Selling a House with a Lien in Florida: Laws, Process & Timeline

Discovering a lien on your Florida property when you’re ready to sell can feel like hitting a brick wall. The dream of moving forward suddenly becomes tangled in legal paperwork, county offices, and questions about whether you can even complete the sale. But here’s the good news: selling a house with a lien in Florida is absolutely possible, and thousands of property owners successfully navigate this process every year.

Understanding the laws, process, and timeline for selling a house with a lien in Florida doesn’t have to be overwhelming. With the right guidance and a clear roadmap, you can move from discovery to closing—even when liens complicate your title. Whether you’re dealing with tax liens, judgment liens, or contractor claims, Florida law provides specific pathways to resolution that protect both sellers and buyers.

This comprehensive guide walks through everything you need to know about selling a house with a lien in Florida: laws, process, and timeline. From identifying different lien types to understanding your legal obligations, negotiating payoffs, and closing successfully, you’ll gain the expert knowledge needed to move forward with confidence.

Key Takeaways

- Liens don’t prevent sales: You can sell a Florida property with liens attached, but they must typically be satisfied at or before closing from the sale proceeds

- Florida lien priority matters: The order in which liens are paid follows strict legal hierarchy, with property tax liens and first mortgages usually taking precedence

- Timeline varies significantly: Selling with liens can take 60-120 days depending on lien type, complexity, and cooperation from lien holders

- Title companies are essential: Professional title work uncovers all liens and coordinates the payoff process to ensure clear title transfer

- Multiple resolution options exist: Beyond paying liens at closing, Florida sellers may negotiate settlements, dispute invalid liens, or work with specialized buyers

Understanding Property Liens in Florida 🏠

A property lien represents a legal claim against your real estate, giving creditors security interest in your home until you satisfy a debt. Think of it as a financial anchor attached to your property—it follows the property, not just the owner, which means it must be addressed before transferring clear title to a new buyer.

In Florida, liens are public records filed with the county where your property is located. This public nature serves an important purpose: it notifies potential buyers, lenders, and other interested parties about existing claims against the property.

How Liens Attach to Florida Real Estate

Florida law allows various creditors to secure their claims by placing liens on real property. Once properly recorded, these liens create what’s called “encumbrances” on your title. The property essentially becomes collateral for the debt, regardless of who owns it.

The attachment process typically involves:

- Filing official documentation with the county clerk’s office

- Recording the lien in public records with legal description of the property

- Serving notice to the property owner (requirements vary by lien type)

- Creating a cloud on the title that appears in title searches

This system protects creditors while providing transparency for property transactions. When you’re ready to sell, any title search will reveal these recorded liens, making them impossible to ignore or transfer unknowingly.

