Imagine finding your dream property at an incredible price, only to discover it comes with hidden legal baggage that could cost you thousands—or worse, prevent the sale entirely. This scenario plays out more often than most people realize, and it’s why understanding encumbered properties is absolutely critical for anyone involved in real estate transactions.

Encumbered Property for Sale: What Buyers & Sellers Need to Know isn’t just about legal jargon and paperwork. It’s about protecting your investment, avoiding costly mistakes, and navigating complex situations with confidence. Whether you’re a seller struggling with liens or a buyer evaluating a property with claims against it, the stakes are high and the path forward requires expert guidance.

An encumbered property is any real estate that has legal claims, restrictions, or liabilities attached to it. These encumbrances can range from mortgages and tax liens to easements and judgments. While some encumbrances are routine and expected, others can derail a sale or create significant financial exposure for unsuspecting parties.

Key Takeaways

- Encumbrances are legal claims or restrictions on property that can affect ownership rights, transferability, and value

- Common types include mortgages, liens, easements, and judgments that must be disclosed and often resolved before closing

- Sellers have legal obligations to disclose known encumbrances and may need to clear them before selling

- Buyers must conduct thorough due diligence including title searches and inspections to identify all encumbrances

- Many encumbered properties can still be sold with the right strategy, professional guidance, and clear communication between parties

Understanding Property Encumbrances: The Foundation

Property encumbrances represent any claim, lien, charge, or liability attached to real estate that may diminish its value or restrict its use. Think of encumbrances as invisible chains attached to a property—they travel with the deed and can impact every future owner until properly resolved.

What Makes a Property “Encumbered”?

A property becomes encumbered when someone other than the owner has a legitimate legal claim or interest in it. These claims don’t necessarily prevent ownership, but they do create obligations or limitations that affect the property’s marketability and value.

