Losing a home to foreclosure is one of the most stressful experiences a property owner can face. Whether you're dealing with unexpected medical bills, job loss, or inherited property with mounting back taxes, understanding the foreclosure timeline in your state can make the difference between losing everything and finding helpful solutions that protect your financial future.

The Foreclosure Timeline by State: Complete Guide to the Process varies dramatically across the United States—from as little as 60 days in some states to over 1,000 days in others. This comprehensive guide breaks down exactly what to expect in each state, how the process works, and what options remain available even when foreclosure seems inevitable.

Key Takeaways

- Foreclosure timelines range from 2 months to over 3 years depending on whether your state uses judicial or non-judicial processes

- Judicial foreclosure states require court involvement and typically take 6-18 months, while non-judicial states can complete the process in 3-6 months

- Pre-foreclosure periods offer critical opportunities to explore alternatives like short sales, deed in lieu, or working with industry experts who specialize in complex property situations

- State-specific redemption rights may allow you to reclaim your property even after the foreclosure sale in certain states

- Understanding your state's specific timeline empowers you to take action before options disappear

Understanding Foreclosure: The Basics Every Homeowner Should Know

Foreclosure is the legal process lenders use to take possession of a property when the borrower fails to make mortgage payments. While the end result is similar across all states, the path to get there varies significantly based on state laws, lending agreements, and individual circumstances.

What Triggers the Foreclosure Process? 🏠

Most lenders don't initiate foreclosure after a single missed payment. The typical sequence looks like this:

30-60 Days Past Due: The lender sends reminder notices and attempts to contact the borrower. Late fees accumulate, but the loan remains in default status rather than foreclosure.

90 Days Past Due: This is the critical threshold. Most lenders can legally begin foreclosure proceedings after three missed payments, though many wait longer to pursue alternatives.

120+ Days Past Due: The formal foreclosure process typically begins. The specific steps from this point forward depend entirely on your state's laws.

