Imagine losing your home to foreclosure, only to discover you still owe tens of thousands of dollars to the lender. This nightmare scenario becomes reality for thousands of homeowners every year who face deficiency judgments—a legal claim that can haunt your finances long after the foreclosure sale ends.

Understanding foreclosure deficiency judgment: what it is & how to avoid it can mean the difference between a fresh financial start and years of wage garnishments, frozen bank accounts, and damaged credit. When a foreclosure sale doesn’t cover the full amount owed on a mortgage, lenders in many states can pursue borrowers for the remaining balance. This additional debt can derail recovery efforts and create overwhelming financial pressure.

The good news? With helpful guidance and expert service, homeowners facing foreclosure have multiple strategies to prevent or minimize deficiency judgments. Whether you’re already in pre-foreclosure or trying to understand your options before missing a payment, knowing your rights and alternatives empowers you to make informed decisions during one of life’s most stressful situations.

Key Takeaways

- A deficiency judgment allows lenders to pursue borrowers for the difference between the foreclosure sale price and the total debt owed, potentially adding tens of thousands in additional liability after losing your home.

- State laws vary dramatically—some states prohibit deficiency judgments entirely (anti-deficiency states), while others allow lenders to pursue borrowers with few restrictions.

- Several proven strategies can help avoid deficiency judgments, including short sales, deed in lieu of foreclosure, loan modifications, and negotiated settlements.

- Acting early provides the most options—homeowners who seek helpful solutions before foreclosure completes have significantly more leverage to negotiate favorable outcomes.

- Professional assistance from industry experts can navigate complex foreclosure situations, especially when dealing with liens, judgments, or title complications that make traditional sales difficult.

What Is a Foreclosure Deficiency Judgment?