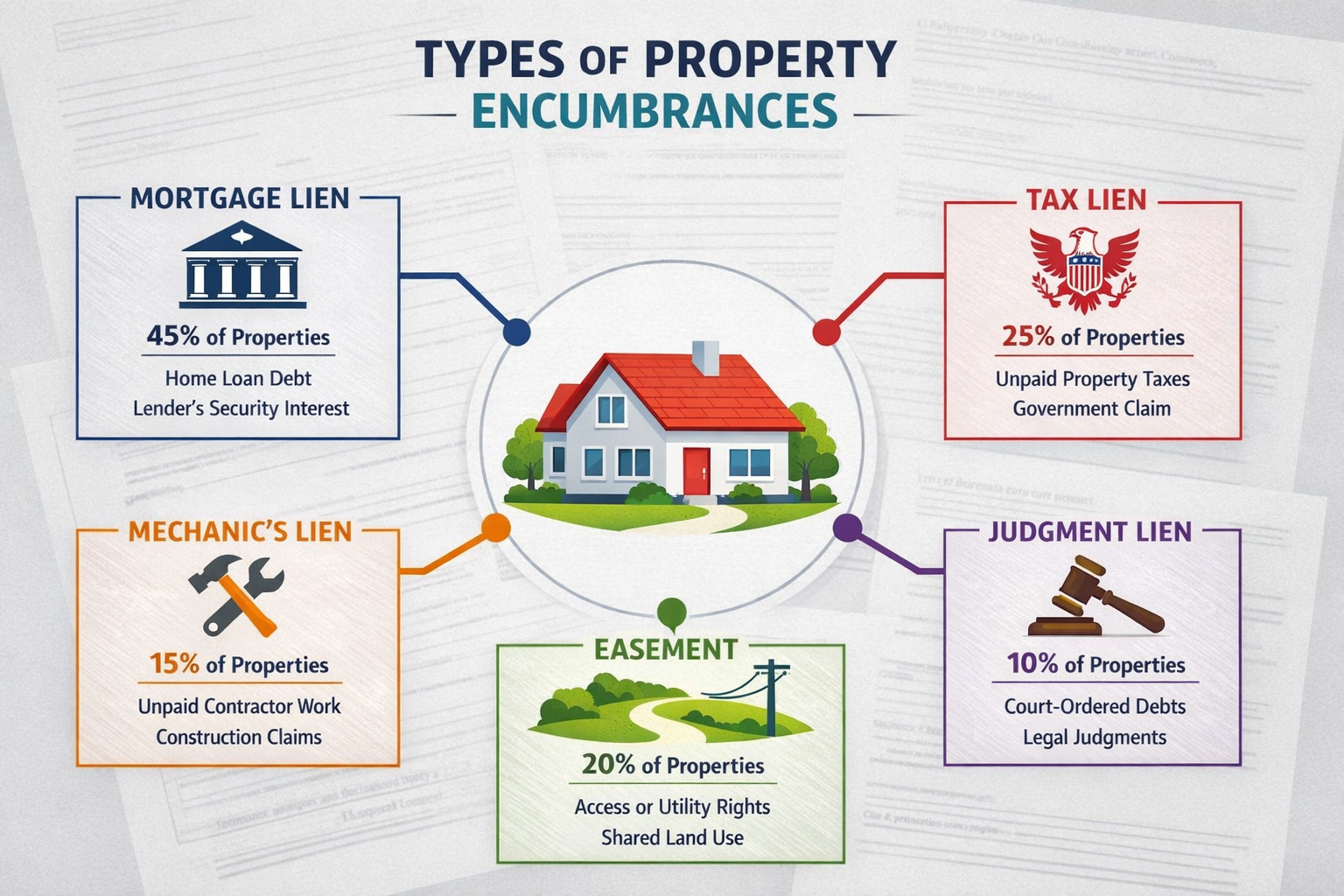

Financial encumbrances involve money owed and include:

- Mortgages and home equity loans

- Property tax liens

- Mechanic’s liens from unpaid contractors

- Judgment liens from court orders

- HOA liens from unpaid association fees

Non-financial encumbrances restrict property use and include:

- Easements granting others access or use rights

- Deed restrictions limiting how property can be used

- Encroachments from neighboring structures

- Zoning restrictions imposed by local government

The distinction matters because financial encumbrances typically must be paid off at closing, while non-financial encumbrances often transfer with the property to the new owner.

How Encumbrances Affect Property Value and Sales

Encumbrances create friction in real estate transactions. They complicate financing, reduce buyer pool, and often require negotiation about who pays what. A property worth $300,000 with $50,000 in liens doesn’t simply become a $250,000 property—it becomes a more complex transaction that many buyers and lenders want to avoid.

Market impact includes:

- Reduced buyer interest and longer time on market

- Lower offers due to perceived risk and hassle

- Difficulty obtaining traditional financing

- Increased closing costs and legal fees

- Potential deal cancellations during due diligence

Properties with significant encumbrances often sell for 10-30% below comparable unencumbered properties, depending on the type and amount of claims involved.

Common Types of Encumbrances Buyers and Sellers Encounter

Understanding the specific types of encumbrances helps both parties navigate the complexities of encumbered property sales. Each type carries different implications, resolution processes, and negotiation strategies.

Mortgage Liens and Home Equity Loans

Mortgages represent the most common and expected encumbrance. When a lender provides financing to purchase property, they secure that loan with a lien against the property itself. This gives them the right to foreclose if payments aren’t made.

Key characteristics:

- Voluntary liens created by the property owner

- Must be satisfied at closing from sale proceeds

- Take priority based on recording date (first mortgage, second mortgage, etc.)

- Payoff amounts include principal, interest, and fees

Most buyers understand and accept mortgage liens because they’re standard and resolved automatically at closing. The seller’s proceeds simply pay off the remaining mortgage balance before the seller receives any funds.

Home equity loans and lines of credit work similarly but represent additional liens beyond the primary mortgage. These must also be satisfied at closing unless the buyer agrees to assume them (rare in today’s market).

Tax Liens: Federal, State, and Local

Tax liens represent serious encumbrances that can complicate or prevent property sales. Government entities have powerful collection rights, and tax liens often take priority over other claims.

Property tax liens arise when owners fall behind on local property taxes. Counties can eventually foreclose on properties with delinquent taxes, making these liens particularly urgent. Many property owners facing financial hardship discover that selling a house with a tax lien requires careful coordination with local tax authorities.

Federal tax liens from the IRS attach to all property owned by someone with unpaid federal taxes. These liens are public record and must be addressed before clear title can transfer.

State tax liens work similarly for unpaid state income taxes, sales taxes, or other state obligations.

The good news? Tax authorities often negotiate payment plans or accept partial payment from sale proceeds because they recognize that foreclosure is expensive and time-consuming for everyone involved.

Mechanic’s Liens and Contractor Claims

When contractors, subcontractors, or suppliers aren’t paid for work performed on a property, they can file a mechanic’s lien to secure payment. These liens give workers a legal claim against the property itself.

Important aspects:

- Must be filed within specific timeframes (varies by state)

- Can be filed even if the property owner paid the general contractor

- Require proper notice and documentation

- Can be challenged if improperly filed

Mechanic’s liens surprise many property owners who thought they paid for all work. If a general contractor doesn’t pay their subcontractors, those subs can still lien the property—even though the owner already paid the general contractor.

Judgment Liens from Lawsuits

When someone wins a lawsuit and obtains a monetary judgment, they can often record that judgment as a lien against the debtor’s real property. This ensures they’ll eventually get paid when the property sells.

Common sources include:

- Unpaid credit card debts

- Medical bills

- Personal injury awards

- Breach of contract claims

- Divorce settlements

Judgment liens can remain attached to property for years, accruing interest and growing larger over time. They must typically be satisfied before title can transfer to a new owner.

