Sell House Before Bank Forecloses: Stop Auction, Get Cash

Imagine receiving a foreclosure notice in the mail. Your heart sinks as you realize the bank has started the process to take your home. The auction date looms on the calendar like a ticking time bomb. Every day that passes brings you closer to losing everything you’ve worked for—and potentially owing thousands more in deficiency judgments. But here’s what many homeowners don’t realize: you have options right up until the auction gavel falls. The ability to sell house before bank forecloses: stop auction, get cash is not only possible—it’s often the smartest financial move you can make when facing foreclosure.

When mortgage payments fall behind, the foreclosure process can feel overwhelming and inevitable. The letters keep coming, the phone calls don’t stop, and the legal jargon makes everything seem impossibly complicated. Many homeowners simply give up, believing they have no choice but to let the bank take their property. This couldn’t be further from the truth. With helpful guidance and expert service, homeowners facing foreclosure can take control of their situation, stop the auction process, and walk away with cash instead of debt.

Key Takeaways

- Time is critical: You can sell your house at any point before the foreclosure auction, but acting quickly gives you more options and better outcomes

- Cash buyers offer speed: Traditional sales take 30-60 days, but cash buyers can close in as little as 7-14 days—fast enough to stop most foreclosure auctions

- Avoid deficiency judgments: Selling before foreclosure helps you control the sale price and potentially avoid owing the bank thousands after losing your home

- Preserve your credit: A foreclosure stays on your credit report for seven years; selling beforehand significantly reduces the long-term damage

- Expert help simplifies the process: Working with industry experts who understand foreclosure timelines, liens, and title issues makes the entire process manageable and stress-free

Understanding the Foreclosure Timeline ⏰

Before exploring how to sell house before bank forecloses: stop auction, get cash, it’s essential to understand what you’re up against. The foreclosure timeline varies by state, but the general process follows a predictable pattern.

The Stages of Foreclosure

Stage 1: Missed Payments (30-90 days)

When mortgage payments are missed, the clock starts ticking. Most lenders don’t immediately begin foreclosure proceedings after one missed payment. Typically, you’ll receive reminder notices and phone calls during the first 30-60 days. However, once you reach 90 days of delinquency, the situation becomes more serious.

Stage 2: Notice of Default (90-120 days)

After approximately three missed payments, the lender files a Notice of Default (NOD) or Lis Pendens, depending on your state. This is the official start of the foreclosure process. This document becomes public record, and you’ll receive formal notification that foreclosure proceedings have begun. Understanding the complete foreclosure timeline helps homeowners know exactly how much time they have to act.

Stage 3: Pre-Foreclosure Period (3-10 months)

This is your window of opportunity. During pre-foreclosure, you still own the property and have the legal right to sell it. The length of this period varies dramatically by state—some judicial foreclosure states like Florida or New York may take 12+ months, while non-judicial states like Texas or Georgia may move much faster.

Stage 4: Auction Notice (20-30 days before sale)

The lender schedules a public auction and publishes notice of the sale. In most states, this notice must be published in local newspapers and posted at the courthouse. The auction date is set, and the countdown begins in earnest.

Stage 5: Foreclosure Auction

On auction day, the property is sold to the highest bidder on the courthouse steps. Once the gavel falls, you no longer own the property. If the winning bid doesn’t cover your mortgage debt, you may face a deficiency judgment for the remaining balance.

Why the Timeline Matters

Understanding where you are in this timeline is critical. The earlier you act, the more options you have. Even if you’re just weeks away from auction, you can still sell house before bank forecloses: stop auction, get cash—but speed becomes absolutely essential.

Why Selling Before Foreclosure Beats Letting the Bank Take Your Home 🏠

Many homeowners facing foreclosure feel defeated and simply stop fighting. They assume foreclosure is inevitable and that there’s nothing they can do. This resignation can cost tens of thousands of dollars and years of financial recovery.

Financial Consequences of Foreclosure

Deficiency Judgments

Here’s what many homeowners don’t realize: losing your home to foreclosure doesn’t necessarily eliminate your debt. If the auction sale price is less than what you owe (which is common), the bank can pursue a deficiency judgment against you for the difference. This means you could lose your home AND owe the bank $20,000, $50,000, or more.

