Back Taxes on Inherited Property: Who Pays & How to Resolve’ in e” />

Back Taxes on Inherited Property: Who Pays & How to Resolve’ in e” />

Inheriting property should feel like receiving a gift, but when you discover thousands of dollars in unpaid property taxes attached to that inheritance, the gift suddenly feels more like a burden. You’re not alone—thousands of heirs across the country face this exact situation every year, wondering who’s responsible for those back taxes and how to move forward without losing the property or their financial stability.

Understanding Back Taxes on Inherited Property: Who Pays & How to Resolve these obligations is crucial for anyone navigating the complex intersection of inheritance law and property taxation. The good news? With the right information and helpful guidance, these challenges are entirely manageable.

Key Takeaways

- Heirs become responsible for back taxes once they inherit property, even if the taxes accrued before the previous owner’s death

- Property tax liens travel with the property, not the person, meaning the debt stays attached regardless of ownership changes

- Multiple resolution options exist, including payment plans, property sales, tax lien redemption, and professional assistance

- Acting quickly prevents escalation such as additional penalties, interest accumulation, and potential tax foreclosure

- Professional help can simplify the process, especially when dealing with probate, multiple heirs, or significant tax debt

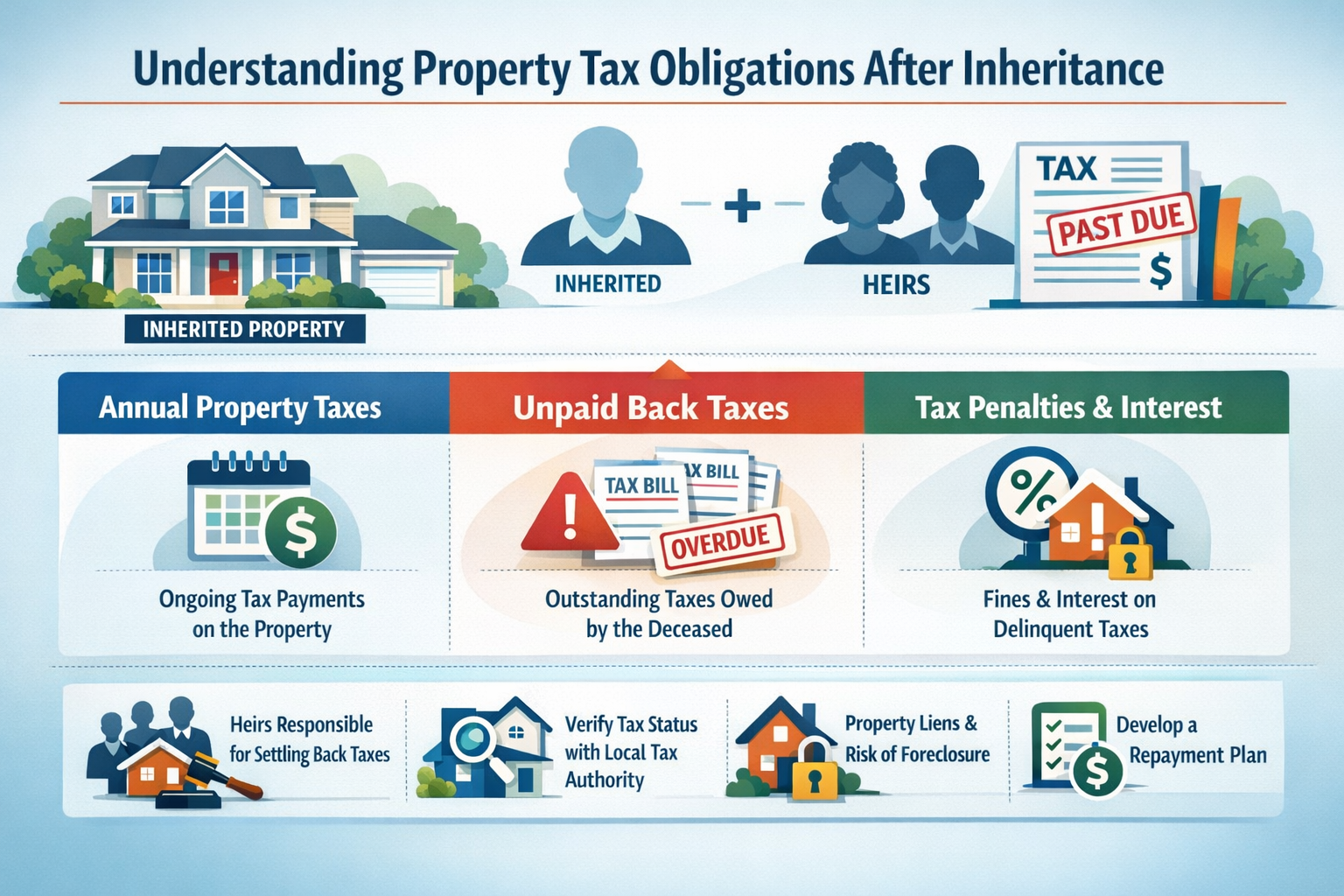

Understanding Property Tax Obligations After Inheritance

When someone passes away and leaves property behind, the tax obligations don’t disappear with them. Property taxes are unique because they attach directly to the real estate itself, creating what’s called a “lien” on the property.

