Title Insurance Claims: When to File & How the Process Works

Imagine discovering that the property you just purchased—your dream home or investment—has a hidden lien from a previous owner's unpaid contractor bills. Or worse, learning that someone else has a legitimate claim to a portion of your land due to an error in the public records. These nightmare scenarios are exactly why title insurance exists, but knowing when and how to file a title insurance claim can mean the difference between a quick resolution and months of legal headaches.

Understanding Title Insurance Claims: When to File & How the Process Works is essential for any property owner facing unexpected title defects. Whether you've inherited property with unclear ownership, discovered liens you didn't know existed, or encountered boundary disputes, navigating the claims process doesn't have to be overwhelming. With the right knowledge and helpful guidance, you can protect your property rights and resolve title issues efficiently.

Key Takeaways

- File a title insurance claim immediately upon discovering any title defect, ownership dispute, lien, or encumbrance that wasn't disclosed before closing

- Title insurance protects against past defects in ownership, not future issues, and covers both legal defense costs and financial losses up to the policy amount

- The claims process typically takes 30-90 days from initial filing to resolution, depending on the complexity of the title defect

- Documentation is critical—gather all property records, title documents, correspondence, and evidence of the defect before filing your claim

- Professional assistance from title experts can significantly improve claim outcomes, especially for complex situations involving multiple heirs, judgments, or clouded titles

What Is Title Insurance and Why It Matters

Title insurance protects property owners and lenders from financial loss due to defects in a property's title. Unlike other insurance types that protect against future events, title insurance safeguards against problems that already exist but weren't discovered during the initial title search.

How Title Insurance Works

When purchasing property, a title company conducts a thorough search of public records to identify any issues with ownership. Despite this careful examination, some problems remain hidden or undiscovered. Title insurance provides coverage when these hidden defects surface after closing.

Two types of title insurance policies exist:

- Owner's Policy: Protects the property buyer's equity and ownership rights

- Lender's Policy: Protects the mortgage lender's investment (required by most lenders)

The owner's policy remains in effect for as long as you or your heirs own the property. This one-time premium paid at closing provides ongoing protection against covered title defects.