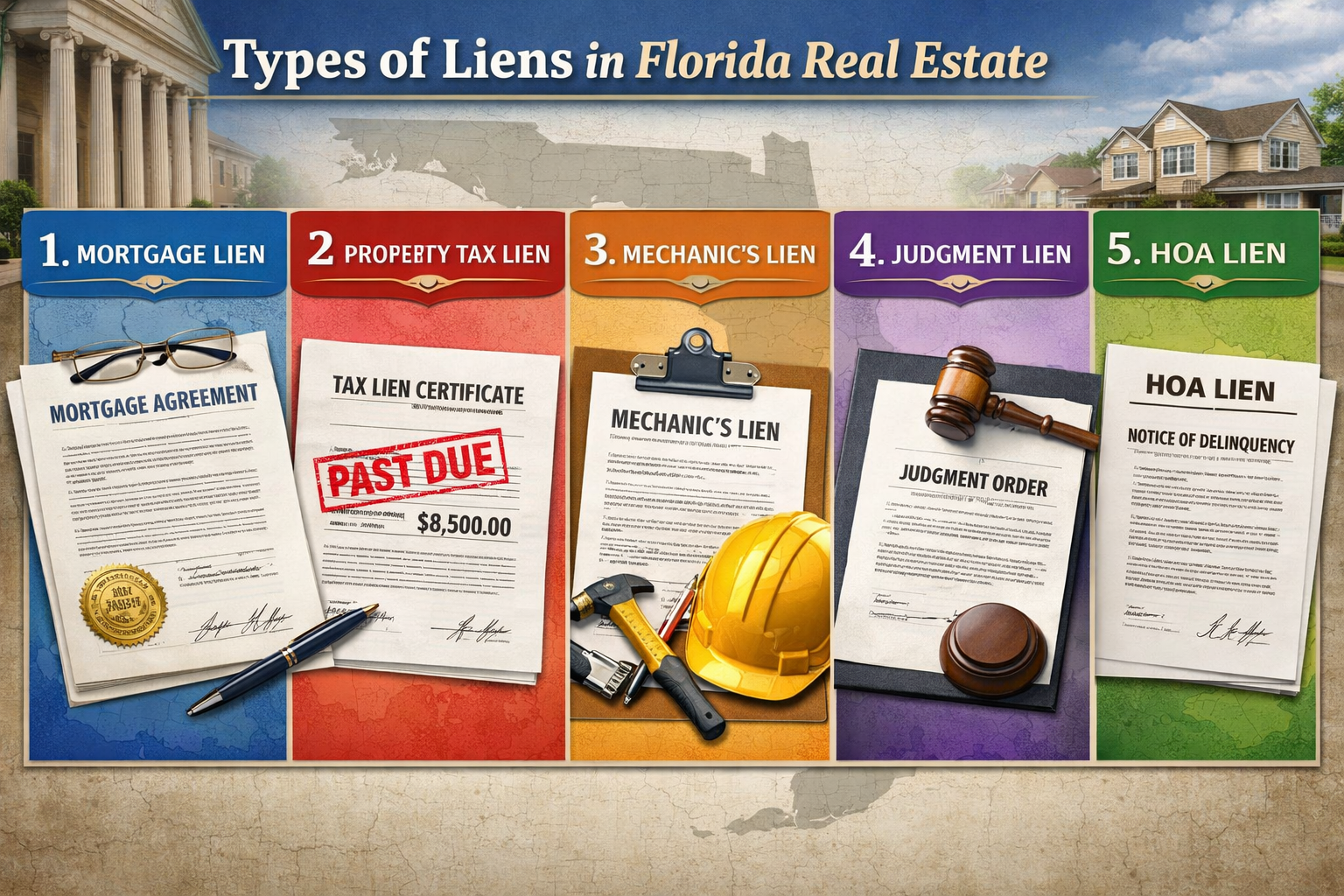

Common Types of Liens on Florida Properties

Not all liens are created equal. Florida recognizes several distinct categories, each with different rules, priorities, and resolution processes. Understanding which type affects your property is the first step toward resolving lien issues.

Property Tax Liens ⚖️

These arise when property owners fall behind on county or municipal taxes. In Florida, property tax liens take priority over almost all other claims, including mortgages. Counties can eventually foreclose on tax liens, making them particularly serious.

Tax liens accrue interest and penalties that compound over time. Florida counties typically offer payment plans and may negotiate settlements, especially when a sale is imminent.

Mortgage Liens

Your primary mortgage and any second mortgages or home equity lines of credit create voluntary liens. You agreed to these when borrowing money to purchase or refinance your property. These must be paid when selling, with proceeds from the sale.

Mechanic’s Liens

Contractors, subcontractors, and suppliers can file mechanic’s liens when they perform work or provide materials but don’t receive payment. Florida’s mechanic’s lien law (Chapter 713, Florida Statutes) gives these creditors powerful rights, but strict deadlines and notice requirements apply.

These liens can be particularly surprising to homeowners who hired a general contractor, paid them, but find out the contractor didn’t pay their subcontractors.

Judgment Liens

When someone wins a lawsuit against you and obtains a monetary judgment, they can record it as a lien against your Florida real estate. These judgment liens remain attached to your property until satisfied or the judgment expires.

Florida law allows judgment liens to last up to 20 years with proper renewal, making them long-term obstacles to clear title.

HOA and Condo Association Liens

Homeowners associations and condominium associations can place liens for unpaid assessments, fees, or fines. Florida’s HOA laws give these liens significant power, including the potential for foreclosure in some circumstances.

IRS and Federal Tax Liens

Federal tax liens arise from unpaid income taxes or other federal debts. These liens attach to all your property in Florida and can be particularly complex to resolve, requiring coordination with IRS representatives.

Florida Laws Governing Selling a House with a Lien: Legal Framework 📜

Florida’s legal framework for selling property with liens balances creditor protection with property owners’ rights to transfer real estate. Understanding these laws helps sellers navigate the process confidently and avoid legal pitfalls.

Florida Statutes on Lien Priority and Enforcement

Florida law establishes a clear hierarchy for lien priority, determining which creditors get paid first when property sells or faces foreclosure. This “first in time, first in right” principle has important exceptions.

The typical priority order in Florida:

- Property tax liens (always first, regardless of recording date)

- Special assessment liens for municipal improvements

- First mortgage liens (recorded first mortgages)

- Second mortgages and HELOCs (in order of recording)

- Judgment liens (by recording date)

- Mechanic’s liens (with special rules dating back to project commencement)

- HOA/Condo liens (limited priority under Florida law)

This hierarchy matters tremendously when sale proceeds aren’t sufficient to pay all liens—a situation called being “underwater” or having negative equity.

Disclosure Requirements for Florida Sellers

Florida law imposes specific disclosure obligations on property sellers. While you’re not required to conduct a title search yourself before listing, you must disclose known liens and encumbrances to potential buyers.