How Property Taxes Transfer to Heirs

The moment you inherit property, you step into the shoes of the previous owner regarding tax responsibilities. This happens regardless of whether you knew about the unpaid taxes or whether the property went through probate.

Here’s what actually happens:

The county tax assessor doesn’t care who owns the property—they only care that the taxes get paid. When ownership transfers through inheritance, the new owner (you) becomes legally responsible for:

- All current year property taxes

- Any back taxes from previous years

- Accumulated interest on unpaid amounts

- Penalties and fees added by the county

- Future taxes as long as you own the property

Think of it like buying a house with a mortgage already on it. The debt stays with the property, not with the person who created it.

The Legal Framework of Tax Liability

Property tax laws vary by state, but the fundamental principle remains consistent: property taxes are a “superior lien.” This means they take priority over almost every other type of debt, including mortgages, judgment liens, and other encumbrances.

Most states follow these general rules:

| Aspect | How It Works |

|---|---|

| Lien Priority | Property taxes rank first, ahead of mortgages and other liens |

| Automatic Attachment | Tax liens attach automatically on the assessment date |

| Inheritance Transfer | Heirs receive property “subject to” existing tax liens |

| Foreclosure Timeline | Counties can foreclose after 1-5 years of non-payment (varies by state) |

| Personal Liability | Heirs are liable only to the extent of inherited property value |

The last point is important: you’re generally not personally liable beyond the value of the property itself. If you inherit a house worth $100,000 with $120,000 in back taxes, you can walk away without owing the difference (though you’d lose the property).

Estate vs. Heir Responsibility

There’s an important distinction between what the estate owes and what you as an heir owe.

During probate, the deceased person’s estate is responsible for settling debts, including property taxes. The executor or administrator should pay outstanding taxes from estate assets before distributing property to heirs.

After probate closes and the property transfers to you, the responsibility shifts entirely to you as the new owner.

However, complications arise when:

- The estate had insufficient funds to pay all debts

- Property transferred outside of probate (through joint tenancy or beneficiary deed)

- Multiple heirs inherit together but disagree on who pays

- The executor failed to identify or pay the tax debt

In these situations, heirs often discover the tax problem only after they’ve already received the property deed. That’s when questions about Back Taxes on Inherited Property: Who Pays & How to Resolve become urgent and personal.

Who Is Legally Responsible for Back Taxes on Inherited Property?

The question of responsibility isn’t always straightforward, especially when multiple people inherit together or when the property passed through different legal mechanisms.

Single Heir Scenarios

If you’re the sole heir who inherited the property, the answer is clear: you are responsible for all property taxes, past and future, from the moment ownership transfers to you.

Your responsibility includes:

✅ Back taxes owed by the deceased owner

✅ Taxes that accrued during probate

✅ Current year taxes

✅ All penalties and interest

You cannot claim ignorance as a defense. Even if the executor never told you about the tax debt, even if you didn’t know the property existed until recently, the legal responsibility falls on you as the current owner.

The silver lining? You also have full decision-making authority to resolve the situation however you see fit.

Multiple Heir Complications

When multiple heirs inherit one property, things get considerably more complex.

Joint and several liability typically applies, meaning:

- Each heir is individually responsible for the entire tax debt

- The county can pursue any one heir for the full amount

- One heir can pay everything and then seek reimbursement from co-heirs

- Disagreements between heirs don’t affect the county’s ability to collect

Common conflict scenarios include:

🔸 One heir wants to keep the property while others want to sell

🔸 Some heirs can afford to pay their share while others cannot

🔸 Heirs disagree about whether to pay taxes or let the property go

🔸 Some heirs live far away and feel disconnected from the property

🔸 Family tensions make cooperation difficult

These situations often require legal intervention through a partition action or a buyout agreement where one heir purchases the others’ interests.

Executor and Administrator Duties

The executor or administrator of an estate has a fiduciary duty to identify and pay the deceased’s debts, including property taxes, before distributing assets to heirs.

Their responsibilities include:

- Researching all properties owned by the deceased

- Contacting county tax assessors to determine amounts owed

- Paying current and back taxes from estate funds

- Ensuring clear title before transferring property to heirs

If an executor fails to pay property taxes when estate funds were available, they may be personally liable for the oversight. Heirs who suffer financial harm due to executor negligence can potentially sue for breach of fiduciary duty.

However, if the estate simply didn’t have enough money to pay all debts, the executor isn’t personally liable—but the tax lien remains on the property when it passes to heirs.

Special Inheritance Situations

Different inheritance methods create different responsibility scenarios:

Transfer-on-Death Deed: Property passes directly to beneficiaries outside probate, meaning there’s no estate process to pay taxes first. Beneficiaries receive the property with all existing liens attached.