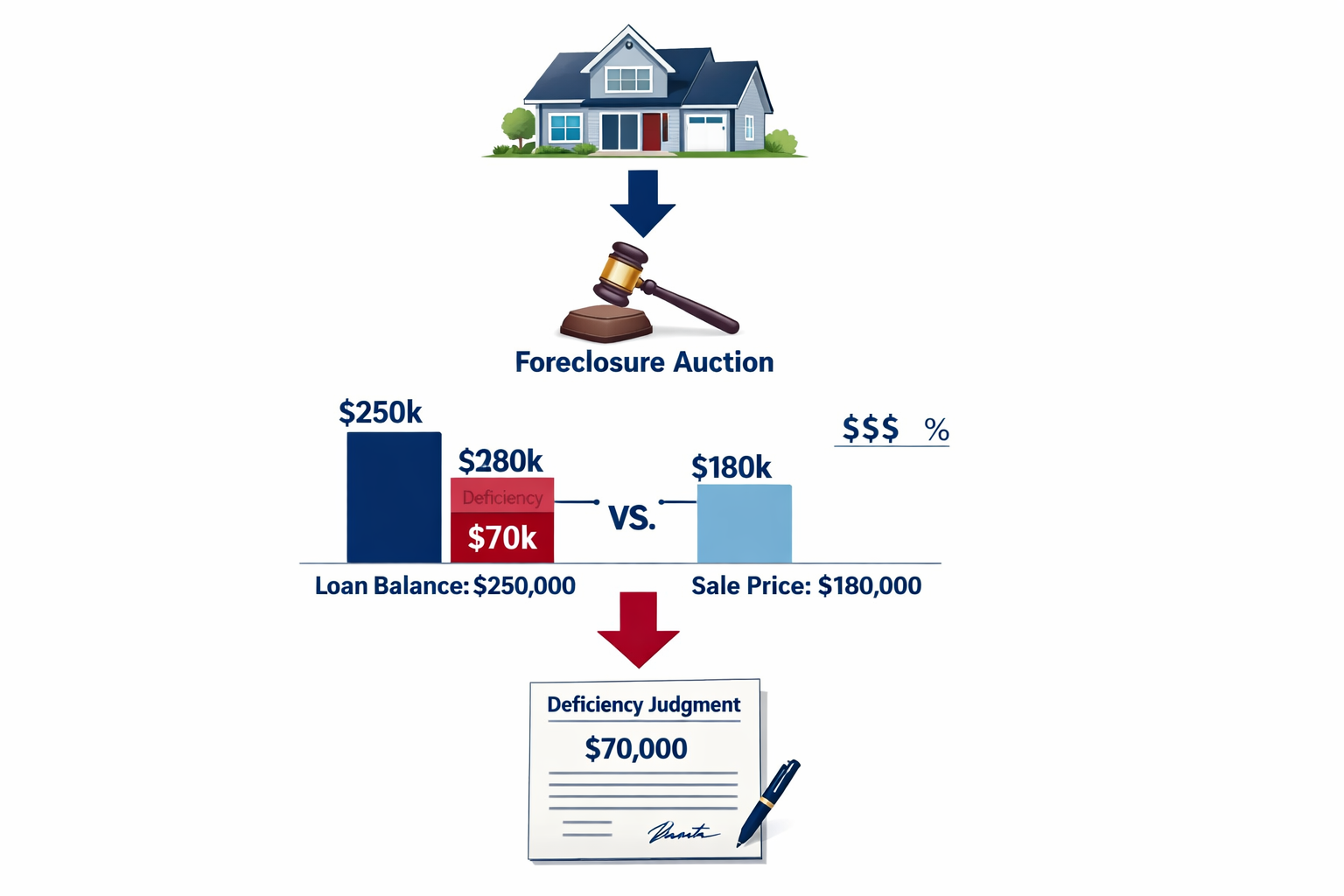

A foreclosure deficiency judgment is a court order that holds a borrower personally liable for the remaining balance after a foreclosure sale fails to cover the full mortgage debt. This legal mechanism allows lenders to recover money beyond what they received from selling the foreclosed property.

The Deficiency Calculation

The deficiency amount represents the gap between what you owe and what the lender recovers. Here’s how lenders calculate it:

Total Debt Owed = Original loan balance + unpaid interest + late fees + foreclosure costs + attorney fees

Foreclosure Sale Price = Amount the property sold for at auction

Deficiency = Total Debt Owed – Foreclosure Sale Price

For example, if you owe $250,000 on your mortgage but the property sells at foreclosure auction for only $180,000, the deficiency would be $70,000. The lender can then seek a judgment against you for this amount.

How Deficiency Judgments Work

The process typically follows these steps:

- Foreclosure Completion: The lender forecloses on the property and sells it at auction

- Deficiency Determination: The lender calculates the shortfall between sale proceeds and total debt

- Legal Action: The lender files a lawsuit seeking a deficiency judgment

- Court Hearing: You have the opportunity to contest the deficiency amount

- Judgment Issued: If successful, the court grants the lender a judgment for the deficiency

- Collection Efforts: The lender can now use various collection methods to recover the money

Collection Methods Lenders Use

Once a lender obtains a deficiency judgment, they gain powerful collection tools:

- 💰 Wage Garnishment: Courts can order your employer to withhold a portion of your paycheck

- 🏦 Bank Account Levy: Lenders can freeze and withdraw funds from your bank accounts

- 🏠 Property Liens: Judgment liens can attach to other real estate you own

- 📊 Credit Reporting: The judgment appears on your credit report, damaging your score for years

- ⚖️ Asset Seizure: In some cases, lenders can force the sale of personal property to satisfy the debt

These collection methods can create severe financial hardship, making it difficult to rebuild after losing your home.

