Selling a house with liens attached can feel like being trapped in a maze with no exit. Traditional buyers run the other way. Real estate agents shake their heads. Banks close their doors. But here’s the truth that many property owners don’t realize: specialized investors actively seek out properties with liens. These professionals understand lien resolution, have the resources to handle complex situations, and can offer helpful solutions when traditional selling methods fail.

Understanding investors who buy houses with liens: how to find & work with them can transform what seems like an impossible situation into a manageable transaction. Whether dealing with tax liens, judgment liens, mechanic’s liens, or multiple encumbrances, the right investor can navigate these challenges and provide a clear path forward.

Key Takeaways

- Specialized lien investors exist specifically to purchase properties with title problems, offering cash solutions when traditional buyers cannot help

- Different types of investors handle liens differently—some pay them off at closing, others negotiate settlements, and some specialize in specific lien types

- Finding reputable lien investors requires research through local real estate investment groups, online directories, and professional referrals

- Working with lien investors typically involves property assessment, lien verification, and negotiated offers that account for payoff costs

- The right investor provides transparent communication, fair offers, and handles the complex title work required to clear encumbrances

Understanding Liens and Why They Complicate Sales

A lien represents a legal claim against property, giving creditors the right to collect debts from sale proceeds. Think of it like a lock on a treasure chest—the property cannot transfer cleanly until the lien holder receives payment or releases their claim.

Common Types of Property Liens

Tax Liens emerge when property owners fall behind on federal, state, or local taxes. These liens take priority over most other claims and can lead to foreclosure if unresolved. Property tax liens are particularly urgent because counties can sell the property at auction to recover unpaid taxes.

Judgment Liens result from court decisions where someone wins a lawsuit against the property owner. These can stem from unpaid debts, medical bills, or civil judgments. Judgment liens on property attach to all real estate the debtor owns in that county.

Mechanic’s Liens protect contractors, subcontractors, and suppliers who performed work or provided materials but weren’t paid. These liens can surprise property owners who hired a general contractor, unaware that subcontractors filed separate claims.

HOA Liens occur when homeowners associations pursue unpaid dues, fines, or special assessments. These can accumulate quickly and sometimes take priority over mortgages.

Mortgage Liens represent the most common encumbrance—the lender’s secured interest in the property until the loan is repaid.

Why Traditional Buyers Avoid Liens

Most conventional buyers cannot purchase properties with unresolved liens. Their lenders require clear title as a condition of financing. Title insurance companies refuse to insure properties with outstanding encumbrances. This creates a catch-22: sellers need sale proceeds to pay off liens, but cannot complete the sale without clearing the liens first.

The complete guide to property liens explains how these encumbrances create barriers to traditional sales and why specialized solutions become necessary.

Who Are Investors Who Buy Houses with Liens?

Lien investors represent a specialized segment of the real estate investment community. These professionals possess three critical advantages: cash resources, lien resolution expertise, and established relationships with title companies and attorneys.