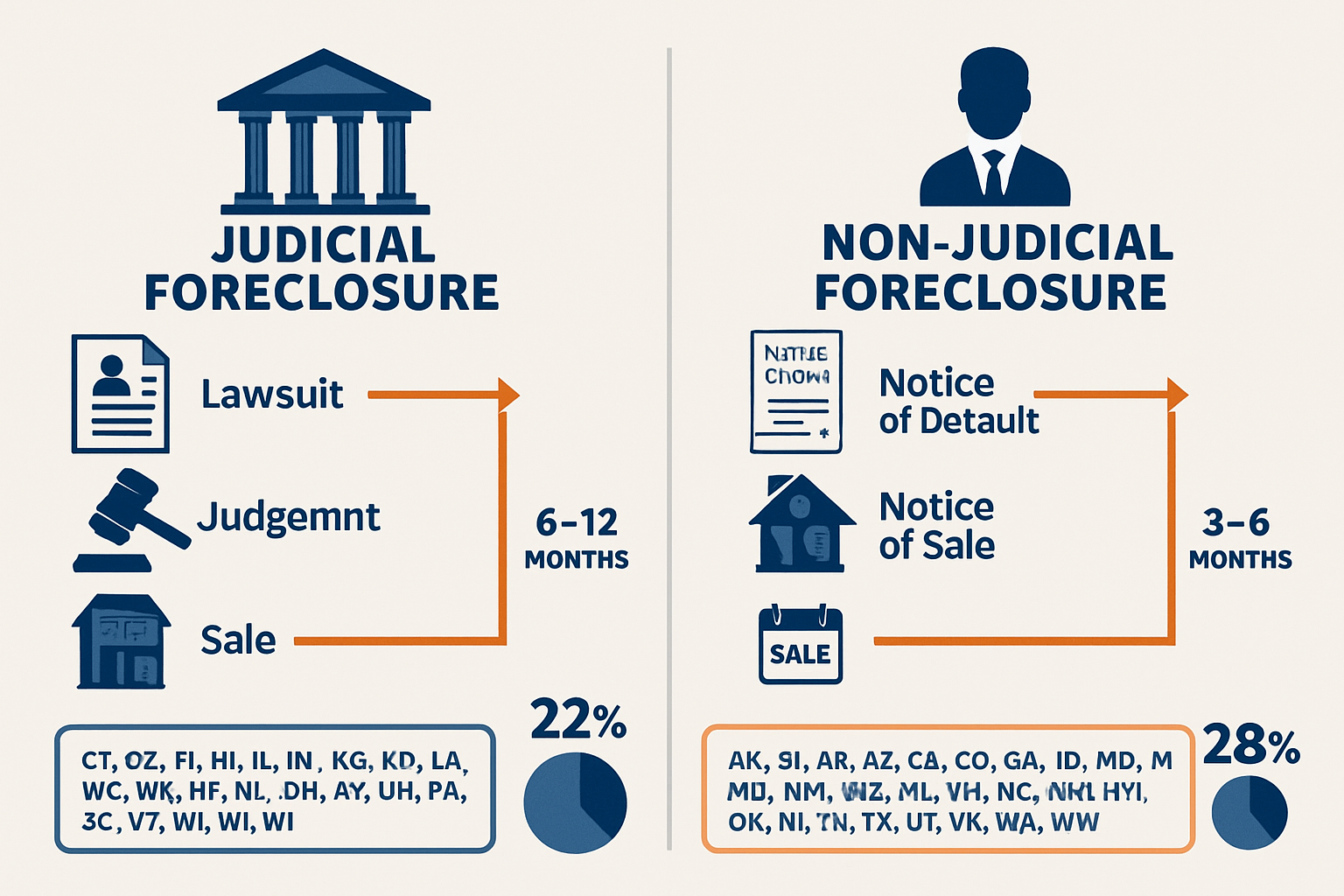

The Two Types of Foreclosure Processes

Understanding whether your state uses judicial or non-judicial foreclosure is essential to knowing your timeline and rights.

Judicial Foreclosure requires the lender to file a lawsuit and obtain a court order before selling the property. This process involves:

- Filing a complaint with the court

- Serving the homeowner with legal notice

- Allowing time for the homeowner to respond

- Court hearings and potential trials

- Judge's ruling and sale authorization

- Public auction

Non-Judicial Foreclosure follows procedures outlined in the mortgage or deed of trust, bypassing the court system. This streamlined process includes:

- Recording a notice of default

- Waiting through a statutory period

- Publishing sale notices

- Conducting a trustee's sale

The difference between these two processes can mean the difference between 4 months and 18 months before losing your home—time that can be used to explore helpful solutions for selling a house with a lien or other alternatives.

Foreclosure Timeline by State: Complete Guide to the Process Variations

The foreclosure timeline varies more than most homeowners realize. Geography isn't just about location—it's about legal protection, procedural requirements, and the time you have to act.

Judicial Foreclosure States: Longer Timelines, More Protections

Twenty-one states primarily use judicial foreclosure, which generally provides homeowners with more time and legal protections. Here's what to expect:

| State | Average Timeline | Key Features |

|---|---|---|

| Connecticut | 62 days | Fastest judicial state; strict mediation program |

| Florida | 135 days | Mandatory mediation available; deficiency judgments allowed |

| Illinois | 300 days | Extended redemption period; strong borrower protections |

| New Jersey | 1,000+ days | Longest foreclosure timeline in the nation; extensive court backlogs |

| New York | 445 days | Settlement conferences required; high legal costs for lenders |

| Ohio | 160 days | Relatively fast for judicial; streamlined court procedures |

| Pennsylvania | 270 days | Court approval required; redemption rights available |

Why Judicial States Take Longer:

The court system adds multiple layers of review and opportunity for homeowners to present defenses. Judges must review documentation, ensure proper notice was given, and verify that the lender has legal standing to foreclose. Court backlogs in states like New Jersey and New York can extend timelines by years.

Non-Judicial Foreclosure States: Faster Process, Fewer Court Protections

Twenty-nine states primarily allow non-judicial foreclosure, which moves much faster but offers fewer opportunities for court intervention:

| State | Average Timeline | Key Features |

|---|---|---|

| Alabama | 60 days | No redemption period; very fast process |

| Arizona | 90 days | 90-day right to cure; no deficiency judgments on primary residences |

| California | 120 days | Strong consumer protections; extensive notice requirements |

| Georgia | 37 days | One of the fastest; minimal state oversight |

| Michigan | 60 days | Statutory redemption period after sale |

| Nevada | 120 days | Mediation program available; notice of default required |

| Texas | 27 days | Fastest foreclosure state; 21-day notice requirement |

| Washington | 120 days | Beneficiary must prove right to foreclose |

The Speed Factor:

In states like Texas and Georgia, the entire process from first notice to auction can happen in less than two months. This compressed timeline makes it absolutely critical to act quickly when facing financial difficulties.