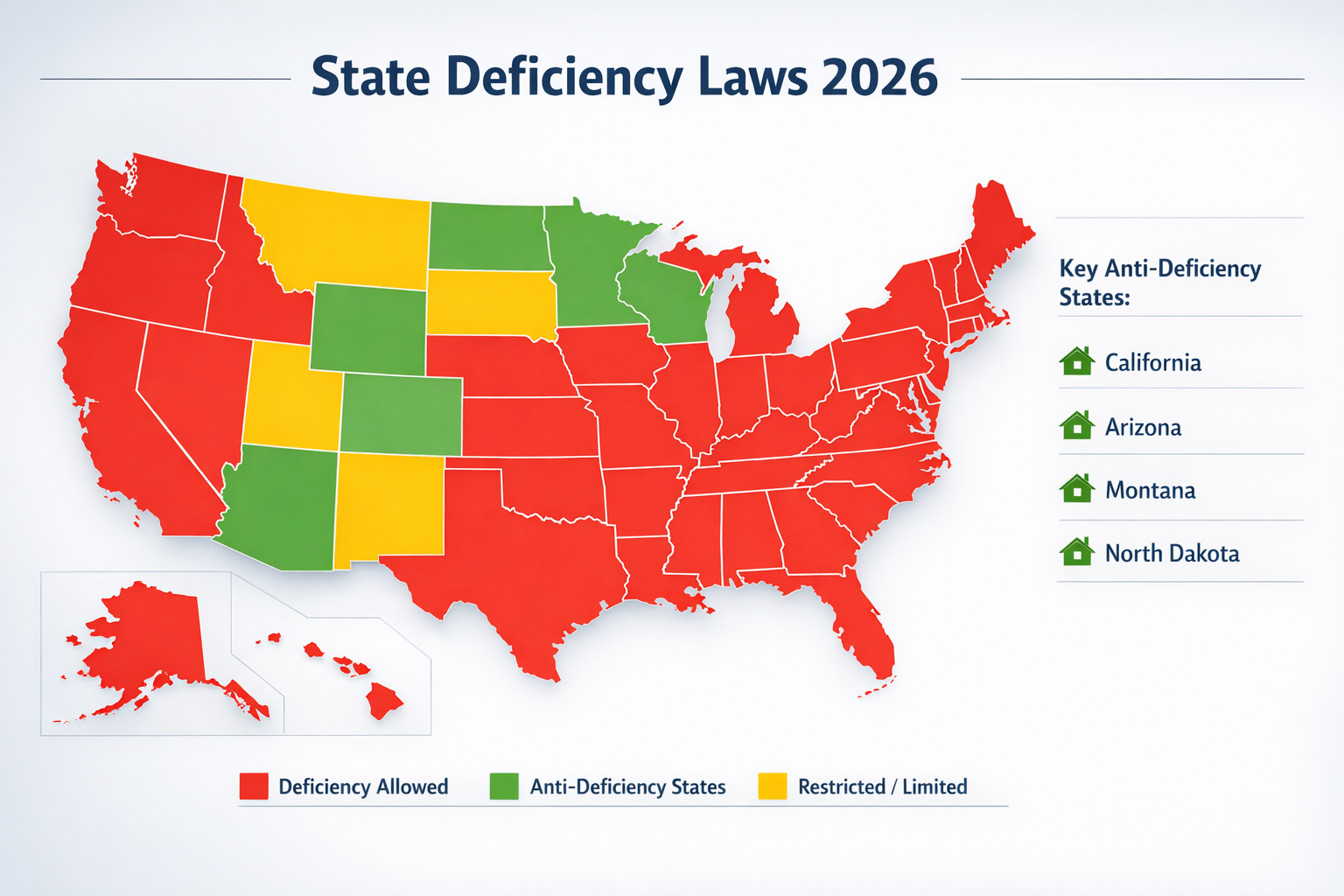

Understanding Your State’s Deficiency Judgment Laws

State laws dramatically impact whether lenders can pursue deficiency judgments and under what conditions. Knowing your state’s rules is essential for understanding your exposure and options.

Anti-Deficiency States

Several states offer strong protections against deficiency judgments, particularly for purchase-money mortgages (loans used to buy the property originally):

| State | Protection Type | Key Restrictions |

|---|---|---|

| California | Anti-deficiency for purchase loans | No deficiency on purchase-money mortgages; refinances may be vulnerable |

| Arizona | Anti-deficiency for residential property | Protects properties 2.5 acres or less |

| Montana | Anti-deficiency protection | Applies to residential properties |

| North Dakota | Anti-deficiency protection | Covers owner-occupied residential properties |

| Alaska | Anti-deficiency for certain loans | Limited protections based on loan type |

| Minnesota | Redemption period protection | Six-month redemption period limits deficiency actions |

| Wisconsin | Redemption period protection | Deficiency judgments prohibited during redemption period |

These states recognize that forcing borrowers to pay for homes they’ve already lost creates undue hardship and can prevent financial recovery.