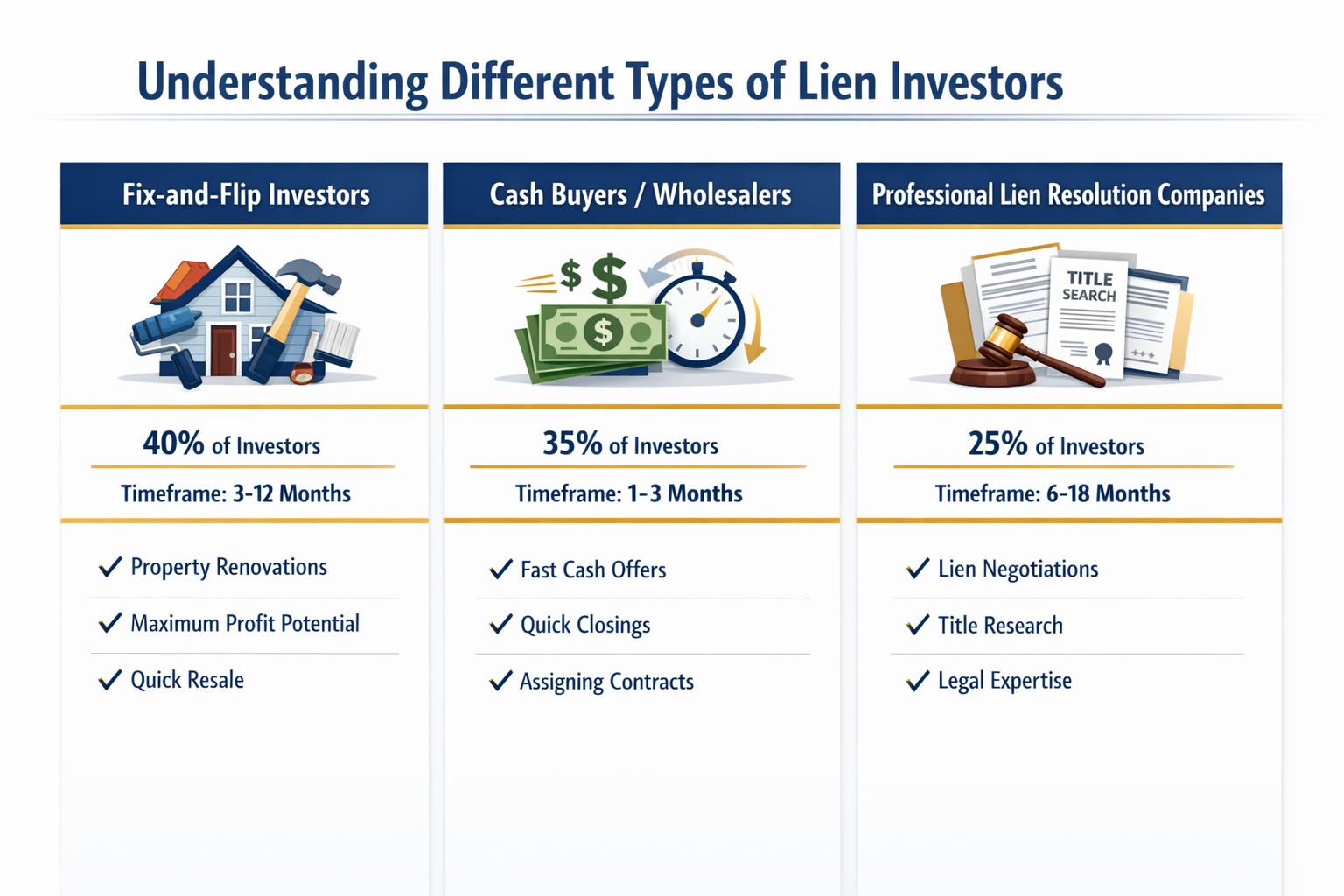

Types of Lien Investors

Fix-and-Flip Investors purchase properties with liens, resolve the title issues, renovate the homes, and resell for profit. They view liens as negotiable obstacles rather than deal-breakers. Their business model accounts for lien payoff costs in their purchase calculations.

Cash Buyers and Wholesalers specialize in quick transactions, often closing within days or weeks. They purchase properties as-is, including all encumbrances, then either resolve the liens themselves or assign the contract to another investor. Companies like Sure Path Property Solutions focus specifically on helping property owners navigate complicated situations including liens and judgments.

Professional Lien Resolution Companies combine real estate investment with legal expertise. These firms employ or partner with attorneys who specialize in lien negotiation, settlement, and removal. They handle everything from simple tax liens to complex multi-lien situations.

Portfolio Investors acquire properties for long-term rental income. They’re often willing to work through lien complications because they focus on the property’s income potential rather than quick resale.

What Makes These Investors Different

Traditional buyers need everything perfect. Lien investors expect problems and build their business models around solving them. They understand lien priority, negotiation strategies, and title curative processes. Most importantly, they have cash reserves to pay off liens at closing without depending on mortgage financing.

These investors also maintain relationships with:

- Title companies experienced in complex closings

- Real estate attorneys specializing in lien resolution

- County tax offices and government agencies

- Other investors who might purchase the property after lien removal

This network enables them to resolve issues that would stop conventional transactions cold.

Why Investors Buy Properties with Liens

The business model makes sense when you understand the numbers. Properties with liens typically sell at significant discounts—often 20% to 40% below market value. This discount compensates investors for:

- Time and effort resolving title issues

- Risk that liens might be larger than expected

- Carrying costs during the resolution period

- Professional fees for attorneys and title work

The Profit Opportunity

Consider a property worth $200,000 with a $30,000 tax lien. Traditional buyers cannot purchase it. The owner faces foreclosure. An investor might offer $140,000, pay the $30,000 lien at closing, invest $20,000 in repairs, and resell for $200,000. After closing costs and holding expenses, they profit $15,000 to $20,000.

The property owner receives $110,000 after the lien payoff ($140,000 purchase price minus $30,000 lien), avoiding foreclosure and escaping a burdensome situation. Both parties benefit from the transaction.

The Service Component

Reputable lien investors provide genuine helpful solutions. They prevent foreclosures, help families escape financial stress, and return blighted properties to productive use. The best investors view themselves as problem-solvers rather than opportunists, offering expert service and trustworthy guidance through complex situations.

How to Find Investors Who Buy Houses with Liens

Finding the right investor requires strategic research and careful vetting. Not all investors possess equal expertise, resources, or integrity.

Online Search Strategies

Start with targeted searches like “cash buyers for houses with liens [your city]” or “investors who buy tax lien properties [your state].” Look beyond the first page of results. Examine company websites for:

- Specific experience with lien properties

- Educational content demonstrating expertise

- Clear contact information and physical addresses

- Professional presentation suggesting established operations

- Testimonials or case studies from previous clients

Cash buyers for tax lien properties and similar specialized services often maintain informative websites explaining their processes.

Local Real Estate Investment Groups

Real Estate Investment Associations (REIAs) exist in most metropolitan areas. These groups host monthly meetings where investors network and share opportunities. Attending a meeting provides direct access to investors who specialize in problem properties.

Ask group members: “Who handles properties with title issues?” or “Which investors work with liens and judgments?” The industry experts in these groups typically know who possesses genuine expertise versus who just claims it.