"Understanding your state's foreclosure timeline isn't just about knowing when you might lose your home—it's about recognizing the window of opportunity you have to explore alternatives." – Real Estate Legal Experts

The Complete Foreclosure Timeline: Stage-by-Stage Breakdown

Regardless of your state, foreclosure follows a predictable pattern. Understanding each stage helps you identify where you are in the process and what actions remain available.

Stage 1: Pre-Foreclosure (30-120 Days)

This is the most critical period for homeowners. You're behind on payments, but foreclosure hasn't officially started.

What Happens:

- Lender sends demand letters and default notices

- Phone calls and attempts to arrange payment plans

- Loan officially enters default status

- Credit score begins to decline

Your Options During Pre-Foreclosure:

This stage offers the most flexibility. Property owners can:

- Negotiate a loan modification with reduced payments or extended terms

- Arrange a repayment plan to catch up on missed payments

- Explore a short sale where the lender agrees to accept less than owed

- Consider a deed in lieu of foreclosure to avoid the foreclosure record

- Sell the property quickly to an investor or cash buyer

Many homeowners don't realize they can sell their house in pre-foreclosure, often with enough proceeds to pay off the loan and avoid foreclosure entirely. This is where expert service from professionals who understand complex property situations becomes invaluable.

Stage 2: Notice of Default or Lis Pendens Filing (Day 1 of Official Foreclosure)

The official foreclosure begins when the lender files the appropriate legal notice.

Non-Judicial States: The lender records a Notice of Default (NOD) with the county recorder's office. This public document starts the foreclosure clock.

Judicial States: The lender files a Lis Pendens (notice of pending lawsuit) and a foreclosure complaint with the court. You'll be served with legal papers.

Timeline Impact:

- Non-judicial: 30-120 days from NOD to sale

- Judicial: 90-365+ days from filing to sale

Critical Actions:

This is your formal notification. Ignoring it won't make it go away. Instead:

- Respond to legal notices within the specified timeframe (usually 20-30 days)

- Consult with an attorney to understand your defenses

- Contact your lender to discuss alternatives

- Explore selling options while you still have time

Stage 3: Pre-Foreclosure Sale Period (Varies by State)

After the initial notice, there's a waiting period before the property can be sold.

What Happens:

- Reinstatement period: Time to pay all past-due amounts plus fees to stop foreclosure

- Publication of sale notices: The foreclosure sale must be advertised publicly

- Acceleration of the loan: The entire loan balance becomes due immediately

- Property inspections: The lender may inspect or appraise the property

State-Specific Variations:

Some states require extensive waiting periods:

- California: 111 days minimum from NOD to sale

- Texas: 21 days from posting notice to sale

- Florida: 20 days from final judgment to sale

Opportunities Still Available:

Even at this stage, helpful solutions exist:

- Cash sales to investors who can close quickly

- Short sale approval if you have a qualified buyer

- Bankruptcy filing to trigger automatic stay (temporary halt)

- Loan modification approval if your financial situation has improved

Stage 4: Foreclosure Auction (The Sale Date)

The property is sold at public auction, typically on the courthouse steps or at a designated location.

How Auctions Work:

- Opening bid: Usually set at the loan balance plus fees and costs

- Public bidding: Anyone can bid, though most sales go to the lender

- Highest bidder wins: Sale is typically final and immediate

- Payment required: Winners must pay immediately or within 24 hours

What Happens to the Homeowner:

In most states, ownership transfers immediately to the winning bidder. However, some states provide a redemption period after the sale.

Last-Minute Options:

Even on auction day, sales can be stopped by:

- Full payment of the entire loan balance plus costs

- Bankruptcy filing before the gavel falls

- Sale postponement negotiated with the lender

- Procedural errors discovered in the foreclosure process

Stage 5: Post-Foreclosure and Eviction (0-12 Months After Sale)

After the auction, the timeline for vacating the property varies significantly.