Easements and Rights of Way

Unlike financial encumbrances, easements grant others the right to use portions of your property for specific purposes. Common examples include:

- Utility easements allowing power, water, or sewer companies access

- Access easements providing neighbors passage to their property

- Conservation easements restricting development to preserve land

- Prescriptive easements established through long-term use

Easements typically transfer with the property and can’t be easily removed. Buyers need to understand exactly what rights others have and how those rights might affect their intended use of the property.

HOA Liens and Special Assessments

Homeowners associations can place liens on properties for unpaid dues, fines, or special assessments. These liens often take priority over mortgages and can lead to foreclosure surprisingly quickly.

Considerations include:

- Monthly or annual dues that accumulate with late fees

- Special assessments for major repairs or improvements

- Fines for rule violations

- Super-priority status in some states

HOA liens must be addressed before closing, and buyers should always request HOA status letters showing current account standing.

Encumbered Property for Sale: The Seller’s Perspective

Selling property with encumbrances requires transparency, strategy, and often professional assistance. Sellers face legal obligations and practical challenges that can’t be ignored or wished away.

Disclosure Requirements and Legal Obligations

Every state requires sellers to disclose known material defects and encumbrances. Failing to disclose known liens, easements, or other claims constitutes fraud and can result in lawsuits, transaction cancellation, and financial penalties.

Sellers must disclose:

- All known liens and judgments

- Existing easements and restrictions

- Pending legal actions affecting the property

- Tax delinquencies and payment plans

- HOA obligations and violations

The disclosure happens through formal documentation, typically a seller’s disclosure statement that buyers review before making offers. Honest disclosure protects sellers from future liability and builds trust with potential buyers.

Many sellers worry that disclosing problems will scare away buyers. In reality, undisclosed issues discovered during due diligence create far more problems—including complete deal collapse after everyone has invested time and money.

Options for Resolving Encumbrances Before Listing

The cleanest approach involves resolving encumbrances before listing the property. This maximizes buyer pool, supports higher offers, and simplifies the transaction process.

Resolution strategies include:

✅ Paying off liens from savings or other resources

- Provides cleanest title and broadest appeal

- Allows traditional listing and financing

- Maximizes sale price potential

✅ Negotiating settlements for less than owed

- Many lienholders accept partial payment

- Particularly effective for old judgments and medical debts

- Requires documentation of financial hardship

✅ Disputing invalid or incorrect liens

- Some liens are improperly filed or legally defective

- Title issues can sometimes be challenged

- Requires legal assistance but can eliminate claims entirely

✅ Obtaining lien releases through payment plans

- Some creditors release liens with agreement for future payment

- Less common but worth exploring

- Requires written agreement and proper documentation

For sellers facing multiple liens and judgments, professional guidance becomes essential. The team at Sure Path Property Solutions specializes in coordinating with creditors, title companies, and counties to create workable solutions.

Selling “As-Is” with Known Encumbrances

When clearing encumbrances before listing isn’t feasible, sellers can sell “as-is” with full disclosure. This approach acknowledges the problems upfront and typically involves:

Reduced asking price reflecting the encumbrances and hassle factor

Limited buyer pool consisting of investors and cash buyers

Faster timeline since traditional financing often won’t work

Clear communication about exactly what encumbrances exist and estimated payoff amounts

Selling as-is doesn’t mean hiding problems—it means being upfront about them and pricing accordingly. Many buyers who purchase properties with legal problems specifically seek these opportunities because they have the expertise and resources to resolve issues.

Working with Title Companies and Attorneys

Title companies play a crucial role in encumbered property sales. They conduct title searches, identify all recorded encumbrances, calculate payoffs, and coordinate lien releases at closing.

The title company process:

- Preliminary title search identifies all recorded claims

- Title commitment lists encumbrances that must be resolved

- Payoff requests sent to all lienholders

- Closing coordination ensures all liens are satisfied

- Title insurance protects buyer from undiscovered claims

Real estate attorneys provide additional protection by reviewing contracts, negotiating with creditors, and ensuring compliance with disclosure laws. For complex situations involving clouded title or breaks in the chain of title, attorney involvement becomes essential.

Pricing Strategy for Encumbered Properties

Pricing encumbered property requires balancing multiple factors:

Calculate net proceeds carefully:

- Market value minus all encumbrances

- Minus selling costs (commissions, fees, repairs)

- Minus any negotiation buffer

Consider buyer perspective:

- Additional risk requires compensation

- Hassle factor reduces perceived value

- Financing limitations narrow buyer pool

Market positioning:

- Price competitively to attract serious buyers

- Highlight property potential beyond problems

- Emphasize transparency and seller cooperation

Many sellers price encumbered properties 15-25% below comparable clean properties, though the exact discount depends on encumbrance type, amount, and local market conditions.

Encumbered Property for Sale: The Buyer’s Perspective

Purchasing encumbered property offers opportunities for savvy buyers but requires thorough due diligence and clear understanding of risks and responsibilities.