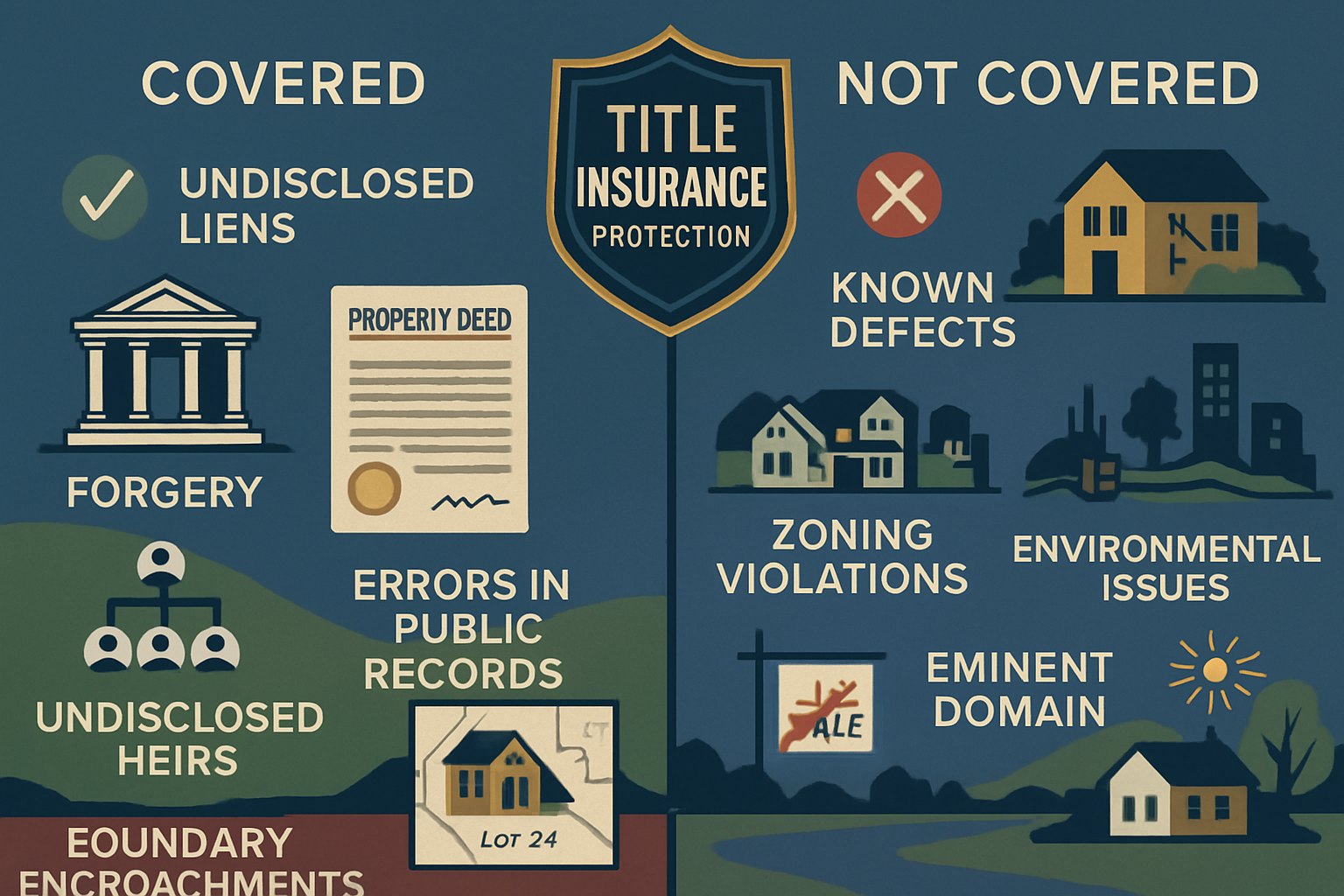

Common Title Defects Covered by Insurance

Title insurance typically covers a wide range of defects and issues:

- Undisclosed liens from previous owners (tax liens, mechanic's liens, judgment liens)

- Errors or omissions in deeds and public records

- Forgery and fraud in the chain of title

- Unknown heirs claiming ownership rights

- Boundary disputes and survey errors

- Easements and encumbrances not revealed in the title search

- Clerical errors in recording documents

For property owners dealing with liens and judgments, title insurance can provide crucial financial protection and legal defense.

"Title insurance is your safety net against the unknown history of your property. It's not just about protecting your investment—it's about protecting your peace of mind." – Industry experts

Understanding Title Insurance Claims: When to File & How the Process Works

Knowing when to initiate a title insurance claim is crucial for protecting your property rights. Many property owners delay filing claims because they don't recognize covered defects or understand the claims process.

When Should You File a Title Insurance Claim?

File a title insurance claim as soon as you discover any of these situations:

📋 Immediate Filing Situations:

- Discovery of undisclosed liens – If you find liens that weren't disclosed before closing, including tax liens, mechanic's liens, or judgment liens

- Ownership disputes – When someone challenges your ownership or claims rights to your property

- Boundary conflicts – If a survey reveals your property boundaries differ from the legal description

- Easement issues – When undisclosed easements limit your property use

- Forgery or fraud – If documents in the chain of title were forged or fraudulent

- Heir claims – When previously unknown heirs assert ownership rights

- Recording errors – If mistakes in public records affect your title

Time-Sensitive Nature of Title Claims

While title insurance policies don't typically have strict filing deadlines like other insurance types, prompt action is essential. Delays can complicate the claims process and potentially weaken your position.

Why timing matters:

- Evidence becomes harder to gather over time

- Witnesses may become unavailable

- Statute of limitations may apply to related legal actions

- Ongoing title defects can worsen and create additional complications

Property owners dealing with title issues should consult with industry experts immediately upon discovering any potential defect.