States With Redemption Periods:

Some states allow former owners to reclaim their property by paying the full sale price plus interest:

- Alabama: 12 months (or 6 months if property is abandoned)

- Kansas: 12 months (3 months for agricultural land)

- Michigan: 6 months for properties over 3 acres; 30 days otherwise

- Iowa: 20 days to 1 year depending on circumstances

During the redemption period, you may be able to remain in the property, though this varies by state.

States Without Redemption Periods:

In most non-judicial states, ownership transfers immediately at sale. The new owner must then:

- Serve eviction notice: Typically 3-30 days depending on state law

- File unlawful detainer: If you don't vacate voluntarily

- Obtain court order: Sheriff enforces eviction

- Physical removal: Usually 30-90 days from sale to forced eviction

Cash for Keys Programs:

Many lenders and new owners offer "cash for keys" incentives—paying you to vacate peacefully and leave the property in good condition. These payments range from $500 to $5,000.

State-by-State Foreclosure Timeline Reference Guide

Understanding the Foreclosure Timeline by State: Complete Guide to the Process requires knowing the specifics for your location. Here's a comprehensive breakdown:

Fastest Foreclosure States ⚡

These states can complete foreclosure in under 90 days:

1. Texas (27 days)

- Process: Non-judicial

- Notice requirement: 21 days

- No right of redemption

- No deficiency judgment restrictions

2. Georgia (37 days)

- Process: Non-judicial

- Notice requirement: 30 days

- No right of redemption

- Deficiency judgments allowed

3. Alabama (60 days)

- Process: Non-judicial

- Notice requirement: 30 days

- 12-month redemption period after sale

- Deficiency judgments allowed

4. Michigan (60 days)

- Process: Non-judicial

- Notice requirement: 30 days

- 6-month redemption period (varies by property type)

- Deficiency judgments restricted

5. Minnesota (60 days)

- Process: Non-judicial

- Notice requirement: 30 days

- 6-month redemption period

- Strict foreclosure procedures

Slowest Foreclosure States 🐌

These states take 12+ months on average:

1. New Jersey (1,000+ days)

- Process: Judicial

- Extensive court backlogs

- Mandatory settlement conferences

- Strong borrower protections

2. New York (445 days)

- Process: Judicial

- Settlement conferences required

- Complex legal procedures

- High legal costs for lenders

3. Florida (135-180 days with delays)

- Process: Judicial

- Mediation programs available

- Court backlogs in some counties

- Deficiency judgments allowed

4. Illinois (300 days)

- Process: Judicial

- Extended redemption rights

- Strict notice requirements

- Strong consumer protections

5. Pennsylvania (270 days)

- Process: Judicial

- Court approval required

- Redemption period available

- Extensive legal procedures

Mid-Range States (90-180 Days)

Most states fall into this category, balancing lender rights with homeowner protections:

- Arizona: 90 days (non-judicial)

- California: 120 days (non-judicial with strong consumer protections)

- Colorado: 125 days (non-judicial)

- Nevada: 120 days (non-judicial with mediation)

- Ohio: 160 days (judicial)

- Washington: 120 days (non-judicial)

Special Circumstances That Affect Foreclosure Timelines

Several factors can extend or accelerate the standard foreclosure timeline in any state.

Bankruptcy Protection 📋

Filing for bankruptcy triggers an automatic stay that immediately halts foreclosure proceedings.

Chapter 7 Bankruptcy:

- Provides 3-6 months of temporary relief

- Doesn't eliminate mortgage debt

- Delays but doesn't prevent foreclosure

- Useful for buying time to arrange alternatives

Chapter 13 Bankruptcy:

- Creates a 3-5 year repayment plan

- Can cure mortgage arrears over time

- Stops foreclosure if payments are maintained

- Allows you to keep the property while catching up

Servicemember Protections (SCRA)

The Servicemembers Civil Relief Act provides special protections for active-duty military:

- Foreclosure stay: Court must approve foreclosure during active duty plus 9 months

- Interest rate caps: 6% maximum on pre-service debts

- Extended timelines: Additional procedural requirements

- Eviction protections: Enhanced notice requirements

COVID-19 Related Protections (2025 Update)

While most pandemic-era foreclosure moratoriums have ended, some protections remain:

- Loss mitigation requirements: Lenders must evaluate alternatives before foreclosing