The standard Florida residential purchase contract includes provisions for the seller to deliver “marketable title”—meaning title free from liens except those specifically agreed upon. Failing to disclose known liens can result in:

- Contract cancellation by the buyer

- Legal liability for fraud or misrepresentation

- Delayed closings and additional costs

- Potential lawsuits after closing

Best practice: Work with a title company early in the process to identify all liens, then disclose them transparently to buyers and real estate agents.

Seller’s Legal Obligations When Liens Exist

When selling a Florida property with liens, sellers have several legal responsibilities:

Providing Clear Title at Closing

Unless the buyer specifically agrees to take the property “subject to” certain liens, sellers must deliver clear, marketable title. This typically means paying off all liens from the sale proceeds at closing.

Accurate Lien Payoff Information

Sellers must obtain current payoff amounts from lien holders, including per-diem interest calculations. Outdated payoff figures can cause closing delays or shortfalls.

Cooperation with Title Company

The title company coordinates lien payoffs and ensures proper releases are recorded. Sellers must provide necessary documentation, signatures, and information to facilitate this process.

Handling Insufficient Proceeds

If sale proceeds won’t cover all liens, sellers must either bring money to closing, negotiate with lien holders for reduced payoffs, or pursue a short sale with lender approval.

Buyer Protections Under Florida Law

Florida law also protects buyers from unknowingly purchasing property with undisclosed liens. Title insurance, required by most lenders, provides financial protection if liens appear after closing that weren’t properly handled.

Buyers can also:

- Conduct independent title searches before closing

- Include contingencies in the purchase contract requiring clear title

- Delay closing until sellers resolve lien issues

- Cancel contracts if sellers can’t deliver marketable title

This balanced legal framework means both parties have rights and responsibilities when selling a house with liens.

The Complete Process for Selling a House with a Lien in Florida 🔄

Successfully selling a Florida property with liens requires a methodical approach. Following these steps helps ensure a smooth transaction and timely closing.

Step 1: Conduct a Comprehensive Title Search

Before listing your property, order a professional title search. This reveals all recorded liens, judgments, and encumbrances affecting your property. Many sellers are surprised to discover liens they didn’t know existed—old judgments, contractor claims, or tax issues from previous owners.

What a title search uncovers:

- All recorded mortgages and home equity loans

- Property tax liens and special assessments

- Judgment liens from lawsuits

- Mechanic’s liens from unpaid contractors

- HOA/condo association liens

- Federal tax liens

- Easements and restrictions

Title companies typically complete searches within 3-7 business days. The cost ranges from $150-$400 depending on property complexity and county.

Step 2: Identify and Verify All Liens

Once you have the title search results, verify each lien’s validity and current balance. This critical step prevents paying incorrect amounts or addressing liens that may have expired or been satisfied without proper release.

Verification checklist:

- Contact each lien holder for current payoff amounts

- Request per-diem interest calculations

- Confirm the lien applies to your specific property (legal description match)

- Check statute of limitations for older liens

- Verify proper recording and notice procedures were followed

Some liens may be invalid due to procedural errors, expired deadlines, or incorrect property descriptions. Disputing invalid liens requires legal assistance but can save thousands of dollars.

Step 3: Calculate Total Lien Obligations

Add up all valid liens to determine your total obligation. Include:

- Principal amounts owed

- Accrued interest to anticipated closing date

- Penalties and late fees

- Recording fees for lien releases

- Any negotiated settlement amounts

Compare this total to your expected sale price minus selling costs (agent commissions, closing costs, title insurance, etc.). This calculation reveals whether you’ll have positive equity, break even, or face a shortfall.

Step 4: Develop a Lien Resolution Strategy

Based on your financial position, choose the appropriate resolution strategy:

Scenario A: Sufficient Equity

If sale proceeds will cover all liens and selling costs with money left over, the process is straightforward. Liens are paid at closing through the title company, and you receive the remaining proceeds.

Scenario B: Breaking Even

When proceeds approximately equal liens and costs, careful calculation and timing are essential. You may need to bring a small amount to closing or negotiate minor reductions with lien holders.

Scenario C: Negative Equity (Underwater)

If you owe more than the property’s worth, you’ll need to either:

- Bring cash to closing to cover the shortfall

- Negotiate short sales with lien holders (especially mortgages)

- Work with lien holders to accept reduced payoffs

- Consider alternative solutions with specialized property buyers

Step 5: Negotiate with Lien Holders

Many lien holders will negotiate, especially when the alternative is receiving nothing through foreclosure or waiting years for payment. Approach negotiations strategically:

Effective negotiation tactics:

- Present clear financial documentation showing limited proceeds

- Emphasize the benefit of immediate payment versus uncertain future collection

- Obtain multiple payoff quotes and settlement offers

- Work with experienced professionals who understand lien negotiation

- Get all settlement agreements in writing before closing

Second mortgage holders, judgment creditors, and some tax authorities often accept 40-70% of the owed amount when faced with junior lien positions that might receive nothing in foreclosure.