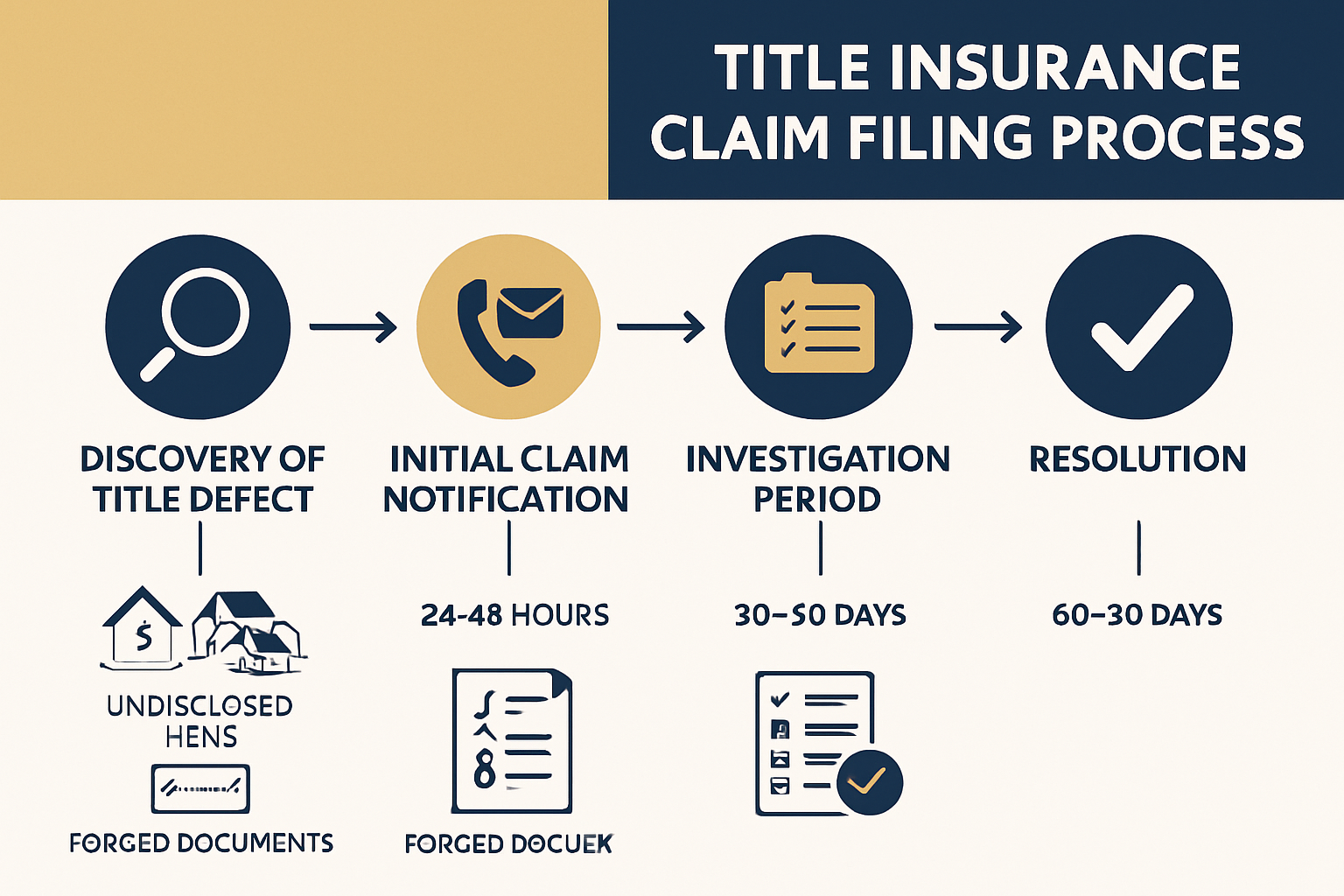

The Title Insurance Claims Process: Step-by-Step Guide

Understanding the complete claims process helps property owners navigate what can seem like a complex system. Here's how title insurance claims work from start to finish.

Step 1: Initial Discovery and Documentation

The moment you discover a potential title defect, begin documenting everything:

Essential documentation includes:

- Original title insurance policy

- Property deed and closing documents

- Evidence of the title defect (lien notices, legal claims, survey discrepancies)

- All correspondence related to the issue

- Public records showing the problem

- Timeline of events

Create a detailed written account of how and when you discovered the defect. Include dates, communications, and any financial impact you've experienced.

Step 2: Contact Your Title Insurance Company

Reach out to your title insurance company immediately. Most policies include contact information for claims departments.

When contacting the insurer:

- Reference your policy number

- Provide a clear, concise description of the defect

- Mention any deadlines or urgent circumstances

- Ask about specific documentation requirements

- Request confirmation of claim receipt in writing

The title company will assign a claims adjuster to your case. This person becomes your primary contact throughout the process.

Step 3: Formal Claim Submission

Submit a formal written claim with all supporting documentation. The title company typically provides specific forms and requirements.

Your claim submission should include:

| Document Type | Purpose | Details Required |

|---|---|---|

| Claim Form | Official notification | Policy number, property address, defect description |

| Title Policy | Proof of coverage | Original or certified copy |

| Property Deed | Ownership verification | Recorded deed showing your ownership |

| Evidence of Defect | Substantiate claim | Lien notices, legal documents, surveys |

| Financial Impact | Damages calculation | Costs incurred, potential losses |

| Correspondence | Timeline documentation | Letters, emails, notices received |

Keep copies of everything you submit. Send documents via certified mail or email with read receipts to maintain a record of submission.