Credit Score Devastation

A foreclosure tanks your credit score by 200-300 points and remains on your credit report for seven years. This makes it extremely difficult to:

- Rent an apartment (many landlords reject applicants with foreclosures)

- Get approved for another mortgage

- Obtain reasonable interest rates on car loans

- Sometimes even secure employment (some employers check credit)

Tax Consequences

Forgiven debt from foreclosure may be considered taxable income by the IRS. While some protections exist, you could receive a 1099-C form for cancelled debt and owe taxes on money you never actually received.

Benefits of Selling Before Foreclosure

Control the Sale Price

When you sell before foreclosure, you control the transaction. You can negotiate the price, choose the buyer, and ensure the sale covers as much of your debt as possible. At auction, the property often sells for 20-40% below market value.

Preserve Your Credit

While selling a home in pre-foreclosure still impacts your credit, the damage is far less severe than a completed foreclosure. Your credit score may drop 50-100 points temporarily, but you can begin rebuilding immediately rather than waiting seven years.

Walk Away with Cash

If you have equity in your home, selling before foreclosure means you keep that equity. Even if you’re underwater, cash buyers for problem properties may negotiate with your lender to accept a short sale, allowing you to walk away without owing anything.

Avoid Additional Fees

Foreclosure comes with attorney fees, court costs, and other expenses that get added to your debt. Selling beforehand eliminates these additional costs.

Maintain Dignity and Control

There’s an emotional component that shouldn’t be overlooked. Choosing to sell on your terms, rather than being forcibly removed from your home, provides a sense of control during an otherwise difficult situation.