Due Diligence: Uncovering All Encumbrances

Smart buyers never rely solely on seller disclosures. Comprehensive due diligence protects against surprises and provides negotiating leverage.

Essential investigation steps:

🔍 Title search and examination

- Professional title company review

- Search of public records for liens and judgments

- Verification of property boundaries and easements

- Review of deed restrictions and covenants

🔍 Property tax verification

- Confirm current tax status with county

- Check for delinquencies and payment plans

- Verify special assessments and upcoming obligations

- Review tax sale or foreclosure status

🔍 Court record searches

- Check for pending lawsuits involving the property

- Verify judgment liens and their amounts

- Research foreclosure actions

- Review probate or estate proceedings if applicable

🔍 HOA investigation

- Request status letter showing account standing

- Review governing documents and restrictions

- Verify special assessments and upcoming projects

- Check for pending violations or fines

🔍 Physical inspection

- Identify potential mechanic’s lien sources

- Document property condition

- Verify easement locations and impacts

- Check for encroachments or boundary issues

This investigation takes time and costs money, but it’s infinitely cheaper than discovering problems after closing when options become severely limited.

Understanding Your Rights and Protections

Buyers have significant legal protections when purchasing real estate, but these protections only work if buyers know about them and exercise them properly.

Key buyer protections include:

Title insurance protects against undiscovered encumbrances and defects. Owner’s title insurance (separate from lender’s insurance) covers the buyer for claims that arise after closing.

Contingency clauses in purchase contracts allow buyers to cancel and recover deposits if unacceptable encumbrances are discovered. Common contingencies include:

- Title contingency requiring clear and marketable title

- Financing contingency (lenders won’t fund with certain encumbrances)

- Inspection contingency revealing lien-worthy unpaid work

- Attorney review contingency

Disclosure laws require sellers to reveal known problems. Buyers can sue for fraud or rescind transactions when sellers hide encumbrances.

Due diligence periods provide time to investigate before committing. Most contracts include 10-30 days for inspections and title review.

Negotiating Purchase Price and Lien Resolution

Discovering encumbrances creates negotiation opportunities. Buyers can request:

Price reductions reflecting the encumbrance amounts and hassle

Seller resolution of specific liens before closing

Escrow holdbacks where funds are held to pay disputed claims

Extended closing allowing time to resolve complex issues

Credits at closing for buyers who agree to handle certain encumbrances

The negotiation approach depends on market conditions, property desirability, and buyer motivation. In seller’s markets, buyers have less leverage. In buyer’s markets or with seriously encumbered properties, buyers can often negotiate significant concessions.

Example negotiation scenario:

- Property listed at $250,000

- Title search reveals $15,000 in liens

- Buyer offers $225,000 with seller paying all liens

- Seller counters at $235,000, agreeing to clear liens

- Final agreement: $232,000 with seller clearing all liens at closing

Assuming vs. Clearing Encumbrances

Buyers sometimes have the option to assume certain encumbrances rather than requiring the seller to clear them. This decision requires careful analysis.

Encumbrances that might be assumed:

- Existing mortgages with favorable rates (rare with due-on-sale clauses)

- Easements that don’t interfere with intended use

- Minor liens that buyers can negotiate with creditors

- HOA obligations (unavoidable in most cases)

Encumbrances that should typically be cleared:

- Tax liens (lenders won’t allow)

- Large judgment liens

- Mechanic’s liens for questionable work

- Any lien where the amount is disputed

Assuming encumbrances can reduce purchase price but increases buyer risk and complexity. Most buyers and lenders prefer clean title with all financial encumbrances cleared at closing.

Financing Challenges and Solutions

Traditional mortgage lenders have strict title requirements. They won’t fund loans on properties with certain encumbrances, particularly:

- Tax liens (federal, state, or local)

- Judgment liens

- Mechanic’s liens

- Unresolved title defects

This limitation creates a financing gap that buyers can bridge through:

Cash purchases eliminate lender requirements entirely. Cash buyers have maximum flexibility and negotiating power.

Hard money loans from private lenders who focus on property value rather than title perfection. These loans carry higher interest rates but provide short-term solutions.

Seller financing where the seller acts as lender. This works when the seller owns the property free and clear or when existing liens can be subordinated.

Delayed closing where the purchase contract allows 60-90 days for the seller to clear encumbrances before closing.

Simultaneous closing where lien payoffs happen at the same closing table, with title insurance ensuring all claims are satisfied before the buyer’s funds are released.

For buyers working with traditional lenders, the title commitment will list all encumbrances that must be cleared as conditions for funding. The seller must satisfy these requirements or the lender won’t provide financing.

Special Situations: Complex Encumbered Property Scenarios

Some encumbered property situations involve additional layers of complexity that require specialized knowledge and strategic approaches.