Step 4: Investigation and Review Period

Once your claim is filed, the title insurance company begins its investigation. This phase typically takes 30-60 days but can extend longer for complex issues.

During the investigation, the insurer will:

- Review all submitted documentation

- Conduct their own title search and research

- Examine public records and historical documents

- Interview relevant parties

- Consult with legal experts

- Assess the validity and extent of the defect

- Determine coverage under the policy terms

The claims adjuster may request additional information during this period. Respond promptly to all requests to avoid delays.

Step 5: Claim Decision and Resolution Options

After completing the investigation, the title company issues a decision. Three possible outcomes exist:

✅ Claim Approved – Full Coverage

The insurer acknowledges the defect is covered and proceeds with resolution. Options include:

- Legal defense: The company provides attorneys to defend your title

- Financial settlement: Payment to resolve the defect (removing liens, settling claims)

- Curative action: Steps to correct the title defect directly

⚠️ Claim Approved – Partial Coverage

The insurer covers some aspects but excludes others based on policy terms. You'll receive an explanation of what's covered and what's not.

❌ Claim Denied

The company determines the defect isn't covered under your policy. Common denial reasons include:

- Defect falls under policy exclusions

- Issue was known before closing

- Problem arose after the policy effective date

- Insufficient evidence of covered defect

If your claim is denied, you have the right to appeal the decision with additional evidence or legal arguments.

Step 6: Resolution and Follow-Through

For approved claims, the title company takes action to resolve the defect:

Resolution methods vary based on the defect type:

- Lien removal: Paying off or negotiating undisclosed liens

- Legal action: Filing quiet title actions to clear ownership disputes

- Boundary corrections: Resolving survey errors and property line disputes

- Document corrections: Filing corrected deeds or other instruments

- Financial compensation: Reimbursing losses when defects can't be cured

Throughout resolution, maintain communication with your claims adjuster. Ask for regular updates and clarification on any steps being taken.

Common Scenarios: When Title Insurance Claims Become Necessary

Real-world situations help illustrate when filing a title insurance claim becomes necessary. These scenarios reflect common experiences of property owners facing unexpected title challenges.

Scenario 1: Inherited Property with Unknown Liens

Sarah inherited her grandmother's house, excited to keep the family home. During the title transfer process, a title search revealed multiple tax liens from unpaid property taxes dating back fifteen years—totaling $47,000.

How title insurance helped:

Sarah's grandmother had purchased title insurance when she originally bought the property. Although Sarah inherited the property, the owner's policy transferred with ownership. She filed a claim, and the title insurance company:

- Verified the liens weren't disclosed in the original title search

- Paid the full amount to clear the tax liens

- Handled all negotiations with the county tax office

- Ensured Sarah received clear title to the property

This helpful solution allowed Sarah to keep her family home without the burden of unexpected debt.

Scenario 2: Undisclosed Mechanic's Lien

Marcus purchased a renovated investment property, only to receive a notice three months later from a contractor claiming an unpaid $32,000 mechanic's lien from work completed before he bought the property.

The claims process:

Marcus immediately contacted his title insurance company with the lien notice. The investigation revealed:

- The previous owner hired the contractor but never paid for completed work

- The contractor filed the lien after Marcus's closing date but for work performed before

- The lien wasn't discovered in the pre-closing title search

The title insurance company provided legal defense and ultimately negotiated a settlement with the contractor, paying the claim and protecting Marcus's investment. Understanding how to handle property liens is crucial for property owners in similar situations.

Scenario 3: Boundary Dispute with Neighbors

Jennifer planned to build a fence on her new property when her neighbor claimed the property line was actually 15 feet into what Jennifer believed was her yard—potentially reducing her lot size by 20%.

Resolution through title insurance:

Jennifer's title policy covered boundary disputes. The title company:

- Hired a professional surveyor to establish accurate boundaries

- Reviewed historical property records and surveys

- Discovered an error in the legal description on Jennifer's deed

- Filed corrective documents to establish proper boundaries

- Paid all legal and surveying costs

The expert service provided by the title company resolved the dispute without Jennifer incurring thousands in legal fees.

Scenario 4: Forged Documents in Chain of Title

Robert was preparing to sell his property when a potential buyer's title search uncovered that a deed from 1998 in the chain of title contained a forged signature. This clouded title made the property unsellable.