Real Estate Attorneys and Title Companies

Professionals who regularly handle complex closings know which investors deliver on their promises. Ask real estate attorneys: “Which investors do you work with on lien properties?” Their recommendations carry weight because they’ve witnessed these investors successfully close difficult transactions.

Title companies also maintain relationships with investors who specialize in curative work. A title officer might say, “We close several lien properties monthly with ABC Investment Company. They’re professional and reliable.”

Wholesaler Networks

Real estate wholesalers connect property owners with investors. While some wholesalers lack expertise, others maintain extensive networks of specialized buyers. A quality wholesaler can quickly identify investors interested in lien properties and facilitate introductions.

Direct Mail and Marketing

Some investors actively market their services through:

- Direct mail campaigns (“We Buy Houses with Tax Problems”)

- Billboard advertising

- Online ads targeting lien-related searches

- Social media presence in local real estate groups

While marketing doesn’t guarantee quality, established investors with consistent advertising often possess the resources and experience to handle complex transactions.

Professional Referrals

Ask for recommendations from:

- Bankruptcy attorneys who work with clients facing foreclosure

- Tax professionals helping clients with IRS or state tax liens

- Probate attorneys dealing with inherited properties with liens

- Foreclosure defense lawyers seeking alternatives for clients

These professionals encounter lien situations regularly and know which investors provide helpful guidance and friendly service.

Vetting and Choosing the Right Investor

Finding investors is step one. Selecting the right partner requires careful evaluation. Remember, you’re trusting this person or company to handle a complex financial and legal transaction.

Essential Questions to Ask

“How many lien properties have you purchased in the past year?”

Specific numbers matter. “We buy them all the time” sounds good but means nothing. An investor who purchased 15 lien properties last year has relevant, current experience. Someone who bought two properties five years ago does not.

“What types of liens have you handled?”

Investors might specialize in tax liens but lack experience with judgment liens or mechanic’s liens. Ensure their expertise matches your situation. Selling a house with a tax lien differs from handling judgment liens, requiring different knowledge and processes.

“Can you provide references from recent sellers?”

Legitimate investors readily provide references. Speak with previous clients about their experiences. Ask: “Did they deliver what they promised? Were they transparent? Did the closing happen on schedule?”

“What is your typical timeline from offer to closing?”

Understanding the timeline helps set realistic expectations. Some investors close in 7-10 days. Others need 30-45 days to complete title work and lien negotiations. Neither is wrong, but you need accurate information for planning.

“How do you determine your offer price?”

Reputable investors explain their calculation methodology. They should account for:

- Current market value

- Lien payoff amounts

- Repair costs

- Holding costs and financing

- Profit margin

- Risk factors

Transparency in pricing demonstrates professionalism and builds trust.

“Who handles the lien resolution process?”

Some investors manage everything internally. Others partner with title companies or attorneys. Understanding the process helps you know what to expect and who will communicate with you.

Red Flags to Avoid

Pressure tactics suggesting you must decide immediately or the offer expires represent manipulation, not helpful solutions. Legitimate investors understand that major decisions require time and consideration.

Requests for upfront fees before closing should trigger alarm bells. Reputable investors make money from successful transactions, not from charging desperate property owners fees that yield nothing.

Vague or evasive answers to direct questions suggest either inexperience or dishonesty. Industry experts provide clear, specific responses because they know their business thoroughly.

Unwillingness to use escrow or title companies indicates potential fraud. All legitimate real estate transactions should close through neutral third parties who ensure proper fund disbursement and title transfer.

Offers that seem too good to be true probably are. If an investor offers significantly more than others for a property with substantial liens, question their business model and ability to close.

Verifying Credentials and Reputation

Check online reviews across multiple platforms: Google, Facebook, Better Business Bureau, Trustpilot. Look for patterns in feedback rather than isolated complaints. Every business receives occasional negative reviews, but consistent complaints about specific issues reveal problems.

Verify business registration through your state’s Secretary of State website. Legitimate companies maintain proper business licenses and registrations.

Search for legal actions through county court records. Investors sued repeatedly for fraud, contract disputes, or failure to close should be avoided.

Confirm insurance and bonding where applicable. Professional investors carry appropriate liability insurance and may be bonded, providing additional protection.

Request proof of funds before signing contracts. Investors claiming they can close quickly with cash should demonstrate they actually have the resources. A bank statement or letter from their lender confirms their capability.

