Imagine opening your mailbox to find your property tax assessment, only to discover your home is now worth $80,000 less than what you owe on your mortgage. Your stomach drops. You're not alone—thousands of homeowners across America face this exact situation in 2025, trapped in what's known as an "underwater" or "upside-down" mortgage. The good news? Underwater Mortgage Options: What to Do When You Owe More Than It's Worth exist, and understanding them can be your first step toward financial freedom.

When you owe more on your mortgage than your property is currently worth, it creates a challenging situation called negative equity. This predicament can feel overwhelming, especially if you're facing additional complications like back taxes, liens, or the need to sell quickly. However, with the right information and helpful guidance, you can navigate these troubled waters and find a path forward.

Key Takeaways

- Negative equity occurs when your mortgage balance exceeds your home's current market value, creating an underwater mortgage situation that affects millions of homeowners in 2025

- Multiple solutions exist including short sales, loan modifications, refinancing programs, deed in lieu of foreclosure, and strategic default—each with distinct advantages and consequences

- Government programs like HARP successors and FHA Streamline Refinancing may offer relief even when traditional refinancing isn't available

- Staying in your home and waiting for market recovery can be a viable long-term strategy if you can afford payments and don't need to sell immediately

- Professional guidance from industry experts is essential when navigating complex situations involving liens, judgments, or title issues alongside negative equity

Understanding Underwater Mortgages and Negative Equity

What Does "Underwater" Really Mean?

