Sell House in Default Fast: Cash Offer Before Foreclosure

The foreclosure notice arrives in the mail, and suddenly everything feels overwhelming. Missed mortgage payments have piled up, threatening letters keep coming, and the auction date looms closer each day. But here’s what many homeowners don’t realize: you still have options, even when your house is in default.

The ability to sell house in default fast with a cash offer before foreclosure can be the lifeline that saves your credit, protects your equity, and gives you a fresh financial start. This isn’t about giving up—it’s about taking control of a difficult situation before it spirals further.

Understanding how to navigate mortgage default and access helpful solutions can make the difference between losing everything at auction and walking away with cash in hand. The foreclosure process moves quickly, but with expert service and the right strategy, homeowners can move even faster.

Key Takeaways

- Time is critical: Once you’re in default, the foreclosure timeline accelerates rapidly, but cash buyers can close in as little as 7-14 days

- Equity preservation: Selling before foreclosure auction helps you capture remaining equity instead of losing it completely

- Credit protection: A pre-foreclosure sale minimizes credit damage compared to a completed foreclosure

- No repairs needed: Cash buyers purchase houses as-is, eliminating the burden of fixing up a property you can’t afford to maintain

- Multiple exit strategies: Options include cash sales, short sales, deed in lieu, and loan reinstatement—each suited to different situations