Inherited Property with Multiple Liens

Inherited property often comes with encumbrances that accumulated during the deceased owner’s lifetime. Heirs face unique challenges:

- Liens that may have priority over inheritance

- Multiple heirs with different opinions about resolution

- Probate requirements complicating the timeline

- Emotional attachment despite financial burdens

When selling deceased parents’ house with liens, heirs must understand that encumbrances typically must be paid from estate assets before heirs receive any inheritance. The property itself serves as the primary estate asset for satisfying claims.

For situations involving selling inherited property with multiple owners, disagreements about handling encumbrances can create additional complications requiring mediation or legal intervention.

Properties in Pre-Foreclosure or Foreclosure

Pre-foreclosure properties carry mortgage liens in default along with accumulated late fees, legal costs, and often additional liens from unpaid taxes or judgments.

Unique considerations:

- Limited timeframe before foreclosure sale

- Lender cooperation required for short sales

- Multiple liens competing for limited equity

- Potential for deficiency judgments

Owners facing foreclosure can often sell before the foreclosure sale, but this requires quick action and often involves short sale processes where the lender accepts less than the full amount owed.

Co-Owned Properties with Disputed Encumbrances

When jointly owned property has encumbrances, disputes between co-owners complicate resolution. Common scenarios include:

- One owner created liens without other owners’ knowledge

- Disagreement about whether to sell or clear encumbrances

- Liens against one owner that attach to shared property

- Partition actions forcing sale despite disagreement

These situations often require legal intervention, mediation, or buyout arrangements to move forward. When siblings won’t agree about selling inherited property, encumbrances add another layer of complexity to already difficult family dynamics.

Properties with Title Defects and Encumbrances

Sometimes properties have both encumbrances and title problems that must be resolved simultaneously. This might include:

- Liens plus missing signatures on prior deeds

- Encumbrances plus boundary disputes

- Judgments plus breaks in the chain of title

- Tax liens plus estate or probate issues

These complex situations often require quiet title actions or other legal proceedings to clear both the title defects and the encumbrances before sale can proceed.

The Resolution Process: Step-by-Step Guide

Successfully selling or buying encumbered property follows a structured process that protects all parties and ensures proper resolution.

Step 1: Comprehensive Title Search and Documentation

The process begins with a thorough title examination conducted by a professional title company or real estate attorney. This search reveals:

- All recorded liens and their priority

- Easements and restrictions

- Ownership history and chain of title

- Pending legal actions

- Tax status and obligations

The title company produces a preliminary title report or title commitment listing every encumbrance that must be addressed. This document becomes the roadmap for the entire transaction.

Step 2: Obtaining Payoff Statements and Lien Information

For each financial encumbrance, the seller or title company must obtain current payoff information including:

- Principal balance owed

- Accrued interest through projected closing date

- Late fees and penalties

- Administrative costs

- Per diem interest rate for closing delays

Payoff statements have expiration dates (typically 30 days), so timing matters. The title company coordinates these requests to ensure current information at closing.

Step 3: Negotiating with Lienholders and Creditors

Many encumbrances can be negotiated, particularly:

Old judgment liens where creditors may accept partial payment

Medical liens that often settle for less than face value

Contractor liens where disputes exist about work quality

Tax liens where payment plans or offers in compromise are possible

Negotiation requires documentation of financial situation, clear communication, and often professional representation. Creditors want to get paid and often recognize that partial payment beats lengthy collection efforts or nothing at all.

Step 4: Coordinating the Closing Process

Once all payoffs are confirmed and funds are available, the closing can proceed. The title company acts as intermediary, ensuring:

✓ All lienholders receive payment simultaneously

✓ Lien releases are obtained and recorded

✓ Title transfers only after encumbrances are cleared

✓ Title insurance protects the buyer

✓ All parties receive proper documentation

The typical closing sequence:

- Buyer’s funds deposited with title company

- Seller signs deed transferring ownership

- Title company pays off all liens from buyer’s funds

- Lienholders provide release documents

- Deed and releases recorded with county

- Title insurance issued to buyer

- Remaining funds disbursed to seller

This simultaneous closing ensures that no party is exposed to risk. The buyer doesn’t own property with liens, lienholders get paid, and the seller receives their net proceeds.

Step 5: Post-Closing Verification and Title Insurance

After closing, the title company ensures all lien releases are properly recorded and the buyer receives:

- Owner’s title insurance policy

- Recorded deed showing clear ownership

- Confirmation that all encumbrances are released

- Documentation of all payments made

Title insurance protects against any undiscovered encumbrances or errors in the title work. If a lien surfaces after closing that should have been discovered, the title insurance company handles it.

Working with Professionals: When and Why You Need Help

Complex encumbered property transactions benefit enormously from professional guidance. Knowing when to seek help and who to engage can mean the difference between successful resolution and costly mistakes.