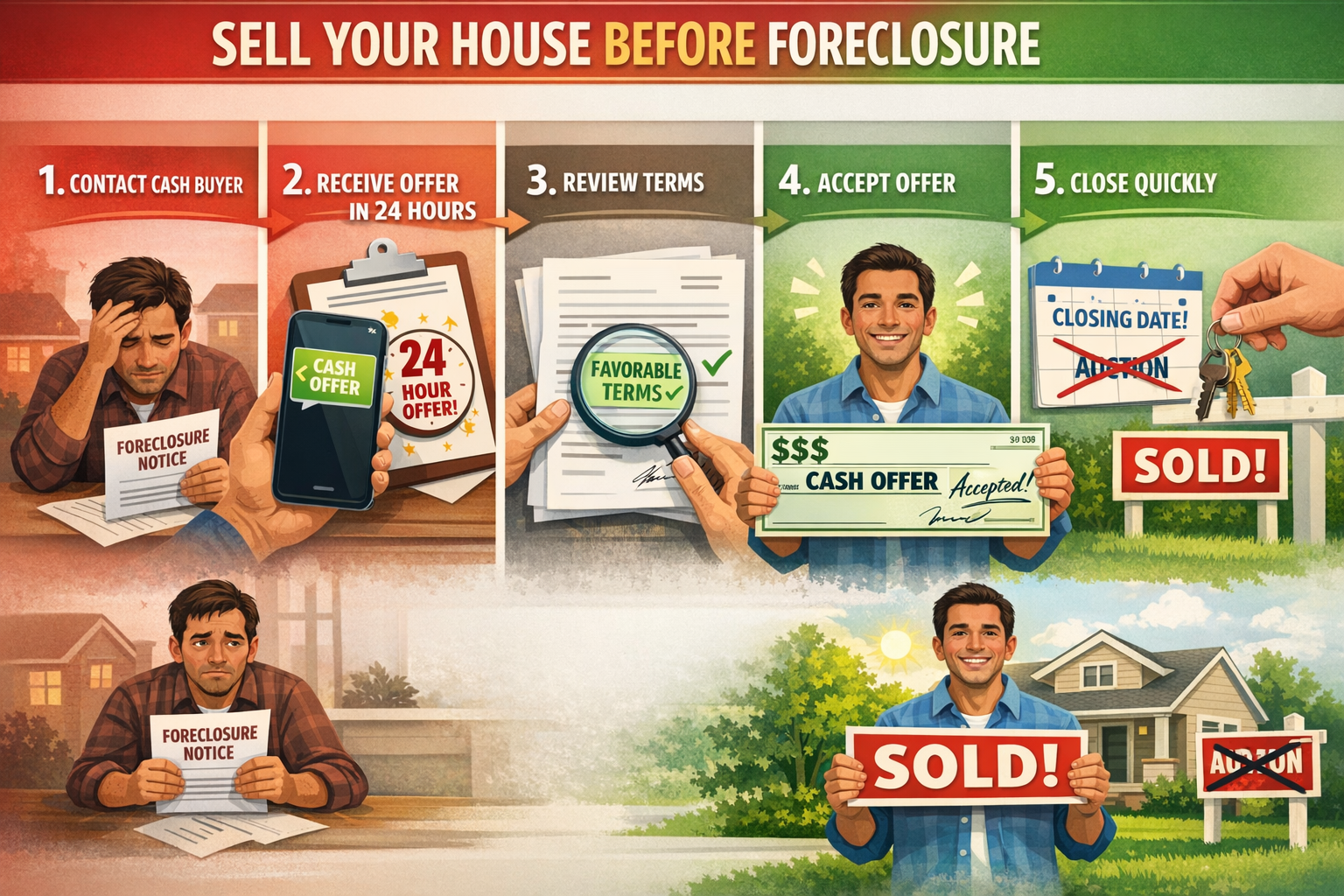

How to Sell House Before Bank Forecloses: Stop Auction, Get Cash 💰

The process of selling your home before foreclosure requires speed, strategy, and often expert service to navigate the complexities. Here’s exactly how it works.

Step 1: Assess Your Timeline Immediately

The first question to answer: How much time do you have?

Check your foreclosure notices carefully. Find the scheduled auction date. This is your absolute deadline. Working backward from that date, you need to determine if you have enough time for a traditional sale (typically 30-60 days) or if you need a cash buyer who can close in 7-14 days.

If your auction is scheduled within 30 days, traditional sales are likely off the table. You need a cash buyer who specializes in pre-foreclosure situations.

Step 2: Understand Your Financial Position

Calculate your numbers:

- Current mortgage balance: What you owe the lender

- Estimated home value: What the property could realistically sell for

- Additional liens or debts: Property taxes, HOA fees, second mortgages, or judgment liens

- Closing costs: Typically 1-3% in a cash sale

This tells you whether you have equity (property worth more than you owe) or if you’re underwater (owing more than the property’s value).

Step 3: Contact Cash Buyers Who Specialize in Pre-Foreclosure

Traditional buyers require mortgage approval, inspections, and lengthy closing periods—luxuries you don’t have when facing foreclosure. Cash buyers offer:

✅ Fast closings: 7-14 days is standard

✅ No financing contingencies: No risk of deals falling through

✅ As-is purchases: No repairs required

✅ Experience with liens: They know how to work with lenders

✅ Foreclosure expertise: They understand the urgency

Sure Path Property Solutions specializes in exactly these situations—helping homeowners navigate complicated circumstances with friendly and caring support.

Step 4: Request and Evaluate Cash Offers

Reputable cash buyers will:

- Ask questions about your property and situation

- Sometimes conduct a brief property walkthrough (or use photos)

- Provide a written cash offer within 24-48 hours

- Explain exactly how they calculated the offer

- Present a clear timeline to closing

The offer may be below retail market value—that’s expected with cash buyers because they’re providing speed and certainty. Evaluate whether the offer:

- Pays off your mortgage completely

- Covers additional liens and debts

- Leaves you with some cash

- Happens fast enough to stop the auction

Step 5: Notify Your Lender

Once you have a solid offer and timeline, contact your lender immediately. Inform them that you have a buyer and a closing date scheduled before the auction. Request that they postpone or cancel the foreclosure sale.

Most lenders prefer to avoid foreclosure—it’s expensive and time-consuming for them too. When presented with a legitimate sale that will pay off the debt, they’re usually willing to work with you.

If you’re underwater and the sale won’t cover the full mortgage, you may need to negotiate a short sale, where the lender agrees to accept less than the full amount owed.

Step 6: Work with a Title Company

Even in fast cash sales, you’ll work with a title company or real estate attorney to handle the closing. They will:

- Conduct a title search to identify all liens

- Coordinate payoffs with your lender and lien holders

- Prepare closing documents

- Facilitate the transfer of funds

- Record the deed transfer

If there are title issues or complex liens, experienced cash buyers have relationships with title professionals who can resolve these problems quickly.