Step 6: List and Market the Property

Once you understand your lien situation and resolution strategy, you can confidently list the property. Transparency with your real estate agent is crucial—they need to know about liens to set appropriate expectations with buyers and structure offers correctly.

Marketing considerations:

- Price competitively considering lien payoff requirements

- Disclose lien situation to serious buyers early

- Consider cash buyers or investors familiar with lien situations

- Allow extra time in closing timeline for lien resolution

- Include appropriate contingencies in purchase contracts

Properties with lien complications often attract investors and specialized buyers who understand the process and can close quickly.

Step 7: Coordinate Closing and Lien Payoffs

The title company plays a central role in coordinating lien payoffs at closing. They:

- Obtain final payoff statements from all lien holders

- Calculate exact amounts due including per-diem interest

- Prepare closing statements showing all debits and credits

- Disburse funds to lien holders on closing day

- Obtain lien releases and record them with the county

- Ensure the buyer receives clear title and title insurance

Typical closing timeline with liens:

- 7-10 days before closing: Final payoff statements ordered

- 3-5 days before closing: Closing disclosure prepared and delivered

- Closing day: Funds disbursed, liens paid, deed recorded

- 1-3 days after closing: Lien releases recorded

- 7-14 days after closing: Final title policy issued

Step 8: Confirm Lien Releases Are Recorded

After closing, verify that all lien releases are properly recorded with the county. While the title company handles this, confirming completion protects you from future claims.

Request copies of recorded releases showing:

- Official county recording stamps with date and document number

- Proper legal description of your property

- Lien holder signatures and notarization

- Reference to the original lien being released

Keep these documents permanently in your records. They prove the liens were satisfied and released, protecting you if questions arise years later.

Timeline for Selling a House with a Lien in Florida ⏰

Understanding realistic timeframes helps you plan effectively and set appropriate expectations. The timeline for selling a house with a lien in Florida varies significantly based on lien complexity and your specific situation.

Typical Timeline Breakdown

Week 1-2: Discovery and Assessment Phase

- Order and receive title search: 3-7 days

- Review results and identify all liens: 1-2 days

- Contact lien holders for payoff information: 3-5 days

- Assess financial position and resolution options: 2-3 days

Week 3-4: Strategy Development and Negotiation

- Develop lien resolution strategy: 2-3 days

- Begin negotiations with lien holders: 1-2 weeks

- Obtain settlement agreements in writing: 3-7 days

- Consult with real estate professionals: ongoing

Week 5-8: Marketing and Offer Phase

- List property for sale: 1 day

- Market to potential buyers: 2-6 weeks (varies by market)

- Receive and negotiate offers: 3-7 days

- Execute purchase contract: 1-2 days

Week 9-12: Contract to Closing

- Buyer’s inspection period: 7-14 days

- Buyer’s financing approval: 21-30 days

- Final lien payoff coordination: 7-10 days

- Closing preparation and execution: 3-5 days

- Post-closing lien release recording: 7-14 days

Total estimated timeline: 60-90 days for straightforward situations with cooperative lien holders and standard market conditions.

Factors That Extend the Timeline

Several circumstances can significantly lengthen the process:

Complex Lien Situations 🕐

- Multiple judgment liens requiring separate negotiations: +2-4 weeks

- Disputed or invalid liens requiring legal action: +4-12 weeks

- Federal tax liens requiring IRS coordination: +4-8 weeks

- Mechanic’s liens with multiple claimants: +3-6 weeks

Negotiation Challenges

- Uncooperative lien holders: +2-6 weeks

- Short sale approval requirements: +8-16 weeks

- Bankruptcy involvement: +12-24 weeks

- Foreclosure proceedings already initiated: +4-12 weeks

Market Conditions

- Slow market with limited buyer activity: +4-12 weeks

- Property condition issues reducing buyer pool: +3-8 weeks

- Pricing challenges due to lien amounts: +2-6 weeks

Title and Legal Issues

- Clouded title requiring quiet title action: +12-24 weeks

- Missing lien holder requiring legal process: +8-16 weeks

- Chain of title breaks needing correction: +6-12 weeks

Expediting the Process

When time is critical, several strategies can accelerate the timeline:

Work with Cash Buyers 💰

Cash buyers eliminate the 21-30 day financing period and often accept properties in as-is condition. Companies specializing in properties with title issues can close in 14-21 days.

Obtain Payoff Quotes Early

Request payoff statements immediately upon discovering liens. Most lien holders provide quotes valid for 30-60 days, giving you working numbers for negotiations.

Hire Experienced Professionals

Real estate attorneys and title companies experienced with lien resolution navigate challenges more efficiently than those handling their first complex case.

Consider Simultaneous Negotiations

Rather than addressing liens sequentially, negotiate with multiple lien holders simultaneously to compress the timeline.

