Property Liens in Texas: Complete Guide to Types, Filing & Removal

Discovering a lien on your Texas property can feel like hitting an unexpected roadblock on what should be a straightforward journey. Whether you’re trying to sell, refinance, or simply understand what you own free and clear, property liens create complications that demand attention. The good news? Understanding Property Liens in Texas: Complete Guide to Types, Filing & Removal empowers property owners to navigate these challenges with confidence and clarity.

A property lien represents a legal claim against your real estate, giving creditors the right to seek payment from your property’s value. In Texas, where property rights run deep and the real estate market moves fast, liens can significantly impact your ability to control, sell, or transfer ownership of your land or home. But with the right knowledge and helpful guidance, even the most complex lien situations can be resolved.

This comprehensive guide walks through everything Texas property owners need to know about liens—from the different types you might encounter to the specific steps for removal. Whether you’re dealing with tax liens, contractor claims, or judgment liens, understanding your options is the first step toward finding helpful solutions.

Key Takeaways

- Property liens are legal claims against Texas real estate that must be satisfied before clear title can be transferred to a new owner

- Multiple lien types exist in Texas, including tax liens, mechanic’s liens, judgment liens, HOA liens, and mortgage liens—each with distinct filing and removal processes

- Lien priority matters significantly—the order in which liens are filed typically determines which creditors get paid first during a sale or foreclosure

- Removal options include full payment, negotiated settlement, lien release, dispute resolution, or waiting for expiration based on statutory timeframes

- Professional assistance from title companies, real estate attorneys, or experienced property solution specialists can simplify the removal process and prevent costly mistakes

What Is a Property Lien in Texas? 📋

A property lien is a legal instrument that gives a creditor a secured interest in your real estate. Think of it as a financial “sticky note” attached to your property’s title that says, “This debt must be paid before ownership can fully transfer.”

In Texas, liens serve as a powerful tool for creditors to ensure they receive payment for debts owed. When someone files a lien against your property, they’re essentially creating a public record that alerts potential buyers, lenders, and other interested parties that money is owed.

How Property Liens Work in Texas

The Texas Property Code and various statutes govern how liens are created, filed, and enforced. Here’s the basic mechanism:

- A debt is created between you (the property owner) and a creditor

- The creditor files a lien with the county clerk’s office where your property is located

- The lien attaches to your property title, creating a cloud on ownership

- The lien must be satisfied (paid or resolved) before you can sell or refinance with clear title

Important distinction: A lien doesn’t mean you lose ownership of your property immediately. You still own the property and can continue living there or using it. However, the lien creates a legal encumbrance that limits your ability to transfer clean title to someone else.

Voluntary vs. Involuntary Liens

Texas recognizes two broad categories of liens:

Voluntary liens are those you agree to when borrowing money. The most common example is a mortgage lien—you voluntarily grant your lender a lien on your property as security for the loan.

Involuntary liens are imposed without your consent, typically as a result of unpaid debts or legal judgments. These include tax liens, mechanic’s liens, and judgment liens. While you didn’t agree to these liens, they’re legally enforceable nonetheless.