Joint Tenancy with Right of Survivorship: When one joint tenant dies, the property automatically passes to the surviving tenant(s). Any tax debt transfers with it, and the surviving owner becomes immediately responsible.

Life Estate: If the deceased had a life estate and you held the remainder interest, you become full owner upon their death—along with responsibility for any tax arrears.

Trust Property: If the property was held in trust, the trust itself may be responsible for taxes, depending on the trust terms and whether it has sufficient assets. Learn more about selling trust property.

Understanding your specific situation is the first step toward finding helpful solutions that work for your circumstances.

How Back Taxes Accumulate and Impact Inherited Property

Property taxes don’t just sit idle—they grow over time through interest, penalties, and additional fees that can quickly turn a manageable debt into an overwhelming burden.

Interest and Penalty Structures

Every state and county has its own formula for calculating interest and penalties on delinquent property taxes, but they all follow the same basic principle: the longer you wait, the more you owe.

Typical accumulation includes:

📊 Interest rates: Usually 6-18% annually, compounded monthly or quarterly

📊 Late payment penalties: Often 5-10% of the tax amount

📊 Collection fees: Additional charges when accounts go to collections

📊 Legal fees: If the county initiates foreclosure proceedings

📊 Administrative costs: Processing fees for payment plans or redemptions

Example calculation:

Let’s say you inherit a property with $5,000 in unpaid property taxes from three years ago in a county that charges 12% annual interest and a 10% penalty:

- Original tax debt: $5,000

- Penalty (10%): $500

- Interest (12% × 3 years, compounded): $2,025

- Total owed: $7,525

That’s more than a 50% increase in just three years! This demonstrates why addressing Back Taxes on Inherited Property: Who Pays & How to Resolve quickly can save thousands of dollars.

Tax Lien Priority and Foreclosure Risk

Property tax liens hold a special position in the hierarchy of property encumbrances. They’re considered “superior liens,” which means they take priority over virtually everything else, including:

- First mortgages

- Home equity loans

- Mechanics liens

- Judgment liens

- HOA liens (in most states)

What this means practically:

If the county forecloses for unpaid taxes, they can sell the property and use the proceeds to pay the tax debt first. Whatever remains goes to pay other lienholders in order of priority, and finally to you as the owner.

Tax Foreclosure Timeline

Counties don’t want to foreclose—they want to collect taxes. But if taxes remain unpaid long enough, they will initiate foreclosure proceedings.

General timeline (varies significantly by state):

Year 1: Tax becomes delinquent

↓

Year 1-2: County sends notices and adds penalties/interest

↓

Year 2-3: Property may be sold at a tax lien sale (investor pays taxes, gets lien)

↓

Year 3-5: Redemption period (you can still pay and keep property)

↓

Year 5+: County or lien holder can foreclose and take ownership

Some states move much faster—as quickly as one year from delinquency to foreclosure. Others give property owners five years or more to resolve the debt.

Understanding your state’s specific property tax lien foreclosure timeline is essential for planning your response strategy.

Impact on Property Value and Marketability

Back taxes don’t just threaten your ownership—they also affect the property’s marketability and effective value.

Title issues: A property with a tax lien has a “clouded title,” making it difficult or impossible to sell through traditional means. Most buyers won’t touch a property with tax problems, and lenders won’t provide financing.

Reduced equity: If you own a property worth $150,000 but owe $30,000 in back taxes, your actual equity is only $120,000. The tax debt reduces what you can net from a sale.

Maintenance deterioration: When heirs can’t afford to pay taxes, they often can’t afford maintenance either. The property may deteriorate while the tax debt grows, creating a downward spiral.

Insurance complications: Some insurance companies won’t provide coverage on properties with significant tax liens, leaving you exposed to additional risk.

The good news? Even properties with substantial tax debt can be sold. You just need to work with buyers or industry experts who understand how to navigate these complexities.

Step-by-Step Guide: How to Resolve Back Taxes on Inherited Property

Facing a property tax debt can feel overwhelming, but breaking the resolution process into clear steps makes it manageable. Here’s your roadmap to addressing Back Taxes on Inherited Property: Who Pays & How to Resolve the situation effectively.

Step 1: Assess the Full Tax Situation

Before you can solve the problem, you need to understand its complete scope.

Action items:

✔ Contact the county tax assessor’s office where the property is located

✔ Request a complete tax history showing all unpaid years

✔ Get a current payoff amount including all interest and penalties

✔ Ask about the redemption deadline if a tax lien has already been sold

✔ Inquire about upcoming tax sales or foreclosure proceedings

✔ Obtain documentation of everything in writing

Most county tax offices are surprisingly helpful when you reach out proactively. They’d rather work with you than foreclose.

Important questions to ask:

- What is the total amount owed, including all fees?

- When is the next deadline or critical date?

- Are payment plans available?

- Has a tax lien certificate been sold to an investor?

- What is the redemption period in this county?

- Are there any tax relief programs for inherited property?

Document everything. Get names, dates, and reference numbers for all communications.