Price Competitively

Properties priced at or slightly below market value attract more buyers quickly, reducing the marketing phase significantly.

Selling Options When You Have Liens in Florida 🎯

Property owners facing lien complications have several viable paths forward. Choosing the right option depends on your equity position, timeline, and financial goals.

Traditional Sale Through Real Estate Agent

This conventional approach works well when you have sufficient equity to pay all liens and selling costs from the proceeds.

Advantages:

- Potentially highest sale price through MLS exposure

- Professional marketing and negotiation support

- Established processes for lien payoff at closing

- Buyer financing options available

Disadvantages:

- Longer timeline (60-90+ days typically)

- Agent commissions reduce net proceeds (5-6% usually)

- Requires property showing-ready condition

- Buyers may be concerned about lien complications

Best for: Sellers with positive equity, standard market-ready properties, and flexibility on timing.

Cash Sale to Investor or Specialized Buyer

Companies and investors who specialize in properties with title complications offer streamlined solutions. These buyers understand lien resolution and often purchase properties as-is.

Advantages:

- Rapid closing (14-30 days typically)

- No repairs or preparation required

- Certainty of closing (no financing contingencies)

- Expertise handling complex lien situations

- Less stress and simplified process

Disadvantages:

- Lower purchase price than retail market (typically 70-85% of market value)

- Less competitive bidding than traditional sales

Best for: Sellers needing quick resolution, properties requiring significant repairs, or complex lien situations making traditional sales difficult.

Sure Path Property Solutions specializes in helping Florida property owners navigate exactly these situations, providing helpful guidance and expert service for properties with liens, title issues, and other complications.

Short Sale (When Underwater)

If you owe more than the property’s worth, a short sale allows you to sell for less than the total debt with lender approval.

The short sale process:

- Document financial hardship to the lender

- List property with short sale-experienced agent

- Submit offers to lender for approval

- Negotiate with lender to accept reduced payoff

- Close once lender approves terms

Advantages:

- Avoid foreclosure and its credit impact

- Lenders may waive deficiency (remaining balance)

- More control than foreclosure process

Disadvantages:

- Lengthy approval process (3-6 months typically)

- Credit score impact (though less than foreclosure)

- Tax implications on forgiven debt (consult tax professional)

- No guarantee lender will approve

Best for: Underwater sellers facing financial hardship who want to avoid foreclosure.

Deed in Lieu of Foreclosure

This option involves transferring the property deed directly to the mortgage lender to satisfy the debt and avoid foreclosure.

Advantages:

- Faster than foreclosure process

- Less credit damage than foreclosure

- Potential for relocation assistance from lender

- Avoids public foreclosure proceedings

Disadvantages:

- Only addresses mortgage liens (junior liens remain)

- Not all lenders accept deed in lieu

- Still impacts credit significantly

- May have tax consequences

Best for: Sellers who cannot maintain payments, have exhausted other options, and want to avoid foreclosure.

Learn more about this option in our deed in lieu guide.

Lien Negotiation and Settlement

Sometimes the best approach is directly negotiating reduced payoffs with lien holders before selling.

Negotiation strategies:

- Offer lump-sum settlements for less than full amount

- Demonstrate limited ability to pay full amount

- Present competing lien priorities reducing recovery

- Leverage time value of money (payment now vs. later)

Typical settlement ranges:

- Second mortgages: 10-40% of balance

- Judgment liens: 30-60% of balance

- Medical liens: 40-70% of balance

- Credit card judgments: 30-50% of balance

Best for: Sellers with multiple junior liens and limited equity who need to reduce total obligations to make a sale feasible.

Common Challenges and Solutions When Selling with Liens 🛠️

Even with careful planning, sellers encounter obstacles when dealing with liens. Knowing common challenges and proven solutions helps you navigate difficulties successfully.

Challenge 1: Discovering Unknown Liens

Many sellers are shocked to find liens they didn’t know existed—old judgments, contractor claims from previous owners, or tax issues.

Solution:

- Order a comprehensive title search early in the process

- Review all public records thoroughly

- Investigate any unfamiliar claims immediately

- Consult with a real estate attorney about questionable liens

- Dispute invalid liens through proper legal channels

Some liens may be invalid due to expired statutes of limitations, improper recording, or incorrect property descriptions. Legal review can identify these issues and potentially eliminate invalid claims.

Challenge 2: Insufficient Sale Proceeds

When your property’s value doesn’t cover all liens and selling costs, you face difficult choices.

Solution:

- Get accurate property valuation from multiple sources

- Negotiate reduced payoffs with junior lien holders

- Consider bringing cash to closing to cover shortfall

- Explore short sale options with primary mortgage holder

- Work with specialized buyers who can structure creative solutions

Remember that junior lien holders often accept reduced amounts rather than receiving nothing if the property forecloses.