States That Allow Deficiency Judgments

Most states permit lenders to seek deficiency judgments, though many impose time limits, procedural requirements, or fair value protections:

States with Time Limits: Lenders must file deficiency lawsuits within specific timeframes (often 30-90 days after foreclosure).

Fair Market Value Requirements: Some states require courts to determine the property’s fair market value rather than accepting the foreclosure sale price, which can reduce or eliminate deficiencies.

Procedural Protections: Certain states require lenders to follow specific notice requirements or prove they made reasonable efforts to obtain fair market value at the sale.

How State Law Affects Your Options

Your state’s deficiency laws influence which strategies work best:

- In anti-deficiency states, you may have less urgency to negotiate alternatives since you’re already protected

- In pro-lender states, pursuing alternatives like short sales or deed in lieu becomes more critical

- Time-sensitive requirements mean acting quickly provides more negotiating leverage

- Fair value protections may give you grounds to contest excessive deficiency claims

Understanding these nuances requires careful research or consultation with industry experts familiar with your state’s specific laws.

The Financial Impact of Deficiency Judgments

Beyond the immediate debt, deficiency judgments create long-lasting financial consequences that can affect your life for years.

Credit Score Damage

A deficiency judgment compounds the credit damage from foreclosure itself:

- Foreclosure alone drops credit scores by 100-300 points

- Adding a judgment creates a second negative entry, further reducing scores

- Collection accounts from the judgment add additional negative marks

- Recovery timeline extends significantly—judgments can remain on credit reports for 7-10 years depending on state law

This credit damage makes it harder to:

- Rent an apartment (many landlords check credit)

- Get approved for new credit cards or loans

- Qualify for employment (some employers review credit reports)

- Obtain reasonable insurance rates

- Finance a vehicle

Long-Term Financial Burden

Deficiency judgments don’t disappear quickly:

Judgment Duration: Most states allow judgments to remain enforceable for 10-20 years, with renewal options that can extend them indefinitely.

Interest Accumulation: Judgments typically accrue interest at statutory rates (often 5-10% annually), causing the debt to grow over time.

Ongoing Collection: Lenders can pursue collection activities throughout the judgment period, creating persistent financial stress.

Tax Implications

Ironically, you may face tax consequences even when dealing with deficiency judgments:

Cancelled Debt Income: If a lender forgives a deficiency (or you settle for less), the IRS may consider the forgiven amount as taxable income.

Form 1099-C: Lenders who cancel debt exceeding $600 must report it to the IRS, potentially creating an unexpected tax bill.

Exceptions: The Mortgage Forgiveness Debt Relief Act provided temporary relief for some homeowners, though provisions have changed over the years. Consulting a tax professional helps navigate these complex rules.

How to Avoid a Foreclosure Deficiency Judgment

The best defense against deficiency judgments is taking proactive action before foreclosure completes. Multiple strategies can help you avoid or minimize this additional debt burden.

Strategy 1: Pursue a Short Sale

A short sale occurs when your lender agrees to accept less than the full mortgage balance, allowing you to sell the property before foreclosure. This approach offers several advantages:

Benefits of Short Sales:

- ✅ You maintain more control over the sale process

- ✅ Less credit damage than foreclosure

- ✅ Opportunity to negotiate deficiency waiver

- ✅ Faster recovery timeline for future homeownership

- ✅ Avoids the public nature of foreclosure proceedings

Negotiating Deficiency Waivers: The key to successful short sales is securing written agreement that the lender will not pursue a deficiency judgment. This requires:

- Hardship Documentation: Demonstrating genuine financial difficulty

- Market Analysis: Proving the short sale price reflects fair market value

- Professional Representation: Working with experienced negotiators who understand lender requirements

- Written Agreement: Ensuring all deficiency waivers are explicitly stated in closing documents

Many homeowners facing pre-foreclosure situations find that short sales provide the most favorable outcome when handled properly.