Understanding Property Liens in Texas: Complete Guide to Types

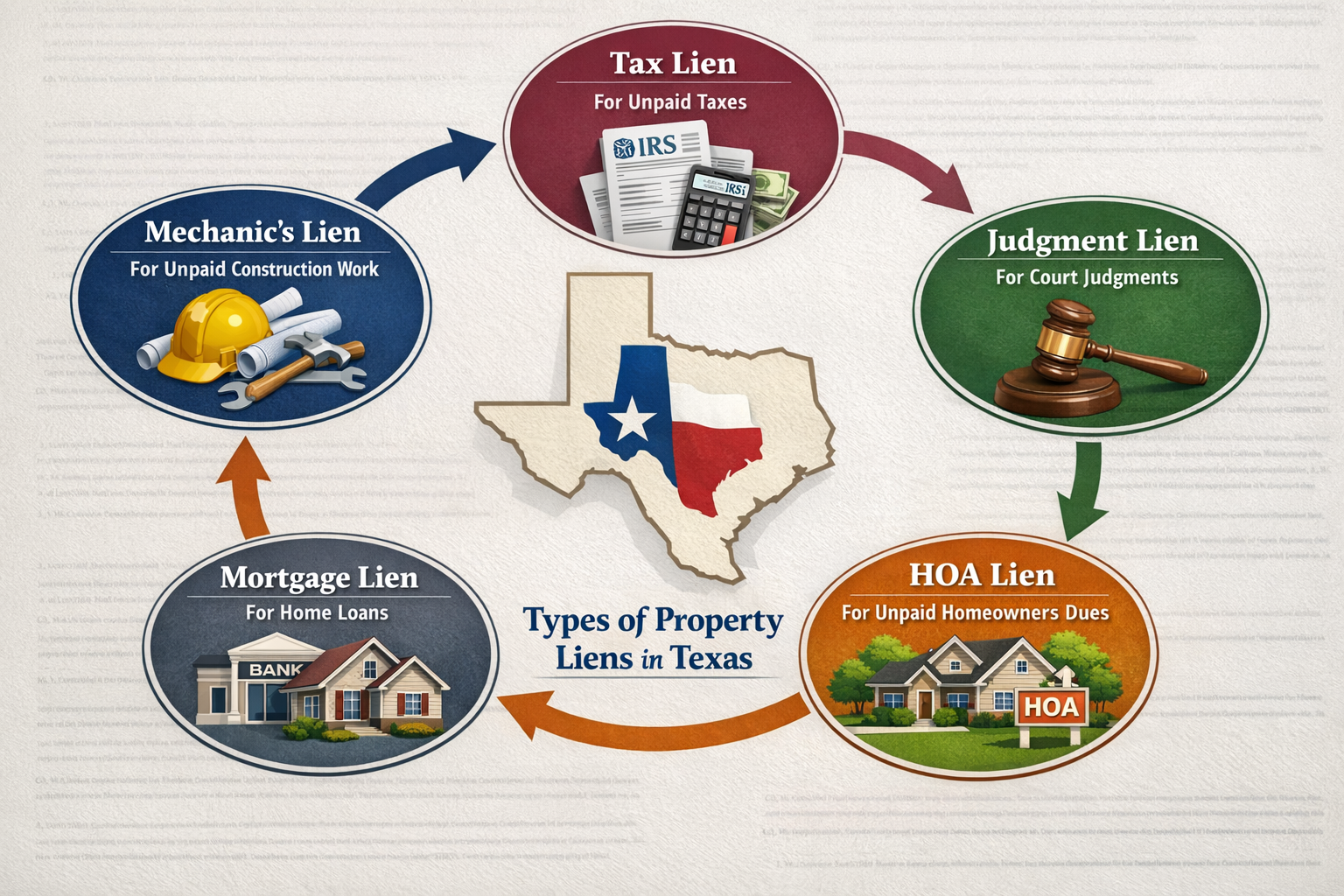

Texas law recognizes several distinct types of property liens, each with unique characteristics, filing requirements, and removal processes. Understanding which type of lien affects your property is essential for developing an effective resolution strategy.

1. Tax Liens (Property Tax and Federal) 💰

Tax liens are among the most serious liens because government entities have powerful collection tools at their disposal.

Property Tax Liens automatically attach to Texas real estate on January 1st of each year for any unpaid property taxes. You don’t receive advance notice—the lien exists by operation of law. Texas counties can foreclose on property tax liens, potentially resulting in the loss of your property at a tax sale.

The timeline is strict:

- Taxes are due January 31st

- Penalties and interest begin February 1st

- Lawsuits for foreclosure can be filed as early as July 1st

Federal Tax Liens are filed by the IRS when you owe back federal income taxes. These liens attach to all your property and rights to property, including real estate. The IRS files a Notice of Federal Tax Lien with the county clerk, creating a public record that severely impacts your credit and ability to sell.

For property owners struggling with tax-related issues, addressing these liens quickly is critical to avoiding foreclosure.

2. Mechanic’s Liens (Construction and Contractor Liens) 🔨

Texas provides strong protections for contractors, subcontractors, and suppliers who improve your property but don’t receive payment. A mechanic’s lien (also called a construction lien) allows these parties to place a claim against your property.

Key requirements for mechanic’s liens in Texas:

- Proper notice must be given before work begins or materials are delivered

- Affidavits must be filed with the county clerk within specific timeframes

- Liens must be perfected within strict deadlines (typically 1-4 months after work completion)

- Lawsuits to foreclose must be filed within specific time limits (usually 1-2 years)

Even if you paid your general contractor in full, you could still face mechanic’s liens from unpaid subcontractors or material suppliers. This makes it essential to obtain lien releases from all parties before making final payment on construction projects.

Understanding how mechanic’s liens work helps property owners protect themselves during renovation or construction projects.

3. Judgment Liens ⚖️

When someone sues you and wins a money judgment, they can convert that judgment into a lien against your real property. In Texas, judgment liens are created by filing an abstract of judgment with the county clerk’s office.

Characteristics of judgment liens:

- Attach to real property in the county where filed

- Valid for 10 years and can be renewed for additional 10-year periods

- Create priority based on filing date

- Can be enforced through execution sale (forced sale of property)

Common sources of judgment liens include:

- Unpaid credit card debts

- Medical bills

- Personal loans

- Business debts

- Court-ordered damages from lawsuits

Property owners dealing with judgment liens have several options for resolution, including payment, settlement, or legal challenges to the underlying judgment.

4. HOA Liens (Homeowners Association Liens) 🏘️

If your property is part of a homeowners association, unpaid HOA dues, assessments, or fines can result in an HOA lien. Texas Property Code gives HOAs significant power to collect debts, including the ability to foreclose.

HOA lien specifics:

- Automatic statutory liens exist for unpaid assessments

- Notice requirements must be followed before foreclosure

- Foreclosure is possible for debts as small as 12 months of assessments

- Priority can be complex, sometimes subordinate to mortgages, sometimes not

HOA liens have become increasingly common as associations aggressively pursue collection. The foreclosure process for HOA liens is often faster and less expensive for the creditor than judicial foreclosure, making these liens particularly threatening.

5. Mortgage Liens (Deed of Trust) 🏦

When you finance a property purchase in Texas, your lender secures the loan with a deed of trust—essentially a mortgage lien. This voluntary lien gives the lender the right to foreclose if you default on loan payments.