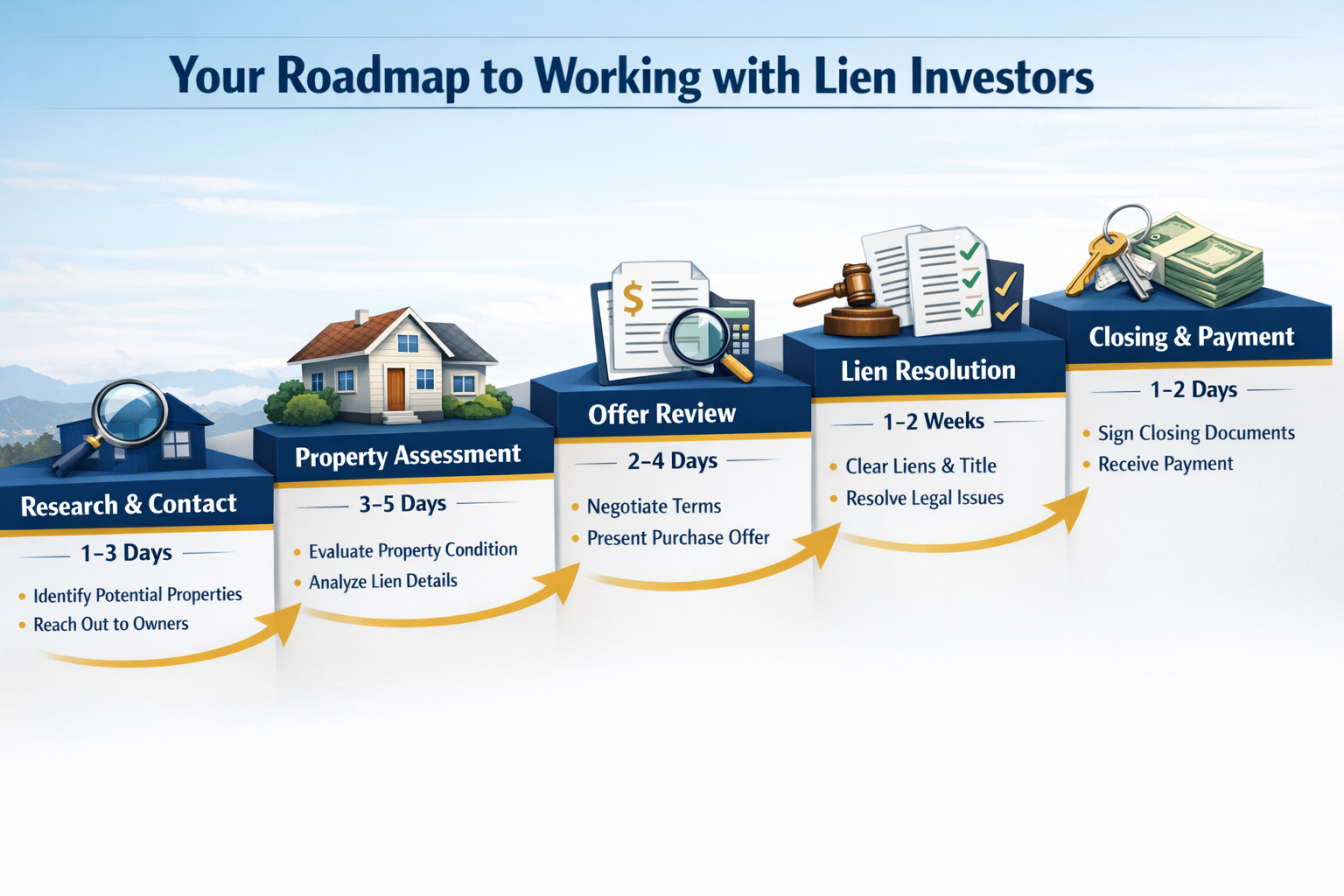

The Process of Working with Lien Investors

Understanding the typical transaction process helps set expectations and prepare appropriately. While specific steps vary by investor and situation, most transactions follow a similar pattern.

Initial Contact and Property Information

The process begins when you contact the investor or they respond to your inquiry. Be prepared to provide:

- Property address and basic details (bedrooms, bathrooms, square footage)

- Current condition assessment

- Known lien information (types, amounts, lien holders)

- Your timeline and motivation for selling

- Property access for inspection

Honesty matters tremendously here. Concealing liens or property problems creates distrust and can derail transactions. Reputable investors appreciate transparency and work more effectively when they understand the complete situation.

Property Assessment and Lien Verification

Most investors conduct two parallel investigations:

Physical property inspection evaluates condition, repair needs, and market value. This might be a simple walk-through or a detailed inspection depending on the investor’s process.

Title search and lien verification confirms exactly what encumbrances exist. Investors order preliminary title reports showing all recorded liens, judgments, and claims. This research often reveals liens the property owner didn’t know existed.

Surprises during this phase are common. A complete guide to property liens helps property owners understand what might appear on title reports.

Offer Presentation and Negotiation

After completing their due diligence, investors present offers. Professional investors provide written offers explaining:

- Purchase price

- Liens to be paid at closing and estimated amounts

- Net proceeds the seller will receive

- Closing timeline

- Contingencies (if any)

- Earnest money deposit amount

The offer should clearly show the math. For example:

| Item | Amount |

|---|---|

| Purchase Price | $150,000 |

| Tax Lien Payoff | -$25,000 |

| Judgment Lien Payoff | -$8,000 |

| Closing Costs | -$3,000 |

| Net to Seller | $114,000 |

This transparency enables informed decision-making. You can evaluate whether the net proceeds meet your needs and compare offers from multiple investors.