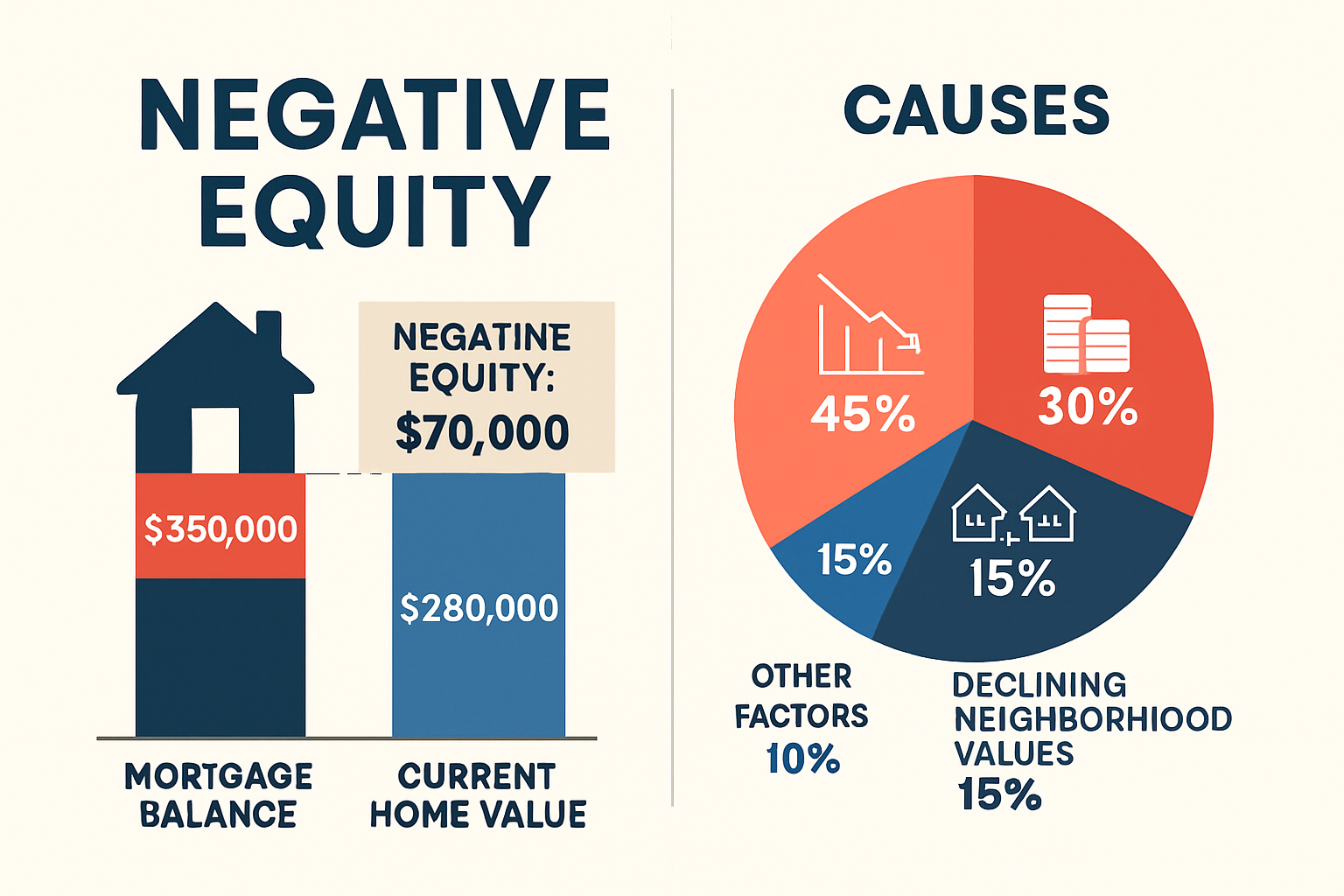

An underwater mortgage exists when the outstanding loan balance exceeds the current fair market value of the property. Think of it like a boat taking on water—the debt weighs more than the asset itself.

Here's a simple example:

- Original purchase price: $400,000

- Current mortgage balance: $375,000

- Current market value: $320,000

- Negative equity: $55,000 underwater

This $55,000 gap represents money you would need to bring to closing if you sold the property today, making traditional sales extremely difficult.

How Homeowners End Up Underwater

Several factors can push a mortgage underwater:

Market Conditions 🏘️

- Economic downturns causing widespread property devaluation

- Local market crashes due to industry closures or population shifts

- Oversupply of housing inventory in specific areas

- Rising interest rates reducing buyer purchasing power

Individual Circumstances

- Purchasing with minimal down payment (3-5%)

- Taking out second mortgages or home equity lines

- Buying at market peak prices

- Property damage or neglect reducing home value

- Neighborhood decline affecting comparable sales

Financial Complications

- Accumulating back taxes that create additional liens

- Judgment liens from lawsuits adding to total debt

- Mechanics liens from unpaid contractor work

- Multiple owners disagreeing on property maintenance investments

The Real Impact of Being Underwater

Being underwater doesn't just affect your ability to sell. It creates a ripple effect across your financial life:

Limited Mobility 🚫

You're essentially trapped in the property. Job opportunities in other cities become impossible to pursue without taking a significant financial loss.

Refinancing Challenges

Most traditional refinancing requires at least 20% equity. With negative equity, you're locked into your current interest rate, even if rates drop significantly.

Psychological Stress

The mental burden of owing more than you own creates anxiety, especially when combined with other financial pressures like medical bills or job loss.

Credit Implications

While simply being underwater doesn't hurt your credit, the decisions you make to resolve the situation certainly can.

Comprehensive Underwater Mortgage Options: What to Do When You Owe More Than It's Worth

When facing negative equity, homeowners have several paths forward. Each option carries different implications for your finances, credit, and future. Let's explore the most effective solutions available in 2025.