- Extended timelines: Many states still have backlogged courts from moratorium periods

- Special programs: Some states offer foreclosure prevention programs funded by federal relief

Contested Foreclosures and Legal Defenses

Homeowners who challenge the foreclosure can significantly extend timelines:

Common defenses include:

- Improper notice: Lender didn't follow required procedures

- Lack of standing: Lender can't prove they own the loan

- Predatory lending: Original loan violated consumer protection laws

- Servicer errors: Payments were misapplied or lost

- Dual tracking: Lender pursued foreclosure while considering modification

Successful defenses can add 6-24 months to the timeline, and in some cases result in loan modifications or settlements.

Properties With Multiple Owners or Title Issues

Properties with complex ownership situations face additional complications:

- Inherited properties: Multiple heirs must be notified

- Joint ownership: All owners must be properly served

- Clouded titles: Title problems must be resolved before sale

- Liens and judgments: Multiple liens complicate the foreclosure process

These situations often require expert service from professionals who specialize in untangling complex property issues.

Your Options During Each Stage of Foreclosure

No matter where you are in the foreclosure timeline, options exist. The key is acting quickly and getting helpful guidance from industry experts.

Pre-Foreclosure Options (Maximum Flexibility) 💡

1. Loan Modification

Work with your lender to modify loan terms:

- Lower interest rate

- Extended repayment period

- Principal forbearance

- Capitalization of arrears

Success rate: Moderate to high if you can demonstrate financial hardship and ability to make modified payments.

2. Repayment Plan

Arrange to pay current mortgage plus a portion of arrears:

- Typically 3-12 month plans

- Requires proof of income

- Brings loan current over time

- Avoids foreclosure record

Success rate: High if you have steady income and the arrears aren't too large.

3. Short Sale

Sell the property for less than the mortgage balance with lender approval:

- Avoids foreclosure on credit report

- Lender forgives deficiency (usually)

- Requires qualified buyer

- Takes 60-120 days typically

Learn more about the short sale process and whether it's right for your situation.

Success rate: Moderate; depends on market conditions and lender cooperation.

4. Deed in Lieu of Foreclosure

Voluntarily transfer the property to the lender:

- Faster than foreclosure

- Less damage to credit

- Lender may forgive deficiency

- No sale process required

Understanding the deed in lieu process can help you negotiate better terms.

Success rate: Moderate; lenders prefer this to foreclosure but have specific requirements.

5. Sell to a Cash Buyer or Investor

Sell quickly to avoid foreclosure:

- Close in 7-30 days

- No repairs needed

- Pay off mortgage

- Avoid foreclosure damage to credit

This is often the best solution for properties with back taxes, liens, or title issues. Companies like Sure Path Property Solutions specialize in these complex situations, providing trustworthy service when traditional sales aren't possible.

Success rate: High if you have equity or if a specialized buyer can work with your situation.

During Active Foreclosure (Limited but Real Options)

1. Reinstatement

Pay all past-due amounts plus fees:

- Stops foreclosure immediately

- Loan returns to normal status

- Requires lump sum payment

- Available until sale date in most states

2. Redemption (Post-Sale in Some States)

Buy back the property after foreclosure sale:

- Pay full sale price plus interest

- Only available in redemption states

- Typically 6-12 months after sale

- Requires significant funds

3. Bankruptcy Filing

Stop foreclosure through automatic stay:

- Immediate halt to proceedings

- Chapter 13 allows catch-up plan

- Buys time for alternatives

- Requires attorney assistance

4. Challenge the Foreclosure

Contest the foreclosure in court:

- Requires valid legal defense

- Extends timeline significantly

- May result in settlement

- Needs experienced attorney

Post-Foreclosure Options (Damage Control)

1. Negotiate Cash for Keys

Accept payment to vacate peacefully:

- Typically $500-$5,000

- Avoids eviction on record

- Provides moving funds

- Leaves property in good condition

2. Request Extended Move-Out Time

Negotiate additional time before eviction:

- Usually 30-90 days

- Helps with relocation planning

- Maintains better relationship

- Avoids forced eviction

3. Credit Repair and Rebuilding

Focus on financial recovery:

- Foreclosure stays on credit 7 years

- Impact decreases over time

- Rebuild with secured credit

- Maintain other accounts in good standing

How to Take Action: Steps to Protect Yourself Today

Understanding the Foreclosure Timeline by State: Complete Guide to the Process is only valuable if you act on that knowledge. Here's your action plan:

Step 1: Determine Where You Are in the Process 📍

Ask yourself:

- How many payments have you missed?