Mortgage lien characteristics:

- First priority when properly recorded (senior to most other liens)

- Non-judicial foreclosure is permitted in Texas through the deed of trust

- Remains in effect until the loan is paid in full

- Released through a deed of release or release of lien document

Unlike many other states, Texas allows non-judicial foreclosure, meaning lenders can foreclose without going to court if the deed of trust contains a power of sale clause (which virtually all do).

Lien Priority in Texas: Which Liens Get Paid First? 🥇

Understanding lien priority is crucial when multiple liens exist on the same property. Priority determines the order in which creditors get paid from sale proceeds or foreclosure.

General Priority Rules

In Texas, lien priority typically follows the “first in time, first in right” principle. The lien recorded first usually has priority over liens recorded later.

Standard priority order:

- Property tax liens (always first priority by statute)

- First mortgage or deed of trust (if recorded before other liens)

- Mechanic’s liens (can have priority over mortgages in certain situations)

- Second mortgages and junior liens (in order of recording)

- Judgment liens (based on filing date)

- HOA liens (complex priority rules apply)

Exceptions to the General Rule

Several important exceptions can disrupt the standard priority order:

Property tax liens always take priority over all other liens, regardless of when filed. This is why tax lien foreclosures can wipe out even first mortgages.

Mechanic’s liens can relate back to the date work began or materials were first delivered, potentially giving them priority over mortgages recorded after construction started.

Federal tax liens have special priority rules under federal law that can supersede state law in certain situations.

Why Priority Matters

Lien priority becomes critical when:

- Selling your property — all liens must typically be satisfied from sale proceeds in priority order

- Facing foreclosure — junior lienholders may receive nothing if senior liens consume all equity

- Negotiating settlements — junior lienholders may accept less because they understand their weak position

- Refinancing — new lenders want first priority position, requiring subordination or payoff of existing liens

Understanding where each lien stands in the priority chain helps you develop realistic strategies for resolution.

How Property Liens Are Filed in Texas 📝

The filing process varies by lien type, but understanding the general procedures helps property owners recognize when liens might be filed against their property.

County Clerk Recording

Most property liens in Texas are filed with the county clerk’s office in the county where the property is located. The clerk maintains public records that anyone can search to discover liens against a property.

Standard filing process:

- Creditor prepares the appropriate lien document (abstract of judgment, mechanic’s lien affidavit, notice of federal tax lien, etc.)

- Document is filed with the county clerk along with required filing fees

- Clerk records the lien in the official property records

- Lien becomes public record, searchable by anyone

Notice Requirements

Texas law requires creditors to provide notice to property owners in many lien situations:

- Mechanic’s liens require advance notice of the right to file a lien

- HOA liens require notice before foreclosure can proceed

- Tax liens may require notice before foreclosure sale

- Judgment liens require proper service in the underlying lawsuit

However, property owners should not rely on receiving notice. Regularly checking your property’s title status is wise, especially if you have outstanding debts.

Title Search and Discovery

Property liens are discovered through title searches conducted by:

- Title companies during real estate transactions

- Attorneys performing due diligence

- Property owners checking their own records

- Lenders during refinancing processes

A comprehensive title search examines county records, court records, and other public documents to identify all liens and encumbrances affecting a property.

When you’re ready to sell a property with liens, a thorough title search is the essential first step.

How Property Liens Affect Your Texas Property 🏠

Property liens create several significant consequences that affect your rights and options as a property owner.

Impact on Selling Your Property

You cannot transfer clear title to a buyer while liens remain attached to your property. Title companies will require all liens to be satisfied before issuing title insurance to a new owner.

Your options when selling with liens include:

- Paying off liens from your own funds before closing

- Using sale proceeds to satisfy liens at closing

- Negotiating with lienholders for reduced payoffs

- Working with cash buyers who purchase properties with title issues

Many traditional buyers won’t consider properties with liens, but selling land with liens is still possible with the right approach.

Impact on Refinancing

Lenders require first lien position when refinancing. Any existing liens must either be:

- Paid off through the refinance

- Subordinated (moved to junior position with lienholder’s agreement)

- Resolved before the refinance can close

Liens also damage your credit score, making it harder to qualify for favorable refinancing terms.

Impact on Property Value and Equity

While liens don’t directly reduce your property’s market value, they do reduce your equity—the amount you’d actually receive from a sale after paying all liens.

Example:

- Property market value: $200,000

- First mortgage: $120,000

- Tax lien: $15,000

- Judgment lien: $8,000

- Your actual equity: $57,000 (not $200,000)

Risk of Foreclosure

Many types of liens carry foreclosure rights, meaning creditors can force the sale of your property to satisfy the debt:

- Tax liens — both property tax and IRS liens can result in foreclosure

- Mortgage liens — default leads to foreclosure

- HOA liens — associations can foreclose for unpaid dues

- Mechanic’s liens — contractors can foreclose if the lien is perfected

- Judgment liens — creditors can execute on the judgment through forced sale

Understanding your foreclosure risk helps you prioritize which liens to address first.

