Selling Options for Distressed Property: Fast Cash vs. Traditional Sale

When a property becomes distressed—whether through back taxes, liens, foreclosure threats, or complicated ownership issues—the pressure to find a solution can feel overwhelming. The good news? Property owners facing these challenges have more Selling Options for Distressed Property: Fast Cash vs. Traditional Sale than they might realize. Understanding which path makes sense for your unique situation can mean the difference between financial relief and prolonged stress.

A distressed property doesn’t have to mean disaster. With the right information and helpful guidance, owners can navigate even the most complicated real estate situations and move forward with confidence.

Key Takeaways

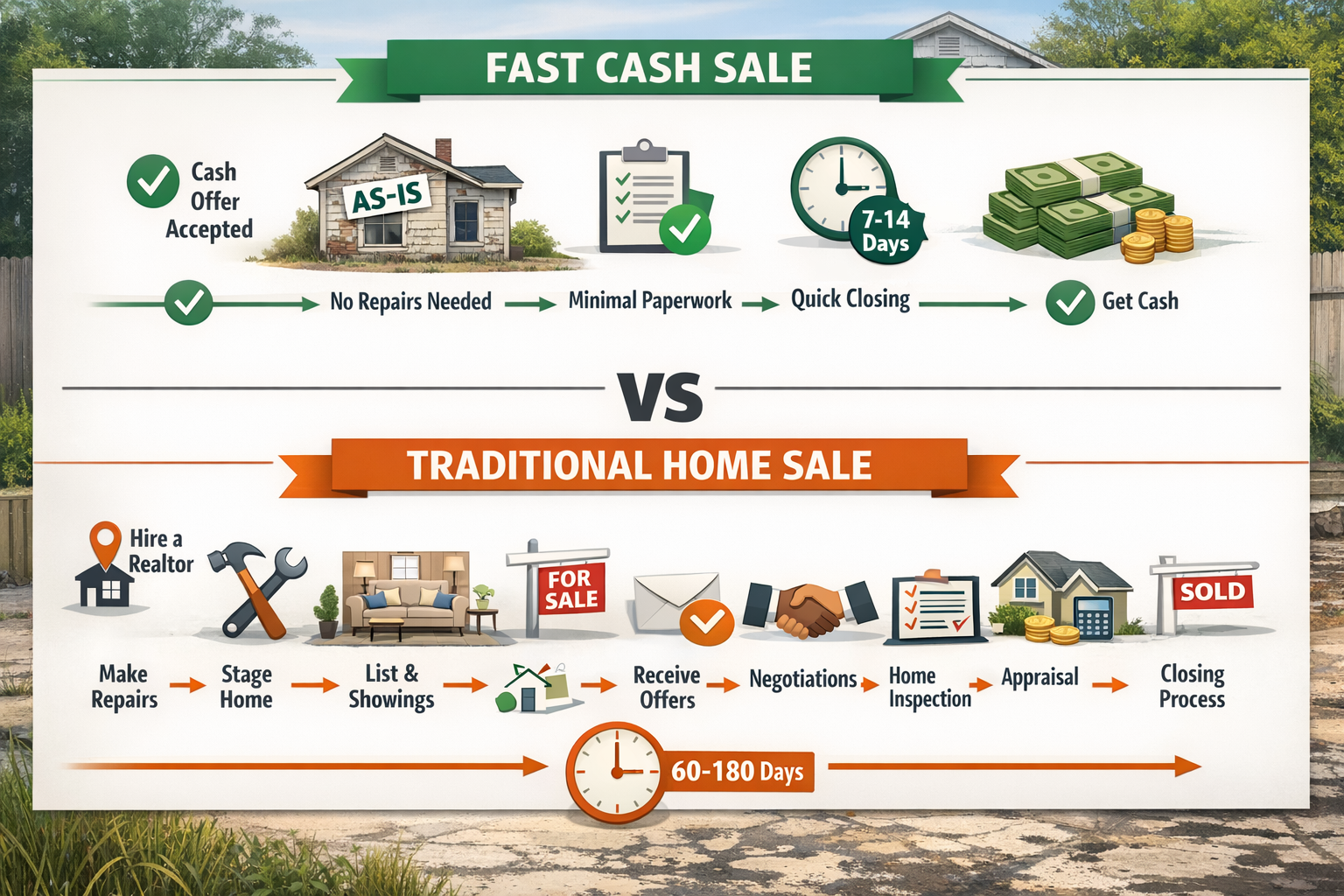

- Fast cash sales typically close in 7-14 days and accept properties as-is, making them ideal for urgent situations involving foreclosure, tax liens, or title problems