Step 2: Evaluate Your Financial Options

Once you know what you owe, assess your ability to pay.

Create a decision matrix:

| Option | Pros | Cons | Best For |

|---|---|---|---|

| Pay in full | Clears debt immediately, stops interest | Requires significant cash | Those with available funds or liquid assets |

| Payment plan | Manageable monthly amounts, keeps property | Interest continues, long-term commitment | Those who want to keep property and have steady income |

| Sell property | Eliminates debt, provides cash | Lose property, may have emotional attachment | Those who don’t want the property or can’t afford ongoing costs |

| Refinance | Lower interest than tax rate | Requires good credit, property must have equity | Property owners with decent credit and equity |

| Let it go | No financial obligation | Lose property and any equity | When debt exceeds property value significantly |

Be honest about your financial capacity. Committing to a payment plan you can’t afford only delays the inevitable and increases your total cost.

Step 3: Explore County Payment Plans and Programs

Most counties offer payment plan options for delinquent property taxes. These programs provide helpful solutions that make large tax debts manageable.

Typical payment plan features:

💰 Duration: Usually 12-60 months depending on the amount owed

💰 Down payment: Often requires 10-25% upfront

💰 Interest: Continues to accrue but at a reduced rate

💰 Penalties: May be partially waived as an incentive

💰 Automatic payments: Most counties prefer automatic bank drafts

Special programs to ask about:

- Senior citizen deferral programs: Some states allow seniors to defer taxes until property sale or death

- Disability exemptions: Reduced tax rates or payment assistance for disabled owners

- Hardship programs: Temporary relief for those experiencing financial difficulties

- Homestead exemptions: Reduced assessments for primary residences (may apply retroactively)

- Inheritance transition programs: Some counties offer special consideration for recent heirs

Each county has different programs and eligibility requirements. The only way to know what’s available is to ask directly.

Step 4: Consider Selling the Property

If keeping the property isn’t feasible or desirable, selling may be your best option. But selling a house with a tax lien requires a different approach than a traditional sale.

Your selling options:

Traditional sale with payoff at closing:

If the property has sufficient equity, you can list it traditionally and pay the tax debt from the sale proceeds at closing. The title company handles the payoff, ensuring clean title transfer.

Cash buyer or investor:

Companies like Sure Path Property Solutions specialize in purchasing properties with tax liens, title issues, and other complications. They can often close quickly and handle all the complexity for you.

Tax deed purchase:

In some cases, you might negotiate directly with a tax lien investor who holds a certificate on your property, selling to them before foreclosure.

Auction or “as-is” sale:

Some investors buy properties at auction specifically to resolve tax issues and resell.

Advantages of selling:

✅ Immediate resolution of tax debt

✅ No ongoing property maintenance or costs

✅ Potential to receive cash if equity remains after payoff

✅ Eliminates stress and complexity

✅ Frees you from property you may not want

When selling makes sense:

- You don’t want to keep the property

- You can’t afford ongoing taxes and maintenance

- The property is in poor condition

- You live far away from the property

- Multiple heirs can’t agree on what to do

- The emotional burden outweighs any potential benefit

Step 5: Negotiate with Tax Lien Holders

If a tax lien certificate has already been sold to an investor, you’ll need to negotiate with them rather than (or in addition to) the county.

Understanding tax lien certificates:

When property taxes go unpaid, many counties sell “tax lien certificates” to investors. The investor pays the back taxes, and in return, receives:

- The right to collect the debt plus interest (often 10-25% annually)

- The potential to foreclose if you don’t pay within the redemption period

- Priority position ahead of all other liens

Negotiation strategies:

🔑 Act before the redemption period expires: Once it expires, the investor can foreclose

🔑 Offer a lump sum settlement: Some investors will accept less than the full amount for immediate payment

🔑 Request a payment plan: Many investors prefer steady income to foreclosure hassle

🔑 Highlight property issues: If the property has problems that reduce its value, use that as leverage

🔑 Get everything in writing: Never make payments without a written agreement

Remember, tax lien investors are businesspeople looking for a return. They often prefer cooperative resolution over the time and expense of foreclosure.

Step 6: Work with Professionals

Complex tax situations often benefit from expert service and professional guidance.

Professionals who can help:

Real estate attorneys: Essential for complex situations, multiple heirs, or potential legal disputes. They can negotiate on your behalf and ensure your rights are protected.

Tax professionals: CPAs or enrolled agents can help you understand tax implications, identify deductions, and potentially reduce your tax burden.

Real estate agents specializing in distressed properties: They understand how to market and sell properties with liens and title issues.

Property solutions companies: Firms like Sure Path Property Solutions provide comprehensive assistance, from coordinating with counties to facilitating sales, offering friendly and caring support throughout the process.

Title companies: They can research the complete lien history and ensure proper payoff procedures.

Estate attorneys: If the property is still in probate or there are estate complications, an estate attorney is invaluable.

The cost of professional help is often far less than the cost of mistakes or missed opportunities. When dealing with significant tax debt or complex inheritance situations, expert guidance provides peace of mind and better outcomes.

