisions about your property.

You Have the Right to Sell

Judgment creditors cannot prevent you from selling your property. You maintain full ownership rights, including:

- The right to list and market the property

- The right to accept offers from buyers

- The right to negotiate terms

- The right to choose your closing date

The creditor’s right is limited to having their lien paid from the proceeds. They cannot block the sale itself.

You Can Negotiate with Creditors

Judgment creditors are often willing to negotiate because:

- Collection is expensive and time-consuming

- They may have purchased the judgment at a discount

- Receiving partial payment is better than continued collection efforts

- They want to avoid the costs of forced sale proceedings

Don’t assume you must pay the full amount. Professional negotiation often yields significant savings.

You’re Protected by Consumer Protection Laws

Various federal and state laws protect you from:

- Harassment by judgment creditors

- Fraudulent or deceptive collection practices

- Improper lien recording procedures

- Violations of due process

If a creditor has violated your rights, you may have grounds to challenge the judgment or lien.

You Can Choose Your Timeline (Within Reason)

While judgment creditors want payment, you generally control when you sell. However, be aware:

- Judgments accrue interest over time

- Creditors may eventually pursue forced sale

- Additional legal actions may complicate your situation

- Property values may fluctuate

Acting sooner rather than later typically provides better outcomes and more control over the process.

The Emotional Side: Moving Past Financial Stress

Dealing with judgment liens isn’t just a financial challenge—it’s emotionally draining. The constant worry, embarrassment, and stress take a real toll on your wellbeing and relationships.

You’re Not Alone

Millions of Americans face judgment liens every year. Common causes include:

- Medical emergencies and unexpected health costs

- Business failures during economic downturns

- Divorce and family disruptions

- Job loss and income reduction

- Simple financial mismanagement during difficult times

This doesn’t define you. It’s a temporary situation that can be resolved.

There’s No Shame in Seeking Help

Asking for help is a sign of strength, not weakness. Working with professionals who understand your situation provides:

- Relief from constant stress

- Expert guidance through complex processes

- Protection from making costly mistakes

- A clear path forward

At Sure Path Property Solutions, we’ve helped hundreds of people in similar situations. We understand the emotional weight you’re carrying, and we’re here to help lift it.

A Fresh Start Is Possible

Selling your property and resolving the judgment lien provides:

- ✅ Freedom from collection calls and legal threats

- ✅ A clean slate to rebuild your financial life

- ✅ Peace of mind knowing the issue is resolved

- ✅ Cash proceeds to start your next chapter

- ✅ Improved credit as the judgment shows satisfied

Many of our clients describe the closing day as feeling like a massive weight has been lifted from their shoulders. That relief is available to you too.

Conclusion: Your Path to Freedom from Judgment Liens

A judgment lien on your property doesn’t have to control your life. While it creates complications, it’s not an insurmountable obstacle. With the right approach and the right partner, you can resolve the lien quickly and move forward with confidence.

The key points to remember:

- Judgment liens can be resolved through property sales – You don’t need to fight the judgment in court or declare bankruptcy to move forward

- Cash buyers provide the fastest path – When you sell house with judgment lien fast: we pay off the judgment, you eliminate months of uncertainty and stress

- Professional negotiation saves money – Experienced buyers can often negotiate significant discounts on judgment amounts

- You maintain control – You choose whether to sell, when to sell, and which offer to accept

- A fresh start is within reach – Resolving the judgment through sale provides both financial relief and emotional peace

At Sure Path Property Solutions, we specialize in turning complicated situations into straightforward solutions. Our team of industry experts provides:

- Helpful solutions tailored to your specific situation

- Trustworthy service with transparent, fair offers

- Helpful guidance throughout the entire process

- Friendly and caring support when you need it most

- Expert service backed by years of experience

We understand that dealing with judgment liens is stressful and overwhelming. That’s why we’ve designed our process to be as simple and supportive as possible. We handle the complexity so you don’t have to.

Take Action Today

Every day you wait, the judgment continues accruing interest and the stress continues mounting. But you can take control right now.

Your next steps:

- Contact us for a free, no-obligation consultation

- Share your situation so we can evaluate your options

- Receive a fair cash offer within 24-48 hours

- Close quickly and walk away free from the judgment lien

Don’t let a judgment lien hold you hostage any longer. Whether you’re facing foreclosure, dealing with multiple liens, or simply want to move on with your life, we’re here to help.

Visit our contact page or call us today to start your journey toward freedom from judgment liens. Our friendly team is ready to provide the helpful guidance and expert service you deserve.

Remember: You have options. You have rights. And you have a partner ready to help. Let’s work together to resolve your judgment lien and open the door to your fresh start.

The path forward is clearer than you think. Take the first step today.