Step 7: Close and Stop the Auction

On closing day, you’ll sign the paperwork transferring ownership to the buyer. The title company distributes funds to pay off your mortgage and any other liens. Your lender receives payment and cancels the foreclosure.

The auction is officially stopped. You walk away without foreclosure on your record.

Special Circumstances That Complicate Pre-Foreclosure Sales 🔧

Not all foreclosure situations are straightforward. Many homeowners face additional complications that make selling before auction seem impossible. The good news? These problems are solvable with helpful solutions and the right expertise.

Multiple Liens on the Property

If you have multiple liens—such as a mortgage, property tax lien, HOA lien, and judgment lien—selling becomes more complex. Each lien holder has a claim on the property, and they must be paid in order of priority.

Solution: Cash buyers experienced in lien resolution can negotiate with multiple lien holders simultaneously. Sometimes junior lien holders will accept partial payment rather than receiving nothing if the property goes to foreclosure auction.

Back Property Taxes

Property tax liens take priority over almost all other debts. If you owe back taxes, they must be addressed before or during the sale.

Solution: Many cash buyers will pay off back taxes as part of the purchase, deducting the amount from your proceeds. This allows the sale to move forward quickly without requiring you to come up with thousands in cash upfront.

Inherited Property in Foreclosure

If you’ve inherited a property that’s in foreclosure, you may be dealing with probate complications, multiple heirs, or unclear title.

Solution: Buyers who specialize in heir property understand how to navigate probate complications and can work with all heirs to reach an agreement quickly.

Judgment Liens

If you have judgment liens from lawsuits, unpaid debts, or other legal judgments, these must be satisfied before clear title can transfer.

Solution: Experienced buyers coordinate with judgment creditors to negotiate payoffs or arrange for liens to be satisfied at closing from sale proceeds.

Properties with Multiple Owners

If the property has multiple owners or heirs who disagree about selling, foreclosure can proceed while family members argue.

Solution: In some cases, one owner can force a sale through partition action, or a cash buyer can purchase individual ownership shares to facilitate a quick resolution.

Alternatives to Selling: Other Ways to Stop Foreclosure ⚖️

While selling house before bank forecloses: stop auction, get cash is often the best option, it’s not the only one. Depending on your circumstances, these alternatives might work:

Loan Modification

Contact your lender to request a loan modification—changing the terms of your mortgage to make payments more affordable. This might include:

- Reducing the interest rate

- Extending the loan term

- Adding missed payments to the end of the loan

Pros: You keep your home

Cons: Requires proof of hardship, lengthy approval process, no guarantee of approval

Forbearance Agreement

A temporary pause or reduction in payments while you get back on your feet financially.

Pros: Immediate relief from payments

Cons: Payments are typically due in a lump sum later, only delays the problem

Reinstatement

Reinstating your mortgage means paying all missed payments, late fees, and legal costs in one lump sum to bring the loan current.

Pros: Stops foreclosure immediately, keeps your home

Cons: Requires significant cash, doesn’t address underlying financial problems

Deed in Lieu of Foreclosure

You voluntarily transfer the deed to your lender in exchange for cancellation of the debt.

Pros: Avoids foreclosure on your record, potentially avoids deficiency judgment

Cons: You lose your home, still damages credit, lender must agree

Important: A deed in lieu still means losing your home without receiving any cash. Selling beforehand is almost always financially superior if you have any equity.

Bankruptcy

Filing Chapter 13 bankruptcy triggers an automatic stay that temporarily halts foreclosure proceedings.

Pros: Buys time, allows you to restructure debts

Cons: Severe credit impact, expensive legal fees, only delays foreclosure unless you can afford the restructured payments

How Cash Buyers Make the Process Simple and Fast ⚡

The traditional home selling process is designed for sellers who have time—time to make repairs, stage the home, wait for buyer financing, and navigate contingencies. When facing foreclosure, you don’t have that luxury.