- Traditional sales may net higher prices but require 60-180 days, property repairs, and clear title—often impossible for distressed properties

- Properties with liens, judgments, back taxes, or multiple owners face unique challenges that cash buyers can often resolve more efficiently

- The best choice depends on your timeline, property condition, financial urgency, and complexity of title issues

- Working with industry experts who understand distressed property situations provides helpful solutions and peace of mind throughout the process

Understanding Distressed Properties 🏚️

What Makes a Property “Distressed”?

A distressed property faces financial, legal, or physical challenges that prevent a straightforward sale. These properties carry complications that traditional buyers and conventional financing typically cannot accommodate.

Common distressed property scenarios include:

- Properties with substantial back taxes owed to the county or municipality

- Homes facing foreclosure or pre-foreclosure status

- Real estate with liens or judgments attached to the title

- Properties with title defects, clouds, or breaks in the chain of ownership

- Inherited properties with multiple heirs who cannot agree on next steps

- Homes requiring extensive repairs that owners cannot afford

- Properties in probate with complicated estate issues

Why Traditional Sales Often Fail for Distressed Properties

Traditional real estate transactions follow a predictable path: list with an agent, market the property, accept offers contingent on financing and inspections, make repairs, and close after 60-90 days. This process works beautifully for properties in good condition with clear titles.

However, distressed properties break this model in several ways:

Financing obstacles: Most mortgage lenders refuse to finance properties with tax liens, judgment liens, or significant title issues. This eliminates 85-90% of potential buyers from the market immediately.

Inspection failures: Properties in poor condition fail inspections, causing deals to collapse. Buyers with conventional financing cannot proceed when appraisals come in below purchase price.

Time constraints: Owners facing foreclosure or tax sales don’t have 3-6 months to wait. Every day counts when auction dates loom.

Repair requirements: Making a distressed property “market ready” often costs $20,000-$50,000 or more—money most distressed property owners simply don’t have.

Title complications: Title problems can take months to resolve through traditional channels, if they can be resolved at all.

“The traditional real estate market operates on the assumption that properties have clear titles and meet minimum condition standards. When those assumptions don’t hold, the entire system breaks down.”

The Traditional Sale Approach for Distressed Properties

How Traditional Sales Work

The traditional sale process involves listing a property with a licensed real estate agent who markets it through the Multiple Listing Service (MLS), hosts open houses, and negotiates with potential buyers. This approach has served the real estate industry well for decades.

The typical traditional sale timeline:

- Preparation phase (2-4 weeks): Repairs, staging, professional photography

- Listing phase (30-60 days): Marketing, showings, open houses

- Negotiation phase (1-2 weeks): Offers, counteroffers, acceptance

- Due diligence phase (30-45 days): Inspections, appraisals, financing approval

- Closing phase (1-2 weeks): Title work, final walkthrough, settlement

Total timeline: 90-180 days from decision to cash in hand

Advantages of Traditional Sales

For properties that can be sold traditionally, this approach offers several benefits:

Higher sale prices: Marketing to the broadest possible buyer pool typically generates competitive offers. Retail buyers often pay 10-20% more than investors or cash buyers.

Professional representation: Experienced agents handle negotiations, paperwork, and coordination with all parties.

Maximum exposure: MLS listings reach thousands of potential buyers through real estate websites and agent networks.

Structured process: Established procedures protect both buyers and sellers through standardized contracts and disclosures.