Prevention and Proactive Strategies

While this article focuses on resolving existing tax debt, understanding prevention strategies helps if you’re currently in probate or expecting to inherit property in the future.

Due Diligence Before Accepting Inheritance

You’re not required to accept an inheritance. If property comes with more debt than value, you can disclaim it.

Before accepting inherited property:

🔍 Research the complete financial picture:

- Property tax status

- Mortgage balance

- Other liens or judgments

- HOA dues or special assessments

- Condition and repair costs

🔍 Calculate total costs vs. value:

Does the property’s market value exceed all debts and anticipated expenses? If not, accepting it may be financial self-harm.

🔍 Consider the disclaimer option:

Most states allow heirs to disclaim (refuse) an inheritance within 9 months of the decedent’s death. The property then passes as if you had predeceased the owner, typically going to contingent beneficiaries or being sold by the estate.

🔍 Consult professionals before deciding:

An attorney or financial advisor can help you make an informed choice.

Estate Planning to Prevent Tax Issues

If you own property and want to ensure your heirs don’t face tax problems, take these proactive steps:

Keep taxes current: The simplest solution is to pay property taxes on time every year.

Set up automatic payments: Many counties offer automatic bank draft options that ensure you never miss a payment.

Create a tax reserve fund: Set aside money specifically for property taxes, especially if they’re paid annually or semi-annually.

Communicate with heirs: Let your intended beneficiaries know about the property and its financial status.

Fund your estate adequately: Ensure your estate has sufficient liquid assets to pay final expenses and property taxes during probate.

Consider life insurance: A policy can provide immediate cash to heirs for paying taxes and other expenses.

Use a living trust: Property in a properly funded trust avoids probate and can include instructions for tax payment.

Ongoing Property Tax Management

If you’ve inherited property and resolved the back taxes, prevent future problems with these practices:

✅ Set up automatic payments with the county tax assessor

✅ Review your tax bill annually for assessment errors

✅ Appeal excessive assessments promptly

✅ Budget for tax increases (typically 2-5% annually)

✅ Maintain adequate insurance to protect your investment

✅ Keep the property maintained to preserve value

✅ Monitor for tax relief programs you might qualify for

Proactive management prevents the stress and expense of dealing with delinquent taxes down the road.

Special Circumstances and Complex Situations

Some inherited property situations involve additional complications that require specialized approaches.

Inherited Property with Multiple Liens

Property tax liens aren’t always the only debt attached to inherited property. You might also discover:

- Mortgage debt

- Home equity loans

- Mechanics liens from contractors

- Judgment liens from lawsuits

- HOA liens

- IRS liens

When multiple liens exist, understanding lien priority becomes critical. Property tax liens almost always take first priority, but the order of other liens affects how sale proceeds are distributed.

Resolution approach:

- Get a complete title search to identify all liens

- Determine lien priority in your state

- Calculate total debt vs. property value

- Decide whether resolution is financially viable

- If selling, work with a title company experienced in complex closings

Sometimes the total debt exceeds property value, making the property “underwater.” In these cases, walking away may be the most rational choice.

Properties in Probate with Tax Issues

When property is still going through probate and has tax debt, the executor has specific responsibilities and options.

Executor’s options:

Pay from estate funds: If the estate has sufficient liquid assets, the executor should pay the taxes before distributing property to heirs.

Sell the property: The executor can sell the property during probate, using proceeds to pay taxes and other debts. Learn more about selling property in probate.

Request court approval for payment plan: Some probate courts will approve payment plans for estate debts.

Distribute property subject to liens: If estate funds are insufficient, the property passes to heirs with the tax lien attached.

The executor must balance the interests of all beneficiaries while fulfilling legal obligations. When tax debt is significant, consulting with a probate attorney is essential.

Out-of-State Inherited Property

Inheriting property in a different state adds layers of complexity:

Challenges:

- Unfamiliarity with local tax laws and procedures

- Difficulty managing property from a distance

- Additional costs for travel or local representation

- Different probate requirements

- Potential for ancillary probate proceedings

Solutions:

🌎 Hire local professionals: Engage an attorney and property manager in the property’s location

🌎 Research state-specific laws: Tax procedures vary significantly by state

🌎 Consider selling quickly: If you don’t plan to use the property, selling eliminates ongoing management burdens

🌎 Use technology: Many counties now offer online tax payment and research tools

🌎 Work with national companies: Some property solutions companies operate in multiple states

Distance shouldn’t prevent you from resolving tax issues, but it does require more intentional coordination and often professional assistance.

Disagreements Among Multiple Heirs

When siblings or multiple heirs disagree about how to handle inherited property with tax debt, resolution becomes as much about family dynamics as finances.

Common conflict scenarios:

😟 One heir wants to keep the property; others want to sell

😟 Some heirs can pay their share of taxes; others cannot

😟 Heirs disagree about the property’s value

😟 Emotional attachment varies among heirs

😟 Communication has broken down

😟 One heir is using the property while others pay taxes

Resolution mechanisms:

Buyout agreement: One heir purchases the others’ interests and assumes full responsibility for the property and taxes.