Title insurance claim outcome:

Robert's title insurance company took immediate action:

- Initiated legal proceedings to clear the title defect

- Hired forensic document experts to prove the forgery

- Filed a quiet title action in court

- Covered all legal fees and court costs (exceeding $18,000)

- Successfully cleared the title within six months

This trustworthy service allowed Robert to complete his sale without personal financial loss.

What Title Insurance Does NOT Cover: Important Exclusions

Understanding policy exclusions is just as important as knowing what's covered. Title insurance policies contain specific exclusions that deny coverage for certain types of defects.

Standard Policy Exclusions

❌ Known defects: Issues you knew about before purchasing the property aren't covered. If the title search revealed a problem and you proceeded with the purchase anyway, you can't later file a claim for that known issue.

❌ Government actions: Title insurance doesn't cover:

- Eminent domain proceedings

- Zoning law changes

- Building code violations

- Environmental regulations and restrictions

❌ Issues arising after policy date: Problems that occur after your policy effective date (typically the closing date) aren't covered. Title insurance is retrospective, not prospective.

❌ Native American land claims: Most policies exclude claims based on indigenous land rights or treaty violations.

❌ Matters not of public record: Defects that wouldn't appear in public records, such as:

- Unrecorded easements you should have discovered through property inspection

- Boundary encroachments visible during a property visit

- Rights of parties in possession (like tenants)

Enhanced Coverage Options

Some title insurance companies offer enhanced or extended coverage policies that include protections beyond standard policies:

- Post-policy forgery: Coverage for documents forged after your purchase

- Building permit violations: Protection against existing permit issues

- Subdivision violations: Coverage for unapproved lot divisions

- Encroachments: Enhanced coverage for structures crossing property lines

- Forced removal of structures: Protection if you must remove buildings due to violations

Enhanced policies cost more but provide broader protection for property owners facing complex situations.

Maximizing Your Title Insurance Claim Success

Filing a successful title insurance claim requires strategy, preparation, and persistence. These practical tips help property owners navigate the process effectively.

Documentation Best Practices

📁 Create a comprehensive claim file:

Organize all documents in chronological order with clear labels. Include:

- Complete timeline of events with dates and descriptions

- All correspondence (emails, letters, notices)

- Financial records showing costs incurred

- Photos or videos of physical defects (boundary issues, encroachments)

- Witness statements if applicable

- Expert opinions (surveys, legal assessments)

Digital copies provide backup protection. Scan all documents and store them securely in cloud storage.

Communication Strategies

Maintain professional, documented communication:

- Always communicate in writing when possible

- Follow up phone conversations with email summaries

- Keep a log of all calls with dates, times, and discussion points

- Request written confirmation of verbal agreements

- Be persistent but professional in follow-ups

- Set calendar reminders for follow-up if you don't receive timely responses

The claims adjuster handles multiple cases. Friendly and caring persistence keeps your claim moving forward without being adversarial.

When to Seek Additional Help

Some title defects are complex enough to warrant professional assistance beyond what the title insurance company provides:

Consider hiring your own attorney when:

- The title company denies your claim and you believe it's covered

- Multiple parties claim ownership rights

- The defect involves significant financial exposure

- You're facing litigation from third parties

- The resolution timeline extends beyond reasonable periods

- You need representation in partition actions or complex title disputes

Property owners facing particularly complicated situations—such as multiple heirs with ownership claims or properties with numerous liens—benefit from expert service provided by companies specializing in complex real estate issues.

Understanding Your Rights as a Policyholder

Title insurance is a contract, and you have specific rights under that agreement:

Your policyholder rights include:

- Right to review: You can review your complete policy and all endorsements

- Right to explanation: The insurer must explain coverage decisions in writing

- Right to appeal: You can challenge claim denials with additional evidence

- Right to legal defense: For covered defects, the company must provide legal representation

- Right to timely response: Insurance regulations require reasonable response times

- Right to file complaints: You can report issues to your state insurance commissioner

Don't hesitate to assert these rights if you feel your claim isn't being handled properly.

The Financial Impact of Title Insurance Claims

Understanding the financial aspects of title insurance claims helps property owners appreciate the value of their coverage and make informed decisions.

Claim Payment Limits and Coverage Amounts

Title insurance policies have maximum coverage limits equal to the property's purchase price (for owner's policies) or loan amount (for lender's policies).

Example coverage scenario:

- Property purchase price: $300,000

- Owner's title insurance coverage: $300,000 maximum

- Discovered undisclosed lien: $45,000

- Title company responsibility: Pay the full $45,000 to clear the lien

If multiple defects exist totaling more than the policy limit, coverage stops at the maximum amount. This is why accurate property valuations at purchase are important.