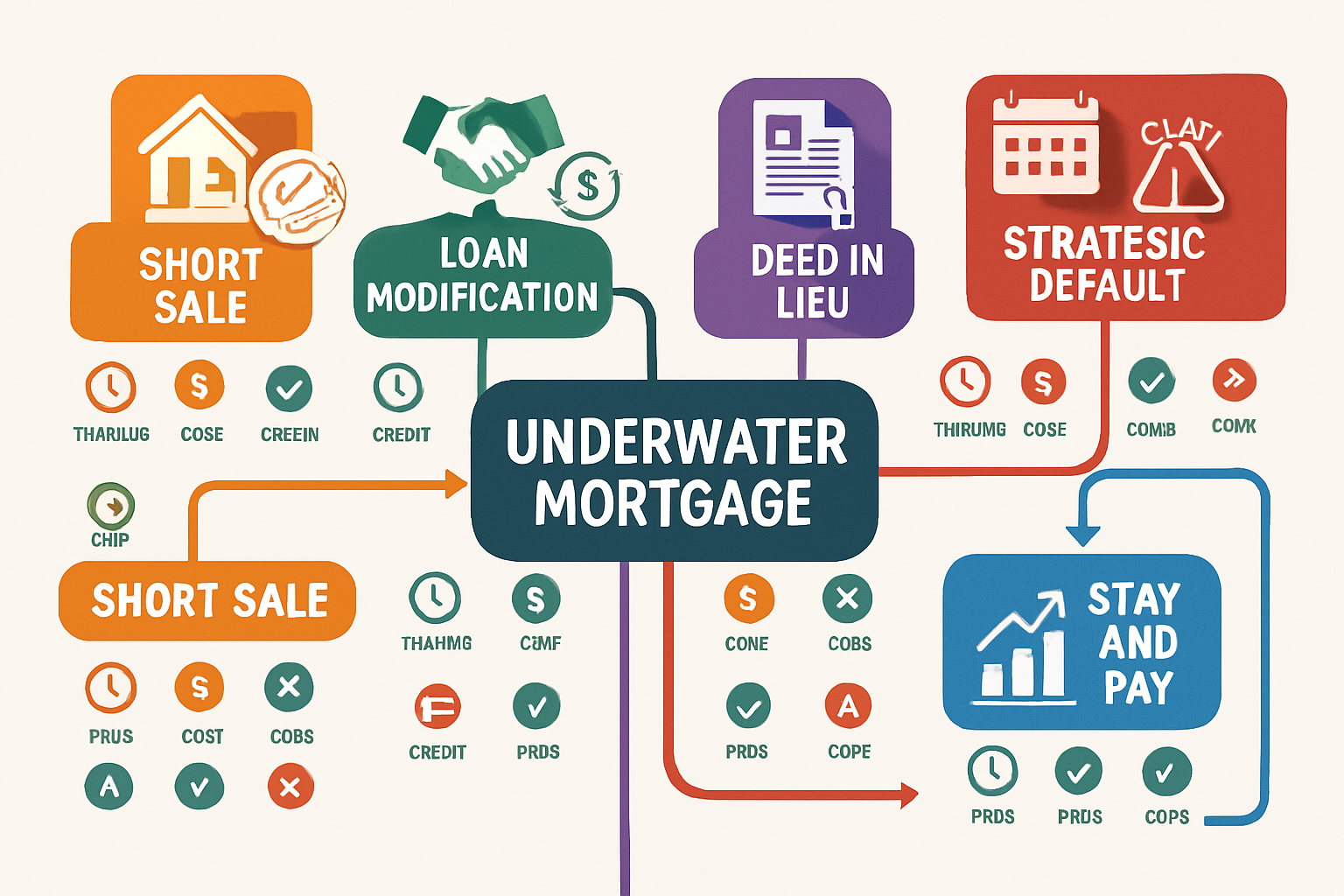

Option 1: Short Sale Solutions

A short sale allows you to sell your property for less than the mortgage balance, with the lender agreeing to accept the proceeds as full or partial satisfaction of the debt.

How Short Sales Work:

- Lender Approval Process – You must demonstrate financial hardship and inability to continue payments

- Property Listing – The home goes on the market at current value, not loan balance

- Offer Negotiation – When an offer arrives, it's submitted to the lender for approval

- Lender Decision – The bank reviews whether accepting less money makes more sense than foreclosure

- Closing – If approved, the sale proceeds, and the lender releases the lien

Advantages of Short Sales:

- ✅ Avoids foreclosure on your credit report

- ✅ Less damaging to credit scores than foreclosure (typically 100-150 point drop vs. 200-300)

- ✅ Shorter waiting period for future mortgages (2-3 years vs. 7 years)

- ✅ Potential for lender to forgive deficiency balance

- ✅ More control over the sale process and timing

Disadvantages to Consider:

- ❌ Still damages credit significantly

- ❌ Lengthy approval process (3-6 months average)

- ❌ No guarantee lender will approve

- ❌ Possible tax consequences on forgiven debt

- ❌ Requires financial hardship documentation

For homeowners dealing with pre-foreclosure situations, short sales often provide the best alternative. The process requires patience and expert service to navigate successfully.

Expert Insight: "Short sales work best when homeowners act early, before missing multiple payments. Lenders are more cooperative when they see proactive problem-solving rather than reactive crisis management."

Option 2: Loan Modification Programs

Loan modifications permanently change the terms of your existing mortgage to make payments more affordable and help you keep your home.

Types of Modifications Available:

Interest Rate Reduction

Your lender lowers your interest rate, reducing monthly payments without changing the principal balance. This works particularly well if you obtained your original loan during a high-rate period.

Term Extension

The loan term extends from 30 years to 40 years, spreading payments over a longer period. While you'll pay more interest overall, monthly obligations decrease significantly.

Principal Forbearance

A portion of your principal is set aside at 0% interest, due when you sell or refinance. This immediately reduces your monthly payment calculation.

Principal Reduction (Rare)

In exceptional cases, lenders may reduce the actual amount owed. This is uncommon but became more prevalent during the 2008 crisis and occasionally appears in 2025 programs.