Forced sale through partition action: Any co-owner can file a partition lawsuit to force a sale, with proceeds divided among owners.

Mediation: A neutral third party helps heirs reach agreement without court intervention.

Rental arrangement: Heirs agree to rent the property, using income to pay taxes and maintenance, with remaining profit shared.

Structured decision-making: Heirs agree to specific decision rules (majority vote, unanimous consent, etc.) in advance.

When family relationships are strained, having trustworthy service from neutral professionals can facilitate solutions that preserve both the property’s value and family harmony.

Tax Implications and Financial Considerations

Resolving back taxes on inherited property has its own tax implications that affect your overall financial picture.

Income Tax Considerations

Stepped-up basis: When you inherit property, you receive a “stepped-up basis” equal to the property’s fair market value on the date of the previous owner’s death. This can significantly reduce capital gains taxes if you sell.

Example:

- Deceased owner bought property for $50,000 in 1990

- Property worth $200,000 when they died in 2025

- Your basis is $200,000 (stepped-up), not $50,000

- If you sell for $205,000, your taxable gain is only $5,000

Deductibility of property taxes: If you itemize deductions on your federal income tax return, you can deduct property taxes you pay (up to $10,000 combined with state and local taxes under current law).

Back taxes paid: Property taxes you pay for prior years are generally deductible in the year you pay them, not the year they were assessed.

Estate Tax Implications

For most estates, federal estate taxes aren’t a concern—the exemption is $13.61 million per person in 2026. However, some states have lower estate tax thresholds.

Key points:

- Estate taxes are the estate’s responsibility, not the heir’s personal obligation

- Property taxes owed at death are estate debts that reduce the taxable estate

- Heirs don’t pay estate tax personally (the estate pays before distribution)

Selling Costs and Net Proceeds

When selling inherited property to resolve tax debt, understanding all costs helps you make informed decisions.

Typical costs when selling:

| Cost Category | Typical Amount | Notes |

|---|---|---|

| Back taxes | Varies | Must be paid for clear title |

| Real estate commission | 5-6% of sale price | Traditional sales only |

| Title insurance | $500-$2,000 | Protects buyer’s title |

| Closing costs | 1-3% of sale price | Various fees and charges |

| Property repairs | Varies widely | May not be needed for cash sales |

| Attorney fees | $500-$3,000+ | Depends on complexity |

| Probate costs | Varies | If property still in probate |

Cash buyers vs. traditional sales:

Traditional sales typically net higher prices but involve more costs and time. Cash buyers like Sure Path Property Solutions offer lower prices but eliminate most selling costs, close quickly, and handle all complexity—often resulting in similar net proceeds with far less hassle.

Long-term Financial Planning

If you decide to keep inherited property, factor these ongoing costs into your financial planning:

💵 Annual property taxes (which typically increase)

💵 Insurance premiums

💵 Maintenance and repairs

💵 Utilities (if vacant)

💵 HOA fees (if applicable)

💵 Property management (if you don’t live nearby)

Make sure the property’s value—whether through personal use, rental income, or appreciation—justifies these ongoing expenses.

Resources and Where to Get Help

You don’t have to navigate Back Taxes on Inherited Property: Who Pays & How to Resolve alone. Numerous resources and professionals stand ready to provide helpful guidance.

County and Government Resources

County Tax Assessor’s Office:

Your first stop for information about tax amounts, payment options, and deadlines. Most counties have websites with online account access.

County Treasurer:

In some jurisdictions, the treasurer handles tax collection while the assessor handles valuation. Know which office to contact for which issue.

State Department of Revenue:

Provides information about state-level tax programs, exemptions, and appeals processes.

Legal Aid Organizations:

Free or low-cost legal assistance for qualifying individuals facing property tax issues.

State Bar Association:

Referral services to connect you with qualified real estate and tax attorneys.

Professional Services

Real Estate Attorneys:

Essential for complex situations, title issues, multiple heirs, or legal disputes. They protect your rights and ensure proper procedures.

Tax Professionals (CPAs, EAs):

Help you understand tax implications, maximize deductions, and plan strategically.

Estate Planning Attorneys:

If the property is still in probate or estate administration is incomplete.

Title Companies:

Research property history, identify all liens, and facilitate proper closing procedures.

Property Solutions Companies:

Sure Path Property Solutions and similar companies specialize in properties with complications like tax liens, title problems, multiple owners, and other issues that make traditional sales difficult. They offer:

- Free property assessments

- Cash offers with quick closings

- Handling of all tax payoff coordination

- Solutions for properties in any condition

- Experience with complex inheritance situations

- No commissions or hidden fees

Educational Resources

Online research:

Government websites, legal information sites, and real estate education platforms provide valuable background information.

Local workshops:

Some counties and nonprofit organizations offer workshops on property tax issues and inheritance matters.