Understanding Mortgage Default and the Foreclosure Process

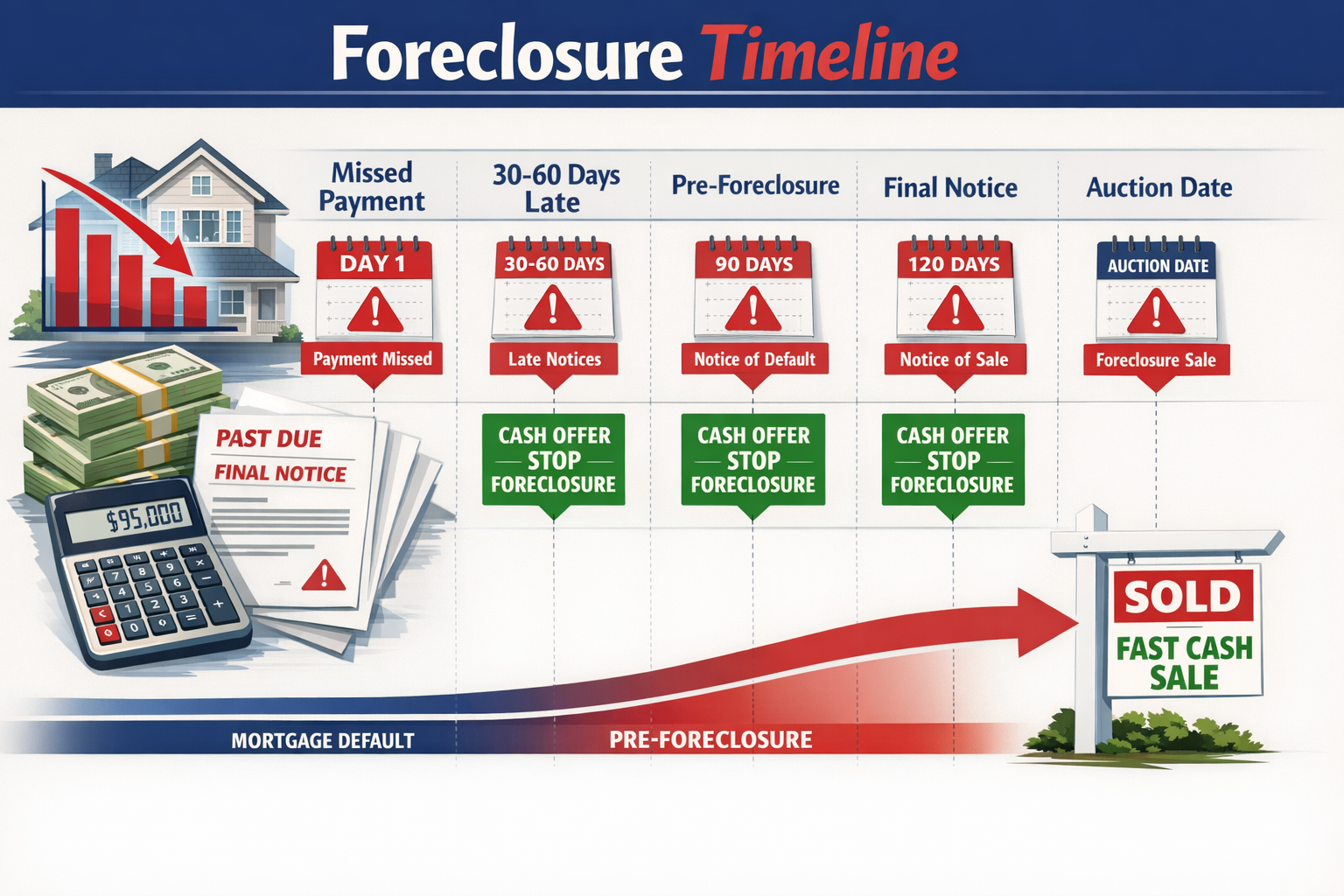

Mortgage default occurs when homeowners fall behind on their loan payments. Missing even one payment can trigger late fees and lender notifications, but the real trouble begins after 90 days of non-payment.

The Stages of Default

Early Default (30-90 days)

During this initial period, lenders send late payment notices and assess fees. Credit scores begin dropping, but foreclosure hasn’t officially started. This window represents the best time to explore alternatives.

Notice of Default (90-120 days)

After three missed payments, most lenders file a Notice of Default. This public record marks the official start of pre-foreclosure. Homeowners typically receive 30-120 days to cure the default, depending on state laws.

Pre-Foreclosure Period

This critical phase offers the last opportunity to sell your house in pre-foreclosure and avoid auction. The timeline varies significantly by state—some allow just a few months while others provide over a year.

Foreclosure Auction

If the default isn’t resolved, the property goes to auction. The lender typically sets the opening bid at the outstanding loan balance. Properties often sell below market value, and homeowners lose any remaining equity.

Why Default Happens

Financial hardship takes many forms:

- Job loss or reduced income

- Medical emergencies and unexpected bills

- Divorce or family changes

- Business failures

- Adjustable-rate mortgages resetting to higher payments

- Property tax accumulation

- Multiple liens creating unmanageable debt

Many homeowners facing default also struggle with back taxes on inherited property or judgment liens that compound their financial challenges.

The Real Cost of Foreclosure

Beyond losing your home, foreclosure carries severe consequences:

- Credit damage: Foreclosures remain on credit reports for seven years, dropping scores by 200-300 points

- Deficiency judgments: If the auction price doesn’t cover the loan balance, lenders may pursue you for the difference

- Tax implications: Forgiven debt may count as taxable income

- Housing difficulties: Future landlords and lenders view foreclosure unfavorably

- Emotional toll: The stress affects families, relationships, and mental health

“Foreclosure doesn’t just take your house—it can take years to rebuild what you lose financially and emotionally. That’s why acting quickly to explore alternatives is so important.” – Industry experts

How to Sell House in Default Fast: Cash Offer Before Foreclosure

When facing default, speed matters. Traditional home sales take 30-60 days minimum, but the foreclosure clock doesn’t wait. Cash offers provide the fastest exit strategy.

Why Cash Offers Work for Defaulted Properties

Cash buyers specialize in purchasing homes that traditional buyers avoid. They understand the urgency of default situations and structure deals accordingly.

Speed of Closing

Cash transactions eliminate mortgage contingencies, appraisals, and lengthy underwriting processes. Closings happen in 7-14 days—sometimes faster in emergency situations.

As-Is Purchases

Homeowners in default rarely have funds for repairs or improvements. Cash buyers purchase properties in any condition, removing this barrier entirely.

Certainty of Sale

Traditional buyers often back out when financing falls through. Cash offers provide certainty—once you accept, the sale proceeds to closing without financing risks.

Flexible Terms

Cash buyers can accommodate various situations, including:

- Delayed move-out dates for relocation planning

- Assistance with moving costs

- Help coordinating lien payoffs

- Solutions for properties with multiple owners

The Cash Sale Process for Defaulted Homes

Step 1: Initial Contact

Reach out to reputable cash buyers who specialize in pre-foreclosure situations. Sure Path Property Solutions provides helpful guidance through this initial consultation, assessing your specific situation.