Strategy 2: Deed in Lieu of Foreclosure

A deed in lieu of foreclosure involves voluntarily transferring property ownership to the lender in exchange for release from the mortgage obligation.

How It Works:

- You sign over the property deed to the lender

- The lender cancels the remaining mortgage debt

- You avoid the foreclosure process entirely

- Both parties save time and money

Advantages:

- 🏡 Cleaner credit impact than foreclosure

- 💼 Faster resolution (weeks vs. months)

- 📋 Less complex than short sales

- 🤝 More cooperative relationship with lender

- ⚖️ Typically includes deficiency waiver

Requirements: Lenders usually require:

- Clear title without junior liens

- Property in reasonable condition

- Demonstrated financial hardship

- Good faith effort to sell the property first

The deed in lieu option works best when you have no equity and want to exit quickly while protecting yourself from future liability.

Strategy 3: Loan Modification

Loan modifications restructure your existing mortgage to make payments more affordable, potentially avoiding foreclosure altogether.

Common Modification Types:

- Interest Rate Reduction: Lowering your rate to reduce monthly payments

- Term Extension: Stretching the loan over more years

- Principal Forbearance: Setting aside a portion of principal to be paid later

- Principal Reduction: Reducing the total amount owed (rare but possible)

Benefits:

- Keep your home

- Avoid foreclosure and deficiency judgments

- Restore loan to current status

- Potentially lower monthly payments significantly

Process: Contact your lender’s loss mitigation department immediately when facing hardship. Provide complete financial documentation and be prepared to demonstrate that modified payments fit your budget.

Strategy 4: Bankruptcy Protection

Filing bankruptcy can halt foreclosure proceedings and potentially eliminate deficiency judgment liability.

Chapter 7 Bankruptcy:

- Discharges personal liability for mortgage debt

- Eliminates potential deficiency judgments

- Lender can still foreclose, but cannot pursue you for deficiency

- Provides fresh financial start

Chapter 13 Bankruptcy:

- Creates repayment plan to catch up on missed payments

- May allow you to keep your home

- Can strip junior liens in some circumstances

- Provides time to reorganize finances

Considerations: Bankruptcy has serious credit consequences and should be considered carefully with legal counsel. However, for homeowners facing both foreclosure and significant unsecured debt, it may provide the most comprehensive solution.

Strategy 5: Negotiate a Settlement

Even after foreclosure, you may be able to negotiate a settlement for less than the full deficiency amount.

Settlement Strategies:

Lump Sum Offer: Propose paying a reduced amount in one payment (often 30-50% of deficiency).

Payment Plan: Negotiate affordable monthly payments over time.

Hardship Documentation: Demonstrate limited ability to pay, encouraging lenders to accept reduced amounts.

Written Agreement: Ensure settlement terms explicitly release you from all remaining liability.

Lenders often prefer collecting something rather than pursuing expensive collection efforts, especially when borrowers demonstrate genuine inability to pay the full amount.

Strategy 6: Challenge the Deficiency Amount

In states requiring fair market value determinations, you can contest the deficiency calculation:

Grounds for Challenge:

- Property sold below fair market value

- Lender failed to properly market the property

- Foreclosure sale process had irregularities

- Deficiency calculation includes improper fees

Process: This requires legal representation and often expert testimony about property value. However, successfully challenging the deficiency can reduce or eliminate the judgment.

Working with Professionals to Navigate Deficiency Judgments

Facing foreclosure and potential deficiency judgments feels overwhelming, but you don’t have to navigate these challenges alone. Professional assistance provides helpful solutions tailored to your specific situation.