Professional consultations:

Many attorneys and tax professionals offer free or low-cost initial consultations to assess your situation.

Industry expert blogs:

Resources like the Sure Path Property Solutions blog provide in-depth articles on specific topics related to property challenges.

Warning Signs You Need Professional Help

Seek professional assistance immediately if:

⚠️ The tax debt exceeds $10,000

⚠️ Foreclosure proceedings have started

⚠️ Multiple heirs disagree about what to do

⚠️ The property has multiple liens or title issues

⚠️ You’ve received legal notices or court documents

⚠️ The redemption period is about to expire

⚠️ You’re unsure about your legal rights or obligations

⚠️ The property is in another state

⚠️ You feel overwhelmed and don’t know where to start

The cost of professional help is almost always less than the cost of mistakes, missed deadlines, or lost opportunities.

Real-World Examples and Case Studies

Understanding how others have successfully resolved Back Taxes on Inherited Property: Who Pays & How to Resolve these challenges can provide both inspiration and practical strategies.

Case Study 1: Single Heir, Manageable Debt

Situation: Jennifer inherited her aunt’s home in suburban Ohio. The property was worth approximately $180,000 but had $12,000 in unpaid property taxes spanning three years, plus penalties and interest.

Challenge: Jennifer lived 500 miles away, had a full-time job, and didn’t want to keep the property, but she also didn’t want to lose the equity her aunt had built.

Solution: Jennifer contacted the county tax office and learned she had six months before a tax lien sale. She then reached out to a local real estate agent who specialized in properties with tax issues. The agent helped her list the property “as-is” and found a buyer willing to purchase subject to the tax lien. At closing, the $12,000 tax debt was paid from proceeds, and Jennifer netted $154,000 after all costs.

Key takeaway: Acting quickly and working with professionals who understand tax lien sales preserved significant equity that would have been lost in foreclosure.

Case Study 2: Multiple Heirs, Family Conflict

Situation: Three siblings inherited their parents’ farmland in rural Tennessee. The property had $28,000 in back taxes. One sibling wanted to keep the land for sentimental reasons, while the other two wanted to sell immediately. None of the siblings could afford to pay the full tax debt alone.

Challenge: Disagreement about the property’s future combined with significant tax debt and limited individual financial resources.

Solution: After months of conflict, the siblings agreed to mediation. The mediator helped them reach a compromise: the sibling who wanted to keep the property would buy out the others’ shares. They obtained an appraisal showing the property’s value at $240,000. The keeping sibling paid each of the others $70,667 (one-third of the value minus one-third of the tax debt). She then worked out a payment plan with the county for the $28,000 in back taxes, paying $600 monthly over five years.

Key takeaway: Professional mediation and creative financial structuring allowed all parties to achieve acceptable outcomes without destroying family relationships.

Case Study 3: Out-of-State Property, Severe Neglect

Situation: Marcus inherited a property in Detroit from a distant relative he barely knew. The property had been vacant for years, had $35,000 in back taxes, needed extensive repairs, and was in a declining neighborhood. Marcus lived in California and had never even seen the property.

Challenge: The property’s value was questionable, the tax debt was substantial, and Marcus had no interest in managing a distant property rehabilitation project.

Solution: Marcus researched his options and discovered he could disclaim the inheritance, but the deadline had passed. He then contacted several cash buyers who specialized in distressed properties. Sure Path Property Solutions offered $15,000 for the property, which would be applied entirely to the tax debt, with the county agreeing to forgive the remaining $20,000 as part of a blight reduction program. While Marcus received no cash, he eliminated a liability and avoided personal responsibility for the remaining debt.

Key takeaway: Sometimes the best outcome is simply eliminating a liability rather than pursuing profit. Understanding all available options, including government programs, can provide unexpected solutions.

Case Study 4: Tax Lien Already Sold

Situation: Patricia inherited a small house in Florida with $8,000 in back taxes. Before she could address the issue, the county sold a tax lien certificate to an investor. The investor now held the right to foreclose if Patricia didn’t pay within two years.

Challenge: The investor was charging 18% annual interest, and the redemption period was ticking down.

Solution: Patricia contacted the investor directly and explained her situation. She offered to pay the original $8,000 plus one year of interest ($1,440) immediately if the investor would waive the second year’s interest. The investor, preferring a guaranteed return to the uncertainty and expense of foreclosure, agreed. Patricia borrowed $9,440 from family members, paid off the lien, and then sold the property for $95,000, repaying her family and keeping the remaining equity.

Key takeaway: Tax lien investors are often willing to negotiate, especially when offered prompt payment. Direct communication can save thousands in interest and fees.

Frequently Asked Questions

Can I refuse an inheritance if the property has too much tax debt?

Yes. Most states allow heirs to “disclaim” an inheritance within nine months of the decedent’s death. Once disclaimed, the property passes as if you had predeceased the owner, typically going to alternate beneficiaries or being sold by the estate. Consult an attorney before disclaiming, as the decision is usually irrevocable.

Will I owe income tax on inherited property?