Qualification Requirements:

- Demonstrated financial hardship (job loss, medical emergency, divorce)

- Sufficient income to afford modified payments

- Property is your primary residence

- Loan originated before specific dates (varies by program)

- No recent bankruptcy filings

The Application Process:

- Contact Your Servicer – Reach out before missing payments if possible

- Submit Hardship Letter – Explain your situation clearly and honestly

- Provide Documentation – Pay stubs, tax returns, bank statements, hardship proof

- Review Trial Period – Make modified payments for 3-6 months

- Permanent Modification – If successful, new terms become permanent

Pros and Cons:

| Advantages | Disadvantages |

|---|---|

| Keep your home | Doesn't reduce principal (usually) |

| Avoid foreclosure | Lengthy application process |

| Lower monthly payments | Not guaranteed approval |

| Minimal credit impact | May extend total interest paid |

| Maintain homeownership | Requires financial hardship proof |

Option 3: Refinancing Programs for Underwater Mortgages

Despite being underwater, certain specialized refinancing programs can help you secure better terms or lower payments.

HARP Successor Programs (2025)

While the original Home Affordable Refinance Program (HARP) ended in 2018, several lenders offer similar "high loan-to-value" refinancing options for underwater borrowers with government-backed loans.

Eligibility Criteria:

- Current on mortgage payments (no late payments in past 6 months)

- Loan owned or guaranteed by Fannie Mae or Freddie Mac

- Originated before specific cutoff dates

- Property is primary residence, second home, or investment property

- No maximum loan-to-value ratio in some cases

FHA Streamline Refinance

For borrowers with existing FHA loans, streamline refinancing offers a simplified process:

- No appraisal required in most cases

- No income verification needed

- No credit check for some borrowers

- Must demonstrate net tangible benefit (lower payment or more stable loan)

VA Interest Rate Reduction Refinance Loan (IRRRL)

Veterans with existing VA loans can refinance underwater mortgages through this program:

- No appraisal or income verification required

- Can refinance up to 100% of home value plus closing costs

- Must result in lower interest rate

- Funding fee can be financed into loan

Conventional Refinancing Considerations:

Traditional refinancing typically requires 20% equity, making it unavailable for underwater homeowners. However, if you're close to breaking even (within 5-10% of current value), consider:

- Making additional principal payments to reach 20% equity faster

- Waiting for market appreciation in your area

- Bringing cash to closing to make up the difference

Option 4: Deed in Lieu of Foreclosure

A deed in lieu of foreclosure allows you to voluntarily transfer property ownership to your lender in exchange for release from the mortgage obligation.

How the Process Works:

- Initial Request – Contact your lender to discuss deed in lieu option

- Financial Review – Lender evaluates your situation and property condition

- Property Inspection – Lender assesses property value and condition

- Negotiation – Terms are discussed, including deficiency forgiveness

- Title Transfer – You sign over the deed, lender releases mortgage

- Move-Out – Typically given 30-90 days to relocate

When Deed in Lieu Makes Sense:

✔️ You cannot afford mortgage payments

✔️ Short sale attempts have failed

✔️ You want to avoid foreclosure proceedings

✔️ Property has no junior liens or they can be negotiated

✔️ You need a quicker resolution than foreclosure

Important Limitations:

⚠️ Junior Liens Problem – If you have second mortgages, home equity lines, or other liens on the property, the lender typically won't accept a deed in lieu unless those are resolved first.

⚠️ Deficiency Balance – Some lenders reserve the right to pursue remaining balance, though many waive this in deed in lieu agreements.

⚠️ Tax Consequences – Forgiven debt may be considered taxable income (though exceptions exist for primary residences under certain conditions).

Credit Impact Comparison:

| Action | Credit Score Impact | Recovery Time |

|---|---|---|

| Deed in Lieu | -150 to -200 points | 3-4 years |

| Foreclosure | -200 to -300 points | 5-7 years |

| Short Sale | -100 to -150 points | 2-3 years |

| Bankruptcy | -200 to -250 points | 7-10 years |

Option 5: Strategic Default Considerations

Strategic default means intentionally stopping mortgage payments despite having the ability to pay, forcing the lender into foreclosure or negotiation.

⚠️ Critical Warning: This option carries serious legal, financial, and ethical implications. It should only be considered after consulting with legal and financial professionals.

Why Some Homeowners Consider It:

- Severely underwater with no prospect of recovery (50%+ negative equity)

- Mortgage payments far exceed rental costs for comparable housing

- No emotional attachment to property

- State laws limit deficiency judgments

- Financial resources better deployed elsewhere

Serious Consequences:

Credit Destruction 💥

Foreclosure remains on credit reports for seven years, making future home purchases, car loans, and even employment difficult.

Deficiency Judgments

In many states, lenders can sue for the difference between sale proceeds and loan balance, potentially garnishing wages or bank accounts.

Tax Liability

Forgiven mortgage debt may be taxable income, creating unexpected IRS bills.