- Have you received a Notice of Default or legal filing?

- Has a sale date been set?

- What is the foreclosure process in your state?

Get documentation:

- Pull your mortgage statement

- Request a payoff statement from your lender

- Gather any legal notices you've received

- Check county records for filed documents

Step 2: Calculate Your Equity Position

Determine your property's value:

- Get a professional appraisal

- Check recent comparable sales

- Use online valuation tools (Zillow, Redfin)

- Consider current market conditions

Calculate your equity:

Current Market Value – Mortgage Balance – Liens – Selling Costs = Equity

If you have equity, selling is usually the best option. If you're underwater (owe more than it's worth), you'll need lender cooperation for a short sale or deed in lieu.

Step 3: Understand Your State's Specific Timeline

Use this guide to determine:

- How much time you have before sale

- Whether you have redemption rights

- What notice requirements apply

- What defenses might be available

Critical state-specific factors:

- Judicial vs. non-judicial process

- Average timeline in your state

- Redemption period (if any)

- Deficiency judgment rules

Step 4: Explore All Available Options

Contact your lender immediately:

- Request loss mitigation department

- Ask about modification programs

- Inquire about repayment plans

- Document all conversations

Consult with professionals:

- Real estate attorney: Understand your legal rights and defenses

- HUD-approved housing counselor: Free foreclosure prevention counseling

- Real estate investor or cash buyer: Quick sale options for complex situations

- Bankruptcy attorney: If bankruptcy might help

For properties with complicated situations—multiple owners, inherited property, liens, judgments, or title problems—working with specialists who understand these challenges is essential. Sure Path Property Solutions provides friendly and caring guidance through exactly these types of complex property situations.

Step 5: Make a Decision and Act Quickly ⚡

Time is your most valuable asset. The earlier in the process you act, the more options you have.

Create a decision timeline:

- Week 1: Gather information and documentation

- Week 2: Consult with professionals and explore options

- Week 3: Make a decision on your path forward

- Week 4: Begin implementation

Don't wait for:

- "The perfect solution" that may not exist

- Your financial situation to magically improve

- The lender to offer you something

- The foreclosure to "just go away"

Common Foreclosure Myths Debunked

Misinformation about foreclosure can lead to poor decisions. Let's clear up some common misconceptions:

Myth 1: "The Bank Wants My House"

Reality: Banks are in the lending business, not the property ownership business. Foreclosure costs lenders tens of thousands of dollars in legal fees, lost interest, property maintenance, and selling costs. They'd much rather work out an alternative.

Myth 2: "I Can't Sell Once Foreclosure Starts"

Reality: You can sell your property at any point before the foreclosure sale is finalized. In fact, selling during pre-foreclosure is often the best option if you have equity or can find a buyer who specializes in these situations.

Myth 3: "Bankruptcy Will Save My House"

Reality: Bankruptcy can delay foreclosure and provide time to catch up on payments through Chapter 13, but it doesn't eliminate your mortgage debt. If you can't afford the payments long-term, bankruptcy only postpones the inevitable.

Myth 4: "Foreclosure Only Takes a Few Months Everywhere"

Reality: As this guide shows, foreclosure timelines range from 27 days in Texas to over 1,000 days in New Jersey. Your state's process makes an enormous difference in how much time you have to act.

Myth 5: "Walking Away Is My Only Option"

Reality: Even in difficult situations, alternatives exist. Short sales, deeds in lieu, loan modifications, and selling to investors who handle complex properties all provide better outcomes than simply abandoning your property.

Myth 6: "I'll Owe the Difference After Foreclosure"

Reality: This depends on your state's deficiency judgment laws. Some states prohibit deficiency judgments entirely, while others allow lenders to pursue you for the difference between the sale price and what you owed. Understanding your state's rules is critical.

The Emotional Side of Foreclosure: You're Not Alone

Facing foreclosure is emotionally devastating. It's not just about losing a house—it's about losing your home, your sense of security, and often your sense of self-worth.