Major Limitations for Distressed Properties

Unfortunately, the very features that make traditional sales attractive become barriers for distressed properties:

❌ Repair requirements are prohibitive

Real estate agents typically advise making properties “show ready” before listing. For a distressed property, this might mean:

- Roof replacement: $8,000-$15,000

- HVAC system: $5,000-$10,000

- Foundation repairs: $10,000-$30,000

- Cosmetic updates: $5,000-$20,000

These costs are impossible for owners already struggling with back taxes or facing foreclosure.

❌ Financing contingencies kill deals

Traditional buyers need mortgage approval. Lenders require:

- Clear title with no liens or judgments

- Property condition meeting minimum standards

- Appraisal supporting the purchase price

If you owe back taxes or have liens attached, conventional financing becomes nearly impossible.

❌ Time works against you

When facing foreclosure auction dates or tax sale deadlines, waiting 4-6 months isn’t an option. Every week that passes increases costs and reduces options.

❌ Agent commission reduces net proceeds

Traditional sales involve 5-6% commission to real estate agents, plus 2-3% in closing costs. On a $200,000 sale, that’s $14,000-$18,000 in transaction costs before addressing any liens or back taxes.

When Traditional Sales Make Sense

Despite these challenges, traditional sales remain the right choice for some distressed property situations:

✅ When you have time: If foreclosure or tax sale is 6+ months away, traditional marketing might work

✅ When repairs are minor: Properties needing only cosmetic updates under $5,000 can often be made market-ready

✅ When title is clear or easily cleared: Simple lien payoffs that can be handled at closing don’t necessarily require cash buyers

✅ When maximizing price is essential: If equity significantly exceeds all debts and costs, the higher traditional sale price might justify the wait and expense

The Fast Cash Sale Alternative 💵

How Cash Sales Work for Distressed Properties

Fast cash sales follow a dramatically different path designed specifically for properties that cannot be sold traditionally. Cash buyers—typically real estate investors or investment companies—purchase properties directly without financing contingencies, inspection requirements, or repair demands.

The typical cash sale timeline:

- Initial contact (Day 1): Property owner reaches out to cash buyer

- Property evaluation (Days 1-3): Cash buyer reviews property details, title issues, lien amounts

- Cash offer (Days 3-5): Buyer presents written offer with terms

- Acceptance and contract (Days 5-7): Owner reviews and accepts offer

- Title work and closing (Days 7-14): Buyer coordinates title clearance and closing

Total timeline: 7-14 days from first contact to cash in hand

Key Advantages of Cash Sales

⚡ Speed and certainty

Cash transactions close in days, not months. When facing urgent situations like foreclosure or tax sales, this speed can literally save your financial future.

🏚️ As-is purchases

Cash buyers purchase properties in any condition. No repairs, no staging, no cleaning required. This saves tens of thousands in renovation costs and weeks of preparation time.

📋 Simplified process

No financing contingencies mean no appraisals, no bank underwriting, no loan denials. The process involves far less paperwork and fewer parties.

🔧 Problem-solving approach

Reputable cash buyers specialize in complicated situations—they’re equipped to handle liens, title issues, multiple owners, and other challenges that derail traditional sales.

💰 No commissions or fees

Legitimate cash buyers don’t charge commissions, fees, or closing costs. The offer you receive is the amount you’ll get at closing (minus any liens or debts being paid off).

Potential Disadvantages of Cash Sales

Honest evaluation requires acknowledging the tradeoffs:

Lower purchase price: Cash buyers typically offer 60-80% of after-repair value (ARV), accounting for repair costs, carrying costs, and profit margin. This means lower gross proceeds compared to a successful traditional sale.

Less competition: Working with a single buyer rather than marketing to many means less competitive pressure to increase offers.

Need for due diligence: Not all cash buyers operate with integrity. Property owners should verify credentials, check references, and ensure they’re working with trustworthy service providers.