Legal Ramifications

Some lenders pursue fraud claims if they believe borrowers misrepresented their situation.

Moral and Community Impact

Strategic defaults contributed to the 2008 crisis and affect neighborhood property values.

States with Anti-Deficiency Protection:

Some states limit lenders' ability to pursue deficiency judgments:

- California (purchase money loans only)

- Arizona

- Alaska

- Montana

- North Carolina (for certain loan types)

- Washington

Even in these states, second mortgages and refinanced loans may not receive protection.

Option 6: Stay and Pay Strategy

Sometimes the best option is simply staying in your home and continuing payments while waiting for market recovery.

When This Makes Sense:

✅ You Can Afford Payments – Current income comfortably covers mortgage and expenses

✅ No Need to Move – Job, family, and lifestyle are stable in current location

✅ Market Recovery Expected – Local economic indicators suggest property values will rebound

✅ Long-Term Perspective – You plan to stay 5-10+ years, giving equity time to rebuild

✅ Emotional Value – The home provides stability, community, and quality of life beyond financial considerations

Advantages of Waiting It Out:

Credit Protection 🛡️

Continuing payments maintains excellent credit, keeping future financial options open.

Tax Benefits

Mortgage interest deductions continue reducing taxable income (though 2025 tax laws limit deductions for many homeowners).

Forced Savings

Principal payments, however small, build equity over time. In year 15 of a 30-year mortgage, payments increasingly go toward principal.

Market Recovery Potential

Real estate historically appreciates over long periods. The 2008 crash saw most markets fully recover within 8-12 years.

Stability Benefits

Avoiding moving costs, maintaining children's schools, and preserving community connections have real value.

Making the Strategy Work:

- Accelerate Principal Payments – Even $100 extra monthly significantly reduces underwater time

- Improve Property Value – Strategic renovations (kitchen, bathrooms) can boost appraisal

- Monitor Market Trends – Stay informed about local real estate recovery

- Build Emergency Fund – Ensure you can weather future financial storms

- Refinance When Possible – As equity builds, better loan terms become available

Option 7: Rent Out the Property

If you need to move but can't sell, converting your home to a rental property might bridge the gap.

Financial Calculations:

Monthly Costs:

- Mortgage payment: $2,500

- Property taxes: $400

- Insurance: $150

- Maintenance reserve: $200

- Total: $3,250

Rental Income:

- Market rent: $2,800

- Vacancy factor (8%): -$224

- Net: $2,576

Monthly Shortfall: $674

Even with negative cash flow, renting can make sense if:

- The shortfall is manageable with your current income

- Property appreciation is expected

- Tax benefits offset losses

- Alternative housing costs are lower

Important Considerations:

Mortgage Terms 📋

Your loan agreement may prohibit renting without lender approval. Owner-occupied mortgages carry lower rates than investment properties, so lenders care about usage.

Landlord Responsibilities

Property management, tenant screening, maintenance, and legal compliance require time, money, and expertise.

Tax Implications

Rental income is taxable, but expenses (mortgage interest, repairs, depreciation) are deductible.

Future Refinancing

Converting to rental may affect your ability to refinance as an owner-occupied property.

Special Situations: Liens, Judgments, and Title Issues

Underwater mortgages become exponentially more complicated when combined with other property problems. These situations require specialized expertise and creative solutions.

Dealing with Tax Liens on Underwater Properties

Selling a house with a tax lien while underwater creates a double challenge. The tax authority has first priority on proceeds, but there aren't enough proceeds to satisfy all debts.

Typical Scenario:

- Property value: $250,000

- First mortgage: $280,000 (underwater by $30,000)

- Tax lien: $15,000

- Total debt: $295,000

Potential Solutions:

Tax Lien Subordination

Tax authorities sometimes agree to subordinate their lien (move to second position) to allow refinancing or sale, especially if it means they'll eventually collect more than in foreclosure.

Offer in Compromise

The IRS and many state tax agencies accept reduced payments to settle tax debts, particularly when full collection is unlikely.

Payment Plans

Establishing payment arrangements keeps liens from growing while you pursue other solutions.

Short Sale Negotiation

In short sales, tax liens must be negotiated alongside the mortgage. Lenders and tax authorities often split proceeds according to priority and negotiated terms.

Judgment Liens and Underwater Mortgages

Judgment liens from lawsuits attach to property, creating additional obstacles when you're already underwater.

How Judgment Liens Complicate Matters:

When you're underwater, judgment creditors face a dilemma. They hold a lien on property worth less than the first mortgage, meaning they'd receive nothing if the property sold today. However, the lien remains attached, preventing clear title transfer.