Property Liens in Texas: Complete Guide to Filing & Removal Process

Removing a lien from your Texas property requires following specific legal procedures that vary by lien type. Here’s your comprehensive guide to the removal process.

Step 1: Identify All Liens on Your Property

Before you can remove liens, you need to know exactly what you’re dealing with.

How to find liens:

- Order a title search from a title company ($150-$400)

- Search county clerk records yourself (usually free online or small fee)

- Review your credit report for judgment liens

- Check with your mortgage servicer for any recorded liens

- Contact your county tax office for property tax lien information

Create a comprehensive list including:

- Type of lien

- Creditor name and contact information

- Amount owed

- Filing date

- Recording information (book and page or document number)

Step 2: Verify Lien Validity and Amount

Not all recorded liens are valid or accurate. Before paying, verify:

- Is the lien legally enforceable? (proper filing, within statute of limitations)

- Is the amount correct? (request an accounting or payoff statement)

- Has it already been paid? (sometimes releases aren’t filed)

- Is it subject to legal defenses? (improper notice, procedural errors)

Consulting with a real estate attorney can help identify invalid liens that can be challenged rather than paid.

Step 3: Choose Your Removal Strategy

Different situations call for different approaches:

Payment in Full ✅

The most straightforward method is paying the lien in full. Once paid:

- Obtain a release document (release of lien, satisfaction of judgment, etc.)

- Ensure it’s properly executed (notarized if required)

- File the release with the county clerk

- Verify recording and obtain a stamped copy for your records

Pro tip: Never make final payment without simultaneously receiving the release document. Some creditors are slow to provide releases after receiving payment.

Negotiated Settlement 💬

Many lienholders will accept less than the full amount, especially for:

- Old judgment liens

- Junior liens with no equity protection

- Disputed amounts

- Liens where collection would be expensive

Settlement negotiation tips:

- Research the lienholder’s position (priority, equity available)

- Make a reasonable offer based on your financial situation

- Get settlement agreements in writing before paying

- Ensure the agreement includes lien release language

- Consider using a settlement company or attorney for complex negotiations

Lien Release Without Payment 🔓

In certain situations, liens can be released without payment:

- Expired liens — judgment liens expire after 10 years if not renewed

- Invalid liens — liens filed improperly can be removed through legal action

- Paid liens — sometimes releases weren’t filed; creditor will provide release

- Bankruptcy discharge — certain liens can be stripped through bankruptcy

Legal Challenges and Disputes ⚖️

If a lien is invalid, you can challenge it through:

- Motion to remove invalid lien in district court

- Declaratory judgment action establishing lien is unenforceable

- Quiet title action to clear all clouds on title

- Slander of title claim if lien was filed in bad faith

Legal challenges require attorney assistance but can save thousands when liens are improper.