Step 2: Property Evaluation

Cash buyers evaluate the property’s condition, location, and market value. Unlike traditional appraisals, this process focuses on current as-is value and typically completes within 24-48 hours.

Step 3: Cash Offer Presentation

Buyers present offers quickly—often within 24 hours. The offer accounts for:

- Current market value

- Repair costs

- Outstanding liens and back taxes

- Closing timeline urgency

- Equity position

Step 4: Offer Acceptance and Agreement

Once you accept, the buyer prepares a purchase agreement outlining terms, timeline, and responsibilities. Review carefully and consider consulting an attorney.

Step 5: Title Work and Lien Resolution

The buyer’s title company researches the property, identifying all liens, judgments, and encumbrances. Cash buyers often help coordinate lien payoffs as part of closing.

Step 6: Closing

At closing, the sale finalizes, liens get paid from proceeds, and you receive any remaining equity. The mortgage default resolves, stopping foreclosure.

Calculating Your Net Proceeds

Understanding what you’ll walk away with helps make informed decisions:

| Item | Description | Typical Amount |

|---|---|---|

| Sale Price | Cash offer amount | Varies by property |

| Mortgage Payoff | Outstanding loan balance | Full remaining balance |

| Back Payments | Missed payments + fees | 3-12 months typically |

| Property Taxes | Outstanding tax debt | Varies by jurisdiction |

| HOA Liens | Unpaid association fees | Varies |

| Other Liens | Judgments, mechanics liens | Varies |

| Closing Costs | Title, recording fees | $1,000-$3,000 |

| Net to Seller | Remaining after payoffs | Your equity |

Even if equity is minimal, selling beats foreclosure. You avoid deficiency judgments and severe credit damage.

Alternatives to Cash Sales When Your House Is in Default

Cash offers aren’t the only option. Understanding all alternatives helps you choose the best path forward.

Loan Reinstatement

Reinstating your mortgage after default means paying all missed payments, fees, and penalties to bring the loan current.

When It Works

Reinstatement makes sense if:

- You’ve experienced temporary financial hardship that’s now resolved

- You have access to funds (savings, family loan, settlement)

- You want to keep the home long-term

- The total amount due is manageable

Requirements

Lenders typically require:

- Full payment of arrears in one lump sum

- Proof of ability to resume regular payments

- Payment of all late fees and legal costs

- Compliance within the reinstatement period (varies by state)

Challenges

The amount needed often exceeds what homeowners can gather quickly. If you’ve missed six months of $2,000 payments, you need $12,000 plus fees—a substantial sum during financial hardship.

Loan Modification

Modification restructures your existing loan to make payments more affordable.

Types of Modifications

- Interest rate reduction: Lowering the rate decreases monthly payments

- Term extension: Spreading the balance over more years reduces payments

- Principal forbearance: Setting aside part of the balance interest-free

- Principal reduction: Forgiving part of the balance (rare)

The Application Process

Lenders require extensive documentation:

- Hardship letter explaining circumstances

- Income verification (pay stubs, tax returns)

- Bank statements

- Expense documentation

- Financial statements

Processing takes 30-90 days, and approval isn’t guaranteed. Many homeowners find the process frustrating and uncertain.

Short Sale

A short sale occurs when lenders agree to accept less than the outstanding loan balance.

How Short Sales Work

- You list the property with a real estate agent

- Buyers make offers below the loan balance

- You submit the offer to your lender with a short sale package

- The lender reviews and either approves, counters, or denies

- If approved, the sale proceeds and the lender forgives the deficiency

Advantages

- Less credit damage than foreclosure

- Lender forgives the shortage

- You avoid deficiency judgments (in most cases)

- More dignified exit than foreclosure

Disadvantages

- Time-consuming (3-6 months typical)

- Lender approval required

- Not guaranteed to succeed

- Still impacts credit negatively

- May have tax implications

Deed in Lieu of Foreclosure

With a deed in lieu, you voluntarily transfer property ownership to the lender in exchange for mortgage forgiveness.