No. Inherited property is not taxable income. However, you may owe capital gains tax if you later sell the property for more than its value on the date you inherited it (the stepped-up basis).

Can the county come after my other assets for property tax debt?

Generally, no. Property tax debt is secured by the property itself. The county’s remedy is to foreclose on the property, not to pursue your personal assets. However, once you become the owner, you are responsible for current and future taxes, and failure to pay those could potentially lead to other collection actions depending on state law.

How long do I have to pay back taxes before foreclosure?

This varies significantly by state and county, ranging from as little as one year to five years or more. Contact your county tax office immediately to learn your specific timeline and deadlines.

Can I negotiate to pay less than the full amount owed?

Sometimes. Some counties offer penalty abatement programs, especially for heirs who inherited the debt. Additionally, counties participating in blight reduction or property rehabilitation programs may accept reduced payments. It never hurts to ask, especially if you’re willing to pay promptly.

What happens if multiple heirs inherit but only one wants to pay the taxes?

The heir who pays can seek reimbursement from the others through civil court. Alternatively, that heir might pursue a buyout of the others’ interests or file a partition action to force a sale. The county doesn’t care who pays—they can collect from any owner.

Can I deduct the back taxes I pay on my income tax return?

If you itemize deductions, you can deduct property taxes you pay, including back taxes, in the year you pay them (subject to the $10,000 SALT cap). Consult a tax professional for advice specific to your situation.

Should I pay the back taxes if I plan to sell the property?

Not necessarily. If you’re selling to a cash buyer or investor, they often handle the tax payoff as part of the transaction. If you’re selling traditionally, the taxes will be paid from closing proceeds. However, paying them sooner stops interest from accumulating.

What if the property is worth less than the tax debt?

You may choose to walk away. The county will foreclose, sell the property, and apply proceeds to the tax debt. You lose the property but have no personal liability for any deficiency (in most states). Alternatively, you might negotiate with the county for a reduced settlement.

How can Sure Path Property Solutions help with inherited property tax issues?

Sure Path Property Solutions specializes in purchasing properties with complications like tax liens, probate issues, and multiple owners. They can make a cash offer, coordinate directly with the county to pay off tax debt, and close quickly—often in as little as two weeks. This eliminates the stress of managing the situation yourself while still preserving any remaining equity. Contact them for a free, no-obligation property assessment.

Conclusion: Taking Action on Back Taxes for Inherited Property

Discovering that inherited property comes with substantial back taxes can feel like receiving a burden instead of a blessing. But as this comprehensive guide demonstrates, Back Taxes on Inherited Property: Who Pays & How to Resolve these obligations is entirely manageable with the right information, resources, and support.

Remember these essential points:

✔ You are responsible for property taxes once you inherit, regardless of when they accrued

✔ Acting quickly saves money by preventing additional interest, penalties, and potential foreclosure

✔ Multiple resolution paths exist, from payment plans to sales to professional assistance

✔ You don’t have to navigate this alone—helpful solutions and expert service are available

✔ Even complex situations have answers, whether involving multiple heirs, out-of-state property, or significant debt

Your Next Steps

Don’t let uncertainty or overwhelm prevent you from taking action. Here’s what to do right now:

1. Assess your situation completely

Contact the county tax office today to get exact figures on what’s owed, when deadlines fall, and what options exist.

2. Evaluate your goals

Decide honestly whether you want to keep the property or sell it. Neither choice is wrong—the right answer depends on your circumstances and preferences.

3. Explore your options

Research payment plans, selling strategies, and professional assistance. Get multiple perspectives before making decisions.

4. Seek professional guidance

For significant tax debt or complex situations, consult with attorneys, tax professionals, or property solutions experts who can provide personalized advice.

5. Take action promptly

Every day you wait costs money in accumulating interest and penalties. Even small steps forward are better than inaction.

How Sure Path Property Solutions Can Help

If you’re feeling overwhelmed by inherited property with tax issues, Sure Path Property Solutions offers friendly and caring support through the entire process. As industry experts in complex property situations, they provide:

🏡 Free property assessments with no obligation

🏡 Fair cash offers that account for tax debt and property condition

🏡 Quick closings (often 2-3 weeks) to stop interest accumulation

🏡 Complete coordination with counties and title companies

🏡 Solutions for any situation, including multiple heirs, probate, liens, and title issues

🏡 Transparent process with no hidden fees or commissions

Whether you ultimately decide to keep the property, sell it traditionally, or work with a cash buyer, having expert guidance helps you make informed decisions that protect your interests and financial future.

The path forward may seem unclear right now, but thousands of property owners have successfully resolved inherited property tax issues—and you can too. With helpful guidance, trustworthy service, and a clear action plan, you can transform this challenge into a resolved chapter of your life.

Ready to explore your options? Contact Sure Path Property Solutions today for a free consultation and discover how they can help you navigate back taxes on inherited property with confidence and peace of mind.

Sure Path is a family-owned, curative-title cash buyer. We handle the paperwork and pay what’s owed at closing — no fees, no repairs, no pressure.