Negotiation may involve:

- Adjusting the purchase price based on property condition

- Modifying the timeline to accommodate your needs

- Clarifying which liens the investor will pay versus which you must resolve

- Determining responsibility for utilities, property taxes, or other costs through closing

Contract Execution and Due Diligence Period

Once you accept an offer, both parties sign a purchase agreement. This contract should include:

- All material terms discussed during negotiation

- Due diligence period allowing the investor to complete final verification

- Contingencies protecting both parties

- Default provisions explaining what happens if either party fails to perform

- Closing date and location

During the due diligence period (typically 7-30 days), the investor:

- Completes final title work

- Confirms lien amounts with creditors

- Arranges financing or verifies cash availability

- Obtains final property inspections

- Coordinates with the closing attorney or title company

Property owners should use this time to:

- Prepare to vacate the property (if occupied)

- Gather necessary documents (deed, property tax records, etc.)

- Notify utility companies of the pending sale

- Make arrangements for personal property removal

Lien Resolution and Title Clearing

This phase involves the most complexity. The investor or their title company contacts each lien holder to:

- Verify current payoff amounts including interest and penalties

- Negotiate settlements when possible (many lien holders accept less than the full amount)

- Obtain payoff letters stating exact amounts required for lien release

- Coordinate timing so all liens can be satisfied at closing

How to sell a house with a lien requires careful coordination between multiple parties. The title company ensures that lien payoffs happen simultaneously with the property transfer, preventing any gaps in the chain of title.

Some liens require additional steps:

- IRS tax liens need specific forms and waiting periods

- Judgment liens may require court filings for release

- Mechanic’s liens might need contractor negotiations

- HOA liens often involve bringing accounts current plus paying attorney fees

Experienced investors handle these complications routinely, working with their network of professionals to resolve each issue.

Closing and Fund Disbursement

Closing day brings everything together. The title company or closing attorney:

- Collects all necessary documents (deed, lien releases, tax certificates, etc.)

- Verifies the investor’s funds are available

- Prepares the settlement statement showing all financial transactions

- Conducts the closing meeting where parties sign documents

- Disburses funds to lien holders and the seller

- Records the new deed transferring ownership

- Ensures lien releases are recorded, clearing the title

The seller receives net proceeds via wire transfer or cashier’s check. The investor receives the property with clear title. All lien holders receive payment and release their claims.

Professional investors ensure smooth closings because they’ve coordinated everything in advance. Last-minute surprises are rare when working with experienced professionals who provide expert service.

What to Expect: Timeline and Typical Offers

Managing expectations prevents disappointment and helps property owners make informed decisions.

Realistic Timelines

Fast-track sales with simple lien situations can close in 7-14 days. This requires:

- Cooperative lien holders who respond quickly

- Clear title with no unexpected issues

- Cash investor with immediate funds availability

- Motivated seller ready to move quickly

Standard transactions typically take 30-45 days, allowing time for:

- Complete title research

- Lien verification and negotiation

- Property inspection and appraisal

- Document preparation and review

- Coordination between all parties

Complex situations involving multiple liens, legal disputes, or title problems may require 60-90 days or longer. Title problems at closing can extend timelines when unexpected issues emerge.

Factors affecting timeline include:

- Number and types of liens (more liens = more complexity)

- Lien holder responsiveness (government agencies often move slowly)

- Title issues beyond liens (breaks in chain of title, missing heirs, etc.)

- Property condition (severe damage may require additional inspections)

- Local government processing times (recording offices, tax offices, courts)

Understanding Offer Amounts

Investors calculate offers using a formula that accounts for all costs and risks:

After Repair Value (ARV) – Repair Costs – Lien Payoffs – Holding Costs – Profit Margin = Maximum Purchase Price

For example:

- ARV: $200,000

- Repair Costs: $30,000

- Lien Payoffs: $40,000

- Holding Costs: $10,000

- Desired Profit: $30,000

- Maximum Offer: $90,000

This might seem low compared to the $200,000 market value, but remember the investor must:

- Pay $40,000 to clear liens

- Invest $30,000 in repairs

- Cover $10,000 in carrying costs, financing, and transaction fees

- Accept risk that estimates might be wrong

The seller receives $50,000 net proceeds ($90,000 purchase price minus $40,000 in liens). While less than full market value, this represents a helpful solution when traditional sales aren’t possible.

Comparing Multiple Offers

Smart sellers obtain offers from several investors to ensure fair pricing. When comparing offers, consider:

Net proceeds matter more than purchase price. An offer of $100,000 with the seller paying $30,000 in liens nets $70,000. An offer of $90,000 where the investor pays all liens also nets $70,000. They’re equivalent.

Closing timeline affects value. Receiving $65,000 in 10 days might be worth more than $70,000 in 90 days, especially when facing foreclosure or financial pressure.

Investor credibility impacts certainty. An offer from a proven investor with references and track record beats a higher offer from an unverified buyer who might not close.

Terms and contingencies create risk. Offers with numerous contingencies and escape clauses provide less certainty than clean offers with minimal conditions.

Communication and professionalism indicate how smoothly the transaction will proceed. Investors who respond promptly, explain clearly, and demonstrate expertise typically deliver better experiences than those who are difficult to reach or vague in their communications.