Challenge 3: Uncooperative Lien Holders

Some creditors refuse to negotiate, provide payoff information slowly, or create obstacles to closing.

Solution:

- Document all communication attempts

- Escalate to supervisors or legal departments

- Involve your real estate attorney in communications

- Consider legal action for unreasonable delays

- Build extra time into your closing timeline

- Have title company coordinate directly with difficult lien holders

Title companies have established relationships with many lien holders and may achieve better cooperation than individual sellers.

Challenge 4: Expired or Stale Liens Still on Record

Old liens that have been paid or expired may still appear on title because releases were never recorded.

Solution:

- Contact the original creditor for satisfaction documentation

- If creditor no longer exists, research successor companies

- Consult attorney about quiet title action for very old liens

- Obtain title insurance to cover certain stale liens

- File affidavits of payment with supporting documentation

Florida’s statute of limitations eventually renders some liens unenforceable, but they may still cloud title until properly removed through legal process.

Challenge 5: Tax Liens with Penalties and Interest

Property tax liens accumulate interest and penalties rapidly, making payoff amounts grow substantially over time.

Solution:

- Contact the county tax collector immediately

- Request detailed payoff calculation

- Inquire about payment plans or settlement programs

- Understand Florida’s tax certificate and tax deed process

- Prioritize tax liens due to their superior priority

Many Florida counties offer hardship programs or will negotiate settlements, especially when a sale is pending. Learn more about selling with tax liens.

Challenge 6: Mechanic’s Liens from Contractors

These liens can be particularly contentious, especially when you paid the general contractor but they didn’t pay subcontractors.

Solution:

- Review the lien for procedural compliance (strict deadlines apply)

- Verify proper notice was provided to you as owner

- Check if lien amount matches actual work performed

- Consider bonding off the lien to clear title

- Negotiate directly with the claimant

- Consult attorney about defenses under Florida’s mechanic’s lien law

Many mechanic’s liens are invalid due to missed deadlines or improper notices. Legal review often reveals defenses that can eliminate these claims.

Challenge 7: Buyer Concerns About Liens

Potential buyers and their lenders may be nervous about purchasing property with lien complications.

Solution:

- Provide full transparency about liens from the beginning

- Obtain title company commitment to insure over the liens

- Show clear plan for lien resolution at closing

- Offer extended closing timeline if needed for resolution

- Consider cash buyers less concerned about title complications

- Work with buyer’s lender to address concerns

Transparency and professional handling build buyer confidence that liens won’t prevent successful closing.

Working with Professionals: Who You Need on Your Team 👥

Successfully selling a Florida property with liens requires expertise from several professionals. Building the right team dramatically increases your success rate.

Title Company or Real Estate Attorney

These professionals are absolutely essential when liens complicate your sale.

Title companies provide:

- Comprehensive title searches revealing all liens

- Lien payoff coordination and disbursement

- Title insurance protecting the buyer

- Closing services and document preparation

- Recording of deeds and lien releases

Real estate attorneys offer:

- Legal advice on lien validity and disputes

- Negotiation support with lien holders

- Representation in legal proceedings if needed

- Contract review and protection of your interests

- Solutions for complex title issues

When to hire an attorney instead of or in addition to a title company:

- Multiple contested or disputed liens

- Foreclosure proceedings already initiated

- Quiet title actions needed

- Complex negotiations with multiple creditors

- Potential fraud or title defect issues

Real Estate Agent Experienced with Liens

Not all agents have experience with lien complications. Choose one who does.

Look for agents who:

- Have successfully closed sales with lien complications

- Understand title issues and resolution processes

- Have relationships with investors and cash buyers

- Can accurately price property considering lien obligations

- Communicate effectively about complications with buyers

Ask potential agents directly about their experience with liens and request references from similar transactions.

Tax Professional or CPA

Tax implications of lien resolution and property sales can be significant.

Consult a tax professional about:

- Capital gains tax on the sale

- Tax treatment of forgiven debt (1099-C issues)

- Deductibility of certain liens and interest

- Timing strategies to minimize tax impact

- Reporting requirements for short sales

The IRS may treat forgiven debt as taxable income, creating unexpected tax bills. Professional guidance helps you plan for these consequences.

Property Buyer Specializing in Complex Situations

Companies like Sure Path Property Solutions focus specifically on helping property owners facing complicated situations including liens, judgments, title issues, and financial distress.

Benefits of working with specialized buyers:

- Deep understanding of lien resolution processes

- Ability to close quickly (often 14-21 days)

- Purchase properties as-is without repairs

- Handle complex title work and negotiations

- Provide helpful solutions tailored to your situation

- Offer trustworthy service with transparent communication

These industry experts can often structure solutions that traditional buyers and agents cannot, providing a valuable alternative when conventional sales prove difficult.

Costs Associated with Selling a House with Liens in Florida 💵

Understanding all costs helps you calculate realistic net proceeds and make informed decisions.