Real Estate Attorneys and Title Attorneys

Attorneys provide legal expertise that protects your interests and ensures compliance with complex real estate laws. Engage an attorney when:

- Multiple liens create priority disputes

- Title defects exist alongside encumbrances

- Creditors dispute payoff amounts or lien validity

- Foreclosure or legal action is pending

- Inherited property involves probate or estate issues

- Co-owners disagree about resolution approaches

Attorneys can negotiate with creditors, file legal actions to clear invalid liens, represent you in court, and ensure all documentation is legally sound.

Title Companies and Escrow Officers

Title companies specialize in identifying encumbrances, calculating payoffs, and coordinating closings. Their expertise includes:

- Comprehensive title searches

- Title insurance underwriting

- Lien payoff coordination

- Escrow services holding funds safely

- Recording of documents

Choose experienced title companies with expertise in complex transactions. Not all title companies handle heavily encumbered properties equally well.

Real Estate Agents Experienced with Encumbered Properties

Most real estate agents handle straightforward transactions. For encumbered properties, seek agents with specific experience in:

- Short sales and foreclosures

- Properties with multiple liens

- Probate and estate sales

- Investor transactions

These specialists understand pricing strategies, know how to market challenged properties, and can guide clients through complex processes.

Property Solutions Companies

Companies like Sure Path Property Solutions specialize in helping property owners navigate complicated situations including liens, judgments, tax issues, and title problems. These companies provide:

🏡 Comprehensive problem assessment identifying all issues and potential solutions

🏡 Creditor coordination negotiating with lienholders and tax authorities

🏡 Title work coordination working with title companies and attorneys

🏡 Multiple exit strategies including traditional sales, investor sales, or creative solutions

🏡 Helpful guidance through every step of the process

For property owners feeling overwhelmed by encumbrances, these companies offer expert service and trustworthy support that simplifies complex situations.

Cost Considerations: What to Expect Financially

Understanding the financial implications of encumbered property transactions helps both buyers and sellers make informed decisions.

Typical Costs for Sellers

Sellers of encumbered properties face several cost categories:

Lien payoffs – The largest expense, including:

- Mortgage balances

- Tax liens with penalties and interest

- Judgment liens with accrued interest

- Mechanic’s liens

- HOA liens and assessments

Transaction costs – Standard selling expenses:

- Real estate commissions (5-6% typically)

- Title insurance and escrow fees

- Attorney fees ($1,500-$5,000+ for complex situations)

- Recording fees and transfer taxes

- Property repairs or concessions

Resolution costs – Expenses specific to clearing encumbrances:

- Title search and examination ($300-$800)

- Lien release processing fees

- Court costs for legal actions

- Negotiation and settlement costs

Example cost breakdown for a $250,000 property:

- Mortgage payoff: $180,000

- Tax lien with penalties: $12,000

- Judgment lien: $8,000

- Real estate commission: $15,000

- Title and closing costs: $3,000

- Attorney fees: $2,500

- Total costs: $220,500

- Net to seller: $29,500

Typical Costs for Buyers

Buyers purchasing encumbered properties may incur additional expenses beyond standard transaction costs:

Due diligence costs:

- Title search and examination

- Property inspections

- Attorney review fees

- Survey costs if boundaries are disputed

Financing costs:

- Higher interest rates for non-traditional financing

- Larger down payments required

- Additional lender fees for complex transactions

Assumption costs:

- If assuming certain encumbrances

- Legal fees for negotiating assumptions

- Potential liability for undisclosed amounts

Protection costs:

- Enhanced title insurance

- Additional legal review

- Contingency reserves for discovered issues

Hidden Costs and Unexpected Expenses

Both parties should budget for potential surprises:

⚠️ Undiscovered liens that surface during title work

⚠️ Payoff amount increases due to accruing interest and fees

⚠️ Extended closing costs when resolution takes longer than expected

⚠️ Legal disputes requiring court intervention

⚠️ Cloud on title requiring quiet title or other legal action

Smart parties include a 5-10% contingency buffer in their financial planning to accommodate unexpected costs.

Preventing Encumbrance Problems: Best Practices

Prevention is always easier than cure. Property owners can avoid many encumbrance problems through proactive management.