Common Feelings During Foreclosure

- Shame and embarrassment: Feeling like you've failed

- Anxiety and stress: Constant worry about the future

- Anger: At yourself, the lender, or your circumstances

- Denial: Hoping the problem will resolve itself

- Depression: Feeling hopeless and overwhelmed

These feelings are normal. Millions of Americans have faced foreclosure, including during the 2008 financial crisis and the COVID-19 pandemic. Financial hardship can happen to anyone due to job loss, medical bills, divorce, or unexpected expenses.

Taking Care of Yourself

Practical self-care during foreclosure:

- Seek support: Talk to friends, family, or a counselor

- Stay informed: Knowledge reduces anxiety

- Take action: Even small steps help you regain control

- Be kind to yourself: This is a situation, not a character flaw

- Focus on solutions: Channel energy into productive options

Getting Professional Support

Resources available:

- HUD-approved housing counselors: Free, confidential foreclosure prevention counseling

- Legal aid organizations: Free or low-cost legal assistance

- Mental health professionals: Support for stress and anxiety

- Financial counselors: Help with budgeting and planning

Working with professionals who provide helpful guidance and treat you with respect makes an enormous difference. The right partners understand that you're facing a difficult situation and focus on finding practical solutions rather than judgment.

Foreclosure's Impact on Your Credit and Future

Understanding the long-term consequences helps you make informed decisions about your options.

Credit Score Impact 📊

Foreclosure's effect on credit:

- Immediate drop: 250-400 points typically

- Duration on report: 7 years from the first missed payment

- Declining impact: Effect diminishes over time

- Other factors matter: Payment history on other accounts affects recovery

Comparison to alternatives:

- Foreclosure: Largest negative impact

- Short sale: Slightly less damaging

- Deed in lieu: Similar to short sale

- Loan modification: Minimal impact if you stay current

- Selling before foreclosure: No foreclosure on record

Future Homeownership Timeline

Waiting periods for new mortgages after foreclosure:

- Conventional loans: 7 years (3 years with extenuating circumstances)

- FHA loans: 3 years

- VA loans: 2 years

- USDA loans: 3 years

Shorter waiting periods apply if you:

- Can document extenuating circumstances (job loss, medical emergency)

- Have rebuilt excellent credit

- Make a larger down payment

- Work with specialized lenders

Financial Recovery Strategies

Rebuilding after foreclosure:

- Maintain other credit accounts: Keep credit cards and other loans current

- Build emergency fund: Prevent future financial crises

- Use secured credit cards: Rebuild credit history

- Monitor credit reports: Ensure accuracy and track progress

- Create a budget: Prevent future financial problems

Timeline for recovery:

- Year 1: Focus on stabilization and basic credit rebuilding

- Years 2-3: Credit score begins recovering; some loan options available

- Years 4-7: Continued improvement; more loan options open

- Year 7+: Foreclosure removed from credit report

Working With Professionals: When and How to Get Help

Navigating foreclosure alone is difficult and often leads to missed opportunities. The right professional help can make the difference between disaster and a manageable outcome.

When to Hire a Foreclosure Attorney

Consider legal representation if:

- You believe the lender made procedural errors

- You have valid defenses to foreclosure

- You're in a judicial foreclosure state

- The property has significant equity

- You're considering bankruptcy

- You've been served with legal papers

What attorneys can do:

- Review foreclosure documents for errors

- File answers and defenses in court

- Negotiate with lenders on your behalf

- Represent you at hearings

- Explore all legal options

- Protect your rights throughout the process

Costs: $1,500-$5,000 typically, though some work on payment plans or contingency.

HUD-Approved Housing Counselors

Free services include:

- Foreclosure prevention counseling

- Budget analysis

- Communication with lenders

- Explanation of options

- Application assistance for programs

- Ongoing support

Find a counselor: Visit HUD.gov or call 1-800-569-4287

Real Estate Professionals for Complex Situations

When traditional real estate agents can't help—due to liens, title issues, back taxes, or time constraints—specialized property buyers provide helpful solutions.