Standard Selling Costs

These apply to most Florida property sales:

| Cost Category | Typical Amount | Notes |

|---|---|---|

| Real estate commission | 5-6% of sale price | Negotiable; lower with discount brokers |

| Title insurance (owner’s policy) | $500-$2,000 | Based on sale price |

| Documentary stamp taxes | $0.70 per $100 | Florida state tax on deed transfer |

| Recording fees | $50-$150 | County fees for deed recording |

| HOA/Condo documents | $200-$500 | If applicable |

| Property survey | $300-$600 | If required by buyer |

| Home warranty | $300-$600 | Sometimes offered to buyers |

Lien-Specific Costs

Additional expenses related to resolving liens:

Lien Payoff Amounts

Obviously the largest cost—the actual amount owed to satisfy each lien, including principal, interest, penalties, and fees.

Title Search and Examination

Comprehensive title work costs $150-$400 but is essential for identifying all liens.

Attorney Fees

If legal assistance is needed for disputes or complex negotiations:

- Consultation: $200-$500

- Lien dispute representation: $1,500-$5,000+

- Quiet title action: $2,000-$5,000+

Lien Release Recording Fees

Each lien release must be recorded with the county: $10-$50 per release.

Negotiation and Settlement Costs

Some lien holders charge processing fees for settlements or early payoffs: $50-$300 per lien.

Per Diem Interest

Interest continues accruing until liens are paid. Calculate carefully to avoid shortfalls at closing.

Cost-Saving Strategies

Negotiate Agent Commission

Some agents accept lower commissions for quick cash sales or when representing both buyer and seller.

Settle Liens for Less

Junior lien holders often accept 30-70% of the balance, significantly reducing total costs.

Sell As-Is to Cash Buyer

Eliminate repair costs, staging expenses, and extended carrying costs by selling quickly as-is.

Time the Sale Strategically

Closing early in the month or year may reduce some interest calculations and tax obligations.

Bundle Title and Legal Services

Some attorneys offer combined services at reduced rates compared to hiring separately.

Frequently Asked Questions About Selling with Liens in Florida ❓

Can I sell my Florida house if it has a lien on it?

Yes, absolutely. You can sell a Florida property with liens attached. The liens must typically be satisfied from the sale proceeds at closing, but the sale itself can proceed. The title company coordinates paying off the liens and ensuring clear title transfers to the buyer.

Do I have to pay off all liens before selling?

Generally, yes—you must pay liens at or before closing to deliver clear title to the buyer. However, in some cases, buyers agree to purchase property “subject to” certain liens, or you may negotiate reduced payoffs with lien holders. The key is ensuring the buyer receives insurable title.

What happens if I don’t have enough money from the sale to pay all the liens?

You have several options: bring cash to closing to cover the shortfall, negotiate with junior lien holders to accept reduced amounts, pursue a short sale with lender approval, or work with specialized buyers who can structure creative solutions. The specific approach depends on your equity position and circumstances.

How long does it take to sell a house with a lien in Florida?

The timeline typically ranges from 60-120 days depending on lien complexity, market conditions, and resolution strategy. Simple situations with cooperative lien holders may close in 45-60 days, while complex cases involving multiple liens, negotiations, or legal disputes can take 4-6 months or longer.

Will liens prevent me from getting a real estate agent?

No, though you should work with an agent experienced in lien situations. Disclose the liens upfront so your agent can price appropriately and structure the transaction correctly. Some agents specialize in these situations and have valuable expertise.

Can a buyer assume my liens instead of paying them off?

In rare cases, buyers may agree to purchase property “subject to” certain liens, meaning they accept responsibility for them. This is uncommon and typically only happens with sophisticated investors. Most buyers and their lenders require clear title at closing.

What if I can’t locate the lien holder to get a payoff?

This occasionally happens with old liens or when companies have gone out of business. Solutions include hiring a skip-tracing service to locate the creditor, working with an attorney to file a quiet title action, or obtaining title insurance to cover the lien. An experienced real estate attorney can guide you through the specific process.

Are there liens that don’t have to be paid when selling?

Most liens must be satisfied to deliver clear title. However, some very old liens may be unenforceable due to expired statutes of limitations, though they may still appear on title until formally removed. Additionally, certain easements and restrictions, while technically encumbrances, don’t require payment but transfer with the property.

How do I find out if there are liens on my Florida property?

Order a title search from a title company or real estate attorney. You can also search public records at your county clerk’s office or online through the county’s official records website. Professional title searches are more comprehensive and less likely to miss recorded liens.

Can I negotiate with lien holders to reduce what I owe?

Yes, many lien holders will negotiate, especially junior lien holders who might receive nothing if the property forecloses. Present clear documentation of your financial situation and the limited proceeds available. Settlement amounts of 30-70% of the balance are common for junior liens.