What Cash Buyers Offer

Speed

Cash buyers can close in 7-14 days because they don’t need:

- Mortgage approval (30-45 days)

- Home inspections and negotiations (1-2 weeks)

- Appraisals (1-2 weeks)

- Repair requests and completion (2-4 weeks)

Certainty

Traditional sales fall through 10-15% of the time due to financing issues, inspection problems, or buyer cold feet. Cash sales close with 95%+ certainty because there are no contingencies.

As-Is Purchases

You don’t need to:

- Make repairs

- Clean or stage the property

- Deal with showings

- Maintain the property during the sale

Expertise with Problem Properties

Professional cash buyers regularly handle:

- Properties with liens

- Homes in foreclosure

- Inherited properties with title issues

- Properties with code violations

- Homes in poor condition

They have systems, relationships, and experience to solve problems quickly.

How to Identify Reputable Cash Buyers

Not all cash buyers are created equal. Look for:

✅ Local presence and reputation: Established businesses with verifiable reviews

✅ Transparent process: Clear explanation of how they calculate offers

✅ No upfront fees: Legitimate buyers don’t charge fees to make offers

✅ Written offers: Professional documentation, not just verbal promises

✅ Proof of funds: Evidence they can actually close quickly

✅ Experience with your specific situation: Ask about similar properties they’ve purchased

Sure Path Property Solutions has built a reputation on trustworthy service, helping homeowners navigate exactly these challenging situations with compassion and expertise.

Real-World Examples: Homeowners Who Stopped Foreclosure 📋

Understanding how to sell house before bank forecloses: stop auction, get cash becomes clearer through real examples.

Case Study 1: Medical Emergency Leads to Foreclosure

Situation: Sarah suffered a serious illness that left her unable to work for eight months. She fell four months behind on her $1,800 monthly mortgage payment. The bank filed a Notice of Default, and an auction was scheduled for 45 days later.

Property Details:

- Owed: $185,000 on mortgage

- Property value: $210,000

- Equity: $25,000

- Additional debt: $3,500 in property taxes

Solution: Sarah contacted a cash buyer specializing in pre-foreclosure properties. Within 48 hours, she received an offer of $195,000. The buyer closed in 12 days—well before the auction date.

Outcome:

- Mortgage paid in full: $185,000

- Property taxes paid: $3,500

- Closing costs: $2,000

- Cash to Sarah: $4,500

While Sarah received less than if she’d sold traditionally, she stopped the foreclosure, avoided a deficiency judgment, and walked away with cash instead of debt.

Case Study 2: Inherited Property with Multiple Issues

Situation: Marcus inherited his grandmother’s house along with two siblings. The property had $12,000 in back taxes, needed $30,000 in repairs, and the siblings couldn’t agree on what to do. Meanwhile, the county was proceeding with a tax foreclosure.

Property Details:

- No mortgage (owned free and clear)

- Property value (as-is): $95,000

- Back taxes: $12,000

- Needed repairs: $30,000

Solution: Marcus contacted a buyer experienced with heir property and tax issues. The buyer made an offer of $80,000, agreeing to pay off the back taxes directly and purchase all three siblings’ shares.

Outcome:

- Back taxes paid: $12,000

- Closing costs: $2,000

- Cash split among three heirs: $66,000 ($22,000 each)

The siblings avoided tax foreclosure, resolved their disagreement, and each walked away with cash without making any repairs.

Case Study 3: Underwater Property with Judgment Lien

Situation: David lost his job and fell behind on his mortgage. He also had a $15,000 judgment lien from a lawsuit. His home was worth $150,000, but he owed $165,000 on the mortgage plus the judgment lien.

Property Details:

- Mortgage owed: $165,000

- Judgment lien: $15,000

- Property value: $150,000

- Total debt: $180,000

- Underwater by: $30,000

Solution: A cash buyer experienced in short sales negotiated with both the mortgage lender and the judgment creditor. The lender agreed to accept $145,000, and the judgment creditor agreed to accept $3,000.

Outcome:

- Sale price: $150,000

- Mortgage payoff: $145,000

- Judgment payoff: $3,000

- Closing costs: $2,000

- David’s debt eliminated: $32,000 in debt forgiven

- Cash to David: $0, but no deficiency judgment

David walked away owing nothing instead of facing a $30,000+ deficiency judgment after foreclosure.