For Current Property Owners

🔐 Pay obligations on time

- Property taxes

- HOA dues and assessments

- Contractor bills

- Mortgage payments

🔐 Maintain good records

- Payment receipts and confirmations

- Lien releases for completed work

- Title insurance policies

- Deed and ownership documents

🔐 Monitor public records

- Check for improperly filed liens

- Verify tax payment posting

- Review property records annually

🔐 Address problems immediately

- Don’t ignore collection notices

- Dispute incorrect liens promptly

- Communicate with creditors proactively

🔐 Obtain proper releases

- Get lien releases for all paid work

- Record releases with the county

- Keep copies in permanent files

For Buyers Considering Purchase

✅ Never skip due diligence

- Always obtain professional title search

- Review all disclosed encumbrances carefully

- Verify payoff amounts independently

✅ Use experienced professionals

- Hire qualified real estate attorney

- Work with reputable title company

- Engage knowledgeable real estate agent

✅ Include protective contingencies

- Title contingency requiring clear title

- Inspection contingency

- Financing contingency

- Attorney review period

✅ Verify everything in writing

- Don’t accept verbal assurances

- Require documentation of all payoffs

- Get lien releases before closing

✅ Purchase title insurance

- Owner’s policy, not just lender’s

- Enhanced coverage if available

- Understand exclusions and limitations

For Sellers Preparing to List

📋 Conduct pre-listing title search

- Identify all encumbrances early

- Address problems before marketing

- Obtain payoff statements in advance

📋 Resolve what you can

- Pay off small liens

- Negotiate settlements

- Clear disputed items

📋 Disclose completely and honestly

- List all known encumbrances

- Provide documentation to buyers

- Don’t hide or minimize problems

📋 Price appropriately

- Account for encumbrances in asking price

- Consider buyer’s perspective

- Build in negotiation room

📋 Work with specialists

- Choose experienced professionals

- Get expert advice on strategy

- Don’t try to handle complex situations alone

Real-World Examples and Case Studies

Understanding how encumbered property transactions work in practice helps illustrate the concepts and strategies discussed.

Case Study 1: Tax Lien Resolution Through Sale

Situation: Maria inherited her father’s home valued at $180,000 but discovered $35,000 in delinquent property taxes with penalties. She couldn’t afford to pay the taxes and maintain the property.

Solution: Maria contacted Sure Path Property Solutions for helpful guidance. The team:

- Negotiated with the county for current payoff amount

- Listed the property with full disclosure

- Found a cash buyer willing to purchase as-is

- Coordinated closing where taxes were paid from proceeds

- Helped Maria net $128,000 after all costs

Outcome: The county received their tax payment, the buyer acquired property below market value, and Maria avoided foreclosure while receiving substantial inheritance.

Case Study 2: Multiple Lien Negotiation

Situation: James needed to sell his property quickly for relocation but had:

- Mortgage balance: $210,000

- Judgment lien from credit card: $18,000

- Mechanic’s lien from roof repair: $12,000

- HOA lien: $3,500

- Property value: $235,000

Solution: Working with a real estate attorney and title company:

- Negotiated judgment lien settlement for $9,000 (50%)

- Disputed mechanic’s lien, settled for $7,000

- Paid HOA lien in full

- Mortgage paid at closing

- Total payoffs: $229,500

Outcome: James sold for $238,000, paid all negotiated amounts, and netted $8,500 after commissions and costs—far better than foreclosure.

Case Study 3: Buyer Opportunity on Encumbered Property

Situation: Sarah, an experienced investor, found a property listed at $150,000 (market value $200,000) with disclosed liens totaling $25,000.

Solution: Sarah:

- Conducted thorough due diligence

- Verified all lien amounts independently

- Offered $140,000 with seller clearing all liens

- Used hard money financing for quick closing

- Seller accepted, desperate to move forward

Outcome: Sarah acquired property for $140,000, all liens cleared at closing. After $15,000 in renovations, she sold for $198,000, netting approximately $30,000 profit.

Frequently Asked Questions About Encumbered Property Sales

Can you sell a house with liens on it?

Yes, absolutely. Houses with liens sell every day. The liens must typically be paid from the sale proceeds at closing, but the sale can proceed. The key is full disclosure and proper coordination with the title company to ensure all liens are satisfied before title transfers.

Who pays off liens when selling a house?

Typically, the seller pays liens from their sale proceeds at closing. However, this is negotiable. Sometimes buyers agree to pay certain liens in exchange for a reduced purchase price. The purchase contract should clearly specify who is responsible for each encumbrance.

What happens if a seller can’t pay off all liens?

If liens exceed the property value (underwater situation), the seller has several options: negotiate short sale with lienholders, bring cash to closing to cover the difference, or pursue foreclosure alternatives like deed in lieu. Walking away isn’t usually the best option due to credit and tax implications.

How do I find out what liens are on a property?

A professional title search conducted by a title company or attorney is the most comprehensive method. You can also search county records yourself (often available online), check with the county tax assessor, and review court records for judgments. However, professional searches are more thorough and include sources individual searchers might miss.

Can a buyer assume existing liens?

In some cases, yes, though it’s uncommon. Easements and deed restrictions typically transfer automatically. Financial liens like mortgages rarely transfer due to due-on-sale clauses. Buyers might assume certain liens by agreement, but most lenders won’t finance properties with outstanding financial encumbrances.

How long does it take to clear liens and close?

Timeline varies significantly based on lien type and complexity. Simple mortgage payoffs happen at closing. Tax liens might require 30-60 days for government processing. Disputed liens or those requiring negotiation can take 60-90 days or longer. Complex situations involving quiet title actions can take 6-12 months.

Are all encumbrances bad?