Resolution Strategies:

Lien Release Negotiation

Judgment creditors often accept reduced settlements, recognizing that their lien position is weak. Offering 20-40% of the judgment amount can secure release.

Bankruptcy Consideration

Chapter 7 bankruptcy may discharge the underlying debt, though liens survive bankruptcy unless specifically addressed through lien avoidance procedures.

Wait and Negotiate

As property value recovers, your negotiating position strengthens. Creditors become more willing to settle when they see potential recovery.

Multiple Owners and Underwater Properties

When multiple people own property jointly and it's underwater, disagreements about solutions can paralyze decision-making.

Common Scenarios:

Inherited Property with Multiple Heirs

Siblings inherit a property with a mortgage exceeding current value. Some want to keep it, others want to sell, and none want to contribute additional funds.

Divorce Situations

Ex-spouses jointly own an underwater home. Neither can afford it alone, neither wants to pay the other's share, and both want out.

Investment Partners

Business partners purchased property together that's now underwater. Their partnership has soured, but the property ties them together.

Legal Solutions:

Partition Action

A partition lawsuit forces property sale when co-owners can't agree. However, with underwater property, this often means foreclosure is the only outcome.

Buyout Agreements

One owner buys out the others' interests at current market value (or negotiated terms), assuming full mortgage responsibility.

Cooperative Short Sale

All owners agree to pursue a short sale, sharing any deficiency liability according to ownership percentages.

Strategic Default Agreement

Owners collectively decide to stop payments and let foreclosure proceed, understanding the credit consequences.

Working with Professionals: When to Seek Expert Help

Navigating Underwater Mortgage Options: What to Do When You Owe More Than It's Worth requires expertise across multiple disciplines. The right professional guidance can save tens of thousands of dollars and years of credit damage.

Real Estate Professionals Specializing in Distressed Properties

Not all real estate agents understand underwater mortgages. You need someone with specific experience in:

- Short sale negotiations and lender approval processes

- Pricing strategies for underwater properties

- Marketing to investors and cash buyers

- Coordinating with multiple lien holders

- Managing complex closings with title issues

Sure Path Property Solutions specializes in exactly these complicated situations, providing helpful solutions when traditional real estate channels fall short.

HUD-Approved Housing Counselors

The Department of Housing and Urban Development (HUD) certifies housing counselors who provide free or low-cost advice on:

- Evaluating all available options objectively

- Negotiating with lenders

- Understanding government assistance programs

- Avoiding foreclosure rescue scams

- Creating sustainable financial plans

Finding a Counselor:

Visit HUD.gov or call 1-800-569-4287 to locate approved counselors in your area.

Real Estate Attorneys

Legal expertise becomes essential when dealing with:

- Deficiency judgment risks in your state

- Bankruptcy considerations

- Lien priority disputes

- Title problems preventing clear transfer

- Foreclosure defense strategies

- Tax implications of debt forgiveness

Financial Advisors and Tax Professionals

CPAs and financial planners help you understand:

- Tax consequences of short sales, deed in lieu, or foreclosure

- Mortgage forgiveness debt relief provisions

- Strategic financial planning around property decisions

- Retirement account implications

- Long-term wealth building despite current setback

The Sure Path Approach to Complex Property Situations

At Sure Path Property Solutions, we understand that underwater mortgages rarely exist in isolation. Homeowners often face multiple challenges simultaneously:

- Underwater mortgage + back property taxes

- Negative equity + judgment liens

- Multiple heirs + inherited underwater property

- Divorce + upside-down home value

Our industry experts coordinate with counties, title professionals, lenders, and attorneys to untangle these complicated situations. We provide trustworthy service that puts your interests first, exploring every possible avenue before recommending the best path forward.

Our Process:

- Comprehensive Situation Analysis – We examine all aspects of your property challenges

- Creative Solution Development – We identify options others might miss

- Professional Coordination – We work with all parties to execute solutions

- Transparent Communication – We explain everything in plain language

- Follow-Through Support – We stay with you through completion

Whether you're dealing with liens and judgments, inherited property complications, or title issues, our friendly and caring team brings decades of combined experience to your unique situation.

Preventing Future Underwater Situations

Once you've resolved your current underwater mortgage, protecting yourself from future negative equity situations becomes paramount.

Smart Home Buying Practices

Substantial Down Payments 💰

Putting down 20% or more creates an immediate equity cushion that protects against market fluctuations. Even if values drop 10-15%, you maintain positive equity.

Buy Below Your Means

Just because you qualify for a $500,000 mortgage doesn't mean you should borrow that much. Buying below maximum qualification leaves financial flexibility for market changes.