When Lenders Accept Deed in Lieu

Lenders prefer this option when:

- The property has clear title without junior liens

- The home’s value approximates the loan balance

- You’ve attempted to sell but couldn’t

- Foreclosure would be costly and time-consuming

Benefits

- Faster than foreclosure

- Less credit damage

- Avoids public auction

- May include relocation assistance

- Typically releases you from deficiency

Limitations

- Lenders aren’t obligated to accept

- Junior liens complicate the process

- Still damages credit (though less than foreclosure)

- You lose any equity

- May have tax consequences

Bankruptcy

Chapter 7 or Chapter 13 bankruptcy can temporarily halt foreclosure through automatic stay.

Chapter 13 Bankruptcy

This reorganization bankruptcy allows you to:

- Stop foreclosure immediately

- Catch up on missed payments over 3-5 years

- Keep your home if you maintain the plan

- Consolidate other debts

Chapter 7 Bankruptcy

Chapter 7 liquidation:

- Temporarily delays foreclosure

- Discharges unsecured debts

- Doesn’t eliminate mortgage liens

- Provides breathing room but rarely saves the home

Considerations

Bankruptcy carries serious consequences:

- Severe credit damage (7-10 years on report)

- Legal fees ($1,500-$3,500+)

- Public record

- Doesn’t eliminate mortgage debt unless you surrender the property

- Complex legal process requiring attorney assistance

Bankruptcy should be a last resort, typically when you have substantial other debts beyond the mortgage.

Working with Cash Buyers: What to Expect

Not all cash buyers operate with the same integrity and expertise. Understanding what to expect helps you identify trustworthy service providers.

Characteristics of Reputable Cash Buyers

Transparency

Professional buyers clearly explain:

- How they calculate offers

- All fees and costs

- The timeline and process

- Your obligations and theirs

- Potential outcomes

Local Market Knowledge

Industry experts understand local market conditions, property values, and foreclosure laws specific to your area.

Problem-Solving Capability

Reputable buyers help navigate complications like:

- Multiple liens on the property

- Title issues and clouds

- Properties with back taxes

- Inherited properties with multiple heirs

Proven Track Record

Look for buyers with:

- Years of experience in your market

- Verifiable references and testimonials

- Professional credentials and licenses

- Clear company information and contact details

Red Flags to Avoid

Pressure Tactics

Beware of buyers who:

- Demand immediate decisions without time to review

- Discourage you from seeking legal advice

- Use high-pressure sales techniques

- Create artificial urgency beyond the foreclosure timeline

Unrealistic Promises

Be skeptical of claims like:

- “We’ll pay more than anyone else”

- “We can stop foreclosure no matter what”

- “You’ll definitely walk away with cash” (before evaluating your equity position)

Lack of Transparency

Avoid buyers who:

- Won’t explain their offer calculation

- Hide fees in fine print

- Provide vague timelines

- Refuse to put agreements in writing

Upfront Fees

Legitimate cash buyers never charge upfront fees. They profit from the property purchase, not from charging distressed homeowners.

Questions to Ask Potential Cash Buyers

Before committing, ask:

- How long have you been buying properties in this area?

- Can you provide references from recent sellers in similar situations?

- How do you calculate your offers?

- What is your typical closing timeline?

- Who pays closing costs?

- How do you handle existing liens and back taxes?

- What happens if title issues arise?

- Can I review the purchase agreement with an attorney?

- What are my obligations if I accept your offer?

- Do you charge any fees to sellers?

Professional buyers welcome these questions and provide clear, detailed answers.

Protecting Your Equity and Financial Future

Even in default, protecting whatever equity remains should be a priority. Strategic decisions now impact your financial recovery for years.

Understanding Your Equity Position

Calculate your true equity position:

Current Market Value – (Mortgage Balance + Arrears + Liens + Taxes + Closing Costs) = Net Equity

Many homeowners in default discover their equity has evaporated, especially if:

- Property values have declined

- The mortgage is relatively new with little principal paid down

- Substantial liens and taxes have accumulated

However, even modest equity is worth preserving through a pre-foreclosure sale rather than losing it at auction.