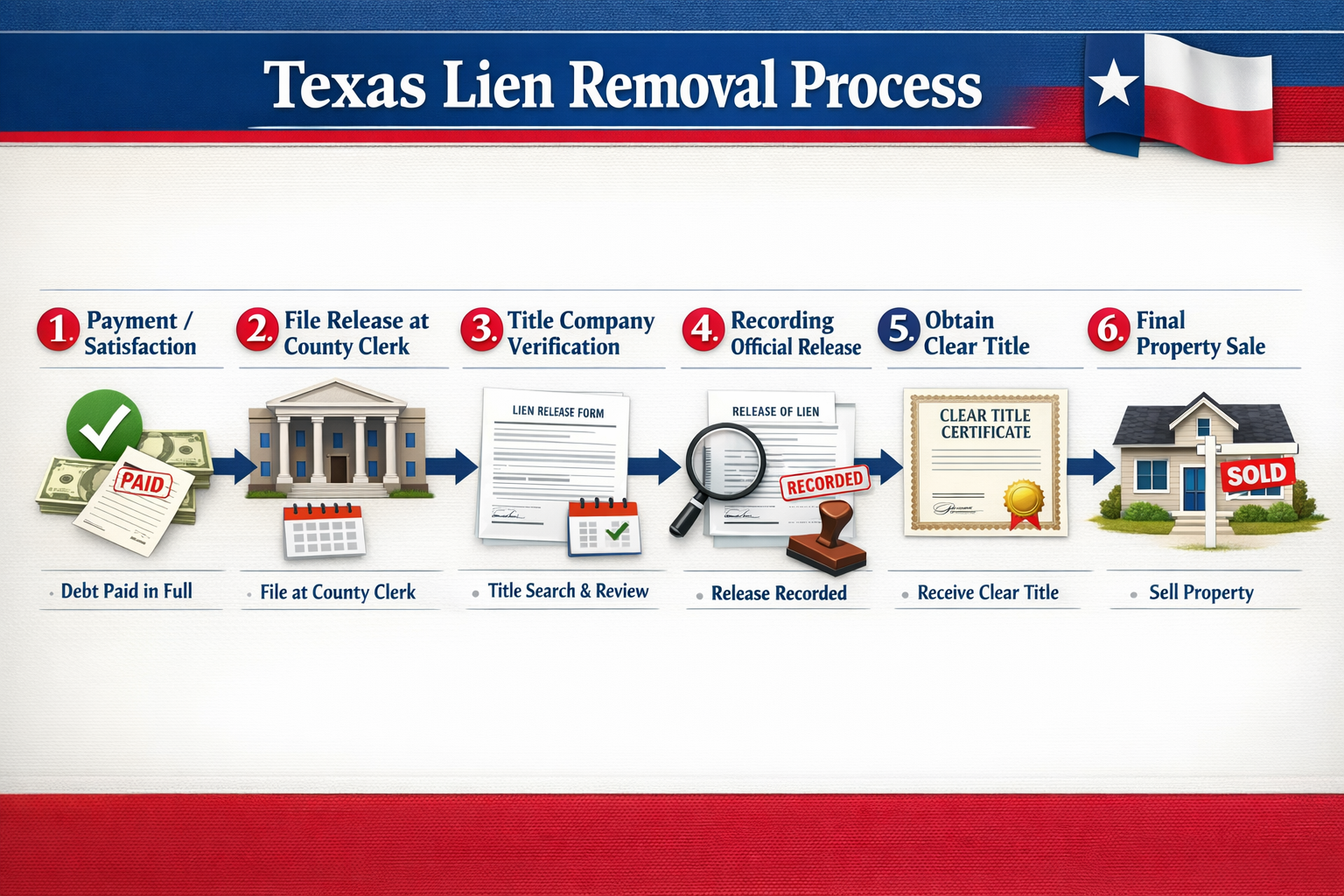

Step 4: Obtain and File the Release

Once a lien is satisfied (through payment, settlement, or legal action), proper documentation must be filed:

Required release documents by lien type:

| Lien Type | Release Document |

|---|---|

| Mortgage/Deed of Trust | Deed of Release or Release of Lien |

| Judgment Lien | Satisfaction of Judgment or Release of Abstract |

| Mechanic’s Lien | Release of Mechanic’s Lien |

| Tax Lien (IRS) | Certificate of Release of Federal Tax Lien |

| Tax Lien (Property) | Tax Certificate showing payment |

| HOA Lien | Release of Lien or Satisfaction |

Filing process:

- Obtain original or certified copy of release document

- Verify proper execution (signatures, notarization)

- File with county clerk where original lien was filed

- Pay recording fees (typically $25-$50)

- Obtain recorded copy with clerk’s stamp and recording information

Step 5: Verify Clear Title

After filing releases, confirm the liens are actually removed:

- Order an updated title search showing liens are released

- Review county records yourself to verify recording

- Obtain title insurance if selling (confirms clear title)

- Keep all documentation (releases, receipts, correspondence)

This verification step is crucial because filing errors or delays can mean liens appear to still exist even after proper release.

Special Considerations for Different Lien Types in Texas

Each lien type has unique removal procedures and considerations.

Removing Tax Liens in Texas

Property tax liens:

- Pay through county tax office — most accept payment plans

- Request tax certificate showing payment

- Automatic release — once paid, lien is satisfied (though certificate should be recorded)

- Redemption rights — if property was sold at tax sale, you may have redemption period

Federal tax liens:

- Pay IRS in full or set up payment plan

- Request Certificate of Release (Form 668-Z)

- IRS files release within 30 days of payment

- Subordination available in some situations (IRS moves to junior position)

- Withdrawal possible if lien was filed in error

For property owners facing tax lien foreclosure, time is critical—act quickly to explore payment plans or other solutions.

Removing Mechanic’s Liens

Options for removing mechanic’s liens:

- Pay the contractor and obtain release

- Bond off the lien by posting a surety bond (lien transfers to bond)

- Challenge validity if notice requirements weren’t met

- Wait for expiration if lawsuit deadline passes without action

- Settle for less if contractor’s claim is inflated

Key deadlines to know:

- Residential projects: Lien must be filed within 3rd month after work completed

- Commercial projects: Lien must be filed within 4th month after work completed

- Lawsuit to foreclose: Generally must be filed within 1-2 years

If the deadline for filing a foreclosure lawsuit passes, the lien becomes unenforceable (though it may still cloud title until formally removed).

Removing Judgment Liens

To remove a judgment lien:

- Satisfy the judgment through payment or settlement

- Obtain satisfaction of judgment document from creditor

- File satisfaction with county clerk

- Verify removal from property records

Alternative methods:

- Appeal the judgment if grounds exist

- File bankruptcy (may discharge underlying debt)

- Wait for expiration (10 years, though renewable)

- Negotiate release for less than full amount

Removing HOA Liens

HOA liens can be particularly tricky because:

- Amounts can include dues, late fees, attorney fees, and collection costs

- HOAs can be aggressive in collection

- Foreclosure can happen relatively quickly

Removal strategies:

- Pay in full and obtain lien release

- Negotiate payment plan with HOA

- Challenge fees if excessive or improper

- Review governing documents for procedural violations

- Attend HOA meetings to request forbearance

Working with Professionals for Lien Removal 👥

While some simple liens can be handled independently, complex situations benefit from expert service and professional guidance.

When to Hire a Real Estate Attorney

Consider legal representation when:

- Multiple liens exist with priority disputes

- Lien validity is questionable (improper filing, expired deadlines)

- Foreclosure is threatened or already initiated

- Large amounts are involved (attorney fees are small compared to potential savings)

- Negotiations are complex (multiple creditors, settlement structures)

- Title issues exist beyond just liens

Attorneys can provide helpful solutions including negotiation, litigation, and strategic advice tailored to your situation.