Why Choose Sure Path Property Solutions for Your Lien Situation 🌟

When you’re facing the challenge of selling a Florida property with liens, having the right partner makes all the difference. Sure Path Property Solutions specializes in exactly these complicated situations, providing helpful solutions tailored to your unique circumstances.

Our Expertise with Liens and Title Issues

The team at Sure Path Property Solutions brings extensive experience navigating complex real estate challenges including:

- Properties with multiple liens and judgments

- Tax lien complications and county negotiations

- Title defects and clouded ownership

- Inherited properties with unclear title

- Properties in pre-foreclosure or financial distress

This specialized expertise means you work with industry experts who understand Florida’s lien laws, county procedures, and resolution strategies. Rather than learning on your property, the team applies proven approaches refined through hundreds of successful transactions.

A Streamlined, Helpful Process

Sure Path Property Solutions simplifies what could otherwise be an overwhelming process:

Step 1: Free Consultation

Discuss your situation with knowledgeable professionals who listen carefully and ask the right questions to understand your specific circumstances and goals.

Step 2: Property and Lien Evaluation

The team conducts thorough research on your property, title, and lien situation to develop a comprehensive understanding of the challenges and opportunities.

Step 3: Clear, Fair Offer

Receive a transparent cash offer based on current market value, lien obligations, and property condition. No hidden fees or surprise deductions at closing.

Step 4: Coordinated Lien Resolution

Sure Path handles the complex work of coordinating with lien holders, title companies, and counties to resolve all title issues efficiently.

Step 5: Fast, Flexible Closing

Close on your timeline—often in as little as 14-21 days—or choose a date that works best for your situation. The friendly and caring team adapts to your needs.

The Sure Path Advantage

No Repairs Required: Sell your property as-is, regardless of condition. No need to invest in repairs, cleaning, or improvements.

No Agent Commissions: Keep more of your equity without paying 5-6% in real estate commissions.

Certainty of Closing: Cash purchases mean no financing contingencies or last-minute loan denials.

Expert Guidance Throughout: Receive helpful guidance at every step from professionals who genuinely care about your success.

Transparent Communication: No pressure, no games—just honest, straightforward information to help you make the best decision for your situation.

Trustworthy Service: A proven track record of helping Florida property owners navigate challenging situations with integrity and professionalism.

When Sure Path Is the Right Choice

Consider reaching out to Sure Path Property Solutions if you:

- Need to sell quickly due to financial pressure or life circumstances

- Have multiple liens complicating traditional sale options

- Own property requiring significant repairs you can’t afford

- Face foreclosure or tax sale deadlines

- Feel overwhelmed by the complexity of your situation

- Want expert service without the stress of traditional selling

The team understands that behind every property challenge is a person facing real stress and uncertainty. That’s why Sure Path Property Solutions combines professional expertise with genuine compassion, helping you move forward with confidence toward a better future.

Conclusion: Moving Forward with Confidence

Selling a house with a lien in Florida—understanding the laws, process, and timeline—doesn’t have to be an insurmountable obstacle. While liens add complexity to property transactions, thousands of Florida property owners successfully navigate this process every year with the right information and support.

The key takeaways for your success:

Knowledge is power: Understanding Florida’s lien laws, priority rules, and resolution options puts you in control of the situation rather than feeling controlled by it.

Professional help matters: Working with experienced title companies, real estate attorneys, and specialized property buyers dramatically increases your success rate and reduces stress.

Multiple paths forward exist: Whether through traditional sales, cash buyers, short sales, or negotiated settlements, you have options regardless of your equity position.

Timeline planning is essential: Realistic expectations about the 60-120 day process help you plan effectively and avoid unnecessary pressure.

Transparency pays dividends: Disclosing liens early and working cooperatively with all parties leads to smoother transactions and fewer surprises.

Your Next Steps

If you’re ready to move forward with selling your Florida property despite lien complications:

- Order a title search to identify all liens and encumbrances affecting your property

- Calculate your equity position by comparing property value to total lien obligations

- Explore your options including traditional sales, cash buyers, and settlement strategies

- Consult with professionals who have specific experience with lien resolution

- Take action rather than letting the situation worsen through inaction

Remember that liens don’t improve with time—interest accrues, penalties add up, and additional legal complications may arise. Taking proactive steps now positions you for the best possible outcome.

Get Expert Help Today

If you’re facing a lien situation and need helpful guidance from industry experts who genuinely care about your success, Sure Path Property Solutions is here to help. The team specializes in exactly these complicated situations, providing trustworthy service and practical solutions tailored to your unique circumstances.

Contact Sure Path Property Solutions today for a free, no-obligation consultation. Discover how expert service combined with friendly and caring support can help you navigate your lien challenges and move forward toward a fresh start.

Your property challenges don’t define you—but how you address them can transform your future. Take the first step today toward resolution and peace of mind.