Cost-Benefit Analysis of Title Insurance

Many property buyers question whether title insurance is worth the cost. Real-world claim statistics demonstrate its value:

Title insurance costs vs. potential exposure:

| Scenario | Title Insurance Premium | Potential Loss Without Coverage | Protection Value |

|---|---|---|---|

| Average home ($300K) | $1,000-$2,000 (one-time) | $5,000-$500,000+ | 250x-500x ROI |

| Undisclosed tax lien | $1,500 premium | $35,000 lien | $33,500 saved |

| Boundary dispute | $1,200 premium | $25,000 legal fees | $23,800 saved |

| Forgery in chain of title | $1,800 premium | $50,000+ legal costs | $48,200+ saved |

Even if you never file a claim, the peace of mind and protection against catastrophic loss make title insurance a valuable investment.

Tax Implications of Title Insurance Claims

When the title insurance company pays to resolve a defect, understanding tax implications is important:

Generally:

- Title insurance claim payments to remove liens or defects are typically not taxable income

- Payments represent restoration of your original property rights, not income

- Legal fees paid by the insurer on your behalf are also not taxable

However:

- If you receive cash settlements exceeding your property basis, consult a tax professional

- Reimbursements for improvements or additions may have different tax treatment

- Keep detailed records of all claim-related financial transactions

Tax situations vary based on individual circumstances. Consult with a qualified tax advisor for guidance specific to your situation.

Preventing Title Issues: Proactive Strategies

While title insurance provides excellent protection, preventing title defects in the first place is ideal. These proactive strategies help property owners avoid title problems.

Thorough Due Diligence Before Purchase

🔍 Pre-purchase investigation steps:

- Order a comprehensive title search – Don't rely solely on the seller's information

- Review the preliminary title report carefully – Read every exception and exclusion

- Hire an independent attorney – Have a real estate lawyer review title documents

- Conduct a professional survey – Verify actual boundaries match legal descriptions

- Research property history – Look for red flags in ownership transfers

- Check for recorded liens – Search county records for judgments, tax liens, and mechanic's liens

For properties with complicated histories—especially inherited properties or those sold through pre-foreclosure—extra diligence is essential.

Working with Reputable Title Companies

Choosing a trustworthy title company significantly impacts your protection:

Qualities of reliable title companies:

- Strong financial ratings (check A.M. Best or similar rating agencies)

- Long operational history in your area

- Positive reviews and references

- Membership in professional organizations (American Land Title Association)

- Clear communication and responsive service

- Comprehensive policy options

- Transparent fee structures

Don't automatically accept the title company suggested by your real estate agent or lender. You have the right to choose your own title company.

Maintaining Clear Property Records

For current property owners, maintaining organized records prevents future complications:

Essential property records to keep:

- Original deed and title insurance policy

- Survey documents and property descriptions

- All property tax records and receipts

- Documentation of improvements and permits

- Easement agreements and restrictions

- Homeowner association documents

- Correspondence regarding property boundaries or rights

Store these documents securely and inform heirs of their location. Proper record-keeping helps future owners avoid title complications.

Special Considerations for Complex Property Situations

Certain property situations create unique title insurance challenges that require specialized knowledge and helpful guidance.

Properties with Multiple Owners or Heirs

When multiple people own property—through inheritance, partnership, or joint purchase—title issues become more complex:

Common complications:

- Disagreements about property use or sale – Different owners may have conflicting goals

- Unknown or missing heirs – Inherited properties may have undiscovered claimants

- Incomplete estate administration – Properties transferred before probate completion

- Tenancy disputes – Confusion about ownership percentages and rights

Title insurance can protect against unknown heir claims, but known ownership disputes typically aren't covered. Property owners dealing with jointly owned property challenges should seek expert guidance early in the process.

Properties with Tax Issues or Government Liens

Government liens create special challenges because they often take priority over other claims:

Title insurance and government liens:

- Property tax liens – Usually discovered in title searches, but older liens may be missed

- Federal tax liens – IRS liens can attach to property without formal recording

- Municipal liens – Unpaid utilities, code violations, or special assessments

- State liens – Various state-level claims against property

While title insurance covers undisclosed government liens, prevention is better. Always verify current tax status before purchasing property. Resources about property tax issues can help property owners understand their obligations and risks.