Taking Action: Your Step-by-Step Plan to Stop Foreclosure 📝

If you’re facing foreclosure, every day matters. Here’s your action plan to sell house before bank forecloses: stop auction, get cash.

Immediate Actions (Today)

- Locate your foreclosure notices and identify the auction date

- Calculate your timeline – how many days until auction?

- Gather financial documents: mortgage statements, property tax bills, any lien notices

- Estimate your property value using online tools or recent comparable sales

- Calculate your equity (value minus all debts)

This Week

- Contact 2-3 reputable cash buyers who specialize in pre-foreclosure properties

- Request written offers with clear timelines

- Ask questions: How did you calculate this offer? What’s your exact timeline? What happens if we find title issues?

- Check references and verify the buyer’s track record

- Notify your lender that you’re actively selling the property

Next Steps

- Accept the best offer that meets your timeline and financial needs

- Sign the purchase agreement with clear closing date

- Work with the title company to resolve any liens or title issues

- Stay in communication with all parties: buyer, lender, title company

- Prepare for closing: gather required documents, arrange for moving

Closing Day

- Review all closing documents carefully

- Sign the deed transfer and other required paperwork

- Receive confirmation that mortgage and liens are paid

- Collect your proceeds (if any equity remains)

- Obtain proof that foreclosure has been cancelled

Common Questions About Selling Before Foreclosure ❓

Can I really sell my house if foreclosure has already started?

Yes! You retain ownership and the right to sell your property right up until the moment the auction gavel falls. Even if you’re just days away from auction, a cash buyer can potentially close fast enough to stop the sale.

What if I owe more than my house is worth?

You can still sell through a short sale, where your lender agrees to accept less than the full amount owed. Many lenders prefer this to foreclosure because it’s less expensive for them. Cash buyers experienced in short sales can negotiate these agreements.

Will I have to pay taxes on forgiven debt?

Possibly, but not always. The Mortgage Forgiveness Debt Relief Act provides some protections, and insolvency exceptions may apply. Consult a tax professional about your specific situation.

How much will a cash buyer offer compared to market value?

Cash offers typically range from 70-85% of retail market value, depending on the property’s condition, local market, and timeline urgency. The trade-off is speed, certainty, and convenience.

What if I have multiple liens on my property?

Experienced cash buyers work with title companies to identify all liens and coordinate payoffs. Selling a house with liens is completely possible—it just requires expertise to navigate the process.

Can the bank refuse to cancel the foreclosure even if I have a buyer?

If you’re selling for enough to pay off the mortgage in full, the bank must accept payment and cancel foreclosure. If you’re doing a short sale (selling for less than owed), the bank must approve the sale, which isn’t guaranteed but is likely if the offer is reasonable.

How do I know if a cash buyer is legitimate?

Look for established local businesses with verifiable reviews, transparent processes, written offers, proof of funds, and no upfront fees. Be wary of buyers who pressure you, charge fees, or make promises that seem too good to be true.

Why Sure Path Property Solutions Specializes in Pre-Foreclosure Sales 🏆

Facing foreclosure is one of the most stressful situations a homeowner can experience. It requires not just a buyer, but a partner who understands the urgency, complexity, and emotional weight of the situation.

Our Approach

Speed Without Pressure

We can close in as little as 7 days when needed, but we never pressure homeowners into decisions. We provide clear information and let you decide what’s best for your situation.

Transparent Offers

We explain exactly how we calculate offers and what factors affect the price. No hidden fees, no surprises at closing.

Problem-Solving Expertise

We regularly handle properties with:

- Multiple liens and judgments

- Back property taxes

- Title issues and unclear ownership

- Multiple heirs or co-owners

- Code violations

- Structural issues

Our team includes industry experts who coordinate with lenders, title companies, county offices, and other parties to resolve complex issues quickly.

Helpful Solutions for Every Situation

Whether you’re facing foreclosure due to:

- Job loss or income reduction

- Medical emergencies and bills

- Divorce or family changes

- Inherited property you can’t maintain

- Business failure

- Overwhelming debt

We provide helpful guidance tailored to your specific circumstances. Our goal isn’t just to buy your house—it’s to help you move forward with dignity and hope.