When Cash Sales Make the Most Sense

Fast cash sales become the optimal choice in specific circumstances common to distressed properties:

✅ Urgent timelines: Foreclosure auctions, tax sales, or other deadlines within 30-60 days

✅ Significant repair needs: Properties requiring $20,000+ in repairs that owners cannot fund

✅ Title complications: Liens, judgments, or title defects that would prevent traditional financing

✅ Multiple ownership issues: Inherited properties with multiple heirs who need quick resolution

✅ Financial distress: Back taxes or other debts consuming any potential profit from a traditional sale

✅ Emotional exhaustion: Situations where the stress and complexity of traditional sales outweigh the potential for higher proceeds

Selling Options for Distressed Property: Detailed Comparison

Side-by-Side Analysis

| Factor | Traditional Sale | Fast Cash Sale |

|---|---|---|

| Timeline | 90-180 days | 7-14 days |

| Property Condition | Repairs required | Sold as-is |

| Buyer Financing | Usually required | All cash, no contingencies |

| Title Requirements | Must be clear | Buyers often resolve issues |

| Commission/Fees | 5-6% + closing costs | No fees or commissions |

| Sale Price | 95-100% of market value | 60-80% of ARV |

| Certainty | 20-30% fall through | 95%+ close as agreed |

| Stress Level | High (showings, negotiations) | Low (single transaction) |

| Best For | Properties in good condition with time | Distressed properties needing speed |

Real-World Scenarios

Scenario 1: Inherited Property with Back Taxes

Situation: Three siblings inherit their parents’ home valued at $180,000. The property needs $25,000 in repairs and has $15,000 in back taxes. Siblings live in different states and want to settle the estate quickly.

Traditional Sale Approach:

- Timeline: 120-150 days

- Repair costs: $25,000 (split three ways)

- Commission/costs: $16,200 (9%)

- Back taxes: $15,000 + penalties

- Net proceeds: ~$123,800 ($41,267 per sibling)

- Challenges: Coordinating repairs from distance, monthly carrying costs, continued tax accumulation

Fast Cash Sale Approach:

- Timeline: 10-14 days

- Cash offer: $125,000

- Back taxes paid at closing: $15,000

- No repair costs: $0

- No commissions: $0

- Net proceeds: $110,000 ($36,667 per sibling)

- Benefits: Quick resolution, no coordination hassles, no additional costs

Analysis: The traditional sale might net $13,800 more, but requires $25,000 upfront, 4+ months of time, and significant coordination. For many families, the certainty and speed of the cash option outweighs the potential higher return.

Scenario 2: Pre-Foreclosure with Judgment Lien

Situation: Homeowner is 90 days behind on mortgage ($220,000 balance) on a property worth $250,000. There’s also a $30,000 judgment lien from a contractor dispute. Foreclosure auction scheduled in 45 days.

Traditional Sale Approach:

- Timeline: 90-120 days (exceeds foreclosure deadline)

- Would need to negotiate postponement with lender

- Judgment lien complicates title for conventional buyers

- Commission/costs: $22,500 (9%)

- Net proceeds: $250,000 – $220,000 – $30,000 – $22,500 = -$22,500 (short sale required)

- Challenges: Lender approval needed, judgment holder negotiation, time constraint impossible

Fast Cash Sale Approach:

- Timeline: 10 days (before foreclosure)

- Cash offer: $200,000

- Mortgage payoff: $220,000

- Judgment negotiated and paid: $20,000

- Net proceeds: $0, but foreclosure avoided

- Benefits: Stops foreclosure, avoids credit damage, fresh start possible

Analysis: Neither option produces cash for the homeowner, but only the cash sale prevents foreclosure and the devastating credit consequences that follow. The cash buyer’s ability to negotiate with lien holders and close quickly provides the only viable path forward.

Financial Reality Check 💰

Many property owners initially focus solely on sale price, but the true measure is net proceeds after all costs and obligations. Consider this breakdown:

Traditional Sale Gross: $200,000

- Agent commission (6%): -$12,000

- Seller closing costs (2-3%): -$5,000

- Pre-listing repairs: -$15,000

- Carrying costs during sale (4 months): -$4,000

- Back taxes and penalties: -$18,000

- Lien payoff: -$25,000

- Net to seller: $121,000

Cash Sale Gross: $155,000

- Agent commission: $0

- Seller closing costs: $0

- Repairs: $0

- Carrying costs: $0

- Back taxes paid at closing: -$18,000

- Lien negotiated and paid: -$20,000

- Net to seller: $117,000

The $45,000 difference in gross price becomes only $4,000 in net proceeds—and that assumes the traditional sale succeeds, which is far from guaranteed for distressed properties.