Commercial vs. Residential Title Insurance Claims

Commercial property title insurance differs from residential coverage in important ways:

Key differences:

| Aspect | Residential | Commercial |

|---|---|---|

| Policy Cost | $1,000-$3,000 typical | $5,000-$50,000+ |

| Coverage Customization | Standard policies common | Highly customized policies |

| Due Diligence | Basic title search | Extensive investigation |

| Claim Complexity | Usually straightforward | Often highly complex |

| Legal Involvement | Sometimes needed | Almost always required |

| Resolution Timeline | 30-90 days typical | 6-18+ months possible |

Commercial property owners should work with title companies experienced in commercial transactions and consider enhanced coverage options.

Working with Title Insurance Professionals

Building effective relationships with title insurance professionals improves claim outcomes and overall property protection.

Questions to Ask Your Title Insurance Company

When purchasing title insurance or filing a claim, ask these important questions:

📝 Before purchasing:

- What specific defects does this policy cover and exclude?

- Are there enhanced coverage options available?

- What is your claims process and typical timeline?

- What is your financial strength rating?

- Can you provide references from recent claimants?

- How do you handle disputes or claim denials?

- What documentation will I need if I file a claim?

📝 When filing a claim:

- What is the expected timeline for investigation and resolution?

- Who will be my primary contact throughout the process?

- What additional documentation do you need from me?

- Will you provide legal representation if needed?

- How will you keep me updated on claim progress?

- What are my options if I disagree with your decision?

- Are there any actions I should avoid while the claim is pending?

Clear communication from the start establishes expectations and prevents misunderstandings.

The Role of Title Agents and Attorneys

Different professionals play important roles in title insurance and claims:

Title Agent/Closer:

- Conducts initial title search

- Coordinates closing process

- Issues title insurance policy

- First point of contact for basic questions

Title Examiner:

- Reviews public records in detail

- Identifies potential title defects

- Prepares title commitment and reports

- Provides technical expertise on title issues

Claims Adjuster:

- Investigates filed claims

- Determines coverage under policy terms

- Coordinates resolution efforts

- Makes claim decisions

Title Attorney:

- Provides legal opinions on title issues

- Represents the company in legal proceedings

- Drafts curative documents

- Handles complex title defects

Understanding these roles helps you direct questions and concerns to the right professional.

When to Consider Alternative Solutions

Sometimes title insurance claims aren't the best or only solution to title problems:

Alternative approaches to consider:

- Direct negotiation – Resolving minor issues directly with the other party

- Quiet title action – Court proceeding to establish clear ownership

- Boundary agreements – Written agreements with neighbors resolving disputes

- Quitclaim deeds – Obtaining releases from parties with questionable claims

- Title curative services – Specialized companies that resolve title defects

Companies like Sure Path Property Solutions specialize in helping property owners navigate complicated title situations, coordinate with counties and title professionals, and find practical solutions when traditional approaches don't fit.

Real-World Timeline: What to Expect During the Claims Process

Understanding realistic timelines helps property owners plan and manage expectations during title insurance claims.

Typical Claims Timeline

Week 1-2: Initial Filing and Acknowledgment

- Submit formal claim with documentation

- Receive acknowledgment from title company

- Claims adjuster assigned to your case

- Initial review of submitted materials

Week 3-6: Investigation Phase

- Title company conducts detailed research

- Additional documentation may be requested

- Public records examined

- Relevant parties contacted for information

- Legal review of coverage and defect

Week 7-10: Evaluation and Decision

- Investigation findings compiled

- Coverage determination made

- Resolution strategy developed

- Decision communicated to policyholder

- Appeal rights explained if claim denied

Week 11+: Resolution Implementation

- Legal actions initiated if necessary

- Negotiations with third parties

- Payment of covered amounts

- Filing of curative documents

- Final resolution and case closure

Total typical timeline: 30-90 days for straightforward claims

Complex claims involving litigation, multiple parties, or significant legal research can extend 6-12 months or longer.

Factors That Accelerate or Delay Claims

⚡ Factors that speed up claims:

- Complete, organized documentation submitted initially

- Clear, undisputed facts

- Cooperative third parties

- Straightforward legal issues

- Responsive communication from all parties

- Simple resolution options available

🐌 Factors that slow down claims:

- Incomplete or missing documentation

- Disputed facts requiring investigation

- Uncooperative third parties

- Complex legal questions

- Multiple parties with conflicting interests

- Need for litigation or court proceedings

- Requests for policy interpretation or legal opinions

Property owners can control some factors (documentation quality, communication responsiveness) but not others (third-party cooperation, legal complexity).