Our Commitment

✅ Fair cash offers based on current market conditions

✅ Fast closings when time is critical

✅ No fees or commissions – you pay nothing

✅ As-is purchases – no repairs required

✅ Professional, caring service throughout the process

✅ Clear communication every step of the way

Contact our team to discuss your situation confidentially and receive a no-obligation cash offer.

The Emotional Side of Foreclosure: You’re Not Alone 💙

Numbers and timelines tell only part of the story. Foreclosure carries an enormous emotional burden—shame, stress, fear, and uncertainty about the future.

Common Feelings

Shame and Embarrassment

Many homeowners feel like they’ve failed or that foreclosure reflects poorly on their character. This isn’t true. Foreclosure happens to good people facing difficult circumstances—medical emergencies, job loss, divorce, or unexpected expenses.

Overwhelm and Paralysis

The complexity of foreclosure can be paralyzing. The legal notices, financial calculations, and tight timelines create decision paralysis. Many homeowners simply freeze, unable to take action.

Isolation

Foreclosure feels isolating. Many people don’t talk about their situation with friends or family due to embarrassment, which increases stress and prevents them from getting help.

Moving Forward with Hope

The ability to sell house before bank forecloses: stop auction, get cash represents more than a financial transaction—it’s a path to a fresh start.

By taking control and selling before foreclosure:

- You preserve your dignity by making an active choice

- You protect your financial future by avoiding the worst credit damage

- You potentially walk away with cash to rebuild

- You eliminate the uncertainty and stress of foreclosure

- You demonstrate resilience and problem-solving

Thousands of homeowners have faced foreclosure and come out the other side. With the right support and helpful solutions, you can too.

Legal Considerations and Consumer Protections 📜

When selling a house in pre-foreclosure, several legal protections and considerations apply.

Fair Debt Collection Practices Act (FDCPA)

This federal law protects you from abusive debt collection practices. Lenders and their representatives cannot:

- Harass you with excessive calls

- Threaten violence or illegal actions

- Use deceptive practices

- Contact you at unreasonable hours

Right to Reinstate

Many states provide a “right to reinstatement,” allowing you to stop foreclosure by paying all missed payments and fees up to a certain point in the process.

Redemption Period

Some states offer a “redemption period” after foreclosure auction during which you can reclaim your property by paying the full amount owed. However, this is rare and expensive—selling before auction is far preferable.

Foreclosure Rescue Scams

Unfortunately, desperate homeowners are targets for scams. Beware of:

- Companies charging large upfront fees

- “Rescue” schemes where you deed your property to someone else temporarily

- Buyers who promise to let you stay and rent the property, then evict you

- High-pressure tactics and promises that sound too good to be true

Legitimate cash buyers:

- Never charge upfront fees

- Provide written offers and clear documentation

- Give you time to review offers and consult professionals

- Work with licensed title companies and attorneys

Consult Professionals

Consider consulting:

- A real estate attorney familiar with foreclosure law in your state

- A HUD-approved housing counselor (free service)

- A tax professional regarding potential tax implications

- A financial advisor about rebuilding after foreclosure

These professionals provide valuable guidance, though when time is short, working with experienced cash buyers who have in-house expertise can streamline the process.

State-Specific Foreclosure Laws and Timelines 🗺️

Foreclosure laws vary significantly by state, affecting how quickly you must act to sell house before bank forecloses: stop auction, get cash.

Judicial vs. Non-Judicial Foreclosure States

Judicial Foreclosure States (foreclosure goes through court):

- Longer timelines: 6-24 months typically

- More opportunities to challenge or delay

- Examples: Florida, New York, New Jersey, Pennsylvania, Illinois

Non-Judicial Foreclosure States (foreclosure happens outside court):

- Faster timelines: 2-6 months typically

- Fewer opportunities to delay

- Examples: Texas, Georgia, California, Arizona, Virginia

Timeline Examples

Texas: Non-judicial state with one of the fastest processes

- Notice of Default: After 120 days delinquent

- Notice of Sale: 21 days before auction

- Total timeline: As little as 5 months from first missed payment

Florida: Judicial state with lengthy process

- Notice of Default: After 90-120 days delinquent

- Court proceedings: 6-12 months

- Total timeline: Often 12-18 months

Georgia: Non-judicial state with quick process

- Notice of Sale: 30 days before auction

- Total timeline: As little as 4-5 months

Understanding your state’s specific timeline helps you gauge urgency and plan accordingly.