Special Considerations for Common Distressed Property Situations

Properties with Back Taxes

Back taxes on property create unique challenges. Counties place tax liens that take priority over nearly all other claims, and tax sales can result in complete loss of the property.

Traditional sale challenges:

- Buyers fear properties with tax issues

- Lenders often refuse financing until taxes are current

- Accumulated penalties increase daily

- Tax sale deadlines create pressure

Cash sale advantages:

- Buyers pay off back taxes at closing

- Quick closings prevent additional penalties

- Experience with tax lien properties streamlines process

- Stops tax sale proceedings

Properties with Liens and Judgments

Liens and judgments attach to property titles, creating obstacles for traditional sales. These include contractor liens, HOA liens, IRS liens, and civil judgment liens.

Traditional sale challenges:

- Must be resolved before closing

- Lien holders may be difficult to locate or negotiate with

- Title companies require clear title for conventional financing

- Process can take months

Cash sale advantages:

- Experienced buyers negotiate lien releases

- Can close with liens and resolve afterward

- Understand lien priority and settlement strategies

- Handle all coordination with lien holders

Inherited Properties with Multiple Owners

Properties inherited by multiple heirs face unique complications. Disagreements about timing, price, or whether to sell at all can paralyze decision-making.

Traditional sale challenges:

- All owners must agree on agent, price, and terms

- Coordinating repairs and maintenance across multiple parties

- Disputes can derail sales mid-process

- Carrying costs continue while family negotiates

Cash sale advantages:

- Single transaction simplifies coordination

- Quick timeline reduces conflict opportunities

- Some buyers can purchase individual shares

- Definitive resolution for all parties

Properties Facing Foreclosure

Pre-foreclosure properties face the ultimate time constraint. Once the foreclosure process begins, the clock ticks toward auction and complete loss of equity.

Traditional sale challenges:

- Timeline almost always exceeds foreclosure deadline

- Lenders must approve any short sale

- Buyers flee at mention of foreclosure

- Process adds stress to already difficult situation

Cash sale advantages:

- Can close before auction date

- Buyers experienced with foreclosure timelines

- Preserve credit by avoiding foreclosure completion

- Walk away with dignity and fresh start

Making Your Decision: Fast Cash vs. Traditional Sale 🤔

Key Questions to Ask Yourself

The right choice depends on your specific situation. Consider these questions:

1. How urgent is your timeline?

- If you have less than 60 days before foreclosure, tax sale, or other deadline, cash sales are likely your only option

- If you have 6+ months, traditional sales become more viable

2. What is your property’s condition?

- Properties needing $20,000+ in repairs strongly favor cash sales

- Properties needing only cosmetic work under $5,000 can potentially be sold traditionally

3. What title issues exist?

- Complex title problems (multiple liens, judgments, title defects) favor cash buyers who specialize in these issues

- Clear or easily cleared titles work for either approach

4. What is your financial situation?

- If you cannot afford repair costs, carrying costs, or commissions, cash sales eliminate these expenses

- If you have resources to invest in preparing the property, traditional sales might net more

5. What is your stress tolerance?

- Traditional sales involve showings, negotiations, inspections, and potential deal failures

- Cash sales offer simplicity and certainty

6. Do you need maximum proceeds or quick resolution?

- If every dollar matters and you have time, traditional sales might be worth pursuing

- If speed, certainty, and peace of mind matter most, cash sales deliver

Red Flags and Warning Signs ⚠️

Not all cash buyers operate with integrity. Watch for these warning signs:

🚩 Pressure tactics: Legitimate buyers give you time to review offers and make informed decisions

🚩 Upfront fees: Reputable cash buyers never charge fees to make offers or purchase properties

🚩 Vague terms: Professional offers include specific purchase prices, closing dates, and terms in writing