When to Seek Professional Help

Consider reaching out to industry experts when:

- 📞 You’ve received a foreclosure notice

- 💰 Your property is underwater (worth less than you owe)

- ⚖️ You have liens or judgments complicating your situation

- 👥 Multiple owners or heirs share property ownership

- 📋 Title issues make traditional sales difficult

- ⏰ Time is running out before foreclosure sale

How Sure Path Property Solutions Helps

At Sure Path Property Solutions, we specialize in helping property owners navigate complicated real estate situations. Our friendly and caring approach combines expert service with practical solutions:

Comprehensive Assessment: We evaluate your complete situation, including:

- Current mortgage status and deficiency exposure

- Property value and market conditions

- Existing liens, judgments, or title complications

- State-specific laws affecting your options

- Timeline constraints and urgency factors

Customized Strategy Development: Based on your circumstances, we develop actionable plans that may include:

- Coordinating with lenders for short sale approval

- Negotiating deficiency waivers

- Addressing title issues that complicate traditional sales

- Working with multiple owners or heirs

- Resolving tax liens or judgment complications

Professional Coordination: We handle the complex coordination with:

- County offices for tax and lien information

- Title companies to resolve ownership issues

- Lenders to negotiate favorable terms

- Legal professionals when necessary

- Multiple stakeholders in complicated situations

Practical Solutions: Our goal is providing clear, actionable paths forward. Whether that means facilitating a quick sale, negotiating with lenders, or coordinating with other professionals, we focus on trustworthy service that puts your interests first.

The Value of Expert Guidance

Working with professionals who understand foreclosure deficiency judgment: what it is & how to avoid it provides several advantages:

Time Savings: Experts navigate bureaucratic processes efficiently, meeting critical deadlines.

Negotiating Power: Experienced professionals understand what lenders will accept and how to structure favorable agreements.

Stress Reduction: Having knowledgeable advocates handle complex details reduces the emotional burden during difficult times.

Better Outcomes: Professional guidance typically results in more favorable financial outcomes than navigating alone.

Comprehensive Solutions: Experts address not just the immediate foreclosure but related issues like property tax liens, judgment liens, or title complications that might otherwise derail solutions.

Special Considerations for Complex Situations

Some foreclosure scenarios involve additional complications that require specialized approaches to avoiding deficiency judgments.

Properties with Multiple Liens

When your property has multiple liens—perhaps a first mortgage, second mortgage, tax liens, and judgment liens—the deficiency picture becomes more complex.

Lien Priority Matters: Foreclosure by the first mortgage typically wipes out junior liens, but those lienholders may still pursue you personally for their debts.

Multiple Deficiency Risks: You could face deficiency judgments from multiple creditors, not just the foreclosing lender.

Strategic Approach: Understanding how to handle properties with multiple liens is essential for minimizing total liability.

Inherited Properties in Foreclosure

Inheriting a property already in foreclosure or with significant mortgage arrears creates unique challenges:

Limited Liability: Heirs typically aren’t personally liable for the deceased’s mortgage debt unless they assumed the loan.

Deficiency Protection: In most cases, lenders cannot pursue heirs for deficiencies on inherited properties.

Strategic Options: Selling inherited property quickly can avoid foreclosure while preserving any remaining equity for beneficiaries.

Multiple Heir Complications: When multiple heirs share ownership, coordinating decisions about foreclosure prevention requires careful navigation.

Investment Properties and Second Homes

Anti-deficiency protections often don’t apply to non-owner-occupied properties:

Greater Exposure: Investment properties and vacation homes typically lack the protections available for primary residences.

Strategic Considerations: The cost-benefit analysis differs for investment properties—sometimes allowing foreclosure makes financial sense.

Tax Implications: Investment property foreclosures have different tax consequences than primary residence foreclosures.

Properties with Title Issues

Title complications can make avoiding foreclosure through sale more difficult:

Common Title Problems:

- Clouded title from previous ownership disputes

- Breaks in the chain of title from improper transfers

- Unresolved estate issues

- Disputed boundary lines or easements

Impact on Options: Title issues can prevent short sales or traditional sales, limiting your deficiency avoidance strategies.

Solutions: Working with professionals experienced in resolving title problems becomes essential for creating viable exit strategies.

Creating Your Action Plan to Avoid Deficiency Judgments

Knowledge without action won’t protect you from deficiency judgments. Here’s a practical roadmap for taking control of your situation.