Appealing a Denied Title Insurance Claim

If your title insurance claim is denied, you have options. Don't accept a denial without understanding the reasoning and exploring your rights.

Understanding Denial Reasons

Title insurance companies must provide written explanations for claim denials. Common reasons include:

Policy Exclusions:

- The defect falls under a specific policy exclusion

- Known defects disclosed before purchase

- Issues arising after the policy effective date

- Government actions or regulations

Coverage Limitations:

- The problem doesn't constitute a covered title defect

- The claim exceeds policy limits

- The defect doesn't affect ownership or marketability

Insufficient Evidence:

- Documentation doesn't prove the claimed defect exists

- The defect can't be verified through public records

- Conflicting information requires clarification

Request a detailed written explanation citing specific policy language and the factual basis for denial.

Steps to Appeal a Denial

1. Review the denial letter carefully

- Identify the specific reasons for denial

- Note any policy sections referenced

- Check for factual errors or misunderstandings

2. Gather additional evidence

- Obtain documents that address the denial reasons

- Collect expert opinions (surveys, legal opinions)

- Find supporting precedents or similar cases

3. Submit a formal appeal

- Write a detailed appeal letter addressing each denial reason

- Include new evidence and documentation

- Reference specific policy language supporting coverage

- Request reconsideration based on the additional information

4. Request an independent review

- Ask for review by a different claims adjuster or supervisor

- Suggest mediation if the company offers it

- Consider involving your state insurance department

5. Consult legal counsel

- Hire an attorney experienced in insurance coverage disputes

- Evaluate whether litigation is appropriate

- Understand your legal options and potential outcomes

Regulatory Complaints and Legal Options

If appeals through the insurance company fail, additional options exist:

State Insurance Department Complaint:

- File a formal complaint with your state's insurance regulatory agency

- Provide complete documentation of your claim and denial

- The department may investigate and facilitate resolution

- This process is free and can be effective

Bad Faith Claims:

- If the insurer acted in bad faith (unreasonable denial, failure to investigate properly), you may have legal claims beyond the policy coverage

- Bad faith claims can result in damages beyond policy limits

- Requires strong evidence of improper conduct

- Consult an attorney to evaluate viability

Litigation:

- Filing a lawsuit to enforce coverage under the policy

- Typically a last resort due to time and expense

- May be necessary for significant claims with clear coverage

- Consider arbitration if your policy includes an arbitration clause

Conclusion: Protecting Your Property Rights Through Title Insurance

Understanding Title Insurance Claims: When to File & How the Process Works empowers property owners to protect their most valuable assets. Whether you've discovered an undisclosed lien, faced an ownership dispute, or encountered boundary issues, knowing how to navigate the claims process makes all the difference.

Key actions to take today:

✅ Locate your title insurance policy – Know what coverage you have and keep it accessible

✅ Review your policy coverage – Understand what's covered, excluded, and your rights as a policyholder

✅ Document any title concerns immediately – Don't wait if you discover potential defects

✅ File claims promptly – Contact your title insurance company as soon as issues arise

✅ Maintain organized property records – Keep all documents related to your property ownership

✅ Seek professional guidance for complex situations – Don't navigate complicated title issues alone

For property owners facing particularly challenging situations—multiple heirs, significant liens, clouded titles, or other title problems—professional assistance can provide helpful solutions and trustworthy service.

Title insurance represents more than just a closing cost—it's your financial protection against unknown defects in your property's history. When title problems arise, the claims process provides a clear path to resolution. With proper documentation, timely filing, and persistent follow-through, most title insurance claims result in successful outcomes that protect your property rights and investment.

Remember that you're not alone in this process. Title insurance companies, real estate attorneys, and specialized property solution providers stand ready to offer expert service and helpful guidance. Whether you're purchasing property, have already discovered a title defect, or simply want to understand your coverage better, taking proactive steps today protects your property rights tomorrow.

If you're dealing with complicated real estate issues—back taxes, multiple heirs, liens, judgments, or unclear title—Sure Path Property Solutions offers friendly and caring assistance to help you navigate these challenges. Our industry experts coordinate with counties and title professionals to guide property owners toward clear, practical solutions. Contact us to discuss your specific situation and explore your options.

Your property represents security, investment, and often family legacy. Protecting those rights through proper title insurance coverage and understanding the claims process ensures that unexpected title defects don't derail your ownership or financial stability. Take action today to review your coverage, document your property rights, and prepare yourself to address any title challenges that may arise.