Look for professionals who:

- Have experience with foreclosure situations

- Understand complex title issues

- Can close quickly (7-30 days)

- Provide fair, transparent offers

- Explain all your options honestly

- Treat you with respect and dignity

Sure Path Property Solutions specializes in exactly these challenging situations, helping property owners navigate complicated real estate issues with expert service and a commitment to finding solutions that work for your specific circumstances. Whether you're dealing with inherited property, judgment liens, or other challenges, working with industry experts who understand these complexities makes the process manageable.

Questions to Ask Any Professional

Before hiring anyone, ask:

- What experience do you have with foreclosure situations?

- What are all my options, including ones you don't provide?

- What are your fees, and when are they due?

- Can you provide references or testimonials?

- What's the realistic timeline for my situation?

- What's the best-case and worst-case outcome?

- How will you communicate with me throughout the process?

Red flags to avoid:

- Pressure to make immediate decisions

- Requests for upfront fees before services

- Promises that sound too good to be true

- Lack of transparency about the process

- No verifiable credentials or references

- Discouraging you from seeking other opinions

Preventing Foreclosure: Proactive Strategies for Homeowners

The best way to handle foreclosure is to prevent it from starting. Even if you're currently facing foreclosure, these strategies can help prevent future problems.

Early Warning Signs of Financial Trouble 🚨

Act immediately if you notice:

- Consistently living paycheck to paycheck

- Using credit cards for basic expenses

- Skipping or delaying mortgage payments

- Ignoring bills or collection notices

- Depleting savings to make payments

- Taking on additional debt to pay existing debt

Proactive Communication With Your Lender

Don't wait until you've missed payments:

- Contact your lender at the first sign of trouble

- Explain your situation honestly

- Ask about hardship programs

- Request forbearance if needed

- Document all conversations

- Follow up in writing

Lenders appreciate proactive borrowers and are more likely to work with you if you contact them before missing payments rather than after.

Building Financial Resilience

Long-term strategies:

- Emergency fund: Save 3-6 months of expenses

- Budget discipline: Track spending and cut unnecessary expenses

- Income diversification: Develop multiple income streams

- Insurance coverage: Protect against job loss, disability, and illness

- Debt reduction: Pay down high-interest debt aggressively

- Regular financial reviews: Assess your situation quarterly

Understanding Your Mortgage Terms

Know these critical details:

- Exact payment amount and due date

- Grace period before late fees

- Prepayment penalties (if any)

- Escrow account details

- Contact information for servicer

- Process for reporting hardship

Conclusion: Taking Control of Your Foreclosure Timeline

The Foreclosure Timeline by State: Complete Guide to the Process reveals one critical truth: time is your most valuable asset. Whether you have 27 days in Texas or 1,000+ days in New Jersey, every day matters when you're facing foreclosure.

Understanding your state's specific process, timeline, and your rights empowers you to make informed decisions rather than reactive ones. Foreclosure isn't inevitable—even after it starts, options exist at every stage.

Your Next Steps Today

Don't wait another day. Take these immediate actions:

- Determine exactly where you are in your state's foreclosure process

- Calculate your equity position to understand your options

- Contact your lender to discuss alternatives

- Consult with professionals who specialize in your situation

- Make a decision and begin taking action

Remember: Acting early provides more options, better outcomes, and less stress. Whether you choose to fight the foreclosure, negotiate with your lender, or sell the property, taking control of the process is better than letting it control you.

Get Expert Help for Complex Situations

If your property has complications—back taxes, liens, judgments, multiple owners, or unclear title—you need professionals who specialize in these exact challenges. Contact Sure Path Property Solutions for a free, no-obligation consultation about your specific situation.

The team provides helpful guidance through complex property issues, working with counties and title professionals to find practical solutions. With friendly and caring service, they help property owners navigate even the most challenging situations with confidence.

Final Thoughts

Foreclosure is one of life's most stressful experiences, but it's not the end of your financial future. Millions of Americans have faced foreclosure and recovered to become homeowners again. With the right information, professional support, and timely action, you can minimize the damage and move forward toward a stronger financial future.

The foreclosure timeline in your state determines how much time you have to act—but only you can decide to use that time wisely. Don't let fear, shame, or uncertainty paralyze you into inaction. Reach out for help, explore your options, and take control of your situation today.

Your home and your financial future are worth fighting for. 💪🏠

Sure Path is a family-owned, curative-title cash buyer. We handle the paperwork and pay what’s owed at closing — no fees, no repairs, no pressure.