Benefits of Working with Specialized Lien Investors

Choosing the right investor provides advantages beyond simply completing the sale.

Speed and Certainty

Traditional sales of lien properties often fail. Buyers back out when they discover title issues. Lenders refuse financing. Deals collapse after weeks or months of effort. Cash buyers for problem properties provide certainty because they:

- Don’t need financing that could fall through

- Expect problems and build them into their offers

- Have systems for resolving common issues

- Close quickly when needed

This certainty matters tremendously when facing foreclosure deadlines, financial emergencies, or family situations requiring quick resolution.

Expertise and Problem-Solving

Lien investors bring specialized knowledge that benefits sellers:

- Lien negotiation skills often reduce payoff amounts

- Title expertise resolves complex ownership issues

- Legal resources handle court filings and releases

- Government relationships expedite tax lien processes

This expertise saves sellers time, stress, and often money. An investor who negotiates a $50,000 tax lien down to $35,000 effectively increases the seller’s net proceeds by $15,000.

Comprehensive Solutions

The best investors address multiple problems simultaneously. A property might have:

- Tax liens

- Judgment liens

- Deferred maintenance

- Code violations

- Inherited ownership complications

Sure Path Property Solutions and similar companies specialize in coordinating solutions for multiple overlapping problems, providing helpful guidance through complex situations that would overwhelm most property owners.

Avoiding Foreclosure and Credit Damage

Selling to a lien investor before foreclosure:

- Prevents foreclosure from appearing on credit reports

- Stops accumulating penalties and interest on liens

- Eliminates deficiency judgment risk

- Provides some equity recovery versus losing everything

Even modest net proceeds beat foreclosure, which yields nothing and damages credit for years.

Stress Reduction and Peace of Mind

The emotional burden of dealing with liens, threatening letters, and legal complications weighs heavily on property owners. Working with professional investors who handle everything provides:

- Relief from constant worry about legal actions

- Freedom from property maintenance burdens

- Escape from overwhelming financial pressure

- Confidence that experts are managing the situation

This psychological benefit, while intangible, holds tremendous value for families struggling with property problems.

Potential Drawbacks and How to Mitigate Them

Honest evaluation requires acknowledging potential disadvantages and how to address them.

Lower Sale Prices

Lien investors pay less than market value—sometimes significantly less. This reflects:

- Real costs they must cover (lien payoffs, repairs, holding costs)

- Risk they assume (unexpected liens, title problems, market changes)

- Profit they need to justify the investment

Mitigation Strategy: Obtain multiple offers to ensure competitive pricing. Consider whether the speed and certainty justify the discount versus attempting a traditional sale that might fail or take much longer.

Risk of Unscrupulous Operators

Some individuals masquerade as professional investors while engaging in:

- Equity stripping (buying properties for far less than they’re worth)

- Deed theft (obtaining ownership through deception)

- Fee scams (charging upfront fees and disappearing)

Mitigation Strategy: Thoroughly vet investors using the criteria discussed earlier. Work only with established companies having verifiable track records. Use reputable title companies or attorneys for closing. Never pay upfront fees or sign documents you don’t understand.

Limited Negotiating Power

Sellers with liens face limited options, reducing negotiating leverage. Investors know that traditional buyers won’t purchase the property, potentially leading to lowball offers.

Mitigation Strategy: Create competition by obtaining multiple offers. Consider alternative solutions like negotiating tax lien payoff directly with creditors, then pursuing traditional sales. Consult with real estate attorneys about all available options before committing to any single approach.

Emotional Attachment and Regret

Selling quickly at a discount may lead to later regret, especially with inherited family properties or homes with sentimental value.

Mitigation Strategy: Take time to process the decision emotionally. Consult family members if appropriate. Consider whether other solutions might preserve ownership while addressing the lien problems. Ensure the decision aligns with both financial needs and emotional readiness.

Alternative Options to Consider

While lien investors provide valuable solutions, other approaches might better serve specific situations.

Direct Lien Negotiation

Contacting lien holders directly to negotiate settlements can reduce amounts owed. Many creditors accept partial payment rather than pursuing expensive legal action. Tax authorities sometimes offer:

- Payment plans spreading costs over time

- Penalty abatement reducing total amounts

- Offers in compromise accepting less than full debt

Successfully negotiating liens down might enable traditional sales at higher prices, yielding better net proceeds.

Traditional Sale with Lien Payoff

If equity exceeds lien amounts, traditional sales remain possible. Work with:

- Experienced real estate agents who understand lien transactions

- Title companies skilled in complex closings

- Real estate attorneys who can coordinate lien payoffs

This approach takes longer but might yield higher net proceeds when market conditions support it.

Refinancing to Pay Liens

Property owners with good credit might refinance, using loan proceeds to pay liens and retain ownership. This works when:

- Property value significantly exceeds lien amounts

- Credit scores support loan approval

- Income justifies monthly payments

- Long-term ownership makes financial sense

Loan Modification or Forbearance

For mortgage-related issues, lenders sometimes offer:

- Loan modifications reducing payments

- Forbearance agreements temporarily suspending payments

- Repayment plans spreading missed payments over time

These solutions help property owners keep homes rather than selling.