🚩 No proof of funds: Serious buyers provide evidence they can close

🚩 Reluctance to answer questions: Trustworthy service providers welcome questions and provide clear answers

Working with Reputable Cash Buyers

When considering cash offers, look for these positive indicators:

✅ Established business presence: Physical office, professional website, verifiable history

✅ Transparent process: Clear explanation of how they determine offers and what happens at each stage

✅ References and reviews: Testimonials from previous sellers, positive online reviews

✅ Professional communication: Prompt responses, written documentation, respectful interaction

✅ No-obligation offers: Willingness to make offers without requiring commitments

✅ Helpful guidance: Focus on solving your problems, not just buying your property

Companies like Sure Path Property Solutions specialize in helping property owners navigate complicated situations with integrity and expertise. Working with industry experts who understand the challenges of distressed properties provides peace of mind during difficult times.

The Role of Professional Guidance and Expert Service 🏆

Why Expertise Matters

Distressed property situations involve complex legal, financial, and practical considerations. The right professional guidance can mean the difference between successful resolution and costly mistakes.

What expert service provides:

Problem diagnosis: Experienced professionals quickly identify all issues affecting your property—liens you didn’t know about, title defects, tax complications, or ownership disputes.

Solution options: Rather than pushing a single approach, helpful guidance means presenting all viable options with honest pros and cons for each.

Coordination: Industry experts handle communication with counties, title companies, lien holders, and other parties, removing the burden from property owners.

Negotiation: Skilled negotiators can often settle liens and judgments for less than full amounts, increasing your net proceeds.

Peace of mind: Knowing experienced professionals are handling complex details reduces stress during already difficult times.

What Sure Path Property Solutions Offers

Sure Path Property Solutions specializes in exactly the situations that make properties “distressed.” The company’s mission centers on providing helpful solutions for property owners facing:

- Back taxes and tax liens

- Multiple heirs and ownership disputes

- Liens and judgments

- Title defects and unclear ownership

- Foreclosure threats

- Properties in any condition

The approach combines expert service with friendly and caring support, recognizing that behind every distressed property is a person or family navigating difficult circumstances.

The Sure Path difference:

Comprehensive problem-solving: Rather than simply making offers, the team evaluates entire situations and coordinates with counties and title professionals to create clear paths forward.

Transparent communication: Property owners receive honest assessments and clear explanations of all options, empowering informed decisions.

Flexible solutions: Whether that means a fast cash purchase, helping coordinate a traditional sale, or connecting owners with other resources, the focus remains on what serves the property owner best.

Respectful process: Every interaction reflects understanding that these situations involve stress, emotion, and often difficult life circumstances.

Taking Action: Your Next Steps 📋

If You’re Considering a Traditional Sale

Step 1: Get a professional property assessment to understand repair needs and costs

Step 2: Research comparable sales in your area to set realistic price expectations

Step 3: Verify your title is clear or can be cleared within reasonable timeframes

Step 4: Calculate total costs (repairs, commissions, carrying costs, closing costs)

Step 5: Ensure your timeline allows 4-6 months from listing to closing

Step 6: Interview multiple real estate agents with experience selling properties in your condition

Step 7: Create a realistic budget and timeline, building in contingency for delays

If You’re Considering a Cash Sale

Step 1: Document your situation—property condition, title issues, liens, timeline constraints

Step 2: Research reputable cash buyers in your area with experience in distressed properties

Step 3: Request offers from 2-3 buyers to compare terms and approaches

Step 4: Ask questions about their process, timeline, and how they handle your specific issues

Step 5: Verify credentials, check references, and review online feedback

Step 6: Review all offers in writing with specific terms and closing dates

Step 7: Choose the buyer who offers the best combination of price, terms, and trustworthy service

Getting Started with Sure Path Property Solutions

If your property faces challenges like back taxes, liens, multiple owners, or title issues, contacting Sure Path Property Solutions provides a no-obligation opportunity to:

- Discuss your specific situation with industry experts

- Receive an honest assessment of your options

- Get a fair cash offer if that’s the right solution

- Obtain helpful guidance even if a cash sale isn’t the best path forward

The initial consultation costs nothing and creates no obligation. It simply provides the information needed to make the best decision for your circumstances.