Step 1: Assess Your Current Situation (Week 1)

Gather Critical Information:

- 📄 Current mortgage statement showing exact balance

- 🏠 Recent property valuation or comparative market analysis

- 💵 List of all liens and judgments against the property

- 📊 Complete picture of your financial situation

- 📅 Foreclosure timeline and key dates

- 🗺️ Your state’s deficiency judgment laws

Calculate Your Exposure:

Estimated Deficiency = (Mortgage Balance + Fees + Costs) – Likely Sale Price

Understanding your potential exposure helps prioritize which strategies to pursue.

Step 2: Explore Your Options (Week 2-3)

Evaluate Each Strategy:

Create a comparison chart assessing:

- Feasibility: Can you realistically pursue this option?

- Timeline: How quickly can it be implemented?

- Deficiency Protection: Does it eliminate or reduce deficiency risk?

- Credit Impact: How will it affect your credit compared to foreclosure?

- Cost: What expenses are involved?

Prioritize Based on Your Circumstances:

- If you want to keep the home: Focus on loan modification

- If you need to exit quickly: Consider deed in lieu

- If you have time and want to minimize damage: Pursue short sale

- If you have multiple debts: Explore bankruptcy

- If you’re in an anti-deficiency state: Understand your existing protections

Step 3: Take Immediate Action (Week 3-4)

Contact Your Lender: Reach out to the loss mitigation department immediately. Many lenders won’t consider alternatives until you formally request them.

Seek Professional Guidance: Contact experts who can evaluate your specific situation and recommend the best path forward.

Document Everything: Keep detailed records of all communications, agreements, and financial transactions related to your foreclosure situation.

Meet Deadlines: Foreclosure involves strict timelines. Missing deadlines can eliminate options and leave you vulnerable to deficiency judgments.

Step 4: Execute Your Strategy (Ongoing)

Follow Through Consistently:

- Submit all required documentation promptly

- Respond to lender requests quickly

- Maintain communication with all parties

- Keep backups of all paperwork

- Track progress toward resolution

Stay Flexible: Sometimes initial strategies don’t work out. Be prepared to pivot to alternative approaches if circumstances change.

Protect Your Rights: If lenders violate procedures or state laws, document violations and consider legal consultation.

Life After Foreclosure: Recovery and Rebuilding

Even if you couldn’t completely avoid foreclosure, understanding how to minimize deficiency judgments and rebuild afterward makes a significant difference in your financial future.

If You Successfully Avoided a Deficiency Judgment

Celebrate the Win: Avoiding a deficiency judgment saves tens of thousands of dollars and accelerates your financial recovery significantly.

Rebuild Your Credit:

- Monitor credit reports for accuracy

- Address any remaining debts systematically

- Establish new positive credit history with secured cards or credit-builder loans

- Keep credit utilization low

- Make all payments on time going forward

Plan for Future Homeownership: Most people can qualify for a new mortgage 2-4 years after foreclosure, depending on the circumstances and loan type.

If You Face a Deficiency Judgment

Don’t Ignore It: Ignoring judgments leads to wage garnishment, bank levies, and other aggressive collection actions.

Explore Settlement: Even after a judgment, many creditors will settle for reduced amounts.

Know Your Rights: Collection laws limit what creditors can do. Understand:

- Wage garnishment limits (typically 25% of disposable income)

- Exempt assets that cannot be seized

- Statute of limitations on collection actions

- Your right to dispute inaccurate claims

Consider Legal Options: Bankruptcy may still discharge deficiency judgments even after they’re entered.

Protect Exempt Assets: Understanding your state’s exemption laws helps protect essential assets from collection efforts.

Long-Term Financial Health

Create a Financial Recovery Plan:

- Emergency Fund: Build 3-6 months of expenses to prevent future crises

- Budget Discipline: Track spending and live within your means

- Debt Reduction: Systematically eliminate remaining debts

- Credit Rebuilding: Establish positive payment history

- Financial Education: Learn from the experience to make better decisions going forward

Seek Ongoing Support: Financial counseling services can provide helpful guidance as you rebuild.

Frequently Asked Questions About Foreclosure Deficiency Judgments

Can a lender pursue a deficiency judgment years after foreclosure?