Bankruptcy Protection

Bankruptcy can:

- Stop foreclosure proceedings temporarily

- Discharge certain liens (depending on type)

- Provide time to reorganize finances

- Protect assets while resolving debts

Consult bankruptcy attorneys to understand whether this option serves your situation.

Family Assistance or Private Loans

Family members might:

- Loan money to pay liens

- Purchase the property at fair value

- Co-sign refinancing to enable lien payoff

Private lenders or hard money loans provide another option, though typically at higher interest rates.

Each alternative has advantages and disadvantages. The best choice depends on individual circumstances, timeline needs, financial resources, and long-term goals.

Real-World Scenarios: When Lien Investors Make Sense

Understanding specific situations helps property owners recognize when working with lien investors represents the best solution.

Scenario 1: Inherited Property with Tax Liens

Maria inherited her grandmother’s house worth $180,000. She discovered $45,000 in unpaid property taxes accumulated over eight years. Living in another state with her own home, Maria couldn’t afford to pay the liens or maintain two properties.

Traditional buyers wouldn’t purchase the property with tax liens. Real estate agents suggested she pay the taxes first, but Maria lacked the funds. The county threatened property tax lien foreclosure.

A lien investor offered $110,000, paid the $45,000 tax lien at closing, and gave Maria $65,000 net proceeds. While less than the $180,000 market value, this solution:

- Prevented foreclosure

- Eliminated ongoing property expenses

- Provided cash without upfront investment

- Resolved the situation in 30 days

For Maria, this represented a helpful solution to an otherwise impossible situation.

Scenario 2: Multiple Liens from Business Failure

James owned a rental property worth $250,000 but faced multiple liens totaling $85,000 from a failed business:

- $35,000 IRS tax lien

- $28,000 judgment lien from a lawsuit

- $22,000 state tax lien

He owed $140,000 on the mortgage, leaving theoretical equity of $25,000 ($250,000 value – $140,000 mortgage – $85,000 liens). However, no traditional buyer would purchase the property, and James couldn’t afford to pay the liens.

An investor offered $165,000, paid off the mortgage and all liens at closing, and James received $15,000. While less than the theoretical $25,000 equity, this outcome:

- Cleared all liens and judgments

- Eliminated the mortgage obligation

- Provided cash to rebuild financially

- Avoided bankruptcy and foreclosure

The investor’s expertise in selling house with judgment lien situations made the transaction possible.

Scenario 3: Divorce with Contested Liens

After a contentious divorce, Sarah and Tom co-owned a house worth $200,000 with $120,000 mortgage and $15,000 in liens from unpaid contractor bills. Neither could afford to buy out the other, and they disagreed about responsibility for the liens.

Traditional sales stalled because buyers backed out upon discovering the liens and ownership disputes. The situation dragged on for 18 months, with both parties paying half the mortgage while living elsewhere.

A lien investor offered $150,000, paid the mortgage and liens at closing, and split the $15,000 net proceeds between Sarah and Tom. While minimal profit, this solution:

- Ended the financial drain of dual housing costs

- Resolved ownership disputes

- Eliminated ongoing conflict

- Allowed both parties to move forward

Sometimes the value lies in ending a difficult situation rather than maximizing financial return.

Working with Sure Path Property Solutions

Sure Path Property Solutions specializes in helping property owners navigate exactly these types of complicated situations. The company focuses on:

Comprehensive Problem-Solving

Rather than simply buying properties, Sure Path coordinates solutions for multiple overlapping issues:

- Lien resolution for tax liens, judgment liens, and mechanic’s liens

- Title clearing for breaks in chain of title, missing heirs, and ownership disputes

- Probate assistance for inherited properties

- Multi-owner coordination when multiple heirs or co-owners disagree

This comprehensive approach addresses the full scope of challenges property owners face, not just isolated problems.

Transparent Communication

The company provides:

- Clear explanations of complex legal and financial issues

- Detailed offer breakdowns showing exactly how prices are calculated

- Regular updates throughout the transaction process

- Honest assessments of realistic timelines and outcomes

This transparency builds trust and helps property owners make informed decisions.

Professional Network

Sure Path maintains relationships with:

- Title companies experienced in complex transactions

- Real estate attorneys specializing in lien resolution

- County tax offices and government agencies

- Other investors for situations outside their focus

This network enables solutions even for the most complicated situations.

Ethical Standards

The company operates with:

- Fair pricing based on market conditions and actual costs

- No upfront fees charged to property owners

- Respectful treatment of people facing difficult circumstances

- Commitment to helpful solutions rather than exploitation

These ethical standards distinguish professional companies from opportunistic operators.

Property owners facing liens, title problems, or complicated ownership situations can contact Sure Path Property Solutions for a no-obligation assessment of their situation and potential solutions.

Legal and Financial Considerations

Understanding the legal and financial implications helps property owners protect their interests.