Timing Your Sale Strategically

The earlier you act, the more options you have:

Early Default (30-90 days)

- Maximum negotiating leverage

- Time for traditional sale if desired

- More buyer interest

- Better credit protection

Mid-Default (90-180 days)

- Still time for cash sale

- Traditional sales become difficult

- Credit damage accelerating

- Urgency increasing

Late Default (180+ days)

- Auction date approaching

- Cash sale may be only option

- Severe time pressure

- Maximum credit damage

⏰ The Golden Rule: Contact cash buyers as soon as you realize you can’t catch up on payments. Don’t wait until the auction date is set.

Tax Implications of Pre-Foreclosure Sales

Understand potential tax consequences:

Forgiven Debt

If you sell for less than you owe and the lender forgives the deficiency, the IRS may consider that forgiven amount taxable income. However, the Mortgage Forgiveness Debt Relief Act (extended through 2025, check 2026 status) may exempt principal residence forgiveness.

Capital Gains

If you have equity and profit from the sale, capital gains taxes may apply. However, the primary residence exclusion ($250,000 single, $500,000 married) typically eliminates this concern for most homeowners.

Consult Tax Professionals

Given the complexity and changing regulations, consult a tax advisor about your specific situation before finalizing any sale.

Rebuilding After Default

Selling before foreclosure minimizes damage and speeds recovery:

Credit Recovery Timeline

- Pre-foreclosure sale: 2-3 years to qualify for new mortgage

- Completed foreclosure: 3-7 years to qualify for new mortgage

- Bankruptcy: 2-4 years (Chapter 13) or 4-7 years (Chapter 7)

Steps to Rebuild

- Create a budget: Understand income and expenses to prevent future problems

- Build emergency fund: Even small amounts ($500-$1,000) provide a buffer

- Monitor credit: Check reports regularly and dispute errors

- Pay all bills on time: Establish a new positive payment history

- Use credit responsibly: Consider secured credit cards to rebuild

- Save for housing: Build down payment for future home purchase

Financial Counseling

HUD-approved housing counselors provide free helpful guidance on:

- Budgeting and financial planning

- Credit repair strategies

- Future homeownership preparation

- Avoiding foreclosure scams

Special Situations: Liens, Judgments, and Title Issues

Default often accompanies other property complications. Understanding how cash buyers handle these issues provides peace of mind.

Properties with Multiple Liens

Liens create a hierarchy of claims against your property:

Priority Order

- Property tax liens (highest priority)

- First mortgage

- Second mortgage/HELOC

- Judgment liens

- HOA liens

- Mechanics liens

When you sell, proceeds pay liens in priority order. If proceeds don’t cover all liens, junior lienholders may receive nothing—giving them incentive to negotiate.

Cash Buyer Advantages

Experienced buyers coordinate with lienholders to:

- Negotiate payoff reductions

- Resolve disputed liens

- Clear title for closing

- Handle complex lien hierarchies

This expertise proves invaluable when selling houses with liens.

Judgment Liens

Court judgments for unpaid debts become liens when recorded against your property. Common sources include:

- Credit card lawsuits

- Medical debt collections

- Business debts

- Personal loans

Cash buyers experienced with judgment liens can negotiate settlements, often for less than the full amount, as part of the sale process.

Tax Liens and Back Taxes

Property tax liens take priority over virtually all other claims. If you’re facing both mortgage default and tax delinquency, the situation is especially urgent.

Cash buyers specializing in tax lien properties understand how to:

- Calculate total tax debt including penalties and interest

- Negotiate with tax authorities

- Coordinate simultaneous payoffs

- Prevent tax foreclosure

Title Defects and Clouds

Title issues complicate any sale, but cash buyers with expertise in title problems can often resolve:

- Missing heirs on inherited properties

- Breaks in chain of title

- Unreleased old mortgages

- Boundary disputes

- Easement conflicts

Professional buyers work with title companies and attorneys to clear these issues, making sales possible when traditional buyers would walk away.

State-Specific Foreclosure Laws and Timelines

Foreclosure laws vary dramatically by state, affecting how quickly you must act.