It depends on your state’s statute of limitations. Most states require lenders to file deficiency lawsuits within 30-90 days after foreclosure, though some allow longer periods. Once the statute of limitations expires, lenders lose the right to pursue deficiency judgments.

Will bankruptcy eliminate a deficiency judgment?

Yes, in most cases. Chapter 7 bankruptcy typically discharges deficiency judgments as unsecured debt. Chapter 13 may include the deficiency in your repayment plan, with remaining balances discharged upon completion.

Do I owe taxes on forgiven deficiency amounts?

Potentially. The IRS generally treats forgiven debt as taxable income. However, exceptions exist for certain foreclosures, insolvencies, and other circumstances. Consult a tax professional to understand your specific situation.

Can I negotiate a deficiency waiver during short sale?

Absolutely. Negotiating a deficiency waiver should be a primary goal in any short sale. Ensure the waiver is explicitly stated in writing in your closing documents—verbal promises aren’t enforceable.

What happens if I move to another state after foreclosure?

Judgments typically follow you across state lines. Lenders can domesticate (transfer) judgments to your new state and pursue collection there. However, your new state’s exemption laws will apply to collection efforts.

How long does a deficiency judgment stay on my credit report?

Typically 7 years from the date of entry, though this varies by state. Some states allow judgments to remain reportable for 10 years or longer.

Can lenders garnish Social Security or disability benefits?

Generally, no. Federal benefits like Social Security, SSI, and disability payments are typically exempt from garnishment for private debts like deficiency judgments. However, these protections have specific requirements and exceptions.

Conclusion: Taking Control of Your Foreclosure Situation

Foreclosure deficiency judgment: what it is & how to avoid it represents one of the most important financial topics for homeowners facing mortgage difficulties. While losing your home creates tremendous stress, understanding that you might also face tens of thousands in additional debt makes the situation even more daunting.

The good news is that you have options. Whether through short sales, deed in lieu arrangements, loan modifications, bankruptcy protection, or negotiated settlements, multiple pathways exist to avoid or minimize deficiency judgments. The key is taking action early, understanding your state’s specific laws, and seeking helpful solutions from industry experts who can guide you through the process.

“The difference between a financial disaster and a manageable setback often comes down to knowledge and timely action. Understanding deficiency judgments and acting on that knowledge empowers you to protect your financial future.”

Remember these critical points:

Act Early: The sooner you address foreclosure, the more options you have. Waiting until the last minute eliminates strategies that could have protected you.

Know Your State Laws: Deficiency judgment rules vary dramatically by state. Understanding your specific protections or vulnerabilities shapes your strategy.

Get Professional Help: Complicated situations involving liens, judgments, multiple owners, or title issues benefit tremendously from expert service and helpful guidance.

Document Everything: Keep detailed records of all communications, agreements, and financial transactions. Written documentation protects your rights and proves agreements.

Don’t Give Up: Even if foreclosure seems inevitable, you can still take steps to minimize the long-term financial impact and protect yourself from deficiency judgments.

At Sure Path Property Solutions, we’ve helped countless property owners navigate these challenging situations with friendly and caring support combined with trustworthy service. Whether you’re dealing with back taxes, liens, judgments, unclear title, or simply need to sell quickly to avoid foreclosure, our team provides the expert service and practical solutions you need.

Your Next Steps

Don’t wait until options disappear. Take action today:

- Assess your situation using the framework outlined in this article

- Research your state’s deficiency laws to understand your exposure

- Contact your lender to explore loss mitigation options

- Reach out for professional help if your situation involves complications

- Develop and execute a concrete plan to avoid deficiency judgments

The path through foreclosure is challenging, but with the right knowledge, helpful guidance, and timely action, you can minimize the damage and protect your financial future. You don’t have to face this alone—industry experts stand ready to help you find the best solution for your unique circumstances.

Contact our team today to discuss your situation and explore your options. Every day matters when facing foreclosure, and the sooner you act, the more leverage you have to negotiate favorable outcomes and avoid the long-term burden of deficiency judgments.

Sure Path is a family-owned, curative-title cash buyer. We handle the paperwork and pay what’s owed at closing — no fees, no repairs, no pressure.