Tax Implications of Lien Sales

Selling property with liens can create tax consequences:

Capital gains taxes apply to the difference between sale price and cost basis. Consult tax professionals about:

- Exclusions for primary residences

- Loss deductions if selling below cost basis

- Installment sales spreading tax liability over time

Cancellation of debt income might apply if lien holders forgive portions of debts. The IRS treats forgiven debt as taxable income in many situations.

1099-S reporting requires sellers to report real estate sales to the IRS. Ensure accurate reporting to avoid future problems.

Legal Protections and Rights

Property owners maintain rights throughout the process:

Right to fair dealing protects against fraud, misrepresentation, and deceptive practices. State real estate laws provide remedies for violations.

Right to representation allows property owners to hire attorneys, even when working with investors. Legal counsel ensures contracts protect your interests.

Right to rescission in some situations allows canceling contracts within specific timeframes. Understand rescission rights before signing.

Right to full disclosure requires investors to reveal material facts about transactions. Hidden fees, undisclosed relationships, or concealed information violate this right.

Contract Considerations

Ensure purchase agreements include:

Clear purchase price and net proceeds calculations

Specific lien payoff responsibilities identifying who pays what

Closing timeline with reasonable deadlines

Contingencies protecting both parties appropriately

Default provisions explaining remedies if either party fails to perform

Dispute resolution procedures for handling disagreements

Have attorneys review contracts before signing, especially for complex transactions.

Title Insurance and Closing Protection

Insist on:

Owner’s title insurance protecting against future claims

Title company closing ensuring proper fund disbursement

Recorded lien releases confirming all liens are properly removed

Final title policy showing clear ownership transfer

These protections prevent future problems and ensure the transaction completes properly.

Questions to Ask Before Signing Anything

Protect yourself by obtaining clear answers to critical questions:

About the Investor

- How long have you been buying properties with liens?

- How many lien properties did you purchase last year?

- Can you provide three recent references?

- What is your business structure and registration?

- Do you have proof of funds for this purchase?

About the Offer

- How did you calculate this offer amount?

- What comparable sales did you use for valuation?

- Which liens will you pay and which am I responsible for?

- What are the exact net proceeds I will receive?

- Are there any fees or costs I must pay?

About the Process

- What is the step-by-step process from here to closing?

- What is the realistic timeline for closing?

- Which title company or attorney will handle closing?

- What happens if unexpected liens are discovered?

- Can I back out if I change my mind? What are the consequences?

About Lien Resolution

- How will you verify current lien amounts?

- Will you negotiate liens down or pay full amounts?

- What happens if lien amounts are higher than expected?

- How will you ensure all liens are properly released?

- What if a lien holder refuses to release their claim?

Legitimate investors welcome these questions and provide clear, specific answers. Evasive or vague responses suggest problems.

Conclusion: Making the Right Decision for Your Situation

Discovering that your property has liens can feel overwhelming. Traditional selling methods often fail, leaving property owners feeling trapped with limited options. Understanding that investors who buy houses with liens: how to find & work with them provides a path forward transforms this challenging situation into a manageable transaction.

The key lies in finding the right investor—someone with genuine expertise, adequate resources, and ethical standards. Not all investors are equal. Some provide helpful solutions and expert service. Others exploit vulnerable property owners. Careful vetting, thorough research, and professional guidance help distinguish between the two.

For many property owners, working with specialized lien investors represents the best available solution. The speed, certainty, and expertise these professionals provide outweigh the discount from market value. Avoiding foreclosure, eliminating financial stress, and moving forward with life holds tremendous value beyond simple dollar amounts.

However, lien investors aren’t the only option. Direct lien negotiation, traditional sales with lien payoff, refinancing, or other alternatives might better serve specific situations. Taking time to explore all options, consult with professionals, and make informed decisions leads to better outcomes.

Next Steps

If facing a property with liens, consider these action steps:

1. Gather complete information about all liens, including types, amounts, and lien holders. Order a preliminary title report if needed.

2. Assess your timeline and priorities. How quickly must you sell? What net proceeds do you need? What outcomes matter most?

3. Research multiple solutions. Contact several lien investors, explore direct negotiation with lien holders, and consult with real estate attorneys about all available options.

4. Obtain multiple offers if pursuing the investor route. Compare not just prices but also timelines, terms, and investor credibility.

5. Seek professional advice from real estate attorneys, tax professionals, and financial advisors before making final decisions.

6. Verify everything before signing contracts. Check references, confirm credentials, and ensure you understand all terms and implications.

7. Use reputable closing professionals. Insist on title company or attorney closings with proper protections.

The situation might seem impossible now, but helpful solutions exist. Thousands of property owners successfully sell lien properties each year, resolving their challenges and moving forward. With the right information, careful vetting, and professional guidance, you can join them.

Companies like Sure Path Property Solutions exist specifically to help property owners navigate these complicated situations. Whether dealing with back taxes on inherited property, selling house fast with liens, or other complex real estate challenges, professional help is available.

Don’t let liens trap you in an impossible situation. Explore your options, find trustworthy service providers, and take action toward resolution. The path forward exists—you just need to find it.

Sure Path is a family-owned, curative-title cash buyer. We handle the paperwork and pay what’s owed at closing — no fees, no repairs, no pressure.