Frequently Asked Questions 🙋

Q: Will a cash offer be much lower than what I could get traditionally?

A: Cash offers typically range from 60-80% of after-repair value, which may be 15-30% less than retail market value. However, when you subtract repair costs, commissions, closing costs, and carrying costs from a traditional sale, the net difference is often much smaller—sometimes only 5-10%. For many sellers, the speed, certainty, and simplicity justify this difference.

Q: Can I sell a property with back taxes without paying them first?

A: Yes. Cash buyers typically pay off back taxes at closing as part of the purchase transaction. The tax amount is deducted from your proceeds, but you don’t need to come up with the money upfront. Learn more about selling property with back taxes.

Q: What if I have liens on my property—can I still sell?

A: Absolutely. Properties with liens can be sold, though traditional buyers often struggle with them. Cash buyers experienced with distressed properties routinely handle lien resolution as part of the purchase process. They coordinate with lien holders, negotiate settlements when possible, and ensure clear title at closing.

Q: How quickly can a cash sale actually close?

A: Most cash sales close within 7-14 days, though the timeline can be adjusted to meet your needs. Some close in as few as 5 days when urgency requires it, while others extend to 30 days if sellers need more time to relocate.

Q: Are there any fees or costs I need to pay with a cash sale?

A: Legitimate cash buyers don’t charge sellers any fees, commissions, or closing costs. Be wary of anyone asking for upfront payments or charging fees to make an offer. The offer amount should be what you receive (minus any liens, back taxes, or mortgages being paid off).

Q: What if multiple family members own the property and we can’t agree?

A: This is a common challenge with inherited properties. Some cash buyers can purchase individual ownership shares, while others work with all owners to find mutually acceptable solutions. Professional mediation or legal guidance may also help resolve disputes. Read more about selling property with multiple owners.

Q: Can I sell a property that’s already in foreclosure?

A: Yes, you can sell right up until the foreclosure auction takes place. Cash buyers who specialize in pre-foreclosure properties can often close quickly enough to prevent the auction. This allows you to avoid foreclosure on your credit record and potentially walk away with some proceeds rather than losing everything.

Q: How do I know if a cash buyer is legitimate?

A: Look for established businesses with physical locations, professional websites, verifiable reviews, and transparent processes. Ask for references from previous sellers. Legitimate buyers provide written offers with specific terms, never pressure you to decide immediately, and welcome your questions. Trust your instincts—if something feels wrong, it probably is.

Conclusion: Choosing Your Best Path Forward

Understanding Selling Options for Distressed Property: Fast Cash vs. Traditional Sale empowers property owners to make informed decisions during challenging times. Neither approach is universally “better”—the right choice depends entirely on your specific circumstances, timeline, property condition, and priorities.

Traditional sales offer the potential for higher gross proceeds when you have time, resources to invest in preparation, and a property that can attract conventional buyers. This path makes sense for properties in relatively good condition with clear titles and owners who can wait 4-6 months for closing.

Fast cash sales provide speed, certainty, and simplicity for properties facing complications that prevent traditional sales. When dealing with back taxes, liens, title issues, multiple owners, foreclosure threats, or properties needing extensive repairs, cash buyers offer helpful solutions that traditional markets cannot match.

The most important step is taking action rather than letting problems compound. Every day of delay with distressed properties typically increases costs, reduces options, and adds stress. Whether you ultimately choose a traditional sale, a cash sale, or another solution entirely, getting expert service and helpful guidance starts the path toward resolution.

Your situation is unique, and you deserve solutions tailored to your specific needs. The friendly and caring professionals at Sure Path Property Solutions stand ready to help you navigate complicated real estate issues with integrity, expertise, and respect. Reach out today for a no-obligation consultation and discover the path forward that’s right for you.

Remember: a distressed property doesn’t mean a hopeless situation. With the right information, trustworthy service, and industry experts by your side, even the most complicated property challenges can be resolved successfully. Your fresh start begins with a single step—understanding your options and choosing your path forward.