Research Market Conditions

Avoid buying at obvious market peaks. Study local price trends, inventory levels, and economic indicators before purchasing.

Location Fundamentals

Properties in areas with strong job markets, good schools, and limited supply hold value better than those in declining or oversupplied areas.

Building Equity Faster

Bi-Weekly Payment Strategy

Making half your mortgage payment every two weeks results in 26 half-payments (13 full payments) annually instead of 12, shaving years off your loan and building equity faster.

Principal Prepayment

Even modest additional principal payments compound dramatically over time:

- $100 extra monthly on a $300,000 loan saves $50,000+ in interest

- Pays off a 30-year mortgage in 24 years

- Builds equity cushion against market downturns

Strategic Improvements

Focus renovations on projects with strong ROI:

- Kitchen remodels (60-80% return)

- Bathroom updates (60-70% return)

- Energy efficiency improvements (50-70% return)

- Curb appeal enhancements (75-100% return)

Market Awareness and Planning

Monitor Local Real Estate Trends 📊

Stay informed about your neighborhood's market conditions through:

- Zillow and Redfin market reports

- Local real estate association data

- County assessor valuations

- Comparable sales in your area

Maintain Financial Reserves

An emergency fund covering 6-12 months of expenses provides flexibility during market downturns, job loss, or unexpected repairs.

Consider Refinancing Timing

When rates drop or equity builds, refinancing to lower rates or shorter terms accelerates equity building and reduces long-term costs.

Government Programs and Assistance in 2025

Federal and state governments continue offering programs to help underwater homeowners, though options have evolved since the 2008 crisis.

Current Federal Programs

Making Home Affordable Successors

While original programs expired, several lenders offer similar modifications through proprietary programs modeled on government initiatives.

FHA Short Refinance

Allows underwater borrowers to refinance into FHA-insured mortgages if their lender agrees to write down the principal balance to 97.75% of current value.

Hardest Hit Fund

Some states still operate programs funded by federal Hardest Hit Fund allocations, offering:

- Mortgage payment assistance

- Principal reduction programs

- Transition assistance for short sales or deeds in lieu

VA Loan Modifications

Veterans with VA loans have access to specialized modification programs through the Veterans Affairs Servicing Purchase (VASP) program.

State-Specific Assistance

Many states operate their own programs:

California

- Keep Your Home California (mortgage assistance)

- California Housing Finance Agency programs

Florida

- Florida Hardest Hit Fund (ongoing assistance)

- State Housing Initiatives Partnership

Illinois

- Illinois Hardest Hit Program

- Emergency mortgage assistance

Check Your State:

Visit your state housing finance agency website to discover available programs in your area.

Avoiding Foreclosure Rescue Scams

Unfortunately, desperate homeowners attract predatory scammlers. Recognize warning signs:

🚩 Red Flags:

- Upfront fees before any services are provided

- Guarantees they can stop foreclosure

- Requests to sign over your deed

- Pressure to stop communicating with your lender

- Promises that sound too good to be true

Legitimate Help:

- HUD-approved counselors charge minimal or no fees

- Attorneys charge transparent, disclosed fees

- Reputable companies like Sure Path Property Solutions explain all options honestly

- Real professionals encourage you to verify their credentials

Real-Life Success Stories: Underwater Mortgage Resolutions

Understanding how others successfully navigated similar situations provides hope and practical insights.

Case Study 1: The Short Sale Success

Situation:

Maria purchased a condo in 2021 for $425,000 with 5% down. By 2024, the market crashed in her area, and comparable units sold for $340,000. She owed $398,000, creating $58,000 in negative equity. A job relocation made staying impossible.

Solution:

Maria worked with a short sale specialist who:

- Listed the property at $345,000

- Negotiated with her lender for four months

- Secured lender approval at $338,000

- Obtained full deficiency waiver

Outcome:

Maria moved for her new job, avoided foreclosure, and qualified for a new mortgage just 2.5 years later. Her credit score dropped 130 points initially but recovered to 720 within three years.

Case Study 2: Loan Modification Saves Family Home

Situation:

The Johnson family faced job loss during the pandemic, falling behind on their $2,400 monthly mortgage payment. Their home, purchased for $380,000, was now worth $315,000, with $352,000 owed.

Solution:

They contacted their servicer immediately and applied for modification:

- Interest rate reduced from 5.25% to 3.5%

- Loan term extended from 30 to 40 years

- $18,000 in arrears added to principal

- New payment: $1,785 monthly

Outcome:

The family kept their home, avoided foreclosure, and maintained positive payment history. As the breadwinner found new employment, they began making extra principal payments to rebuild equity.