Judicial vs. Non-Judicial Foreclosure States

Judicial Foreclosure States

These states require lenders to sue in court:

- Longer timelines (6-24 months)

- More opportunities to respond

- Court oversight and protections

- Higher lender costs

Examples: Florida, Illinois, New York, New Jersey, Pennsylvania

Non-Judicial Foreclosure States

These states allow foreclosure without court involvement:

- Faster timelines (3-6 months)

- Less oversight

- Fewer opportunities to delay

- Lower lender costs

Examples: Texas, California, Georgia, Arizona, Nevada

Timeline Variations

Understanding your state’s foreclosure timeline helps you plan:

Fast States (3-4 months)

- Texas: ~4 months

- Georgia: ~3 months

- Nevada: ~4 months

Moderate States (6-12 months)

- California: ~6-8 months

- Arizona: ~6 months

- Ohio: ~6-8 months

Slow States (12+ months)

- Florida: ~12-18 months

- New York: ~15-18 months

- New Jersey: ~15-24 months

Even in slow states, acting quickly provides more options and better outcomes.

Redemption Rights

Some states grant redemption rights—the ability to reclaim your property after foreclosure by paying the full amount:

Pre-Sale Redemption

Most states allow redemption before the auction by paying all arrears, fees, and costs.

Post-Sale Redemption

Some states allow redemption even after auction:

- Typically 6-12 months post-sale

- Requires paying full sale price plus costs

- Rare in practice due to financial requirements

Redemption rights vary significantly, so understanding your state’s specific laws is essential.

How Sure Path Property Solutions Helps Homeowners in Default

When facing default, working with experienced professionals who understand the complexity makes all the difference.

Our Approach to Default Situations

Sure Path Property Solutions specializes in helping homeowners navigate complicated situations, including mortgage default and foreclosure.

Comprehensive Evaluation

We assess your complete situation:

- Current default status and timeline

- Equity position and property value

- Existing liens and encumbrances

- Back taxes and other debts

- Your goals and priorities

Customized Solutions

Every situation is unique. We develop strategies tailored to your specific circumstances, whether that means:

- Fast cash purchase to stop foreclosure

- Coordinating with lienholders

- Resolving title complications

- Addressing tax issues

- Working with co-owners or heirs

Transparent Communication

We provide clear, honest information about:

- Realistic timelines

- Expected outcomes

- Your options and their implications

- Our process and offer calculation

- What you can expect at each stage

Our Process for Defaulted Properties

1. Initial Consultation (Free)

Contact us by phone or through our website. We’ll discuss your situation confidentially and explain how we can help—with no obligation.

2. Property Assessment (24-48 hours)

We evaluate your property and research liens, taxes, and title issues. This comprehensive assessment informs our offer.

3. Cash Offer Presentation (24 hours)

We present a fair cash offer based on current market value and your specific situation. We explain exactly how we calculated the offer and answer all questions.

4. Flexible Timeline

Once you accept, we work on your schedule—closing as quickly as 7 days if needed, or allowing more time if that serves you better.

5. Professional Coordination

We coordinate with:

- Title companies

- Lienholders and creditors

- Tax authorities

- Attorneys

- Your mortgage lender

This coordination ensures smooth closing and resolution of all issues.

6. Closing and Relief

At closing, all liens and debts are paid from proceeds, the foreclosure stops, and you receive any remaining equity. You walk away with the situation resolved and can begin rebuilding.

Why Homeowners Choose Us

✅ Experience: Years of helping homeowners in default situations

✅ Expertise: Deep understanding of liens, title issues, and foreclosure laws

✅ Speed: Closings in as little as 7-14 days when urgency matters

✅ Fairness: Transparent offers based on market value and your equity position

✅ Compassion: We understand the stress of default and treat you with respect and dignity

✅ Solutions: We solve problems other buyers walk away from

✅ No Fees: We never charge homeowners fees—you pay nothing out of pocket

Frequently Asked Questions

Can I sell my house if I’m already in foreclosure?

Yes, you can sell anytime before the foreclosure auction. Once the property sells at auction, it’s too late. The earlier you act, the better your options.

Will I owe money after selling a house in default?

It depends on your equity position. If sale proceeds cover all debts (mortgage, liens, taxes, costs), you may receive cash. If proceeds fall short, you typically won’t owe the difference when selling to cash buyers who negotiate full releases.

How much will I get for my house in default?