Working with Title Companies

Title companies offer valuable services:

- Title searches to identify all liens

- Title insurance to protect against undiscovered liens

- Closing services to ensure proper lien payoff and release

- Escrow services to hold funds until releases are obtained

When selling property, the title company typically coordinates lien payoffs and ensures all releases are properly recorded.

Property Solution Specialists

Companies like Sure Path Property Solutions specialize in helping property owners navigate complex situations involving liens, judgments, and title issues.

How property solution specialists help:

- Assess your entire situation including all liens and encumbrances

- Coordinate with creditors to negotiate payoffs and releases

- Work with counties and title professionals to clear title issues

- Provide purchase options when traditional sales aren’t feasible

- Offer friendly and caring support throughout the process

For property owners feeling overwhelmed by multiple liens or complicated title problems, expert service from specialists who understand Texas property law can be invaluable.

Preventing Property Liens: Proactive Strategies 🛡️

While this guide focuses on removing existing liens, prevention is always better than cure.

Pay Debts on Time

The most effective prevention strategy is simple: pay your obligations when due.

- Property taxes (January 31st deadline)

- HOA dues and assessments

- Contractor invoices

- Court judgments

- Federal taxes

Setting up automatic payments or payment reminders helps ensure nothing falls through the cracks.

Protect Yourself During Construction Projects

When hiring contractors for property improvements:

- Verify contractor credentials (licensed, insured, bonded)

- Use written contracts specifying payment terms

- Require lien releases before making final payment

- Make checks payable jointly to contractor and subcontractors

- File completion affidavits when work is finished

- Obtain statutory notices as required by Texas law

These steps significantly reduce mechanic’s lien risk.

Monitor Your Property Title

Regularly checking your property’s title status helps you catch liens early:

- Annual title checks through county clerk records

- Credit monitoring to identify judgment liens

- Tax account reviews to ensure payments are properly credited

- HOA account statements to verify dues are current

Early detection means easier resolution.

Maintain Good Records

Keep organized files including:

- Payment receipts for all property-related expenses

- Lien releases from contractors

- Tax payment confirmations

- HOA payment records

- Legal documents related to your property

Good records help you quickly prove liens are invalid or already satisfied.

Common Mistakes to Avoid When Dealing with Liens ⚠️

Understanding common pitfalls helps you navigate lien removal more successfully.

Ignoring Liens

Biggest mistake: Hoping liens will go away on their own.

While some liens do expire, most remain enforceable for years and can lead to foreclosure. Address liens promptly rather than avoiding the problem.

Paying Without Getting Releases

Never make final payment to a lienholder without simultaneously receiving the release document. Some creditors are slow to provide releases, leaving you with proof of payment but no recorded release.

Best practice: Use escrow arrangements where payment and release are exchanged simultaneously.

Failing to Record Releases

Even if you obtain a release document, the lien remains on public record until the release is filed with the county clerk.

Your responsibility: Ensure releases are properly recorded and verify they appear in county records.

Paying Wrong Amount

Lien amounts can include:

- Original debt

- Interest

- Penalties

- Attorney fees

- Collection costs

- Recording fees

Always request a current payoff statement before paying to ensure you’re paying the correct amount.

Not Verifying Lien Priority

When multiple liens exist, understanding priority determines your negotiation leverage and payment strategy.

Example mistake: Paying a junior judgment lien in full while ignoring a senior tax lien that could wipe out the judgment through foreclosure.

Attempting Complex Removals Without Help

Some lien situations are straightforward; others require professional expertise. Knowing when you’re in over your head and need helpful guidance from industry experts can save time, money, and stress.

Liens and Inherited Property in Texas 👨👩👧👦

Inheriting property with liens creates unique challenges, especially when multiple heirs share ownership.

Heir Responsibility for Liens

Generally, heirs are not personally liable for debts of the deceased. However, liens attached to inherited property must still be satisfied before clear title can be transferred.

Key principles:

- Liens survive death and remain attached to the property

- Estate must address liens before distributing property to heirs

- Heirs inherit subject to liens (property comes with encumbrances)

- Sale proceeds must satisfy liens before heirs receive anything

Probate and Lien Resolution

During probate, the executor or administrator should:

- Identify all liens through title search

- Notify creditors as required by probate law

- Pay valid liens from estate assets

- Obtain releases and record them

- Distribute property to heirs with clear title

If the estate lacks funds to pay liens, the property may need to be sold with proceeds used to satisfy debts.

Options for Heirs with Liens

When you inherit property with liens:

- Pay liens from personal funds to keep the property

- Sell the property and use proceeds to satisfy liens

- Negotiate with lienholders for reduced payoffs

- Disclaim the inheritance if liens exceed property value

- Work with property buyers who handle lien payoffs

For heirs dealing with complicated situations, selling inherited property through experienced professionals can simplify the process significantly.

Selling Property with Liens: Your Options 🏘️

Having liens doesn’t mean you’re stuck with your property forever. Several pathways exist for selling even when liens complicate the transaction.