Financial Planning After Selling Before Foreclosure 💵

Successfully selling your house before foreclosure is a major accomplishment, but it’s just the beginning of your financial recovery.

Immediate Priorities

Secure Housing

If you received cash from the sale, use it wisely:

- First and last month’s rent on a new place

- Security deposit

- Moving expenses

- Essential furniture and household items

Build Emergency Fund

Even a small emergency fund ($500-$1,000) provides crucial breathing room and prevents future financial crises from spiraling.

Address Remaining Debts

If you have other debts (credit cards, medical bills, personal loans), create a payment plan. Consider:

- Debt consolidation

- Negotiating payment plans

- Credit counseling services

Credit Rebuilding

Check Your Credit Report

Ensure the foreclosure doesn’t appear on your credit report since you sold before completion. Verify that the mortgage shows as “paid” or “settled.”

Rebuild Strategically

- Pay all bills on time going forward

- Keep credit card balances low

- Consider a secured credit card to rebuild credit

- Avoid taking on new debt unnecessarily

Timeline to Recovery

Most people who sell before foreclosure completion can qualify for a new mortgage in 2-4 years with responsible financial management, compared to 7 years after completed foreclosure.

Learning and Growing

Identify What Went Wrong

Understanding what led to the foreclosure helps prevent future problems:

- Was it a one-time crisis (medical emergency, job loss)?

- Ongoing overspending or poor budgeting?

- Insufficient emergency savings?

- Income instability?

Build Better Financial Habits

- Create and follow a realistic budget

- Build 3-6 months of expenses in emergency savings

- Increase income through side work or career advancement

- Avoid lifestyle inflation as income grows

Seek Education

Free resources for financial education:

- Local library workshops

- Non-profit credit counseling agencies

- Online courses and resources

- Community college personal finance classes

Conclusion: Take Control of Your Foreclosure Situation Today

Foreclosure doesn’t have to be the end of your story. The ability to sell house before bank forecloses: stop auction, get cash provides a powerful alternative that protects your financial future, preserves your dignity, and gives you a fresh start.

The Key Points to Remember

Time is your most valuable asset. The earlier you act, the more options you have. Even if auction is just weeks away, you can still take action—but don’t wait.

You have more control than you think. Foreclosure feels inevitable, but it’s not. You own the property until the auction gavel falls, which means you can sell it.

Cash buyers provide speed and certainty. Traditional sales take too long when facing foreclosure. Cash buyers who specialize in pre-foreclosure situations can close in days, not months.

Selling beats foreclosure financially. Avoiding deficiency judgments, preserving your credit, and potentially walking away with cash makes selling the superior choice in almost every scenario.

Help is available. You don’t have to navigate this alone. Industry experts who specialize in complicated property situations provide helpful guidance and trustworthy service throughout the process.

Your Next Steps

If you’re facing foreclosure, take these actions today:

- Find your auction date – this is your deadline

- Calculate your numbers – what you owe versus what your property is worth

- Contact experienced cash buyers – get written offers with clear timelines

- Make a decision – choose the option that best protects your financial future

- Take action – sign the agreement and move forward with confidence

We’re Here to Help

At Sure Path Property Solutions, we’ve helped hundreds of homeowners stop foreclosure and move forward with hope. We understand the stress, urgency, and complexity of your situation. Our team provides:

- Fast cash offers within 24-48 hours

- Quick closings in as little as 7 days

- Expert problem-solving for liens, title issues, and complex situations

- Compassionate, pressure-free service throughout the process

- Clear communication so you always know what’s happening

Foreclosure is overwhelming, but you don’t have to face it alone. Contact us today for a confidential conversation about your situation and a no-obligation cash offer.

Your fresh start begins with a single decision: to take control and explore your options. That decision can change everything.

Remember, thousands of homeowners have successfully navigated foreclosure by selling before auction. With helpful solutions, expert service, and the right support, you can be one of them. The auction date on your calendar doesn’t have to be your destiny—it can be the deadline that motivated you to take action and create a better outcome.

Take the first step today. Your future self will thank you.