Your net proceeds equal the sale price minus all debts and costs. Cash offers reflect current as-is value. Even if equity is minimal, selling beats foreclosure’s consequences.

Can I sell if I have liens on the property?

Yes, cash buyers regularly purchase properties with liens. Liens are paid from sale proceeds at closing, and experienced buyers help negotiate payoffs.

How fast can I close on a cash sale?

Typically 7-14 days, sometimes faster in emergencies. The timeline depends on title work, lien negotiations, and your preferences.

Will selling before foreclosure hurt my credit?

Selling impacts credit less than completed foreclosure. While late payments damage credit, avoiding foreclosure minimizes long-term harm and speeds recovery.

What if I owe more than the house is worth?

If you’re underwater, a short sale or deed in lieu may be options. Cash buyers can sometimes negotiate with lenders on your behalf, though success isn’t guaranteed.

Do I need to make repairs before selling?

No, cash buyers purchase as-is. You don’t need to fix anything, clean extensively, or make improvements.

Can I sell if there are multiple owners?

Yes, though all owners must typically agree to the sale. Cash buyers experienced with jointly owned properties can help navigate these situations.

What documents do I need to sell?

Basic documents include:

- Photo ID

- Mortgage statements

- Property tax records

- HOA information (if applicable)

- Any lien or judgment documentation

Your cash buyer will guide you through specific requirements.

Taking Action: Your Next Steps

Facing default feels overwhelming, but taking action empowers you to regain control.

Immediate Actions (Today)

- Assess your timeline: Determine exactly where you are in the foreclosure process and how much time remains

- Gather documentation: Collect mortgage statements, default notices, and property tax records

- Calculate your position: Estimate your equity by subtracting all debts from current property value

- Contact cash buyers: Reach out to reputable buyers for free consultations and offers

- Explore all options: Consider reinstatement, modification, short sale, and cash sale simultaneously

This Week

- Get multiple offers: Contact 2-3 cash buyers to compare offers and approaches

- Consult professionals: Speak with a real estate attorney or HUD counselor about your options

- Review your finances: Determine if you can realistically save the home or if selling is the best path

- Communicate with your lender: Inform them you’re actively pursuing solutions

- Make a decision: Choose your path forward based on all available information

Moving Forward

Once you’ve decided to sell:

- Accept the best offer: Choose the buyer offering the best combination of price, terms, and reliability

- Review all paperwork: Read purchase agreements carefully and ask questions about anything unclear

- Coordinate with the buyer: Provide requested documentation promptly to keep the process moving

- Prepare for closing: Arrange for moving, forwarding addresses, and utility transfers

- Close and move on: Complete the sale and begin your financial recovery

Resources and Support

HUD Housing Counseling: 1-800-569-4287 or www.hud.gov

National Foundation for Credit Counseling: 1-800-388-2227

Legal Aid: Search for free legal services in your area at www.lawhelp.org

Sure Path Property Solutions: Contact us for a free, no-obligation consultation about your specific situation

Conclusion

The ability to sell house in default fast with a cash offer before foreclosure provides a powerful alternative to losing your home at auction. While default and foreclosure feel overwhelming, understanding your options empowers you to make informed decisions that protect your financial future.

Cash sales offer speed, certainty, and solutions that traditional sales can’t match when time is critical. Reputable buyers provide helpful guidance through the process, coordinate with lienholders and tax authorities, and purchase properties as-is—eliminating the burdens that make traditional sales impossible during financial hardship.

The key is acting quickly. Every day that passes moves you closer to auction and reduces your options. Whether you ultimately choose a cash sale, loan modification, short sale, or another alternative, taking action now gives you the best chance of preserving equity and minimizing credit damage.

Remember, default doesn’t define you—it’s a financial challenge that thousands of homeowners face each year. With expert service, trustworthy partners, and the right strategy, you can navigate this difficult time and emerge ready to rebuild.

Don’t wait until the auction date is set. Contact Sure Path Property Solutions today for a free consultation. We’ll evaluate your situation, explain your options clearly, and provide a fair cash offer if selling makes sense for you. Our friendly and caring team has helped countless homeowners in default find helpful solutions and move forward with confidence.

Your fresh start begins with a single phone call. Take that step today.