Traditional Sale with Lien Payoff

In a conventional sale:

- List property with real estate agent

- Disclose liens to potential buyers

- Negotiate sale price considering lien payoffs

- Use closing proceeds to satisfy all liens

- Title company coordinates payoffs and releases

- Close with clear title transferred to buyer

This works when sale proceeds exceed all liens with enough left over to make selling worthwhile.

Short Sale (When Liens Exceed Value)

If you owe more than the property is worth, a short sale may be an option:

- Lender agrees to accept less than full mortgage payoff

- Junior lienholders negotiate reduced settlements

- Property sells for current market value

- Deficiencies may be forgiven (depending on agreements)

Short sales require all lienholders to agree, making them complex and time-consuming.

Cash Buyer Purchase

Cash buyers and property solution companies offer advantages:

- Purchase properties with liens and handle payoffs

- Close quickly (often 2-4 weeks)

- No repairs required (buy as-is)

- No financing contingencies (deals rarely fall through)

- Coordinate with creditors to satisfy liens

This option works well when you need a fast, certain sale and don’t want to navigate lien negotiations yourself.

Deed in Lieu or Foreclosure

If you can’t sell and can’t pay liens, you might consider:

- Deed in lieu of foreclosure (voluntarily transfer to lender)

- Allow foreclosure (lender takes property through legal process)

These options damage credit but may be necessary when no other solution exists.

When you’re ready to explore your options, contact property solution specialists who can provide a comprehensive assessment and trustworthy service.

Understanding Lien Expiration and Statute of Limitations ⏰

Not all liens last forever. Understanding expiration rules can sometimes provide a pathway to lien removal.

Judgment Lien Expiration

In Texas, judgment liens are valid for 10 years from the date of filing. After 10 years, the lien expires unless:

- The creditor renews the abstract of judgment (can be renewed for additional 10-year periods)

- The judgment is revived through legal action

Strategy: If a judgment lien is approaching 10 years old, waiting for expiration may be cheaper than paying.

Mechanic’s Lien Deadlines

Mechanic’s liens have strict enforcement deadlines:

- Lien must be filed within specific timeframes after work completion (3-4 months)

- Foreclosure lawsuit must be filed within 1-2 years of lien filing

- Lien becomes unenforceable if deadlines aren’t met

Even after becoming unenforceable, the lien may still appear on title and require legal action to remove.

Tax Lien Limitations

Property tax liens don’t expire—they remain until paid and can always be enforced through foreclosure.

Federal tax liens remain in effect for 10 years from the date of assessment, plus any time the collection period is suspended (bankruptcy, payment agreements, etc.).

Statute of Limitations vs. Lien Duration

Important distinction:

- Statute of limitations — time limit for filing a lawsuit on the underlying debt

- Lien duration — how long a filed lien remains enforceable

Even if the statute of limitations has expired on the underlying debt, a properly filed lien may still be valid and enforceable.

Property Liens and Title Insurance 📄

Title insurance plays a crucial role in protecting property owners and buyers from lien-related issues.

What Title Insurance Covers

Owner’s title insurance protects against:

- Undiscovered liens existing before you purchased

- Recording errors that failed to show liens

- Forgery or fraud in lien releases

- Errors in public records affecting lien status

Lender’s title insurance protects the mortgage lender’s interest (required by most lenders but doesn’t protect you as the owner).

Title Insurance and Known Liens

Title insurance typically does not cover liens disclosed in the title search before purchase. These “exceptions” are listed in the policy and excluded from coverage.

However, title insurance does cover:

- Liens that should have been discovered but weren’t

- Liens that were supposed to be released but weren’t

- Priority disputes between liens

Title Clearing Before Sale

Before issuing title insurance for a new buyer, title companies require:

- Comprehensive title search identifying all liens

- Payoff of all liens or specific buyer agreement to take subject to certain liens

- Recording of releases for all satisfied liens

- Clear chain of title with no gaps or defects

This process ensures buyers receive clean title and title insurance coverage.

For properties with title problems, working with experienced professionals helps resolve issues efficiently.

Liens in Specific Texas Property Situations 🏡

Certain property circumstances create unique lien considerations.

Homestead Property Protections

Texas offers strong homestead protections, but they do not prevent all liens:

Liens that CAN attach to homestead property:

- Property tax liens

- Mortgage liens

- Mechanic’s liens for improvements

- Home equity loans (with restrictions)

- HOA liens

Liens that CANNOT attach to homestead:

- Most judgment liens (with exceptions for specific debts)

- Creditor liens for consumer debt

However, even though judgment liens may not attach to your homestead while you occupy it, they can attach when you sell or the property loses homestead status.

Rental and Investment Properties

Non-homestead properties receive fewer protections:

- All judgment liens attach to investment property

- Fewer restrictions on foreclosure

- Shorter notice requirements in some situations

- No homestead exemption protections

Vacant Land

Liens attach to vacant land just as they do to improved property:

- Property tax liens

- Judgment liens

- Liens for improvements (wells, fencing, clearing, etc.)

Vacant land may be easier to sell with liens if equity exists, as buyers can use the land as security for financing the lien payoff.