No. Some encumbrances are routine and expected (mortgages, utility easements). Others are problematic (tax liens, judgments). The impact depends on the type, amount, and how they affect property use and transferability. Full understanding through due diligence is essential.

What’s the difference between a lien and an encumbrance?

A lien is a type of encumbrance—specifically, a financial claim against property. Encumbrances include both financial claims (liens) and non-financial restrictions (easements, deed restrictions, encroachments). All liens are encumbrances, but not all encumbrances are liens.

Taking Action: Your Next Steps

Understanding Encumbered Property for Sale: What Buyers & Sellers Need to Know is the first step. Taking appropriate action is what actually resolves problems and moves transactions forward.

For Sellers with Encumbered Property

If you’re selling property with liens, judgments, tax issues, or other encumbrances:

1. Get a complete picture

- Order a professional title search

- Obtain current payoff statements for all liens

- Document all known encumbrances

- Calculate your potential net proceeds

2. Explore your options

- Can you pay off liens before listing?

- Should you negotiate settlements?

- Is selling as-is the best approach?

- Do you need professional help?

3. Assemble your team

- Experienced real estate attorney

- Title company familiar with complex transactions

- Real estate agent or property solutions company

- Tax advisor for implications of sale

4. Develop a strategy

- Pricing approach

- Marketing plan

- Timeline and milestones

- Contingency plans for complications

5. Execute with transparency

- Full disclosure to potential buyers

- Honest communication with professionals

- Proactive problem-solving

- Patience through the process

For property owners facing overwhelming situations with multiple liens, back taxes, or complex title issues, Sure Path Property Solutions offers friendly and caring expert service. The team coordinates with all parties, negotiates with creditors, and provides helpful solutions tailored to your specific situation.

For Buyers Considering Encumbered Property

If you’re evaluating a property with known encumbrances:

1. Conduct thorough due diligence

- Professional title search and examination

- Independent verification of all lien amounts

- Property inspection for additional issues

- Review of all disclosure documents

2. Understand the full financial picture

- Purchase price plus assumption costs

- Required repairs and improvements

- Financing costs and requirements

- Total investment and potential return

3. Assess your risk tolerance

- Comfort level with complexity

- Financial reserves for surprises

- Timeline flexibility

- Exit strategy if problems arise

4. Negotiate strategically

- Price reflecting encumbrances and risk

- Clear allocation of resolution responsibility

- Protective contingencies

- Extended closing if needed

5. Protect yourself legally

- Experienced real estate attorney

- Comprehensive title insurance

- Written agreements for all terms

- Verification of all lien releases

For Anyone Uncertain About Next Steps

Real estate transactions involving encumbrances can feel overwhelming. You don’t have to navigate these challenges alone. Professional guidance provides:

✨ Clarity about your situation and options

✨ Strategy tailored to your specific circumstances

✨ Coordination with all necessary parties

✨ Protection of your legal and financial interests

✨ Peace of mind through the process

The team at Sure Path Property Solutions specializes in helping property owners and buyers work through complicated real estate situations. Whether you’re dealing with tax liens, judgments, inherited property issues, or complex title problems, industry experts provide trustworthy service and helpful guidance every step of the way.

Conclusion: Knowledge Empowers Better Decisions

Encumbered Property for Sale: What Buyers & Sellers Need to Know encompasses a wide range of legal, financial, and practical considerations. While these transactions are more complex than standard real estate sales, they’re far from impossible. With proper knowledge, professional guidance, and strategic approach, both buyers and sellers can successfully navigate encumbered property transactions.

For sellers, the key is transparency, realistic pricing, and proactive problem-solving. Hiding encumbrances never works and always creates bigger problems. Addressing issues head-on with expert help leads to successful outcomes.

For buyers, thorough due diligence and protective measures are essential. Encumbered properties can offer excellent opportunities, but only when buyers fully understand what they’re acquiring and protect themselves appropriately.

The complexity of encumbered property transactions is exactly why professional help is so valuable. Real estate attorneys, experienced title companies, knowledgeable agents, and specialized property solutions companies bring expertise that protects your interests and smooths the path forward.

Remember that every encumbered property situation is unique. The specific combination of encumbrance types, amounts, property value, and party motivations creates a distinct puzzle requiring customized solutions. Generic advice only goes so far—professional assessment of your specific situation provides the clarity and direction needed for confident decision-making.

Whether you’re a seller struggling with liens and tax issues or a buyer evaluating an encumbered property opportunity, you have options. The first step is understanding your situation completely. The second step is assembling the right professional team. The third step is developing and executing a strategic plan.

Don’t let encumbrances prevent you from achieving your real estate goals. With the right approach and helpful guidance, these challenges become manageable problems with practical solutions. Reach out to Sure Path Property Solutions today to discuss your specific situation and explore the options available to you. The path forward may be clearer than you think.

Sure Path is a family-owned, curative-title cash buyer. We handle the paperwork and pay what’s owed at closing — no fees, no repairs, no pressure.