Case Study 3: Strategic Rental Conversion

Situation:

David inherited an underwater property from his parents with $245,000 owed and current value of $210,000. He lived across the country and couldn't manage it personally.

Solution:

Rather than pursue a short sale immediately, David:

- Hired a property management company

- Rented the home for $1,950 monthly

- Covered $350 monthly shortfall from his income

- Waited three years for market recovery

Outcome:

Property values rebounded to $265,000, creating positive equity. David then sold the property, paid off the mortgage, and netted $15,000 after selling costs and management fees.

Taking Action: Your Next Steps

If you're facing an underwater mortgage situation, taking action today prevents options from narrowing tomorrow. Here's your roadmap forward.

Immediate Actions (This Week)

1. Determine Your Exact Situation 📋

- Request current mortgage payoff statement

- Research comparable sales for accurate property value

- Calculate your negative equity precisely

- List all other debts against the property (tax liens, judgments, second mortgages)

2. Assess Your Financial Reality

- Can you afford current payments comfortably?

- Do you need to move in the next 1-2 years?

- What's your employment stability?

- Do you have emergency reserves?

3. Document Everything

- Gather pay stubs, tax returns, bank statements

- Document any hardship (medical bills, job loss, divorce)

- Collect property tax statements

- Obtain recent mortgage statements

Short-Term Actions (This Month)

4. Research Your Options

- Review all options outlined in this article

- Investigate government programs you might qualify for

- Understand your state's deficiency judgment laws

- Calculate potential outcomes for each option

5. Consult Professionals

- Contact a HUD-approved housing counselor (free)

- Schedule consultations with real estate attorneys

- Speak with tax professionals about implications

- Reach out to Sure Path Property Solutions if you have complex situations involving liens, title issues, or multiple owners

6. Contact Your Lender

- Inquire about modification programs

- Ask about refinancing options

- Discuss short sale procedures

- Understand their deed in lieu process

Long-Term Planning (Next 3-6 Months)

7. Make Your Decision

Based on professional advice and your situation, choose the path that best serves your long-term interests:

- Stay and pay if affordable and sensible

- Pursue modification if you want to keep the home

- Initiate short sale if you need to move

- Consider deed in lieu if other options fail

- Explore rental conversion if timing allows

8. Execute Your Plan

- Follow through consistently

- Maintain detailed records

- Communicate regularly with all parties

- Stay patient through bureaucratic processes

9. Protect Your Future

- Rebuild credit systematically

- Create emergency fund

- Learn from the experience

- Plan smarter for next home purchase

Conclusion: Finding Your Path Forward

Being underwater on your mortgage feels overwhelming, but it's not insurmountable. Thousands of homeowners successfully navigate these challenging waters every year, emerging with their financial futures intact.

The key is understanding that Underwater Mortgage Options: What to Do When You Owe More Than It's Worth exist across a spectrum—from staying put and waiting for recovery to strategic exit through short sales or deed in lieu arrangements. No single solution fits everyone. Your optimal path depends on your unique combination of:

- Financial capacity and stability

- Timeline and mobility needs

- Property location and market trends

- Additional complications (liens, judgments, co-owners)

- Long-term goals and priorities

Remember these fundamental truths:

✨ You have more options than you think. Even in seemingly impossible situations, creative solutions exist when you work with the right professionals.

✨ Taking action beats paralysis. The worst decision is no decision. Even difficult choices move you forward.

✨ Professional guidance matters. Complex property situations require expert service from industry experts who've navigated these challenges hundreds of times.

✨ Your credit will recover. Even significant hits to credit scores heal with time and responsible financial management.

✨ This situation is temporary. Whether through market recovery, loan modification, or strategic exit, you will move past this challenge.

If your underwater mortgage comes with additional complications—back taxes, liens and judgments, title issues, or multiple owners—the path forward becomes even more complex. That's exactly where Sure Path Property Solutions provides helpful solutions.

Our friendly and caring team specializes in untangling complicated property situations that traditional real estate channels can't handle. We coordinate with counties, title professionals, attorneys, and lenders to find creative solutions that work for your specific circumstances. Our trustworthy service puts your interests first, exploring every avenue before recommending the best path forward.

Don't let an underwater mortgage define your financial future. With the right information, helpful guidance, and expert service, you can navigate these troubled waters and reach solid ground. Your next chapter starts with a single step—understanding your options and taking action.

Ready to explore your options? Contact Sure Path Property Solutions today for a confidential consultation about your unique situation. We're here to help you find your path forward.

Sure Path is a family-owned, curative-title cash buyer. We handle the paperwork and pay what’s owed at closing — no fees, no repairs, no pressure.