Commercial Property

Commercial properties face:

- More complex lien situations (multiple creditors, business debts)

- Higher dollar amounts typically involved

- Sophisticated creditors with aggressive collection practices

- Commercial title insurance requirements

Resources for Texas Property Owners Dealing with Liens 📚

Navigating liens is easier when you know where to find helpful guidance and information.

Government Resources

County Clerk Offices — Search property records and file lien releases

- Most Texas counties offer online record searches

- In-person assistance available during business hours

County Tax Offices — Property tax information and payment

- Payment plans often available

- Tax certificates showing payment history

Texas State Bar — Attorney referrals

- Lawyer referral service for finding real estate attorneys

- Consumer information about legal issues

Texas Department of Licensing and Regulation — Contractor licensing

- Verify contractor credentials

- File complaints about improper liens

Professional Assistance

Real Estate Attorneys — Legal representation for complex lien issues

Title Companies — Title searches, insurance, and closing services

Property Tax Consultants — Help with tax protests and payment arrangements

Property Solution Companies — Sure Path Property Solutions and similar companies offer comprehensive assistance with lien resolution and property sales

Educational Resources

Texas Property Code — Official statutes governing liens

County Websites — Local rules and procedures

Real Estate Blogs — Industry expert insights and helpful solutions

Frequently Asked Questions About Texas Property Liens ❓

Can I sell my house with a lien on it in Texas?

Yes, you can sell property with liens, but the liens must typically be satisfied from the sale proceeds before you receive any money. Buyers rarely accept property with liens attached, so liens are usually paid at closing. Selling a house with a lien requires coordination between you, the buyer, creditors, and the title company.

How long does a lien stay on property in Texas?

Duration varies by lien type:

- Judgment liens: 10 years (renewable)

- Mechanic’s liens: Until foreclosure deadline passes (1-2 years) or lien is satisfied

- Tax liens: Until paid (no expiration)

- Mortgage liens: Until loan is paid off

Can a lien be placed on property with multiple owners?

Yes, liens can attach to property with multiple owners, though the specifics depend on how title is held (joint tenancy, tenants in common, etc.). A lien against one owner may attach only to that owner’s interest, or it may affect the entire property depending on the circumstances and lien type.

What happens if I inherit property with liens?

You inherit the property subject to the liens, meaning the liens remain attached. You’re not personally liable for the deceased person’s debts, but liens must be satisfied before you can sell or transfer clear title. The estate should address liens during probate before distributing property to heirs.

Can I remove a lien myself without an attorney?

For simple liens where the amount isn’t disputed and you can afford to pay, you can handle removal yourself by paying the debt and filing the release. Complex situations involving multiple liens, disputes, or large amounts typically benefit from attorney assistance to avoid costly mistakes.

How much does it cost to remove a lien in Texas?

Costs vary widely:

- DIY filing fees: $25-$50 to record a release

- Attorney fees: $500-$5,000+ depending on complexity

- Lien payoff amount: The actual debt (can range from hundreds to hundreds of thousands)

- Title search: $150-$400

- Settlement negotiations: Often result in paying less than full amount

Will paying off a lien improve my credit score?

Paying judgment liens can improve credit over time, though the original judgment may remain on your credit report for up to seven years. Tax liens no longer appear on credit reports as of 2018, but the underlying tax debt still affects your financial situation. Mortgage liens are expected and don’t negatively impact credit when paid as agreed.

Conclusion: Taking Control of Property Liens in Texas

Understanding Property Liens in Texas: Complete Guide to Types, Filing & Removal empowers you to take control of challenging property situations. While liens can feel overwhelming, they’re simply legal problems with legal solutions—and you have more options than you might think.

Whether you’re dealing with tax liens, mechanic’s liens, judgment liens, or any other encumbrance on your Texas property, the path forward starts with:

✅ Identifying exactly what liens exist through comprehensive title searches

✅ Understanding your options for each specific lien type

✅ Developing a strategic plan based on your financial situation and goals

✅ Taking action rather than hoping liens will resolve themselves

✅ Working with professionals when situations are complex or stakes are high

Remember that liens don’t make your property worthless or unsellable—they simply require attention and resolution. Many property owners successfully navigate lien removal and move forward with selling, refinancing, or simply clearing their title for peace of mind.

Your Next Steps

If you’re facing property liens in Texas, consider these action steps:

- Order a title search to identify all liens against your property

- Request payoff statements from all lienholders to know exact amounts owed

- Assess your financial options for paying, settling, or disputing liens

- Consult with professionals who can provide helpful guidance tailored to your situation

- Develop a timeline for addressing liens based on urgency and foreclosure risk

For property owners who feel overwhelmed by liens, judgments, back taxes, or other title complications, remember that friendly and caring professionals are available to help. Sure Path Property Solutions specializes in helping Texas property owners navigate exactly these types of complex situations.

The team provides expert service coordinating with counties, creditors, and title professionals to find practical solutions—whether that means helping you clear liens to sell traditionally, or purchasing your property directly and handling all lien resolution themselves.

Don’t let property liens control your future. With the right knowledge and trustworthy service, you can resolve even the most complicated lien situations and move forward with confidence.

Ready to explore your options? Contact the industry experts at Sure Path Property Solutions for a no-obligation consultation about your specific situation. Clear title and peace of mind are closer than you think.